公司理财英文版题库

英文版罗斯公司理财习题答案

CHAPTER 8MAKING CAPITAL INVESTMENT DECISIONSAnswers to Concepts Review and Critical Thinking Questions1. In this context, an opportunity cost refers to the value of anasset or other input that will be used in a project. The relevant cost is what the asset or input is actually worth today, not, for example, what it cost to acquire.2. a.Yes, the reduction in the sales of the company’s otherproducts, referred to as erosion, and should be treated as an incremental cash flow. These lost sales are included because they are a cost (a revenue reduction) that the firm must bear if it chooses to produce the new product.b. Yes, expenditures on plant and equipment should be treatedas incremental cash flows. These are costs of the new product line. However, if these expenditures have already occurred, they are sunk costs and are not included as incremental cash flows.c. No, the research and development costs should not be treatedas incremental cash flows. The costs of research and development undertaken on the product during the past 3 years are sunk costs and should not be included in the evaluation of the project. Decisions made and costs incurred in the past cannot be changed. They should not affect the decision to accept or reject the project.d. Yes, the annual depreciation expense should be treated as anincremental cash flow. Depreciation expense must be taken into account when calculating the cash flows related to a given project. While depreciation is not a cash expense that directly affects c ash flow, it decreases a firm’s netincome and hence, lowers its tax bill for the year. Because of this depreciation tax shield, the firm has more cash on hand at the end of the year than it would have had without expensing depreciation.e.No, dividend payments should not be treated as incrementalcash flows. A firm’s decision to pay or not pay dividends is independent of the decision to accept or reject any given investment project. For this reason, it is not an incremental cash flow to a given project. Dividend policy is discussed in more detail in later chapters.f.Yes, the resale value of plant and equipment at the end of aproject’s life should be treated as an incremental cashflow. The price at which the firm sells the equipment is a cash inflow, and any difference between the book value ofthe equipment and its sale price will create gains or losses that result in either a tax credit or liability.g.Yes, salary and medical costs for production employees hiredfor a project should be treated as incremental cash flows.The salaries of all personnel connected to the project must be included as costs of that project.3.I tem I is a relevant cost because the opportunity to sell theland is lost if the new golf club is produced. Item II is also relevant because the firm must take into account the erosion of sales of existing products when a new product is introduced. If the firm produces the new club, the earnings from the existing clubs will decrease, effectively creating a cost that must be included in the decision. Item III is not relevant because the costs of Research and Development are sunk costs. Decisions made in the past cannot be changed. They are not relevant to the production of the new clubs.4. For tax purposes, a firm would choose MACRS because it providesfor larger depreciation deductions earlier. These larger deductions reduce taxes, but have no other cash consequences.Notice that the choice between MACRS and straight-line is purely a time value issue; the total depreciation is the same;only the timing differs.5.It’s probably only a mild over-simplification. Currentliabilities will all be paid, presumably. The cash portion of current assets will be retrieved. Some receivables won’t be collected, and some inventory will not be sold, of course.Counterbalancing these losses is the fact that inventory sold above cost (and not replaced at the end of the project’s life) acts to increase working capital. These effects tend to offset one another.6.Management’s discretion to set the firm’s capital structureis applicable at the firm level. Since any one particular project could be financed entirely with equity, another project could be financed with debt, and the firm’s overall capital structure remains unchanged, financing costs are not relevant in the analysis of a project’s incremental cash flows according to the stand-alone principle.7. The EAC approach is appropriate when comparing mutuallyexclusive projects with different lives that will be replaced when they wear out. This type of analysis is necessary so that the projects have a common life span over which they can be compared; in effect, each project is assumed to exist over an infinite horizon of N-year repeating projects. Assuming that this type of analysis is valid implies that the project cash flows remain the same forever, thus ignoring the possible effects of, among other things: (1) inflation, (2) changing economic conditions, (3) the increasing unreliability of cash flow estimates that occur far into the future, and (4) the possible effects of future technology improvement that could alter the project cash flows.8. Depreciation is a non-cash expense, but it is tax-deductible onthe income statement. Thus depreciation causes taxes paid, an actual cash outflow, to be reduced by an amount equal to the depreciation tax shield, t c D. A reduction in taxes that would otherwise be paid is the same thing as a cash inflow, so the effects of the depreciation tax shield must be added in to get the total incremental aftertax cash flows.9. There are two particularly important considerations. The firstis erosion. Will the “essentialized”book simply displace copies of the existing book that would have otherwise been sold?This is of special concern given the lower price. The second consideration is competition. Will other publishers step in and produce such a product? If so, then any erosion is much less relevant. A particular concern to book publishers (and producers of a variety of other product types) is that the publisher only makes money from the sale of new books. Thus, it is important to examine whether the new book would displace sales of used books (good from the publisher’s perspective) or new books (not good). The concern arises any time there is an active market for used product.10.D efinitely. The damage to Porsche’s reputation is definitely afactor the company needed to consider. If the reputation was damaged, the company would have lost sales of its existing car lines.11.O ne company may be able to produce at lower incremental cost ormarket better. Also, of course, one of the two may have made a mistake!12.P orsche would recognize that the outsized profits would dwindleas more products come to market and competition becomes more intense.Solutions to Questions and ProblemsNOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability constraints, when these intermediate steps are included in this solutions manual, rounding may appear to have occurred. However, the final answer for each problem is found without rounding during any step in the problem.Basic1. Using the tax shield approach to calculating OCF, we get:OCF = (Sales – Costs)(1 – t C) + t C DepreciationOCF = [($5 × 2,000 –($2 × 2,000)](1 –0.35) +0.35($10,000/5)OCF = $4,600So, the NPV of the project is:NPV = –$10,000 + $4,600(PVIFA17%,5)NPV = $4,7172. We will use the bottom-up approach to calculate the operatingcash flow for each year. We also must be sure to include the net working capital cash flows each year. So, the total cash flow each year will be:Year 1 Year 2 Year 3 Year 4 Sales Rs.7,000 Rs.7,000 Rs.7,000 Rs.7,000Costs 2,000 2,000 2,000 2,000Depreciation 2,500 2,500 2,500 2,500EBT Rs.2,500 Rs.2,500 Rs.2,500 Rs.2,500Tax 850 850 850 850Net income Rs.1,650 Rs.1,650 Rs.1,650 Rs.1,650OCF 0 Rs.4,150 Rs.4,150 Rs.4,150 Rs.4,150Capital spending –Rs.10,000 0 0 0 0NWC –200 –250 –300 –200 950 Incremental cashflow –Rs.10,200 Rs.3,900 Rs.3,850 Rs.3,950 Rs.5,100The NPV for the project is:NPV = –Rs.10,200 + Rs.3,900 / 1.10 + Rs.3,850 / 1.102+ Rs.3,950 / 1.103 + Rs.5,100 / 1.104NPV = Rs.2,978.333. U sing the tax shield approach to calculating OCF, we get:OCF = (Sales – Costs)(1 – t C) + t C DepreciationOCF = (R2,400,000 – 960,000)(1 – 0.30) + 0.30(R2,700,000/3) OCF = R1,278,000So, the NPV of the project is:NPV = –R2,700,000 + R1,278,000(PVIFA15%,3)NPV = R217,961.704.T he cash outflow at the beginning of the project will increasebecause of the spending on NWC. At the end of the project, the company will recover the NWC, so it will be a cash inflow. The sale of the equipment will result in a cash inflow, but we also must account for the taxes which will be paid on this sale. So, the cash flows for each year of the project will be:Year Cash Flow0 – R3,000,000 = –R2.7M – 300K1 1,278,0002 1,278,0003 1,725,000 = R1,278,000 + 300,000 + 210,000 + (0 – 210,000)(.30)And the NPV of the project is:NPV = –R3,000,000 + R1,278,000(PVIFA15%,2) + (R1,725,000 / 1.153) NPV = R211,871.465. First we will calculate the annual depreciation for theequipment necessary for the project. The depreciation amount each year will be:Year 1 depreciation = R2.7M(0.3330) = R899,100Year 2 depreciation = R2.7M(0.4440) = R1,198,800Year 3 depreciation = R2.7M(0.1480) = R399,600So, the book value of the equipment at the end of three years, which will be the initial investment minus the accumulated depreciation, is:Book value in 3 years = R2.7M –(R899,100 + 1,198,800 + 399,600)Book value in 3 years = R202,500The asset is sold at a gain to book value, so this gain is taxable.Aftertax salvage value = R202,500 + (R202,500 – 210,000)(0.30) Aftertax salvage value = R207,750To calculate the OCF, we will use the tax shield approach, so the cash flow each year is:OCF = (Sales – Costs)(1 – t C) + t C DepreciationYear Cash Flow0 – R3,000,000 = –R2.7M – 300K1 1,277,730.00 = (R1,440,000)(.70) + 0.30(R899,100)2 1,367,640.00 = (R1,440,000)(.70) + 0.30(R1,198,800)3 1,635,630.00 = (R1,440,000)(.70) + 0.30(R399,600) + R207,750 + 300,000Remember to include the NWC cost in Year 0, and the recovery of the NWC at the end of the project. The NPV of the project with these assumptions is:NPV = – R3.0M + (R1,277,730/1.15) + (R1,367,640/1.152) +(R1,635,630/1.153)NPV = R220,655.206. First, we will calculate the annual depreciation of the newequipment. It will be:Annual depreciation charge = €925,000/5Annual depreciation charge = €185,000The aftertax salvage value of the equipment is:Aftertax salvage value = €90,000(1 – 0.35)Aftertax salvage value = €58,500Using the tax shield approach, the OCF is:OCF = €360,000(1 – 0.35) + 0.35(€185,000)OCF = €298,750Now we can find the project IRR. There is an unusual feature that is a part of this project. Accepting this project means that we will reduce NWC. This reduction in NWC is a cash inflow at Year 0. This reduction in NWC implies that when the project ends, we will have to increase NWC. So, at the end of theproject, we will have a cash outflow to restore the NWC to its level before the project. We also must include the aftertax salvage value at the end of the project. The IRR of the project is:NPV = 0 = –€925,000 + 125,000 + €298,750(PVIFA IRR%,5) + [(€58,500 – 125,000) / (1+IRR)5]IRR = 23.85%7. First, we will calculate the annual depreciation of the newequipment. It will be:Annual depreciation = £390,000/5Annual depreciation = £78,000Now, we calculate the aftertax salvage value. The aftertax salvage value is the market price minus (or plus) the taxes on the sale of the equipment, so:Aftertax salvage value = MV + (BV – MV)t cVery often, the book value of the equipment is zero as it is in this case. If the book value is zero, the equation for the aftertax salvage value becomes:Aftertax salvage value = MV + (0 – MV)t cAftertax salvage value = MV(1 – t c)We will use this equation to find the aftertax salvage value since we know the book value is zero. So, the aftertax salvage value is:Aftertax salvage value = £60,000(1 – 0.34)Aftertax salvage value = £39,600Using the tax shield approach, we find the OCF for the project is:OCF = £120,000(1 – 0.34) + 0.34(£78,000)OCF = £105,720Now we can find the project NPV. Notice that we include the NWC in the initial cash outlay. The recovery of the NWC occurs in Year 5, along with the aftertax salvage value.NPV = –£390,000 –28,000 + £105,720(PVIFA10%,5) + [(£39,600 + 28,000) / 1.15]NPV = £24,736.268. To find the BV at the end of four years, we need to find theaccumulated depreciation for the first four years. We could calculate a table with the depreciation each year, but an easier way is to add the MACRS depreciation amounts for each of the first four years and multiply this percentage times the cost of the asset. We can then subtract this from the asset cost. Doing so, we get:BV4 = $9,300,000 – 9,300,000(0.2000 + 0.3200 + 0.1920 + 0.1150) BV4 = $1,608,900The asset is sold at a gain to book value, so this gain is taxable.Aftertax salvage value = $2,100,000 + ($1,608,900 –2,100,000)(.40)Aftertax salvage value = $1,903,5609. We will begin by calculating the initial cash outlay, that is,the cash flow at Time 0. To undertake the project, we will have to purchase the equipment and increase net working capital. So, the cash outlay today for the project will be:Equipment –€2,000,000NWC –100,000Total –€2,100,000Using the bottom-up approach to calculating the operating cash flow, we find the operating cash flow each year will be:Sales €1,200,000Costs 300,000Depreciation 500,000EBT €400,000Tax 140,000Net income €260,000The operating cash flow is:OCF = Net income + DepreciationOCF = €260,000 + 500,000OCF = €760,000To find the NPV of the project, we add the present value of the project cash flows. We must be sure to add back the net working capital at the end of the project life, since we are assuming the net working capital will be recovered. So, the project NPV is:NPV = –€2,100,000 + €760,000(PVIFA14%,4) + €100,000 / 1.144NPV = €173,629.3810.W e will need the aftertax salvage value of the equipment tocompute the EAC. Even though the equipment for each product hasa different initial cost, both have the same salvage value. Theaftertax salvage value for both is:Both cases: aftertax salvage value = $20,000(1 –0.35) = $13,000To calculate the EAC, we first need the OCF and NPV of each option. The OCF and NPV for Techron I is:OCF = – $34,000(1 – 0.35) + 0.35($210,000/3) = $2,400NPV = –$210,000 + $2,400(PVIFA14%,3) + ($13,000/1.143) = –$195,653.45EAC = –$195,653.45 / (PVIFA14%,3) = –$84,274.10And the OCF and NPV for Techron II is:OCF = – $23,000(1 – 0.35) + 0.35($320,000/5) = $7,450NPV = –$320,000 + $7,450(PVIFA14%,5) + ($13,000/1.145) = –$287,671.75EAC = –$287,671.75 / (PVIFA14%,5) = –$83,794.05The two milling machines have unequal lives, so they can only be compared by expressing both on an equivalent annual basis, which is what the EAC method does. Thus, you prefer the Techron II because it has the lower (less negative) annual cost.Intermediate11.F irst, we will calculate the depreciation each year, which willbe:D1 = ¥480,000(0.2000) = ¥96,000D2 = ¥480,000(0.3200) = ¥153,600D3 = ¥480,000(0.1920) = ¥92,160D4 = ¥480,000(0.1150) = ¥55,200The book value of the equipment at the end of the project is:BV4= ¥480,000 –(¥96,000 + 153,600 + 92,160 + 55,200) = ¥83,040The asset is sold at a loss to book value, so this creates a tax refund.After-tax salvage value = ¥70,000 + (¥83,040 – 70,000)(0.35) = ¥74,564.00So, the OCF for each year will be:OCF1 = ¥160,000(1 – 0.35) + 0.35(¥96,000) = ¥137,600.00OCF2 = ¥160,000(1 – 0.35) + 0.35(¥153,600) = ¥157,760.00OCF3 = ¥160,000(1 – 0.35) + 0.35(¥92,160) = ¥136,256.00OCF4 = ¥160,000(1 – 0.35) + 0.35(¥55,200) = ¥123,320.00Now we have all the necessary information to calculate the project NPV. We need to be careful with the NWC in this project.Notice the project requires ¥20,000 of NWC at the beginning, and ¥3,000 more in NWC each successive year. We will subtract the ¥20,000 from the initial cash flow, and subtract ¥3,000 each year from the OCF to account for this spending. In Year 4, we will add back the total spent on NWC, which is ¥29,000. The ¥3,000 spent on NWC capital during Year 4 is irrelevant. Why?Well, during this year the project required an additional ¥3,000, but we would get the money back immediately. So, thenet cash flow for additional NWC would be zero. With all this, the equation for the NPV of the project is:NPV = –¥480,000 –20,000 + (¥137,600 –3,000)/1.14 + (¥157,760 – 3,000)/1.142+ (¥136,256 –3,000)/1.143+ (¥123,320 + 29,000 + 74,564)/1.144NPV = –¥38,569.4812.I f we are trying to decide between two projects that will notbe replaced when they wear out, the proper capital budgeting method to use is NPV. Both projects only have costs associated with them, not sales, so we will use these to calculate the NPV of each project. Using the tax shield approach to calculate the OCF, the NPV of System A is:OCF A = –元120,000(1 – 0.34) + 0.34(元430,000/4)OCF A = –元42,650NPV A = –元430,000 –元42,650(PVIFA20%,4)NPV A = –元540,409.53And the NPV of System B is:OCF B = –元80,000(1 – 0.34) + 0.34(元540,000/6)OCF B = –元22,200NPV B = –元540,000 –元22,200(PVIFA20%,6)NPV B = –元613,826.32If the system will not be replaced when it wears out, then System A should be chosen, because it has the more positive NPV.13.If the equipment will be replaced at the end of its useful life,the correct capital budgeting technique is EAC. Using the NPVs we calculated in the previous problem, the EAC for each system is:EAC A = –元540,409.53 / (PVIFA20%,4)EAC A = –元208,754.32EAC B = –元613,826.32 / (PVIFA20%,6)EAC B = –元184,581.10If the conveyor belt system will be continually replaced, we should choose System B since it has the more positive NPV.14.S ince we need to calculate the EAC for each machine, sales areirrelevant. EAC only uses the costs of operating the equipment, not the sales. Using the bottom up approach, or net income plus depreciation, method to calculate OCF, we get:Machine A Machine BVariable costs –₪3,150,000 –₪2,700,000Fixed costs –150,000 –100,000Depreciation –350,000 –500,000EBT –₪3,650,000 –₪3,300,000Tax 1,277,500 1,155,000Net income –₪2,372,500 –₪2,145,000+ Depreciation 350,000 500,000OCF –₪2,022,500 –₪1,645,000The NPV and EAC for Machine A is:NPV A = –₪2,100,000 –₪2,022,500(PVIFA10%,6) NPV A = –₪10,908,514.76EAC A = –₪10,908,514.76 / (PVIFA10%,6)EAC A = –₪2,504,675.50And the NPV and EAC for Machine B is:NPV B = –₪4,500,000 – 1,645,000(PVIFA10%,9)NPV B = –₪13,973,594.18EAC B = –₪13,973,594.18 / (PVIFA10%,9)EAC B = –₪2,426,382.43You should choose Machine B since it has a more positive EAC.15.W hen we are dealing with nominal cash flows, we must be carefulto discount cash flows at the nominal interest rate, and we must discount real cash flows using the real interest rate.Project A’s cash flows are in real terms, so we need to find the real interest rate. Using the Fisher equation, the real interest rate is:1 + R = (1 + r)(1 + h)1.15 = (1 + r)(1 + .04)r = .1058 or 10.58%So, the NPV of Project A’s real cash flows, discounting at the real interest rate, is:NPV = –฿40,000 + ฿20,000 / 1.1058 + ฿15,000 / 1.10582 + ฿15,000 / 1.10583NPV = ฿1,448.88Project B’s cash flow are in nominal terms, so the NPV discount at the nominal interest rate is:NPV = –฿50,000 + ฿10,000 / 1.15 + ฿20,000 / 1.152+ ฿40,000 /1.153NPV = ฿119.17We should accept Project A if the projects are mutually exclusive since it has the highest NPV.16.T o determine the value of a firm, we can simply find thepre sent value of the firm’s future cash flows. No depreciation is given, so we can assume depreciation is zero. Using the tax shield approach, we can find the present value of the aftertax revenues, and the present value of the aftertax costs. The required return, growth rates, price, and costs are all given in real terms. Subtracting the costs from the revenues will give us the value of the firm’s cash flows. We must calculate the present value of each separately since each is growing at a different rate. First, we will find the present value of the revenues. The revenues in year 1 will be the number of bottles sold, times the price per bottle, or:Aftertax revenue in year 1 in real terms = (2,000,000 ×$1.50)(1 – 0.34)Aftertax revenue in year 1 in real terms = $1,650,000Revenues will grow at six percent per year in real terms forever. Apply the growing perpetuity formula, we find the present value of the revenues is:PV of revenues = C1 / (R–g)PV of revenues = $1,650,000 / (0.10 – 0.06)PV of revenues = $41,250,000The real aftertax costs in year 1 will be:Aftertax costs in year 1 in real terms = (2,000,000 ×$0.65)(1 – 0.34)Aftertax costs in year 1 in real terms = $858,000Costs will grow at five percent per year in real terms forever.Applying the growing perpetuity formula, we find the present value of the costs is:PV of costs = C1 / (R–g)PV of costs = $858,000 / (0.10 – 0.05)PV of costs = $17,160,000Now we can find the value of the firm, which is:Value of the firm = PV of revenues – PV of costsValue of the firm = $41,250,000 – 17,160,000Value of the firm = $24,090,00017.To calculate the nominal cash flows, we simple increase eachitem in the income statement by the inflation rate, except for depreciation. Depreciation is a nominal cash flow, so it does not need to be adjusted for inflation in nominal cash flow analysis. Since the resale value is given in nominal terms as of the end of year 5, it does not need to be adjusted for inflation. Also, no inflation adjustment is needed for either the depreciation charge or the recovery of net working capital since these items are already expressed in nominal terms. Note that an increase in required net working capital is a negative cash flow whereas a decrease in required net working capital isa positive cash flow. The nominal aftertax salvage value is:Market price $30,000Tax on sale –10,200Aftertax salvage value $19,800Remember, to calculate the taxes paid (or tax credit) on the salvage value, we take the book value minus the market value, times the tax rate, which, in this case, would be:Taxes on salvage value = (BV – MV)t CTaxes on salvage value = ($0 – 30,000)(.34)Taxes on salvage value = –$10,200Now we can find the nominal cash flows each year using the income statement. Doing so, we find:Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Sales $200,000 $206,000 $212,180 $218,545 $225,102Expenses 50,000 51,500 53,045 54,636 56,275Depreciation 50,000 50,000 50,000 50,000 50,000EBT $100,000 $104,500 $109,135 $113,909 $118,826Tax 34,000 35,530 37,106 38,729 40,401Net income $66,000 $68,970 $72,029 $75,180 $78,425OCF $116,000 $118,970 $122,029 $125,180 $128,425Capital spending –$250,000 $19,800NWC –10,000 10,000Total cash flow –$260,000 $116,000 $118,970 $122,029 $125,180 $158,22518.T he present value of the company is the present value of thefuture cash flows generated by the company. Here we have real cash flows, a real interest rate, and a real growth rate. The cash flows are a growing perpetuity, with a negative growth rate. Using the growing perpetuity equation, the present value of the cash flows are:PV = C1 / (R–g)PV = $120,000 / [.11 – (–.07)]PV = $666,666.6719.T o find the EAC, we first need to calculate the NPV of theincremental cash flows. We will begin with the aftertax salvage value, which is:Taxes on salvage value = (BV – MV)t CTaxes on salvage value = (€0 – 10,000)(.34)Taxes on salvage value = –€3,400Market price €10,000Tax on sale –3,400Aftertax salvage value €6,600Now we can find the operating cash flows. Using the tax shield approach, the operating cash flow each year will be:OCF = –€5,000(1 – 0.34) + 0.34(€45,000/3)OCF = €1,800So, the NPV of the cost of the decision to buy is:NPV = –€45,000 + €1,800(PVIFA12%,3) + (€6,600/1.123)NPV = –€35,987.95In order to calculate the equivalent annual cost, set the NPV of the equipment equal to an annuity with the same economic life. Since the project has an economic life of three years and is discounted at 12 percent, set the NPV equal to a three-year annuity, discounted at 12 percent.EAC = –€35,987.95 / (PVIFA12%,3)EAC = –€14,979.8020.W e will find the EAC of the EVF first. There are no taxes sincethe university is tax-exempt, so the maintenance costs are the operating cash flows. The NPV of the decision to buy one EVF is:NPV = –₩8,000 –₩2,000(PVIFA14%,4)NPV = –₩13,827.42In order to calculate the equivalent annual cost, set the NPV of the equipment equal to an annuity with the same economic life. Since the project has an economic life of four years and is discounted at 14 percent, set the NPV equal to a three-year annuity, discounted at 14 percent. So, the EAC per unit is:EAC = –₩13,827.42 / (PVIFA14%,4)EAC = –₩4,745.64Since the university must buy 10 of the word processors, the total EAC of the decision to buy the EVF word processor is:Total EAC = 10(–₩4,745.64)Total EAC = –₩47,456.38Note, we could have found the total EAC for this decision by multiplying the initial cost by the number of word processors needed, and multiplying the annual maintenance cost of each by the same number. We would have arrived at the same EAC.We can find the EAC of the AEH word processors using the same method, but we need to include the salvage value as well. Thereare no taxes on the salvage value since the university is tax-exempt, so the NPV of buying one AEH will be:NPV = –₩5,000 –₩2,500(PVIFA14%,3) + (₩500/1.143)NPV = –₩10,466.59So, the EAC per machine is:EAC = –₩10,466.59 / (PVIFA14%,3)EAC = –₩4,508.29Since the university must buy 11 of the word processors, the total EAC of the decision to buy the AEH word processor is:Total EAC = 11(–₩4,508.29)Total EAC = –₩49,591.21The university should buy the EVF word processors since the EAC is lower. Notice that the EAC of the AEH is lower on a per machine basis, but because the university needs more of these word processors, the total EAC is higher.21.W e will calculate the aftertax salvage value first. Theaftertax salvage value of the equipment will be:Taxes on salvage value = (BV – MV)t CTaxes on salvage value = (₫0 – 100,000)(.34)Taxes on salvage value = –₫34,000Market price ₫100,000Tax on sale –34,000Aftertax salvage value ₫66,000Next, we will calculate the initial cash outlay, that is, the cash flow at Time 0. To undertake the project, we will have to purchase the equipment. The new project will decrease the net working capital, so this is a cash inflow at the beginning of the project. So, the cash outlay today for the project will be:Equipment –₫500,000NWC 100,000Total –₫400,000Now we can calculate the operating cash flow each year for the project. Using the bottom up approach, the operating cash flow will be:Saved salaries ₫120,000Depreciation 100,000EBT ₫20,000。

公司理财(英文版)试题库7

CHAPTER 7Net Present Value and Other Investment Rules Multiple Choice Questions:I. DEFINITIONSNET PRESENT VALUEa 1. The difference between the present value of an investment and its cost is the:a. net present value.b. internal rate of return.c. payback period.d. profitability index.e. discounted payback period.Difficulty level: EasyNET PRESENT VALUE RULEc 2. Which one of the following statements concerning net present value (NPV) is correct?a. An investment should be accepted if, and only if, the NPV is exactlyequal to zero.b. An investment should be accepted only if the NPV is equal to the initialcash flow.c. An investment should be accepted if the NPV is positive and rejected ifit is negative.d. An investment with greater cash inflows than cash outflows, regardlessof when the cash flows occur, will always have a positive NPV andtherefore should always be accepted.e. Any project that has positive cash flows for every time period after theinitial investment should be accepted.Difficulty level: EasyPAYBACKc 3. The length of time required for an investment to generate cash flowssufficient to recover the initial cost of the investment is called the:a. net present value.b. internal rate of return.c. payback period.d. profitability index.e. discounted cash period.Difficulty level: EasyPAYBACK RULEa 4. Which one of the following statements is correct concerning thepayback period?a. An investment is acceptable if its calculated payback period is less thansome pre-specified period of time.b. An investment should be accepted if the payback is positive andrejected if it is negative.c. An investment should be rejected if the payback is positive andaccepted if it is negative.d. An investment is acceptable if its calculated payback period is greaterthan some pre-specified period of time.e. An investment should be accepted any time the payback period is lessthan the discounted payback period, given a positive discount rate.Difficulty level: EasyDISCOUNTED PAYBACKe 5. The length of time required for a project’s discounted cash flows toequal the initial cost of the project is called the:a. net present value.b. internal rate of return.c. payback period.d. discounted profitability index.e. discounted payback period.Difficulty level: EasyDISCOUNTED PAYBACK RULEd 6. The discounted payback rule states that you should accept projects:a. which have a discounted payback period that is greater than some pre-specified period of time.b. if the discounted payback is positive and rejected if it is negative.c. only if the discounted payback period equals some pre-specified periodof time.d. if the discounted payback period is less than some pre-specified periodof time.e. only if the discounted payback period is equal to zero.Difficulty level: EasyAVERAGE ACCOUNTING RETURNc 7. An investment’s average net income divided by its average book valuedefines the average:a. net present value.b. internal rate of return.c. accounting return.d. profitability index.e. payback period.Difficulty level: EasyAVERAGE ACCOUNTING RETURN RULEb 8. An investment is acceptable if its average accounting return (AAR):a. is less than a target AAR.b. exceeds a target AAR.c. exceeds the firm’s return on equity (ROE).d. is less than the firm’s return on assets (ROA).e. is equal to zero and only when it is equal to zero.Difficulty level: EasyINTERNAL RATE OF RETURNb. 9. The discount rate that makes the net present value of an investmentexactly equal tozero is called the:a. external rate of return.b. internal rate of return.c. average accounting return.d. profitability index.e. equalizer.Difficulty level: EasyINTERNAL RATE OF RETURN RULEd 10. An investment is acceptable if its IRR:a. is exactly equal to its net present value (NPV).b. is exactly equal to zero.c. is less than the required return.d. exceeds the required return.e. is exactly equal to 100 percent.Difficulty level: EasyMULTIPLE RATES OF RETURNe 11. The possibility that more than one discount rate will make the NPV ofan investment equal to zero is called the _____ problem.a. net present value profilingb. operational ambiguityc. mutually exclusive investment decisiond. issues of scalee. multiple rates of returnDifficulty level: MediumMUTUALLY EXCLUSIVE PROJECTSc 12. A situation in which accepting one investment prevents the acceptanceof another investment is called the:a. net present value profile.b. operational ambiguity decision.c. mutually exclusive investment decision.d. issues of scale problem.e. multiple choices of operations decision.Difficulty level: EasyPROFITABILITY INDEXd. 13. The present value of an investment’s future cash flows divided by theinitial cost of the investment is called the:a. net present value.b. internal rate of return.c. average accounting return.d. profitability index.e. profile period.Difficulty level: EasyPROFITABILITY INDEX RULEa 14. An investment is acceptable if the profitability index (PI) of theinvestment is:a. greater than one.b. less than one.c. greater than the internal rate of return (IRR).d. less than the net present value (NPV).e. greater than a pre-specified rate of return.Difficulty level: EasyII. CONCEPTSNET PRESENT VALUEd 15. All else constant, the net present value of a project increases when:a. the discount rate increases.b. each cash inflow is delayed by one year.c. the initial cost of a project increases.d. the rate of return decreases.e. all cash inflows occur during the last year of a project’s life instead ofperiodically throughout the life of the project.Difficulty level: EasyNET PRESENT VALUEa 16. The primary reason that company projects with positive net present values areconsidered acceptable is that:a. they create value for the owners of the firm.b. the project’s rate of return exceeds the rate of inflation.c. they return the initial cash outlay within three years or less.d. the required cash inflows exceed the actual cash inflows.e. the investment’s cost exceeds the present value of the cash inflows.Difficulty level: EasyNET PRESENT VALUEd 17. If a project has a net present value equal to zero, then:I. the present value of the cash inflows exceeds the initial cost of the project.II. the project produces a rate of return that just equals the rate required to accept theproject.III. the project is expected to produce only the minimally required cash inflows.IV. any delay in receiving the projected cash inflows will cause the project to have a negative net present value.a. II and III onlyb. II and IV onlyc. I, II, and IV onlyd. II, III, and IV onlye. I, II, and III onlyDifficulty level: MediumNET PRESENT VALUEb 18. Net present value:a. cannot be used when deciding between two mutually exclusive projects.b. is more useful to decision makers than the internal rate of return when comparingdifferent sized projects.c. is easy to explain to non-financial managers and thus is the primary method of analysisused by the lowest levels of management.d. is not an as widely used tool as payback and discounted paybacke. is very similar in its methodology to the average accounting return.Difficulty level: EasyPAYBACKc 19. Payback is frequently used to analyze independent projects because:a. it considers the time value of money.b. all relevant cash flows are included in the analysis.c. it is easy and quick to calculate.d. it is the most desirable of all the available analytical methods from a financialperspective.e. it produces better decisions than those made using either NPV or IRR.Difficulty level: EasyPAYBACKc 20. The advantages of the payback method of project analysis include the:I. application of a discount rate to each separate cash flow.II. bias towards liquidity.III. ease of use.IV. arbitrary cutoff point.a. I and II onlyb. I and III onlyc. II and III onlyd. II and IV onlye. II, III, and IV onlyDifficulty level: MediumPAYBACKd 21. All else equal, the payback period for a project will decrease whenever the:a. initial cost increases.b. required return for a project increases.c. assigned discount rate decreases.d. cash inflows are moved forward in time.e. duration of a project is lengthened.Difficulty level: MediumDISCOUNTED PAYBACKd 22. The discounted payback period of a project will decrease whenever the:a. discount rate applied to the project is increased.b. initial cash outlay of the project is increased.c. time period of the project is increased.d. amount of each project cash flow is increased.e. costs of the fixed assets utilized in the project increase.Difficulty level: MediumDISCOUNTED PAYBACKa 23. The discounted payback rule may cause:a. some positive net present value projects to be rejected.b. the most liquid projects to be rejected in favor of less liquid projects.c. projects to be incorrectly accepted due to ignoring the time value of money.d. projects with negative net present values to be accepted.e. some projects to be accepted which would otherwise be rejected under the paybackrule.Difficulty level: EasyINTERNAL RATE OF RETURNb 24. The internal rate of return (IRR):I. rule states that a project with an IRR that is less than the required rate should beaccepted.II. is the rate generated solely by the cash flows of an investment.III. is the rate that causes the net present value of a project to exactly equal zero.IV. can effectively be used to analyze all investment scenarios.a. I and IV onlyb. II and III onlyc. I, II, and III onlyd. II, III, and IV onlye. I, II, III, and IVDifficulty level: MediumINTERNAL RATE OF RETURNa 25. The internal rate of return for a project will increase if:a. the initial cost of the project can be reduced.b. the total amount of the cash inflows is reduced.c. each cash inflow is moved such that it occurs one year later than originally projected.d. the required rate of return is reduced.e. the salvage value of the project is omitted from the analysis.Difficulty level: MediumINTERNAL RATE OF RETURNc 26. The internal rate of return is:a. more reliable as a decision making tool than net present value whenever you areconsidering mutually exclusive projects.b. equivalent to the discount rate that makes the net present value equal to one.c. difficult to compute without the use of either a financial calculator or a computer.d. dependent upon the interest rates offered in the marketplace.e. a better methodology than net present value when dealing with unconventional cashflows.Difficulty level: MediumINTERNAL RATE OF RETURNa 27. The internal rate of return tends to be:a. easier for managers to comprehend than the net present value.b. extremely accurate even when cash flow estimates are faulty.c. ignored by most financial analysts.d. used primarily to differentiate between mutually exclusive projects.e. utilized in project analysis only when multiple net present values apply.Difficulty level: EasyINCREMENTAL INTERNAL RATE OF RETURNe 28. You are trying to determine whether to accept project A or project B. These projectsare mutually exclusive. As part of your analysis, you should computethe incremented IRR by determining:a. the internal rate of return for the cash flows of each project.b. the net present value of each project using the internal rate of return as the discountrate.c. the discount rate that equates the discounted payback periods for each project.d. the discount rate that makes the net present value of each project equal to 1.e. the internal rate of return for the differences in the cash flows of the two projects.Difficulty level: MediumINCREMENTAL INTERNAL RATE OF RETURNb 29. Graphing the incremental IRR helps explain:a. why one project is always superior to another project.b. how decisions concerning mutually exclusive projects are derived.c. how the duration of a project affects the decision as to which project to accept.d. how the net present value and the initial cash outflow of a project are related.e. how the profitability index and the net present value are related.Difficulty level: MediumPROFITABILITY INDEXd 30. The profitability index is closely related to:a. payback.b. discounted payback.c. the average accounting return.d. net present value.e. mutually exclusive projects.Difficulty level: EasyPROFITABILITY INDEXb 31. Analysis using the profitability index:a. frequently conflicts with the accept and reject decisions generated bythe application ofthe net present value rule.b. is useful as a decision tool when investment funds are limited.c. is useful when trying to determine which one of two mutually exclusive projectsshould be accepted.d. utilizes the same basic variables as those used in the average accounting return.e. produces results which typically are difficult to comprehend or apply.Difficulty level: MediumPROFITABILITY INDEXe 32. If you want to review a project from a benefit-cost perspective, you should use the_____ method of analysis.a. net present valueb. paybackc. internal rate of returnd. average accounting returne. profitability indexDifficulty level: EasyPROFITABILITY INDEXb 33. When the present value of the cash inflows exceeds the initial cost of a project, thenthe project should be:a. accepted because the internal rate of return is positive.b. accepted because the profitability index is greater than 1.c. accepted because the profitability index is negative.d. rejected because the internal rate of return is negative.e. rejected because the net present value is negative.Difficulty level: EasyMUTUALLY EXCLUSIVE PROJECTSc 34. Which one of the following is the best example of two mutually exclusive projects?a. planning to build a warehouse and a retail outlet side by sideb. buying sufficient equipment to manufacture both desks and chairs simultaneouslyc. using an empty warehouse for storage or renting it entirely out to another firmd. using the company sales force to promote sales of both shoes and sockse. buying both inventory and fixed assets using funds from the same bond issueDifficulty level: MediumMUTUALLY EXCLUSIVE PROJECTSd 35. The Liberty Co. is considering two projects. Project A consists of building a wholesalebook outlet on lot #169 of the Englewood Retail Center. Project B consists of buildinga sit-down restaurant on lot #169 of the Englewood Retail Center. When trying todecide whether or build the book outlet or the restaurant, management should relymost heavily on the analysis results from the _____ method of analysis.a. profitability indexb. internal rate of returnc. paybackd. net present valuee. accounting rate of returnDifficulty level: MediumMUTUALLY EXCLUSIVE PROJECTSc 36. When two projects both require the total use of the same limited economic resource,the projects are generally considered to be:a. independent.b. marginally profitable.c. mutually exclusive.d. acceptable.e. internally profitable.Difficulty level: EasyMUTUALLY EXCLUSIVE PROJECTSc 37. Matt is analyzing two mutually exclusive projects of similar size and has prepared thefollowing data. Both projects have 5 year lives.Project A Project B Net present value $15,090$14,693Payback period 2.76 years 2.51 yearsAverage accounting return 9.3 percent 9.6 percent Required return 8.3 percent8.0 percentRequired AAR 9.0 percent 9.0 percentMatt has been asked for his best recommendation given thisinformation. His recommendation should be to accept:a. project B because it has the shortest payback period.b. both projects as they both have positive net present values.c. project A and reject project B based on their net present values.d. project B and reject project A based on their average accounting returns.e. project B and reject project A based on both the payback period andthe averageaccounting return.Difficulty level: MediumINVESTMENT ANALYSISa 38. Given that the net present value (NPV) is generally considered to be the best methodof analysis, why should you still use the other methods?a. The other methods help validate whether or not the results from the net present value analysis are reliable.b. You need to use the other methods since conventional practice dictates that you onlyaccept projects after you have generated three accept indicators.c. You need to use other methods because the net present value method is unreliable when a project has unconventional cash flows.d. The average accounting return must always indicate acceptance since this is the bestmethod from a financial perspective.e. The discounted payback method must always be computed to determine if a projectreturns a positive cash flow since NPV does not measure this aspect of a project.Difficulty level: MediumINVESTMENT ANALYSISe 39. In actual practice, managers frequently use the:I. AAR because the information is so readily available.II. IRR because the results are easy to communicate and understand.III. payback because of its simplicity.IV. net present value because it is considered by many to be the best method of analysis.a. I and III onlyb. II and III onlyc. I, III, and IV onlyd. II, III, and IV onlye. I, II, III, and IVDifficulty level: MediumINVESTMENT ANALYSISa 40. No matter how many forms of investment analysis you do:a. the actual results from a project may vary significantly from the expected results.b. the internal rate of return will always produce the most reliable results.c. a project will never be accepted unless the payback period is met.d. the initial costs will generally vary considerably from the estimated costs.e. only the first three years of a project ever affect its final outcome.Difficulty level: EasyINVESTMENT ANALYSISb 41. Which of the following methods of project analysis are biased towards short-termprojects?I. internal rate of returnII. accounting rate of returnIII. paybackIV. discounted paybacka. I and II onlyb. III and IV onlyc. II and III onlyd. I and IV onlye. II and IV onlyDifficulty level: MediumINVESTMENT ANALYSISa 42. If a project is assigned a required rate of return equal to zero, then:a. the timing of the project’s cash flows has no bearing on the value of the project.b. the project will always be accepted.c. the project will always be rejected.d. whether the project is accepted or rejected will depend on the timing of the cash flows.e. the project can never add value for the shareholders.Difficulty level: MediumDECISION RULESe 43. You are considering a project with the following data:Internal rate of return 8.7 percentProfitability ratio .98Net present value -$393Payback period 2.44 yearsRequired return 9.5 percentWhich one of the following is correct given this information?a. The discount rate used in computing the net present value must have been less than 8.7percent.b. The discounted payback period will have to be less than 2.44 years.c. The discount rate used to compute the profitability ratio was equal to the internal rate of return.d. This project should be accepted based on the profitability ratio.e. This project should be rejected based on the internal rate of return.Difficulty level: MediumNET PRESENT VALUEc 44. A ccepting positive NPV projects benefits the stockholders because:a. it is the most easily understood valuation process.b. the present value of the expected cash flows are equal to the cost.c. the present value of the expected cash flows are greater than the cost.d. it is the most easily calculated.e. None of the above.Difficulty level: EasyNET PRESENT VALUEa 45. W hich of the following does not characterize NPV?a. NPV does not incorporate risk into the analysis.b. NPV incorporates all relevant information.c. NPV uses all of the project's cash flows.d. NPV discounts all future cash flows.e. Using NPV will lead to decisions that maximize shareholder wealth.Difficulty level: EasyPAYBACKe 46. T he payback period rule:a. discounts cash flows.b. ignores initial cost.c. always uses all possible cash flows in its calculation.d. Both A and C.e. None of the above.Difficulty level: EasyPAYBACKc 47. T he payback period rule accepts all investment projects in which thepayback period for the cash flows is:a. equal to the cutoff point.b. greater than the cutoff point.c. less than the cutoff point.d. positive.e. None of the above.Difficulty level: EasyPAYBACKd 48. T he payback period rule is a convenient and useful tool because:a. it provides a quick estimate of how rapidly the initial investment will berecouped.b. results of a short payback rule decision will be quickly seen.c. it does not take into account time value of money.d. All of the above.e. None of the above.Difficulty level: EasyDISCOUNTED PAYBACKa 49. T he discounted payback period rule:a. considers the time value of money.b. discounts the cutoff point.c. ignores uncertain cash flows.d. is preferred to the NPV rule.e. None of the above.Difficulty level: EasyPAYBACKc 50. T he payback period rule:a. determines a cutoff point so that all projects accepted by the NPV rulewill be accepted by the payback period rule.b. determines a cutoff point so that depreciation is just equal to positivecash flows in the payback year.c. requires an arbitrary choice of a cutoff point.d. varies the cutoff point with the interest rate.e. Both A and D.Difficulty level: EasyAVERAGE ACCOUNTING RETURNc 51. T he average accounting return is determined by:a. dividing the yearly cash flows by the investment.b. dividing the average cash flows by the investment.c. dividing the average net income by the average investment.d. dividing the average net income by the initial investment.e. dividing the net income by the cash flow.Difficulty level: EasyAVERAGE ACCOUNTING RETURNb 52. T he investment decision rule that relates average net income to averageinvestment is the:a. discounted cash flow method.b. average accounting return method.c. average payback method.d. average profitability index.e. None of the above.Difficulty level: EasyMODIFIED INTERNAL RATE OF RETURNd 53. M odified internal rate of return:a. handles the multiple IRR problem by combining cash flows until onlyone change in sign change remains.b. requires the use of a discount rate.c. does not require the use of a discount rate.d. Both A and B.e. Both A and C.Difficulty level: MediumAVERAGE ACCOUNTING RETURNd 54. T he shortcoming(s) of the average accounting return (AAR) method is(are):a. the use of net income instead of cash flows.b. the pattern of income flows has no impact on the AAR.c. there is no clear-cut decision rule.d. All of the above.e. None of the above.Difficulty level: MediumINTERNAL RATE OF RETURNe 55. T he two fatal flaws of the internal rate of return rule are:a. arbitrary determination of a discount rate and failure to consider initialexpenditures.b. arbitrary determination of a discount rate and failure to correctlyanalyze mutually exclusive investment projects.c. arbitrary determination of a discount rate and the multiple rate ofreturn problem.d. failure to consider initial expenditures and failure to correctly analyzemutually exclusive investment projects.e. failure to correctly analyze mutually exclusive investment projects andthe multiple rate of return problem.Difficulty level: MediumMUTUALLY EXCLUSIVE PROJECTSd 56. A mutually exclusive project is a project whose:a. acceptance or rejection has no effect on other projects.b. NPV is always negative.c. IRR is always negative.d. acceptance or rejection affects other projects.e. cash flow pattern exhibits more than one sign change.Difficulty level: EasyINTERNAL RATE OF RETURNd 57. A project will have more than one IRR if:a. the IRR is positive.b. the IRR is negative.c. the NPV is zero.d. the cash flow pattern exhibits more than one sign change.e. the cash flow pattern exhibits exactly one sign change.Difficulty level: EasyINTERNAL RATE OF RETURN RULESb 58. U sing internal rate of return, a conventional project should be acceptedif the internal rate of return is:a. equal to the discount rate.b. greater than the discount rate.c. less than the discount rate.d. negative.e. positive.Difficulty level: EasyINTERNAL RATE OF RETURNa 59. The internal rate of return may be defined as:a. the discount rate that makes the NPV cash flows equal to zero.b. the difference between the market rate of interest and the NPV.c. the market rate of interest less the risk-free rate.d. the project acceptance rate set by management.e. None of the above.Difficulty level: MediumMULTIPLE INTERNAL RATE OF RETURNSd 60. The problem of multiple IRRs can occur when:a. there is only one sign change in the cash flows.b. the first cash flow is always positive.c. the cash flows decline over the life of the project.d. there is more than one sign change in the cash flows.e. None of the above.Difficulty level: EasyTIMING AND SCALE ISSUES WITH INTERNAL RATE OF RETURNb 61. T he elements that cause problems with the use of the IRR in projectsthat are mutually exclusive are:a. the discount rate and scale problems.b. timing and scale problems.c. the discount rate and timing problems.d. scale and reversing flow problems.e. timing and reversing flow problems.Difficulty level: MediumNET PRESENT VALUE DECISIONc 62. If there is a conflict between mutually exclusive projects due to the IRR,one should:a. drop the two projects immediately.b. spend more money on gathering information.c. depend on the NPV as it will always provide the most value.d. depend on the AAR because it does not suffer from these sameproblems.e. None of the above.Difficulty level: MediumPROFITABILITY INDEXe 63. The profitability index is the ratio of:a. average net income to average investment.b. internal rate of return to current market interest rate.c. net present value of cash flows to internal rate of return.d. net present value of cash flows to average accounting return.e. present value of cash flows to initial investment cost.Difficulty level: EasyINVESTMENT DECISION RULESa 64. Which of the following statement is true?a. One must know the discount rate to compute the NPV of a project butone can compute the IRR without referring to the discount rate.b. One must know the discount rate to compute the IRR of a project butone can compute the NPV without referring to the discount rate.c. Payback accounts for time value of money.d. There will always be one IRR regardless of cash flows.e. Average accounting return is the ratio of total assets to total net income.Difficulty level: MediumCAPITAL BUDGETING PRACTICEb 65. Graham and Harvey (2001) found that ___ and ___ were the two mostpopular capital budgeting methods.a. Internal Rate of Return; Payback Periodb. Internal Rate of Return; Net Present Valuec. Net Present Value; Payback Periodd. Modified Internal Rate of Return; Internal Rate of Returne. Modified Internal Rate of Return; Net Present Value。

公司理财期末试题及答案(英文版)

EXAM PAPER 1I. True(T) or False(F). Please fill in the bracket with T or F. (15%)1. In financial management, the more appropriate goal of the firm is maximization of shareholderwealth. ( )2. The component cost of preferred stock must be adjusted for taxes which the stockholdersmust pay on the dividends. ( )3. If an investment project has a profitability index of 1.15, the project’s internal rate of returnexceeds its net present value. ( )4. With an annuity due the payments occur at the end of each period. ( )5. If the firm decides to impose a capital constraint on investment projects, the appropriatedecision criterion is to select the set of projects with the highest NPV subject to the capital constraint. ( )6. Business risk refers to the relative dispersion in the firm’s EBIT. ( )7. Net working capital equals current assets less current liabilities. ( )8. Under MM’s model with corporate taxes, the benefits of debt financing stem solely from the taxdeductibility of interest payments. ( )9. Investors can only expect to receive a return for incurring unsystematic risk. ( )10. The Security Market Line is a risk-return trade-off for combinations of the market portfolio andthe riskless asset. ( )II. Multiple Choice (15%)1. Dorset Ltd wishes to calculate its weighted average cost of capital for use in investmentappraisal. The company is financed by 150 million $1 ordinary shares, which have a current market value of $2, and $100 million 12 per cent irredeemable debentures, which are currently quoted at $150 per $100 nominal value. The cost of ordinary share capital is 11 per cent and the rate of corporation tax is 25 per cent.What is the weighted average cost of capital for Dorset Ltd? (To one decimal place)A. 9·0 per centB. 9·3 per centC. 10·4 per centD. 11·4 per cent2. Cheshire Ltd has developed a revolutionary form of tyre gauge at a cost of $300,000 to date.To produce the tyre gauge, a new machine will be acquired immediately at a cost of $750,000.The machine will be sold at the end of the five years for $350,000 and will be depreciated over its life using the straight-line method.The tyre gauge has an expected life of five years and estimated future profits from the product are: Years1 2 3 4 5$000 $000 $000 $000 $000Estimated profit 80 160 240 140 130What is the payback period for the new tyre gauge? (To the nearest month)A. 3 years 2 monthsB. 4 years 2 monthsC. 4 years 3 monthsD. 4 years 11 months3. Cumbria Ltd has $1 ordinary shares in issue that have a current market value of $3. Thedividend expected for next year is $0·40 and future dividends are expected to grow at the rate of 5 per cent per annum. The rate of corporation tax is 20 per cent and the dividend Growth model is used to calculate the cost of ordinary shares.What is the cost of ordinary shares to the business?A. 6·1%B. 15·7%C. 18·3%D. 19·0%4. Calcite Ltd used the NPV and IRR methods of investment appraisal to evaluate a project thathas an initial cash outlay followed by annual net cash inflows over its life. After the evaluationhad been undertaken, it was discovered that the cost of capital had been incorrectly calculated and that the correct cost of capital figure was in fact higher than that used.What will be the effect on the NPV and IRR figures of correcting for this error?Effect onNPV IRRA. Decrease DecreaseB. Decrease No changeC. Increase IncreaseD. Increase No Change5. A business evaluates an investment project that has an initial outlay followed by annual netcash inflows of $10 million throughout its infinite life. The evaluation of the inflows produced a present value of $50 million and a profitability (present value) index of 2·0.What is the internal rate of return and initial outlay of this project?IRR Initial outlay% $mA. 20 25B. 20 100C. 40 25D. 10 1006. Quartz Ltd pays an annual dividend of 30 cent per share to shareholders, which is expected tocontinue in perpetuity. The average rate of return for the market is 9% and the company has a beta coefficient of 1·5. The risk-free rate of return is 4%.What is the expected rate of return for the shareholders of the company and the predicted value of the shares in the company?Expected rate Predictedof return value(%) (cent)A. 23·5 705B. 17·5 171C. 16·5 182D. 11·5 2617. Tourmaline Ltd pays its major credit supplier 40 days after receiving the goods and receives nosettlement discount. The supplier has recently offered the company revised credit terms of 3/10, net 40.If Tourmaline Ltd refuses the settlement discount and pays in full after 40 days, what is the approximate, implied, interest cost that is incurred by the company per year?A. 10·3%B. 27·4%C. 28·2%D. 37·6%8. Carrickfergus Ltd wishes to forecast its financial performance and position for the forthcomingyear. The forecast model used by the company incorporates the following relationships: Sales: total assets employed 2·5:1Current assets: current liabilities 1·8:1Quick assets: current liabilities 1·2:1Fixed assets: current assets 1·0:1If sales for the forthcoming year are expected to be $800,000, what is the forecast closing stock figure?A. $53,333B. $71,111C. $85,926D. $96,000.9. The Modigliani and Miller (no taxes) proposition concerning capital gearing states that, as thelevel of capital gearing increases from zero,A. the cost of equity capital will remain unchangedB. the weighted average cost of capital will decreaseC. the value of the business will remain unchangedD. the cost of loan capital will increase.10. A study of the shares of companies listed on a particular stock market found that:(i) share prices were independent of past share price movements and followed a random path. (ii) some investors used the published accounts of the companies to analyse performance and, by doing so, made abnormal gains over many years.Which of the following would be consistent with these findings?A. The stock market is inefficientB. The stock market is efficient in the weak formC. The stock market is efficient in the semi-strong formD. The stock market is efficient in the strong form11. The economic order quantity (EOQ) for stocks can be calculated by using an equation of theform:)/2(ZXY EOQ=What is Z in the above equation?A. Cost of placing an orderB. Annual demand for the item of stockC. Cost of holding one unit of stock for one yearD. The lead time between placing an order and receiving the goods12. Which of the following is associated with the problem of “overtrading”?A. Higher-than-normal earnings per shareB. Higher-than-normal sales to capital employed ratioC. Lower-than-normal gearing ratioD. Lower-than-normal stock turnover ratio13. Investors have an expected rate of return of 8% from ordinary shares in Algol Ltd, which have abeta of 1·2. The expected returns to the market are 7%.What will be the expected rate of return from ordinary shares in Rigel Ltd, which have a beta of 1.8?A. 9·0%B. 10·5%C. 11·0%D. 12·6%.14. Chrysotile Ltd has ordinary shares with a par value of $0·50 in issue. The company generatedearnings per share of 45c for the financial year that has just ended. The dividend cover ratio is 2·5 times and the gross dividend yield is 2% (Ignore taxation).What is the price/earnings ratio of the company?A. 2·8 timesB. 5·0 timesC. 20·0 timesD. 40·0 times15. Ethical behavior is important because it:A. builds customer loyaltyB. builds a good reputationC. avoids fines and legal expensesD. all of the aboveIII. Solving the following problems. (60 marks)1. Brambling (Electronics) Ltd is a research-led business that specialises in the development of surveillance equipment. The company has recently developed a new form of camera with a powerful fibre-optic lens and is currently considering whether or not to produce the camera. The Board of Directors will soon meet to make a final decision and has the following information available to help it decide:(i) The cost of developing the camera has been $1,400,000 to date and the company iscommitted to spending a further $350,000 within the next two months.(ii) The company has spare production capacity and can produce the camera using machinery that will cost $4,700,000 and which will be purchased immediately. It isexpected to be sold at the end of four years for $800,000.(iii) Total fixed costs identified with the production of the camera are $1,725,000 per year.This includes a depreciation charge in respect of the machinery of $975,000 per yearand a charge allocated to represent a fair share of the fixed costs of the business as awhole of $250,000 per year.(iv) The cameras are expected to sell for $10,000 each and the marketing department believes that the business can sell 800 cameras per year over the next four years.(v) The variable costs of production are $7,000 per camera.(vi) If the business decides not to produce the camera it can sell the patents immediately for $1,300,000.The company has a cost of capital of 12%.Ignore taxation.Required:(a) Calculate the net present value of producing and selling the new camera versus thealternative of selling the patent. (6 marks)(b) Carry out a separate sensitivity analysis to show by how much the following factorswould have to change before the proposal to produce and sell the new camera has an NPV of zero:(i) the initial outlay on the machinery;(ii) the discount rate;(iii) the residual value of the machinery;(iv) the annual net operating cash flows. (11 marks)(c) Briefly evaluate your findings in (a) and (b) above. (3 marks)(20 marks)2.Grebe Ltd operates a chain of cellular telephone stores in the UK. An abbreviated profit and loss account and balance sheet of the business for the year that has just ended is as follows: Abbreviated profit and loss account for the year ended 31 May 2003$000SalesOperating profit for the year Debenture interest payable 6,450 800 160Net profit before taxation Corporation tax (20%)Net profit after taxation Dividends proposed Retained profit for the year 640 128 512 256 256Abbreviated balance sheet as at 31 May 2003$000$000 Fixed assets at written down valuesCurrent assetsLess Creditors: amounts falling due within one yearLess Creditors: amounts falling due after more than one yearCapital and reserves$0·50 Ordinary sharesRetained profit 1,8001,1003,5007004,2002,0002,2006001,6002,200The company is expecting a surge in sales following advances in cellular telephone technology that should translate into additional operating profits of $180,000 per year for the foreseeable future. However, the company will need to invest $1,200,000 immediately in expanding the asset base of the business if it is to achieve these additional profits.The business has approached a large supplier that already has an equity investment in the business to see whether it would be prepared to provide further funds for the business. The supplier has indicated it would be willing to provide the necessary funds by either:(i) an issue of $0·50 ordinary shares at a premium of $1·50 per share, or(ii) an issue of $1,200,000 10% debentures at par.The Board of Directors of Grebe Ltd has already announced that it will maintain the same dividend payout ratio in future years as in the past and that this policy will be unaffected by the form of finance raised.Required:(a) For each of the financing options, calculate the forecast earnings per share for theforthcoming year;(10 marks)(b) Calculate the level of operating profit at which the earnings per share will be the sameunder each financing option. (10 marks)(20 marks)3. Bartok Ltd produces a single product. Financial data concerning the product is as follows:$ $Selling price per unit 20Variable cost per unit 17Fixed costs per unit 2 19Net profit 1At present, total credit sales for the product are $1·2m and the average collection period is one month. In order to stimulate sales for the product, the company is considering liberalising its credit policy so as to allow an average collection period of 1 1/2 months. This change of policy will allow the company to break into the US market where, currently, it has no presence. As a result of this breakthrough, sales will increase by 25%. However, there would be an additional investment required in stocks of $150,000 and an increase in trade creditors of $50,000.The company requires a 25% rate of return on its investments.Ignore taxation.Required:(a) Evaluate the proposal to increase the average collection period for debtorsassuming:(i) all customers take advantage of the longer credit period (8 marks)(ii) only new customers take advantage of the longer credit period. (8 marks)(b) Identify and discuss the main factors which influence the credit terms granted tocustomers by a company. (4 marks)(20 marks)ANSWERS FOR EXAM PAPER 1I. (10%, 1 mark each)1. T2. F3. F4. F5. T6. T7. T8. T9. F 10. FII. (30%, two marks each)1. B2. A3. C4. B5. C6. D7. D8. A9. C 10. B 11. C 12. B 13. C 14. C 15. DIII. (60%, 20marks each)1. (a) Annual operating cash flows can be calculated as follows:$m $m Sales (800 x $10,000) LessVariable costs (800 x $7,000) Fixed costs5·6 0·58·0 6·1 1·9(2 marks)Cash flows relating to the project are as follows:Year0 $m1 $m 2$m 3 $m 4 $m Machinery Opportunity cost Annual cash flows(4·7) (1·3) (6·0)1·9 1·91·9 1·91·9 1·90.8 1·9 2·7(2 marks)The net present value of the project is:$m $m $m $m $mCash flows Discount rate (12%) Present valueNPV (6·0)1·0(6·0)0·291·90·891·691·90·801·521·90·711·352·70·641·73(2maks)(b) (i) The increase required in the initial outlay on machinery before the project becomes nolonger profitable will be $0·29m. The machinery is already expressed in present value terms and so this figure is the same as the net present value of the project. This figure is 6·2% higher than the initial cost figure stated. (2 marks)(ii) If the discount rate is increased to 14%, the NPV of the project is:$m $m $m $m $mCash flows Discount rate (14%) Present valueNPV (6·0)1·0(6·0)0·011·90·881·671·90·771·461·90·681·292·70·591·59Thus, the project will become unprofitable at approximately 14% cost of capital.This represents a 16·7% increase in the cost of capital. (3 marks)(iii) The decrease in the residual value of the equipment (R) that will make the project no longer profitable is calculated as follows:(R x discount factor at the end of four years) – NPV of the project = 0This can be rearranged as follows:(R x discount factor at the end of four years) = NPV of the projectR x 0.64 = $0·29 mR = $0·29m/0·64= $0·45mThis represents a 43·8% decrease in the estimated residual value. (3marks)(iv) The decrease in annual net operating cash flows (C) to make the project no longer profitable is calculated as follows:(C x annuity factor for a four-year period) – NPV = 0This can be rearranged as follows:(C x annuity factor for a four-year period) = NPV C x 3·04 = $0·29m C = $0·29m/3·04 C = $0·095mThis represents a decrease of 5·0% on the estimated annual net operating cash flows. (3marks)(c) The net present value calculations in (a) above indicate that the project will increaseshareholder wealth if it is accepted. The sensitivity calculations in (b) above show by how much each of the key variables will have to change before the project becomes no longer profitable. It can be seen that the most sensitive factor is the annual net operating cash flows followed by the initial cost of the machinery, the discount rate and finally the residual value of the machinery. The annual net operating cash flows will require only a five per cent decrease before the project ceases to be profitable. (3marks)2 (a) Forecast profit and loss account for the year ended 31 May 2004Shares $000Debentures$000 Profit before interest and taxation Debenture interest payable Profit before taxation Corporation tax (20%) Profit after taxation DividendRetained profit for the year Forecast earnings per share980 160 820 164 656 328 328$656,000/1,800,000=36·4c (5marks)980 280 700 140 560 280 280$560,000/1,200,000 46·7c (5marks)(b) The level of operating profit, or profit before interest and taxation (PBIT), at which earnings per share under each method are equal (PBIT = x) is calculated as follows:Shares Debentures(x – B/E PBIT)(1 – tax rate) (x – B/E PBIT)(1 – tax rate)––––––––––––––––––––––– = –––––––––––––––––––––––No. of shares No. of sharesThe level of PBIT at which earnings per share are equal is:(x – $0·16m)(1 – 0·20) (x – $0·28m)(1 – 0·20)–––––––––––––––––––– = –––––––––––––––––––– (3 marks)1·8m 1·2m(0·8 x – $0·128m) (0·8 x – $0·224m)––––––––––––––––– = ––––––––––––––––1·8m 1·2m0·96m x – $0·1536m = 1·44m x – $0·4032m0·48m x = $0·2496mx = $0·52m (2 marks)3. (a) (i) The contribution per unit is $3 (i.e. $20 - $17). A 25% increase in sales will lead to anincrease of sales revenue of $0·3m or 15,000 units (i.e. $0·3m/$20). Hence the increase in contribution and profit will be:15,000 x $3 = $45,000 (4marks)The additional investment required will be:$Increase in stocksIncrease in debtors [($1·5m/12 ) x 11/2m] - [(1·2m/12) x 1m)]Increase in creditorsNet increase in working capitalReturn on investment 150,00087,500237,50050,000187,500= 45,000 x 100% 187,500= 24·0 %(6 marks)(ii) The additional investment required will be:$Increase in stocksIncrease in debtors [($0·3m/12) x 11/2]Increase in creditorsNet increase in working capital Return on investment 150,00037,500187,50050,000137,500= 45,000 x 100% 137,500= 32·7 %(6 marks)Thus, it is if new customers only take advantage of the longer credit period that the proposed change in policy will meet the profit requirements of the company.(b) The main factors that influence the credit terms granted to customers are: Management policies/Market strength /Order size and frequency /Profitability /Resources of the business /Resources of the customer/Industry norms, etc.(4 marks)。

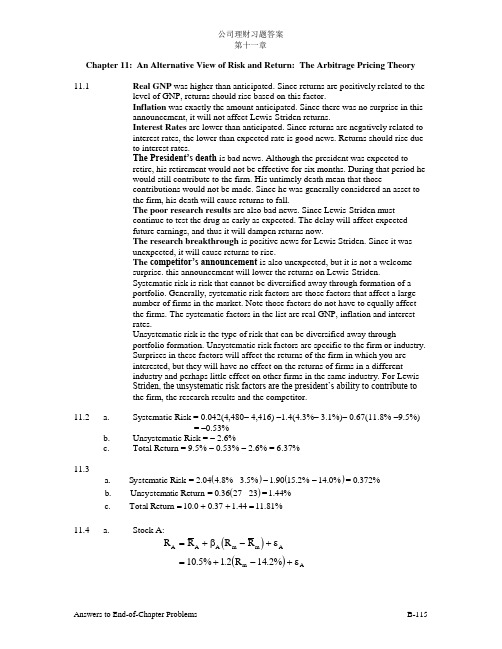

罗斯《公司理财》英文习题答案DOCchap011-推荐下载

公司理财习题答案第十一章Chapter 11: An Alternative View of Risk and Return: The Arbitrage Pricing Theory 11.1Real GNP was higher than anticipated. Since returns are positively related to the level of GNP, returns should rise based on this factor.Inflation was exactly the amount anticipated. Since there was no surprise in this announcement, it will not affect Lewis-Striden returns.Interest Rates are lower than anticipated. Since returns are negatively related to interest rates, the lower than expected rate is good news. Returns should rise due to interest rates.The President’s death is bad news. Although the president was expected to retire, his retirement would not be effective for six months. During that period he would still contribute to the firm. His untimely death mean that thosecontributions would not be made. Since he was generally considered an asset to the firm, his death will cause returns to fall.The poor research results are also bad news. Since Lewis-Striden must continue to test the drug as early as expected. The delay will affect expected future earnings, and thus it will dampen returns now.The research breakthrough is positive news for Lewis Striden. Since it was unexpected, it will cause returns to rise.The competitor’s announcement is also unexpected, but it is not a welcome surprise. this announcement will lower the returns on Lewis-Striden.Systematic risk is risk that cannot be diversified away through formation of a portfolio. Generally, systematic risk factors are those factors that affect a large number of firms in the market. Note those factors do not have to equally affect the firms. The systematic factors in the list are real GNP, inflation and interest rates.Unsystematic risk is the type of risk that can be diversified away throughportfolio formation. Unsystematic risk factors are specific to the firm or industry.Surprises in these factors will affect the returns of the firm in which you are interested, but they will have no effect on the returns of firms in a different industry and perhaps little effect on other firms in the same industry. For Lewis-Striden, the unsystematic risk factors are the president’s ability to contribute to the firm, the research results and the competitor.11.2a.Systematic Risk = 0.042(4,480– 4,416) –1.4(4.3%– 3.1%)– 0.67(11.8% –9.5%)= –0.53%b.Unsystematic Risk = – 2.6%c.Total Return = 9.5% – 0.53% – 2.6% = 6.37%11.3()()()11.81%1.440.3710.0Return Total c.1.44%=23-270.36=Return ic Unsystemat b.0.372%=14.0%15.2%1.903.5%-4.8%2.04=Risk Systematic a.=++=--11.4 a.Stock A:()()R R R R R A A A m m Am A=+-+=+-+βεε105%12142%...Stock B:()()R R R R R B B m m Bm B=+-+=+-+βεε130%098142%...Stock C:()R R R R R C C C m m Cm C=+-+=+-+βεε157%137142%)..(.b.()[]()[]()[]()()()()()()[]()()CB A m cB A m c m B m A m CB A P 25.045.030.0%2.14R 1435.1%925.1225.045.030.0%2.14R 37.125.098.045.02.130.0%7.1525.0%1345.0%5.1030.0%2.14R 37.1%7.1525.0%2.14R 98.0%0.1345.0%2.14R 2.1%5.1030.0R 25.0R 45.0R 30.0R ε+ε+ε+-+=ε+ε+ε+-+++++=ε+-++ε+-++ε+-+=++=c.i.()R R R A B C =+-==+-==+-=105%1215%142%)1113%09815%142%)137%157%13715%142%168%..(..46%.(......ii.R P =+-=12925%1143515%142%)138398%..(..11.5a.Since five stocks have the same expected returns and the same betas, theportfolio also has the same expected return and beta.()R F F E E E E E p =+++++++110084169151212345...b.公司理财习题答案第十一章R F F E N E N E NAs N s are fini F F p N =++++++→∞→=++1100841690110084169121212......,...,1Nbut E te,Thus, R j p 11.6To determine which investment investor would prefer, you must compute the variance of portfolios created by many stocks from either market. Note, because you know that diversification is good, it is reasonable to assume that once an investor chose the market in which he or she will invest, he or she will buy many stocks in that market.Known:E EF ====001002 and and for all i.i σσεε..Assume: The weight of each stock is 1/N; that is, for all i.X N i =1/If a portfolio is composed of N stocks each forming 1/N proportion of the portfolio, thereturn on the portfolio is 1/N times the sum of the returns on the N stocks. Recall that the return on each stock is 0.1+βF+ε.()()()()()()[]()()()()()()()[]()[]()[]()()[]()()()()()j i 2j i 22j i i 2222222222P P P P iP ,0.04Corr 0.01,Cov s =isvariance the ,N as limit In the ,Cov 1/N 1s 1/N s )(1/N 1/N F 2F E 1/N F E 0.10.1/N F 0.1E R E R E R Var 0.101/N 00.1E 1/N F E 0.11/N F 0.1E R E 1/N F 0.1F 0.1(1/N)R 1/N R εε+β=εε+β∞⇒εε-+ε+β=ε∑+εβ+β=ε+β=-ε+β+=-==+β+=ε+β+=ε∑+β+=ε+β+=ε+β+==∑∑∑∑∑∑∑∑()()()()()()Thus,F R f E R E R Var R Corr Var R Corr ii ip P pi jPijR 1i =++=++===+=+010*********002250040002500412212111222.........,,εεεεεεa.()()()()Corr Corr Var R Var R i j i j ppεεεε112212000225000225,,..====Since Var , a risk averse investor will prefer to invest()()R p 1 Var R 2p 〉in the second market.b.Corr ()()εεεε112090i j j ,.,== and Corr 2i ()()Var R Var R pp120058500025==..Since Var averse investor will prefer to invest()()risk a ,R Var R 2p p 1〉in the second market.c.()()()()Corr Var R Var R i j j ppεεεε112120050022500225,,...==== and Corr 2i Since , a risk averse investor will be indifferent ()()Var R Var R pp12=between investing in the two market.d.Indifference implies that the variances of the portfolio in the two markets are equal.()()()()()()Var R Var R Corr Corr Corr Corr p pijiji jij1211222211002250040002500405=+=+=+..,..,,,.εεεεεεεε公司理财习题答案第十一章This is exactly the relationship used in part c.11.7()()()()()()()()()()()() 2.7225%1.211.5s 1.7424%1.211.2s 0.5929%1.210.7s R Var R Var 0/N Var ,N As i.b.22.30%0.22304.9725/100s 4.9725%2.251.211.5s 17.84%0.17843.1824/100s 3.1824%1.441.211.2s 12.62%1.5929/100s 1.5929%1.001.210.7s Var R Var R Var a.22C 22B 22A m 2i i j C 22C B 2B 2A 2A 2i m 2i j ======β=∴→ε∞→===⇒=+====⇒=+===⇒=+=∴ε+β=ii.APT Model:()R R R R i F m F i=+-β%25.14)5.1)(3.36.10(3.3R %06.12)2.1)(3.36.10(3.3R %41.8)7.0)(3.36.10(3.3R C B A =-+==-+==-+=APT Model shows that assets A & B are accurately priced but asset C isoverpriced. Thus, rational investors will not hold asset C.iii.If short selling is allowed, all rational investors will sell short asset C so that the price of asset C will decrease until no arbitrage opportunity exists. In other words, price of asset C should decrease until the return become 14.25%.11.8 a.Let X= the proportion of security of one in the portfolio and (1-X) = the proportion of security two in the portfolio.()()[]()()[]t 222t 121t 2t 212t 111t 1t2t 1pt F F R E x 1F F R E x R X 1XR R β+β+-++β+=-+=The condition that the return of the portfolio does not depend on implies:F 1()05.0)X 1(X 0X 1X 2111=-+=β-+βThus, P=(-1,2); i.e. sell short security one and buy security two.()()()()()()5.2225.11%20%202%201R E 2p p =+-=β=+-=b.Follow the same logic as in part a, we have()()3X 05.1X 1X 0X 1X 4131==-+=β-+βWhere X is the proportion of security three in the portfolio. Thus, sell short security four and buy security three.()()()()()()075.025.03%10%102%103R E 2p p =-=β=-+=this is a risk free portfolio!c.The portfolio in part b provides a risk free return of 10% which is higher than the5% return provided by the risk free security. To take advantage of this opportunity, borrow at the risk free rate of 5% and invest the funds in a portfolio built by selling short security four and buying security three with weights (3,-2).d.Assuming that the risk free security will not change. The price of security four ( that everyone is trying to sell short) will decrease and the price of security three ( that everyone is trying to buy ) will increase. Hence the return of security four will increase and the return of security three will decrease.The alternative is that the prices of securities three and four will remain the same, and the price of the risk-free security drops until its return is 10%.Finally, a combined movement of all security prices is also possible. The prices of security four and the risk-free security will decrease and the price of security four will increase until the opportunity disappears.E (R j 20%10%5%()ββ1210i =2.5。

英文版罗斯公司理财习题答案