百富便利支付维护手册

EMV2000_book_4中文版

EMV2000支付系统集成电路卡规范 第四册持卡人、服务员和收单行接口需求版本 4.02000年12月所有版权归©2000 EMVCo, LLC (“EMVCo”)所拥有。

任何对EMV2000规范(“资料”)的使用都必须遵照用户和EMVCo之间的授权协议(见<http://www.emvco.com/specificationss.cfm>)的条款的规定。

本文档和其中包括的资料可能包含瑕疵,EMVCo不接受由本文档的错误或缺失所导致的任何责任和义务。

EMVCo对本文档及其包含的资料不提供任何显式或隐含的承诺和保证。

特别地,EMVCo对特定目的的商业性和实用性不承担任何显式的或隐含的责任。

对本资料包含或相关的第三方知识产权, EMVCo不提供任何声明和保证。

EMVCo没有义务判断本材料任何部分的任何物理实现是否可能侵犯、破坏或以其它方式使用第三方的专利、版权、商标、商业秘密、技术和/或其它知识产权,因此,任何人在任何实现本档任何部分之前,请首先咨询知识产权律师。

EMVCo拒绝对本文档内包含相关的第三方知识产权承担任何责任或义务,包括但不限于任何对特定目的的无害性、适用性的显式或隐含的保证(无论EMVCo是否已经被告知、有原因了解还是事实上已经得知任何信息)。

使用本文档中包含的信息的用户必须独自承担确定和获取用于根据本文档及其包含的信息开发产品和服务所需要的所有专利和知识产权。

除上述限制之外本材料还提供公开密钥加密技术的使用,而这在某些国家是专利项目。

任何试图实现本材料的人必须确定自己的行为是否需要包括,但不限于,公开密钥技术专利的授权。

EMVCo不承担由于任何人侵犯知识产权所引发的责任。

目录 1. 范围 (6)2. 标准化参考 (7)3. 定义 (8)4. 缩写,符号和术语 (10)第一部分一般要求 (12)1.终端类型和性能 (13)1.1 终端类型 (13)1.2 终端性能 (14)1.3 终端配置 (15)2.功能需求 (18)2.1 应用无关的IC卡对终端接口的需求 (18)2.2 安全和密钥管理 (18)2.3 应用规范 (18)2.3.1 初始化应用过程 (18)2.3.2数据验证。

盒子支付产品培训手册45p

银行卡发卡行属地相同的(含同城同行),参考费率如下: 即时转账每笔最大限额为30000元; 金额1万元(含)以下的,转出卡每笔支付3元的交易手续费,1万-3万以下的,转出卡每 笔支付5元的交易手续费; 银行卡发卡行属地不同的(如:上海农业银行转账深圳中国银行),参考费率如下: 转出机构每笔支付的交易手续费为金额的1%,最低为5元,最高为50元。

快速划过;刷卡间隔不要过快,若遇到刷卡失败重新刷卡时,请稍微等待然后重新刷卡即可;刷卡时 卡与卡槽不平衡或者刷卡过慢均可能导致刷卡失败。 5、使用盒子耗费流量吗? 盒子交易时的数据量极小,使用一次的数据量约为3KB,因此您不用担心流量问题。 6、在手机端插入刷卡器之后,有电话接入听不到声音怎么办? 刷卡器插入的是音频口,有电话接入时需先拔出刷卡器即可正常接听电话。

分销100台

提货价格

498元

498元

分润

自行定义

自行定义

任务(月录入系统的量)70

50

三级分销 50台 498元 自行定义

30

分销首次提货可以贵一些

5.2媒体报道

2012年盒子支付用户数呈几何增长

29

5.2 媒体报道

盒子支付借助中国银联弯道超车

30

5.3 市场推广方式

4.1 Q&A

信用卡还款手续费

给交通银行、建设银行信用卡还款每笔2元,给工商银行信用卡还款每笔3元。其他银行信 用卡还款都是免费的。

支付宝充值手续费

交易额的1%,最低2元最高10元

即时转账与转账汇款区别

a、支持的银行:即时转账支持部分银行(借记卡)、转账汇款支持所有银行(借记卡) b、到账时间:即时转账即时到账、转账汇款T+1个工作日到账 c、手续费:

Skrill 商户门户批量支付指南说明书

Skrill Merchant PortalMass Payments GuideThis guide describes how to use the Mass Payment service.Version 2.2Paysafe Holdings UK Limited, 25 Canada Square, Canary Wharf, London, E14 5LQ, UKCopyright© 2021 Paysafe Holdings UK Limited. All rights reserved.Skrill ® is a registered trademark of Paysafe Holdings UK Limited and is licensed to Skrill USA, Inc., Skrill Limited and Paysafe Payment Solutions Limited (collectively, the “Paysafe Companies”). Skrill USA Inc. is a Delaware corporation, company number 4610913, with a business address of 2 S. Biscayne Blvd, suite 2630, Miami, Florida, 33131. It is a licensed money transmitter, registered with FinCEN and various states across the US. The Skrill Visa ® Prepaid Card is issued by Community Federal Savings Bank, member FDIC, pursuant to a license from Visa®. Skrill Limited is registered in England and Wales, company number 04260907, with its registered office at 25 Canada Square, London E14 5LQ. It is authorized and regulated by the Financial Conduct Authority under the Electronic Money Regulations 2011 (FRN: 900001) for the issuance of electronic money. Paysafe Payment Solutions Limited trading as Skrill, Skrill Money Transfer, Rapid Transfer and Skrill Quick Checkout is regulated by the Central Bank of Ireland. Paysafe Payment Solutions is registered in Ireland, company number 626665, with its registered office is Grand Canal House, Upper Grand Canal Street, Dublin, 4DO4 Y7R5, Ireland. The Skrill Prepaid Mastercard is issued by Paysafe Financial Services Ltd in selected countries and by Paysafe Payment Solutions Limited as an affiliate member of Paysafe Financial Services Limited in selected countries pursuant to a license from Mastercard International. Mastercard® is a registered trademark of Mastercard International.The material contained in this guide is copyrighted and owned by Paysafe Holdings UK Limited together with any other intellectual property in such material. Except for personal and non-commercial use, no part of this guide may be copied, republished, performed in public, broadcast, uploaded, transmitted, distributed, modified, or dealt with in any manner at all, without the prior written permission of Paysafe Holdings UK Limited and then, only in such a way that the source and intellectual property rights are acknowledged.To the maximum extent permitted by law, none of Paysafe Holdings UK Limited or the Paysafe Companies shall be liable to any person or organization, in any manner whatsoever from the use, construction or interpretation of, or the reliance upon, all or any of the information or materials contained in this guide.The information in these materials is subject to change without notice and neither Paysafe Holdings UK Limited nor the Paysafe Companies assume responsibility for any errors.Skrill Ltd.Registered office: Skrill Limited, 25 Canada Square, Canary Wharf, London, E14 5LQ, UK.Version Control TableSkrill Merchant Portal Mass Payments Guide1.ABOUT THIS GUIDE (5)1.1 Objectives and target audience (5)1.2 Related documentation (5)1.3 Conventions used in this guide (5)1.4 Prerequisites (5)2.Skrill Merchant portal (6)3.Mass Payments (7)3.1 Prerequisites (7)3.2 Mass Payments using a Payment File (8)3.3 Mass Payment – Transaction Statuses (11)3.4 Mass Payment Error Scenarios (12)3.5 Transfer with an API Request (Standalone Credits) (12)4.APPENDICES (13)4.1 ISO 4217 currencies (13)4.2 Languages supported by Skrill (13)4.3 ISO country codes (3-digit) (13)5.GLOSSARY (18)1.ABOUT THIS GUIDE1.1Objectives and target audienceThis document can be used as a reference in using the Mass Payments section of the Skrill Merchant Portal. This guide does not cover payments using the Skrill Automated Payments Interface (API). 1.2Related documentationAlong with this guide, you can use the following Skrill documents to understand about the Skrill Merchant Portal.1.3Conventions used in this guideThe following table lists the text conventions used in this guide.1.4PrerequisitesYou must complete the merchant setup process to access the various features of the Skrill Merchant Portal. To complete this process, reach out to your Account Manager or send an email to ***************************.2.SKRILL MERCHANT PORTALThe Skrill Merchant Portal provides you a single interface to manage your digital wallet accounts. Using the portal, you can manage digital wallets and the associated transactions. In this portal, you can also perform actions like transfer money instantly to an account, exchange money between wallets, send money to multiple recipients at once, import funds to wallets, view balances / reserves, and withdraw money to a bank account, and so on. Following is a list of transactions supported by the Merchant Portal.•Send money.•Make payments to multiple customers.•Upload money•Exchange money•Withdraw money to your bank account.•Switch between your accounts•Manage your bank accounts.•Manage your account balances.•Search, filter, and view transactions•Check bank transfers from other accounts.•Create and manage users.•Configure your wallet account and API security settings.•Contact Merchant Services Team and get help.3. MASS PAYMENTSThe Mass Payment service enables you to make payments from your Skrill account to multiple recipients. The Mass Payments service should be enabled on your account before using this feature. Once the feature is enabled, you can see the Mass Payment button from the Home page > Quick Links or from Transfers > Mass Payments . To use the Mass Payments service, a payment file must be created with the details of recipients.Figure 3-1: Quick LinksSkrill Merchant Portal supports the following pay-out options:1. Pay-outs using the Mass Payments option with a payments file. You can send as many varyingamounts as required to hundreds of payment recipients at a time in a choice of 40 currencies (no integration is required). This method supports a maximum of 3000 payments per batch.2. Using a HTTPS API Request (standalone credits) - Automate your mass payments with Skrill.This advanced option, via an API interface, supports unlimited payments in varying amounts and different currencies. (Integration required). See the Automated Payments Interface guide for more details. 3.1 PrerequisitesBefore using the mass payment feature in the Skrill Merchant Portal, you should ensure you have an application that can create worksheets in Microsoft Excel or CSV format.Read through the following payment file restrictions if you encounter any errors in the mass payment process.o If the number of records in the payment file exceeds 3000 or if the file’s size exceeds 5MB, then the file will not be processed, and an error is displayed.o If you attempt to upload a file with the same name as a previous file uploaded inthis account, it will be rejected as a duplicate.o A new line character must replace row data.o Each item in a row can be separated from the previous item using a tab, comma, or semi‐colon cha racter. No other delimiters are allowed.o If you choose a payment currency that is different from the currency used by your Skrill account, then an exchange conversion fee will apply. Each merchant can seethe FX fee applicable for their account in the Fee Schedule they had signed duringthe onboarding process. For example, if you have a GBP Skrill account and thepayment is sent in EUR, the currency conversion fee will be applicable in your case.3.2Mass Payments using a Payment FileYou can create a payment file containing details of all the recipients you want to pay.To prepare a Mass Payment file:e an application like Microsoft Excel and create a blank worksheet.2.Save the file as comma-separated values CSV file (.csv).3.Add the details of the payment’s recipients in the following format. The file must contain thefollowing columns:Table 3-1: Mass Payment FieldsFollowing is an example of the payment file. Note the commas separating records as the file is saved in comma separated format (CSV).Figure 3-2: Example of a CSV file3.2.1Uploading the payment fileAfter you have prepared the mass payment file, upload the file using Mass Payments option:1.Login to your Skrill account.2.Click the Mass Payment option from the Quick Links menu. You can optionally add a message tothe payments/transactions by selecting the Message option. This message will be displayed in the email the recipients receive.3.Select a Currency Account.4.Click Browse and select the CSV or text file or drag the same file into the Drag and Drop/browsethe file here field and drop it.Table 3-2: Mass payment ‐ choose file and enter details.5.Click Next. Once the payment file is uploaded, you can see the list of recipient details on thescreen. The screen provides a preview of both valid transactions and transactions with errors. It also includes the total amount to be sent from your account and the total fees (calculated in thecurrency of your Digital Wallet account). Each merchant can see the FX fee applicable for their account in the fee schedule they have signed during the onboarding process.Figure 3-3: Mass payments transfer details.6.From the From Account list, select the currency account.Figure 3-4: From Account drop-down list•Check if the payment details are correct. To make changes click Cancel and update the CSV file and upload again.•If there are any errors in the payment file, the Mass Payment module does not allow you to proceed further.•If there are insufficient funds in the wallet, then you can proceed further. Select a wallet with sufficient funds.7.Click Confirm & Process. Once the file is processed, the Receipt page appears.•The Receipt page shows a whole list of transactions and a status for each transaction;for information about the different status values (See Table 3-3: List of PaymentTransaction Status Values below for information about the different status values).•If you get any errors during the mass payments procedure, see Mass Payment Error Scenarios section for more information.3.3Mass Payment – Transaction Statuses3.4Mass Payment Error Scenarios3.5Transfer with an API Request (Standalone Credits)You can also make mass payments using the Skrill Automated Payments Interface (API). It enables you to automate the sending of payment details from your servers to Skrill using an HTTPS request. See the Automated Payments Interface guide for more information.4.APPENDICES4.1ISO 4217 currenciesTable 3‐2: ISO 4217 Currencies accepted by Skrill4.2Languages supported by SkrillSkrill supports the following languages (2-character ISO codes):4.3ISO country codes (3-digit)Skrill does not accept customers from the following countries: Afghanistan, Cuba, Eritrea, Iran, Iraq, Japan, Kyrgyzstan, Libya, North Korea, Sudan, South Sudan, and Syria.5.GLOSSARYThis section provides a description of some key terms used in this guide.。

移动支付系统操作手册

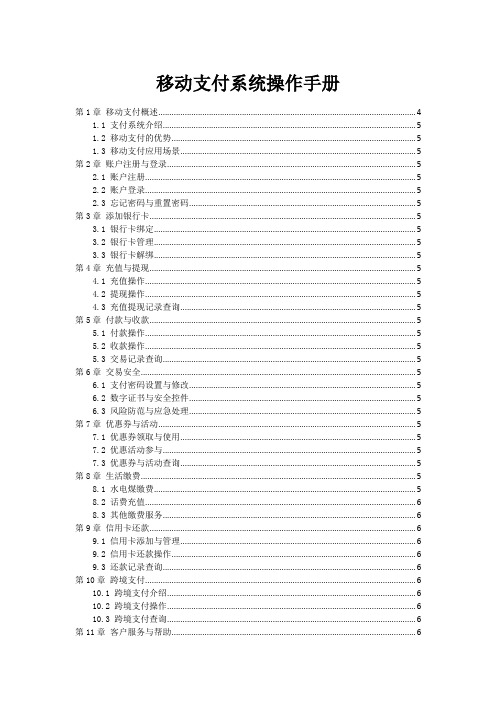

移动支付系统操作手册第1章移动支付概述 (4)1.1 支付系统介绍 (5)1.2 移动支付的优势 (5)1.3 移动支付应用场景 (5)第2章账户注册与登录 (5)2.1 账户注册 (5)2.2 账户登录 (5)2.3 忘记密码与重置密码 (5)第3章添加银行卡 (5)3.1 银行卡绑定 (5)3.2 银行卡管理 (5)3.3 银行卡解绑 (5)第4章充值与提现 (5)4.1 充值操作 (5)4.2 提现操作 (5)4.3 充值提现记录查询 (5)第5章付款与收款 (5)5.1 付款操作 (5)5.2 收款操作 (5)5.3 交易记录查询 (5)第6章交易安全 (5)6.1 支付密码设置与修改 (5)6.2 数字证书与安全控件 (5)6.3 风险防范与应急处理 (5)第7章优惠券与活动 (5)7.1 优惠券领取与使用 (5)7.2 优惠活动参与 (5)7.3 优惠券与活动查询 (5)第8章生活缴费 (5)8.1 水电煤缴费 (5)8.2 话费充值 (6)8.3 其他缴费服务 (6)第9章信用卡还款 (6)9.1 信用卡添加与管理 (6)9.2 信用卡还款操作 (6)9.3 还款记录查询 (6)第10章跨境支付 (6)10.1 跨境支付介绍 (6)10.2 跨境支付操作 (6)10.3 跨境支付查询 (6)第11章客户服务与帮助 (6)11.2 常见问题解答 (6)11.3 意见反馈与投诉 (6)第12章关于我们 (6)12.1 应用介绍 (6)12.2 用户协议与隐私政策 (6)12.3 版本更新与联系方式 (6)第1章移动支付概述 (6)1.1 支付系统介绍 (6)1.2 移动支付的优势 (6)1.3 移动支付应用场景 (7)第2章账户注册与登录 (7)2.1 账户注册 (7)2.2 账户登录 (8)2.3 忘记密码与重置密码 (8)第3章添加银行卡 (9)3.1 银行卡绑定 (9)3.1.1 登录账户 (9)3.1.2 进入绑定页面 (9)3.1.3 填写信息 (9)3.1.4 提交绑定 (9)3.2 银行卡管理 (9)3.2.1 查看银行卡信息 (9)3.2.2 设置默认支付卡 (10)3.2.3 解绑银行卡 (10)3.3 银行卡解绑 (10)3.3.1 确认解绑 (10)3.3.2 输入验证码 (10)3.3.3 解绑成功 (10)第4章充值与提现 (10)4.1 充值操作 (10)4.1.1 登录账户 (10)4.1.2 选择充值方式 (10)4.1.3 输入充值金额 (10)4.1.4 确认充值信息 (10)4.1.5 充值成功 (10)4.2 提现操作 (11)4.2.1 登录账户 (11)4.2.2 选择提现方式 (11)4.2.3 输入提现金额 (11)4.2.4 确认提现信息 (11)4.2.5 提现审核 (11)4.2.6 提现成功 (11)4.3 充值提现记录查询 (11)4.3.2 查看充值记录 (11)4.3.3 查看提现记录 (11)4.3.4 查询条件筛选 (11)第5章付款与收款 (11)5.1 付款操作 (12)5.2 收款操作 (12)5.3 交易记录查询 (12)第6章交易安全 (13)6.1 支付密码设置与修改 (13)6.1.1 设置强密码 (13)6.1.2 修改支付密码 (13)6.2 数字证书与安全控件 (13)6.2.1 数字证书 (13)6.2.2 安全控件 (14)6.3 风险防范与应急处理 (14)6.3.1 风险防范 (14)6.3.2 应急处理 (14)第7章优惠券与活动 (14)7.1 优惠券领取与使用 (14)7.1.1 领取优惠券 (15)7.1.2 使用优惠券 (15)7.2 优惠活动参与 (15)7.2.1 查看优惠活动 (15)7.2.2 参与优惠活动 (15)7.3 优惠券与活动查询 (15)7.3.1 优惠券查询 (15)7.3.2 活动查询 (15)第8章生活缴费 (16)8.1 水电煤缴费 (16)8.1.1 线上缴费 (16)8.1.2 线下缴费 (16)8.1.3 自动扣费 (16)8.2 话费充值 (16)8.2.1 线上充值 (16)8.2.2 线下充值 (16)8.2.3 自动充值 (16)8.3 其他缴费服务 (16)8.3.1 物业费 (16)8.3.2 停车费 (17)8.3.3 学费 (17)8.3.4 信用卡还款 (17)第9章信用卡还款 (17)9.1 信用卡添加与管理 (17)9.1.2 管理信用卡 (17)9.2 信用卡还款操作 (17)9.2.1 绑定储蓄卡自动扣款 (17)9.2.2 网银转账还款 (18)9.2.3 手机银行还款 (18)9.2.4 还款 (18)9.2.5 还款 (18)9.3 还款记录查询 (18)第10章跨境支付 (18)10.1 跨境支付介绍 (18)10.1.1 定义与类型 (19)10.1.2 重要性 (19)10.2 跨境支付操作 (19)10.2.1 支付发起 (19)10.2.2 支付处理 (19)10.2.3 支付清算 (19)10.2.4 结算 (19)10.3 跨境支付查询 (20)10.3.1 支付发起人查询 (20)10.3.2 收款人查询 (20)第11章客户服务与帮助 (20)11.1 在线客服咨询 (20)11.1.1 在线客服工作时间 (20)11.1.2 在线客服渠道 (20)11.1.3 在线客服服务范围 (20)11.2 常见问题解答 (21)11.2.1 如何注册账号? (21)11.2.2 如何修改个人信息? (21)11.2.3 如何查看订单状态? (21)11.2.4 退货和换货的条件是什么? (21)11.3 意见反馈与投诉 (21)11.3.1 意见反馈 (21)11.3.2 投诉渠道 (21)第12章关于我们 (21)12.1 应用介绍 (21)12.2 用户协议与隐私政策 (22)12.3 版本更新与联系方式 (22)好的,以下是一份移动支付系统操作手册的目录:第1章移动支付概述1.1 支付系统介绍1.2 移动支付的优势1.3 移动支付应用场景第2章账户注册与登录2.1 账户注册2.2 账户登录2.3 忘记密码与重置密码第3章添加银行卡3.1 银行卡绑定3.2 银行卡管理3.3 银行卡解绑第4章充值与提现4.1 充值操作4.2 提现操作4.3 充值提现记录查询第5章付款与收款5.1 付款操作5.2 收款操作5.3 交易记录查询第6章交易安全6.1 支付密码设置与修改6.2 数字证书与安全控件6.3 风险防范与应急处理第7章优惠券与活动7.1 优惠券领取与使用7.2 优惠活动参与7.3 优惠券与活动查询第8章生活缴费8.1 水电煤缴费8.2 话费充值8.3 其他缴费服务第9章信用卡还款9.1 信用卡添加与管理9.2 信用卡还款操作9.3 还款记录查询第10章跨境支付10.1 跨境支付介绍10.2 跨境支付操作10.3 跨境支付查询第11章客户服务与帮助11.1 在线客服咨询11.2 常见问题解答11.3 意见反馈与投诉第12章关于我们12.1 应用介绍12.2 用户协议与隐私政策12.3 版本更新与联系方式第1章移动支付概述1.1 支付系统介绍互联网和电子商务的快速发展,支付系统在人们日常生活中扮演着越来越重要的角色。

商家维护工作手册

文档编号 siro-dxsyb-20070810-V1.0-05签约商家维护工作手册编写 冯保龙校对 ____________________ 审核 ____________________ 编写部门 电信114增值部版本历史记录口口2007 年_08_ 月 _10_ 日______ 年 ____ 月 ____ 日2007年 ____ 月 _____ 日电话:0571 8885 7555 传真:0571 8885 7555 分机8801刍l「・」IMFCiRMATK.,目录一、制定本手册目的: (3)二、维护方法描述:(CRM ) (3)三、具体工作标准: (3)四、对业务人员的维护工作考核; (6)口口51 氏匚I URF口RfM凫HON商家维护工作手册电信114增值部一、制定本手册目的:1、制定维护工作的具体工作内容,指导办事处工作;2、确保商家服务能按照合同规定的承诺执行,保障百事通卡消费体系顺利运作;3、明确工作职责,便于业务考核;4、形成知识手册,便于推广使用;二、维护方法描述:(CRM)1、签约商家资料整理,商家的资料包括但不局限于合同信息,具体信息格式见《商家登记表》;2、商家质量、实力评估,通过商家质量评估及合作配合度等指标,形成重点商家名单,详细评估报表见XXX ;这些商家将成为维护工作的重点。

3、商家店头布展工作,包括桌牌、宣传海报、展架、横幅等,在商家收银台或餐桌或前厅等明显地方做好宣传布置,便于消费者感知;4、电话维护,通过杭州电话信息小组,对各项目新签或原商家作电话回访,达到提升商家感知目的;5、策划营销活动,整合电信、思创、市场、商家资源,针对前向用户或后向商家策划阶段性的营销活动,提升用户与商家的感知,推广百事通卡消费体系品牌价值;6、前向持卡用户激活,只有不断有持卡用户到商家处消费,才能保障该系统能顺利运行;因此后期维护工作中,对前向持卡用户的维护与激活变的非常重要;三、具体工作标准:商家资料,资料表格必须包含以下指标:(其他指标可以再增加)口口商家评估分2个指标,1个是商家硬件实力,1个是商家对合作的态度,硬件实力占60分,备注:根据评判指标,重点合作商家是各办事处重点维护的商家,办事处维护的80%精力要放在这些商家身上;商家店头布展工作:主要工作是将桌牌(宣传海报、展架、横幅)等有形的宣传物品放置在商家营业范围内,口口所有签约商家必须放置桌牌等物品;新签商家,在签约的当月必须放置以上布展物品;电信交给的商家或其他渠道合作商家,要求在交接名单的30天内必须放置以上物品;如果桌牌等物品更新,重点商家必须要求在30天内作相应更新,普通商家可以不做更新;杭州电话回访与维护;各项目的商家电话回访工作均由杭州电话中心执行,对商家的回访功能主要分2块;1、作为新签约商家的回访确认:签约后7个工作日内必须执行;目的:一是作为项目签约工作的过程监督方法,二是提高商家的品牌感知;2、作为签约商家的正常维护方法之一;要求:a、签约次月底前,所有商家必须作回访;b、对于普通商家,次月底全部正常维护回访后,以后每个3个月全部维护回访一次;c、对于重点商家,每月底均要求回访一次;3、回访脚本:略,4、回访数据分析:由信息中心负责,分6种情况:5、杭州无效率必须控制在30%以下,其他地方必须控制在20%以下;第2、6种情况判断无效,第3、5种情况50%判断无效;如出现电话不通情况,必须拨打2次以上;拨测报告提交给各项目负责人;6、办事处各项目负责人员必须对第2、3、4、5、6种情况作出处理,并将意见在次月通报给部门经理及信息中心;营销策划营销策划的目的是整合电信、思创、市场、商家的营销资源,提高商家、用户的感知,提升百事通卡品牌价值。

大小额支付系统操作手册(第一版)

一、 普通贷记.........................................................................................................10 (一)基本规定 ............................................................................................................. 10 (二)业务操作 ............................................................................................................. 10 二、 来账信息打印.................................................................................................15 (一)业务操作 ............................................................................................................. 15 三、 退汇.................................................................................................................16 (一)业务操作 ............................................................................................................. 16 四、 来账挂账手工处理.........................................................................................17 (一)业务操作 ............................................................................................................. 17 五、 来账未入账手工入账.....................................................................................20 (一)业务操作 ............................................................................................................. 20 六、 手工补账.........................................................................................................22 (一)业务操作 ............................................................................................................. 22 七、 事务信息打印.................................................................................................24 (一)业务操作 ............................................................................................................. 24 八、 查询.................................................................................................................24 (一)基本规定 ............................................................................................................. 25 (一)业务操作 ............................................................................................................. 25 九、 查复.................................................................................................................25 (一)基本规定 ............................................................................................................. 26 (二)业务操作 ............................................................................................................. 26 十、 银行承兑汇票查询.........................................................................................27 (一)业务操作 ............................................................................................................. 27 十一、 自由格式报文.................................................................................................28 (一)基本规定 ............................................................................................................. 28 (一)业务操作 ............................................................................................................. 28 第四节小额支付系统业务 ..................................................................................................... 29 一、 普通贷记.........................................................................................................29 (一)基本规定 ............................................................................................................. 29 二、 来账信息打印.................................................................................................33 (一)业务操作 ............................................................................................................. 33 三、 退汇.................................................................................................................34 (一)业务操作 ............................................................................................................. 34 四、 来账挂账手工处理.........................................................................................35

POS机保养和简易维护方法最新

POS机保养和简易维护方法最新

POS机是一种常见的商业设备,用于处理支付交易和管理商店销售。

为了保证POS机的正常运行和延长其使用寿命,以下是一些常见的POS机保养和简易维护方法:

1. 定期清洁:使用干净的软布轻轻擦拭POS机的外壳和触摸屏,以去除灰尘和污渍。

避免使用带有酒精或强烈化学成分的清洁剂,以免损坏设备表面。

2. 定期清理磁卡读卡器:使用专用的磁卡读卡器清洁卡片,将其插入和拔出几次,以清除读卡器内的灰尘和污渍。

3. 保持通风畅通:确保POS机周围没有杂物堆积,以确保良好的通风,防止过热。

4. 避免液体接触:尽量避免将液体食物或饮料溅到POS机上,以免进入设备内部造成损坏。

5. 注意电源连接:确保POS机的电源连接稳定,并在不使用时及时关闭电源。

6. 定期更新软件:根据POS机供应商的建议和指导,定期更新POS机的软件和驱动程序,以确保系统的安全性和稳定性。

7. 定期备份数据:定期备份POS机中的数据,以防止数据丢失或意外损坏。

8. 定期检查硬件:定期检查POS机的硬件部件,如打印机、键盘和显示屏,确保它们正常工作并及时更换损坏的部件。

请注意,以上方法只是一般性的保养和维护建议,具体的操作方法可能会因不同的POS机型号和品牌而有所不同。

因此,请在进行任何维护之前,确保查阅POS机的用户手册或咨询供应商或设备维修专业人员的建议和指导。

mbfe支付系统操作培训12

6、假设MBFE旗县联社端网络出现异 常情况,无法登陆时,应及时通知科技 人员处理。假设在半小时内无法解决, 及时与自治区联社科技中心相关人员及 清算中心业务主管取得联系。

第四局部:系统操作流程系来自状态查询◆ 系统状态查询 :在工作日当中前置机 将自动接收上级节点下发的系统状态变 更通知,并根据通知内容更新本身系统 状态,前置机系统所有用户均可随时查 询变更类型及变更时间。 ◆ 操作人员:业务主管、系统管理员、 操作员

第一局部:前置机系统介绍

前置机系统概念

前置机系统是出于本行行内系统和外界系统 的中间设备,当两个系统之间相互传递信息时, 将由它负责完成信息格式的转换和收发工作。

第一局部:前置机系统介绍

MBFE前置机系统介绍

◆MBFE前置机系统在自治区联社及各旗 县联社均设置客户端,用于对全区及辖 内机构支付业务监控及相关业务处理。 ◆自治区联社支付系统采用直联方式集 中接入中国现代化支付系统,自治区联 社属于中国现代化支付系统的直接参与 者;各旗县联社属于现代化支付系统的 间接参与者。

止口

存在排队队 列或存在透 支清算账户

定

清 算 窗 口 关 闭

关 闭 清 算 窗 口

切 换 工 作 日

日间业务处理

清算窗口处理

日终业务处理

营业前准备

第二局部:系统运行根本规定

小额支付系统运行时序

16:00

24小时连续运行 逐笔发起 组包发送 实时传输, 双边轧差 定时清算

第二局部:系统运行根本规定

◆附言内容用于对本次系统状态变更进行说明,可将光标定位于变更记录上以观察相应附言。

第四局部:系统操作流程

大额业务授权

◆大额业务授权:为加强对大额业务 的控制,针对全区农村信用社发起的 支付业务设置“授权金额〞参数 〔100万元〕。在日常业务处理过程 中,如录入的支付业务金额高于或等 于此参数,那么在复核完成后还需由 MBFE旗县联社端业务主管授权前方 可发送至上级节点。

百富POS操作手册

羊城通3代充值业务百富POS操作手册VER 1.0.0目录修改记录 (3)1 概述 (4)2 连线说明 ....................................................................................................................................错误!未定义书签。

3 交易流程说明 (4)3.1 柜员签到 (5)3.2 消费 ....................................................................................................................错误!未定义书签。

3.3 结算 (12)3.4 充值 (6)3.5 售卡 ....................................................................................................................错误!未定义书签。

3.6 查询卡片余额 ....................................................................................................错误!未定义书签。

3.7 查询卡片交易记录 ............................................................................................错误!未定义书签。

3.8 打印上一笔交易 (25)3.9 打印任意一笔交易 ............................................................................................错误!未定义书签。

电子支付系统建设与运营维护手册

电子支付系统建设与运营维护手册第1章电子支付系统概述 (3)1.1 支付系统的基本概念 (3)1.2 电子支付系统的分类与功能 (4)1.3 国内外电子支付系统发展现状 (4)第2章电子支付系统建设规划 (5)2.1 建设目标与原则 (5)2.1.1 建设目标 (5)2.1.2 建设原则 (5)2.2 系统架构设计 (5)2.2.1 总体架构 (5)2.2.2 模块划分 (5)2.3 技术选型与标准规范 (6)2.3.1 技术选型 (6)2.3.2 标准规范 (6)第3章电子支付系统核心模块设计 (6)3.1 用户模块设计 (6)3.1.1 用户注册与登录 (6)3.1.2 用户信息管理 (6)3.1.3 用户权限管理 (7)3.1.4 用户反馈与投诉 (7)3.2 安全认证模块设计 (7)3.2.1 密码安全 (7)3.2.2 交易验证 (7)3.2.3 数字证书 (7)3.2.4 防火墙与入侵检测 (7)3.3 支付交易模块设计 (7)3.3.1 支付渠道接入 (7)3.3.2 交易处理 (7)3.3.3 资金清算 (7)3.3.4 交易风险控制 (7)3.3.5 交易查询与对账 (8)第4章电子支付系统基础设施建设 (8)4.1 硬件设备选型与部署 (8)4.1.1 服务器选型 (8)4.1.2 存储设备选型 (8)4.1.3 网络设备选型 (8)4.1.4 设备部署 (8)4.2 软件环境搭建与优化 (9)4.2.1 操作系统选型与配置 (9)4.2.2 数据库选型与优化 (9)4.2.3 中间件部署与优化 (9)4.3.1 防火墙配置 (9)4.3.2 入侵检测与防护 (9)4.3.3 数据加密与传输安全 (9)4.3.4 安全审计与合规 (10)第5章电子支付系统关键技术 (10)5.1 加密技术 (10)5.1.1 对称加密算法 (10)5.1.2 非对称加密算法 (10)5.1.3 混合加密算法 (10)5.2 安全认证技术 (10)5.2.1 数字签名技术 (10)5.2.2 身份认证技术 (10)5.2.3 CA认证 (10)5.3 数据处理与分析技术 (10)5.3.1 数据加密存储 (10)5.3.2 数据脱敏技术 (11)5.3.3 数据挖掘与分析 (11)5.3.4 大数据分析 (11)第6章电子支付系统运营管理 (11)6.1 运营组织架构 (11)6.1.1 运营管理部门设置 (11)6.1.2 岗位职责 (11)6.1.3 人员培训与考核 (11)6.2 用户服务与管理 (11)6.2.1 用户服务 (11)6.2.2 用户培训与宣传 (12)6.2.3 用户反馈与优化 (12)6.3 风险管理与合规性 (12)6.3.1 风险识别与评估 (12)6.3.2 风险防范与控制 (12)6.3.3 合规性检查与整改 (12)6.3.4 应急预案与演练 (12)第7章电子支付系统风险防范 (12)7.1 风险识别与评估 (12)7.1.1 系统安全风险 (12)7.1.2 用户行为风险 (12)7.1.3 法律合规风险 (13)7.1.4 业务风险 (13)7.2 风险防范策略与措施 (13)7.2.1 系统安全风险防范 (13)7.2.2 用户行为风险防范 (13)7.2.3 法律合规风险防范 (13)7.2.4 业务风险防范 (13)7.3.1 事件报告:发觉安全事件后,第一时间向相关负责人报告,保证及时响应。

e+Pay Payment Alliance 支付拍檔 用戶指南说明书

「e+Pay Payment Alliance 支付拍檔」(“ePA”)User Guide用戶指南Last revision date修訂日期:10/11/2022Version 版本:v1.4目錄Overview概述 (2)Introduction 簡介 (2)Log in 登入 (3)Logout登出 (3)Forgot password 忘記密碼 (4)Change language 更改語言 (5)Transaction Summary主頁–交易總匯 (6)Transaction Summary 交易總匯 (7)Merchant Management 商戶管理 (8)Merchant Information 商戶資料 (8)Payment service 支付服務 (10)Store Information 分店資料 (12)Transaction management 交易管理 (14)Real-time transaction 實時交易查詢 (14)Reconciliation 結算報告 (16)Fund Settlement 打款報告 (19)Account Management 帳戶管理 (22)Account status 帳戶狀態 (22)Overview概述This user guide introduces the operation method of electronic payment management platform, “e+Pay Payment Alliance” (ePA) provided by eft Payments (Asia) Limited.本「用戶指南」介紹易付達(亞洲)有限公司提供的電子支付管理平台「e+Pay 支付拍檔」(“ePA”)的操作方法。

Introduction 簡介“e+Pay Payment Alliance” (ePA) is an electronic payment management platform providing comprehensive functions for merchants to review and manage transaction records, receive the latest electronic payment service information and help merchants to manage related services effectively.e+Pay 支付拍檔(ePA)是一個電子支付商戶管理平台,為商戶提供的一站式查閱交易記錄及管理交易的功能,並可收取最新的電子支付服務資訊,幫助商戶更有效管理相關服務。

小商户安全支付指南说明书

Data Security Essentials for Small Merchants: Guide to Safe PaymentsCopyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.This Guide to Safe Payments is provided by the PCI Security Standards Council (PCI SSC) to inform and educate merchants and other entities involved in payment card processing. For more information about the PCI SSC and the standards we manage, please visit .The intent of this document is to provide supplemental information, which does not replace or supersede PCI Standards or their supporting documents.UNDERSTANDINGYOUR RISKCOST TO UK BUSINESS DUE TO CYBER SECURITY BREACHES IN 2016(Beaming UK)OF SMALL BUSINESSES HAVE BEEN BREACHED IN THE PAST 12 MONTHS.(Ponemon Institute)50%£30 billion5Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.A PAYMENT SYSTEM includes the entire process for accepting card payments. Also called the cardholder data environment (CDE), your payment system may include a payment terminal, an electronic cash register, other devices or systems connected to a payment terminal (for example, Wi-Fi for connectivity or a PC used for inventory), and the connections out to a merchant bank. It is important to use only secure payment terminals and solutions to support your payment system. See page 21 for more information.A PAYMENT TERMINAL is the device used to take customer card payments via swipe, dip, insert, tap, or manual entry of the card number. Point-of-sale (or POS) terminal, credit card machine, PDQ terminal, or EMV/chip-enabled terminal are also names used to describe thesedevices.ENCRYPTION (or cryptography) makes card data unreadable to people without special information (called a key). Cryptography can be used on stored data and data transmitted over a network. Payment terminals that are part of a PCI-listed P2PE solution provide merchants the best assurance about the quality of the encryption. With a PCI-listed P2PE solution, card data is always entered directly into a PCI-approved payment terminal with something called “secure reading and exchange of data (SRED)” enabled. This approach minimizes risk to clear-text card data and protects merchants against payment-terminal exploits such as “memory scraping” malware. Any encryption that is not done within a PCI-listed P2PE should be discussed with your vendor.Accepting face-to-face card payments from your customers requires special equipment. Depending on where in the world you are located, equipment used to take payments is called by different names. Here are the types we reference in this document and what they are commonly called.A MERCHANT BANK is a bank or financial institution that processes credit and/or debit card payments on behalf of merchants. Acquirer, acquiring bank, and card or payment processor are also terms for this entity.An INTEGRATED PAYMENT TERMINAL is a payment terminal and electronic cash register in one, meaning it takes payments, registers and calculates transactions, and prints receipts.An ELECTRONIC CASH REGISTER (or till) registers and calculates transactions, and may print out receipts, but it does not accept customer card payments. 6Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.An E-COMMERCE WEBSITE houses and presentsyour business website and shopping pages to yourcustomers. The website may be hosted and managed byyou or by a third party hosting provider.An E-COMMERCE PAYMENT SYSTEM encompasses the entireprocess for a customer to select products or services and forthe e-commerce merchant to accept card payments, including awebsite with shopping pages and a payment page or form, otherconnected devices or systems (for example Wi-Fi or a PC used forinventory), and connections to the merchant bank (also called apayment service provider or payment gateway). Depending onthe merchant’s e-commerce payment scenario, an e-commercepayment system is either wholly outsourced to a third party,partially managed by the merchant with support from a third party,or managed exclusively by the merchant.When you sell products or services online, you are classified as a e-commerce merchant.Here are some common terms you may see or hear and what they mean.Your PAYMENT PAGE is the web page or form used tocollect your customer’s payment card data after theyhave decided to purchase your product or services.Handling of card data may be 1) managed exclusivelyby the merchant using a shopping cart or paymentapplication, 2) partially managed by the merchant withthe support of a third party using a variety of methods,or 3) wholly outsourced to a third party. Most times,Your SHOPPING PAGES are the web pages that showyour product or services to your customers, allowingthem to browse and select their purchase, and provideyou with their personal and delivery details. No paymentcard data is requested or captured on these pages.7Data Security Essentials for Small Merchants: Guide to Safe PaymentsCopyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.How is your business at risk?How do you sell your goods or services? There are three main ways:1. A person walks into your shop and makes a purchase with their card.2. A person visits your website and pays online.3. A person calls your shop and provides card details over the phone, or sends the details in the mail or via fax.The more features your payment system has, the more complex it is to secure.Think carefully about whether you really need extra features such as Wi-Fi, remote access software, Internet-connected cameras, or call recording systems for your business. If not properly configured and managed, each of these features can provide criminals with easy access to your customers’ payment card data.If you are an e-commerce merchant, it is very important to understand how or if payment data is captured on your website. In most cases, using a wholly outsourced third party to capture and process payments is the safest option.HARDER TO REDUCE RISK COMPLEX ENVIRONMENT EASIER TO REDUCE RISKSIMPLE ENVIRONMENT 8Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.recommended security tips as a starting point for conversations with your merchant bank and vendor partners.Your security risks vary greatly depending on the complexity of your payment system, whether face-to-face or online.TYPE 1Complex e-commerce payment system for online shop purchases, with merchant managing their own website and payment page 9Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.PROTECT YOUR BUSINESS WITH THESE SECURITY BASICSThese security basics are organized from easiest and least costly to implement to those that are more complex and costly to implement. The amount of risk reduction that each provides to small merchants is also indicated in the “Risk Mitigation” column.The good news is, you can start protecting your business today with these security basics:Use strong passwords and change defaultonesDon’t give hackers easy access to yoursystemsUse anti-virus softwareScan for vulnerabilitiesand fix issuesUse secure paymentterminals and solutionsProtect your business from the InternetFor the best protection, make your data uselessto criminalsProtect your card data and only store whatyou needInspect payment terminals for tamperingInstall patches fromyour vendorsUse trusted business partners and know how to contact themProtect in-house access to your card data 11Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.12Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.13Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.14Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.15Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.16Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.17Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.18Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.19Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.20Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.21Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.22Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.23Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.WHERE TO GET HELP25Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.ResourceURLInfographic: It’s Time to Change Your https:///pdfs/its_time_to_change_your_password_infographic.pdfhttps:///documents/Payment-Data-Security-Essential-Secure-Remote-Access.pdf PCI Data Security Essentials for Small Merchants and Related GuidanceResourceURL26Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.Dept for Culture Media and Sport – Cyber security breaches survey 2017Ponemon Institute – 2016 State of Cybersecurity in Small & Medium-Sized Businesses (SMB) (Sponsored by Keeper Security), June 2016National Cyber Security Centre – Cyber Security Small Business Guide, 2017Beaming UK – Cyber security breaches cost British Businesses almost £30 billion in 2016, March 2017Verizon 2017 – Verizon Data Breach Investigations Report27Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.28Data Security Essentials for Small Merchants: Guide to Safe Payments Copyright 2018 PCI Security Standards Council, LLC. All Rights Reserved.。

BEPS运行维护手册

Vbpa重要目录介绍$HOME/app二次路由交易源码目录$HOME/app/vbpa/synctran/src编译文件$HOME/app/vbpa/synctran/src/makefile三次路由交易源码目录$HOME/app/vbpa/asynctran/src编译文件$HOME/app/vbpa/synctran/src/obj.mak (生成.o文件)$HOME/app/vbpa/synctran/obj/lib.mak (生成.a文件)公共函数目录$HOME/app/vbpa/common建表工具目录$HOME/app/vbpa/crtdb建view的sql目录$HOME/app/vbpa/crtdb /crtview.sql小额系统头文件目录$HOME/app/vbpa/include小额应用系统公共头文件$HOME/app/vbpa/include/bminc/bmapp.h小额应用系统表头文件$HOME/app/vbpa/include/dbase.h$HOME/backup日终数据备份目录$HOME/backup/当日小额日期(格式:Y4MMDD) 备份文件应用数据库表备份文件APPDByyyymmdd.tar.Z平台数据库表备份文件DByyyymmdd.tar.Z被清理的历史数据备份文件HISCLEAR_yyyy-mm-dd.tar.Z当日小额交易日志备份文件LOGyyyymmdd.tar.Z小额系统日志目录MCP平台日志目录$HOME/cspsys/runtime/trace日志文件名T_交易数据集.log 记录本类数据集的交易日志Com_R_xx.log 记录本类静态路由的日志Routein_xxx.log 记录本sysrouterinp记录本Routeout_xxx.log 记录本sysrouteroutp记录本Cspsys.log 记录csp平台产生的日志MCP交易日志目录$HOME/log日志文件名构成机构码/t_柜员号.log日志文件构成生成日志的时间戮|源码行数|源码文件|交易码|响应码|日志内容交易数据集日志$HOME/runtime/trace日志文件名构成m机构码_柜员号.log小额系统执行码及其sh平台执行码目录$HOME/cspsys/runtime/exe应用执行码及其sh目录$HOME/runtime/exeShell脚本介绍bmbackup.sh 日终备份脚本bmclearhisdata.sh 日终历史数据清理脚本bmrcvfrombeps.sh 从BEPSMBFE上取文件bmrcvfromvbpi.sh 从VBPI上取文件bmsndtovbpi.sh 将文件放到VBPI上dirchk.sh 检查指定目录是否存在loadbankinf.sh 检查大额行号是否存在更新脚本conc.sh 将VOST生成的数据字典导入MCP相关表MCP常用表介绍表名bmacctdiff 详细说明小额支付对帐差错明细登记薄表名bmcntdayoff 详细说明小额支付业务日终统计表名bmenv 详细说明小额支付系统环境表(重要)表名bmpkgerr 详细说明小额支付包处理错误信息表表名bmprtlno 详细说明小额支付代扣业务多方协议号表名bmpubholi 详细说明小额支付公共假期表表名bmreceipt 详细说明小额支付包头/回执登记薄(重要)表名bmstopccpc 详细说明小额支付参与者行号表(重要)表名bmsusacct 详细说明小额支付来帐挂帐登记薄(重要)表名bmterm 详细说明小额支付定期批量业务登记薄(重要)表名bmtransfer 详细说明小额支付系统转帐业务登记薄(重要)表名bmtxctl 详细说明小额支付业务流程控制表表名bmtxsum 详细说明小额支付业务统计表表名pmbankinf 详细说明支付系统行名行号表(重要)表名pmbranmap 详细说明支付系统机构行号对照表(重要)表名pmupdown 详细说明支付系统机构上下级定义表表名vbpiserial 详细说明人行来帐报文流水表名autosendrec 详细说明定时定量发送配置表表结构请参照mcp中showtab 表名MCP中新增交易1.交易路由配置参见《小额支付Mcp应用安装配置》中5.32.在前台配好交易后用contr.sh 前台交易码同步到MCP开发平台中3.在MCP开发平台中用conc.sh 前台交易码MCP交易码将数据字典导入MCP相关表中4.在$HOME/cspsys/runtime/etc/trancoderef.cfg中加入前后台交易码转换定义5.如果是二次路由交易,在$HOME/app/vbpa/synctran/src加好相关交易,并在app/vbpa/synctran/src/tapivbpa.c中加入该交易的定义,在makefile文件中加入对该交易的编译策略;如果是三次路由交易,在$HOME/app/vbpa/asynctran/src加好相关交易,并在app/vbpa/asynctran/src/tapivbpa.c中加入该交易的定义,在obj.mak文件中加入对该交易的编译策略,并在app/vbpa/asynctran/obj/lib.mak中加入该交易的编译策略。

小额支付系统(MBFE)安装与维护手册

中国现代化支付系统小额支付系统(MBFE)安装与维护手册版本号:2.00中国人民银行二○○五年九月目录1.概述 (1)2.BEPSMBFE系统初装 (2)2.1.BEPSMBFE服务器端安装与配置 (2)2.1.1.安装前须知 (2)2.1.2.安装步骤 (2)2.1.3.配置文件说明 (8)2.1.4.环境变量说明 (12)2.1.5.其他注意事项 (12)2.1.6.BEPSMBFE安装程序包含的文件列表 (14)2.2.BEPSMBFE客户端安装与配置 (15)2.2.1.安装运行环境 (15)2.2.2.运行环境 (15)2.2.3.安装步骤 (15)2.2.4.环境配置说明 (21)2.3.BEPSMBFE数据库的创建与设置 (23)2.3.1.SYBASE客户端的登录 (23)2.3.2.BEPSMBFE数据库的创建过程 (23)2.4.BEPSMBFE数据初始化 (25)2.4.1.客户端登录 (27)2.4.2.新建用户............................................................................. 错误!未定义书签。

2.4.3.导入基础数据 (27)2.4.4.设置连接模式..................................................................... 错误!未定义书签。

3.系统启动 (29)4.系统关闭 (31)5.系统校时 (32)6.日常维护 (33)6.1.备份与恢复 (33)6.1.1.数据库备份 (33)6.1.2.恢复数据库 (34)6.1.3.业务数据备份 (35)6.2.双机热备的切换 (35)6.3.数据清理 (36)6.3.1.数据库日志定期清理 (36)6.3.2.临时数据清理 (37)MBFE安装维护手册1. 概述本系统维护手册是中国现代化支付系统商业银行前台(BEPSMBFE)系统管理员的维护手册。

BNSF EDI 820 支付订单 回款建议实施指南说明书

EDIELECTRONIC DATA INTERCHANGE820 PAYMENT ORDER /ADVICE REMITTANCEIMPLEMENTATION GUIDELINE__________________________________ USING ASC X12 TRANSACTION SET 820004010VERSION1999MAYBNSF EDI820 IMPLEMENTATION GUIDE__________________________________________________________________Table of ContentsIntroduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 Payment Order/Remittance Advice Processing . . . . . . . . . . . . . . . . . . 4 EDI Functional Acknowledgments . . . . . . . . . . . . . . . . . . . . . . . . . 4 The Transaction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 Segment ID Name . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 Data Element Type . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Data Element Requirement Designator . . . . . . . . . . . . . . . . . . . . . . 6 Data Element Length . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Sample 820 . . . (Waybill Number) . . . . . . . . . . . . . . . . . . . . . . . . . 7 Sample 820 . . . (Freight Bill Number) . . . . . . . . . . . . . . . . . . . . . . . 8 Segments and Data Elements:GS Functional Group Header . . . . . . . . . . . . . . . . . . . 9ST Transaction Set Header . . . . . . . . . . . . . . . . . . . . 11BPR Beginning Segment forPayment Order/Remittance Advice . . . . . . . . . 12 TRN Trace . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14REF Reference Identification . . . . . . . . . . . . . . . . . . . 15DTM Date/Time Reference . . . . . . . . . . . . . . . . . . . . . 16N1 Name . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17ENT Entity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Advice Accounts ReceivableRemittanceRMROpen Item . . . . . . . . . . . . . . . . . . . . . . . . 19 REF Reference Numbers . . . . . . . . . . . . . . . . . . . . . . 20DTM Date/Time Reference . . . . . . . . . . . . . . . . . . . . . 21SE Transaction Set Trailer . . . . . . . . . . . . . . . . . . . . 22GE Functional Group Trailer . . . . . . . . . . . . . . . . . . . 23BNSF EDI820 IMPLEMENTATION GUIDE__________________________________________________________________ IntroductionTransaction Set 820: Payment Order/Remittance AdviceThe 820 standard provides the format and establishes the data content of the PaymentOrder/Remittance advice transaction set within the context of an Electronic Data Interchange (EDI) environment. This transaction set is used to transmit remittance and/or payment information to a bank with instructions to begin funds transfer. The bank subsequently passes the funds transfer request to BNSF's bank along with the 820 detail. At settlement, the Railroad's bank passes the 820 to Burlington Northern Santa Fe Railroad.Using the ASC X12 820 transaction set to electronically transmit data between business partners allows for consistent interpretation of payment information and reduces the chances of interpretive and data entry errors.Burlington Northern Santa Fe will accept the Payment Order/Remittance Advice information published by DISA for ASC X12. The following guidelines are all-inclusive and identify unique accounting requirements for use of the ASC X12 820 transaction set when transmitting data to Burlington Northern Santa Fe.To obtain X12 standards and documentation, contact:Data Interchange Standards Association, Inc.1800 Diagonal Road, Suite 200Alexandria, VA 22314-2840703-548-7005orWashington Publishing Company800-972-4334Orders:301-590-9337Phone:__________________________________________________________________ Payment Order/Remittance Advice ProcessingThe general steps in processing 820s electronically are initiated when the customer enters or creates payment order/remittance advice in their computer. This information, or data, is then formatted into the ASC X12 820 transaction set. This formatting may be performed by you, the customer, or your agent. After formatting, the transaction is delivered to your bank. Your bank will initiate funds transfer and pass the 820 to BNSF's bank. Once funds have transferred, BNSF's bank will send the 820 detail. This detail will be used to perform cash application of the identified records to BNSF's accounts receivable system.EDI Functional AcknowledgmentsBNSF will generate a 997 Functional Acknowledgment to our bank in response to the 820 that is received. Depending on your bank's EDI capabilities, you may receive your bank's 997 when you deliver the 820 to them.__________________________________________________________________The TransactionA transaction set is used to describe the electronic transmission of a single document (Payment Order/Remittance Advice, Bill of Lading, etc.) between one company's computer and another company's computer.EDI transactions are defined by segments, and each item within the segment becomes a data element. Segment ID Name, Data Element Type, Requirement Designator, and Length are described below. These identifiers are listed for each Data Element throughout the remainder of this guide. Segment ID Name(Header)SetHeaderTransactionSTGroupHeaderFunctionGSBPR Beginning Segment for Payment Order/Remittance AdviceInstructionNTE Note/SpecialTRN TraceCUR CurrencyReferenceIdentificationREFReferenceDTMDate/TimeNameN1InformationNameAdditionalN2InformationN3AddressLocationGeographicN4Communications ContactPERAdministrativeMethoddeliveryRDMRemittance(Detail)EntityENTNM1 Individual or Organization NameIdentificationReferenceREFAdministrativeCommunications ContactPERReferenceDate/TimeDTMIT1 Baseline Item Data (Invoice)RMR Remittance Advice Accounts Receivable Open Item ReferenceInstructionNote/SpecialNTE(Summary)TrailerSetTransactionSE__________________________________________________________________ Data Element TypeSpecifies the characters that may be used.Nn Numeric N indicates that it is numeric; n indicates decimal place.R Decimal R indicates an optional decimal point for integer values ora required decimal for decimal values. BNSF can acceptpositive and decimal values. Do not send fractions orvalues.negativeID Identifier A specific code taken from a table defined in the DataElement Dictionary such as unit of measure.AN String A series of alpha/numeric characters, such as a company name.DT Date Date expressed as CCYYMMDDTM Time HHMM expressed in 24-hour clock format.Data Element Requirement DesignatorIndicates when this element must be included in an electronic document.M Mandatory The Data Element is required in the Segment.C Conditional The Data Element may be required in the Segment basedisused.elementwhetheronanotherO Optional The Data Element may or may not be used in the Segmentat the option of the user.Data Element LengthThe minimum length and maximum length of the characters in the data element.1/15 Indicates that "1" is the minimum acceptable value andmaximum.theis"15"BNSF EDI820 IMPLEMENTATION GUIDESample 820[SAMPLE: WAYBILL NUMBER IN RMR SEGMENT]GS*RA*CUSTID0001*BNSF*19990101*1530*9102*X*004010ST*820*000000001BPR*C*10000*C*ACH*CTX*01*1234*DA*555*CUSTID0001**01*987*DA*345123*19990101 TRN*1*1001983525REF*CD*1234564114REF*TN*1001983525 (Mandatory if TRN segment is not used)DTM*007*19990101N1*PE*BURLINGTON NORTHERN SANTA FEN1*PR*CUSTOMER NAMEENT*1RMR*WY*123456**2000REF*D0*RATE AUTHORITY*PER ITEM 12121 RATE SHOULD BE $2000 PER CARREF*BM*1001REF*EQ*BNSF456002DTM*095*19990101RMR*WY*999999**5000REF*BM*1002REF*EQ*BNSF458869DTM*095*19990101RMR*WY*999787**3000REF*BM*1003REF*EQ*BNSF458870DTM*095*19990101SE*23*0000000001GE*1*9102__________________________________________________________________ Sample 820[SAMPLE: FREIGHT BILL NUMBER IN RMR SEGMENT]GS*RA*CUSTID0001*BNSF*19990101*1530*9102*X*004010ST*820*000000001BPR*C*10000*C*ACH*CTX*01*1234*DA*555*CUSTID0001**01*987*DA*345123*19990101 TRN*1*1001983525REF*CD*1234564114REF*TN*1001983525 (Mandatory if TRN segment is not used)DTM*007*19990101N1*PE*BURLINGTON NORTHERN SANTA FEN1*PR*CUSTOMER NAMEENT*1RMR*FR*018923888**5000REF*BM*1003DTM*022*19990101RMR*FR*018923889**5000REF*BM*1004DTM*022*19990101SE*16*0000000001GE*1*9102[SAMPLE: FREIGHT BILL NUMBER IN RMR SEGMENT WITH DISPUTED PAYMENT] GS*RA*CUSTID0001*BNSF*19990101*1530*9102*X*004010ST*820*000000001BPR*C*9500*C*ACH*CTX*01*1234*DA*555*CUSTID0001**01*987*DA*345123*19990101 TRN*1*1001983525REF*CD*1234564114REF*TN*1001983525 (Mandatory if TRN segment is not used)DTM*007*19990101N1*PE*BURLINGTON NORTHERN SANTA FEN1*PR*CUSTOMER NAMEENT*1RMR*FR*018923888**4500REF*D0*OTHER*DIVERSION TO DENVERREF*BM*1003DTM*022*19990101RMR*FR*018923889**5000REF*BM*1004DTM*022*19990101SE*17*0000000001GE*1*9102__________________________________________________________________Segment : GS - Functional Group Header Loop : - Level : Functional Group Usage : Mandatory Max Use : 1 Max Length : - Purpose : To indicate the beginning of a functional group and to provide control information.Example :GS*RA*CUSTID0001*BNSF*19990101*1530*9102*X*004010SEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTSGS01 479 Functional ID Code2/2MIDCode identifying a group of application related transaction sets RA=Payment Order/Remittance Advice (820)GS02 142 ApplicationSender's Code 2/15 M AN Code identifying partysending transmission; codes agreed to by trading partnersGS03 124 ApplicationReceiver's Code2/15 M AN Code identifyingreceiving transmission; Codes agreed to by trading partners "BNSF"GS04 373 Date 8/8 M DT Date of transmission;expressed as YYYYMMDDGS05337Time4/8 M TM Time of transmission;expressed as HHMM; expressed in 24-hr clock time (00-23)GS Segment continued on next page__________________________________________________________________GS Segment ContinuedSEG DATAELEMENT NAME MIN-MAXREQ TYPE CONTENTSGS06 28Group ControlNumber 1/9 M N0Assignednumberoriginated &maintained by thesender. The number inthis header must beIdentical to the samedata element in theassociated functionalgroup trailer, GE02.GS07 455ResponsibleAgency Code1/2 M ID "X" only for ASC X12GS08 480Version/ReleaseIndustry IdentifierCode 1/12 M ANSender'stransmissionstandard version004010.__________________________________________________________________Segment : ST - Transaction Set Header Loop : -Level : Header Usage : Mandatory Max Use : 1 Max Length : 17 Purpose : To indicate the start of a transaction set and to assign a control number.Example : ST*820*000000001SEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTSST01143TS ID CODE3/3MID"820" Definition: Payment Order / Remittance AdviceST02 329 TS CONTROL NUMBER 4/9 M AN Sender's messagecontrol number__________________________________________________________________Segment : BPR - Beginning Segment for Payment Order/Remittance AdviceLoop : -Level : Header Usage : Mandatory Max Use : 1 Max Length : 245 Purpose : To indicate the beginning of a Payment Order/Remittance Advice Transaction Set and total payment amount, or to enable related transfer of funds and/or information from payer to payee to occurExample : BPR*C*10000*C*ACH*CTX*01*1234*DA*555* CUSTID0001**01*987*DA*345123*19990101 SEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTSBPR01 305 Transaction Handling Code 1/1 M ID C=Payment accompaniesremittance adviceBPR02 782 Monetary Amount 1/18 M R Total payment amount for allitemsBPR03 478 Credit/Debit Flag Code1/1 M ID C=CreditD=Debit BPR04 591 Payment Method Code 3/3 M ID Instruction to the origin bankon the method of pmt orderbeing transmitted.ACH=Automated Clearing HouseBPR05 812Payment Format Code 1/10 O ID1.CTX=Corporate Trade Exchange (CTX)(ACH)P=(CCD+)(ACH)Optional - helpful if usedBPR06 506 DFI ID Number Qualifier2/2 M ID01=ABA Transit Routing Number.BPR Segment Continued on next page__________________________________________________________________BPR Segment ContinuedSEG DATAELEMENT NAME MIN-MAXREQ TYPE CONTENTSBPR07507DFI ID Number3/12M AN Depository FinancialInstitution (DFI) ID Number.BPR08569Account NumberQualifier Code 1/3O ID Type of Account.DA=Demand DepositBPR09508Account Number1/35C AN Acct Number of Companyoriginating payment..If BPR08 is present, then BPR09is required.BPR10509OriginatingCompany ID 10/10O AN Unique identifier designatingthe company initiating thefunds transfer instructions.First character is one-digitANSI ID code followed by 9-digit ID NumberBPR11510OriginatingCompanySupplementalCode 9/9O AN Code defined between theOriginating Company &Originating DepositoryFinancial Institution thatidentifies the Companyinitiating the transfer.BPR12506DFI ID NumberQualifier 2/2M ID01=ABA Transit RoutingNumber.BPR13507DFI ID Number3/12M AN Depository FinancialInstitution (DFI) ID Number.BPR14569Account NumberQualifier Code 1/3O ID Type of Account.DA=Demand DepositIf BPR14 is present, then BPR15is required.BPR15508Account Number1/35C AN Payee's Account NumberBPR16373PaymentEffective Date 8/8M DT Date expressed asCCYYMMDD__________________________________________________________________Segment : TRN – TraceLoop : - Level : Header Usage : Mandatory Max Use : 1 Max Length : Purpose : To uniquely identify a transaction to an application. The Trace Number identifies the payment.Example : TRN*1*1001983525SEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTSTRN01 481 Trace Type Code 1/2 M ID 1=Current Transaction TraceNumbersTRN02 127 ReferenceNumber1/10MAN Trace Number (with nospaces or punctuation) -provides unique identification for the transactionTRN03 509 Originating Company ID10/10O AN Identifies an organizationTRN04 127 Reference Number1/30OAN Not used by BNSFNote: If Software does not provide for a TRN Segment, then REF01*TN and REF02 asindicated on following page is required.__________________________________________________________________ Segment :REF - Reference IdentificationLoop : -Level :HeaderUsage :Optional-May be required on certain BNSF ProgramsMaxUse :>1MaxLength:120Purpose : To specify identifying informationExample :REF*CD*1234564114SEG DATAELEMENT NAME MIN-MAXREQ TYPE CONTENTSREF01128 Ref ID Qualifier 2/3 M ID CD=BNSF Patron CodeCK=Check NumberTN=Trace NumberREF02 127 Reference ID 1/10 C AN As defined by the Ref IDQualifier.(Required if REF01 is used) REF03 352 Description 1/80 C AN Free form description Note: If TRN Segment is not used, then REF01 TN or CK is required.__________________________________________________________________ Segment :DTM - Date/Time ReferenceLoop : -Level :HeaderUsage :MandatoryMaxUse :>1MaxLength:69Purpose : To specify pertinent dates and timesExample :DTM*007*19990101SEG DATAELEMENT NAME MIN-MAXREQ TYPE CONTENTSDTM01 374 Date/TimeQualifier 3/3 M ID007=EffectiveDTM02 373 Date 8/8 C DTCCYYMMDD DTM03337Time 4/8 C TM HHMM, Time expressed in24-hr clock timeDTM04 623 TimeCode 2/2 O IDCT=CentralTimeET=Eastern TimeMT=Mountain TimePT=Pacific Time__________________________________________________________________Segment :N1 - Name Loop : N1 Repeat: >1 Level : Header Usage : Mandatory Max Use : >1 Max Length : 159 Purpose : To identify a party by type of organization, name and codeExample : N1*PR*CUSTOMER NAME N1*PE*BURLINGTON NORTHERN SANTA FESEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTSN101 98 Entity Identifier Code 2/3 M ID PE=PayeePR=PayerN102 93 Name 1/60 C AN Free Form Name (Required if N101 is used)N103 66 ID CodeQualifier1/2 C ID Not used by BNSF N104 67 ID Code 2/80C AN Not used by BNSF N105 706 EntityRelationship Code2/2 O ID Not used by BNSF N106 98 Entity ID Code2/3OID Not used by BNSFBNSF EDI820 IMPLEMENTATION GUIDE__________________________________________________________________Segment : ENT - EntityLoop : ENT Repeat: >1 Level : Detail Usage : Mandatory Max Use : 1 Max Length : 222 Purpose : To designate the entities which are parties to a transaction and specify a reference meaningful to those entitiesExample : ENT*1 SEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTSENT01 554 Assigned Number 1/6 O N0 Only ENT01 is necessarybecause there is a singleentity communicating with a single entity (sender to receiver)ENT02 98 Entity ID Code2/3C ID Not used by BNSF ENT03 66 ID CodeQualifier1/2 C ID Not used by BNSFENT04 67 ID Code 2/80 C AN Not used by BNSF ENT05 98 Entity ID Code 2/3 C ID Not used by BNSF ENT06 66 ID CodeQualifier1/2 C ID Not used by BNSF ENT07 67 ID Code 2/80 C AN Not used by BNSF ENT08 128 Ref ID Qualifier 2/3 C ID Not used by BNSF ENT09 127 Reference ID1/30CAN Not used by BNSF__________________________________________________________________Segment : RMR - Remittance Advice Accounts Receivable Open Item Loop : ENT/RMR Repeat: >1 Level : Detail Usage : Mandatory Max Use : 1 Max Length : 121 Purpose : To specify the accounts receivable open item(s) to be included in the cash application and to convey the appropriate detailExample : RMR*WY*123456**5000SEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTSRMR01 128 ReferenceIdentification Qualifier2/3 M ID WY=Waybill NumberBM=Bill of Lading Number FR=Freight Bill Number or Miscellaneous Bill Number(See Note Below)RMR02 127 Reference ID 1/30 CAN Reference information asdefined by the Reference ID Qualifier in RMR01 WY=123456RMR03 482 Payment Action Code 2/2OID PO=Payment on AccountSpecifies how the cash is to be appliedRMR04 782.00 MonetaryAmount1/18 M R Amount PaidNote:The preferred qualifier in RMR01 is WY or FR. If WY or FR is notavailable, then BM should be used. IF RMR*WY or RMR*BM is used, then REF*EQ is mandatory.DTM Segment is required in conjunction with RMR01*WY and RMR01*BM.__________________________________________________________________Segment : REF – Reference NumbersLoop : ENT/RMR Level : Detail Usage : Optional Max Use : >1 Max Length : 120 Purpose : To specify identifying informationExample : REF*BM*1001 REF*EQ*BNSF456002 REF*D0*RATE AUTHORITY*RATE SHOULD BE $2000 PER CARSEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTSREF01128 Reference Identification Qualifier 2/3 M ID WY=Waybill NumberBM=Bill of Lading Number EQ=Equipment NumberFR=Freight Bill Number or Miscellaneous Bill Number(See Note 1 Below)D0=Dispute Reason Code(See Note 2 Below)REF02 127 Reference ID 1/30 CAN Reference information asdefined by the Reference ID Qualifier in REF01 BM=1001IDs for D0 (Dispute Reason Code):Equipment Size Origin/Destination OtherRate Authority Service LevelThrough Rate vs Rule 11 WeightREF03 352 Description 1/60 CAN A free form description toclarify the related data elements & their contentNote 1. If Waybill Number or Bill of Lading Number or Freight Bill Number is used in the RMR Segment, then same Number is not needed in the REF Segment. If REF*WY or REF*BM is used, then REF*EQ is mandatory. Note 2. If payment is based on an amount that is different from the amount shown on BNSF’s Freight Bill, use an REF Segment with a D0 qualifier. The REF02 should be one of the Reference IDs listed under Contents. The REF03 is used to provide additional information related to the amount being paid.BNSF EDI820 IMPLEMENTATION GUIDE__________________________________________________________________Segment : DTM - Date/Time ReferenceLoop : ENT/RMR Level : Detail Usage : Optional Max Use : >1 Max Length : 69 Purpose : To specify pertinent dates and timesExample : DTM*095*19990101SEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTSDTM01 374. Date/TimeQualifier 3/3MID 095=Bill of Lading Date orWaybill Date 022=Freight Bill DateDTM02 373 Date8/8 C DT CCYYMMDD__________________________________________________________________Segment : SE - Transaction Set TrailerLoop : - Level : Summary Usage : Mandatory Max Use : 1 Max Length : 24 Purpose : To indicate the end of the transaction set and provide the count of the transmitted segments (including the beginning (ST) and ending (SE) segments) Comment : An (SE) is the last segment of each transaction setExample : SE*18*000000001SEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTS SE01 96 Number of included Segments 1/10MN0 Total number of Segmentsincluded in a transaction set including ST and SE SegmentsSE02 329 Transaction Set Control Number4/9MAN Transaction Set ControlNumber - must be identical to the Transaction Set Control Number in the ST Segment__________________________________________________________________Segment : GE - Functional Group TrailerLoop : - Level : Functional Group Usage : Mandatory Max Use : 1 Max Length : 24 Purpose : To indicate the end of a functional group and to provide control information.Example : GE*1*9102SEG DATA ELEMENT NAME MIN - MAXREQ TYPE CONTENTSGE01 97 Number of Transaction Sets Included 1/6MN0 Total number of transactionsets included in the functional group terminated by the trailer containing this data elementGE02 28 Group Control Number1/9MN0 Assigned number originated& maintained by the sender. This number must be identical to the same data element in the associated functional group header, GS06.。

A-005 佰付通收单系统架构设计说明书V1.0

佰付通收单系统系统架构设计说明书版本V1.0文档编号保密等级机密作者最后修改日期审核人最后审批日期批准人最后批准日期文档修订记录编号章节名称修订内容简述修订日期修订前版本号修订后版本号修订人批准人12345678备注说明:1、提交全文时,请作者自行检查正文文字的字体、大小、颜色和格式。

要求交付件文字为:宋体、五号、黑色、非斜体和非下划线。

目录1简介 (1)1.1目的 (1)1.2范围 (1)1.3术语定义 (1)2架构的目标和约束 (1)2.1架构的目标 (1)2.2架构的约束 (1)3系统架构图 (2)3.1总体架构图 (2)3.2逻辑架构图 (2)3.3部署架构图 (4)3.4其他 (4)4与关联系统架构设计 (6)5关键性技术设计机制 (6)6架构质量 (6)6.1安全设计 (6)6.1.1应用安全 (7)6.1.2网络安全 (7)6.1.3管理安全 (7)6.1.4其他 (7)6.2账务设计 (8)6.2.1批量业务 (8)6.2.2其他 (8)6.3运行设计 (8)6.3.1系统性能 (8)6.3.2可靠性 (9)6.3.3可维护性 (9)6.3.4可扩展性 (9)6.3.5可移植性 (9)6.3.6易用性 (9)6.3.7其他 (10)6.4开发高效性设计 (10)1简介1.1目的本概要设计说明定义了系统技术边界,描述了应用架构设计、技术架构设计和数据架构设计等,是后续详细设计、编码的基础依据,同时也作为确定与关联系统接口的规范文件。

1.2范围本文档覆盖了集中式收单业务系统的所有子功能,包括:POSP管理平台POSP联机交易功能POSP批量处理功能1.3术语定义2架构的目标和约束2.1架构的目标根据需求分析,介于整体架构的合理性、各系统间分工的明确和独立性,以及将来架构和业务的可拓展性等多方面考虑,架构目标如下:●统一的终端管理与渠道交易接入,提供完整的终端生命周期管理功能,屏蔽不同厂商终端带来的差异;●完善的商户管理功能,支持各类商户的静态数据、动态参数维护;●风险控制功能,提供对于收单系统所处理交易的事中和事后的风险控制和分析的能力;●统一清分清算,通过文件处理系统接收行内各系统提供的对账文件,进行清分清算处理,并生成各类清算业务报表;●完善的报表统计功能,提供详细的统计报表反映业务开展情况。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

百富便利支付维护手册

POS终端分三类操作员,系统管理员,主管管理员,一般操作员。

在签到界面,输入系统操作员号“99“,密码在env文件(主密码)中有设定,缺省”12345678“。

进入到系统管理

1、终端参数设置

商户号15位终端号8位商户中文名称20个汉字

2、通讯参数设置

GPRS 无线

CDMA 无线

PSTN 拨号IP

3、交易功能设置

屏蔽交易选项中,在便利支付中可以用的项是,手输卡号,选择是,在信用卡还款中,信用卡卡号可以手输而不用刷卡。

签退和小费比例,便利支付中暂时不用。

冲正重发次数,打印张数,最大交易笔数,根据需要调整。

4、终端密钥管理

主密钥索引

主密钥值

DES算法

5、修改密码

管理员密码,即系统管理员的密码。

安全密码,即修改重要参数时(比如修改商户号,终端号时),会要求输入的一个密码。

不属于任何一个操作员。

6、其他功能

清除交易流水,会清楚交易文件。

用于特殊情况。

轻易不要使用。

参数打印。

打印POS终端参数。

其他功能中,可以选择打印交易报文。

商户那里不会使用。

技术人员查找问题时使用。

在签到界面,输入主管操作员号“00“,密码缺省“123456”。

主管改密,修改主管操作员密码

增加操作员,增加一般操作员,最大可有11个,这个值由程序设定。

目前11个

查询操作员,查询当前有多少个操作员。

操作员编号为01,02,03,04等等

删除操作员,删除一般操作员

主管签退,退出主管操作界面。

进入到签到状态。

系统参数,输入系统管理员密码,进入到系统管理界面。