德勤-信用风险管理PPT课件

合集下载

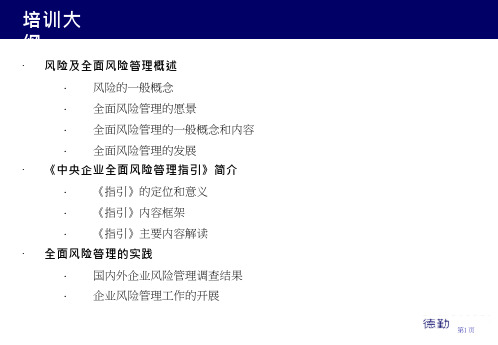

德勤企业全面风险管理专项培训ppt47页

控制措施

?

•流程是否存在•设计是否合理•职责是否明确•执行是否严格•奖惩是否明白•效果是否满意

•风险是否辨识•影响什么指标•影响哪些环节•影响哪些部门或 哪一级企业•分析是否彻底

•应对是否存在•设计是否合理•职责是否明确•是否经过检验•效果是否满意

参见《指引》 第五章

第29 页

参见《指引》第六章

风险管理的监控改进

战略趋同对于符合集团发展战略的风险,如投资风险,集团可以采取积极利用的态度对于不符合集团发展战略的风险,如非主业市场风险,集团应该采取坚决避免的态 度

管理能力对于集团管理能力较强的风险,如投资风险,集团可以采取积极利用的态度对于集团管理能力较差的风险,如业务模式风险,集团可以采取适度承担的态度

风险偏好

提炼

对比

分类组合

风险评估

不同类别收集的范围、方法、频率有所不同;注重信息的系统、完整、真实、及时

程序规范、方法合理

参见《指引》第二章

第18 页

风险评估是风险管理的基础,《指引》要求,“ 企业应对收集的风险管理初始信息和企业各项 业务管理及其重要业务流程进行风险评估。”

访谈研讨

定性定量 分析

其他工具 方法

风 险 战 略

组 织 职 能

综 合 内 控

风 险 理 财

风险管理信息系统

信 息 框 架

风 险 评 估

风 险 战 略

监 控 改 进解决 方 案

全面风险管理框架的结构

+

风险管理 基本流程

全面风险 管理体系

风险管理文化

第17 页

风险管理初始信息

收集与风险和风险管理相关的内外部信息,并将 其整理成可用于分析的形式,为风险评估和风险 战略的制定奠定基础。筛选

?

•流程是否存在•设计是否合理•职责是否明确•执行是否严格•奖惩是否明白•效果是否满意

•风险是否辨识•影响什么指标•影响哪些环节•影响哪些部门或 哪一级企业•分析是否彻底

•应对是否存在•设计是否合理•职责是否明确•是否经过检验•效果是否满意

参见《指引》 第五章

第29 页

参见《指引》第六章

风险管理的监控改进

战略趋同对于符合集团发展战略的风险,如投资风险,集团可以采取积极利用的态度对于不符合集团发展战略的风险,如非主业市场风险,集团应该采取坚决避免的态 度

管理能力对于集团管理能力较强的风险,如投资风险,集团可以采取积极利用的态度对于集团管理能力较差的风险,如业务模式风险,集团可以采取适度承担的态度

风险偏好

提炼

对比

分类组合

风险评估

不同类别收集的范围、方法、频率有所不同;注重信息的系统、完整、真实、及时

程序规范、方法合理

参见《指引》第二章

第18 页

风险评估是风险管理的基础,《指引》要求,“ 企业应对收集的风险管理初始信息和企业各项 业务管理及其重要业务流程进行风险评估。”

访谈研讨

定性定量 分析

其他工具 方法

风 险 战 略

组 织 职 能

综 合 内 控

风 险 理 财

风险管理信息系统

信 息 框 架

风 险 评 估

风 险 战 略

监 控 改 进解决 方 案

全面风险管理框架的结构

+

风险管理 基本流程

全面风险 管理体系

风险管理文化

第17 页

风险管理初始信息

收集与风险和风险管理相关的内外部信息,并将 其整理成可用于分析的形式,为风险评估和风险 战略的制定奠定基础。筛选

德勤-信用风险管理(英文PPT 35页)

Compliance

Transactions

Collateral management

Contracts & Documentation

Credit Risk Management

A complete and coherent risk management framework contains the following elements

Objectives

Type of Exposure

Instruments or Methods

Performance Management

Performance-based management utilizes metrics that measure actual performance against predetermined thresholds. The thresholds are established taking into account the organization’s strategy, operating environment and process controls.

Business Strategy Systems Operations Finance

Business Performance

Measures

Value Creation

Organizations need a rigorous set of measures to support continuous improvement

Credit Risk Management

Enhancing Your Bottom Line

The AFP 23rd Annual Conference New Orleans November 3-6, 2002

德勤风险管理课件

定期风险评估

定期对项目或企业进行风险评估,识 别潜在风险,制定应对措施。

强化风险意识

提高全员风险意识,使员工认识到风 险管理的重要性,并积极参与风险管 理。

风险监控与调整

对已实施的风险管理措施进行监控和 评估,根据实际情况进行调整和优化 。

风险监控与调整

01 持续监控

通过定期检查、审计和报告等方式,持续监控项 目或企业面临的风险。

转移风险

将风险转移给其他方,如 保险公司或承包商,以减 少自身承担的风险。

缓解风险

采取措施降低风险发生的 可能性或减轻风险发生时 的后果。

接受风险

在无法避免、转移或缓解 风险的情况下,接受并承 担风险,制定应急计划以 应对风险发生。

风险控制手段

建立健全风险管理机制

建立完善的风险管理流程和制度,明 确风险管理目标、原则和责任。

特点

风险管理具有综合性、系统性、复杂性和动态性的特点 。它需要综合考虑组织内外部的多种因素,运用多种方 法和工具,以实现对风险的有效管理和控制。

风险管理的意义

01

提高组织的安全性和稳定性

通过风险管理,组织可以有效地减少和避免潜在的风险事件,从而避免

或减少这些事件对组织造成的负面影响,提高组织的安全性和稳定性。

风险问卷调查:通过问卷 调查,收集不同部门和人 员的风险意见。

风险评估的流程

确定评估对象和目标

明确要评估的对象和评估 的目标。

收集信息

收集与评估对象相关的历 史数据、行业数据、内部 数据等。

风险分析

对收集到的数据进行深入 分析,预测可能的风险。

风险评级

根据分析结果,对每个风 险进行评级。

风险报告

撰写风险报告,总结评估 结果。

定期对项目或企业进行风险评估,识 别潜在风险,制定应对措施。

强化风险意识

提高全员风险意识,使员工认识到风 险管理的重要性,并积极参与风险管 理。

风险监控与调整

对已实施的风险管理措施进行监控和 评估,根据实际情况进行调整和优化 。

风险监控与调整

01 持续监控

通过定期检查、审计和报告等方式,持续监控项 目或企业面临的风险。

转移风险

将风险转移给其他方,如 保险公司或承包商,以减 少自身承担的风险。

缓解风险

采取措施降低风险发生的 可能性或减轻风险发生时 的后果。

接受风险

在无法避免、转移或缓解 风险的情况下,接受并承 担风险,制定应急计划以 应对风险发生。

风险控制手段

建立健全风险管理机制

建立完善的风险管理流程和制度,明 确风险管理目标、原则和责任。

特点

风险管理具有综合性、系统性、复杂性和动态性的特点 。它需要综合考虑组织内外部的多种因素,运用多种方 法和工具,以实现对风险的有效管理和控制。

风险管理的意义

01

提高组织的安全性和稳定性

通过风险管理,组织可以有效地减少和避免潜在的风险事件,从而避免

或减少这些事件对组织造成的负面影响,提高组织的安全性和稳定性。

风险问卷调查:通过问卷 调查,收集不同部门和人 员的风险意见。

风险评估的流程

确定评估对象和目标

明确要评估的对象和评估 的目标。

收集信息

收集与评估对象相关的历 史数据、行业数据、内部 数据等。

风险分析

对收集到的数据进行深入 分析,预测可能的风险。

风险评级

根据分析结果,对每个风 险进行评级。

风险报告

撰写风险报告,总结评估 结果。

德勤-信用风险管理

Credit Background

Thorough identification and accurate measurement of credit risk, supported by strong risk management can help improve the bottom line …..An uncertain and volatile economic

stability with higher P/E multiples – Marketplace penalizes credit induced volatility and “surprises”

Raises questions about quality of management

Corporate Credit Risk

– Project Finance – Structured Transactions – Leases with Recourse

Derivatives Exposures

– FX, Interest Rate Risk, Commodities etc.

Collateral Risk

– Parent or Third Party Guarantees – Commercial and Standby Letters of Credit

Effective credit risk management limits credit losses and provides stable cash flows and earnings – Marketplace rewards companies exhibiting earnings and cash flow

德勤-信用风险管理(英文PPT 35页)

Companies are exposed to significant levels of credit risk emanating from different sources

Accounts Receivables Other Notes Receivables Buyer and Franchise Financing With Recourse Financing

Effective credit risk management limits credit losses and provides stable cash flows and earnings – Marketplace rewards companies exhibiting earnings and cash flow

Credit Risk Management

Enhancing Your Bottom Line

The AFP 23rd Annual Conference New Orleans November 3-6, 2002

Ebrahim Shabudin Managing Director Deloitte & Touche LLP

Peer Average 51.3

Hypothetical

D Cash

DSOsቤተ መጻሕፍቲ ባይዱ

51.3

Q3 Sales

$261,201,000

\ Q3 A/R = $122,002,230 +$173,393,770

* Equals 295.4M/261.2M x 90(or number of days in sales period)

Credit as a Facilitator

Accounts Receivables Other Notes Receivables Buyer and Franchise Financing With Recourse Financing

Effective credit risk management limits credit losses and provides stable cash flows and earnings – Marketplace rewards companies exhibiting earnings and cash flow

Credit Risk Management

Enhancing Your Bottom Line

The AFP 23rd Annual Conference New Orleans November 3-6, 2002

Ebrahim Shabudin Managing Director Deloitte & Touche LLP

Peer Average 51.3

Hypothetical

D Cash

DSOsቤተ መጻሕፍቲ ባይዱ

51.3

Q3 Sales

$261,201,000

\ Q3 A/R = $122,002,230 +$173,393,770

* Equals 295.4M/261.2M x 90(or number of days in sales period)

Credit as a Facilitator

德勤信用风险管理(英文版)(PPT)

第二页,共三十六页。

Value Proposition

Credit plays a critical role in “selling〞 products and services Expands revenue opportunities with creditworthy, incremental customers Utilizes innovative structures to support business relationships

– Project Finance

– Structured Transactions

– Leases with Recourse

Derivatives Exposures

– FX, Interest Rate Risk, Commodities etc.

Collateral Risk

– Parent or Third Party Guarantees

tends to include managing on a transactional basis by evaluating specific attributes such as structuring, collateral and pricing

represents managing on a portfolio basis including aspects such as concentrations, correlations and diversification

Actual Q3 A/R Q3 Sales \ DSOs =

Company A $295,396,000 $261,201,000 124*

Peer Average 51.3

Value Proposition

Credit plays a critical role in “selling〞 products and services Expands revenue opportunities with creditworthy, incremental customers Utilizes innovative structures to support business relationships

– Project Finance

– Structured Transactions

– Leases with Recourse

Derivatives Exposures

– FX, Interest Rate Risk, Commodities etc.

Collateral Risk

– Parent or Third Party Guarantees

tends to include managing on a transactional basis by evaluating specific attributes such as structuring, collateral and pricing

represents managing on a portfolio basis including aspects such as concentrations, correlations and diversification

Actual Q3 A/R Q3 Sales \ DSOs =

Company A $295,396,000 $261,201,000 124*

Peer Average 51.3

德勤的信用风险管理

– Credit is a facilitator of business growth and performance

– High business margins tend to attract lower quality clients and therefore higher risk profile to maformance Management

Performance-based management utilizes metrics that measure actual performance against predetermined thresholds. The thresholds are established taking into account the organization’s strategy, operating environment and process controls.

2020/5/21

Corporate Credit Risk

• Companies are exposed to significant levels of credit risk emanating from different sources

• Accounts Receivables • Other Notes Receivables • Buyer and Franchise Financing • With Recourse Financing

Business Strategy Systems Operations Finance

– Project Finance – Structured Transactions – Leases with Recourse

– High business margins tend to attract lower quality clients and therefore higher risk profile to maformance Management

Performance-based management utilizes metrics that measure actual performance against predetermined thresholds. The thresholds are established taking into account the organization’s strategy, operating environment and process controls.

2020/5/21

Corporate Credit Risk

• Companies are exposed to significant levels of credit risk emanating from different sources

• Accounts Receivables • Other Notes Receivables • Buyer and Franchise Financing • With Recourse Financing

Business Strategy Systems Operations Finance

– Project Finance – Structured Transactions – Leases with Recourse

德勤-信用风险管理

Compliance

Transactions

Collateral management

Contracts & DocumentationCreΒιβλιοθήκη it Risk Management

A complete and coherent risk management framework contains the following elements

– Clients (buyers) may be concentrated in selected industries and provide limited portfolio diversification opportunity

– Poor credit risk management resulting in negative impact to bottom-line is heavily penalized by markets

The measures drive value creation and should support problem identification and correction.

Credit Risk Management’s Inter-related Activities

CREDIT POLICY

Companies are exposed to significant levels of credit risk emanating from different sources

Accounts Receivables Other Notes Receivables Buyer and Franchise Financing With Recourse Financing

德勤-信用风险管理

Reassessment Credit Strategy & Risk Tolerance

A New Paradigm

A new business paradigm had evolved: causing a lack of reliance on good fundamental analysis The idea that stock market values would continue to go up indefinitely

Monitoring/ Control

Risk Management

Exposure

Management

– Aggregation

– Control

Periodic Account Reviews – Payments/Aging – Credit Condition

Compliance with Covenants, Terms

stability with higher P/E multiples – Marketplace penalizes credit induced volatility and “surprises”

Raises questions about quality of management

Corporate Credit Risk

Credit Risk Management

Enhancing Your Bottom Line

The AFP 23rd Annual Conference New Orleans November 3-6, 2002

Ebrahim Shabudin Managing Director Deloitte & Touche LLP

德勤-信用风险管理

Improve Profitability

Credit Strategy/ Plan

Common Performance

Metrics

Credit Objectives and Risk

Tolerances

Credit Policies

Credit Risk Management

Processes

Reporting

Credit Risk Management

Enhancing Your Bottom Line

Ebrahim Shabudin Managing Director Deloitte & Touche LLP

Credit Background

Thorough identification and accurate measurement of credit risk, supported by strong risk management can help improve the bottom line …..An uncertain and volatile economic

Companies are exposed to significant levels of credit risk emanating from different sources

Accounts Receivables Other Notes Receivables Buyer and Franchise Financing With Recourse Financing

Recoveries

Disposal / Risk

mitigation

Collections

Exposure measurement

德勤-信用风险管理

Technology/Reports – Transactions/

Bookings

– Risk-adjusted

Return

Portfolio Management

Concentration

Diversification

Allowance for Bad Debts

Risk Mitigation

stability with higher P/E multiples – Marketplace penalizes credit induced volatility and “surprises”

Raises questions about quality of management

Corporate Credit Risk

The measures drive value oblem identification and correction.

Credit Risk Management’s Inter-related Activities

CREDIT POLICY

environment significantly impacts this ability …..The desire to grow and turn in outstanding

results has a tendency to put pressure on the checks and balances within businesses

– Clients (buyers) may be concentrated in selected industries and provide limited portfolio diversification opportunity

德勤-信用风险管理(英文PPT 35页)

Effective credit risk management limits credit losses and provides stable cash flows and earnings – Marketplace rewards companies exhibiting earnings and cash flow

Peer Average 51.3

Hypothetical

D Cash

DSOs

51.3

Q3 Sales

$261,201,000

\ Q3 A/R = $122,002,230 +$173,393,770

* Equals 295.4M/261.2M x 90(or number of days in sales period)

Credit as a Facilitator

Credit risk management is important

– Credit is a facilitator of business growth and performance

– High business margins tend to attract lower quality clients and therefore higher risk profile to manage

Credit Risk Areas to Consider

Origination/ Assessment

Sales Channels

Risk Strategy

Underwriting Standards

Credit Application

Analysis

Business/ Industry

Peer Average 51.3

Hypothetical

D Cash

DSOs

51.3

Q3 Sales

$261,201,000

\ Q3 A/R = $122,002,230 +$173,393,770

* Equals 295.4M/261.2M x 90(or number of days in sales period)

Credit as a Facilitator

Credit risk management is important

– Credit is a facilitator of business growth and performance

– High business margins tend to attract lower quality clients and therefore higher risk profile to manage

Credit Risk Areas to Consider

Origination/ Assessment

Sales Channels

Risk Strategy

Underwriting Standards

Credit Application

Analysis

Business/ Industry

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

environment significantly impacts this ability …..The desire to grow and turn in outstanding

results has a tendency to put pressure on the checks and balances within businesses

Peer Average 51.3

Hypothetical

D Sales

$261,201,000

\ Q3 A/R = $122,002,230 +$173,393,770

* Equals 295.4M/261.2M x 90(or number of days in sales period)

Companies are exposed to significant levels of credit risk emanating from different sources

Accounts Receivables Other Notes Receivables Buyer and Franchise Financing With Recourse Financing

– Note also that Critical Suppliers to the company may pose specific credit risk

4

DSO Impact … an example

Actual Q3 A/R Q3 Sales \ DSOs =

Company A $295,396,000 $261,201,000 124*

6

Credit Strategy & Risk Tolerance

Credit Strategy Statement and Specific Quantifiable Objectives Risk Tolerance

Coordination with Business Plan

Management Review Methodology

2

Value Proposition

Credit plays a critical role in “selling” products and services – Expands revenue opportunities with creditworthy, incremental

customers – Utilizes innovative structures to support business relationships

stability with higher P/E multiples – Marketplace penalizes credit induced volatility and “surprises”

Raises questions about quality of management

3

Corporate Credit Risk

Credit Risk Management

Enhancing Your Bottom Line

Ebrahim Shabudin Managing Director Deloitte & Touche LLP

1

Credit Background

Thorough identification and accurate measurement of credit risk, supported by strong risk management can help improve the bottom line …..An uncertain and volatile economic

Effective credit risk management limits credit losses and provides stable cash flows and earnings – Marketplace rewards companies exhibiting earnings and cash flow

Improve Profitability

Common Performance

Metrics

Credi t Strategy/Plan

Credit Objectives and Risk

Tolerances

Credit Policies

– Project Finance – Structured Transactions – Leases with Recourse

Derivatives Exposures

– FX, Interest Rate Risk, Commodities etc.

Collateral Risk

– Parent or Third Party Guarantees – Commercial and Standby Letters of Credit

5

Credit as a Facilitator

Credit risk management is important

– Credit is a facilitator of business growth and performance

– High business margins tend to attract lower quality clients and therefore higher risk profile to manage

– Clients (buyers) may be concentrated in selected industries and provide limited portfolio diversification opportunity

– Poor credit risk management resulting in negative impact to bottom-line is heavily penalized by markets

results has a tendency to put pressure on the checks and balances within businesses

Peer Average 51.3

Hypothetical

D Sales

$261,201,000

\ Q3 A/R = $122,002,230 +$173,393,770

* Equals 295.4M/261.2M x 90(or number of days in sales period)

Companies are exposed to significant levels of credit risk emanating from different sources

Accounts Receivables Other Notes Receivables Buyer and Franchise Financing With Recourse Financing

– Note also that Critical Suppliers to the company may pose specific credit risk

4

DSO Impact … an example

Actual Q3 A/R Q3 Sales \ DSOs =

Company A $295,396,000 $261,201,000 124*

6

Credit Strategy & Risk Tolerance

Credit Strategy Statement and Specific Quantifiable Objectives Risk Tolerance

Coordination with Business Plan

Management Review Methodology

2

Value Proposition

Credit plays a critical role in “selling” products and services – Expands revenue opportunities with creditworthy, incremental

customers – Utilizes innovative structures to support business relationships

stability with higher P/E multiples – Marketplace penalizes credit induced volatility and “surprises”

Raises questions about quality of management

3

Corporate Credit Risk

Credit Risk Management

Enhancing Your Bottom Line

Ebrahim Shabudin Managing Director Deloitte & Touche LLP

1

Credit Background

Thorough identification and accurate measurement of credit risk, supported by strong risk management can help improve the bottom line …..An uncertain and volatile economic

Effective credit risk management limits credit losses and provides stable cash flows and earnings – Marketplace rewards companies exhibiting earnings and cash flow

Improve Profitability

Common Performance

Metrics

Credi t Strategy/Plan

Credit Objectives and Risk

Tolerances

Credit Policies

– Project Finance – Structured Transactions – Leases with Recourse

Derivatives Exposures

– FX, Interest Rate Risk, Commodities etc.

Collateral Risk

– Parent or Third Party Guarantees – Commercial and Standby Letters of Credit

5

Credit as a Facilitator

Credit risk management is important

– Credit is a facilitator of business growth and performance

– High business margins tend to attract lower quality clients and therefore higher risk profile to manage

– Clients (buyers) may be concentrated in selected industries and provide limited portfolio diversification opportunity

– Poor credit risk management resulting in negative impact to bottom-line is heavily penalized by markets