会计企业决策的基础(15)财务会计书后大题

会计学企业决策的基础

会计学企业决策的基础在现代企业中,会计学扮演着至关重要的角色。

它不仅是按照一定标准记录企业交易的基础,还能为企业提供大量的财务信息,帮助企业管理者做出正确的企业决策。

本文将介绍会计学在企业决策中的重要性以及相关底层原则和概念。

会计学在企业决策中的重要性企业决策是企业发展过程中必不可少的一部分。

它可以帮助企业管理者做出正确的选择和决策,以实现企业利润最大化和可持续发展。

而会计学正是帮助企业管理者做出正确判断和决策的重要工具之一。

下面我们将详细介绍会计学在企业决策中的作用。

提供财务信息会计学的首要任务是提供精确、客观的财务信息,让企业管理者能够了解企业的经营状况和财务状况。

通过会计学记录企业的交易信息,可以及时得到企业的资产、负债、收入和支出等财务状况。

企业管理者可以通过这些信息来判断企业是否正常运营,是否需要调整经营决策。

分析经营状况会计学不仅可以提供财务信息,还可以通过财务分析来帮助企业管理者了解企业的长期和短期财务状况。

企业管理者可以通过利润表、资产负债表和现金流量表等报表来分析企业状况,从而评估企业财务稳定性、赢利能力和成长性等因素。

预测未来趋势会计学的应用还可以帮助企业管理者预测未来趋势。

通过对过去和当前的财务状况进行分析,企业管理者可以预测未来企业的发展趋势。

这对于企业的长期规划和策略制定非常重要。

会计学的基本原则和概念要正确理解会计学在企业决策中的作用,有必要了解会计学的一些基本原则和概念。

会计主体和会计客体会计主体是指进行会计记录和报告的组织和个人,如企业、个体工商户等。

会计客体是指需要记录的经济活动,如企业的交易、收入和支出等。

会计等式会计等式是会计学中的基本概念之一。

它是指资产=负债+所有者权益。

通过这个等式,企业管理者可以了解企业的资产来源和运用情况,包括企业的负债情况和所有者权益。

会计要素会计要素是指企业在经济活动中发生的一系列基本事项。

包括资产、负债、所有者权益、收入和费用等。

会计学企业决策的基础 答案

管理会计作业(chapter16-20) Chapter 16 P757 16、5AChapter 16 P761 16、4BChapter 17 P802 17、3Aa、Department One overhead application rate based onmachine-hours:ManufacturingOverhead = $420,000 = $35 per machine-hour Machine-Hours 12,000Department Two overhead application rate based on direct labor hours:ManufacturingOverhead = $337,500 = $22、50 per direct labor hourDirect Labor Hours 15,000Chapter 17 P805 17、8Ad、The Custom Cuts product line is very labor intensive in comparison to the Basic Chunksproduct line、Thus, the company’s current practice of using direct labor hours toallocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line、If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line isoverpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace、This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline、e、The benefits the company would achieve by implementing an activity-based costing systeminclude: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrificesignificant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality、Chapter 18 P835 18、1B、Ex、a、job costing (each project of a construction company is unique)18、1b、both job and process costing (institutional clients may representunique jobs)c、job costing (each set of equipment is uniquely designed andmanufactured)d、process costing (the dog houses are uniformly manufactured inhigh volumes)e、process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18、3A4,000 EU @ $61、50 = $246,000b4,000 EU @ $13、50 = $54,000Chapter 18 P845 18、2Ba、(1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b、In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a)、Chapter 20 P918 20、1Ad、No、With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even、Chapter 20 P918 20、2AChapter 20 P920 20、6ASales volume required to maintain current operating income:Sales Volume = Fixed Costs + Target OperatingIncomeUnit Contribution Margin= $390,000 + $350,000= $20,000 units $37。

会计学企业决策的基础

会计学企业决策的基础会计学作为现代企业管理的基本学科,对企业决策具有重要的支撑作用。

在企业运营过程中,会计学有助于企业管理者更加准确地把握企业的经营状况,制定科学的决策方案。

本文将从会计学对企业决策的作用、职能以及核算体系等方面进行探讨。

会计学对企业决策的作用1.提供信息支持:会计学的主要职责是收集、处理和汇报企业财务信息,通过财务报表、经营分析报告等形式,为企业管理者提供准确、全面的信息支持,帮助管理者把握企业经营状况,制定决策方案。

2.帮助评估经营结果:会计学通过记录和反映企业经济活动的历史,反映和评价企业的经营状况,判断企业各项事务的优劣,帮助管理者做出合理的经营决策。

3.辅助经营风险管理:通过会计核算,可以实现对企业不同部门、不同环节的财务状况监控,帮助管理者识别、分析和评估风险,及时采取措施控制或缓解风险。

4.促进企业治理:会计学通过财务报告等信息披露,监督企业管理行为,维护股东、投资者等人的合法权益,促进企业的良性治理。

会计职能对企业决策的支持1.记账职能:会计的首要职责是记录企业的经济业务活动,通过会计帐簿的形式,反映企业的经济状况,为企业决策提供准确的信息支持。

2.核算职能:会计核算是会计学的核心内容,贯穿整个会计工作,在企业决策中具有举足轻重的地位。

经过核算,企业能够准确、全面地了解自己的财务状况,制定合理的决策方案。

3.处理职能:会计处理职能是指利用会计方法和技术,对企业的财务信息进行分析和处理,在企业决策中发挥重要作用。

通过处理,会计人员能够对经济事务进行有序管理,优化企业的决策效果。

4.报告职能:会计报告包括财务报表、经营分析报告等,是向企业管理者、股东等外部人员提供的信息。

会计人员通过报告,向外部用户传达企业的财务状况,以便他们能够了解企业的经营状况,做出相应的决策。

会计核算体系对企业决策的支持1.资产负债表:资产负债表反映企业的资产、负债和所有者权益状况,是企业财务状况的总结表。

2023年中级会计职称之中级会计财务管理基础试题库和答案要点

2023年中级会计职称之中级会计财务管理基础试题库和答案要点单选题(共30题)1、某企业的营业净利率为20%,总资产周转率为0.5,资产负债率为50%,则该企业的净资产收益率为()。

A.5%B.10%C.20%D.40%【答案】 C2、关于吸收直接投资的出资方式,下列表述中错误的是()。

A.以货币资产出资是吸收直接投资中最重要的出资方式B.股东或者发起人可以以特许经营权进行出资C.燃料可以作为实物资产进行出资D.未退还职工的集资款可转为个人投资【答案】 B3、下列不属于企业纳税筹划必须遵循的原则的是()。

A.合法性原则B.实现税收零风险原则C.经济性原则D.先行性原则【答案】 B4、下列投资项目可行性评价指标中,最适用于寿命期相等的互斥项目决策的是()。

A.净现值法B.现值指数法C.内含收益率法D.动态回收期法【答案】 A5、某投资项目的项目期限为5年,投资期为1年,投产后每年的现金净流量均为1500万元,原始投资额现值为2500万元,资本成本为10%,(P/A,10%,4)=3.1699,(P/A,10%,5)=3.7908,(P/F,10%,1)=0.9091,则该项目年金净流量为()万元。

A.574.97B.840.51C.594.82D.480.80【答案】 D6、公司采用协商型价格作为内部转移价格时,协商价格的下限一般为()。

A.完全成本加成B.市场价格C.单位变动成本D.单位完全成本【答案】 C7、甲持有一项投资,预计未来的收益率有两种可能,分别为10%和20%,概率分别为70%和30%,则该项投资预期收益率为()。

A.12.5%B.13%C.30%D.15%【答案】 B8、事中成本管理阶段主要是对营运过程中发生的成本进行监督和控制,并根据实际情况对成本预算进行必要的修正,即()步骤。

A.成本预测B.成本决策C.成本控制D.成本核算【答案】 C9、(2018年真题)企业所有者作为投资人,关心其资本的保值和增值状况,因此较为重视企业的()指标。

会计学-企业决策的基础 答案教学资料

会计学-企业决策的基础答案管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based on machine-hours:Manufacturing Overhead= $420,000= $35 per machine-hourMachine-Hours 12,000Department Two overhead application rate based on direct labor hours:Manufacturing Overhead= $337,500= $22.50 per direct labor hourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the BasicChunks product line. Thus, the company’s current practice of using direct laborhours to allocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probablyexplains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costingsystem include: (1) a better identification of its operating inefficiencies, (2) a betterunderstanding of its overhead cost structure, (3) a better understanding of theresource requirements of each product line, (4) the potential to increase the sellingprice of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability todecrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1a. job costing (each project of a construction company is unique)B. Ex.18.1b. both job and process costing (institutional clients may represent uniquejobs)c. job costing (each set of equipment is uniquely designed andmanufactured)d. process costing (the dog houses are uniformly manufactured in highvolumes)e. process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18.3Ab4,000 EU @ $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume =Fixed Costs + Target Operating IncomeUnit Contribution Margin=$390,000 + $350,000= $20,000 units$37。

会计学企业决策的基础财务会计分册第17版

会计学企业决策的基础财务会计分册第17版下载提示:该文档是本店铺精心编制而成的,希望大家下载后,能够帮助大家解决实际问题。

文档下载后可定制修改,请根据实际需要进行调整和使用,谢谢!本店铺为大家提供各种类型的实用资料,如教育随笔、日记赏析、句子摘抄、古诗大全、经典美文、话题作文、工作总结、词语解析、文案摘录、其他资料等等,想了解不同资料格式和写法,敬请关注!Download tips: This document is carefully compiled by this editor. I hope that after you download it, it can help you solve practical problems. The document can be customized and modified after downloading, please adjust and use it according to actual needs, thank you! In addition, this shop provides you with various types of practical materials, such as educational essays, diary appreciation, sentence excerpts, ancient poems, classic articles, topic composition, work summary, word parsing, copy excerpts, other materials and so on, want to know different data formats and writing methods, please pay attention!企业决策在当前竞争激烈的市场环境中显得尤为重要。

会计学——企业决策的基础(英文版)课后习题答案_comprehensive_problem_1(完整版)

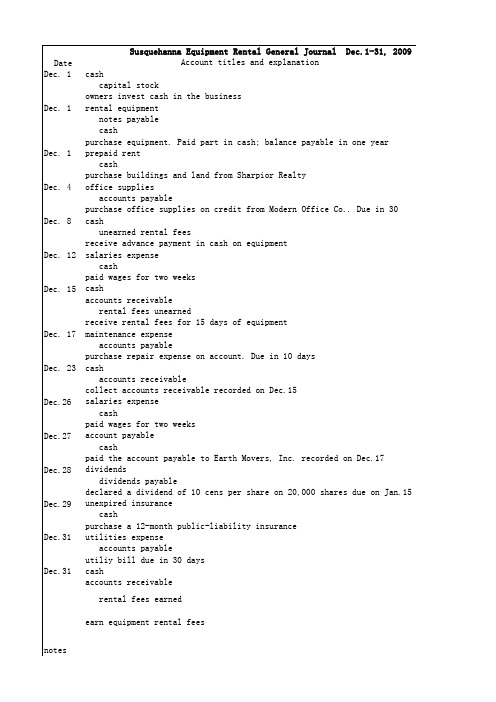

notes

unadjusted trail balance

Susquehanna Equipment Rental adjustments Dr Cr Dr Cr

work sheet for

balance sheet accounts cash accounts receivable prepaid rent unexpired insurance office supplies rental equipment accumulated depreciation: rental equipment notes payable accounts payable interest payable salaries payable dividends payable unearned rental fees income taxes payable capital stock retained earnings dividends income statement accounts rental fees earned salaries expense maintenance expense utilities expense rent expense office supplies expense depreciation expense interest expense income taxes expense income summary subtotal net income total

Dec.26

Dec.27

Dec.28

Dec.29

Dec.31

Dec.31

cash capital stock owners invest cash in the business rental equipment notes payable cash purchase equipment. Paid part in cash; balance payable in one year prepaid rent cash purchase buildings and land from Sharpior Realty office supplies accounts payable purchase office supplies on credit from Modern Office Co.. Due in 30 days cash unearned rental fees receive advance payment in cash on equipment salaries expense cash paid wages for two weeks cash accounts receivable rental fees unearned receive rental fees for 15 days of equipment maintenance expense accounts payable purchase repair expense on account. Due in 10 days cash accounts receivable collect accounts receivable recorded on Dec.15 salaries expense cash paid wages for two weeks account payable cash paid the account payable to Earth Movers, Inc. recorded on Dec.17 dividends dividends payable declared a dividend of 10 cens per share on 20,000 shares due on Jan.15 unexpired insurance cash purchase a 12-month public-liability insurance utilities expense accounts payable utiliy bill due in 30 days cash accounts receivable rental fees earned earn equipment rental fees

会计学:企业决策的基础财务会计分册(机械工业出版社,英文原书第15版)课后练习答案chapter05

Exercises 5.1 5.2 5.3 5.4 5.5 5.6 5.7 5.8 5.9 5.10 5.11 5.12 5.13 5.14 5.15

Topic Accounting terminology Financial statement preparation Financial statement preparation Closing and after-closing trial balance Closing and after-closing trial balance Real World: Circuit City Adequate Disclosure Closing entries of profitable firms Closing entries of unprofitable firms Adjusting versus closing entries Profitability and liquidity measures Profitability and liquidity measures Interim results Interim results Effects of accounting errors Real World: Home Depot, Inc. Using an annual report

Communication, analysis

© The McGraw-Hill Companies, Inc., 2008 Overview

© The McGraw-Hill Companies, Inc., 2008 Overview

CHAPTER 5 THE ACCOUNTING CYCLE: REPORTING FINANCIAL RESULTS

会计学企业决策的基础《会计学企业决策的基础》

§ 负债(Liabilities)是由过去的交易、事项形 成的现有义务,履行该义务预期会导致经济 利益流出企业。

§ 负债的特征是:

§ (1)负债是由于过去的交易或事项所引起的企 业的现有义务。企业预期在将来要发生的交 易或事项可能产生的债务,不能作为会计上 的负债处理;

PPT文档演模板

会计学企业决策的基础《会计学企业 决策的基础》

PPT文档演模板

•成本和收入决定: • 分批成本法 • 分步成本法 • 作业成本法 •销售:收入和利润 •资产和负债 •厂房和设备 •贷款和资产 •应收和应付款项 •现金和存款 •现金流: • 经营活动现金流 • 筹资活动现金流 • 投资活动现金流

•决策支持 •本-量-利分析 •业绩评估 •增值分析 •预算 •资本分配 •每投收益 •比率分析

会计学企业决策的基础《会计学企业 决策的基础》

三、所有者权益

§所有者权益(owner‘s equity),是所有者在企 业资产中享有的经济利益,其金额为资产减 去负债后的余额。它表明企业的资产总额在 抵偿了现存的一切债务后的差额,所有者享 有的份额。

§ 所有者权益就其形成看,除投入资本与资本 公积外,主要来源于企业的经营积累。

会计行为可分为三类:

§ (一)会计核算行为 § 即以货币为主要的计量单位,采用专门方法,

通过计量、计算、记录、分类、汇总等程序, 对单位的经济活动进行连续、系统、完整的 反映,以提供会计信息的活动。

PPT文档演模板

会计学企业决策的基础《会计学企业 决策的基础》

(二)会计监督行为

§ 即从单位内部和外部对单位会计核算本身, 以及纳入经济核算范围之内的经济业务事项 进行监督的活动。

公布等,特别是对其中的会计信息进行监督,以防 欺骗投资人。 § (4)财税部门——对纳税额的监督核实。 § (5)工会、职工、社会公众、专业分析师等。

大学基础会计习题

一、单选题1.决策有用观是一种关于(会计目标)的观点。

2.(会计核算)是会计的主要内容,是会计的基础。

3.(会计恒等式)既反映了会计要素间的基本数量关系,同时也是复式记账法的理论依据。

4.总分类科目和明细分类科目之间有密切关系,从性质上说,是(统驭和从属)的关系。

5.在复式记账法下,对每项经济业务都应以相等的金额,在(两个或两个以上)账户中登记。

6.在借贷记账法下,资产类账户的结构特点是(借方记增加,贷方记减少,余额在借方)。

7.“限额领料单”按其填制方法属于(累计凭证)。

8.当经济业务只涉及货币资金相互间的收付时,一般填制(付款凭证)。

9.明细账从账簿的外表形式上看,一般采用(活页式)账簿。

10.在结账以前,如发现账簿记录有文字或数字错误,而记账凭证没错,应采用(划线更正法)进行错帐更正。

11.清查银行存款所采用的方法一般是(对账单法)。

12.财产清查中发现某种材料盘亏时,在报经批准处理前应作会计分录为(借:待处理财产损溢贷:原材料)。

13.下列属于静态报表的是(资产负债表)。

14.“累计折旧”和“坏账准备”账户属于(抵减类账户)。

15.下列选项中,正确反映资产负债表中所有者权益项目的排列顺序是(实收资本资本公积盈余公积未分配利润)。

16.下列资产负债表项目中,需根据总账账户期末余额合计数填列的项目是(货币资金)。

17.下列项目中不属于会计假设的是(实质重于形式)。

18.会计核算应当以实际发生的交易或事项为依据,如实反映企业的财务状况,经营成果和现金流量,这是会计核算的(可靠性原则)。

19.资产负债表的资产项目,说明了企业所拥有的各种经济资源以及企业(偿还债务的能力)。

20.直接根据各种记账凭证登记总分类帐,这种会计核算形式是(记账凭证核算形式)。

21.一项资产增加,不可能引起(一项负债减少)。

22.下列经济业务中,会引起一项负债减少,而另一项负债增加的经济业务是(以银行借款偿还应付账款)。

23.在“资产=负债+所有者权益”这一会计恒等式的右端,两个会计要素的位置(不能颠倒)。

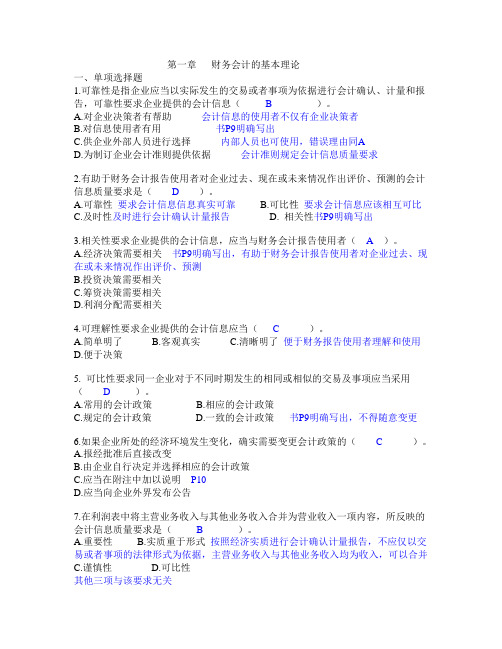

第1章习题财务会计的基本理论(答案完整版)

第一章财务会计的基本理论一、单项选择题1.可靠性是指企业应当以实际发生的交易或者事项为依据进行会计确认、计量和报告,可靠性要求企业提供的会计信息( B )。

A.对企业决策者有帮助会计信息的使用者不仅有企业决策者B.对信息使用者有用书P9明确写出C.供企业外部人员进行选择内部人员也可使用,错误理由同AD.为制订企业会计准则提供依据会计准则规定会计信息质量要求2.有助于财务会计报告使用者对企业过去、现在或未来情况作出评价、预测的会计信息质量要求是(D)。

A.可靠性要求会计信息信息真实可靠B.可比性要求会计信息应该相互可比C.及时性及时进行会计确认计量报告D. 相关性书P9明确写出3.相关性要求企业提供的会计信息,应当与财务会计报告使用者(A)。

A.经济决策需要相关书P9明确写出,有助于财务会计报告使用者对企业过去、现在或未来情况作出评价、预测B.投资决策需要相关C.筹资决策需要相关D.利润分配需要相关4.可理解性要求企业提供的会计信息应当(C)。

A.简单明了B.客观真实C.清晰明了便于财务报告使用者理解和使用D.便于决策5. 可比性要求同一企业对于不同时期发生的相同或相似的交易及事项应当采用( D )。

A.常用的会计政策B.相应的会计政策C.规定的会计政策D.一致的会计政策书P9明确写出,不得随意变更6.如果企业所处的经济环境发生变化,确实需要变更会计政策的(C)。

A.报经批准后直接改变B.由企业自行决定并选择相应的会计政策C.应当在附注中加以说明P10D.应当向企业外界发布公告7.在利润表中将主营业务收入与其他业务收入合并为营业收入一项内容,所反映的会计信息质量要求是(B)。

A.重要性B.实质重于形式按照经济实质进行会计确认计量报告,不应仅以交易或者事项的法律形式为依据,主营业务收入与其他业务收入均为收入,可以合并C.谨慎性D.可比性其他三项与该要求无关8.实质重于形式要求企业对交易或者事项进行会计确认、计量和报告时应按照其(A)。

[财经类试卷]会计专业技术资格中级财务管理(财务管理基础)模拟试卷15及答案与解析

![[财经类试卷]会计专业技术资格中级财务管理(财务管理基础)模拟试卷15及答案与解析](https://img.taocdn.com/s3/m/5644b8a084868762caaed563.png)

会计专业技术资格中级财务管理(财务管理基础)模拟试卷15及答案与解析一、单项选择题本类题共25小题,每小题1分,共25分。

每小题备选答案中,只有一个符合题意的正确答案。

多选、错选、不选均不得分。

1 在下列各项货币时间价值系数中,表示普通年金现值系数的是( )。

(A)[1一(1+i)-n]/i(B)i/[(1十i)n一1](C)[(1+i)n一1]/i(D)i/[1一(1+i)-n]2 在下列各项中,无法计算出确切结果的是( )。

(A)后付年金终值(B)即付年金终值(C)递延年金终值(D)永续年金终值3 第2至8年每年年初有等额收付款100元,此等额收付款在第1年年初的价值计算属于( )。

(A)预付年金现值计算(B)普通年金现值计算(C)递延年金现值计算(D)预付年金终值计算4 某公司第一年年初借款80000元,每年年末还本付息额均为16000元,连续9年还清。

则该项借款的实际利率为( )。

(A)13.72%(B)12%(C)14%(D)无法确定5 企业年初借得50000元贷款,10年期,年利率12%,每年末等额偿还。

已知年金现值系数(P/A,12%,10)=5.6502,则每年应偿还的金额为( )元。

(A)8849(B)5000(C)6000(D)282516 某人拟在5年后还清293330元债务,假定银行利息率为8%,5年、年利率为8%的年金终值系数为5.8666,5年、年利率为8%的年金现值系数为3.9927,则应从现在起每年末等额存入银行的偿债基金为( )元。

(A)58666(B)55000(C)56000(D)500007 某投资人于年初向银行存入10000元资金,年利率为4%,每半年复利一次,已知(F/P,4%,4)=1.1699,(F/P,2%,10)=1.2190,(F/P,2%,4)=1.0824,(F/P,2%,8)=1.1717,则第5年初可得到的本利和为( )元。

(A)11699(B)12190(C)11717(D)108248 已知(F/A,10%,9)=13.579,(F/A,10%,11)=18.531。

2024年国家电网招聘之财务会计类题库附答案(典型题)

2024年国家电网招聘之财务会计类题库附答案(典型题)单选题(共45题)1、企业在预测、决策的基础上,以数量和金额的形式反映企业未来一定时期内经营、投资、财务等活动的具体计划,为实现企业目标而对各种资源和企业活动做的详细安排指的是( )。

A.投资B.筹资C.预算D.分析与评价【答案】 C2、下列各项关于期初余额审计的表述中,不正确的是()。

A.如果与期初余额相关的会计政策未能在本期得到一贯运用,并且会计政策的变更未能得到正确的会计处理和恰当的列报,注册会计师应当出具保留意见或否定意见的审计报告B.注册会计师在执行财务报表审计时,必须对期初余额发表专门的审计意见C.注册会计师应当保持应有的职业谨慎,充分考虑期初余额对所审财务报表的影响D.注册会计师应当根据已获取的审计证据,形成对期初余额的审计结论,并在此基础上,确定其对审计意见的影响【答案】 B3、经常性调查和一次性调查的区别是()。

A.调查时间有无规律性B.调查时间间隔是否相等C.调查时间间隔是否超过一年D.调查时间是否连续【答案】 D4、如果注册会计师将财务报表日前适当日期作为函证的截止日,则说明注册会计师评估的认定层次重大错报风险是()。

A.高水平B.低水平C.特别风险D.无法应对风险【答案】 B5、A投资项目投资额为300万元,使用寿命15年,已知该项目第15年的经营净现金流量为40万元,期满处置固定资产残值收入及回收流动资金共12万元,则该投资项目第15年的净现金流量为()万元。

A.33B.55C.52D.40【答案】 C6、以下内部控制要素中,主要与财务报表层次的重大错报风险相关的是()。

A.控制活动B.信息系统与沟通C.控制环境D.对控制的监督【答案】 C7、能够使预算期间保持为一个固定长度的预算方法为( )。

A.弹性预算B.固定预算C.定期预算D.滚动预算【答案】 D8、某公司2011年年初的未分配利润为100万元,当年的税后利润为400万元,2012年年初公司讨论决定股利分配的数额。

会计基础各章节习题汇总

会计基础各章节习题汇总第一章会计的基本概念和会计核算的基本特征问题一什么是会计?回答一会计是一门研究经济活动中的资产负债关系、收入和费用关系以及所有者权益变动关系等问题,并进行相关记录和报告的学科。

它是一种通过对经济事务进行分类、计量、记录和汇总的方法,来提供经济信息,并为经济主体的决策和经营管理提供依据的技术。

问题二会计核算的基本特征有哪些?回答二会计核算的基本特征包括: 1. 记账原则:按照经济实质来进行会计核算,以真实、准确、完整地反映经济活动。

2. 会计等式:资产=负债+所有者权益,这是会计核算的基本平衡关系。

3. 会计分期:按照一定的时间段对经济活动进行核算,通常以年为单位,也可细化到月、季度或其他时间段。

4. 会计主体:会计核算对象是一个明确的经济实体,如企业、事业单位、个体工商户等。

5. 会计对象:会计核算范围包括资产、负债、所有者权益、收入和费用等。

第二章会计分录和账户的作用和基本方法问题三什么是会计分录?会计分录是会计核算的基本方法之一,是按照会计等式的平衡关系,将经济事项和交易分解为与其相关的借方和贷方,进行记录的过程。

会计分录通常包括借方金额、贷方金额和摘要等内容。

问题四账户的作用是什么?账户是会计核算的基本工具,它用于记录和整理经济交易和事件的借方和贷方发生额。

账户的作用包括: 1. 记录经济交易和事件的发生额,保证会计核算的准确性。

2. 提供对经济活动的追溯和分析,帮助经济主体了解其财务状况和经营情况。

3. 掌握经济主体的相对权益和所有者权益的变化,为决策和管理提供依据。

第三章会计凭证和会计账簿的用途和编制方法问题五什么是会计凭证?回答五会计凭证是会计核算的重要工具,用来记录和证明经济交易和事件的发生以及其对账户余额的影响。

会计凭证一般由凭证号码、日期、摘要、借方金额和贷方金额等组成。

问题六会计账簿的用途是什么?回答六会计账簿是对会计凭证进行分类、整理和汇总的工具,其中记录了经济交易和事件对各个账户的影响情况。

会计学-企业决策的基础 答案

管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based onmachine-hours:ManufacturingOverhead = $420,000 = $35 per machine-hour Machine-Hours 12,000Department Two overhead application rate based on direct labor hours:ManufacturingOverhead = $337,500 = $22.50 per direct labor hourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the Basic Chunksproduct line. Thus, the company’s current practice of using direct labor hours toallocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line isoverpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costing systeminclude: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrificesignificant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1B. Ex.18.1a. job costing (each project of a construction company is unique)b . both job and process costing (institutional clients may represent unique jobs)c. job costing (each set of equipment is uniquely designed andmanufactured)d . process costing (the dog houses are uniformly manufactured in high volumes)e. process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18.3Ab4,000 EU @ $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume =Fixed Costs + Target OperatingIncomeUnit Contribution Margin=$390,000 + $350,000= $20,000 units$37c.Current AfterCapacity Expansion(20,000Units)(25,000 Units) Total contribution margin ($37 per unit) $ 740,000 $ 925,000Less: Fixed costs390,000530,000*Operating income at full capacity $ 350,000$ 395,000*$390,000 + additional depreciation per year on newmachinery, $140,000 (20% of $700,000).盛年不重来,一日难再晨。

财务基础知识题库及答案

财务基础知识题库及答案

一、财务基础知识概述

1. 什么是财务管理?

财务管理是指对企业的财务活动进行全面的规划、组织、指导和控制,以达到有效利用资金、提高企业的经济效益的管理活动。

2. 财务管理的目标是什么?

财务管理的目标是实现资金最优配置,提高企业的盈利能力和竞争力。

3. 财务管理的职责包括哪些方面?

财务管理的职责包括财务规划、资金筹措、资金运用、成本控制、财务分析、利润分配等方面。

二、财务基础知识题库

1. 什么是资产负债表?

资产负债表是描绘一家企业在某一特定时间点的财务情况的财务报表,它显示了企业的资产、负债和所有者权益的情况。

2. 什么是利润表?

利润表是企业在一定时期内的经营活动所获得的盈利情况的财务报表,它包括营业收入、营业成本、税前利润等项目。

3. 企业的净资产等于什么?

企业的净资产等于资产减去负债,即所有者权益。

三、财务基础知识答案

1. 什么是资产负债表?

资产负债表是企业在某一特定时间点的财务情况的展示,它包括了企业拥有的资产和承担的负债,通过资产负债表可以了解企业的资产组成、负债情况以及净资产状况。

2. 什么是利润表?

利润表是反映企业在一定时期内盈亏情况的财务报表,也称为损益表。

它主要展示了企业在特定时期内的营业收入、营业成本、税前利润等财务指标,通过利润表可以了解企业的盈利能力和经营状况。

3. 企业的净资产等于什么?

企业的净资产等于资产减去负债,即所有者权益。

净资产是企业的净资产额,是企业资产中归所有者所有的部分。

企业的净资产反映了企业的所有者权益情况,也是企业的净值。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

3.6 Satka Fishing Expeditions ,Inc., recorded the following transactions in July…………………..Indicate the effects that each of these transactions will have upon the following six total amounts in the company’s financial statements for the month of July. Organize your answer in tabular form, using the column headings shown, and use the code letters I for increase, D for decrease, and NE for no effect.3.7 A number of transactions of Claypool Construction are described below in terms of accountsdebited and credited.a. Indicate the effects of each transactions upon the elements of the income statement and the balance sheet. Use the code letters I for increase, D for decrease, and NE for no effect. Organize your answer in tabular form, using the column headings shown,b. Write a one-sentence description of each transaction.3.8 Shown below are selected transactions of the architectural firm of Baxter, Claxter, and Stone,Inc.a. Prepare journal entries to record the transactions in the firm’s accounting records.b. Identify any of the above transactions that will not result in a change in the company’s net income.3.10 Trafflet Enterprises incorporated on May 3,2009. The company engaged in the followingtransactions during its first month of operations:a. Prepare journal entries, including explanations, for the above transactions.b. Post each entry to the appropriate ledger accountsc. Prepare a trial balance dated May 31, 2009. Assume accounts with zero balances are not included in the trial balance.3.11 The McMillan Corporation incorporated on September 2, 2009. The company engaged inthe following transactions during its first month of operations:a. Prepare journal entries, including explanations, for the above transactions.b. Post each entry to the appropriate ledger accountsc. Prepare a trial balance dated May 30, 2009. Assume accounts with zero balances are notincluded in the trial balance.Exercise 5.2Tutors for Rent, Inc., performs adjusting entries every month, but closes its accounts only at year-end. The company’s year-end adjusted trial balance dated December 31, 2009, was:TUTORS FOR RNET,INC.Adjusted Trial BalanceDecember 31, 2009 Cash....................................................................................... $91,100 Accounts receivable.....................................................................4,500 Supplies (300)Equipment………………………………………………………………………12,000 Accumulated depreciation: equipment…………………………………………$5,000 Accounts payable………………………………………………………………1,500 Income taxes payable………………………………………………………….. 3,500 Capital stock……………………………………………………………………25,000 Retained earnings………………………………………………………………45,000 Dividends………………………………………………………………………2,000Tutoring revenue earned………………………………………………………96,000 Salary expense…………………………………………………………………52,000Supply expense…………………………………………………………………1,200Advertising expense (300)Depreciation expense: equipment………………………………………………1,000 Income taxes expense………………………………………………………….. 11,600$176,000 $176,000 a. Prepare an income statement and statement of retained earnings for the year ended December31, 2009. Also prepare the company’s balance sheet dated December 31, 2009.b. Dose the company appear to be liquid? Defend your answer.c. Has the company been profitable in the past? Explain.Exercise 5.3Wilderness Guide Services, Inc., performs adjusting entries every month, but closes its accounts only at year-end. The company’s year-end adjusted trial balance dated December 31, 2009, follows:Wilderness Guide Services, Inc.Adjusted Trial BalanceDecember 31, 2009 Cash…………………………………………………………………………… $12,200Accounts receivable……………………………………………………………31,000Camping supplies………………………………………………………………7,900 Unexpired insurance policies………………………………………………….. 2,400 Equipment………………………………………………………………………70,000 Accumulated depreciation: equipment…………………………………………$60,000 Notes payable(due 4/1/10)…………………………………………………….. 18,000 Accounts payable………………………………………………………………9,500 Capital stock……………………………………………………………………25,000 Retained earnings………………………………………………………………15,000 Dividends………………………………………………………………………1,000Guide revenue earned…………………………………………………………102,000 Salary expense…………………………………………………………………87,500 Camping Supply expense………………………………………………………1,200 Insurance expense……………………………………………………………9,600 Depreciation expense: equipment………………………………………………5,000 Interest expense…………………………………………………………………1,700$229,500 $229,500 a. Prepare an income statement and statement of retained earnings for the year ended December31, 2009. Also prepare the company’s balance sheet dated December 31, 2009.(Hint: Unprofitable companies have no income taxes expense.)b. Dose the company appear to be liquid? Defend your answer.c. Has the company been profitable in the past? Explain.Exercise 5.10ORGON FOODSBalance SheetDecember 31, 2009Assets Cash.......................................................................................$6,800 Accounts receivable.....................................................................7,200 Office supplies (700)Prepaid rent……………………………………………………………………. 1,700Equipment……………………………………………………………………… $ 12,000 Accumulated depreciation: equipment……………………………………….. (4,800) $7,200 Total assets………………………………………………………….. $23,200LiabilitiesAccounts payable………………………………………………………………. $2,200 Income taxes payable……………………………………………………………1,800 Total Liabilities…………………………………………………………………. $4,000Stockholders’ EquityCapital stock……………………………………………………………………. $10,000 Retained earnings………………………………………………………………. 9,200 Total Stockholders’ Equity…………………………………………………….. $19,200 Total Liabilities and Stockholders’ Equity………………………………………$23,200Other information provided by the company is as follows:Total Revenue for the year ended December 31, 2009……………………………$25,500 Total ecpense for the year ended December 31, 2009………………………….....20,400 Total Stockholders’ Equity, January 1, 2009………………………………………14,800Compute and discuss briefly the significance of the following measures as they relate to Oregon Foods:a. Net income percentage in 2009.b. Return on equity in 2009.c. Working capital on December 31, 2009.d. Current ratio on December 31, 2009.10.2 Listed below are eight events or transactions of GemStar Corporation.Indicate the effects that each of these transactions on the following financial statements categories. Organize your answer in tabular form, using the column headings. Use the following code letters to indicate the effects of each transaction on the accounting element listed in the column heading: I for increase, D for decrease, and NE for no effect.10.9 Swanson Corporation issued $8 million of 20-year, 8 percent bonds on April 1, 2009, at102. Interest is due on March 31 and September 30 of each year, and all of the bonds in the issue mature on March 31, 2029. Swanson’s fiscal year ends on December 31. Prepare the following journal entries:Ex. 10.9a. 2009Apr. 1 Cash …………………………………………….8,160,000 Premium on Bonds Payable ………………… 160,000Bond Payable …………………………………8,000,000 To record issuance of bonds at 102.b. 2009Sept. 30 Bon d Interest Expense ……………316,000Pre mium on Bonds Payable ……… 4,000Cash …………………………320,000 To pay interest and amortize bond premium.Semiannual interest payment:$8,000,000 x 8% x 1/2 ……… $320,000Less premium amortized:[$160,000 / 20 yrs.] x 1/2 …… (4,000)Interest expense $316,000c. 2029Mar. 31 Bond Interest Payable ……………160,000Bon d Interest Expense ……………158,000Prem ium on Bonds Payable ………2,000Cash …………………………………320,000 To record final interest payment and amortizebond premium:(1) Interest expense for 3 months in 2029 = $316,000 x 3/6 = $158,000(2) Premium amortized in 2029 = $4,000 x 3/6 = $2,000(3) Interest payable from 12/31/28 = $320,000 x 3/6 = $160,000Mar. 31 Bonds Payable ……………………… 8,000,000Cash ……………………………………8,000,000 To retire bonds at maturity.d. (1) Amortization of a bond premium decreases annual interest expense and, consequently, increases annual net income.(2) Amortization of a bond premium is a noncash component of the annual interest expense computation. Thus, it has no effect upon annual net cash flow from operating activities. (Receipt of cash upon issuance of bonds and payment of cash to retire bonds at maturity are both classified as financing activities.)10.10 Mellilo Corporation issued $5 million of 20-year, 9.5 percent bonds on July 1,2009, at 98.Interest is due on June 30 and December 31 of each year, and all of the bonds in the issue mature on June 30,2009. Mellilo’s fiscal year ends on December 31. Prepare the following journal entries:Ex. 10.10a. 2009July 1 Cash ………………………4,900,000Discount on Bonds Payable … 100,000Bonds Payabl e ………………………5,000,000 To record issuance of bonds at 98.b. 2009Dec. 31 Bond Interest Expense ………………240,000Discount on Bonds Payable ……………… 2,500Cash ……………………………………237,500 To pay interest and amortize bond discount:Semiannual interest payment:$5,000,000 x 9 1/2% x 1/2 …….. $237,500Add discount amortized:[$100,000 ? 20 yrs.] x 1/2 …… 2,500Interest expense $240,000c. 2029June 30 Bond Interest Expense ……………… 240,000D iscount on Bonds Payable ……………2,500Cash ………………………………………… 237,500 To make final interest payment and amortize bond discount(same calculation as in part b. above).June 30 Bond Payable …………………………5,000,000Cash ………………………………………… 5,000,000 To retire bonds at maturity.d. (1) Amortization of bond discount increases annual interest expense and, consequently, reduces annual net income.(2) Amortization of bond discount is a noncash component of annual interest expense and has no effect upon annual net cash flow from operating activities. (Receipt of cash upon issuance of bonds and payment of cash to retire bonds at maturity are both classified as financing activities.)。