互联网金融外文翻译银行业是必要的而银行不是,互联网时代的金融中介的未来

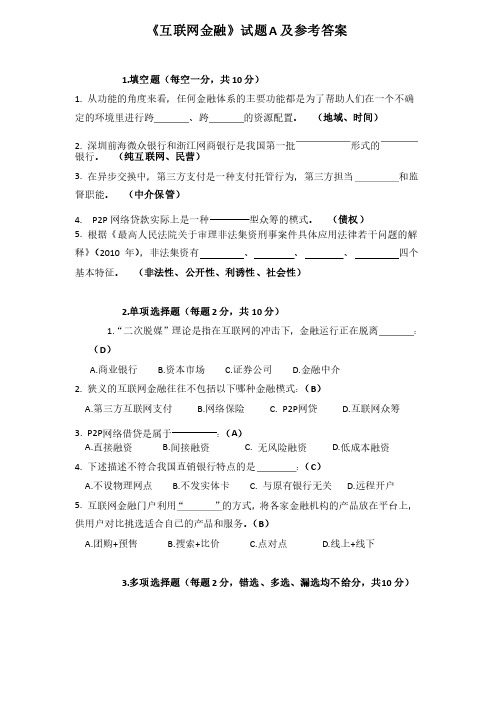

《互联网金融》试题A及参考答案

《互联网金融》试题A 及参考答案1.填空题(每空一分,共10分)1. 从功能的角度来看,任何金融体系的主要功能都是为了帮助人们在一个不确定的环境里进行跨、跨的资源配置。

(地域、时间)2. 深圳前海微众银行和浙江网商银行是我国第一批形式的银行。

(纯互联网、民营)3. 在异步交换中,第三方支付是一种支付托管行为,第三方担当和监督职能。

(中介保管)4. P2P 网络贷款实际上是一种型众筹的模式。

(债权)5. 根据《最高人民法院关于审理非法集资刑事案件具体应用法律若干问题的解释》(2010年),非法集资有、、、四个基本特征。

(非法性、公开性、利诱性、社会性)2.单项选择题(每题2分,共10分)1.“二次脱媒”“二次脱媒”理论是指在互联网的冲击下,理论是指在互联网的冲击下,理论是指在互联网的冲击下,金融运行正在脱离金融运行正在脱离:(D )A.商业银行B.资本市场C.证券公司D.金融中介2. 狭义的互联网金融往往不包括以下哪种金融模式:(B )A.第三方互联网支付B.网络保险C. P2P 网贷D.互联网众筹3. P2P 网络借贷是属于:(A )A.直接融资B.间接融资C. 无风险融资D.低成本融资4. 下述描述不符合我国直销银行特点的是:(C )A.不设物理网点 B.不发实体卡 C. 与原有银行无关 D.远程开户5. 互联网金融门户利用“”的方式,将各家金融机构的产品放在平台上,供用户对比挑选适合自己的产品和服务。

(B )A.团购+预售B.搜索+比价C.点对点D.线上+线下3.多项选择题(每题2分,错选、多选、漏选均不给分,共10分)1. 互联网金融借助于互联网技术,秉承“开放、平等、协作、分享”的互联网精神,是实现精神,是实现 等功能的新兴金融服务模式。

(ACD ) A.支付结算支付结算 B.信用创造信用创造 C. 资源配置资源配置 D.信息处理信息处理2. 第三方支付机构可以从事的支付业务主要有以下几种第三方支付机构可以从事的支付业务主要有以下几种 : A.网络支付网络支付 B.预付卡预付卡 C.银行卡收单银行卡收单 D.清算中心清算中心3. 股权型众筹的运营模式一般有以下种类股权型众筹的运营模式一般有以下种类 :(ABCD ) A.凭证式凭证式 B.会员式会员式 C. 直接股权式直接股权式 D.基金间接股权式基金间接股权式4. 互联网金融风险的叠加性体现在互联网金融风险的叠加性体现在 等风险的叠加上:(BD ) A.操作风险操作风险 B.金融风险金融风险 C.市场风险市场风险 D.互联网风险互联网风险5. 芝麻信用评分体系体现了大数据在金融征信领域的应用,它构建了个人的信用历史、人脉关系以及用历史、人脉关系以及 等评分维度。

2023年银行从业资格考试《银行业法律法规与综合能力(中级)》选择题专练(44)【含答案】

2023年银行从业资格考试《银行业法律法规与综合能力(中级)》选择题专练(44)一、单选题(80题)1.下列关于外汇交易业务的说法中,不正确的是()。

A.外汇交易既包括各种外国货币之间的交易,也包括本国货币与外国货币的兑换买卖B.外汇交易既可以满足企业贸易往来的结汇、售汇需求,也可供市场参与者进行投资或投机的交易活动C.根据外汇交易方式的不同,外汇交易可以分为即期外汇交易和远期外汇交易D.远期外汇交易是指在交易日后的第二个营业日或成交当日办理实际货币交割的外汇交易2.某债券面值为100元,票面利率为8%,每年支付2次利息。

某银行购买时价格为102元,持有一年后出售时价格为98元。

期间获得2次利息分配,则其持有期收益率为()。

A.3.9%B.5.9%C.7.8%D.8.0%3.备用信用证与其他信用证相比,描述错误的是( )。

A.备用信用证的实质是银行对借款人的一种担保行为B.只有当借款人发生意外才会发生资金的垫付C.备用信用证业务关系中,开证行是第一付款人D.一般信用证业务中,银行都要承担对受益人的第一付款责任4.企业甲与企业乙签订合同,为其提供某项工程的建设施工。

企业乙若担心企业甲不能如期完工而给自己的经营造成损失,可以要求企业甲向银行申请()。

A.借款保函B.开立信贷证明C.履约保函D.项目贷款承诺5.银行的市场风险不包括( )。

A.流动风险B.汇率风险C.商品价格风险D.股票价格风险6.以下金融工具中,()的职能主要是用于保值、投机。

A.股票B.公司债券C.商业票据D.期货7.下列不属于商业银行现金资产的是( )。

A.库存现金B.存放同业款项C.托收中的款项D.在央行的超额准备金存款8.1999年,我国为了管理和处置国有银行的不良贷款,成立了四家资产管理公司,分别收购.管理和处置四家国有商业银行和( )的部分不良资产?A.国家开发银行B.中国进出口银行C.中国农业发展银行D.中国人民银行9.下列关于理财业务管理说法不正确的是( )。

互联网金融中英文对照外文翻译文献

中英文对照外文翻译文献(文档含英文原文和中文翻译)互联网金融对传统金融的影响摘要网络的发展,深刻地改变甚至颠覆了许多传统行业,金融业也不例外。

近年来,金融业成为继商业分销、传媒之后受互联网影响最为深远的领域,许多基于互联网的金融服务模式应运而生,并对传统金融业产生了深刻的影响和巨大的冲击。

“互联网金融”成为社会各界关注的焦点。

互联网金融低成本、高效率、关注用户体验,这些特点使其能够充分满足传统金融“长尾市场”的特殊需求,灵活提供更为便捷、高效的金融服务和多样化的金融产品,大大拓展了金融服务的广度和深度,缩短了人们在时空上的距离,建立了一种全新的金融生态环境;可以有效整合、利用零散的时间、信息、资金等碎片资源,积少成多,形成规模效益,成为各类金融服务机构新的利润增长点。

此外,随着互联网金融的不断渗透和融合,将给传统金融行业带来新的挑战和机遇。

互联网金融可以促进传统银行业的转型,弥补传统银行在资金处理效率、信息整合等方面的不足;为证券、保险、基金、理财产品的销售与推广提供新渠道。

对于很多中小企业来说,互联网金融拓展了它们的融资渠道,大大降低了融资门槛,提高了资金的使用效率。

但是,互联网金融的跨行业性决定了它的风险因素更为复杂、敏感、多变,因此要处理好创新发展与市场监管、行业自律的关系。

关键词:互联网金融;商业银行;影响;监管1 引言互联网技术的不断发展,云计算、大数据、社交网络等越来越多的互联网应用为传统行业的业务发展提供了有力支持,互联网对传统行业的渗透程度不断加深。

20世纪末,微软总裁比尔盖茨就曾断言,“传统商业银行会成为新世纪的恐龙”。

如今,随着互联网电子信息技术的发展,我们真切地感受到了这种趋势,移动支付、电子银行早已在我们的日常生活中占据了重要地位。

由于互联网金融的概念几乎完全来自于商业实践,因此目前的研究多集中在探讨互联网金融的具体模式上,而对传统金融行业的影响力分析和应对措施则缺乏系统性研究。

中国银行招聘必考题 中英文版

为什么选择银行业首先,金融行业在经济发展过程中扮演着极为重要的角色。

我国经济发展前景良好,银行业也将迎来极佳的发展机遇。

我希望能参与进来,提升自己的能力的同时,也为银行业的发展贡献自己的一份力量。

At first, banking plays an important role in economic development。

Economy in China has a very good prospect, that means banking sector will embrace a precious opurtunity. Thus I want to join in banking, to improve my self, as well as to contribute my bit in banking industry.其次,金融行业的国际化趋势日益显著,比如客户的国际化,金融资本. 的国际化,行业监管规则的国际化,以及人民币的国际化。

英语作为国际通用语,在金融行业国际化的进程中发挥着重要的作用。

作为英语专业的学生,我相信我能学以致用。

Secondly, as the globalization trend of financial industry goes on, such as the globalization of the clients, the capitals, the regulations and so on. English as a global language, plays a crucial role in the process of the globalization. As an English major, I believe I will have the chance to put what I learned into practice.最后,我性格开朗,善于与人沟通,我认为我比较适合在银行,金融服务行业工作。

金融英语第二版刘文国课后翻译题答案

金融英语第二版刘文国课后翻译题答案中译英:一.1.金融管理是商业管理的重要方面之一,没有合适的金融计划企业是不可能成功的。

Finance is one of the most important aspects of business management. Without proper financial planning a new enterprise is unlikely to be successful.2.金融中介机构的基本宗旨是把不受公众欢迎的金融资产转变为他们能够接受的金融资产。

Financial intermediaries play the basic role of transforming financial assets that less desirable for a large part of the public into other financial assets-their own liabilities-which are more widely preferred by the public.3.企业经营是有风险的,因而,财务经理必须对风险进行评估和管理。

Businesses are inherently risky, so the financial manager has to identify risks and make sure they are managed properly.4.投资决策首先是指投资机会,常常指资本投资项目。

The investment decision stars with the identification of investment opportunities, often referred to as capital investment projects.5.现金预算常常被用来评估企业是否有足够的现金来维持企业的日常经营运转和(或)是否有太多现金富裕。

2023年初级银行从业资格之初级银行管理押题练习试题B卷含答案

2023年初级银行从业资格之初级银行管理押题练习试题B卷含答案单选题(共40题)1、资产负债表中,资产类项目的排列顺序是( )。

A.按资产获得的难易程度排列B.按投资人拥有该资产的永久性程度,先长后短的顺序排列C.按照资产流动性的程度由强到弱顺序排列D.按各类资产总量的大小顺序排列【答案】 C2、商业银行对贷款进行分类应考虑的因素不包括( ):A.借款人的还款能力B.借款人的还款时间C.借款人的还款意愿D.借款人的还款记录【答案】 B3、当前我国货币政策的主要传导媒介是()。

A.证券公司B.上市公司C.保险公司D.商业银行【答案】 D4、( )将互联网金融定义为:“是传统金融机构与互联网企业利用互联网技术和信息通信技术实现资金融通、支付、投资和信息中介服务的新型金融业务模式。

”A.《关于促进互联网金融健康发展的指导意见》B.《关于促进互联网金融快速发展的指导意见》C.《关于促进金融健康发展的指导意见》D.《关于促进互联网+金融健康发展的指导意见》【答案】 A5、商业银行、商业银行的工作人员、借款人、其他单位或者个人违反《商业银行法》所应承担的责任,不包括( )。

A.刑事责任B.民事责任C.民法责任D.行政责任【答案】 C6、(2018年真题)下列选项中,不属于《中华人民共和国银行业监督管理法》规定监管措施的是()。

A.限制资产转让B.责令暂停部分业务、停止批准开办新业务C.限制分配红利和其他收入D.罚款【答案】 D7、当一家银行的实力范围狭窄、资源有限,或是面对强大的竞争对手的时候,它的可行性营销策略是()。

A.专业化策略B.情感营销策略C.大众营销策略D.产品差异策略【答案】 A8、下列选项中,属于董事会应对商业银行经营活动的合规性履行的合规管理职责的是( )。

A.制定书面的合规政策,并根据合规风险管理状况以及法律、规则和准则的变化情况适时修订合规政策,报经董事会审议批准后传达给全体员工B.审议批准高级管理层提交的合规风险管理报告,并对商业银行管理合规风险的有效性作出评价,以使合规缺陷得到及时有效的解决C.识别商业银行所面临的主要合规风险,审核批准合规风险管理计划,确保合规管理部门与风险管理部门、内部审计部门以及其他相关部门之间的工作协调D.明确合规管理部门及其组织结构,为其履行职责配备充分和适当的合规管理人员,并确保合规管理部门的独立性【答案】 B9、下列关于商业银行会计系统控制的说法中,错误的是()。

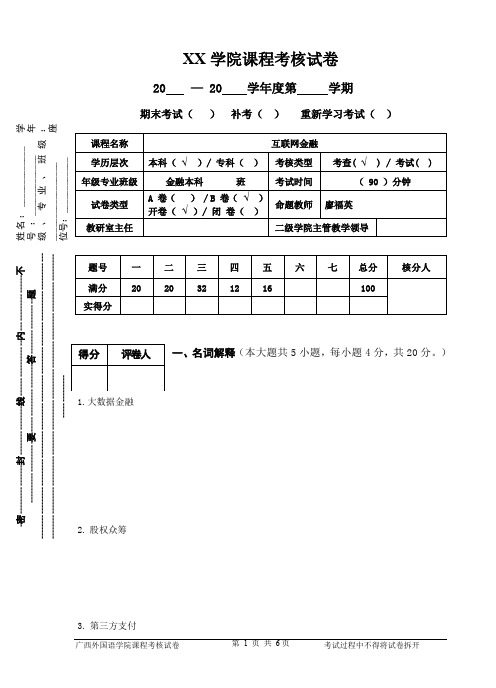

(完整word版)互联网金融期末考查试卷B

XX 学院课程考核试卷一、名词解释(本大题共5小题,每小题4分,共20分。

)1.大数据金融2. 股权众筹3. 第三方支付-密----------------封----------------线------------------内------------------不--------------------要----------------------答------------------题------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------ 姓名:_____________ 学号 :_____________ 年级、专业、班级:_________________ 座位号:____________期末考试( ) 补考( ) 重新学习考试( )4.智能理财5.Peer-to-Peer Lending二、判断题(本大题共10小题,每小题2分,共20分,把正确答案填入答案框内,对的打“√”,错的打“×”。

)1.移动支付包括了网络支付中“移动电话支付”和机遇移动通信终端的“互联网支付”,即所谓移动互联网支付,以及“近场支付”。

2.手机微信支付属于近场支付。

3.手机支付宝支付属于近场支付。

4.根据《网络借贷信息中介机构备案管理登记指引》的规定,新设立的网络借贷信息中介机构在依法完成工商登记注册、领取企业法人营业执照后,应当于10天内向工商登记注册地地方金融监管部门申请备案登记。

5.《关于促进互联网金融健康发展的指导意见》(银发〔2015〕221号)提出了互联网支付应始终坚持服务电子商务发展和为社会提供小额、快捷、便民小微支付服务的宗旨。

中国银行业的改革和盈利能力毕业论文中英文资料对照外文翻译文献综述

中英文资料对照外文翻译文献综述China’s Banking Reform and Profitability1Erh-Cheng Hwa Yang Lei1. IntroductionThe World Bank (1997) once claimed that China’s financial sector was the soft-belly in the economy. Financial sector reform has long been argued as necessary to raise efficiency in the use of the capital and in rebalancing the economy toward consumption-based growth, without which the country’s growth sustainability is in jeopardy (see Lardy, 1998; Prasad, 2007).Indeed, not too long ago, China’s state banks were deemed “technically insolvent”and their survival hinged solely on the nation’s abundant liquidity.However, after the launching of banking reform, strong profitability has returned to state commercial banks recently. But it may be too early to declare a complete victory on banking reform as yet, since Chinese state banks have embarked on the path of reform not too long ago. In addition,their strong financial performance has ridden on the back of strong but unsustainable growth. As growth has begun to soften under the weight of a global recession in 2008, banks are expected to navigate in a more difficult economic terrain than hitherto. The aim of this paper is not to evaluate the effect of banking reform on bank performance, which is better tackled after the completion of a full credit cycle. Rather, our aim is to take stock of the progress in reforming China’s state banks by reviewing the banking reformstrategy and analyzing their recent strong post-reform financial performancewhich, however, cannot be entirely separated from reforms efforts1Review of Pacific Basin Financial Markets and PoliciesVol. 13, No. 2 (2010) 215–236©World Scientific Publishing Co.and Center for Pacific Basin Business, Economics and Finance ResearchDOI: 10.1142/S0219091510001925undertaken thus far.This paper has three sections. In Section 2, we review the reform strategy of China’s large state banks, which is the main thrust of China’s banking reform, as well as its implementation. The Section 3 analyzes 2007 financial performance focusing on the four largest state commercial banks that have floated shares in the market: Industrial Commercial Bank of China (ICBC),China Construction Bank (CCB), Bank of China (BOC), and Bank of Communications (BOCOM). The conspicuous exception is Agriculture Bank of China (ABC), which is still in the process of restructuring for market listing at an appropriate time later. Section 4 concludes with an assessment on bank performance.2. Bank Reform Strategy and Its Implementation2.1. Bank reform strategyBefore reform, state banks were solely owned by the State and served national economic policy goals.1 Since they were not wholly profit-making commercial entities, common commercial banking criteria for evaluating their financial performance do not apply strictly. Nevertheless, as soon as the country decided to embark upon the path of a socialist market economy in the October 1992 CCP Congress, commercialization of the state banks had become a foregone conclusion. The goal of banking reform is to turn state banks into commercial entities that are competitive in the marketplace and can provide efficient intermediation of the nation’s saving. Given their dominance in financial intermediation, the banks play a crucial role in the efficient allocation of capital.2.1.1. Creating the enabling environment for banking reformThe country’s market reform and opening program has greatly accelerated since 1992 when in October that year the 14th CCP Congress declared that the goal of reform and opening was to create a socialist market economy,which effectively ended the experimental nature of economic reform and opening program launched since the late 1970s. The firming up of market-oriented reforms has created an enabling environment for a host of reforms central to the socialist market economy construct including foremost the banking reform. In early 1994, in response to the inflation threat, the government launched macroeconomic reform encompassing central banking,exchange rate management, and fiscal policy and taxation. The macroeconomic reform permitted the central authorities to regain macroeconomiccontrol lost to local authorities in the decade of the 1980s under the decentralization policy of “fang quan rang li”.2 While decentralization ushered a period of rapid growth, it also generated significant macroeconomic instability.Indeed, the pursuit of macroeconomic reform significantly dampened macroeconomic cycles in the 1990s. Second, in the same year, the government created three policy banks —State Development Bank, Agriculture Development Bank, China ExportImport Bank —to relieve state commercial banks of their traditional policy mandates.Third, the government promulgated central banking and commercial banking laws in 1995 to provide the legal foundation for banking reform.Fourth, beginning from 1996 the government began to vigorously pursuit enterprise reform that paved the way for banking reform, even this resulted in large and painful layoffs of redundant state workers. Pursuingenterprise reform ahead of banking reform was necessary considering that state-owned enterprises were the main clients of state banks and hence their main source of non-performing loans NPLs, which was at the same time the contingent liability to the government. Hence, unless the reform of stateowned enterprises takes hold, any reform effort of the state banks would be in vain. On the other hand, as soon as the state-owned enterprise reform was pressed forward, the banking reform could no longer be postponed. This is because as state-owned enterprises were restructured, liquidated, merged, or bankrupted out of existence, the banks must start to recognize the hidden losses on their books. This, in turn, triggered the need to recapitalize the banks, as a large amount of non-performing loan was written-off.Fifth, the State Council in February 2002 decided to reform solely stateowned commercial banks into internationally competitive financial enterprises, transform them into state-controlled shareholding commercial banks,and encourage listing their shares in the market.Sixth, China Banking Supervisory Committee was created in 2003 to raise the regulatory capacity to supervise banks. Finally, adhering to the 2001 WTO accession agreement, the government uses the entry of foreign banks into the local banking market to inject competitive pressure to the local banking industry in order to gain efficiency. Beginning from the end of 2006, foreign banks can engage in local currency business.2.1.2. Reforming corporate governance and restructuringthe balance sheetThe country’s large state banks have followed several steps to undertake internal corporate reform. The first is to reform the corporate governance by inviting other investors to dilute the sole state ownership while still retaining its dominance. In particular, the banks have made an effort to seek foreign strategic partnership with the view to bringing in modern banking practices and technology. The broadening of ownership also entails selling a portion of bank shares to the equity market to make bank management accountable to the marketplace. To successfully woo outside investors, be it strategic partners or public investors, the banks must put forward a creditable inhouse reform plan and implement it credibly. No doubt, the better and more credible the internal reform plan is, the more likely it is for the banks to attract reputable outside partners and fetch a better deal with their counterparts or in the equity market.Hence, the first step the government undertook was to strengthen the balance sheet of state banks whose credit flows had been clogged up by inadequate capital and piles of bad debts accumulated under the previous economic planning regime. In 1998, the government issued RMB270 billion (US$32.6 billion) worth of 30-year fiscal bonds to recapitalize the balance sheets of the four largest state banks: ICBC, BOC, CCB, and ABC in order to comply with the international capital adequacy standards. Again, on December 30, 2003, the government provided US$22.5 billion each to CCB and BOC, with US$15 billion provided later in April 2005 to ICBC to support their respective listings in the Hong Kong stock exchange.Among the four largest state banks, CCB was the first to have its shares successfully listed in the Hong Kong stock exchange and thus the first to have its reform effort passed by the market test. In addition, as part of the scheme of recapitalization, the banks also issued subordinated debt to the local market:BOC, RMB60 billion; CCB, RMB40 billion; ICBC, RMB35 billion; and BOCOM, RMB12 billon.In 1999, the government created four asset management corporations AMCs, one for each of the “big four”: ICBC, CCB, BOC, and ABC, to manage RMB1.4 trillion of loans purchased from the books of the state banks at face value, of which 1.3 trillion were deemed non-performing (about 15% of GDP). The transaction was financed partly by central bank loan(RMB573 billion) and partly by treasury bonds (RMB820 billion). A second transferring of NPLs in the amount of RMB1.186 trillionto the AMCs took place during the period from June 2004 through June 2006.The banks also launched reform measures to improve internal management including strengthening the human resource base, introducing modern risk management practices, and moving up the standard of NPL classification to comply with the international standards.2.2. Implementation of reform2.2.1. Seeking diversification and attracting foreign strategic partners Following the blueprint of reform, the banks have successfully launched and implemented the reform strategy. ICBC, CCB, BOC, and BOCOM all have their full state stake in the company diluted to below 70% by incorporating non-state ownerships, which includes foreign ownership, domestic legal persons, and public ownership (publicly owned and traded shares). Among non-state owners, foreign strategic partnership usually has the highest stake in the company: ICBC, 7.2%, BOC, 13.9%, CCB, 10.3%, and BOCOM,18.7% (Table 1).The participation of foreign and domestic capital as well as public shares in state commercial banks has not only strengthened bank capital, but also exerted a positive influence on the corporate governance, in particular in the case of foreign participation, in so far as it stems the undue intrusion of government into the banking business. Second, all state commercial banks have installed modern corporate governance structure encompassing shareholders congress, corporate board plus outside directors and supervisors,supervisory board, and senior management structure. By the end of 2007, 33 foreign institutional investors have invested in twenty-five domestic banks, with a total capital injection of US$21.3 billion.These foreign strategic investors have entered in various strategic corporative agreements with domestic partners in widely diversified areas of banking,including retail banking, corporate governance and risk-management,trading, RMB derivatives and currency swaps, foreign exchange structured products, and trade and small-and-medium enterprises SME financing. In addition, domestic banks and their foreign partners share their networks and custom base for providing services and cross-selling financial products.Finally, human resource development program is a common feature in strategic corporative agreements, with training courses offered in SME management and financing, wealth management, fund trading, risk management, and implementation of the Basel Capital Agreements, etc.2.2.2. Successful public listingsAfter launching internal restructuring and successful attraction of reputable foreign strategic partners, state commercial banks were successful in listing their shares in the Hong Kong (H share) and Shanghai (A share) stock exchanges and hence for the first time subject to the market discipline:BOCOM, June 2005; CCB, October 2005; BOC, June 2006; ICBC, October 2006 (which was the first double listing in both the Hong Kong stock exchange and the Shanghai stock exchange). Public listing of bank shares together raised RMB445 billion (US$60 billion) in the open market, about 26% of combined net capital. In comparison, the funds raised through foreign strategic partners was US$15 billion. In 2007, two small shareholding banks were listed in the Shanghai stock exchange, bringing the total listed to seven among 12 shareholding banks. In addition, three city commercial banks based, respectively, in Beijing, Nanjing, and Ningbo were listed in the Shanghai A share market, paving the way for other city commercial banks to restructure and then seek listing in the stock exchange. Having benefited from rising share prices, ICBC, CCB, and BOC were, respectively, the first,second, and the fourth largest bank in the world by market capitalization at the end of 2007: US$338.9 billion, US$2202.5 billion, and US$197.8 billion.2.2.3. Strengthening capitalBy the end of 2007, nearly 80% of banks by asset have fulfilled capital adequacy standards. The capital adequacy ratio for the four listed state commercial banks was, respectively, 13% for ICBC; 13.3% for BOC; 12.6% for CCB; and 14.1 for BOCOM. The core capital adequacy ratio was, respectively, 11% for ICBC; 10.7% for BOC;10.4% for CCB; and 10.2% for BOCOM.2.2.4. Building risk management systemsSince 2006 CCB and other large state commercial banks have begun to introduce a vertical risk management system to consolidate risk management into the hands of the newly created chief risk officer. The reform has helped to stem undue interferences in the loan decision process at the local level. At the same time, by taking advantage of information technology, banks have begun to streamline and optimize the operational processes and procedures in order to reduce operational risks. Banks have also begun to use quantitative risk models to gauge and simulate various risk scenarios facing them such as stress test. The concept of economic/risk capital has been adopted to manage risk quotas, allocate bank resources, and pricing of products. Banks have alsostrengthened the analysis of market and liquidity risks while controlling operational risks through improved internal control procedures by employing quantitative tools and models. Last but not least, banks have taken steps to build a new risk or credit culture.2.2.5. Pursuing strategic transformation of the business modelChinese banks have traditionally focused on corporate businesses, the wholesale banking so to speak. However, as the local capital market gradually matures and the income and wealth of Chinese households continue to grow apace, the banks find growing business opportunities in consumer-oriented financial services such as mutual funds, mortgage financing, wealth management, and personal loans. These are also areas of financial services where the newly arrived foreign banks aim to capture with their competitive strength.Hence, both for seeking new sources of profit growth and achieving a more diversified and balanced revenue base, as well as for meeting the competition from foreign banks head on, the Chinese banks are compelled to seize the opportunity and meet the challenge to embark on the path of a strategic transformation of the traditional business model toward retailing banking.New thrusts of retail banking include credit card, personal loans, and wealth management, mutual fund, insurance products and other products generating fee-based income. Retail banking, in turn, has called for greater investment in information technology to develop efficient systems in processing personal loan, internet banking, and tele-banking, as well as improve the efficiency of retail networks to better serve the needs of retail rge state commercial banks like CCB have also initiated special programs to cater to the need of small and medium enterprises, SMEs. In addition, they have started to branch out into new areas of financial services, thus gradually and steadily moving toward universal banking encompassing investment banking, issuance, securities, private banking, and financial leasing.Banks have also started to grow overseas business either by establishing more new overseas branches or through merging and acquisitions of foreign financial entities.4. Conclusion: Assessment of Bank PerformanceThe strong financial performance of large state banks was carried into the first half of 2008 even as growth slowed by nearly 2 percentage points to 10.4% from the firsthalf of 2007 due to a combination of falling external demand and tighter credit policy. In the first half of 2008, net profit (profit after tax) grew, respectively, 71.3% for CCB, 56.8% for ICBC, and 36% for BOC over a year ago. Although the reduction of corporate income tax from 33% to 25% accounted for partly the increase in profit, but the key underlying factors driving profit growth remained the same as the last year. First,net interest income continued to benefit from rising interest margins as well as rapid asset growth and still is the main source of operating income, possibly for the foreseeable future. Second, fee and commission income again witnessed an explosive growth: CCB, 59.3%; BOCOM, 50%, ICBC, 48%;BOC, 45.1%, in spite of a sharply cooled stock market that has curtailed income derived from hot-selling market-based financial products of the previous year such as stock mutual funds. For large state commercial banks,the share of fee and commission income in total operating income reached a new record in the first half of 2008: CCB 14.9%; ICBC, 12.3%; BOC,31.4%. In the meantime, asset quality continued to improve as the NPL ratio continued to drop. By the end of June, the NPL ratio of ICBC and CCB were, respectively, 2.4% and 2.2%, representing a decline of 0.33 and 0.39 percentage points, respectively, from the end of 2007.Judged by record profit, much improved asset quality, and high ROE,the recent financial performance of the four large state commercial banks is nothing short of spectacular. Furthermore, as fee and commission income and more broadly retail banking revenue has taken off to become a strong source of profit growth, banks appear on track to realize their long-term strategic goal of diversifying into a more stable base of income generation that is less prone to business cycle risks. Thus, large state commercial banks appear to have come a long way in reforming themselves into a modern commercial bank. This outcome should be a surprise to some of earlier research findings that argue state commercial banks did not seem to have changed bank behavior fundamentally after launching banking reform. For instance,Podpiera (2006) shows that banks do not appear to make lending decision based on a commercial basis. Dobson and Kashyap (2006) assemble macroeconomic, microeconomic and anecdotal evidence suggesting that the pressure to make policy loans is continuing despite the reforms. However, the recent empirical work by Demetriades et al. (2008) seems to counter their findings by showing that bank loans is positively correlated with future value added and TFP growth during 1999–2005,even for state-owned enterprises. Moreover they find that firms with access to bank loans tend to grow faster in regions with greater banking sector development.Can this financial performance of banks be sustained? It appears that the good financial performance has been the result of two crucial factors,although it is not easy to delineate the two. First, a supportive macroeconomic environment —with a strong growth averaging 10.7% per annum over the period: 2003–2007 and a partially liberalized interest rate regime —helped to boost revenues. Second, banking reform has been instrumental in raising efficiency and holding down costs, both of which boost the return on capital.Compared to the impact of banking reform, the supportive macroeconomic environment exerts more a cyclical than fundamental impact on bank performance and is thus a less sustainable force. Indeed, the surging inflation as well as bubbles in the stock and real estate markets in 2007 already served as warning signals that the high growth in last several years is unsustainable. In 2008, the economic growth slowed sharply as a result of tightened money and credit policy and an unexpected large decline in external demand that sharply slowed down export growth. Although bank performance held up pretty well so far, a precipitous economic slowdown would sooner or later raise business risks and worsen asset quality for the banks. The immediate challenge of banks is how to skillfully navigate the more difficult economic water by properly controlling risks and staying on the course of restructuring and reform.If the successful public listing marked the end of the first phase of banking reform, it is clear that banks have entered a new phase of reform only a short while ago with much of the journey still lying ahead. Many of the recently launched corporate reforms: governance, internal control and operation procedures, risk management, and human resources are still work in progress and have not yet been brought to fruition. Banks are also in the early phase in adapting to the new business model mandating more attention being paid to retail customers and commission and fee-based incomes. Hence, they have to continue to be valiant on reform and learn to adapt to the vagaries of financial markets while catering to the evolving needs of customers as their demand for new financial services grow.While putting the bet on banking reform, there is no reason to be overly pessimistic on the short-term macroeconomic risks. China ran a budget surplus and had a lowgovernment debt of about 22% of GDP in 2007, as well as a relatively low urbanization ratio at around 44%. More importantly, Chinese banks have embarked on a reform path with healthy balance sheets and a strong capital base. Thus, China enjoys considerable flexibility to deploy a strong public sector investment program in order to strengthen domestic demand and mitigate the downside risks caused by the expected sharp decline in exports. The government unveiled such a public sector investment program with price tag of RMB4 trillion in mid-November 2008 (about 12% of GDP) that covered two years to last through 2010. The program complimented the expansionary money and credit policy that had been initiated a couple of months ago. If properly implemented and, in particular, in conjunction with structural rebalancing policies, the program should help to sustain strong growth in the short-run and even more important to regain macroeconomic balance over the medium-term.中国银行业的改革和盈利能力1概述世界银行(1997年)曾声称,中国的金融业是其经济的软肋。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

译文银行业是必要的而银行不是,互联网时代的金融中介机构的未来摘要本文探讨了互联网时代下金融机构和银行作为特殊的金融机构的未来可能是怎样的问题。

由于互联网而导致的交易费用的减少会降低进入金融产品市场的壁垒,因为有可能不再需要运行成本密集型的分支的大型系统。

但是,对金融机构的职能研究表明,不是每个人都可以销售和经销金融产品。

这是真的,因为金融业务中的信息不对称问题需要一个拥有良好信誉的中介,也因为需要限制大型资本基金转换资产的风险。

这两个要求变现了进入金融中介市场的重要壁垒。

并不是每一个金融产品会因为互联网的崛起而将面临更多的竞争,只有那些标准化和低风险的产品。

此外,那些拥有可观资本和良好声誉的大公司可能被视为银行的新竞争者。

关键字:银行业,银行,金融机构,互联网1、引言“银行业是19世纪的钢铁行业。

”当谈到关于新的信息技术对银行的影响的谈论时,这句话经常被提起。

更一般来说,可能有人会问,新信息技术是如何成功的,特别是互联网的,可能会改变商业和金融机构的市场情况。

在互联网的帮助下,人们可以执行所有银行的业务,而不需要银行。

这意味着传统银行分支机构的中介。

此外,互联网已经使客户直接从网上购买股票而不需要访问当地的分支银行。

从更广泛的意义上来说,在互联网的帮助下,金融市场的供给和需求可能通过互联网满足,而不需要金融中介机构。

互联网的崛起是否真的是金融中介机构的威胁?在急剧减少的交易成本情况下,商业和竞争将如何变化?本文考察了互联网的成功对金融机构和银行的影响。

2、金融机构的发展几个世纪以来,许多金融交易需要个人的存在。

随着现代信息技术的发展,这些都被改变了。

如今,客户可以在不进入当地分支银行的情况下进行任何金融交易。

转移支付和支付账单可以通过网络进行,个人金融交易以及关于金融问题的信息咨询业可以通过网络进行。

此外,互联网创新类似智能卡或者其他电子支付系统消除了为了得到一些现金而访问分支银行的需要。

但是互联网也会改变咨询活动:在许多情况下,它甚至可能减少个人存在的需要。

许多金融机构不仅通过网络提供大量与客户相关的信息,而且也推荐股票和其他投资机会。

互联网将使客户拥有一个综合的个人金融管理系统,而不需要银行分支或者个人经纪。

另一个重要的业务是支付交易:目前,借记卡和信贷业务以及现金付款,主要是通过银行和信用卡公司。

因为电子传输比传统支付系统更加便宜、快捷和方便,它可能只是一个时间问题,直到传统付款计划将完全被电子支付所取代。

相反这些发展,现代通信技术的兴起也可能使金融中介机构嫩巩固提高顾客的个人联系。

在未来,顾问在银行的工作地点可能不是一个部门或者一个办公室,而是在客户的家里。

3、金融中介机构的职能金融中介机构的职能可以分为三类:⑴首先,他们帮助处理由于信息问题而存在的问题。

⑵作为第二功能,他们转换资产的性质,为他们的客户提供流动性。

后者的功能主要由银行提供。

⑶作为第三功能,金融中介机构发布金融产品和关于这些产品的信息。

这些功能现在应当再间断的解释。

金融中介机构最重要的功能源自于这样一个事实,一个银行可能无法找出回报最好和最佳的投资,无法估计债权人的偿付能力。

金融中介代理解决信息问题的债务人,帮助找到最好的投资。

一个中介也对第二个信息问题有帮助:大多数投资需要大量的资金,大量的债务人将资助一个项目。

单一银行可能无法监控债权人的行为,这样他可能不确定贷款的债权人是否用在最好的用途以便他偿还贷款。

中介通过监测债务人来充当这些债权人的代理。

这个论点表明他们是在给客户节约交易成本,同时考虑规模经济,因此他们可以提供比单个投资者更便宜的金融服务。

金融机构的第二个作用是他们转换获得的资产。

他们将不同期限、大小和风险的资产进行转换。

对于单个银行或者借款人来说,找到一个合适的需要贷款的伙伴将非常耗时。

金融中介可以转换期限和存款或贷款池的大小。

比如,他可以资助一个大的长期贷款循环许多小的短期贷款。

通过提供一个集中的市场,中介机构支持银行和借款人的匹配提供的所有类型。

中介来匹配的能力显然不一致的类型的合同有时被称为转化效果。

金融中介机构的第三个功能可以被描述为产品和关于这些产品的信息的分布。

金融中介机构提供服务的生产者的金融产品,分销他们的产品,通知消费者产品的存在和特征。

4、互联网下的金融中介机构4.1金融业务良好声誉的必要性互联网最重要的一个特性是降低交易成本。

这将导致市场的扩张和劳动力的分工。

交流成本的减少将帮助金融中介机构达成新的市场和客户,不需要建立一个昂贵的分支网络。

此外,在互联网的帮助下,从技术观点来看是可能的,银行和借款人都在电子平台上因此资本供给和需求可以被匹配,而这可能都不需要传统意义上的金融中介机构。

这意味着计算机将是获得贷款或储蓄的唯一的工具。

考虑到金融中介机构的功能上面所讨论的,这个想法很不现实。

不是每个人都能成为一个金融中介机构。

但是怎么使出借人信任那些金融中介机构呢?它可能联合借款人欺骗出借人。

这是一个由于信息不对称而存在的经典的主要代理问题。

解决这个问题的一个方法是信任:如果代理显示出了良好的性能在过去,投资者愿意相信这个代理。

金融中介的良好的声誉将帮助他吸引新顾客,因为新投资者确信他过去好的结果。

4.2大型基金的必要性金融中介机构的第二项职能包括哪些?如上所述,金融中介机构帮助转换资产的成熟、规模和风险。

第一眼看去,因为潜在借款人和贷款人沟通成本的减少,互联网将让资产转换变得更加便捷。

通过互联网,将更容易找到适当的寻求贷款的合作伙伴,而借款人又有提供相当规模和成熟度的贷款的意愿。

正如上面的小节中解释的那样,中介机构的一个重要功能是,一个集中的市场供应来缓解资本的供应需求匹配了。

这不是真正的转换资产的风险。

加入大型基金,金融中介机构可以减少投资者的投资风险。

如果银行贷款给一个人,借款人未能偿还贷款,贷款人将损失所有的钱。

如果银行未能偿还贷款金融中介,中介不会破产,因为这种贷款只占一小部分的资金。

正如以上所说,做这样的金融中介机构需要一个很大的基金池。

这种基金同时也需要保证客户一定数量资金的流动性。

保持一定量的必要性的资产无疑是一个障碍对新进入者进入市场金融服务。

考虑到这些因素,我们可以假设与金融交易的风险更大,需要更多的资金来减少这种风险,或资产(这意味着较小的标准化该资产的流动性较差的市场)新的竞争对手的进入可能会变得不太可能,因为并不是每个中介可以保持一个大型基金的资产,以改变消费者的风险资产,并保证他们的流动性。

4.3金融产品的分布但是互联网可能克服金融中介机构的第三个功能:金融产品和信息的分布会变得比现在更容易和便宜。

这意味着成本密集的银行分支机构可能会变得过时:电子货币的发展,网上银行和在线咨询可能使这种中介形式的减少。

这意味着金融中介进入这个市场的一个重要壁垒可能会消失。

但是尚不清楚银行的传播职能将会过时。

这可能只适用于通过分支机构的产品和信息分布。

5、金融中介机构的未来考虑到金融中介机构的功能,有一些关于金融中介机构未来发展的注意事项。

首先尚不清楚互联网的兴起会导致金融服务领域中介机构的多或少。

道德风险和信息不对称等问题将不会完全被消除的互联网,所以,金融中介仍然是必要的。

此外,市场的扩展将通过互联网将提供更多专业化的机会,从而为金融中介机构创造新的商业机会。

市场的扩大和交易成本的降低也会扩大分工的数量,从而为中介机构创造更多的商业机会。

但是同时银行也存在潜在的危险:由于上面列出的参数和分支的减少系统的必要性,新的竞争者可以进入市场并提供的产品或服务被提供之前只能通过银行。

金融产品的两个特征可能很重要,如果一个人想要回答未来金融产品的竞争:金融产品的标准化程度和它的风险。

产品的标准化程度决定了质量评价的需要,减少了关于产品和客户信息的需要。

考虑这些金融服务的特点,可以哪些金融产品提供的可能仍然是传统的金融中介机构和哪些产品可能基于互联网的新中介机构。

总的来说,金融中介机构将不会成为未来几十年的“钢铁行业”。

银行业不会消失,此外,金融服务的需求将日益旺盛。

然而,这种需求不仅对银行有利,而且对大公司和保险公司也有利。

互联网甚至可以创造新的就业机会:互联网上日益增加的信息可能需要一个代理金融信息服务。

此外,互联网的兴起可以促进虚拟金融中介机构的发展:他们可以通过互联网向不同的公司或银行提供各种金融服务。

外文原文Banking is essential, banks are not. The future of financial intermediation in the age of the InternetThis paper examines the question how the future of financial intermediaries and banks as special financial intermediaries may look like in the age of the Internet. The reduction of transaction costs caused by the Internet will reduce the barriers to enter the market for financial products, because there may be no longer a need to run a large system of cost-intensive branches. But as closer examination of the functions of financial intermediaries shows, not everybody can sell and distribute financial products. This is true because of asymmetric information problems in financial business which require an intermediary with a good reputation and because of the need to keep large funds of capital to transform the risk of assets. Both requirements represent an important barrier to enter the market for financial intermediation.Not every financial product will be exposed to more competition due to the rise of the Internet but only products which are standardized and have a low risk. Moreover, large firms with high amounts of capital and a good reputation can be considered as new competitors for banks.Keywords: banks, banking, financial intermediaries, Internet1. Introduction“Banks are the steel industry of the nineties.” This statement is often heard when it comes to a discussion of the consequences of new information technologies for banks.More in general, it can be asked, how the success of new informationtechnologies,especially of the Internet, may change business and market situation for financial intermediaries.With the help of the Internet it will be possible to execute all banking business from home without the need of a bank. This would mean the end of traditional banking by means of branches. Moreover, the Internet already enables customers to buy stocks directly without visiting a local branch of a bank. In some years it may be even possible to buy stocks via the Internet directly from the issuer without the need of a stock exchange and a broker. In a broader sense, with the help of the Internet it may be possible that supply and demand on financial markets may meet via the Internet without the help of financial intermediaries. Is the rise of the Internet really a threat for financial intermediaries? How will business and competition change in a world with extremely strong reduced transaction costs? This paper examines the consequences of the success of the Internet for financial intermediaries and banks. A financial intermediary shall be Paper presented at the Second Berlin Internet Economics Workshop.defined as an institution that acts as an intermediary on capital markets by matching supply and demand on these markets. He does not only provide market transparency but moreover acts as a middleman between lenders and borrowers.A bank is a special financial intermediary with a lot of cost-intensive local branches. Moreover, a bank provides a bundle of different services while most other intermediaries only concentrate on one or few specific business. For example, a bank provides credit to firms and private customers, sells stocks and mutual funds and pays interest for saving deposits and distributes the money it receives from the central bank by providing its customers with cash. (These arguments are valid for the European Universalbanken system, but partially also for the anglo-american Trennbanken system.) As a consequence, the balance sheet of a bank consists of immediately withdrawable liabilities which are used as legal means of payment as well as of liabilities with a longer maturity. Moreover, a lot of these liabilities deposited by the customers are not assigned to a special purpose. To sum up, a bank bundles a lot of financial products and services like consulting and is not as much specialized than other financial intermediaries.The second section will give a short overview of developments in the financial sector driven by technical progress. The third section will examine the functions of financial intermediaries and how they will be affected by new information technologies. In the following section, some conclusions shall be drawn from these considerations. This may help to answer the question how the landscape for financial intermediaries willlook like in the age of the Internet.2. Developments in financial intermediationFor centuries, many financial transactions required personal presence. This has changed with the rise of modern communication techniques. Nowadays a customer can do all his financial business without entering a local branch of a bank. This can be demonstrated with online-banking: The customer does all his banking (business) at home via the Internet. The transfer of payments and the payment of bills can be done via the net and information about personal financial transactions as well as consultation about financial questions can also be given via the net. Moreover, innovations like smart cards or other electronic payment systems eliminate the need to visit a branch in order to get some cash.But the Internet will also change consulting activities: it may even reduce the need for personal presence in many cases. Many financial intermediaries provide not only a lot of customer-relevant information via the net, but also recommendations on stocks and other investment opportunities. Moreover, techniques like video-conferencing or Web-TV by means of a so-called settop-box will enforce this development. The Internet will enable intermediaries to bundle the capacities of their consultants wherever they may be located. This means that a customer can consult many experts from without even leaving his home. The Internet will enable a customer to have a comprehensive personal financial management system without the need of a branch or personal contacts. Banks like Barclays have already implemented a system called RATE (remote access to exTHE FUTURE OF FINANCIAL INTERMEDIATION IN THE AGE OF THE INTERNET 9 perts): Customers can contact specialist staff at Barclays Stockbrokers in Glasgow for detailed advice. The experts can give comments and background information as well as predictions by using a video-conference-link within the screen (see [5]).These forms of banking without branches will not only appear in the home of customers but even in remaining branches. A first glimpse at the potential branch of the future can be caught at the Lisbon Branch of the Banco Portugues do Atlantica (BPA).Instead of human staff the customer is faced with a set of multimedia kiosks set into the walls, which not only distribute money, but offer a range of other functions (see [5]): a scanner reads the bill, deducts the money from the account of the customer, transfers the money to the account of the issuer and notifies the company that the bill is paid. The end of this development may be a virtual bank, where all financialbusiness will be executed via the Internet without the need of any branches.Another important business are payment transactions: At the moment, the debit and credit business as well as cash payment is mostly done by banks and credit card companies. Because electronic transmissions are much cheaper, quicker and easier than conventional payment systems, it may be only a matter of time until traditional payment schemes will be replaced completely by electronic purses. But even classical intermediation services of banks as the emission of stocks or industrial obligations may be replaced by direct emission of these securities by the enterprises themselves. Opposite to these developments, the rise of modern communication techniques may also enable financial intermediaries to improve the personal contact to their customers.In the future, the working place for a consultant in a bank may not be a branch or an office, but the home of the customer. Laptops and mobile phones may help him to bring his back-office to the home of the customer. This development is called “mobile consulting” (see [3]).This short overview shows that the rise of the Internet may change the business of financial intermediaries in many ways. The most striking point in these developments may be the fact that financial intermediation in the age of the Internet may no longer require the existence of branches because much of this business will be done via the Internet. The word of a virtual bank has already spread (an overview can be found in[9,10]).This may have important implications on the competition in financial intermediation as later shall be shown. To get an idea how financial intermediaries may look like in the digital future, it will be necessary to examine the functions of a financial intermediary.With these functions in mind, it will be possible to ask how these functions will be affected by the growth of Internet-based financial business.3. Functions of financial intermediariesThe functions of financial intermediaries can be divided into three categories (for an overview over theories of financial intermediation see also [1]):First, they help to deal with questions that arise due to the existence of information problems.As a second function, they transform the nature of assets and provide their customers with liquidity. The latter function is mostly provided by banks.As a third function, financial intermediaries distribute financial products and information about these products.These functions shall now be explained in brief. The most important function of financial intermediaries arises from the fact that a single lender may not be able to find out the best investment with the highest return and to estimate the solvency of the creditor. A financial intermediary solves both information problems by acting as an agent for the debtor and helping to find the best investment. An intermediary helps also with the second information problem (see [9]): Most investments require larger amounts of money so that a large number of debtors will finance one single project.A single lender may not be able to monitor the behavior of the creditor so that he may not be sure whether the creditor uses the loan in the best way so that he will be able to pay it back. The intermediary acts as agent for these borrowers by monitoring the lender. Thereby, he also acts as principal for the lender by supervising him. By solving these information problems for many lenders, intermediaries are realizing economies of scale. This argument shows that they are saving transaction costs to their customers and that they can provide financial services much cheaper than a single investor due to the existence of economies of scale. By acting as an agent for the lender and principal for the borrower, financial intermediaries also provide a certain amount of control about lenders and borrowers, i.e., they provide a certain level of quality of the financial products they distribute. This gives more security to their customers about their savings and loans and saves transaction costs by providing an appropriate definition and level of quality.The second function of financial intermediaries is the transformation of the assets they acquire. They transform maturities, size and risks of these assets. For a single lender or borrower, it would be very time-consuming to find an appropriate partner who wants to give a loan in the amount and time-horizon desired by him. A financial intermediary can transform the maturities and the size of savings or loans by pooling them.E.g., he can finance one large long-term loan by revolving many small short-term loans.Intermediaries support the matching of lenders and borrowers of all types by supplying a centralized market for them. The ability of intermediaries to matchapparently inconsistent types of contracts is sometimes called transmutation effect (see [8]). Moreover, a intermediary can also transform the risk of an asset. He guarantees the borrower a certain interest rate and gives his money as venture capital, thereby transforming a risky investment into a safe one. The difference between the interest rate the lender receives from the intermediary and the interest rate the intermediary demands from the venture capitalist is the risk premium. By pooling savings and loans, intermediaries provide the possibility for a single customer to trade the risk of a single loan or saving against a share of the risk of a portfolio of these savings and loans. With the help of the law of THE FUTURE OF FINANCIAL INTERMEDIATION IN THE AGE OF THE INTERNET 11,large numbers, the possibility of a total loss for a single investor can be diminished by pooling large funds.As easily can be seen, the transformation of maturities and the transformation of risks requires a certain amount of deposits. This makes it clear that a financial intermediary needs a certain minimum size –measured in terms of deposits –to perform these functions well. This will be an important feature in the discussion of the future business fields for financial intermediaries. These funds are also necessary for another function of financial intermediaries that is mostly done by banks: Banks provide their customers with liquidity. A consumer has to take measures against a sudden unexpected need of consumption. Without a bank, he would be forced to keep a certain amount of liquidity as an insurance against this case instead of investing it in long-term interest rate bearing assets. If he gives his money to a bank, it can be invested into such assets while it is still possible for the customer to get money in cases of unexpected needs of liquidity, thereby loosing only a smaller share of the return of these assets than in the case of keeping this money as an insurance against a sudden need of consumption. By transforming the maturities of its deposits, a bank allows its customers to keep a smaller amount of liquidity as it would be the case in a world without banks.The third function of financial intermediaries can be described as the distribution of products and of information about these products. Financial intermediaries provide services for the producers of financial products by distributing their products and informing consumers about the existence and the characteristics of their products. For example, a bank provides a consumer with information about the existence and the quality of investment funds (but one should keep in mind that most banks inform mainly about their own investment funds, this is not the case for independent financialadvisors). But intermediaries can also have some influence on the consumers purchasing behavior. This is also a value for the producer of financial products. At least, a financial intermediary may help the producer of financial products to collect valuable information about his customers by aggregating demand information from a variety of local markets. By providing information about the average conditions on the market, a financial intermediary provides some market transparency. But intermediaries may not only provide information about the product, but also about the usefulness of the product and may help their customers to identify their needs reliably.The insurance business seems to be a good example for this.The distribution of products is a very important economic feature of financial intermediaries because it requires a widespread system of branches which is very capitalintensive.Banks can realize large economies of scale by distributing many financial products via their branches. This means that the distribution of financial services leads to a reduction in average costs (see [6]). This explains why banks supply several services:If a large net of branches once is set up, the banks gain the more economies of scale, the more products are distributed via these branches. These arguments show that only a limited number of banks with a broad regional system of branches can co-exist in a market, as long as the most financial services are distributed via these branches. In other words: The need to keep an expensive system of branches is a high barrier to enter the market for financial intermediation. This may change due to the rise of new communication techniques. This shall be discussed in the next section.4. Functions of financial intermediaries in a net-based world4.1. The need for reputation in financial businessThe most important single feature of the Internet is the reduction of transaction costs. This will lead to enlarged markets and to an extended division of labor. The reduction of communication costs will help financial intermediaries to reach new markets and customers without building up an expensive network of branches. Moreover, with the help of the Internet, from a technical point of view it may be possible that a lender and a borrower meet in electronic platforms so that demand and supply of capital may be matched without the need of a financial intermediary in the traditional sense. This would mean that a computer would be the only tool required to get a loan or to place a saving. Considering the functions of financial intermediaries discussed above, this ideaseems quite unrealistic. Not everybody can become a financial intermediary.The most important reason why financial intermediaries will still be necessary in the age of the Internet is their function as principals and agents. If a intermediary acts as an agent for the lender, a problem of asymmetric information rises. If a creditor gives money to a debtor, he faces two severe problems. First, he has only incomplete information about the ability of the debtor to pay back the loan. As a consequence of this, he will not be able to distinguish between “good” and “bad” loans (adverse selection).Moreover, a bad risk may be willing to pay a higher interest rate, because he might already have decided not to pay the loan back. Adverse selection generates a dilemma for the lender: He has to consider the trade-off between a higher interest rate he might get paid and the risk to loose the loan. If a lender is not able to distinguish between good and bad loans, he treats all borrowers equally, charging a risk-premium from every borrower. This means that the good must suffer with the bad. Banks handle this problem by putting in place a credit function, demanding a collateral or by limiting the volume of credit available to a single borrower (see [4]). This shows a strong argument for the further existence of financial intermediaries in the age of the Internet. A creditor cannot observe the behavior of the debtor after he received the loan. A bad debtor may not attempt to use the borrowed capital in a productive way in order to pay back the loan. After he received the loan, he may change his behavior (moral hazard). This leaves the creditor with the problem to control the behavior of the borrower after he received the loan. For a single lender, the task of finding a trustworthy borrower and to monitor his behavior may be very expensive if not impossible.To avoid this, he gives his money to a financial intermediary who acts as agent for him. The intermediary distinguishes between good and bad risks and supervises the debtor. This makes sense because the intermediary is an expert in identifying good risks and supervising debtors. The division of labor makes sense even in the business THE FUTURE OF FINANCIAL INTERMEDIATION IN THE AGE OF THE INTERNET 13 of financial intermediation. If there are fixed cost of monitoring borrowers, financial intermediaries will obtain economies of scale. This means that there is an advantage for financial intermediaries who specialize in this business. The existence of economies of scale rules out a world in which there are only bilateral relationships between lenders and borrowers.But how can the lender trust the financial intermediary? He may cooperate with theborrower to cheat the lender. This is a classical principal-agent-problem caused by the existence of asymmetric information. One way to overcome this problem is trust(see [11]): If the agent has shown a good performance in the past, the principal (the investor) is willing to trust this agent. A good reputation of a financial intermediary will help him to attract new customers, because new investors are convinced by his good results in the past. These considerations show that an important function of financial intermediaries cannot be replaced by the Internet: The intermediary acts as an agent for the customer; and a customer will not give his money to a financial intermediary without a good reputation. If a intermediary has shown in the past that he is reliable and does not cheat his customers, a customer may consider him as reliable for future business. Moreover, a long term relationship between the lender and the borrower is very helpful because there is already some trust between the lender and the borrower established (see [4]). A customer would never choose a partner as an agent for his money he never heard of before, because he could not be sure whether he would cheat him. The intermediary himself faces the problem of moral hazard and adverse selection when he is investing the money of his customers. This means he acts as agent for the lenders and as principal for the debtors.Choosing an intermediary makes only sense for the creditor if the intermediary has a good reputation. If the intermediary wants to stay in business, he will be aware to pay back the loan in time plus an adequate interest rate. If he will not be able to do this, he will loose his business. His reputation is a signal to potential lenders that he will pay back the money he received. To sum up, a financial intermediary with a reputation as a good debtor reduces the risk for the creditor that a loan may not be paid back. Therefore, the idea of financial business without financial intermediaries is not realistic at all.4.2. The need for large fundsWhat about the second function of intermediaries? As explained above, a financial intermediary helps to transform assets in their maturity, size and risk. At a first glimpse, the Internet will make it easier to transform assets because of the reduced costs of communication between potential borrowers and lenders. It will be easier to find an adequate partner or partners via the Internet looking for a loan that has the size and maturity the lender is willing to supply. Insofar, the matching of assets in maturity and size may become easier in the age of the Internet. One important function of intermediaries explained in the section above, the supply of an centralized market to ease the matching of supply and demand on capital, seems to be endangered. The needto transform as14 sets may be reduced due to the fact that it will become much easier to find an adequate partner.This is not true for the transformation of the risk of assets. By pooling large funds, financial intermediaries reduce the risk of an investment to the investor. If a lender gives a loan to a single person and the borrower fails to pay back the loan, the lender will loose all his money. If a lender fails to pay back a loan to a financial intermediary,this intermediary will not become insolvent, because this loan represents only a small fraction of his funds. From this point of view it makes sense to an investor to invest his money not in a single project or give it to a single borrower. If he puts his money in a fund, he trades the risk of a single project against the share of a risk of a portfolio of investments. These considerations show that it requires much more than a computer to provide financial services – even in the age of the Internet. A financial intermediary needs a large fund of savings, loans and investments to reduce the risk for the single customer. By giving their customers products with stable distributions of cash-flows, financial intermediaries can reduce the costs of an investment for their customers (see[1]). This shows that not everybody will be able to become a financial intermediary. The function of financial intermediaries as risk-pooling institutions will be very important in market segments with illiquid assets or long-term maturities. In these segments, the risk and the standard deviation of the returns on investment are very high. It requires a high risk premium and a large pool of funds to compensate for this risk.As shown above, to do this a financial intermediary needs a large pool of funds. This pool of funds is also needed to guarantee his customers a certain amount of liquidity. The necessity of keeping a certain amount of assets is surely a barrier for new entrants to enter the market for financial services. With these considerations in mind, one can assume that with a greater risk of a financial transaction – that requires a larger pool of funds to reduce this risk – or lesser standardization of an asset (which means a more illiquid market for this asset) the entry of new competitors may become less likely because not every intermediary may be able to keep a large fund of assets in order to transform the risk of its consumers assets and to guarantee them liquidity. One important function of financial intermediaries, the transformation of risks, will not be endangered by the rise of the Internet. This seems to be a very important argument, because the importance of risk management undertaken by financial intermediaries has grown rapidly in recent years (see [1]).。