交易风险管理(managing transaction exposure)

国际财务管理与外汇风险管理

国际财务管理与外汇风险管理国际财务管理是指在跨国经营活动中对资本、资金和风险进行管理的过程。

而外汇风险管理则是国际财务管理中的重要组成部分,面对全球化时代经济快速变化的挑战,企业如何科学合理地管理外汇风险成为了一个关键问题。

本文将从国际财务管理的角度探讨外汇风险的管理策略。

一、外汇风险的概念与分类外汇风险指的是由于跨国经营活动中涉及的货币兑换而带来的资金损失的可能性。

根据风险的来源和性质,可以将外汇风险分为三类:交易风险、经济风险和转换风险。

1. 交易风险:企业进行跨国贸易时,由于汇率的波动,可能导致交易成本的增加和利润的减少。

交易风险是由于对未来或已存在交易的外汇现金流量的价值变动所导致的损失。

2. 经济风险:指企业由于跨国经营活动带来的外汇收入和支出的波动,从而导致企业的整体经济效益上升或下降,包括合同风险和财务风险。

3. 转换风险:指企业进行跨国投资或跨国经营时,由于汇率的变动,可能导致外币资产或负债的价值发生波动,从而给企业带来损失。

二、外汇风险管理的策略为了有效应对外汇风险,企业可采取多种管理策略。

1. 前期策略:在接触外汇风险前,企业可以采取以下策略:(1)选择适合的交易对手方:在选择跨国合作伙伴时,应评估其经济实力和信用状况,选择实力雄厚、信誉良好的企业进行合作,减少交易风险。

(2)选择合适的市场:在选择跨国市场时,应综合考虑市场潜力、风险程度等因素,选择风险相对较低的市场进行拓展。

(3)建立有效的信息系统:建立完善的信息系统,及时了解国际市场的动态,以便做出及时的战略调整。

2. 短期策略:(1)远期合同:为规避交易风险,企业可以与供应商或客户签订远期合同,锁定货币兑换汇率,在固定时间内实现按固定汇率结算。

(2)选择合适的外汇管道:选择合适的外汇管道进行资金的收付,如利用掉期、期货、期权等金融工具进行风险对冲。

(3)合理利用金融工具:通过购买外汇期权、期货等金融工具,可以在一定程度上保护企业免受汇率波动的影响。

第六章外汇风险管理

3.经营风险(Operating Risk )

经营风险是指由于意料不到的汇率波 动,引起公司末来一定时期内收益发生 变化的一种潜在性的风险。

收益变化的大小,主要取决于汇率变 动对该公司产品成本、价格乃及生产数 量的影响程度

*经济风险的管理

1)经营多样化。是指在国际范围内实 现其销售市场、生产基地以及原料来源 地的多样化。

2)融资多样化。是指在不同的金融市 场上追求多种货币资金的来源和应用, 即实现筹资多样化和投资多样化。

三、外汇风险的构成和外汇风险管理 的基本原理

1.外汇风险基本构成因素: 货币因素和时间因素

2.外汇风险管理的基本原理:

(1)消除构成外汇风险的货币因素或时 间因素

(2)合理调整货币因素或时间因素的结 构

外汇市场(远期外汇交易、外币期货、外币 期权、掉期交易)

货币市场的套期保值是指通过货币市场上的 借贷来抵消已有的债权和债务的外汇风险。

(一)外汇风险管理的基本方法

1.远期合同法(Forward Contract). 2.借款一即期合同一投资法 (Borrow一Spot-Inevest,简称BSI)。 3.提前收付一即期合同一投资法(Lead-

换回本币。

(3)以本币进行投资,或存入银行或进行 其他投资,以投资收入,抵冲一部分采 取防险措施的费用支出。

3. LSI法:

LSI法可以下列步骤操作: (1) 具 有 外 汇 应 收 账 款 的 公 司 , 征 得 债 务 方的同意,请其提前支付货款,并给其 一定折扣。

(2)应收外币账款收讫后,通过即期合同 卖予银行换成本币。

(3)套期保值操作——针对存在的外汇敞 口,实行反向交易,构成一项方向相反 的货币流动,可以全部或部分抵消外汇 风险对企业的影响。

国际投资 名词解释

第七章外国债券:是指一国筹资者在某一国外债券市场上发行的,以该国货币为面值的,并由该国金融机构成效的债券。

主要在美国、瑞士、日本、德国和卢森堡这几个国家的债券市场上发行。

欧洲债券:是指以国筹资者在本国以外的国际债券市场上发行的,以欧洲货币为面值的,有一个或几个国家的金融机构组成辛迪加承销的债券。

这种债券由国际承销团承销。

全球债券:是指在全世界各主要资本市场同时大量发行,并且可以在这些市场内部和市场之间自由交易的一种国际债券。

做市商(market maker):即场外交易市场的交易商,他一方面充当经纪人,替客户服务;另一方面,又是自营商,替自己做买卖。

国际股票:是指由股票市场所在地的非居民股份公司开发的股票。

国际股票是发行人在国际资本市场上筹措长期资金的工具之一。

存托凭证(Depository Receipts,简称DR〕:又称存券收据或存股证.是指在一国证券市场流通的代表外国公一有价证券的可转让凭证,属公司融资业务范畴的金融衍生工具。

存托凭证一般代表公司股票,但有时也代表债券。

(from MBA智库百科)股票存托凭证(depository receipts,DR):是国际股票的一种特殊形式。

股票存托凭证是发型地银行开出的代表其保管的外国公司股票的凭证。

它既可以代表已在发行人国内流通交易的上市股票,也可以代表在发行人国内将上市的新股票。

美国存托凭证(American depository receipts,ADR):是在美国发行和出售的存托凭证。

它是一种以证书形式发行的可转让证书。

全球存托凭证(global depository receipts,GDRs):是在美国以外的其他国家发行和出售的存托凭证,是与美国存托凭证相似的金融工具,但是,它可以同时在全世界的股票交易所发行。

第一上市:第一上市发行既是指交易所所在地的非居民公司发行股票并在该交易所直接挂牌。

第一上市要求上市公司遵守当地的法律制度和会计标准,符合上市证券交易所的上市要求。

irs交易规则 -回复

irs交易规则-回复IRS交易规则解析:一步一步回答引言:IRS(Interest Rate Swap,利率互换)是一种金融衍生品交易。

在金融市场中,它是非常常见的一种工具,可以用来分散风险、管理利率风险以及实现利差收益。

本文将详细解析IRS的交易规则,包括交易流程、交易对象、交易机构以及风险与监管等方面内容。

一、什么是IRS?1. IRS的定义IRS是指在指定期限内,两个意向交换方以约定利率交换本金的一种合约,用来管理利率风险。

2. IRS的作用(1)分散风险:IRS可以帮助交易方通过互相交换固定利率和浮动利率,实现利差收益,从而分散风险。

(2)管理利率风险:IRS可以帮助金融机构或企业在利率波动不确定的情况下,锁定或管理利率风险。

二、IRS的交易流程1. 交易准备阶段(1)确定交易目标:交易方确定交易目标,包括期限、利率类型、本金规模等。

(2)选择交易对手方:交易方通过市场寻找合适的交易对手方,签订交易协议。

2. 协商阶段(1)商定交易条款:包括交换的利率类型、交换的本金、交换的期限等。

(2)制定交易协议:交易双方达成一致后,签订正式的交易协议。

3. 交易确认阶段(1)向第三方机构确认交易:交易双方向确认订立交易的第三方机构提交确认请求。

(2)交易确认:第三方机构确认交易,并向交易双方发送交易确认函。

4. 交割与履约阶段(1)交割:交易双方根据交易协议约定的条件,进行交换本金和利息。

(2)履约:交易双方按照交易协议的规定,履行合同义务。

三、IRS的交易对象1. 交易方交易方可以是金融机构、公司、个人等。

它们可以作为意向交换方与其他交易方进行IRS交易。

2. 意向交换方意向交换方是指有交易意向的金融机构、公司等。

意向交换方通过市场寻找合适的交易对手方进行IRS交易。

3. 交易对手方交易对手方是指与交易方进行IRS交易的另一方。

交易对手方通常是金融机构或其他有相应资质和经验的合作伙伴。

四、IRS的交易机构1. 金融机构金融机构是IRS交易的核心参与者,包括商业银行、投资银行、证券公司等。

会计专业词汇英语翻译

会计专业词汇英语翻译政治风险 political risk再开票中心 re-invoicing center现代管理会计专门方法special methods of modern management accounting现代管理会计 modern management accounting提前与延期支付 leads and lags特许权使用管理费 fees and royalties跨国资本成本的计算 the cost of capital for foreign investments 跨国运转资本会计 multinational working capital management 跨国经营企业业绩评价 multinational performance evaluation 经济风险管理 managing economic exposure交易风险管理 managing transaction exposure换算风险管理 managing translation exposure国际投资决策会计 foreign project appraisal国际投资决策会计 foreign project appraisal国际存货管理 international inventory management股利转移 dividend remittances公司内部贷款 inter-company loans冻结资金转移 repatriating blocked funds冻结资金保值 maintaining the value of blocked funds调整后的净现值 adjusted net present value配比原则 matching旅游、饮食服务企业会计 accounting of tourism and service施工企业会计 accounting of construction enterprises民航运输企业会计 accounting of civil aviation transportation enterprises企业会计 business accounting商品流通企业会计 accounting of commercial enterprises权责发生制原则 accrual basis农业会计 accounting of agricultural enterprises实现原则 realization principle历史成本原则 principle of historical cost外商投资企业会计accounting of enterprises with foreign investment通用报表 all-purpose financial statements铁路运输企业会计accounting of rail way transportation enterprises所有者权益 owners equity所有者权益 owners equity实质量于形式 substance over form修正性惯例 principle of exceptions信息系统论 information system perspective相关性原则 relevance微观会计 micro-accounting客观性原则 objectivity可比性原则 comparability谨慎性原则 prudence金融企业会计 accounting of financial institutions交通运输企业会计accounting of communication and transportation enterprises建设单位会计 accounting of construction units记账本位币 recording currency计量属性 measurement attributes及时性原则 timeliness货币计量 monetary measurement会计准则 accounting standards会计主体 accounting entity会计职业道德 accounting professional ethics会计职能 functions of accounting会计预测 accounting forecasting会计要素 accounting elements会计研究 accounting research会计学科体系 accounting science system会计学 accounting会计信息 accounting information会计任务 targets of accounting activities会计人员 accounting personnel会计确认 accounting recognition会计目标 accounting objective会计理论结构 theoretical structure of accounting 会计理论 accounting theory会计控制 accounting control会计决策 accounting decision making会计监督 accounting supervision会计假设 accounting assumption会计记录 accounting records会计计量 accounting measurement会计机构 accounting department会计环境 accounting environment会计核算 financial accounting会计管理体制 system of accounting administration 会计分期 accounting periods会计对象 accounting object会计等式 accounting equation会计本质 nature of accounting会计报表 accounting statements宏观会计 macro-accounting会计 accounting汇总报表 combination statements划分资本性支出与收益性支出原则distinguishment between capital expenditure and revenue expenditure合并报表 consolidated financial statements管理活动论 management activities perspective管理会计 management accounting管理工具论 management tool perspective股份制企业会计 accounting of stock companies公认会计原则 generally accepted accounting principle, gaap 公共会计 public accounting工业会计 accounting of industrial enterprises个别报表 individual statements高新技术企业会计 accounting of high technology enterprises 负债 liability费用 expense反馈价值 feedback value对外经济合作企业会计accounting of foreign economic cooperation enter prises对外报表 external statements对内报表 internal statements一致性原则 consistency艺术论 art perspective房地产开发企业会计 accounting of real estate enterprises邮电通信企业会计 accounting of post and telecommunication enterprises预测价值 forecast value真实与公允 true and fair view持续经营 going concern成本报表 cost statement财务会计原则 financial accounting principles财务会计概念框架 financial accounting conceptual framework 财务会计 financial accounting政府及非营利组织会计governmental and non-profit organization accounting重要性原则 materiality专用报表 special purpose financial statements资产 assets资金 funds资金运动 funds movement财务报告 financial report财务报表要素 elements of financial statements财务报表 financial statements币值稳定假设 constant-dollar assumption保险企业会计 accounting of insurance companies收入的确认 recognition of revenue公司债券发行价格 corporate bond issuing price固定资产折旧 depreciation of fixed assets可转换债券 convertible bonds公司债券利息摊销加速折旧法 accelerated depreciation methods营业外收支净额公司债券利率 interest rate on debenture应收账款出借 assignment of accounts receivable无担保债券 debenture bonds后进先出法 last-in, first-out, lifo其他货币资金应付票据贴现 discount on notes payable先进先出去 first-in, first-out缩写fifo在发建工程 constructions in process固定资产更换与改良 improvements and replacements of fixedassets实地盘存制 periodic inventory system收益总括观点 all-inclusive concept of income损益表法可变现净值法 net realizable value应付福利费基本业务利润固定资产扩建 additions of fixed assets应收账款出售 sale or factoring of accounts receivable 或有负债 contingent liability销货退回与折让 sales returns and allowances零售价格法 retail method现金折扣 cash discount特定履行法其他业务利润公司债券 bonds payable销售法 sale method应付票据 notes payable认股权 stock rights固定资产修理 repairs and maintenance of fixed assets 有担保债券 mortgage bonds销售费用 selling expenses应付股利 dividends payable应收票据 notes receivable无形资产 intangible assets收款法 collection method所得税 income tax流动负债 current liabilities生产法 production method计划成本核算废弃和生置法 retirement and replacement method 盘存法 inventory method流动资产 current assets购货折扣 purchases discounts商誉 goodwill应收账款 accounts receivable投资收益 investment income营业利润 operating income预提费用股本 capital stock公司债券偿还 redemption of bonds坏账 bad debts固定资产重估价 revaluations of fixed assets银行存款 cash in bank固定资产 fixed assets利润总额利益分配 profit distribution应计费用 accrued expense商标权 trademarks and trade names全部履行法净利润 net income应付利润 profit payable未分配利润收益债券 income bonds货币资金利息资本化 capitalization of interests公益金工程物资预付账款 advance to supplier其他应收款 other receivables现金 cash预收账款公司债券发行 corporate bond floatation应付工资 wages payable实收资本 paid-in capital盈余公积 surplus reserves管理费用土地使用权股利 dividend应交税金 taxes payable负商誉 negative goodwill费用的确认 recognition of expense短期投资 temporary investment短期借款 short-term loans递延资产 deferred charges低值易耗品当期经营观点 current operating concept of income 待摊费用待核销基建支出[旧]待处理流动资产损失待处理固定资产损失存货销售的影响 effects of inventory errors折旧[旧]折旧方法 depreciation method折旧率 depreciation rate支出 payment直线法 straight-line职工福利基金 welfare fund专项拨款【旧】专利权 patents住房基金 housing fund重置成本法 replacement costing专项物资[旧]专项资产【旧】专有技术 know-how专营权 franchises资本公积 capital reserves资产负债表 balance sheet资金占用和资金来源[旧]自然资源 natural resources存货 inventory车间经费【旧】偿债基金 sinking fund长期应付款 long-term payables长期投资 long-term investments长期借款 long-term loans长期负债 long-term liability of long-term debt财务费用 financing expenses拨定留存收益 appropriated retained earnings标准成本法 standard costing变动成本法 variable costing比例履行法包装物版权 copyrights汇总原始凭证 cumulative source document汇总记账凭证核算形式bookkeeping procedure using summary vouchers工作底稿 working paper复式记账凭证 multiple account titles voucher复式记账法 double entry bookkeeping复合分录 compound entry划线更正法 correction by drawing a straight ling汇总原始凭证 cumulative source document会计凭证 accounting documents会计科目表 chart of accounts会计科目 account title红字更正法 correction by using red ink会计核算形式 bookkeeping procedures过账 posting会计分录 accounting entry会计循环 accounting cycle会计账簿 book of accounts活页式账簿 loose-leaf book集合分配账户 clearing accounts计价对比账户 matching accounts记账方法 bookkeeping methods记账规则 recording rules记账凭证 voucher记账凭证核算形式 bookkeeping procedure using vouchers记账凭证汇总表核算形式bookkeeping procedure using categorized account summary简单分录 simple entry结算账户 settlement accounts结账 closing account结账分录 closing entry借贷记账法 debit-credit bookkeeping局部清查 partial check卡片式账簿 card book跨期摊提账户 inter-period allocation accounts累计凭证 multiple-record document联合账簿 compound book明细分类账簿 subsidiary ledger明细分类账户 subsidiary account盘存账存 inventory accounts平行登记 parallel recording全面清查 complete check日记总账 combined journal and ledger日记总账核算形式 bookkeeping procedure using summarized journal三式记账法 triple-entry bookkeeping实账户 real accounts试算表 trial balance试算平衡 trial balancing收付记账法 receipts-payment bookkeeping收款凭证 receipt voucher损益表账户 income statement accounts通用记账凭证 general purpose voucher通用日记账核算形式bookkeeping procedure using general journal外来原始凭证 source document from outside现金日记账 cash journal虚账户 nominal accounts序时账簿 book of chronological entry一次凭证 single-record document银行存款日记账 deposit journal永续盘存制 perpetual inventory system原始凭证 source document暂记账户 suspense accounts增减记账法 increase-decrease bookkeeping债权结算账户 accounts for settlement of claim债权债务结算账户 accounts for settlement of claim and debt 债务结算账户 accounts for settlement of debt账户 account账户编号 account number账户对应关系 debit-credit relationship账项调整 adjustment of account专用记账凭证 special-purpose voucher转回分录 reversing entry资金来源账户 accounts of sources of funds资产负债账户 balance sheet accounts转账凭证 transfer voucher资金运用账户 accounts of applications of funds自制原始凭证 internal source document总分类账簿 general ledger总分类账户 general account附加账户 adjunct accounts付款凭证 payment voucher分类账簿 ledger多栏式日记账核算形式bookkeeping procedure using columnar journal对账 checking对应账户 corresponding accounts定期清查 periodic checking method定期盘存制 periodic inventory system订本式账簿 bound book调整账户 adjustment accounts调整分录 adjusting journal entry单式记账凭证 single account title voucher单式记账法 single-entry bookkeeping从属账户 secondary accounts成本计算账户 costing accounts财产清查 physical inventory簿记 bookkeeping不定期清查 non-periodic checking method 补充登记法 correction by extra recording表外账户 off-balance sheet accounts备抵账户 provision accounts备抵附加账户 provision and adjunct accounts 备查账簿 memorandum。

会计专业英语词汇大全

会计专业英语词汇Accounting system 会计系统American Accounting Association 美国会计协会American Institute of CPAs 美国注册会计师协会Audit 审计Balance sheet 资产负债表Bookkeepking 簿记Cash flow prospects 现金流量预测Certificate in Internal Auditing 内部审计证书Certificate in Management Accounting 管理会计证书Certificate Public Accountant注册会计师Cost accounting 成本会计External users 外部使用者Financial accounting 财务会计Financial Accounting Standards Board 财务会计准则委员会Financial forecast 财务预测Generally accepted accounting principles 公认会计原则General-purpose information 通用目的信息Government Accounting Office 政府会计办公室Income statement 损益表Institute of Internal Auditors 内部审计师协会Institute of Management Accountants 管理会计师协会Integrity 整合性Internal auditing 内部审计Internal control structure 内部控制结构Internal Revenue Service 国内收入署Internal users 内部使用者Management accounting 管理会计Return of investment 投资回报Return on investment 投资报酬Securities and Exchange Commission 证券交易委员会Statement of cash flow 现金流量表Statement of financial position 财务状况表Tax accounting 税务会计Accounting equation 会计等式Articulation 勾稽关系Assets 资产Business entity 企业个体Capital stock 股本Corporation 公司Cost principle 成本原则Creditor 债权人Deflation 通货紧缩Disclosure 批露Expenses 费用Financial statement 财务报表Financial activities 筹资活动Going-concern assumption 持续经营假设Inflation 通货膨涨Investing activities 投资活动Liabilities 负债Negative cash flow 负现金流量Operating activities 经营活动Owner's equity 所有者权益Partnership 合伙企业Positive cash flow 正现金流量Retained earning 留存利润Revenue 收入Sole proprietorship 独资企业Solvency 清偿能力Stable-dollar assumption 稳定货币假设Stockholders 股东Stockholders' equity 股东权益Window dressing 门面粉饰Account 帐政治风险political risk再开票中心re-invoicing center现代管理会计专门方法 special methods of modern management accounting现代管理会计modern management accounting提前与延期支付Leads and Lags特许权使用管理费fees and royalties跨国资本成本的计算the cost of capital for foreign investments跨国运转资本会计multinational working capital management跨国经营企业业绩评价multinational performance evaluation经济风险管理managing economic exposure交易风险管理managing transaction exposure换算风险管理managing translation exposure国际投资决策会计foreign project appraisal国际存货管理international inventory management股利转移dividend remittances公司内部贷款inter-company loans冻结资金转移repatriating blocked funds冻结资金保值maintaining the value of blocked funds调整后的净现值adjusted net present value配比原则matching旅游、饮食服务企业会计accounting of tourism and service施工企业会计accounting of construction enterprises民航运输企业会计accounting of civil aviation transportation enterprises企业会计business accounting商品流通企业会计accounting of commercial enterprises权责发生制原则accrual basis农业会计accounting of agricultural enterprises实现原则realization principle历史成本原则principle of historical cost外商投资企业会计 accounting of enterprises with foreign investment 通用报表all-purpose financial statements铁路运输企业会计accounting of rail way transportation enterprises所有者权益owners equity实质量于形式substance over form修正性惯例principle of exceptions信息系统论information system perspective相关性原则relevance微观会计micro-accounting客观性原则objectivity可比性原则comparability谨慎性原则prudence金融企业会计accounting of financial institutions交通运输企业会计accounting of communication and transportation enterprises建设单位会计accounting of construction units记账本位币recording currency计量属性measurement attributes及时性原则timeliness货币计量monetary measurement会计准则accounting standards会计主体accounting entity会计职业道德accounting professional ethics会计职能functions of accounting会计预测accounting forecasting会计要素accounting elements会计研究accounting research会计学科体系accounting science system会计学accounting会计信息accounting information会计任务targets of accounting activities会计人员accounting personnel会计确认accounting recognition。

国际金融 International Finance Test Bank_11

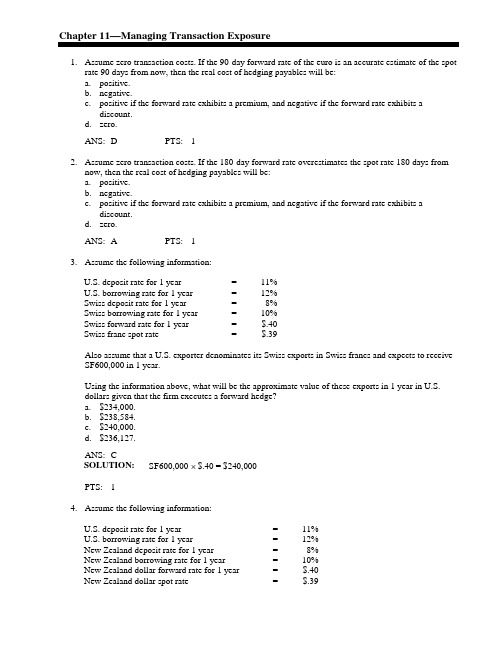

Chapter 11—Managing Transaction Exposure1. Assume zero transaction costs. If the 90-day forward rate of the euro is an accurate estimate of the spotrate 90 days from now, then the real cost of hedging payables will be:a. positive.b. negative.c. positive if the forward rate exhibits a premium, and negative if the forward rate exhibits adiscount.d. zero.ANS: D PTS: 12. Assume zero transaction costs. If the 180-day forward rate overestimates the spot rate 180 days fromnow, then the real cost of hedging payables will be:a. positive.b. negative.c. positive if the forward rate exhibits a premium, and negative if the forward rate exhibits adiscount.d. zero.ANS: A PTS: 13. Assume the following information:U.S. deposit rate for 1 year = 11%U.S. borrowing rate for 1 year = 12%Swiss deposit rate for 1 year = 8%Swiss borrowing rate for 1 year = 10%Swiss forward rate for 1 year = $.40Swiss franc spot rate = $.39Also assume that a U.S. exporter denominates its Swiss exports in Swiss francs and expects to receive SF600,000 in 1 year.Using the information above, what will be the approximate value of these exports in 1 year in U.S.dollars given that the firm executes a forward hedge?a. $234,000.b. $238,584.c. $240,000.d. $236,127.ANS: CSOLUTION: SF600,000 $.40 = $240,000PTS: 14. Assume the following information:U.S. deposit rate for 1 year = 11%U.S. borrowing rate for 1 year = 12%New Zealand deposit rate for 1 year = 8%New Zealand borrowing rate for 1 year = 10%New Zealand dollar forward rate for 1 year = $.40New Zealand dollar spot rate = $.39Also assume that a U.S. exporter denominates its New Zealand exports in NZ$ and expects to receive NZ$600,000 in 1 year. You are a consultant for this firm.Using the information above, what will be the approximate value of these exports in 1 year in U.S.dollars given that the firm executes a money market hedge?a. $238,584.b. $240,000.c. $234,000.d. $236,127.ANS: DSOLUTION:1. Borrow NZ$545,455 (NZ$600,000/1.1) = NZ$545,455.2. Convert NZ$545,455 to $212,727 (at $.39 per NZ$).3. Invest $212,727 to accumulate $236,127 ($212,727 1.11) = $236,127.PTS: 15. An example of cross-hedging is:a. find two currencies that are highly positively correlated; match the payables of the onecurrency to the receivables of the other currency.b. use the forward market to sell forward whatever currencies you will receive.c. use the forward market to buy forward whatever currencies you will receive.d. B and CANS: A PTS: 16. Which of the following reflects a hedge of net receivables in British pounds by a U.S. firm?a. purchase a currency put option in British pounds.b. sell pounds forward.c. borrow U.S. dollars, convert them to pounds, and invest them in a British pound deposit.d. A and BANS: D PTS: 17. Which of the following reflects a hedge of net payables on British pounds by a U.S. firm?a. purchase a currency put option in British pounds.b. sell pounds forward.c. sell a currency call option in British pounds.d. borrow U.S. dollars, convert them to pounds, and invest them in a British pound deposit.e. A and BANS: D PTS: 18. If Lazer Co. desired to lock in the maximum it would have to pay for its net payables in euros butwanted to be able to capitalize if the euro depreciates substantially against the dollar by the time payment is to be made, the most appropriate hedge would be:a. a money market hedge.b. purchasing euro put options.c. a forward purchase of euros.d. purchasing euro call options.e. selling euro call options.ANS: D PTS: 19. If Salerno Inc. desired to lock in a minimum rate at which it could sell its net receivables in Japaneseyen but wanted to be able to capitalize if the yen appreciates substantially against the dollar by the time payment arrives, the most appropriate hedge would be:a. a money market hedge.b. a forward sale of yen.c. purchasing yen call options.d. purchasing yen put options.e. selling yen put options.ANS: D PTS: 110. The real cost of hedging payables with a forward contract equals:a. the nominal cost of hedging minus the nominal cost of not hedging.b. the nominal cost of not hedging minus the nominal cost of hedging.c. the nominal cost of hedging divided by the nominal cost of not hedging.d. the nominal cost of not hedging divided by the nominal cost of hedging.ANS: A PTS: 111. From the perspective of Detroit Co., which has payables in Mexican pesos and receivables in Canadiandollars, hedging the payables would be most desirable if the expected real cost of hedging payables is ____, and hedging the receivables would be most desirable if the expected real cost of hedgingreceivables is ____.a. negative; positiveb. zero; positivec. zero; zerod. positive; negativee. negative; negativeANS: E PTS: 112. Use the following information to calculate the dollar cost of using a money market hedge to hedge200,000 pounds of payables due in 180 days. Assume the firm has no excess cash. Assume the spot rate of the pound is $2.02, the 180-day forward rate is $2.00. The British interest rate is 5%, and the U.S. interest rate is 4% over the 180-day period.a. $391,210.b. $396,190.c. $388,210.d. $384,761.e. none of the aboveANS: ESOLUTION:1. Need to invest £190,476 (£200,000/1.05) = £190,476.2. Need to exchange $384,762 to obtain the £190,476 (£190,476 ⨯ $2.02) = $384,762.3. At the end of 180 days, need $400,152 to repay loan ($384,762 ⨯ 1.04) = $400,152.PTS: 113. Assume that Cooper Co. will not use its cash balances in a money market hedge. When decidingbetween a forward hedge and a money market hedge, it ____ determine which hedge is preferable before implementing the hedge. It ____ determine whether either hedge will outperform an unhedged strategy before implementing the hedge.a. can; canb. can; cannotc. cannot; cand. cannot; cannotANS: B PTS: 114. Foghat Co. has 1,000,000 euros as receivables due in 30 days, and is certain that the euro willdepreciate substantially over time. Assuming that the firm is correct, the ideal strategy is to:a. sell euros forward.b. purchase euro currency put options.c. purchase euro currency call options.d. purchase euros forward.e. remain unhedged.ANS: A PTS: 115. Spears Co. will receive SF1,000,000 in 30 days. Use the following information to determine the totaldollar amount received (after accounting for the option premium) if the firm purchases and exercises a put option:Exercise price = $.61Premium = $.02Spot rate = $.60Expected spot rate in 30 days = $.5630-day forward rate = $.62a. $630,000.b. $610,000.c. $600,000.d. $590,000.e. $580,000.ANS: DSOLUTION: ($.61 - $.02) ⨯ SF1,000,000 = $590,000PTS: 116. A ____ involves an exchange of currencies between two parties, with a promise to re-exchangecurrencies at a specified exchange rate and future date.a. long-term forward contractb. currency option contractc. parallel loand. money market hedgeANS: C PTS: 117. If interest rate parity exists and transactions costs are zero, the hedging of payables in euros with aforward hedge will ____.a. have the same result as a call option hedge on payablesb. have the same result as a put option hedge on payablesc. have the same result as a money market hedge on payablesd. require more dollars than a money market hedgee. A and DANS: C PTS: 118. Assume that Parker Company will receive SF200,000 in 360 days. Assume the following interestrates:U.S. Switzerland360-day borrowing rate 7% 5%360-day deposit rate 6% 4%Assume the forward rate of the Swiss franc is $.50 and the spot rate of the Swiss franc is $.48. IfParker Company uses a money market hedge, it will receive ____ in 360 days.a. $101,904b. $101,923c. $98,769d. $96,914e. $92,307ANS: DSOLUTION:1. Borrow SF190,476 (SF200,000/1.05) = SF190,476.2. Convert SF190,476 to $91,428 (SF190,476 ⨯ $.48) = $91,428.3. Invest $91,428 at 6% to accumulate $96,914 ($91,428 ⨯ 1.06) = $96,914.PTS: 119. The forward rate of the Swiss franc is $.50. The spot rate of the Swiss franc is $.48. The followinginterest rates exist:U.S. Switzerland360-day borrowing rate 7% 5%360-day deposit rate 6% 4%You need to purchase SF200,000 in 360 days. If you use a money market hedge, the amount of dollars you need in 360 days is:a. $101,904.b. $101,923.c. $98,770.d. $96,914.e. $92,307.ANS: CSOLUTION:1. Need to invest SF192,308 (SF200,000/1.04) = SF192,308.2. Need to borrow $92,308 to exchange for SF192,308 (SF192,308 ⨯ $.48) = $92,308.3. At the end of 360 days, need $98,769 to repay the loan ($92,308 ⨯ 1.07) = $98,770.PTS: 120. Your company will receive C$600,000 in 90 days. The 90-day forward rate in the Canadian dollar is$.80. If you use a forward hedge, you will:a. receive $750,000 today.b. receive $750,000 in 90 days.c. pay $750,000 in 90 days.d. receive $480,000 today.e. receive $480,000 in 90 days.ANS: ESOLUTION: C$600,000 ⨯ $0.80 = $480,000PTS: 121. A call option exists on British pounds with an exercise price of $1.60, a 90-day expiration date, and apremium of $.03 per unit. A put option exists on British pounds with an exercise price of $1.60, a 90-day expiration date, and a premium of $.02 per unit. You plan to purchase options to cover your future receivables of 700,000 pounds in 90 days. You will exercise the option in 90 days (if at all).You expect the spot rate of the pound to be $1.57 in 90 days. Determine the amount of dollars to be received, after deducting payment for the option premium.a. $1,169,000.b. $1,099,000.c. $1,106,000.d. $1,143,100.e. $1,134,000.ANS: CSOLUTION: ($1.60 - $.02) ⨯ £700,000 = $1,106,000PTS: 122. Assume that Smith Corporation will need to purchase 200,000 British pounds in 90 days. A call optionexists on British pounds with an exercise price of $1.68, a 90-day expiration date, and a premium of $.04. A put option exists on British pounds, with an exercise price of $1.69, a 90-day expiration date, and a premium of $.03. Smith Corporation plans to purchase options to cover its future payables. It will exercise the option in 90 days (if at all). It expects the spot rate of the pound to be $1.76 in 90 days. Determine the amount of dollars it will pay for the payables, including the amount paid for the option premium.a. $360,000.b. $338,000.c. $332,000.d. $336,000.e. $344,000.ANS: ESOLUTION: ($1.68 + $.04) ⨯ £200,000 = $344,000PTS: 123. Assume that Kramer Co. will receive SF800,000 in 90 days. Today's spot rate of the Swiss franc is$.62, and the 90-day forward rate is $.635. Kramer has developed the following probabilitydistribution for the spot rate in 90 days:$.64 40%$.65 30%The probability that the forward hedge will result in more dollars received than not hedging is:a. 10%.b. 20%.c. 30%.d. 50%.e. 70%.ANS: CSOLUTION: The forward hedge will result in more dollars if the spot rate is less than theforward rate, which is true in the first two cases.PTS: 124. Assume that Jones Co. will need to purchase 100,000 Singapore dollars (S$) in 180 days. Today's spotrate of the S$ is $.50, and the 180-day forward rate is $.53. A call option on S$ exists, with an exercise price of $.52, a premium of $.02, and a 180-day expiration date. A put option on S$ exists, with an exercise price of $.51, a premium of $.02, and a 180-day expiration date. Jones has developed the following probability distribution for the spot rate in 180 days:Possible Spot Ratein 90 Days Probability$.48 10%$.53 60%$.55 30%The probability that the forward hedge will result in a higher payment than the options hedge is ____ (include the amount paid for the premium when estimating the U.S. dollars required for the options hedge).a. 0%b. 10%c. 30%d. 40%e. 70%ANS: BSOLUTION: There is a 10% probability that the call option will not be exercised. In thatcase, Jones will pay $.48 ⨯ S$100,000 = $48,000, which is less than theamount paid with the forward hedge ($.53 ⨯ S$100,000 = $53,000).PTS: 125. Assume that Patton Co. will receive 100,000 New Zealand dollars (NZ$) in 180 days. Today's spotrate of the NZ$ is $.50, and the 180-day forward rate is $.51. A call option on NZ$ exists, with an exercise price of $.52, a premium of $.02, and a 180-day expiration date. A put option on NZ$ exists with an exercise price of $.51, a premium of $.02, and a 180-day expiration date. Patton Co. hasdeveloped the following probability distribution for the spot rate in 180 days:$.55 30%The probability that the forward hedge will result in more U.S. dollars received than the options hedge is ____ (deduct the amount paid for the premium when estimating the U.S. dollars received on the options hedge).a. 10%b. 30%c. 40%d. 70%e. none of the aboveANS: DSOLUTION: The put option will be exercised in the first two cases, resulting in an amountreceived per unit of $.51 - $.02 = $.49. Thus, the forward hedge will result inmore U.S. dollars received ($.51 per unit).PTS: 126. The ____ hedge is not a technique to eliminate transaction exposure discussed in your text.a. indexb. futuresc. forwardd. money markete. currency optionANS: A PTS: 127. Money Corp. frequently uses a forward hedge to hedge its Malaysian ringgit (MYR) receivables. Forthe next month, Money has identified its net exposure to the ringgit as being MYR1,500,000. The 30-day forward rate is $.23. Furthermore, Money's financial center has indicated that the possiblevalues of the Malaysian ringgit at the end of next month are $.20 and $.25, with probabilities of .30 and .70, respectively. Based on this information, the revenue from hedging minus the revenue from not hedging receivables is____.a. $0.b. -$7,500.c. $7,500.d. none of the aboveANS: CSOLUTION: RCH(1) = (MYR1,500,000 ⨯ $0.20) - (MYR1,500,000 ⨯ $0.23)= -$45,000RCH(2) = (MYR1,500,000 ⨯ $0.25) - (MYR1,500,000 ⨯ $0.23)= $30,000E[RCH] = (.30)(-45,000) + (.7)(30,000) = 7,5000PTS: 128. Hanson Corp. frequently uses a forward hedge to hedge its British pound (£) payables. For the nextquarter, Hanson has identified its net exposure to the pound as being £1,000,000. The 90-day forward rate is $1.50. Furthermore, Hanson's financial center has indicated that the possible values of theBritish pound at the end of next quarter are $1.57 and $1.59, with probabilities of .50 and .50,respectively. Based on this information, what is the expected real cost of hedging payables?a. $80,000.b. -$80,000.c. $1,570,000.d. $1,580,000.ANS: BSOLUTION: RCH(1) = (£1,000,000 ⨯ $1.50) - (£1,000,000 ⨯ $1.57) = -$70,000RCH(2) = (£1,000,000 ⨯ $1.50) - (£1,000,000 ⨯ $1.59) = -$90,000E[RCH] = (.50)(-70,000) + (.50)(-$90,000) = -$80,000PTS: 1Exhibit 11-1U.S. Jordan360-day borrowing rate 6% 5%360-day deposit rate 5% 4%29. Refer to Exhibit 11-1. Perkins Corp. will receive 250,000 Jordanian dinar (JOD) in 360 days. Thecurrent spot rate of the dinar is $1.48, while the 360-day forward rate is $1.50. How much will Perkins receive in 360 days from implementing a money market hedge (assume any receipts before the date of the receivable are invested)?a. $377,115.b. $373,558.c. $363,019.d. $370,000.ANS: DSOLUTION:1. Borrow JOD238,095.24 (JOD250,000/1.05) = JOD238,095.24.2. Convert JOD238,095.24 to $352,380.95 (JOD238,095.24 ⨯ $1.48) = $352,380.95.3. Invest $352,380.95 at 5% to accumulate $370,000 ($352,280.95 ⨯ 1.05) = $370,000.PTS: 130. Refer to Exhibit 11-1. Pablo Corp. will need 150,000 Jordanian dinar (JOD) in 360 days. The currentspot rate of the dinar is $1.48, while the 360-day forward rate is $1.46. What is Pablo's cost fromimplementing a money market hedge (assume Pablo does not have any excess cash)?a. $224,135.b. $226,269.c. $224,114.d. $223,212.ANS: BSOLUTION:1. Need to invest JOD144,230.76 (JOD150,000/1.04) = JOD144,230.76.2. Need to convert $213,461.52 to obtain the JOD144,230.76 dinar (JOD144,230.76 ⨯ $1.48)= $213,461.52.3. At the end of 360 days, need $226,269.22 ($213,461.52 ⨯ 1.06) = $226,269.21.PTS: 131. Lorre Company needs 200,000 Canadian dollars (C$) in 90 days and is trying to determine whether ornot to hedge this position. Lorre has developed the following probability distribution for the Canadian dollar:Possible Value ofCanadian Dollar in 90 Days Probability$0.54 15%0.57 25%0.58 35%0.59 25%The 90-day forward rate of the Canadian dollar is $.575, and the expected spot rate of the Canadian dollar in 90 days is $.55. If Lorre implements a forward hedge, what is the probability that hedging will be more costly to the firm than not hedging?a. 40%.b. 60%.c. 15%.d. 85%.ANS: ASOLUTION: Since Lorre locks into the $.575 with a forward contract, the first two caseswould have been cheaper had Lorre not hedged (15% + 25% = 40%).PTS: 132. Quasik Corporation will be receiving 300,000 Canadian dollars (C$) in 90 days. Currently, a 90-daycall option with an exercise price of $.75 and a premium of $.01 is available. Also, a 90-day put option with an exercise price of $.73 and a premium of $.01 is available. Quasik plans to purchase options to hedge its receivable position. Assuming that the spot rate in 90 days is $.71, what is the net amount received from the currency option hedge?a. $219,000.b. $222,000.c. $216,000.d. $213,000.ANS: CSOLUTION: ($.73 - $.01) ⨯ 300,000 = $216,000.PTS: 133. FAB Corporation will need 200,000 Canadian dollars (C$) in 90 days to cover a payable position.Currently, a 90-day call option with an exercise price of $.75 and a premium of $.01 is available. Also,a 90-day put option with an exercise price of $.73 and a premium of $.01 is available. FAB plans topurchase options to hedge its payable position. Assuming that the spot rate in 90 days is $.71, what is the net amount paid, assuming FAB wishes to minimize its cost?a. $144,000.b. $148,000.c. $152,000.d. $150,000.ANS: ASOLUTION: ($.71 + $.01) 200,000 = $144,000. Note: the call option is not exercisedsince the spot rate is less than the exercise price.PTS: 134. You are the treasurer of Arizona Corporation and must decide how to hedge (if at all) futurereceivables of 350,000 Australian dollars (A$) 180 days from now. Put options are available for a premium of $.02 per unit and an exercise price of $.50 per Australian dollar. The forecasted spot rate of the Australian dollar in 180 days is:Future Spot Rate Probability$.46 20%$.48 30%$.52 50%The 90-day forward rate of the Australian dollar is $.50.What is the probability that the put option will be exercised (assuming Arizona purchased it)?a. 0%.b. 80%.c. 50%.d. none of the aboveANS: CSOLUTION: Arizona will exercise when the exercise price is greater than the future spot(20% + 30% = 50%).PTS: 135. If interest rate parity exists, and transaction costs do not exist, the money market hedge will yield thesame result as the ____ hedge.a. put optionb. forwardc. call optiond. none of the aboveANS: B PTS: 136. Which of the following is the least effective way of hedging exposure in the long run?a. long-term forward contract.b. currency swap.c. parallel loan.d. money market hedge.ANS: D PTS: 137. When a perfect hedge is not available to eliminate transaction exposure, the firm may considermethods to at least reduce exposure, such as ____.a. leadingb. laggingc. cross-hedgingd. currency diversificatione. all of the aboveANS: E PTS: 138. Sometimes the overall performance of an MNC may already be insulated by offsetting effects betweensubsidiaries and it may not be necessary to hedge the position of each individual subsidiary.a. Trueb. FalseANS: T PTS: 139. To hedge a ____ in a foreign currency, a firm may ____ a currency futures contract for that currency.a. receivable; purchaseb. payable; sellc. payable; purchased. none of the aboveANS: C PTS: 140. A forward contract hedge is very similar to a futures contract hedge, except that ____ contracts arecommonly used for ____ transactions.a. forward; smallb. futures; largec. forward; larged. none of the aboveANS: C PTS: 141. Celine Co. will need €500,000 in 90 days to pay for German imports. Today's 90-day forward rate ofthe euro is $1.07. There is a 40 percent chance that the spot rate of the euro in 90 days will be $1.02, and a 60 percent chance that the spot rate of the euro in 90 days will be $1.09. Based on thisinformation, the expected value of the real cost of hedging payables is $____.a. -35,000b. 25,000c. -1,000d. 1,000ANS: DSOLUTION: E[RCH p] = -$35,000 ⨯ 0.40 + $25,000 ⨯ 0.60 = $1,000PTS: 142. In a forward hedge, if the forward rate is an accurate predictor of the future spot rate, the real cost ofhedging payables will be:a. highly positive.b. highly negative.c. zero.d. none of the aboveANS: C PTS: 143. If an MNC is hedging various currencies, it should measure the real cost of hedging in each currencyas a dollar amount for comparison purposes.a. Trueb. FalseANS: F PTS: 144. Samson Inc. needs €1,000,000 in 30 days. Samson can earn 5 percent annualized on a German security.The current spot rate for the euro is $1.00. Samson can borrow funds in the U.S. at an annualizedinterest rate of 6 percent. If Samson uses a money market hedge, how much should it borrow in the U.S.?a. $952,381.b. $995,851.c. $943,396.d. $995,025.ANS: BSOLUTION: 1,000,000/[1 + (5% ⨯ 30/360) = $995,851PTS: 145. Blake Inc. needs €1,000,000 in 30 days. It can earn 5 percent annualized on a Ge rman security. Thecurrent spot rate for the euro is $1.00. Blake can borrow funds in the U.S. at an annualized interest rate of 6 percent. If Blake uses a money market hedge to hedge the payable, what is the cost ofimplementing the hedge?a. $1,000,000.b. $1,055,602.c. $1,000,830.d. $1,045,644.ANS: CSOLUTION:1. Borrow $995,851 from a U.S. bank (€1,000,000 ⨯ $1.00 ⨯ [1 + (.05 ⨯ 30/360)]2. Convert $995,851 to €995,851, given the exchange rate of $1.00 per euro.3. Use the euros to purchase a German security that offers 0.42% interest over 30 days.4. Repay the U.S. loan in 30 days, plus interest; the amount owed is $1,000,830 (computed as$995,851 ⨯ [1 + (.06 ⨯ 30/360)]).PTS: 146. Since the results of both a money market hedge and a forward hedge are known beforehand, an MNCcan implement the one that is more feasible.a. Trueb. FalseANS: T PTS: 147. If interest rate parity exists, the forward hedge will always outperform the money market hedge.a. Trueb. FalseANS: F PTS: 148. To hedge a contingent exposure, in which an MNC's exposure is contingent on a specific eventoccurring, the appropriate hedge would be a(n) ____ hedge.a. money marketb. futuresc. forwardd. optionsANS: D PTS: 149. A ____ is not normally used for hedging long-term transaction exposure.a. long-term forward contactb. futures contractc. currency swapd. parallel loanANS: B PTS: 150. The ____ does not represent an obligation.a. long-term forward contractb. currency swapc. parallel loand. currency optionANS: D PTS: 151. Hedging the position of individual subsidiaries is generally necessary, even if the overall performanceof the MNC is already insulated by the offsetting positions between subsidiaries.a. Trueb. FalseANS: F PTS: 152. If an MNC is extremely risk-averse, it may decide to hedge even though its hedging analysis indicatesthat remaining unhedged will probably be less costly than hedging.a. Trueb. FalseANS: T PTS: 153. A money market hedge involves taking a money market position to cover a future payables orreceivables position.a. Trueb. FalseANS: T PTS: 154. To hedge a payable position with a currency option hedge, an MNC would write a call option.a. Trueb. FalseANS: F PTS: 155. MNCs generally do not need to hedge because shareholders can hedge their own risk.a. Trueb. FalseANS: F PTS: 156. Currency futures are very similar to forward contracts, except that they are standardized and are moreappropriate for firms that prefer to hedge in smaller amounts.a. Trueb. FalseANS: T PTS: 157. To hedge payables with futures, an MNC would sell futures; to hedge receivables with futures, anMNC would buy futures.a. Trueb. FalseANS: F PTS: 158. When the real cost of hedging is positive, this implies that hedging was more favorable than nothedging.a. Trueb. FalseANS: F PTS: 159. A futures hedge involves taking a money market position to cover a future payables or receivablesposition.a. Trueb. FalseANS: F PTS: 160. If interest rate parity (IRP) exists, then the money market hedge will yield the same result as theoptions hedge.a. Trueb. FalseANS: F PTS: 161. The price at which a currency put option allows the holder to sell a currency is called the settlementprice.a. Trueb. FalseANS: F PTS: 162. A put option essentially represents two swaps of currencies, one swap at the inception of the loancontract and another swap at a specified date in the future.a. Trueb. FalseANS: F PTS: 163. The hedging of a foreign currency for which no forward contract is available with a highly correlatedcurrency for which a forward contract is available is referred to as cross-hedging.a. Trueb. FalseANS: T PTS: 164. The exact cost of hedging with call options (as measured in the text) is not known with certainty at thetime that the options are purchased.a. Trueb. FalseANS: T PTS: 165. The tradeoff when considering alternative call options to hedge a currency position is that an MNC canobtain a call option with a higher exercise price, but would have to pay a higher premium.a. Trueb. FalseANS: F PTS: 166. When comparing the forward hedge to the options hedge, the MNC can easily determine which hedgeis more desirable, because the cost of each hedge can be determined with certainty.a. Trueb. FalseANS: F PTS: 167. When comparing the forward hedge to the money market hedge, the MNC can easily determine whichhedge is more desirable, because the cost of each hedge can be determined with certainty.a. Trueb. FalseANS: T PTS: 168. Assume zero transaction costs. If the 90-day forward rate of the euro underestimates the spot rate 90days from now, then the real cost of hedging payables will be:a. positive.b. negative.c. positive if the forward rate exhibits a premium, and negative if the forward rate exhibits adiscount.d. zero.ANS: B PTS: 169. Johnson Co. has 1,000,000 euros as payables due in 30 days, and is certain that euro is going toappreciate substantially over time. Assuming the firm is correct, the ideal strategy is to:a. sell euros forwardb. purchase euro currency put options.c. purchase euro currency call options.d. purchase euros forward.e. remain unhedged.ANS: D PTS: 1。

交易员如何管理风险

交易员如何管理风险在金融市场中,风险是无法避免的,尤其对于交易员来说,管理风险是至关重要的。

一个优秀的交易员应该具备良好的风险管理能力,以便在市场波动时能够保护自己和客户的利益。

本文将探讨交易员如何管理风险的几个关键方面。

一、制定有效的风险管理策略交易员需要制定一套有效的风险管理策略,以便在面临市场风险时能够做出明智的决策。

这些策略应该包括风险评估、头寸管理、资金管理等要素。

风险评估是交易员首先要做的事情,他们需要评估每个交易的潜在风险并制定相应的止损点。

头寸管理是指交易员如何分配交易头寸,平衡不同市场的风险。

资金管理则是关注如何合理利用资金,控制风险的大小。

通过制定有效的风险管理策略,交易员能够在保护资金的同时,寻求更多的盈利机会。

二、密切关注市场动态交易员需要密切关注市场动态,并及时更新自己的交易策略。

市场变化是随时发生的,而且往往是突然发生的。

只有交易员通过持续地跟踪市场,了解市场的走势和影响因素,才能够做出正确的决策。

他们应该关注相关新闻、经济指标和其他市场参与者的言论,同时也要学会技术分析和基本面分析等方法,以增加对市场的准确预判能力。

三、建立有效的风险监控系统交易员需要建立一个有效的风险监控系统,通过监控和控制交易风险。

这个系统应该能够实时监测市场价格、交易头寸和资金状况等多个方面的数据,并及时发出警报。

交易员可以利用不同的工具和技术来建立风险监控系统,如设置止损单、利用交易软件的风险管理功能等。

有了一个有效的风险监控系统,交易员可以及时调整交易策略,降低潜在风险。

四、培养良好的心态和纪律管理风险需要具备良好的心态和纪律。

交易员应该保持冷静、理性,不被市场情绪所左右。

他们应该坚守自己的交易计划和策略,不随意更改。

同时,交易员也要学会接受失败,不断总结经验教训,以进一步提高自己的风险管理能力。

纪律性是交易员成功的关键之一,只有严格遵守纪律,不偏离交易规则,才能有效地管理风险。

五、不断学习和改进金融市场是一个不断变化的领域,交易员需要不断学习和改进自己的技能。

交易风险

交易风险百科名片交易风险(Transaction Exposure)一个国际企业组织的全部活动中,即在它的经营活动过程、结果、预期经营收益中,都存在着由于外汇汇率变化而引起的外汇风险,在经营活动中的风险为交易风险(Transaction Exposure),在经营活动结果中的风险为会计风险(Accounting Exposure)预期经营收益的风险为经济风险(Economic Exposure)。

目录具体内容交易风险指在约定以外币计价成交的交易过程中,由于结算时的交易风险汇率与交易发生时即签订合同时的汇率不同而引起收益或亏损的风险。

这些风险包括:1、以即期或延期付款为支付条件的商品或劳务的进出口,在货物装运和劳务提供后,而货款或劳务费用尚未收付前,外汇汇率变化所发生的风险。

2、以外币计价的国际信贷活动,在债权债务未清偿前所存在的汇率风险。

例如:某项目借入是日元,到期归还的也应是日元。

而该项目产生效益后收到的是美元。

若美元对日元汇率猛跌,该项目要比原计划多花许多美元,才能兑成日元归还本息,结果造成亏损。

3、向外筹资中的汇率风险。

借入一种外币而需要换成另一种外币使用,则筹资人将承受借入货币与使用货币之间汇率变动的风险。

4、待履行的远期外汇合同,约定汇率和到期即期汇率变动而产生的风险。

形成原因交易风险是未了结的债权债务在汇率变动后,进行外汇交割清算时出现的风险。

这些债权债务在汇率变动前已发生,但在汇率变动后才清算。

汇率制度体系是外汇交易风险产生的直接原因。

固定汇率体制将风险给屏蔽了,而浮动汇率体制增加了未来货币走势的不确定性,扩大了风险敞口。

外汇风险一般包括两个因素:货币和时间。

如果没有两种不同货币间的兑换或折算,也就不存在汇率波动所引起的外汇风险。

同时,汇率和利率的变化总是与时间期限相对应,没有时间因素也就无外汇风险可言。

经济主体帐款收付与最后清算日的时间跨度越大,汇率波动的幅度可能越大,货币间的折算风险也就越大。

财务风险管理中的外汇风险

财务风险管理中的外汇风险外汇风险是指在国际贸易和投资活动中,由于汇率波动而导致的交易成本和价值变动的风险。

随着全球经济一体化的推进,越来越多的企业参与国际贸易,外汇风险管理成为了他们不可忽视的问题。

本文将讨论财务风险管理中的外汇风险,并探讨有效的风险管理策略。

一、外汇风险的类型在财务风险管理中,外汇风险主要表现为交易风险、转换风险和经济风险三种类型。

1. 交易风险交易风险是指企业进行跨境货物或服务交易时,由于汇率波动导致的交易成本变动的风险。

举例来说,如果一个中国企业与美国企业进行跨境贸易,合同金额为100万美元,若在签约时1美元兑换人民币为6.5元,但交易发生后汇率变为1美元兑换人民币为6.8元,那么该企业将面临巨大的交易风险。

2. 转换风险转换风险是指企业拥有外汇资产或负债,在将其转化为本国货币时由于汇率波动导致的价值变动的风险。

例如,某企业持有美元现金100万元,若在兑换时汇率为1美元兑换人民币为6.5元,但在兑换时汇率变为1美元兑换人民币为6.2元,那么企业将损失30000元人民币。

3. 经济风险经济风险是指企业由于国际贸易和投资活动中汇率变动导致的影响其市场竞争力和盈利能力的风险。

当企业的产品或服务价格受到汇率波动的影响时,就会发生经济风险。

例如,一个中国企业出口产品到美国市场,在人民币升值的情况下,产品价格将上升,从而影响其在美国市场的竞争力。

二、外汇风险管理策略为了降低外汇风险对企业经营的不利影响,企业可以采取一系列的风险管理策略。

1. 使用远期合同远期合同是一种外汇风险管理工具,它允许企业以事先约定的汇率购买或销售外汇,从而规避由于汇率波动导致的交易风险和转换风险。

举例来说,如果某企业预计在未来一年将需要购买100万美元的外汇,那么它可以与银行签订一份100万美元的远期购汇合同,在未来一年内以固定的汇率购买美元,从而规避汇率波动风险。

2. 多元化经营多元化经营是指企业通过扩大市场和产品的范围,使其业务分布在多个国家和地区,从而可以分散外汇风险。

最新会计专业科目英语名称

会计专业科目英语名称资产负债表:balance sheet损益表:income statement利润分配表:profit distribution statement<中国注册会计师独立审计准则>:the independent auditing standard for chinese certified public accountants会计报表:financial statement在抽查的基础上:on a test basis主任会计师或授权副主任会计师:chief accountant or authorized assistant chief accountant中国注册会计师:chinese certified public accountant ccpa无钢印无效:shall not be valid without bearing the embossing seal年初数,年末数:opening amounting\ closing amounting资产负债表:balance sheet流动资产:current assets货币资金:cash短期、长期投资:short-term、long-term investment应收票据:notes receivable应收账款:account receivable减:坏账准备:less: provision for bad debt应收账款净额:net value of account receivable预付账款:advance to supplier应收出口退税:receivable drawback for export应收补贴款: receivable subsidy其他应收款:other receivable存货:inventories待转其他业务支出:other business expense to be transferred待摊费用:prepaid expense待处理流动资产净损失:net loss of current assets to be settled一年内到期的长期债券投资:long-term bonds investment due in 1 year 其他流动资产:other current assets流动资产合计:total current assets固定资产:fixed assets固定资产原价:original value of fixed assets累计折旧:accumulated depreciation固定资产净值:net value of fixed assets固定资产清理:disposal of fixed assets在建工程:construction in process待处理固定资产净损失:net loss of fixed assets to be settled 固定资产合计:total fixed assets无形资产及递延资产:intangible assets & deferred assets递延税项目:deferred tax负债及所有者权益:liabilities & owner’s equity流动负债:current liabilities短期/长期借款:short-term/long-term loan应付票据:notes payable预收账款:advance from clients其他应付款:other payable应付工资:accrued payroll应付福利费:welfare payable应交税金/应付利润:tax/ profits payable其他应交款:unpaid others预提费用:accrued expense一年内到期的长期负债:long-term liabilities due in 1 year 应付债券:bonds payable长期应付款:long-term payable实收资本:paid-in capital资本公积:capital accumulation盈余公积:surplus accumulation其中:公益金:including; commonweal funds本年利润:profits of current year未分配利润:undistributed profits损益表/利润表:income statement产品(商品)销售收入:revenue of sales of products (commodities) 出口产品销售收入:sales income of export products销售折扣与折让:discount& transfer of sales产品销售净额;net value of sales of products产品销售税金/成本:sales tax/cost of products出口产品销售成本:sales cost of export products销售费用(经营费用):sales expense (operation expense)产品销售利润:sales profits of products加:其他业务利润:add: other business profits营业/管理/财务费用;operation/overhead / finance expense利息支出(减利息收入):interest expense (less: interest income) 汇兑损失(减汇兑收益):exchange loss(exchange income)营业利润:operation profits投资收益;return on investment主营业务收入:revenue of main business主营业务成本:cost of main business主营业务税金及附加:tax & surtax of main business营业外收入/支出:non-operation income /expense投资收益:return on business补贴收入:subsidy income以前年度损益调整:adjustment for profits & loss of previous year 所得税:income tax利润分配表:profits distribution statement法定盈余公积:legal surplus accumulation法定公益金:legal commonweal funds年初/末未分配利润: undistributed profits of opening / closing year 已弥补亏损:loss being made up可供所有者分配的利润:profits distributable to owner已分配股利:distributed dividends其他转入:other transferred in提取法定公益金:retained legal commonweal funds提取职工奖励及福利基金:retained employee’s bonus & welfare funds提取储备基金:retained reversed funds提取企业发展基金:retained enterprise development funds利润归还投资:retained profits into investor应付优先股/普通股股利:dividends payable to preference / common stock提取任意盈余基金:retained random surplus accumulation转作资本的普通股股利:dividends of common stock transferred into capital来源:(/s/blog_61cbc91a0100hfml.html) - 审计/财务常用英语词汇_天际星语_新浪博客审计、财务常用英文词汇审计、财务常用英文词汇审计报告: Audit report资产负债表:Balance Sheet损益表:Income statement利润分配表:Profit distribution statement<中国注册会计师独立审计准则>:the Independent Auditing Standard for Chinese Certified Public Accountants会计报表:Financial statement在抽查的基础上:on a test basis主任会计师或授权副主任会计师:Chief Accountant or Authorized Assistant Chief Accountant中国注册会计师:Chinese Certified Public Accountant无钢印无效:shall not be valid without bearing the embossing seal年初数,年末数:Opening amounting\ closing amounting资产负债表:Balance sheet流动资产:Current assets货币资金:Cash短期、长期投资:Short-term、long-term investment应收票据:Notes receivable应收账款:Account receivable减:坏账准备:Less: provision for bad debt应收账款净额:Net value of account receivable预付账款:Advance to supplier应收出口退税:Receivable drawback for export应收补贴款: Receivable subsidy其他应收款:Other receivable存货:Inventories待转其他业务支出:Other business expense to be transferred待摊费用:Prepaid expense待处理流动资产净损失:Net loss of current assets to be settled一年内到期的长期债券投资:Long-term bonds investment due in 1 year 其他流动资产:Other current assets流动资产合计:Total current assets固定资产:fixed assets固定资产原价:Original value of fixed assets累计折旧:accumulated depreciation固定资产净值:Net value of fixed assets固定资产清理:Disposal of fixed assets在建工程:Construction in process待处理固定资产净损失:Net loss of fixed assets to be settled 固定资产合计:Total fixed assets无形资产及递延资产:Intangible assets & deferred assets递延税项目:Deferred tax负债及所有者权益:Liabilities & owner’s equity流动负债:current liabilities短期/长期借款:Short-term/long-term loan应付票据:Notes payable预收账款:Advance from clients其他应付款:Other payable应付工资:Accrued payroll应付福利费:Welfare payable应交税金/应付利润:Tax/ Profits payable其他应交款:Unpaid others预提费用:Accrued expense一年内到期的长期负债:Long-term liabilities due in 1 year 应付债券:Bonds payable长期应付款:Long-term payable实收资本:Paid-in capital资本公积:Capital accumulation盈余公积:Surplus accumulation其中:公益金:Including; commonweal funds本年利润:Profits of current year未分配利润:Undistributed profits损益表/利润表:Income statement产品(商品)销售收入:Revenue of sales of products (commodities) 出口产品销售收入:sales income of export products销售折扣与折让:Discount& transfer of sales产品销售净额;Net value of sales of products产品销售税金/成本:sales tax/cost of products出口产品销售成本:Sales cost of export products销售费用(经营费用):Sales expense (operation expense)产品销售利润:Sales profits of products加:其他业务利润:Add: other business profits营业/管理/财务费用;operation/overhead / finance expense利息支出(减利息收入):Interest expense (Less: interest income) 汇兑损失(减汇兑收益):Exchange loss(exchange income)营业利润:Operation profits投资收益;Return on investment主营业务收入:Revenue of main business主营业务成本:cost of main business主营业务税金及附加:Tax & surtax of main business营业外收入/支出:Non-operation income /expense投资收益:return on business补贴收入:subsidy income以前年度损益调整:Adjustment for profits & loss of previous year 所得税:income tax利润分配表:Profits Distribution Statement法定盈余公积:legal surplus accumulation法定公益金:Legal commonweal funds年初/末未分配利润: Undistributed profits of opening / closing year 已弥补亏损:Loss being made up可供所有者分配的利润:Profits distributable to owner已分配股利:Distributed dividends其他转入:other transferred in提取法定公益金:Retained legal commonweal funds提取职工奖励及福利基金:Retained employee’s bonus & welfare funds提取储备基金:retained reversed funds提取企业发展基金:retained enterprise development funds利润归还投资:Retained profits into investor应付优先股/普通股股利:Dividends payable to preference / common stock 提取任意盈余基金:Retained random surplus accumulation转作资本的普通股股利:Dividends of common stock transferred into capital l 附注:annotation to *《企业法人营业执照》:Business License for Legal Person经营期限:operation period投产:begin to produce采用的会计政策:Accounting policies implemented《企业会计准则》:Accounting Standard for Enterprises《工业企业会计制度》:Accounting System for Industrial Enterprise会计期间:Fiscal year记账原则和计价基础:Accounting principle and valuation basis会计核算;Accounting records以权责发生制为原则;base on accrual-basis principle以历史成本为计价基础:be valued at one’s historical cost坏账:bad debt直接转销法:direct amortized method存货核算方法:Accounting method of inventories存货的够入与入库:inventories at purchasing and inventories to warehouse 使用年限:service life固定资产折旧:Depreciation of fixed assets采用直线法平均计算:Be calculated using average service life method预计使用年限:anticipated service life预计净残值:anticipated net residual value使用年限:actual useful life专用生产设备:production machinery equipment 收入实现条件:Recognition of revenue订单法:order method增值税:value added tax (VAT)现金:cash on hand银行存款:Bank deposit账龄:account-age期末余额:closing balance产成品:finished products实收资本: Paid-in capital本年实际:Actual amount of current year办公费; office expenses差旅费:traveling expenses电话费: telephone charge水电费:water and electricity charge金融机构手续费:Handling change of finance authority出资额:investment amount档案查询专用章:Special Seal for Archive Inquiry工商行政管理局:Administration for Industry and Commerce套印无效:Overprint shall be ineffective主管:authoritative organ原审批单位:the original examine and approve authority会计报表审计 Auditing Financial statements资本验证 Capital verification企业财务会计制度设计 Setting up financial systems for enterprises exchange business代理记帐 Bookkeeping services外汇年检专项审计 Special audit and annual auditing of foreign exchange business企业合并、分立、清算审计 Auditing transactions such as enterprises’ merger、split and liquidation投资可行性研究 Feasibility analysis for investment project/viewthread.php?tid=9865Accounting system 会计系统American Accounting Association 美国会计协会American Institute of CPAs 美国注册会计师协会Audit 审计Balance sheet 资产负债表Bookkeepking 簿记Cash flow prospects 现金流量预测Certificate in Internal Auditing 内部审计证书Certificate in Management Accounting 管理会计证书Certificate Public Accountant注册会计师Cost accounting 成本会计 External users 外部使用者Financial accounting 财务会计Financial Accounting Standards Board 财务会计准则委员会Financial forecast 财务预测Generally accepted accounting principles 公认会计原则General-purpose information 通用目的信息Government Accounting Office 政府会计办公室Income statement 损益表Institute of Internal Auditors 内部审计师协会Institute of Management Accountants 管理会计师协会Integrity 整合性Internal auditing 内部审计Internal control structure 内部控制结构Internal Revenue Service 国内收入署Internal users 内部使用者Management accounting 管理会计Return of investment 投资回报Return on investment 投资报酬Securities and Exchange Commission 证券交易委员会Statement of cash flow 现金流量表Statement of financial position 财务状况表Tax accounting 税务会计Accounting equation 会计等式Articulation 勾稽关系Assets 资产Business entity 企业个体Capital stock 股本Corporation 公司Cost principle 成本原则Creditor 债权人Deflation 通货紧缩Disclosure 批露Expenses 费用Financial statement 财务报表Financial activities 筹资活动Going-concern assumption 持续经营假设Inflation 通货膨涨Investing activities 投资活动Liabilities 负债Negative cash flow 负现金流量Operating activities 经营活动Owners equity 所有者权益Partnership 合伙企业Positive cash flow 正现金流量Retained earning 留存利润Revenue 收入Sole proprietorship 独资企业Solvency 清偿能力Stable-dollar assumption 稳定货币假设Stockholders 股东Stockholders equity 股东权益Window dressing 门面粉饰Account 帐/htmlnews/2007/05/10/1100604.htm/zhuanti/english/index.htm并购活动* mergers and acquisitions仓 position个人大股东具报书 Individual Substantial Shareholders Notification个人投资者户口 Individual Investor Account个人客户 individual client个人交易所参与者 Individual Exchange Participant个人计算机终端机用户 PC terminal user借方结余 debit balance借款股 loan stock借壳上市 backdoor listing借贷资本 loan capital借额 debit伦敦国际金融期货及期权交易所 London International Financial Futures and Options Exchange (LIFFE)伦敦期权市场 London Traded Options Market (LTOM)伦敦证券交易所 London Stock Exchange (LSE)冻结 locked up冻结股份机制 securities-on-hold mechanism原油期货 crude oil futures套戥 / 套汇* / 套利* arbitrage差价 spread差额缴款 marks / marks payment库存股份/股票 treasury stock弱势货币 soft currency息股证 Equity Linked Instrument (ELI)挟仓 cornering; squeeze; short squeeze时间值 time value; time premium时间戳记 time stamp核心盈利 core earnings核准可赎回股份 approved redeemable share核准借入人 approved borrower核准借出代理人 approved lending agent核数委员会【证监会】 Audit Committee【SFC】核数师 auditor核数师报告 auditors' report核证附注 verification notes浮息存款证 floating rate certificate of deposit (FRCD) 浮息按揭 variable-rate mortgage浮息票据 floating rate note (FRN)海外发行人 overseas issuer消耗性资产【期权】 wasting asset【options】流动性不足 / 流通性不足 illiquidity流动资金 liquid capital流动资金比率/幅度 liquidity ratio; liquidity margin流动资金调节窗 Liquidity Adjustment Window (LAW)流动资金调节机制【金管局】 Liquidity Adjustment Facility (LAF)【HKMA】流动资产 liquid asset流通性 liquidity流通风险 liquidity risk流通量提供者 liquidity provider特别限价盘 special limit order特别处理股【中国内地】 Special Treatment【Mainland China】特别征费 Special Levy特别转让股【中国内地】 Particular Transfer【Mainland China】特快登记/过户登记服务 expedited registration service特殊项目 exceptional item特许使用者 privileged user特许财务分析员 chartered financial analyst特许财务分析员公会 Institute of Chartered Financial Analysts特许管理会计师公会 Chartered Institute of Management Accountants (CIMA) 「特许证券商」制度【美国】 Specialist System【US】特种国债【中国内地】 Special Treasury【Mainland China】特种备兑证信息【大利市】 exotic warrant information【Teletext】留存股票 treasury stock留存盈利/收益 retained earnings; retained income「粉红价单」【美国】 Pink Sheets【US】留存溢利/盈利 retained profits留成资金 / 保留资金 retained capital「粉红价单」【美国】 Pink Sheets【US】纯交易板 trading-only board纸黄金 paper gold索偿通知 claim notice蚊型股 penny stock被动受托人 bare trustee讯框传送交易网络 frame relay trading network托管人 custodian托管商参与者【中央结算系统参与者】 Custodian Participant【CCASS Participants】记名证券 registered securities记名证书 registered certificate记账式国库券【中国内地】 Registered Treasury【Mainland China】财政司司长 Financial Secretary财政年度 financial year财政股东 financial shareholder财政健全 financial integrity财政部【中国内地】 Ministry of Finance【Mainland China】《财政资源规则》 Financial Resources Rules财务申报 financial reporting财务风险 financial risk; financial exposure财务租赁 financial lease财务通融 financial accomodation财务业绩 financial results财务摘要报告 summary financial report财务监管 financial regulation财务顾问 financial adviser财经市场发展专责小组 The Financial Market Development Task Force /word/smcy/2008-05-18/37870.html政治风险 political risk再开票中心 re-invoicing center现代管理会计专门方法 special methods of modern management accounting 现代管理会计 modern management accounting提前与延期支付 Leads and Lags特许权使用管理费 fees and royalties跨国资本成本的计算 the cost of capital for foreign investments跨国运转资本会计 multinational working capital management跨国经营企业业绩评价 multinational performance evaluation经济风险管理 managing economic exposure交易风险管理 managing transaction exposure换算风险管理 managing translation exposure国际投资决策会计 foreign project appraisal国际投资决策会计 foreign project appraisal国际存货管理 international inventory management股利转移 dividend remittances公司内部贷款 inter-company loans冻结资金转移 repatriating blocked funds冻结资金保值 maintaining the value of blocked funds调整后的净现值 adjusted net present value配比原则 matching旅游、饮食服务企业会计 accounting of tourism and service施工企业会计 accounting of construction enterprises民航运输企业会计 accounting of civil aviation transportation enterprises 企业会计 business accounting商品流通企业会计 accounting of commercial enterprises权责发生制原则 accrual basis农业会计 accounting of agricultural enterprises实现原则 realization principle历史成本原则 principle of historical cost外商投资企业会计 accounting of enterprises with foreign investment通用报表 all-purpose financial statements铁路运输企业会计 accounting of rail way transportation enterprises所有者权益 owners equity所有者权益 owners equity实质量于形式 substance over form修正性惯例 principle of exceptions信息系统论 information system perspective相关性原则 relevance微观会计 micro-accounting客观性原则 objectivity可比性原则 comparability谨慎性原则 prudence金融企业会计 accounting of financial institutions交通运输企业会计 accounting of communication and transportation enterprises 建设单位会计 accounting of construction units记账本位币 recording currency计量属性 measurement attributes及时性原则 timeliness货币计量 monetary measurement会计准则 accounting standards会计主体 accounting entity会计职业道德 accounting professional ethics会计职能 functions of accounting会计预测 accounting forecasting会计要素 accounting elements会计研究 accounting research会计学科体系 accounting science system会计学 accounting会计信息 accounting information会计任务 targets of accounting activities会计人员 accounting personnel会计确认 accounting recognition会计目标 accounting objective会计理论结构 theoretical structure of accounting 会计理论 accounting theory会计控制 accounting control会计决策 accounting decision making会计监督 accounting supervision会计假设 accounting assumption会计记录 accounting records会计计量 accounting measurement会计机构 accounting department会计环境 accounting environment会计核算 financial accounting会计管理体制 system of accounting administration会计分期 accounting periods会计对象 accounting object会计等式 accounting equation会计本质 nature of accounting会计报表 accounting statements宏观会计 macro-accounting会计 accounting汇总报表 combination statements划分资本性支出与收益性支出原则 distinguishment between capital expenditure and revenue expenditure合并报表 consolidated financial statements管理活动论 management activities perspective管理会计 management accounting管理工具论 management tool perspective股份制企业会计 accounting of stock companies公认会计原则 generally accepted accounting principle, GAAP公共会计 public accounting工业会计 accounting of industrial enterprises个别报表 individual statements高新技术企业会计 accounting of high technology enterprises负债 liability费用 expense反馈价值 feedback value对外经济合作企业会计 accounting of foreign economic cooperation enter prises 对外报表 external statements对内报表 internal statements一致性原则 consistency艺术论 art perspective房地产开发企业会计 accounting of real estate enterprises邮电通信企业会计 accounting of post and telecommunication enterprises预测价值 forecast value真实与公允 true and fair view持续经营 going concern成本报表 cost statement财务会计原则 financial accounting principles财务会计概念框架 financial accounting conceptual framework财务会计 financial accounting政府及非营利组织会计 governmental and non-profit organization accounting 重要性原则 materiality专用报表 special purpose financial statements资产 assets资金 funds资金运动 funds movement财务报告 financial report财务报表要素 elements of financial statements财务报表 financial statements币值稳定假设 constant-dollar assumption保险企业会计 accounting of insurance companies收入的确认 recognition of revenue公司债券发行价格 corporate bond issuing price固定资产折旧 depreciation of fixed assets可转换债券 convertible bonds公司债券利息摊销加速折旧法 accelerated depreciation methods营业外收支净额公司债券利率 interest rate on debenture应收账款出借 assignment of accounts receivable无担保债券 debenture bonds后进先出法 last-in, first-out, LIFO其他货币资金应付票据贴现 discount on notes payable先进先出去 first-in, first-out缩写FIFO在发建工程 constructions in process固定资产更换与改良 improvements and replacements of fixed assets 实地盘存制 periodic inventory system收益总括观点 all-inclusive concept of income损益表法可变现净值法 net realizable value应付福利费基本业务利润固定资产扩建 additions of fixed assets应收账款出售 sale or factoring of accounts receivable 或有负债 contingent liability销货退回与折让 sales returns and allowances零售价格法 retail method现金折扣 cash discount特定履行法其他业务利润公司债券 bonds payable销售法 sale method应付票据 notes payable认股权 stock rights固定资产修理 repairs and maintenance of fixed assets 有担保债券 mortgage bonds销售费用 selling expenses应付股利 dividends payable应收票据 notes receivable无形资产 intangible assets收款法 collection method所得税 income tax流动负债 current liabilities生产法 production method计划成本核算废弃和生置法 retirement and replacement method 盘存法 inventory method流动资产 current assets购货折扣 purchases discounts商誉 goodwill应收账款 accounts receivable投资收益 investment income营业利润 operating income预提费用股本 capital stock公司债券偿还 redemption of bonds坏账 bad debts固定资产重估价 revaluations of fixed assets银行存款 cash in bank固定资产 fixed assets利润总额利益分配 profit distribution应计费用 accrued expense商标权 trademarks and trade names全部履行法净利润 net income应付利润 profit payable未分配利润收益债券 income bonds货币资金利息资本化 capitalization of interests 公益金工程物资预付账款 advance to supplier其他应收款 other receivables现金 cash预收账款公司债券发行 corporate bond floatation 应付工资 wages payable实收资本 paid-in capital盈余公积 surplus reserves管理费用土地使用权股利 dividend应交税金 taxes payable负商誉 negative goodwill费用的确认 recognition of expense短期投资 temporary investment短期借款 short-term loans递延资产 deferred charges低值易耗品当期经营观点 current operating concept of income 待摊费用待核销基建支出[旧]待处理流动资产损失待处理固定资产损失存货销售的影响 effects of inventory errors折旧[旧]折旧方法 depreciation method折旧率 depreciation rate支出 payment直线法 straight-line职工福利基金 welfare fund专项拨款【旧】专利权 patents住房基金 housing fund重置成本法 replacement costing专项物资[旧]专项资产【旧】专有技术 know-how专营权 franchises资本公积 capital reserves资产负债表 balance sheet资金占用和资金来源[旧]自然资源 natural resources存货 inventory车间经费【旧】偿债基金 sinking fund长期应付款 long-term payables长期投资 long-term investments长期借款 long-term loans长期负债 long-term liability of long-term debt 财务费用 financing expenses拨定留存收益 appropriated retained earnings 标准成本法 standard costing变动成本法 variable costing比例履行法包装物版权 copyrights汇总原始凭证 cumulative source document汇总记账凭证核算形式 bookkeeping procedure using summary vouchers 工作底稿 working paper复式记账凭证 multiple account titles voucher复式记账法 Double entry bookkeeping复合分录 compound entry划线更正法 correction by drawing a straight ling汇总原始凭证 cumulative source document会计凭证 accounting documents会计科目表 chart of accounts会计科目 account title红字更正法 correction by using red ink会计核算形式 bookkeeping procedures过账 posting会计分录 accounting entry会计循环 accounting cycle会计账簿 Book of accounts活页式账簿 loose-leaf book集合分配账户 clearing accounts计价对比账户 matching accounts记账方法 bookkeeping methods记账规则 recording rules记账凭证 voucher记账凭证核算形式 Bookkeeping procedure using vouchers记账凭证汇总表核算形式 bookkeeping procedure using categorized account summary简单分录 simple entry结算账户 settlement accounts结账 closing account结账分录 closing entry借贷记账法 debit-credit bookkeeping局部清查 partial check卡片式账簿 card book跨期摊提账户 inter-period allocation accounts累计凭证 multiple-record document联合账簿 compound book明细分类账簿 subsidiary ledger明细分类账户 subsidiary account盘存账存 inventory accounts平行登记 parallel recording全面清查 complete check日记总账 combined journal and ledger日记总账核算形式 bookkeeping procedure using summarized journal三式记账法 triple-entry bookkeeping实账户 real accounts试算表 trial balance试算平衡 trial balancing收付记账法 receipts-payment bookkeeping收款凭证 receipt voucher损益表账户 income statement accounts通用记账凭证 general purpose voucher通用日记账核算形式 bookkeeping procedure using general journal 外来原始凭证 source document from outside现金日记账 cash journal虚账户 nominal accounts序时账簿 book of chronological entry一次凭证 single-record document银行存款日记账 deposit journal永续盘存制 perpetual inventory system原始凭证 source document暂记账户 suspense accounts增减记账法 increase-decrease bookkeeping债权结算账户 accounts for settlement of claim债权债务结算账户 accounts for settlement of claim and debt债务结算账户 accounts for settlement of debt账户 account账户编号 Account number账户对应关系 debit-credit relationship账项调整 adjustment of account专用记账凭证 special-purpose voucher转回分录 reversing entry资金来源账户 accounts of sources of funds资产负债账户 balance sheet accounts转账凭证 transfer voucher资金运用账户 accounts of applications of funds自制原始凭证 internal source document总分类账簿 general ledger总分类账户 general account附加账户 adjunct accounts付款凭证 payment voucher分类账簿 ledger多栏式日记账核算形式 bookkeeping procedure using columnar journal 对账 checking对应账户 corresponding accounts定期清查 Periodic checking method定期盘存制 periodic inventory system订本式账簿 bound book调整账户 adjustment accounts调整分录 adjusting journal entry单式记账凭证 single account title voucher单式记账法 single-entry bookkeeping从属账户 Secondary accounts成本计算账户 costing accounts财产清查 physical inventory簿记 bookkeeping不定期清查 non-periodic checking method补充登记法 correction by extra recording表外账户 off-balance sheet accounts备抵账户 provision accounts备抵附加账户 provision and adjunct accounts备查账簿 memorandum/word/smcy/2008-04-28/35514.html。

5外汇风险管理20100518

二、远期合同法

指具有外汇债权或债务的公司与银行签定卖出 或买进远期外汇的合同,以消除外汇风险的方 法。 具体做法:出口商 出口商在签定贸易合同后,按当时 出口商 的远期汇率预先卖出 卖出合同金额和币别的远期 远期, 卖出 远期 在收到货款时再按原订汇率进行交割。进口商 进口商 则预先买进 买进所需外汇的远期,到支付货款时按 买进 原定汇率进行交割。 优点:一方面将防范外汇风险的成本固定在一 定的范围内;另一方面,将不确定的汇率变动 因素转化为可计算的因素,有利于成本核算。

例如:美国某公司赊销l 300 000日元的商 品给日本某一家买主,60天后支付,汇 率是US$1=J¥130,美国卖主在收到贷款 时,希望用l 300 000日元兑换10 000美元. 如果到期汇率为:US$1=J¥140 如果到期汇率为:US$1=J¥120

经济风险 预期经营收益 预期经营收益 经营收益的风险 是指由于突然的汇率波动,引起公司或 企业的未来一定期间的收益发生变化。 它是一种潜在性 潜在性的风险,其程度大小取 潜在性 决于汇率变动对产品数量、价格及成本 汇率变动对产品数量、 汇率变动对产品数量 的影响程度。 的影响程度

什么是外汇风险?

以外币计价 外币计价的资产或负债因 外币计价 外汇汇率的变动而引起其价 外汇汇率的变动 值上涨或下跌的可能。

外汇风险双向:

风险收益(Gain)与风险损失 风险损失 (Loss)

外汇风险的三个要素:

本币 外币 时间

缺一不可

多头地位与空头地位 多头地位(Long Foreign Currency):一 个企业在一定时期以后将有一笔外汇资 外汇资 金流入,则该企业处于多头地位; 金流入 空头地位(Short Foreign Currency):一 个企业在一定时期以后将有一笔外资流 外资流 出,则处于空头地位。

国际贸易与金融名词解释(3)

国际贸易与金融名词解释(3)国际贸易与金融名词解释29、对冲基金:是一种投资于多种证券的私营有限合伙制企业。

30、金融互换交易:主要通过场外交易市场进行,交易双方签订互换协议,在未来一定时期内:)具有不同内容或不同性质的现金流。

31、风险投资公司:是专门风险基金(或风险资本),把所掌管的资金有效地投入富有盈利潜力的高科技企业,并通过后者的上市或被并购而获取资本报酬的企业。

part two1.欧洲货币市场指集存于伦敦与其他金融中心的境外美元和其他境外欧洲货币,而用于贷放的国际金融市场,也可以概括为一国境外,进行该国货币存储与贷放的市场。

2.金融创新狭义指金融机构在金融工具和金融业务方面的创新,广义,除金融工具和金融业务创新之外,还包括金融机构与金融市场的创新,3.外汇管制指一国政府对居民和非居民的外汇获取,持有,使用和国际支付或转移中使用本币或外币所采取的管理措施与政策规定。

4. 外汇交易风险由于外汇汇率波动而引起的应收资产与债务价值变化的风险即为交易风险5.国际收支狭义一国在一定时期内的外汇收支,广义在一定时期内,一国居民与非居民之间经济交易的统计记录指标1,外债余额/国民生产总值,称负债率10%2.外债余额/出口商品,称债务率100%3.外债还本付息额/出口商品,劳务的外汇收入额,称偿债率20%6.国际转租赁是指一国出租人a根据本国最终承租人的要求,先以承租人的身份从另一国出租人b处租进设备,然后再以出租人的身份转租给用户使用的一项租赁交易。

7.国际杠杆租赁杠杆租赁在英,美法系国家称衡平租赁,是指在一项租赁交易中,出租人只需投资租赁设备购置款项20%-40%的金额,即可在法律上拥有该设备的完整所有权,享有如同对设备100%投资的同等税收待遇;设备购置款项的60%-80%由银行等金融机构提供的无追索权贷款解决,但需出租人以租赁设备做抵押,以转让租赁合同和收取租金的权利作担保的一项租赁交易;当杠杆租赁的承,出租人为份属两国的企业时即为国际杠杆租赁。

外汇风险管理ppt课件

精品课件

财务会计准则公告第52号

1981年,第52号《外币折算》 根据环境,选择使用时态法或现行汇率法 母公司货币观,子公司的活动是母公司的扩展和延

伸,用时态法,折算损益记入损益表 子公司货币观,用现行汇率法,折算损益记入资产

负债表

精品课件

3、折算风险的控制

资产负债表保值 合约保值

精品课件

2、折算方法的选择

财务会计准则公告第8号

1975年,第8号《外币交易会计与外币财务报表折 算》,时态法是唯一公认会计准则。

认为外币折算是一种计量变换的过程,是对报表项 目按外币重新表述,它仅仅改变计量的货币单位, 不改变计量项目的属性

折算损益不允许递延,在汇率变动的当期记入损益 表

经济风险(economic exposure)

指汇率变动对企业的产销数量、价格、成本、费用 等产生的影响,从而导致企业未来现金流量发生改 变的风险。

交易风险(transaction exposure)

指汇率变动对企业已发生尚未结算的外币债权、债 务的价值产生的影响,从而导致企业未来收入或支 出的现金价值发生改变的风险。

精品课件

资产负债表保值

风险资产,折算时使用现行汇率的资产 风险负债, 目的是风险资产和风险负债在总额上相等 【例】美国跨国公司一海外子公司期末有1000

美元的风险净资产,

将现金兑换成美元 从银行借款,兑换成美元持有

精品课件

合约保值

即利用外汇远期市场进行保值 假设上述公司预计当地汇率下跌,风险净资产

680 700 1380

680 700 1380

1500 2600 4100 11000

375 500

80 2430 -150

国际金融第七章外汇风险管理

五.借款投资法

六.借款法:指有远期外汇收入的企业通过向其银行借进一 笔与其远期收入相同金额、相同期限、相同货币的贷款, 以达到融通资金、防止外汇风险的方法。

例7-6:美国A公司半年后将从德国收回一笔10万欧元的 出口外汇收入。该公司为防止半年后汇率下跌的风险,则 利用借款法向本国银行借相同金额、相同期限的欧元贷款, 然后将这笔欧元作为现汇卖出,作为美元流动资金。

三.经济风险(Economic Exposure): 指难以预料的汇率变动引起企业未来一定期间收益变化的一种潜在风险。

外汇风险的构 成因素

本币

外币

时间

第二节 外汇风险管理 含义 对外汇风险的特性以及影响因素进行识别与测

定,并设计和选择防止和减少损失发生的处理 方案,以最小成本达到风险管理的最佳效果。 原则 分类防范 风险最小化 稳妥防范

二.拥有应付帐款的企业

三.从银行借入与外币金额等同的本币贷款;

四.将借入的本币通过即期合同兑换成外币;

五.以兑换成的外币提前支付给出口商,并得到一定数额的折扣。

例7-11:中国香港A公司在90天后有一笔10万美元的应付货 款。为避免外汇风险,可先从银行借入或利用自有资金78万港 元;然后与银行签定即期外汇合同,购买10万美元;最后以美 元提前支付,获得折扣。

外汇风险 的种类

01

交易风险(Transaction Exposure)

02

指以外币计价的交易活动中,由于汇率波动而

引起应收账款和应付账款价值变化的风险。

例7-2:

我国一家企业某日向美国某公司出口一批 价值10万美元的货物,付款期限为90天。

按成交当日现汇价 USD100=CNY677.65 ,该企业应收 账款为677650元人民币。

外汇敞口名词解释

外汇敞口名词解释

外汇敞口(Foreign Exchange Exposure),也被称为外汇风险敞口,指的是企业或个人在跨国贸易或投资活动中由于汇率波动所面临的风险。

外汇敞口反映了一个实体在其财务状况中与汇率变动相关的敏感性。

以下是一些与外汇敞口相关的常见名词解释:

1. 汇率风险(Exchange Rate Risk):指由于汇率波动引起的货币价值变动所导致的风险。

当一个实体持有或操作不同货币的资产和负债时,由于汇率的变动,其价值可能会受到影响。

2. 交易敞口(Transaction Exposure):指企业在未来的交易中可能由于汇率波动而导致货币价值变动的风险。

例如,企业签订了一项外国合同,合同金额以外币计价,如果汇率发生变化,该企业可能会面临交易敞口。

3. 经济敞口(Economic Exposure):指企业或个人由于汇率变动而对经济环境产生的风险。

汇率变动可能会对企业的市场份额、竞争力、成本和利润等方面产生影响。

4. 套期保值(Hedging):指采取某种金融工具或策略来减少或

抵消外汇敞口的风险。

常见的套期保值工具包括远期合约、期货合约、期权合约等。

5. 外汇衍生品(Foreign Exchange Derivatives):是一种金融合约,其价值的变动基于一个或多个外汇汇率。

外汇衍生品包括远期合约、期货合约、期权合约等,可以用于管理外汇敞口的风险。

外汇敞口管理对于跨国企业和投资者来说非常重要,它可以帮助减少不确定性和损失,保护财务状况免受汇率波动的影响。

合理的外汇敞口管理可以通过套期保值、多样化业务地域、灵活的定价策略等方式来实现。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

交易风险管理(managing transaction exposure)

把握交易风险状况并及时进行有效防范和控制的工作。

交易风险指已达成协议但尚未结算的外币交易,由于汇率变动而引起外汇损益的可能性。

它衡量的是特定汇率变而引起外汇损益的可能性。

它衡量的是特定汇率变动对已达成协议的外币交易价值可能产生的影响。

交易风险管理方法包括:

(1)远期市场套期保值(ForwardMarketHedge)。

利用远期外汇市场,通过签订具有抵消性质的远期外汇合约来防范由于汇率变动而可能蒙受的损失,以达到保值的目的。

远期外汇合约反映的是一种契约关系,即规定一方当事人在将来某个特定日期,以确定的汇率向另一方当事人交割一定数额的某种货币以换取特数额的另一种货币。

至于履行合约的资金来源可能是现存的或经营业务的应收款或尚无着落,需要时再到即期外汇市场购买。

通过远期市场套期保值可以得到完全确定的现金流量价值,但它未必是最大化的价值。

利用远期市场套期保值的前提是必须存在远期外汇市场,而在现实世界中,并不是任何货币都存在远期外汇市场。

(2)货币市场套期保值(MoneyMardetHedge)。

通过在货币市场上的短期借贷,建立配比性质或抵消性质的债权、债务,从而达成抵补外币应收应付款项所涉及的汇率变动风险的目的。

与远期市场套期保值一亲,货币市场套期保值也涉及一个合约以及履行合约资金来源问

题。

但是,这是签订的是一个贷款协议即寻求货币市场套期保值的公司需要从某个货币市场借入一种货币,并将其在即期外汇市场上兑换成另一种货币,投入另一个货币市场。

至于履行合约的资金来源无非是经营业务的应收款或尚无着落,需要时再到即期外汇市场购买。

如果属于前者,那么,货币市场套期保值就是“抛补性质的”(Covered);如果属于后者,货币市场套期保值则是没有保值仍存在一定的风险。

货币市场套期保值涉及借款换汇和投资(即借贷)两个过程和两个货币市场,其保值机制在于两个货币市场的利率差异与远期汇率升(贴)水的关系。

(3)期权市场套期保值(OptionMarketHedge)。

根据对外汇汇率变化趋势的预,在外汇期权市场上,购买看涨或看跌期权,坐观外汇市场变化,决定行使或放弃期权,以达到既能保值又有盈利机会的目的。

由于期权给予购买方的是一种权利而不是义务,购买方在汇率变化于已有利时行使期权,于已不利则放弃期权,做到坐地观天,确保收入底线而可望获得无限的盈利。

如果跨国公司不能确定未来现金流量是否发生或何时发生,那么,期权市场套期保值是最理想的保值工具。