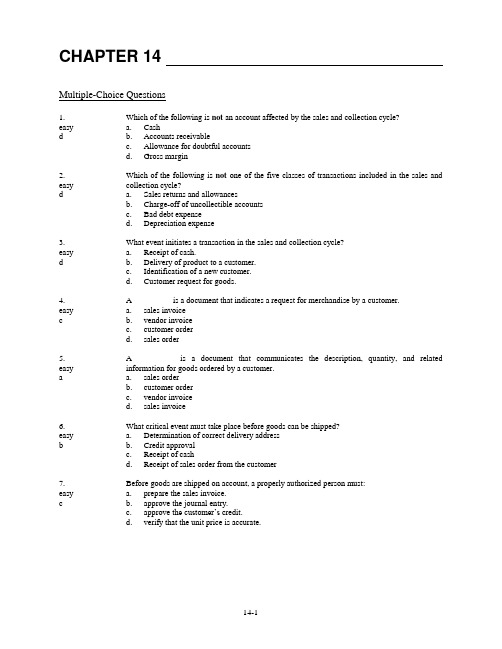

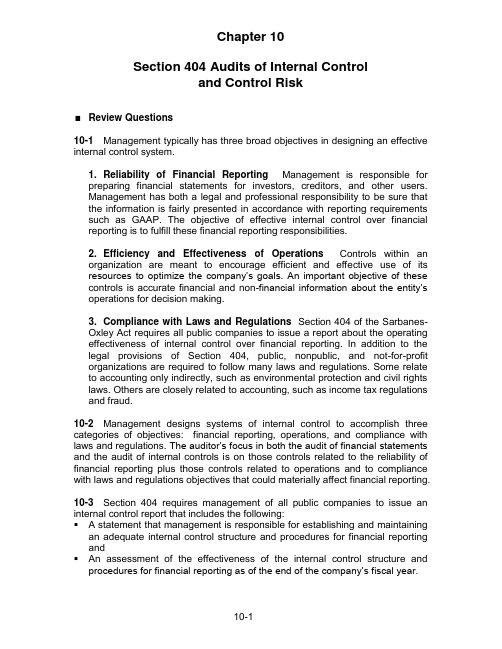

审计学:一种整合方法_第12版_英文版Chapter14

审计学:一种整合方法_第12版_英文版Chapter01-46页精选文档

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

1 - 10

Distinguish Between Auditing and Accounting

Accounting is the recording, classifying, and summarizing of economic events for the purpose of providing financial information used in decision making.

Auditing should be done by a competent, independent person.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

1-4

Information and Established Criteria

The competence of the individual performing the audit is of little value if he or she is biased in the accumulation and evaluation of evidence.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

1 - 12

Economic Demand for Auditing

Information risk reflects the possibility that the information upon which the business risk decision was made was inaccurate.

墨菲物流学英文版第12版课后习题答案

PART IIANSWERS TO END-OF-CHAPTER QUESTIONSCHAPTER 14: INTERNATIONAL LOGISTICS14-1. Discuss some of the key political restrictions on cross-border trade.Political restrictions on cross-border trade can take a variety of forms. Many nations ban certain types of shipments that might jeopardize their national security. Likewise, individual nations may band together to pressure another country from being an active supplier of materials that could be used to build nuclear weapons. Some nations restrict the outflow of currency because a nation,s economy will suffer if it imports more than it exports over a long term. A relatively commonpolitical restriction on trade involves tariffs, or taxes that governments place on the importation of certain items. Another group of political restrictions can be classified as nontariff barriers, which refer to restrictions other than tariffs that are placed upon imported products. Another political restriction involves embargoes, or the prohibition of trade between particular countries.14-2. How might a particular country,s government be involved in international trade?Governments may exert strong control over ocean and air traffic because they operate as extensions of a nation,s economy and most of the revenue flows into that nation's economy. In some cases, import licenses may restrict movement to a vessel or plane owned or operated by the importing country. In addition, some nations provide subsidies to develop and/or maintain their ocean and air carriers. Governments also support their own carriers through cargo preference rules, which require a certain percentage of traffic to move on a nation,s flag vessels. Although federal governments have often owned ocean carriers and international airlines, some government-owned international carriers are moving toward the private sector.14-3. Discuss how a nation,s market size might impact international trade and, in turn,international logistics.Population is one proxy for market size, and China and India account for about one-third of the world's population. As such, these two countries might be potentially attractive markets because of their absolute and relative size. Having said this, India has a relatively low gross domestic product per capita, and because of this some customers buy singleuse packets of products called sachets. From a logistical perspective, single-use packets require different packaging, and are easier to lose and more prone to theft than products sold in larger quantities.14-4. How might economic integration impact international logistics?Potential logistical implications of economic integration include reduced documentation requirements, reduced tariffs, and the redesign of distribution networks. For example,Poland and the Czech Republic have become favorite distribution sites with the eastward expansion of the European Union.14-5. How can language considerations impact the packaging and labeling of international shipments?With respect to language, cargo handlers may not be able to read and understand the language of the exporting country, and it would not be unusual for cargo handlers in some countries to beilliterate. Hence, cautionary symbols, rather than writing, must be used. A shipper,s mark, which looks like a cattle brand, is used in areas where dockworkers cannot read but need a method to keep documents and shipments together.14-6. What is a certificate of origin, a commercial invoice, and a shipper,s export declaration?A certificate of origin specifies the country or countries in which a product is manufactured .This document can be required by governments for control purposes or by an exporter to verify thelocation of manufacture. A commercial invoice is similar in nature to a domestic bill of lading in the sense that a commercial invoice summarizes the entire transaction and contains (or should contain) key information to include a description of the goods, the terms of sale and payment, the shipment quantity, the method of shipment, and so on. A shipper,s export declaration contains relevant export transaction data such as the transportation mode(s), transaction participants, and a description of what is being exported.14-7. Discuss international terms of sale and Incoterms.International terms of sale determine where and when buyers and seller will transfer 1) the physical goods; 2) payment for goods, freight charges, and insurance for the in-transit goods; 3) legal title to the goods; 4) required documentation; and 5) responsibility for controlling or caring for the goods in transit. The International Chamber of Commerce is in charge of establishing, and periodically revising, the terms of sale for international shipments, commonly referred to as Incoterms. The most recent revision, Incoterms 2010, reflects the rapid expansion of global trade with a particular focus on improved cargo security and new trends in cross-border transportation. Incoterms 2010 are now organized by modes of transport and the terms can be used in both international and domestic transportation.14-8. Name the four methods of payment for international shipments. Which method is riskiest for the buyer? For the seller?Four distinct methods of payment exist for international shipments: cash in advance, letters of credit, bills of exchange, and the open account. Cash in advance is of minimal risk to the seller, but is the riskiest for the buyer-what if the paid-for product is never received? The open account involves tremendous potential risk for the seller and minimal risk for the buyer.14-9. Discuss four possible functions that might be performed by international freight forwarders.The text describes eight functions, such as preparing an export declaration and booking space on carriers, so discussion of any four would be appropriate.14-10. What is an NVOCC?An NVOCC (nonvessel-operating common carrier) is often confused with an international freight forwarder. Although both NVOCCs and international freight forwarders must be licensed by the Federal Maritime Commission, NVOCCs are common carriers and thus have common carrier obligations to serveand deliver, among other obligations. NVOCCs consolidate freight from different shippers and leverage this volume to negotiate favorable transportation rates from ocean carriers. From the shipper's perspective, an NVOCC is a carrier; from an ocean carrier,s perspective, an NVOCC is a shipper.14-11. What are the two primary purposes of export packing?One function is to allow goods to move easily through customs. For a country assessing duties on the weight of both the item and its container, this means selecting lightweight packing materials. The second purpose of export packing is to protect products in what almost always is a more difficult journey than they would experience if they were destined for domestic consignees.14-12. Discuss the importance of water transportation for international trade.A frequently cited statistic is that approximately 60 percent of cross-border shipments move by water transportation. Another example of the importance of water transportation in international trade involves the world,s busiest container ports as measured by TEUs (twenty-foot equivalent units) handled; 9 of the 10 busiest container ports are located in Asia, with 7 of the busiest ports located in China.14-13. Explain the load center concept. How might load centers affect the dynamics of international transportation?Load centers are major ports where thousands of containers arrive and depart each week. As vessel sizes increase, it becomes more costly to stop at multiple ports in a geographic area, and as a result, operators of larger container ships prefer to call at only one port in a geographic area. Load centers might impact the dynamics of international trade in the sense that some ports will be relegated to providing feeder service to the load centers.14-14. Discuss the role of ocean carrier alliances in international logistics.In the mid-1990s, ocean carrier alliances, in which carriers retain their individual identities but cooperate in the area of operations, began forming in the container trades. These alliances provide two primary benefits to participating members, namely, the sharing of vessel space and the ability to offer shippers a broader service network. The size of the alliance allows them to exercise considerable clout in their dealings with shippers, port terminal operators, and connecting land carriers.14-15. How do integrated air carriers impact the effectiveness and efficiency of international logistics?Integrated air carriers own all their vehicles and the facilities that fall in-between. These carriers often provide the fastest service between many major points. They are also employed to carry the documentation that is generated by—and is very much a part of— the international movement of materials. The integrated carriers also handle documentation services for their clients.14-16. How do open-skies agreements differ from bilateral agreements?Bilateral agreements generally involved two countries and tended to be somewhat restrictive in nature. For example, the bilateral agreements would specify the carriers that were to serve particular city pairs. By contrast, open skies agreements liberalize aviation opportunities andlimit federal government involvement. For example, the Open Aviation Agreement between the United States and 27 European Union (EU) member states allows any EU airline as well as any U.S. airline to fly between any point in the EU and any point in the United States.14-17. Discuss the potential sources of delays in certain countries with respect to motor carrier shipments that move across state borders.One source of delays is that certain countries limit a motor carrier,s operations to within a particular state,s borders; as a result, multi-state shipments must be transferred from one company,s vehicle to another company,s vehicle whenever crossing into another state. Another source of delays is that certain countries conduct inspections of trucks as they move from one state to another. This can include physical counting and inspection of all shipments, inspection of documentation, and vehicle inspection, as well as driver inspection.14-18. Define what is meant by short-sea shipping (SSS), and discuss some advantages of SSS.Short-sea shipping (SSS) refers to waterborne transportation that utilizes inland and coastal waterways to move shipments from domestic ports to their destination. Potential benefits to SSS include reduced rail and truck congestion, reduced highway damage, a reduction in truck-related noise and air pollution, and improved waterways utilization.14-19. What are some challenges associated with inventory management in cross-border trade?Because greater uncertainties, misunderstandings, and delays often arise in international movements, safety stocks must be larger. Furthermore, inventory valuation on an international scale isdifficult because of continually changing exchange rates. When a nation,s (or the world's) currency is unstable, investments in inventories rise because they are believed to be less risky than holding cash or securities.Firms involved in international trade must give careful thought to their inventory policies, in part because inventory available for sale in one nation may not necessarily serve the needs of markets in nearby nations. Product return policies are another concern with respect to international inventory management. One issue is that, unlike the United States where products can be returned for virtually reason, some countries don,t allow returns unless the product is defective in some respect.14-20. What is the Logistics Performance Index? How can it be used?The Logistics Performance Index (LPI) was created in recognition of the importance of logistics in global trade. The LPI measures a country,s performance across six logistical dimensions:•Efficiency of the clearance process (i.e., speed, simplicity, and predictability of formalities) by border control agencies, including customs;•Quality of trade- and transport-related infrastructure (e.g., ports, railroads, roads, and information technology);•Ease of arranging competitively priced shipments;•Competence and quality of logistics services (e.g., transport operators and customs brokers);•Capability to track and trace consignments;•Timeliness of shipments in reaching the destination within the scheduled or expected delivery time.The LPI is a potentially valuable international logistics tool because the data can be analyzed from several different perspectives. First, the LPI can be analyzed for all countries according to the overall LPI score as well as according to scores on each of the six dimensions. Second, the LPI can be analyzed in terms of an individual country's performance over time, relative to its geographic region, and relative to its income group.PART IIICASE SOLUTIONSCASE 14-1: Nurnberg Augsburg Maschinenwerke (N.A.M.)Question 1: Assume that you are Weiss. How many viable alternatives do you have to consider regarding the initial shipment of 25 buses?The answer to this question can vary depending on how students define “viable alternatives.” If we take a broad perspective and just focus on the primary cities, Bremerhaven does not appear to be an option because there is no scheduled liner service in the desired time frame. That leaves us with Prague to Santos through Hamburg and Prague to Santos through Rotterdam. Several of the vessel departure dates for both alternatives are not feasible. For example, the 18-day transit time from Hamburg eliminates both the October 31 and November 3 departures; likewise, the 17-day transit time from Rotterdam eliminates the November 2 departure. And although the October 27 departure from Hamburg or the October 28 departure from Rotterdam should get the buses to Santos by November 15, neither departure leaves much room for potential transit delays (e.g., a late season hurricane). As such, it appears that Weiss has but two viable alternatives: the October 24 departure from Hamburg and the October 23 departure from Rotterdam.Question 2: Which of the routing alternatives would you recommend to meet the initial 90-day deadline for the 25-bus shipment? Train or waterway? To which port(s)? What would it cost?If one assumes that rail transport is used from Prague to either Hamburg or Rotterdam, then thetotal transportation costs of the two alternatives are virtually identical. Although rail costs to Rotterdam are €300 higher than to Hamburg, the shipping costs from Rotterdam are €300 lower than from Hamburg (based on €6000 x .95). Because the total transportation costs are essentially the same, the decision likely needs to be based on service considerations. The initial shipment is extremely important. It might be suggested that Prague to Hamburg by rail and Hamburg to Santos by ocean vessel is the preferred alternative. Our rationale is that the provided transit times with Hamburg are definitive— that is, 3 days by rail and 18 days by water. With Rotterdam, by contrast, the rail transit time is either 4 or 5 days, although water transportation is 17 days.Question 3: What additional information would be helpful for answering Question 2?A variety of other information would be helpful for answering Question 2. For example, the case offers no insight about port congestion issues and how this congestion might impact the timeliness of shipment loadings. There also is no information about port performance in terms of loss and damage metrics. In addition, although the case indicates that rail transit time from Prague iseither four or five days, it might be helpful to know what percentage of shipments is completed in four days. Students are likely to come up with more suggestions.Question 4: How important, in fact, are the transport costs for the initial shipment of 25 buses?Clearly, with ocean shipping costs of either €5700 or €6000 per bus, transportation costs cannot be ignored. Having said this, the initial shipment holds the key to the remainder of the order (another 199 buses) and appears to be instrumental in securing another order for 568 buses (for a total of 767 more buses). As such, N.A.M might be somewhat flexible with respect to transportation costs for the initial shipment. Suppose, for example, that N.A.M. can earn a profit of €5000 per bus (such profit on a €120000 bus is by no means exorbitant). A profit of €5000 x 767 buses yields a total profit of €3,835,000. Because of such a large upside with respect to additional orders,N.A.M. might focus on achieving the specified metrics for the initial shipment without being overly concerned with transportation costs.Question 5: What kinds of customer service support must be provided for this initial shipment of 25 buses? Who is responsible?Although a number of different constituencies is involved in the initial shipment (e.g., railroads, dock workers, ocean carrier, etc.), the particular customers—the public transit authorities—are buying product from N.A.M. Because of this, N.A.M. should be the responsible party with respect to customer service support. There are myriad customer service support options that might be provided. Real-time shipment tracking should be an option so that the customers can know, at any time, the location of the shipment. N.A.M. might also provide regular updates of shipment progress; perhaps N.A.M. could email or fax important progress points (e.g., the shipment has left Prague; the shipment has arrived in Hamburg, etc.) to the customers. Because successful performance on theinitial shipment is crucial to securing future business, N.A.M. might have one of its managers actually accompany the shipment.Question 6: The Brazilian buyer wants the buses delivered at Santos. Weiss looks up theInternational Chamber of Commerce,s Incoterms and finds three categories of “delivered” terms:DAT (Delivered at Terminal). In this type of transaction, the seller clears the goods forexport and bears all risks and costs associated with delivering the goods and unloading them at the terminal at the named port or place of destination. The buyer is responsible for all costs and risks from this point forward including clearing the goods for import at the named country of destination.DAP (Delivered at Place). The seller clears the goods for export and bears all risks and costs associated with delivering goods to the named place of destination not unloaded. The buyer is responsible for all costs and risks associated with unloading the goods and clearing customs to import goods into the named country of destination.DDP (Delivered Duty Paid). The seller bears all risks and costs associated with delivering the goods to the named place of destination ready for unloading and clearing for import.How should he choose? Why?Again, given the importance of the initial shipment, it would appear that the more control thatN.A.M. has over the process, the better. Although the DDP option is likely the costliest option, it also affords N.A.M. more control later into the shipment process. Moreover, a willingness by N.A.M. to take on the additional costs associated with DDP might be viewed in a positive fashion by the customers.Question 7: Would you make the same routing recommendation for the second, larger (199 buses) component of the order, after the initial 90-day deadline is met? Why or why not?Time pressures do not appear to be as critical for the larger component of the order, so this might argue for use of water transportation between Prague and Hamburg. The rationale would be that even though water transportation is slower, it saves money (€48 per bus) over rail shipments. Alternatively, given that the selling price per bus is likely to be around €120000, trading off three days of transit time in exchange for a savings of €48 might not be such a good idea.Question 8:How important, if at all, is it for N.A.M. to ship via water to show its support of the European Union,s Motorways of the Seas concept?This question may generate a variety of opinions from students. For example, some students might argue that Question 75s answer also applies to Question 8. Having said this, the case doesn,t delve too deeply into potential environmental considerations associated with water transportation, so a pure cost-benefit analysis (such as Question 7) might be insufficient. Furthermore, because the European Union (EU) continues to be a contentious issue for many Europeans, the answer to Question 8 might depend upon one,s view of the EU. Thus, someone who is supportive of the EU might lean toward supporting the Motorways of the Seas concept, while someone not supportive of the EU might lean against supporting the Motorways of the Seas concept.。

审计学-一种整合的方法

4 - 12

Resolving Ethical Dilemmas

4. Identify the alternatives available to the person who must resolve the dilemma

5. Identify the likely consequence of each alternative

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

4 - 16

Special Need for Ethical Conduct in Professions

Our society has attached a special meaning to the term professional. Professionals are expected to conduct themselves at a higher level than most other members of society.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

4-6

A Person Chooses to Act Selfishly – Example

Person A finds a briefcase containing important papers and $1,000. He tosses the briefcase and keeps the money.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 4 - 14

审计学:一种整合方法_第12版_英文版Cha(1)

Accumulating Evidence and Evaluating Evidence

Evidence is any information used by the auditor to determine whether the information being audited is stated in accordance with the established criteria.

Determines correspondence

Report on results

Report on tax deficiencies

Established criteria

Internal Revenue Code and all

interpretations

Learning Objective 2

Auditing is determining whether recorded information properly reflects the economic events that occurred during the accounting period.

Learning Objective 3

The final stage in the auditing process is preparing the Audit Report, which is the communication of the auditor’s findings to users.

Audit of a Tax Return Example

Learning Objective 1

Describe auditing.

Nature of Auditing

审计学-一种整合的方法

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-3

Steps to Develop Audit Objectives

1. Understand objectives and responsibilities for the audit.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-5

Learning Objective 2

Distinguish management’s

responsibility for the financial

6-4Βιβλιοθήκη Steps to Develop Audit Objectives

4. Know general audit objectives for classes of transactions and accounts.

5. Know specific audit objectives for classes of transactions and accounts.

statements and internal control

from the auditor’s responsibility

for verifying the financial

statements and effectiveness

of internal control.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

审计学:一种整合方法阿伦斯英文版第12版课后问题详解Chapter18SolutionsManual

Chapter 18Audit of the Payroll andPersonnel CycleReview Questions18-1 General ledger accounts that are likely to be affected by the payroll and personnel cycle in most audits include the following:Cash Direct laborInventory Salary expenseConstruction in progress Commission expenseWages payable Payroll tax expensePayroll taxes withheldAccrued payroll taxes18-2In companies where payroll is a significant portion of inventory, as in manufacturing and construction companies, the improper account classification of payroll can significantly affect asset valuation for accounts such as work in process, finished goods, and construction in process. For example, if the salaries of administrative personnel are incorrectly charged to indirect manufacturing overhead, the overhead charged to inventory on the balance sheet can be overstated. Similarly, if the indirect labor cost of individual employees is charged to specific jobs or processes, the valuation of inventory is affected if labor is improperly classified. When some jobs are billed on a cost plus basis, revenue and the valuation of inventory are both affected by improperly classifying labor to jobs.18-3Five tests of controls that can be performed for the payroll and personnel cycle are:1. Examine time card for indication of approval to ensure thatpayroll payments are properly authorized. The purpose ofthis test is to determine that recorded payroll payments arefor work actually performed by existing employees(occurrence).2. Account for a sequence of payroll checks to ensure existingpayroll payments are recorded. The purpose of this test isto determine that existing payroll transactions are recorded(completeness).3. Examine time cards to ensure that recorded payroll paymentsare for work actually performed by existing employees. The purpose of this test is the same as in item 1 above.4. Compare postings to the chart of accounts to ensure thatpayroll transactions are properly classified.(Classification)5. Observe when recording takes place to ensure that payrolltransactions are recorded on a timely basis. (Timing)18-4The percentage of total audit time in the cycle devoted to performing tests of controls and substantive tests of transactions is usually far greater in the payroll and personnel cycle than for the sales and collection cycle because there is relatively little independent third party evidence, such as confirmation, to verify the related payroll accounts. In contrast, the accounts related to the sales and collection cycle can usually be verified for the most part by confirmations from customers. In addition, in the sales and collection cycle, verification of the realizability of receivables and sales cutoff tests are important and time- consuming tasks.18-5The auditor should be concerned with whether the human resources department is following the proper hiring and termination procedures. An obvious reason for this would be to ensure that there are adequate safeguards against hiring and retaining incompetent and untrustworthy people. The ramifications of hiring such people can range from simple inefficiency and waste to outright fraud or theft. More importantly, though, it is necessary for the auditor to assure himself or herself that the client is hiring and terminating according to operations standards and procedures. It is necessary to see if the internal controls are working as planned before they can be effectively evaluated. To say that the auditor doesn't care who is hired and who is fired is to suggest that he or she doesn't care if the internal controls work according to any standards. Failure to follow proper termination procedures could lead to fraudulent payments for work not performed.18-6To trace a random sample of prenumbered time cards to the related payroll checks in the payroll register and compare the hours worked to the hours paid is to test if those employees who worked are being paid for their time actually worked. Employees are likely to inform management if they are not paid, or underpaid. To trace a random sample of payroll checks from the payroll register and compare the hours worked to the hours paid is to test if the recorded payroll payments are for work actually performed by existing employees. This test, in effect, attempts to discover nonexistent employees or duplicate payments, if there are any. For this reason, the second procedure is typically more important to the audit of payroll.18-7In auditing payroll withholding and payroll tax expense, the emphasis should normally be on evaluating the adequacy of the payroll tax return preparation procedures rather than the payroll tax liability, because a major reason for misstatements in the liability account is incorrect preparation of the returns in the past. If the preparationprocedures are inadequate, and the amounts do not appear reasonable, then the auditor should expand his or her work and recompute the withholding and expense amounts to determine that the proper amount has been accrued. In addition, the auditor should consider the amount of penalties which may be assessed for inadequate withholdings and include these amounts in the accrual if they are significant.18-8Several analytical procedures for the payroll and personnel cycle and misstatements that might be indicated by significant fluctuations are as follows:18-9An auditor should perform audit tests primarily designed to uncover fraud in the payroll and personnel cycle when he or she has determined that internal controls are deficient (or the opportunity exists for management to override the internal controls) or when there are other reasons to suspect fraud. Audit procedures that are primarily for the detection of fraud in the payroll and personnel cycle include:1. Examine cancelled payroll checks for employee name,authorized signature, and proper endorsement (especially forsecond endorsements) to discover checks going to nonexistentemployees. The endorsement should be compared to signatureson W-4 forms.2. Trace selected transactions recorded in the payroll journalor listing to the human resources department files to determine whether the employees were actually employed during the period.3. Select several terminated employees from payroll records todetermine whether each former employee received his or her termination pay in accordance with company policy and to determine that the employee's pay was discontinued on the date of termination.18-9 (continued)4. Examine the subsequent payroll periods of terminatedemployees to ascertain that the employees are no longerbeing paid.5. Request a surprise payroll payoff to observe if anyunclaimed checks result, which will necessitate extensiveinvestigation.18-10 The Payroll Master File is maintained for each employee indicating the gross pay for each payment period, deductions from the gross pay, the net pay, the check number, and the date. The purpose of this record is to provide detailed information for federal and state income tax purposes, and to serve as the final record of what each employee was actually paid.The W-2 Form is issued to each employee at the end of each calendar year and indicates his or her gross pay, income taxes withheld, and FICA withheld for the year. In serving as a summary of the employee's earnings record, the W-2 form conveniently provides information necessary for the employee to fill out his or her income tax returns.A Payroll Tax Return is the form required by and submitted to the local, state and federal governments for the payment of withheld taxes and the employer's portion of FICA taxes and state and federal unemployment compensation taxes.18-11 Where the primary objective is to detect fraud, the auditor will examine the following supporting documents and records:1. Cancelled payroll checks for employee name, authorizedsignature and proper endorsement, watching specifically forunusual or recurring second endorsements.2. Payroll journal or listing, tracing transactions to thepersonnel files to determine whether the employees wereactually employed during the payroll period.3. Payroll journal or listing and individual payroll records,selecting terminated employees to determine whether eachterminated employee received his or her termination pay inaccordance with company policy and whether each employee waspaid in the subsequent payroll period.4. Payroll checks, observing each employee as he or she picksup and signs for his or her check.5. Time cards, testing them for reasonableness or observingwhether they are being punched by the proper employees.18-12 Types of authorizations in the payroll and personnel cycle are:1. Deduction authorization, without which the wrong amount (orno deduction) may be deducted from the employee's paycheck.2. Rate authorizations, without which the employee may begetting paid at the wrong rate.3. Time card authorization, without which the employee may begetting paid for the wrong quantity of hours worked.18-12(continued)4. Payroll check authorization, without which unauthorizedfunds may be paid out.5. Commission rate authorization, without which the salespeoplemight be improperly compensated for their sales efforts.6. Authorization to hire a new employee, without whichnonexistent or unqualified personnel may be added to thepayroll.18-13 It is common to verify total officers' compensation even when the tests of controls and substantive tests of transactions results in payroll are excellent because the salaries and bonuses of officers must be included in the SEC's 10-K Report and the federal income tax return and because management may be in a position to pay themselves more than the authorized amount, since the controls over the officers' payroll are typically weaker and therefore easier to override than those of the normal payroll.The usual audit procedure used to verify the officers' compensation is to obtain the authorized salary of each officer from the minutes of the board of directors and compare it to the related earnings record.18-14 An imprest payroll account is a separate payroll bank account in which a constant balance, either zero or small, is maintained. When a payroll is paid, the exact amount of the net payroll is transferred by check or electronic funds transfer from the general account to the imprest account. The purpose and advantage of an imprest payroll account is that it limits the company's exposure to payroll fraud by limiting the amount that may be misappropriated.18-15 Several audit procedures the auditor can use to determine whether recorded payroll transactions are recorded at the proper amounts are:1. Recompute hours worked from time cards.2. Compare pay rates with union contract, approval by the boardof directors, or other source.3. Recompute gross pay.4. Check withholdings by reference to tax tables andauthorization forms in personnel files.5. Recompute net pay.6. Compare cancelled check with payroll journal or listing foramount.18-16 Attributes sampling can be used in the payroll and personnel cycle in performing tests of controls and substantive tests of transactions with the following objectives:1. Time card hours agree with payroll computations.2. Overtime hours are approved.3. Foreman approves all time cards.4. Hourly rates agree with personnel files and union contracts.18-16 (continued)5. Gross pay calculation is verified.6. Exemptions taken agree with W-4.7. Income tax, other deductions, and net pay calculations areverified.8. Authorizations are available for voluntary withholdings andmiscellaneous deductions.9. Paycheck endorsement is same as signature on W-4 form.The frequency of control deviations or monetary errors must be estimated prior to performing the tests. This estimate together with the acceptable risk of assessing control risk too low (ARACR) and the tolerable exception rate will enable the auditor to determine the sample size required. Once the tests are performed on the sample, evaluation of the results will indicate whether the exception rate is lower than, equal to, or higher than that anticipated. The auditor must then use this judgment to decide the appropriate action to take.Multiple Choice Questions From CPA Examinations18-17 a. (2) b. (1) c. (3)18-18 a. (1) b. (4) c. (4) d. (4)Discussion Questions and Problems18-1918-2018-2118-2218-23 A flowchart of steps for each type of test is given below(requirements a, b, and c):18-24 a. Brendin's approach to determining why this year's payroll tax expense was so high suffers from two seriousdeficiencies: First, it lacks relevance, and second, it istoo narrowly focused. The approach lacks relevance in thathe is testing payroll withholding which is not the same aspayroll tax expense. Some payroll taxes are related towithholding such as FICA, but income tax withheld does notgive rise to an expense, and certain payroll taxes, such asunemployment compensation, are not withheld. The approach istoo narrowly focused in that the analytical test resultscould have resulted from a misstatement of the payrollitself; Brendin does not appear to be considering thispossibility.b. A more suitable approach for determining whether payroll taxwas properly stated in the current year would be to evaluatethe reasonableness of the total payroll, reconcile thepayroll to amounts shown on payroll tax reports, and checkcomputations as shown on those reports for reasonableness.18-25 The following audit procedures should be used to verify the payroll related accounts:1. Accrued payroll:a. Review the company's policy for computing the accrualand whether it is consistent with the prior year.b. Assess whether 60 percent is a reasonableapproximation of the portion of the subsequent payrollapplication to the current year.c. Test the subsequent payroll for cutoff and accuracy.d. Determine that the computation of the accrual iscorrect.2. Withheld payroll taxes:a. Compare the balance in the liability account with thepayroll journal or listing.b. Reconcile the amount to subsequent payroll tax reportsand cash disbursed.c. Review in light of the subsequent period's payroll.3. Accrued payroll taxes:a. Trace FICA withheld from payroll journal or listing topayroll tax reports.b. Review amounts on payroll tax reports forreasonableness.c. Reconcile accruals to payroll tax reports.d. Examine subsequent cash disbursed.18-26 a. The purpose of a surprise payroll payoff is to determine whether or not nonexistent personnel are included in thepayroll.b. Procedures other than a surprise payroll payoff that can beused to discover nonexistent employees are:1. Examine cancelled payroll checks for employee name,authorized signature, and proper endorsement that agreeswith the employee's signed W-4 form.18-26(continued)2. Select several terminated employees from payroll recordsto determine whether each former employee received his orher termination pay in accordance with company policy andwas not paid in subsequent payrolls.c. When the payroll payoff is taking place, the client shouldobserve these control procedures:1. All employees must prove identity.2. Unclaimed paychecks must be further investigated.Unclaimed paychecks might be accounted for byemployees who are sick or on vacation. After allpresent employees have received their checks, theremaining paychecks should be traced to the personnelfiles to determine if these employees were everemployed by the client. Thereafter, if practical, theremaining checks should be held until the employeescan be present with proper identification to claim thecheck.d. See c.2 above.18-2718-27 (continued)18-28 a. An audit program to verify sales commission expense is as follows:1. Select a sample of office copies of sales invoices.a. Check commissions rate to commissions rate file.b. Check computation of sales commissions.c. Examine invoices for internal verification byaccounts receivable clerk.d. Trace sales commission amounts to salescommission ledger.2. Foot the sales commission ledger for one or moremonths, and trace the total to the general ledger.3. Compare totals for periods in the sales commissionledger to period balances of sales commission expense.b. An audit program to verify accrued sales commissions is:1. Compare the accrual with that of the previous year.Investigate any significant change.2. Compare the amount of commissions paid to the salesmenon the fifteenth of the month following year-end tothe total accrued commissions at year-end. Obtain areconciliation and explanation for any reconcilingitems.3. Send confirmations to salesmen for the larger amountsof accrued commissions and a sample of the smalleramounts.Case18-29 a. Conventional forms and documents in a payroll system include the following:Personnel recordsDeduction authorization formsRate authorization formsTime cards and job time ticketsPayroll checksPayroll journal or listing and labor distributionEarnings recordW-2 formPayroll tax returnsIn using the computer service center, it appears that there is no loss in documentation in substance; however, theearnings record is not printed out each pay period, thus,the current version is usually in machine readable form.(This assumes that authorization forms exist although theyare not discussed in the case.) The fact that the earningsrecord is in magnetic form is not a problem, as long as theservice bureau has adequate backup and recovery controls.The above analysis reflects the fact that Leggert's internal controls in the payroll area are generally good.There is good segregation of duties between the Presidentand Clark, assuming both are trustworthy, honest people.Procedures, forms, records, and reports are comprehensiveand well-designed.The only potential deficiency in internal control is that errors in details could be made by the service bureauand not necessarily be caught. It is difficult to imagine that these would be material.18-29 (continued)b.c. Procedures in performance format:1. Make observations of the following activities by MaryClark:a) Control, collection and processing of time cards.b) Rechecking of hours on time cards.c) Processing and approval of payroll journal or listing.d) Posting of general ledger.2. Make observations of the following activities by thePresident:a) Maintenance of personnel files.b) Distribution of paychecks.c) Processing and approval of payroll journal or listing.d) Posting of general ledger.3. Make observations of the following general matters andactivities:a) Use of time clock by employees.b) Existence and use of adequate chart of accounts.4. Select a sample of payroll check numbers and:a) Account for existence and recording of paychecks.b) Examine paychecks for President's signature.c) Examine checks for proper endorsement.d) Compare cancelled checks with personnel records. 18-29 (continued)e) Compare date on check with date recorded inpayroll journal or listing and on the time card.5. Select a sample of payroll entries from the payrolljournal or listing and perform the following steps:a) Obtain time cards, examine for President'sapproval, and trace hours to payroll journal orlisting.b) Examine personnel files and authorization forrates and deductions.c) Recompute gross pay, deductions, and net pay.d) Compare account classification with chart ofaccounts or procedures manual.6. Select a sample of payroll journals and perform thefollowing steps:a) Examine payroll journal for approval by Clark.b) Trace postings to general ledger.d. A sampling data sheet follows. Note that this sampling datasheet was prepared using attributes sampling. The onlydifference between this approach and a nonstatisticalapproach is the determination of sample size. Undernonstatistical sampling, students’ sample sizes will vary.Internet Problem Solution: Outsourcing the Payroll Function18-1 You have just landed a new client for your firm - a new hotel constructed in Atlanta, Georgia. Although construction of the hotel is complete, the company has not completed hiring all the necessary employees. The company's president has approached you with several questions related to the company's payroll. Please answer the following questions posed by the president about outsourcing the payroll function. (Hint: Visit [/] to find some of your answers. You may need to do other research on the Internet to answer these questions.)1.“I'm considering outsourcing our payroll function. What aresome of the issues that I should think about before deciding to outsource?”Answer: Student responses will vary. However, the following issues are among those that the president should consider:∙Typical outsourcing agreements are long-term. A long-term contract with the outsourcing provider mayprove inflexible if future business needsnecessitate a change.∙Outsourcing results in a loss of control over the company’s data. The president may be concernedabout sharing of data with competitors.∙The president should also consider the adequacy of the service provider’s system. Does the providerutilize the most current technology? Can theprovider manage a significant increase in volume oftransactions? Will the provider continue to offerexcellent service?∙Can the service provider deliver all of the necessary salaries and wages reports and analysesthat the company may want or need?∙Costs are typically lower when outsourcing major IS functions. The company will be able to avoidinvestments in certain hardware and software as wellas in personnel if the payroll function isoutsourced.2.“If I decide to outsource the payroll function, whatpayroll service companies would you suggest I consider?”Answer: There are a variety of payroll service companies including ADP [/] and Ceridian [/].18-1 (continued)3.“I have several vacant positions at my new hotel. I'mconcerned that my beginning salaries might be too low. Couldyou find out what nationwide median salaries are for thevacant positions? The vacant positions are: restaurantmanager, catering sales manager, security director, and thefront office manager. Make certain that you let me know whatsalaries are in our region of the country. I may have notconsidered that properly when I advertised the positions.”Answer: Median salary information can be found on’s web site. The “HCECompensation”link[/careerresources/lodgprop.asp] will direct students to the appropriate location.There they will have to select the appropriate categorywhich, in this case, is a “lodging property.”Studentsshould then scroll down the salaries information until theyfind data for the South Atlantic Region. The median salariesare: restaurant manager - $37,151.62; catering sales manager- $38,472.10; security director - $52,810.67; and frontoffice manager - $37,947.73. You might wish to point out tothe students the difficulty in interpreting such data asthat presented on this site. Specifically, median salariesdata are presented for a number of categories such as sizeof facility, geographic region, and location. Theinquisitive student should inquire about these differencesand so a liberal view may be appropriately applied whengrading this component of the problem.(Note: Internet problems address current issues using Internet sources. Because Internet sites are subject to change, Internet problems and solutions are subject to change. Current information on Internet problems is available at /arens).。

审计学:一种整合方法_第12版_英文版Cha

Financial Statements Cycles

Learning Objective 4

• Classify transactions and account • balances into financial statement • cycles and identify benefits of a • cycle approach to segmenting • the audit.

Objective of Conducting an Audit o f Financial Statements

The objective of the ordinary audit of financial statements is the expression of an opinion of the fairness with which they present fairly, in all respects, financial position, result of operations, and its cash flows in conformity with GAAP.

Management’s Responsibilities

Management is responsible for the financial statements and for internal control.

The Sarbanes-Oxley Act increases management’s responsibility for the finຫໍສະໝຸດ ncial statements.

The Sarbanes-Oxley Act provides for criminal penalties for anyone who knowingly falsely certifies the statements.

审计学:一种整合方法_第12版_英文版Chapter14

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

14 - 9

Bad Debt Expense Transaction

Accounts Business Functions Documents and Records

Accounts receivable trial balance

Monthly statement

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

14 - 14

Processing and Recording Cash Receipts

Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions

Chapter 14

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

14 - 2

Accounts in the Sales and Collection Cycle

Sales Cash sales

Sales on account Accounts Receivable Beginning Cash receipts balance Sales on account Ending balance Sales returns and allowances Write-off of uncollectible accounts

审计学一种整合方法英文版第十四版教学设计 (2)

Audit: A Comprehensive Approach to Integrated Methodology - Teaching Design for the 14th Edition BackgroundAuditing is a crucial aspect of modern business practices. It involves examining financial statements, records, and operations to ensure that they comply with legal and industry standards. To prepare students for this critical field of work, a comprehensive approach for auditing must be taught. The 14th edition of the Audit: A Comprehensive Approach to Integrated Methodology textbook is designed to provide students with a comprehensive understanding of auditing.Learning ObjectivesThe primary learning objectives of this course are to:•Introduce students to the fundamentals of auditing.•Equip students with the knowledge necessary to understand how auditing is conducted.•Teach students to think critically and analyze data to identify potential issues.• d students in developing strong communication skills.•Help students understand the legal and ethical issues that arise in the field of auditing.Course OutlineThe course is divided into ten modules, each contning several chapters. The breakdown is as follows:Module 1: Introduction to AuditingThis module introduces students to the basics of auditing and explns the importance of the field in modern business practices.Module 2: The Auditing ProcessHere, students learn about the various steps involved in theauditing process, including planning, testing, and reporting.Module 3: Risk AssessmentThis module focuses on teaching students the importance of risk assessment in auditing and helps them understand how to identify potential risks.Module 4: Internal ControlsIn this module, students learn about the essential role of internal controls in auditing and how to design and evaluate internal controls.Module 5: Audit EvidenceThis module focuses on teaching students how to gather and analyze audit evidence to support their findings.Module 6: SamplingHere, students learn about the importance of sampling in auditing and how to design and use different sampling techniques.Module 7: Fraud DetectionThis module teaches students about the various types of fraud, how to detect them, and how to design internal controls to prevent fraud from occurring.Module 8: Legal EnvironmentIn this module, students learn about the legal and ethical issues that arise in the field of auditing.Module 9: Audit ReportsHere, students learn about the different types of audit reports and how to write them.Module 10: Special Auditing TopicsThe final module covers special topics in auditing, such as auditing information systems and environmental auditing.Teaching MethodologyThe course will be taught using a variety of methods, including lectures, case studies, and group projects. The lectures will provide students with an overview of the module topics and key concepts, while case studies will allow them to apply their knowledge to real-world scenarios. Group projects will encourage students to collaborate with their peers and develop strong communication and teamwork skills.AssessmentAssessment will be based on a combination of quizzes, exams, case studies, and group projects. The quizzes and exams will test students’understanding of the module topics, while the case studies and group projects will assess their ability to apply their knowledge to real-world situations.ConclusionThe 14th edition of Audit: A Comprehensive Approach to Integrated Methodology provides students with a comprehensive understanding of auditing and prepares them for successful careers in the field. Through a combination of lectures, case studies, and group projects, students will learn how to think critically, analyze data, and communicate effectively in this critical field.。

审计学:一种整合方法(英文版) 第14版 参考答案AEB14_SM_CH01_v1

Chapter 1The Demand for Audit and Other Assurance ServicesReview Questions1-1The relationship among audit services, attestation services, and assurance services is reflected in Figure 1-3 on page 12 of the text. An assurance service is an independent professional service to improve the quality of information for decision makers. An attestation service is a form of assurance service in which the CPA firm issues a report about the reliability of an assertion that is the responsibility of another party. Audit services are a form of attestation service in which the auditor expresses a written conclusion about the degree of correspondence between information and established criteria.The most common form of audit service is an audit of historical financial statements, in which the auditor expresses a conclusion as to whether the financial statements are presented in accordance with an applicable financial reporting framework such as U.S. GAAP or IFRS. An example of an attestation ser vice is a report on the effectiveness of an entity’s internal control over financial reporting. There are many possible forms of assurance services, including services related to business performance measurement, health care performance, and information system reliability.1-2 An independent audit is a means of satisfying the need for reliable information on the part of decision makers. Factors of a complex society which contribute to this need are:1. Remoteness of informationa. Owners (stockholders) divorced from managementb. Directors not involved in day-to-day operations or decisionsc. Dispersion of the business among numerous geographiclocations and complex corporate structures2. Biases and motives of providera. Information will be biased in favor of the provider when his orher goals are inconsistent with the decision maker's goals.3. Voluminous dataa. Possibly millions of transactions processed daily viasophisticated computerized systemsb. Multiple product linesc. Multiple transaction locations4. Complex exchange transactionsa. New and changing business relationships lead to innovativeaccounting and reporting problemsb. Potential impact of transactions not quantifiable, leading toincreased disclosures1-3 1. Risk-free interest rate This is approximately the rate the bank could earn by investing in U.S. treasury notes for the same length of timeas the business loan.2. Business risk for the customer This risk reflects the possibility thatthe business will not be able to repay its loan because of economicor business conditions such as a recession, poor managementdecisions, or unexpected competition in the industry.3. Information risk This risk reflects the possibility that the informationupon which the business risk decision was made was inaccurate. Alikely cause of the information risk is the possibility of inaccuratefinancial statements.Auditing has no effect on either the risk-free interest rate or business risk. However, auditing can significantly reduce information risk.1-4The four primary causes of information risk are remoteness of information, biases and motives of the provider, voluminous data, and the existence of complex exchange transactions.The three main ways to reduce information risk are:1. User verifies the information.2. User shares the information risk with management.3. Audited financial statements are provided.The advantages and disadvantages of each are as follows:1-5 To do an audit, there must be information in a verifiable form and some standards (criteria) by which the auditor can evaluate the information. Examples of established criteria include generally accepted accounting principles and the Internal Revenue Code. Determining the degree of correspondence between information and established criteria is determining whether a given set of information is in accordance with the established criteria. The information for Jones Company's tax return is the federal tax returns filed by the company. The established criteria are found in the Internal Revenue Code and all interpretations. For the audit of Jones Company's financial statements the information is the financial statements being audited and the established criteria are generally accepted accounting principles.1-6The primary evidence the internal revenue agent will use in the audit of the Jones Company's tax return include all available documentation and other information available in Jones’ office or from other sources. For example, when the internal revenue agent audits taxable income, a major source of information will be bank statements, the cash receipts journal and deposit slips. The internal revenue agent is likely to emphasize unrecorded receipts and revenues. For expenses, major sources of evidence are likely to be cancelled checks and electronic funds transfers, vendors' invoices, and other supporting documentation.1-7This apparent paradox arises from the distinction between the function of auditing and the function of accounting. The accounting function is the recording, classifying and summarizing of economic events to provide relevant information to decision makers. The rules of accounting are the criteria used by the auditor for evaluating the presentation of economic events for financial statements and he or she must therefore have an understanding of accounting standards, as well as auditing standards. The accountant need not, and frequently does not, understand what auditors do, unless he or she is involved in doing audits, or has been trained as an auditor.1-81-9Five examples of specific operational audits that could be conducted by an internal auditor in a manufacturing company are:1. Examine employee time records and personnel records to determineif sufficient information is available to maximize the effective use ofpersonnel.2. Review the processing of sales invoices to determine if it could bedone more efficiently.3. Review the acquisitions of goods, including costs, to determine ifthey are being purchased at the lowest possible cost consideringthe quality needed.1-9 (continued)4. Review and evaluate the efficiency of the manufacturing process.5. Review the processing of cash receipts to determine if they aredeposited as quickly as possible.1-10 When auditing historical financial statements, an auditor must have a thorough understanding of the client and its environment. This knowledge should include the client’s regulatory and operating environment, business strategies and processes, and measurement indicators. This strategic understanding is also useful in other assurance or consulting engagements. For example, an auditor who is performing an assurance service on information technology would need to understand the client’s business strategies an d processes related to information technology, including such things as purchases and sales via the Internet. Similarly, a practitioner performing a consulting engagement to evaluate the efficiency and effectiveness of a client’s manufacturing process woul d likely start with an analysis of various measurement indicators, including ratio analysis and benchmarking against key competitors.1-11 The major differences in the scope of audit responsibilities are:1. CPAs perform audits in accordance with auditing standards ofpublished financial statements prepared in accordance with U.S.GAAP or IFRS.2. GAO auditors perform compliance or operational audits in order toassure the Congress of the expenditure of public funds in accordancewith its directives and the law.3. IRS agents perform compliance audits to enforce the federal taxlaws as defined by Congress, interpreted by the courts, and regulatedby the IRS.4. Internal auditors perform compliance or operational audits in orderto assure management or the board of directors that controls andpolicies are properly and consistently developed, applied andevaluated.1-12 The four parts of the Uniform CPA Examination are: Auditing and Attestation, Financial Accounting and Reporting, Regulation, and Business Environment and Concepts.1-13 It is important for CPAs to be knowledgeable about information technology, including e-commerce, because many of their clients rely extensively on these technologies. Examples of commonly used e-commerce technologies include purchases and sales of goods through the Internet, automatic inventory reordering via direct connection to inventory suppliers, and online banking. CPAs who perform audits or provide other assurance services about information generated with these technologies need a basic knowledge and understanding of information technology and e-commerce in order to identify and respond to risks in the financial and other information generated by these technologies.Multiple Choice Questions From CPA Examinations1-14 a. (3) b. (2) c. (2) d. (3)1-15 a. (2) b. (3) c. (4) d. (3)Discussion Questions And Problems1-16 a. The relationship among audit services, attestation services and assurance services is reflected in Figure 1-3 on page 12 of the text.Audit services are a form of attestation service, and attestationservices are a form of assurance service. In a diagram, auditservices are located within the attestation service area, andattestation services are located within the assurance service area.b. 1. (2) An attestation service other than an audit service2. (1) An audit of historical financial statements3. (2) An attestation service other than an audit service4. (2) An attestation service other than an audit service; or(3) An assurance service that is not an attestation service(WebTrust developed from the AICPA Special Committeeon Assurance Services, but the service meets thecriteria for an attestation service.)5. (2) An attestation service other than an audit service6. (2) An attestation service other than an audit service7. (2) An attestation service that is not an audit service(Review services are a form of attestation, but areperformed according to Statements on Standards forAccounting and Review Services.)8. (2) An attestation service other than an audit service9. (2) An attestation service other than an audit service10. (3) An assurance service that is not an attestation service 1-17 a. The interest rate for the loan that requires a review report is lower than the loan that did not require a review because of lowerinformation risk. A review report provides moderate assurance tofinancial statement users, which lowers information risk. An auditreport provides further assurance and lower information risk. As aresult of reduced information risk, the interest rate is lowest for theloan with the audit report.b. Given these circumstances, Busch should select the loan from FirstCity Bank that requires an annual audit. In this situation, theadditional cost of the audit is less than the reduction in interest dueto lower information risk. The following is the calculation of totalcosts for each loan:c. Busch should select the loan from United National Bank due to thehigher cost of the audit and the reduced interest rate for the loanfrom United National Bank. The following is the calculation of totalcosts for each loan:d. Busch may desire to have an audit because of the many otherbenefits that an audit provides. The audit will provide Busch’smanagement with assurance about annual financial information usedfor decision-making purposes. The audit may detect errors or fraud, andprovide management with information about the effectiveness ofcontrols. In addition, the audit may result in recommendations tomanagement that will improve efficiency or effectiveness.e. The auditor must have a thorough understanding of the client and itsenvironment, including the client’s e-commerce technologies, industry,regulatory and operating environment, suppliers, customers, creditors,and business strategies and processes. This thorough analysis helpsthe auditor identify risks associated with the client’s strategies thatmay affect whether the financial statements are fairly stated. Thisstrategic knowledge of the client’s business often helps the auditoridentify ways to help the client improve business operations, therebyproviding added value to the audit function.1-18 a. The services provided by Consumers Union are very similar to assurance services provided by CPA firms. The services providedby Consumers Union and assurance services provided by CPAfirms are designed to improve the quality of information for decisionmakers. CPAs are valued for their independence, and the reportsprovided by Consumers Union are valued because ConsumersUnion is independent of the products tested.b. The concepts of information risk for the buyer of an automobile andfor the user of financial statements are essentially the same. They are both concerned with the problem of unreliable information being provided. In the case of the auditor, the user is concerned about unreliable information being provided in the financial statements.The buyer of an automobile is likely to be concerned about the manufacturer or dealer providing unreliable information.c. The four causes of information risk are essentially the same for abuyer of an automobile and a user of financial statements:(1) Remoteness of information It is difficult for a user to obtainmuch information about either an automobile manufactureror the automobile itself without incurring considerable cost.The automobile buyer does have the advantage of possiblyknowing other users who are satisfied or dissatisfied with asimilar automobile.(2) Biases and motives of provider There is a conflict betweenthe automobile buyer and the manufacturer. The buyer wantsto buy a high quality product at minimum cost whereas theseller wants to maximize the selling price and quantity sold.(3)Voluminous data There is a large amount of availableinformation about automobiles that users might like to havein order to evaluate an automobile. Either that information isnot available or too costly to obtain.(4) Complex exchange transactions The acquisition of anautomobile is expensive and certainly a complex decisionbecause of all the components that go into making a goodautomobile and choosing between a large number ofalternatives.d. The three ways users of financial statements and buyers ofautomobiles reduce information risk are also similar:(1) User verifies information him or herself That can be obtainedby driving different automobiles, examining the specifications ofthe automobiles, talking to other users and doing research invarious magazines.(2) User shares information risk with management Themanufacturer of a product has a responsibility to meet itswarranties and to provide a reasonable product. The buyerof an automobile can return the automobile for correction ofdefects. In some cases a refund may be obtained.(3) Examine the information prepared by Consumer ReportsThis is similar to an audit in the sense that independentinformation is provided by an independent party. Theinformation provided by Consumer Reports is comparable tothat provided by a CPA firm that audited financial statements.1-19 a. The following parts of the definition of auditing are related to the narrative:(1) Altman is being asked to issue a report about qualitative andquantitative information for trucks. The trucks are thereforethe information with which the auditor is concerned.(2) There are four established criteria which must be evaluatedand reported by Altman: existence of the trucks on the nightof June 30, 2011, ownership of each truck by RegionalDelivery Service, physical condition of each truck and fairmarket value of each truck.(3) Samantha Altman will accumulate and evaluate four types ofevidence:(a) Count the trucks to determine their existence.(b) Use registrations documents held by Burrow forcomparison to the serial number on each truck todetermine ownership.(c) Examine the trucks to determine each truck's physicalcondition.(d) Examine the blue book to determine the fair marketvalue of each truck.(4) Samantha Altman, CPA, appears qualified, as a competent,independent person. She is a CPA, and she spends most ofher time auditing used automobile and truck dealerships andhas extensive specialized knowledge about used trucksthat is consistent with the nature of the engagement.(5) The report results are to include:(a) which of the 25 trucks are parked in Regional'sparking lot the night of June 30.(b) whether all of the trucks are owned by RegionalDelivery Service.(c) the condition of each truck, using establishedguidelines.(d) fair market value of each truck using the current bluebook for trucks.b. The only parts of the audit that will be difficult for Altman are:(1) Evaluating the condition, using the guidelines of poor, good,and excellent. It is highly subjective to do so. If she uses adifferent criterion than the "blue book," the fair market valuewill not be meaningful. Her experience will be essential inusing this guideline.(2) Determining the fair market value, unless it is clearly definedin the blue book for each condition.1-20 a. The major advantages and disadvantages of a career as an IRS agent, CPA, GAO auditor, or an internal auditor are:(b) Other auditing careers that are available are:Auditors within many of the branches of the federal government(e.g., Atomic Energy Commission)Auditors for many state and local government units (e.g., state insurance or bank auditors)1-21 The most likely type of auditor and the type of audit for each of the examples are:1-22 a. Financial statement audits reduce information risk, which lowers borrowing costs. An audit also provides assurances to managementabout information used for decision-making purposes, and may alsoprovide recommendations to improve efficiency or effectiveness ofoperations.b. Hogan and Czarnecki likely provide tax services, accountingservices, and management advisory services. They may also provideadditional assurance and attestation services other than audits offinancial statements.c. Student answers will vary. They may identify new types of informationthat require assurance, such as environmental or corporateresponsibility reporting. Students may also identify opportunitiesfor consulting or management advisory services, such as assistancewith the adoption of international financial reporting standards.Internet Problem Solution: CPA RequirementsInternet Problem 1-1a. Answers will vary by state. Most states require 150 hours ofeducation, with specific requirements for number of accounting hoursand credit hours in other subject areas.b. Most states have frequently addressed questions. Many of theseaddress education requirements, as well as information on how toprepare for the exam, as well as information on applying for licensure.Internet Problem 1-1 (continued)c. The Elijah Watt Sells award program was established in 1923by the American Institute of Certified Public Accountants(AICPA) to recognize outstanding performance on the UniformCPA Examination. The Sells award is presented annually to tencandidates with the highest cumulative scores who completedtesting during the previous calendar year and passed all foursections of the Uniform CPA Examination on their first attempt.d. Passing information is available on the CPA Examination portion ofthe AICPA web site. Recent passing rates have been approximately45% for each section.(Note: Internet problems address current issues using Internet sources. Because Internet sites are subject to change, Internet problems and solutions may change. Current information on Internet problems is available at /arens.)。

审计学一种整合方法第英文版

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

1-4

Information and Established Criteria

The Act established the Public Company Accounting Oversight Board.

It also requires auditors to attest to management reports on the effectiveness of internal control over financial reporting.

1-3

Nature of Auditing

Auditing is the accumulation and evaluation of evidence about information to determine and report on the degree of correspondence between the information and established criteria.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

1-6

Competent, Independent Person

The auditor must be qualified to understand the criteria used and must be competent to know the types and amount of evidence to accumulate to reach the proper conclusion after the evidence has been examined.

审计学一种整合方法第版英文版Chapter

Four-Step Approach to Designing Control and Substantive Tests

Apply transaction-related audit objectives to a class

of transactions (Step 1)

Further Audit Procedures

Tests of controls Substantive tests of transactions Analytical procedures Tests of details of balances

Relationship Between Further Audit Procedures and Evidence Type of Evidence

tests of transactions for sales and collection cycle

Audit procedures Sample size

Items to select Timing

Approach to Designing Tests of Details of Balances

Inquiries of the Client Reperformance Analytical Procedures Recalculation

Further Audit Procedures

Tests of controls Substantive tests of transactions Analytical procedures Tests of details of balances

Role of All Audit Tests in the Sales and Collection Cycle

审计学:一种整合方法_第12版_英文版Chapter01

1 - 11

Learning Objective 3

Explain the importance of auditing in reducing information risk.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

The competence of the individual performing the audit is of little value if he or she is biased in the accumulation and evaluation of evidence.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

1 - 16

Learning Objective 5

Describe assurance services and distinguish audit services from other assurance and nonassurance services provided by CPAs.

1 - 18

Attestation Services

An attestation service is a type of assurance service in which the CPA firm issues a report about the reliability of an assertion that is the responsibility of another party.

审计学:一种整合方法_第12版_英文版Chapter01-46页PPT资料

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

1-1

Learning Objective 1

Describe auditing.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

1-2

Nature of Auditing

Auditing is the accumulation and evaluation of evidence about information to determine and report on the degree of correspondence between the information and established criteria.

1-7

Audit of a Tax Return Example

Competent, independent

person

Information

Federal tax returns filed by taxpayer

Internal Revenue

Chapter14 - final