【复旦大学 投资学】Section3 Returns equity mutual funds

复旦

2013复旦大学431考研真题【回忆版】名词解释:1.汇率超调2.Sharpe指数3.在险价值(Value at risk)4.实物期权5.资本结构均衡分析选择:1.马克维茨组合的假设中哪个正确2.以下几个中收益率最高A半年复利率10% B年复利率10% C年连续复利率10% D忘了3.完美市场,如果再仅仅考虑税收,高股利政策是有益有害?如果仅仅考虑信息不对称,高股利政策有益有害?4.无税MM,甲乙公司财务杠杆不一样,其他都一样。

甲负债权益50%:50%,乙40%:60%,投资者有8%甲股票,什么情况下继续持有甲股票A:甲公司价值大于一公司B:无套利均衡C:忘了D:忘了5.通胀、逆差,用什么政策计算:1.股票收益率和a指数计算2.给出各种成本,折旧方法,计算NPV,财务盈亏平衡点简答:1:金融市场功能2:为什么NPV法最可靠论述:1.07年美国金融危机是否与有效市场假设直接相关2.汇率对国际收支影响,什么情况会使一些国家统一货币,根据国金理论分析欧元危机(25分)第一题选择B是年复利8% D是年复利10%马克维茨的那个看了书应该是选“投资者都是风险规避者”第二题我选了A.半年利率高股利那个题,考虑税收有害,考虑不对称有益第四题选了无套利均衡2013年复旦大学431金融学综合大部分试题回忆一、名词解释夏普指数实物期权风险作用资本结构权衡理论二选择题三计算题1运用CAPM求两只股票的期望收益率,然后求出超常收益率,并分析X,Y两只股票,方差X 大于方差Y,收益率X大于Y,各自符合下面哪两个方案:a:一支股票与风险被充分分散了的组合b:单独持有一只股票2求净现值和盈亏平衡点,题目含折旧(直线折旧法求)四解答题1简述金融系统的功能和作用这道题我用一些金融工具来答了,比如期货,还有利率,感觉没怎么答好2为什么净现值法是最不容易犯错的资本预算法?我把资本预算法中所有的方法都列出来了,并分析了个方法容易犯的错误五论述题1有人说美国2007金融危机的原因是因为基于“有效市场”的治理原则,请对此观点作出评价,并谈谈你的看法。

复旦大学经济学院2013~2014学年第二学期期末考试试卷

复旦大学经济学院2013~2014学年第二学期期末考试试卷A卷答案(共4页)课程名称:投资学原理课程代码: ECON130031.01开课院系:经济学院考试形式:闭卷姓名:学号:专业:一、选择题(单选或多选:4’*5=20’)1、B2、A C3、B D4、ABD5、CDF二、名词(4’*5=20’)1、股权风险溢价股权风险溢价ERP(equity risk premium,ERP)是指市场投资组合或具有市场平均风险的股票收益率与无风险收益率的差额。

从这个定义可看出:一是市场平均股票收益率是投资者在市场参与投资活动的预期“门槛”,若当期收益率低于平均收益时,理性投资者会放弃它而选择更高收益的投资;二是市场平均收益率是一种事前的预期收益率,这意味着事前预期与事后值之间可能存在差异。

2、资本配置线正是由于无风险资产引入,才可以形成无风险资产和风险资产之间的资本配置线CAL(capital allocation line,CAL),但是CAL仅仅为风险资产和无风险组合的“一般搭配”,并非“最优搭配”;而市场组合M与无风险资产构成全部资产组合的集合形成资本市场线(CML),是与“有效边界”相切的资本配置线,是一种“最优的”资本配置线。

3、市盈率增长因子(PEG)市盈率增长因子(PEG)是对P/E静态性缺陷的重要补充。

PEG是将一只股票的市盈率除以该公司的成长性。

其中,用估计盈利增长率除市盈率可以测算公司成长的速度,这就是著名的预期市盈率增长因子(Prospective PEG)。

市盈率增长因子越低,表示公司的发展潜力越大,公司的潜在价值也就越高。

市盈率/公司利润增长率,大于1说明估值高;小于1说明便宜。

4、动量效应投资者行为的研究表明,股票上涨得越多,就有也越多的投资者认为它继续上涨,因而股价的上涨存在一种自我实现机制,即存在动量效应(momentum effect)。

在股价的正反馈机制中,噪声交易这对股价上涨起到推动作用,而明智的专业投资者将从噪声交易者的追逐动能效应策略的过程中获取收益。

复旦大学研究生金融英语PPT

How much should people get paid for investing in the stockmarket?

Investors are betting that high returns from equities will pay for decent pensions. They are kidding themselves. Equities, the best asset for the long run, higher returns, diversified portfolio, cash, government bonds, safety in the short term, risk from inflation over longer periods

unexpected death

fatal accident enquiry, inquiry court hearing庭审 awards for injury n. 判决;裁定;裁定额

prudential but non liability insurance prudential: 1. Arising from or characterized by prudence. 2. Exercising prudence, good judgment, or common sense business interruption insurance业务中断保险 loss of turnover or trading profits营业额 money insurance reimburse v. 偿还 is open to liability claims that are not quantifiable

【复旦大学 投资学】Section2 Equity Premium Puzzle

Is the post-1926 period special?

• Mehra & Prescott(1985)

• Since 1926, annual returns for stocks and TB are 7 % and less than 1 %

•

1% for T-B (real)

• Mehra and Prescott (1989) argue that it is difficult to explain

• coefficient of relative risk aversion

• 30 VS 1

• Why is the premium so large? • Why is anyone willing to hold bonds?

the bet played out.

• Samuelson’s theorem of irrationality:

• Rationale for turning down the bet:

• “Because I would feel $100 loss more than $200 gain”

• Mental accounting • aggregation rules are not neutral • Example: • 50% win $200 • 50% loss $100 • Whether you will accept such a bet?

复旦大学 研究生投资学讲义 CHPT10-Investment Styles

Investment Styles Fan LongzhenIntroduction•Overview of investment styles;•Empirical evidence on returns of small capitalization firms and value stocks;•How to identify investment styles of a mutual fund –Characteristic-based style analysis–Return-based style analysis•Style benchmarks•Why value stock outperform growth stocks;•Earning and price momentumTypes of investment styles •Growth investing–Primarily concerned with the earning component of the P/E ratio–Look for high growth rate•Value (non-growth) investing–Primarily concerned with the price component of theP/E ratio–Look for cheap stocks•Small cap investing (as opposed to large cap)–Looking for neglected stocks–Undervalued relative to large cap equitiesInvestment styles•Value:–low price/book; low P/E; utilities industry •Growth: high EPS Growth–high profitability; health & technology •Small capitalizationWhy style analysis?•Returns of stocks in one category (e.g. growth) behave quite differently from stocks in another category (e.g. value)•Style analysis facilities–Monitoring style characteristics;–Diversification and risk control;–Performance valuation•In September 2001, a total of 3271 domestic equity managers participated in the survey–962 identify themselves as value managers;–1124 identify themselves as growth managers.Returns of small capitalization stocks•Fama and French (1992)–Rank the stocks into ten deciles based on marketcapitalization every year;–Compute the average 1-year holding period return after portfolio formation.–Found small stocks have higher returns than big stocks(1963-1991)–Fama and French do a secondary sort by beta withineach size decile, and find that beta can not explain thereturns.Return of high/low book-to-market stocks•Fama and French (1992, Journal of finance)–Rank stocks into ten deciles based on book-to-market ratio every year;–Compute the average 1-year holding periodreturn after portfolio formation;–Value stocks have higher average returns thangrowth stocks.Morningstar Fund Analysis •Market capitalization classification–Step 1: rank all stocks based market capitalization •Top 5% of the stocks as large cap;•Next 15% of the stocks are medium cap;•Remaining 80% of the stocks as small cap.---step 2:assign a score of 3 for large-cap stocks, 2 for mid-cap stocks, and 1 for small-cap stocks.---step3: calculate the weighted average of the market cap score across all stocks in the fund.---Step 4: classification•If market cap score<1.5 small cap fund •If 1.5<market cap score<2.5 medium cap fund•If market score>2.5 large cap fund ⇒⇒⇒Morningstar Fund Analysis •Growth/value classification–Step 1: estimate mediam P/E and P/B ratio of the stocks in three market-cap groups;–Step 2 compute the P/E and P/B score for each stock: divide each stock’s P/E and P/B by the median P/E and median P/B (respectively) of the stock’s market-cap group;–Step 3 calculate the average P/E and P/B score for each fund: average P/E or P/B score is 1.–Step 4 combined score=P/E score +P/B score –Step5 classification•If combined score>2.25 growth fund •If 1.75<combined score<2.25 blend fund •If combined score<1.75 value fund ⇒⇒⇒Return-based style analysis •Based on multiple factor model:•Where =return on fund •= return on style benchmark k •How to estimate the style exposure?–Regression of fund I on the return of style benchmarks;•Unconstrained regression•Constrained regression ( )•Quadratic programming ( )i K iK i i i e F b F b F b R ~~...~~~2211++++=i R ~k F ~1=∑ik b 0,1>=∑ik ik b bStyle benchmark•Six style index–S&P 500/Barra growth and value–S&P midcap 400/Barra growth and value–S&P smallcap 600/Barra growth and value•Growth and value indexes are constructed by dividing the stocks in the corresponding basic index based on book-to-price ratio. Each company in the index is assigned to either the value or growth index so that the two style add up to the full index.•The growth and value indexes are constructed so that they have the same market capitalization. Since growth companies are bigger than value companies, there are many more companies in the value index than the growth index.。

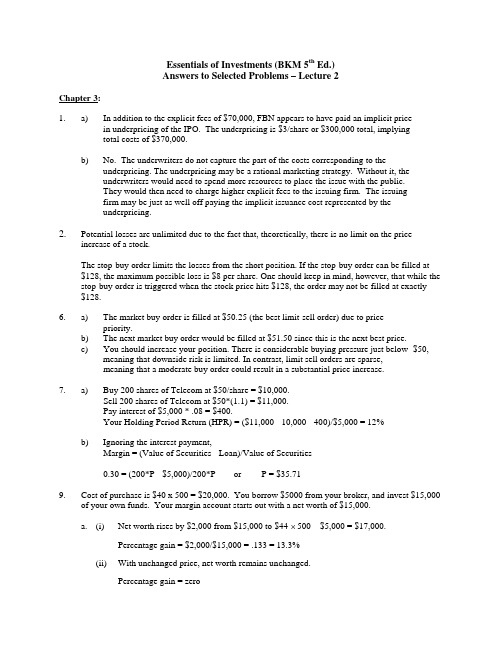

投资学精要(博迪)(第五版)习题答案英文版chapter3

Essentials of Investments (BKM 5th Ed.)Answers to Selected Problems – Lecture 2Chapter 3:1. a) In addition to the explicit fees of $70,000, FBN appears to have paid an implicit pricein underpricing of the IPO. The underpricing is $3/share or $300,000 total, implyingtotal costs of $370,000.b) No. The underwriters do not capture the part of the costs corresponding to theunderpricing. The underpricing may be a rational marketing strategy. Without it, theunderwriters would need to spend more resources to place the issue with the public.They would then need to charge higher explicit fees to the issuing firm. The issuingfirm may be just as well off paying the implicit issuance cost represented by theunderpricing.2. Potential losses are unlimited due to the fact that, theoretically, there is no limit on the priceincrease of a stock.The stop-buy order limits the losses from the short position. If the stop-buy order can be filled at $128, the maximum possible loss is $8 per share. One should keep in mind, however, that while the stop-buy order is triggered when the stock price hits $128, the order may not be filled at exactly $128.6. a) The market buy order is filled at $50.25 (the best limit-sell order) due to pricepriority.b) The next market buy order would be filled at $51.50 since this is the next best price.c) You should increase your position. There is considerable buying pressure just below $50,meaning that downside risk is limited. In contrast, limit sell orders are sparse,meaning that a moderate buy order could result in a substantial price increase.7. a) Buy 200 shares of Telecom at $50/share = $10,000.Sell 200 shares of Telecom at $50*(1.1) = $11,000.Pay interest of $5,000 * .08 = $400.Your Holding Period Return (HPR) = ($11,000 - 10,000 - 400)/$5,000 = 12%b) Ignoring the interest payment,Margin = (Value of Securities - Loan)/Value of Securities0.30 = (200*P - $5,000)/200*P or P = $35.719. Cost of purchase is $40 x 500 = $20,000. You borrow $5000 from your broker, and invest $15,000of your own funds. Your margin account starts out with a net worth of $15,000.a. (i) Net worth rises by $2,000 from $15,000 to $44 × 500 – $5,000 = $17,000.Percentage gain = $2,000/$15,000 = .133 = 13.3%(ii) With unchanged price, net worth remains unchanged.Percentage gain = zero(iii) Net worth falls to $36 × 500 – $5,000 = $13,000.Percentage gain = –$2,000/$15,000 = –.133 = –13.3%The relationship between the percentage change in the price of the stock and the investor’s percentage gain is given by:% gain = % change in price × Total investment investor's initial equity = % change in price × 1.33For example, when the stock price rises from 40 to 44, the percentage change in price is 10%, while the percentage gain for the investor is 1.33 times as large, 13.3%:% gain = 10% × $20,000$15,000 = 13.3%b. The value of the 500 shares is 500P. Equity is 500P – 5000. You will receive a margin call when500P-5000500P = .25 or when P = $13.33.c. The value of the 500 shares is 500P. But now you have borrowed $10,000 instead of $5,000. Therefore, equity is only 500P – $10,000. You will receive a margin call when500P-10,000500P = .25 or when P = $26.67.With less equity in the account, you are far more vulnerable to a margin call.d. The margin loan with accumulated interest after one year is $5,000 x 1.08 = $5,400. Therefore, equity in your account is 500P – $5,400. Initial equity was $15,000. Therefore, your rate of return after one year is as follows:(i) (500 × $44 – $5400) – $15,00015,000= .1067, or 10.67%.(ii) (500 × $40 – $5400) – $15,00015,000= –.0267, or –2.67%.(iii) (500 × $36 – $5400) – $15,00015,000= –.160, or –16.0%.The relationship between the percentage change in the price of Intel and investor’s percentage return is given by:% gain = % change in price x Total investment investor's initial equity – 8% x Funds borrowed Initial net worthFor example, when the stock price rises from 40 to 44, the percentage change in price is 10%, while the percentage gain for the investor is10% × 20,00015,000 – 8% × 500015,000 = 10.67%e. The value of the 500 shares is 500P. Equity is 500P – 5,400. You will receive a margin call when500P – 5400500P= .25 or when P = $14.4010. a)The gain or loss on the short position is –500 x ∆P. Invested funds are $15,000.Therefore the rate of return = (-500 x ∆P)/15,000. The returns in each of the threescenarios are:(i) (-500 x 4)/15000 = -13.3%(ii) (-500 x 0)/15000 = 0%(iii) (-500 x (–4))/15000 = 13.3%b)Total assets in the margin account are $20,000 (from the sale of stock) plus $15,000(the initial margin) = $35,000. Liabilities are 500P (the price of buying back theshares). A margin call will be issued when:(20,000 + 15,000 – 500P)/500P = 0.25 or P=$56c)With a $1 dividend, the short position must also pay $1 per share or $500 ($1 x 500)on the borrowed shares. The rate of return will be (-500 x ∆P – 500)/15,000.(i) [(-500 x 4) – 500]/15000 = -16.7%(ii) [(-500 x 0) – 500]/15000 = -3.33%(iii) [(-500 x (–4)) – 500]/15000 = 10.0%Liabilities are now (500P + 500). A margin call will be issued when:(20,000 + 15,000 – 500P - 500)/500P = 0.25 or P=$55.2013. a)55 ½ b)55 ¼ c)The trade will not be executed since the price on the limit sell order is higher than the quotedbid price (and the quoted ask price). d) In a purely dealer market, the trade will not be executed since the price on the limit buy orderis lower than the quoted ask price and all buy orders must be executed against the dealer’s ask quote.However, even on the Nasdaq market, customer limit orders now get priority over dealerquotes when they offer a better price than the quotes. In addition, the order could besubmitted to an ECN where it would set the inside quote. As a result, the Nasdaq dealermarket is looking more and more like an exchange market (see 14(b) below). Since this limitbuy order is offering to pay a higher price than the dealer (whose bid quote is 55¼), the limitorder would be executed against the next incoming market sell order.14. a) There can be price improvement for the two market orders. Brokers for each of themarket orders (i.e., the buy and the sell orders) can agree to do a trade inside thequoted spread. For example, they can trade at $55 3/8, thus improving the price forboth customers by $1/8 relative to the quoted bid and ask prices. The buyer gets thestock for $1/8 less than the quoted ask price and the seller receives $1/8 more for thestock than the quoted bid price.b) Whereas the limit buy order at $55 3/8 would not be executed in a purely dealer market(since the ask price is $55 ½), it could be executed in an exchange market. A brokerfor another customer with an order to sell at the market price would view the limitbuy order as the best bid price. The two brokers could agree to the trade and bring itto the specialist who would then execute the trade.19. d) Your order will be triggered at a price of $55. However, when the stock price dropsbelow your stop-loss price of $55, your stop-loss order immediately becomes amarket order and is executed at the prevailing market price. Thus, you could get $55per share, but you could also get a little bit more or a little bit less.。

金 融 市 场 学 - 复旦大学经济学院

Interest from Munis

Is not subject to federal income tax. Hence the yields are lower:

r (1- t) = rm r - before tax return on taxable bond rm - return on municipal bond t - marginal tax rate Attractive to wealthy investors.

thus the bank discount yield is 7.91% rBD=(10,000-P)/10,000 · 360/n effective annual yield is: (1+400/9600)2-1=8.51% bond equivalent yield is: rBEY=(10,000-P)/P · 365/n

Small investors buy it through mutual funds. Most issues have credit rating.

Treated for tax purposes as regular debt.

LC backed (letter of credit) optional.

违约风险保护

偿债基金 未来债务 红利限制 抵押

债券定价(Bond Pricing)

Repurchase agreements (RPs) used by dealers in

government securities. Term repo has a maturity of 30 days or more. Reverse repo is the result of a dealer finding an investor buying government securities with an agreement to sell them at a specified price at a specified future date.

复旦大学本科生课件 - 投资学

投资学

第 1章

19

金融体系:间接融资、直接融资与资金、证券的流动

资金

金融中介 机构

资金

储蓄 证券

贷款 资金

贷款人(储蓄者 投资者): 1、个人与家庭 2、企业 3、政府 4、外国投资者

证券 资金

金融市场

证券 资金

借款人(筹资者、 发行者): 1、个人与家庭 2、企业 3、政府 4、外国投资者

20

投资学

金融资产的价值与其物质形态没有任何关系:债券可

能并不比印制债券的纸张更值钱。 整个社会财富的总量与金融资产数量无关,金融资产 不是社会财富的代表。

投资学 第 1章 5

金融资产在经济中的作用

1.

2.

3.

消费的时间安排( Consumption Timing):个 人现实消费与现实收入分离,将高收入期的购 买力转移到低收入期。 风险的分配( Allocation of Risk):风险来源 于实际资产,风险在全社会的分散和优化配置。 问题:金融工具能否减少总体经济的风险? 所有权与经营权分离( Separation of Ownership),复合所有权:变不可分割的资 产为可分割的资产。例如:GE的股东有50万, 股东的退出不影响公司的经营。

投资学

第 1章

7

1.2 金融市场

1.2.1 金融市场(Financial market)是金融 资产的交易场所。 合约性质:债券市场、股票市场、期货市 场、期权市场。 期限长短:货币市场和资本市场 功能:初级(一级)市场——发行市场, 二级市场——交易市场。

区别:第一市场、第二市场等

投资学 第 1章 17

1.2.3 金融机构(Financial institutions) (1)金融中介( Financial intermediaries)为 间接融资提供服务,包括:商业银行、保险 公司、投资基金、养老基金等。 (2)证券业(Security industry)为直接融资提 供服务:

复旦大学金融431复试专业英语--标记版

专业英语汇总1. How to define the aggregate price level? 如何衡量价格指数?Three measures of the aggregate price level are commonly encountered in economic data.(1)The first is the GDP deflator (GDP平减指数), which is defined as nominal GDP divided by real GDP.(2)Another popular measure of the aggregate price level is the Producer Price Index (生产者价格指数) which is a measure of the cost of a basket of goods and services bought by firms.(3)The measure of the aggregate price level that is most frequently reported in the press is the Consumer Price Index (消费者价格指数), which is measured by pricing a basket of goods and services bought by a typical urban household.2. What’s the disadvantage and advantage of holding equity rather than debt? 持有股权的优劣?(1)The main disadvantage of own ing a corporation’s equities rather than its debt is that an equity holder is a residual claimant (剩余求偿权), that is, the corporation must pay all its debt holders before it pays its equity holders .(2)The main advantage of holding equities is that equity holders benefit directly from any increases in the corporation’s profitability or asset value because equities confer ownership rights on the equity holders. Debt holders do not share in this benefit, because their payments are fixed.3. What’s the difference between primary and secondary market? 一级市场与二级市场的区别?(1)A primary market is a financial market in which new issues of a security, such as a bond or a stock, are sold to initial buyers by the corporation or government agency borrowing the funds.(2)A secondary market is a financial market in which securities that have been previously issued can be resold.4. What’s the difference between foreign bond and Eurobond? 外国债券和欧洲债券的区别?(1)Foreign bonds are sold in a foreign country and are denominated in that c ountry’s currency. For example, a bond issued by a Chinese company denominated in U.S. dollars sold in New York.(2)Eurobond is a bond denominated in a currency other than that of the country in which it is sold. For example, a bond denominated in U.S. dollars sold in China.5. What’s asset transformation and diversification?资产转换和分散化(1)Financial intermediaries create and sell assets with risk characteristics that people are comfortable with, and the intermediaries then use the funds they acquire by selling these assets to purchase other assets that may have far more risk. This process of risk sharing is referred as asset transformation, because in a sense, risky assets are turned into safer assets for investors.(2)Diversification entails investing in a portfolio of assets whose returns do not always move together with the result that overall risk is lower than for individual assets. It also refers to “You shouldn't put all your eggs in one basket”. Diversification can eliminate firm-specific risk—the uncertainty associated with the specific companies. But diversification cannot eliminate market risk—the uncertainty associated with the entire economy, which affects all companies traded on the stock market. For example, when the economy goes into a recession, most companies experience falling sales, profit and low stock returns. Diversification reduces the risk of holding stocks, but it does not eliminate it.6. Explain the following concepts: asymmetric information, adverse selection and moral hazard.(1)A symmetric information (信息不对称) refers to that one party often does not know enough about the other party to make accurate decisions. For example, a borrower who takes out a loan usually has better information about the potential returns and risk associated with the investment projects for which the funds are invested than the lender does.(2)Adverse selection(逆向选择) is the problem created by asymmetric information before the transaction occurs. Adverse selection in financial markets occurs when the potential borrowers who are the most likely to default are the ones who most actively seek out a loan and are thus most likely to be selected.(3)Moral hazard (道德风险) is the problem created by asymmetric information after the transaction occurs. Moral hazard in financial markets is the risk that the borrower might engage in activities that are undesirable from the lenders point of view, because they make it less likely that the loan will be paid back.7. What’s the function of money? 货币的职能?Money has three primary functions in any economy: as a medium of exchange, as a unit of account, and as a store of value.(1)When money is used to pay for goods and services, it plays the role of a medium of exchange (流通手段). The use of money as a medium of exchange promotes economic efficiency by minimizing the time spent in exchanging goods and services.(2)The second role of money is to provide a unit of account (价值尺度), that is, it is used to measure value of goods and services in the economy.(3)Money also functions as a store of value (储藏手段). A store of value is used to save purchasing power from the time income is received until the time it is spent. This function of money is useful, because most of us do not want to spend our income immediately upon receiving it, but rather prefer to wait until we have the time or the desire to shop.8. What’s the Fisher equation and Fisher effect? 费雪等式与费雪效应?(1)The Fisher equation states that the nominal interest rate equals the real interest rate plus the expected rate of inflation. The equation tells us that all else equal, a rise in a country’s expected inflation rate will eventually cause an equal rise in the nominal interest rate. Similarly, a fall in the expected inflation rate will eventually cause a fall in the nominal interest rate.(2)This long-run relationship between inflation and interest rates is called the Fisher effect. The Fisher effect implies, for example, that if U.S. inflation were to rise permanently from a constant level of 5 percent per year to a constant level of 10 percent per year, dollar interest rates would eventually catch up with the higher inflation, rising by 5 percentage points per year from their initial level. These changes would leave the real rate of return on dollar assets unchanged. The Fisher effect is therefore another example of the general idea that in the long run, purely monetary developments should have no effect on an economy’s real variables.9. How to explain the negative relation between the quantity of money demanded and the interest rate? We can explain that the quantity of money demanded and the interest rate should be negatively related by using the concept of opportunity cost (机会成本), the amount of revenue sacrificed by taking one course of action rather than another. As the interest rate on bonds rises, the opportunity cost of holding money rises, thus money is less desirable and the quantity of money demanded must fall.10. Risk Premium 风险溢价The spread between the interest rates on bonds with default risk and default-free bonds, both of the same maturity, called the risk premium, indicates ho\ much additional interest people must earn to be willing to hold that risky bond.11. Briefly introduce expectations theory, segmented markets theory and liquidity premium theory. (1)The expectations theory (预期假说) of the term structure states the following proposition: the interest rate on a long-term bond will equal an average of the short-term interest rates that people expect to occur over the life of the long-term bond.(2)The segmented markets theory (市场分割假说) of the term structure sees markets for different-maturitybonds as completely separate and segmented. The interest rate for each bond with a different maturity is then determined by the supply of and demand for that bond, with no effects from expected returns on other bonds with other maturities.(3)The liquidity premium theory(流动性溢价假说) of the term structure states that the interest rate on a long-term bond will equal an average of short-term interest rates expected to occur over the life of the long-term bond plus a liquidity premium. It is also called preferred habitat theory (偏好停留假说).12. What’s the difference between adaptive expectation and rational expectation?(1)Adaptive expectation(适应性预期) states that expectations form from past experience only and changes in expectations will occur slowly over time as past data change. For example, expectations of inflation is typically viewed as being an average of past inflation rates. So if inflation had formerly been steady at a 5% rate, expectations of future inflation would be 5% also.(2)Rational expectation(理性预期) can be stated as follows: expectations will be identical to optimal forecasts (the best guess of the future) using all available information.13. Efficient Market Hypothesis 有效市场假说The efficient market hypothesis states that current prices in a financial market will be set so that the optimal forecast of a security’s return using all available information equals the security’s equilibrium return, because in an efficient market all unexploited profit opportunities will be eliminated by arbitrager (套利者).14. “Lemons Problem”次品问题A particular aspect of the way the adverse selection problem interferes with the efficient functioning of a market is called “lemons problem”.We can use the used-car market to illustrate this concept. Potential buyers of used cars are frequently unable to assess the quality of the car, that is, they can’t tell whether a particular used car is a good car or a lemon (次品). The price that a buyer pays must therefore reflect the average quality of the cars in the market, somewhere between the low value of a lemon and the high value of a good car. The owner of a used car, by contrast, is more likely to know whether the car is a good car or a lemon. If the car is a lemon, the owner is more than happy to sell it at the price the buyer is willing to pay, which, being somewhere between the value of a lemon and a good car, is greater than the lemons value. However, if the car is a good car, the owner knows that the car is undervalued at the price the buyer is willing to pay, and so the owner may not want to sell it. As a result of this adverse selection, few good used cars will come to the market. Because the average quality of a used car available in the market will be low and because few people want to buy a lemon, there will be few sales. The used-car market will function poorly or even disappear.15. Principal-agent Problem 委托-代理问题Principal-agent problem refers to that the managers in control (the agents) may act in their own interest rather than in the interest of the stockholder (the principals) because the managers have less incentive to maximize profits than the stockholder do. The principal-agent problem, which is an example of moral hazard, arises only because a manager has more information about his activities than the stockholder does. So, there is asymmetric information.16. What’s “irrational exuberance” proposed by Alan Greenspan? 非理性繁荣Irrational exuberance refers to a phenomenon that asset prices, in the stock market and real estate, are driven well above their fundamental economic values by investor psychology. The result is an asset-price bubble (资产价格泡沫), such as the tech stock market bubble of the late 1990s or the recent housing price bubble in subprime crisis.17. How to solve asymmetric information problems? 如何解决信息不对称的问题?18. Securitization and Subprime mortgage 资产证券化与次级抵押贷款(1)Subprime mortgages are mortgages for borrowers with less-than-stellar credit records.(2)Securitization is the process of transforming otherwise illiquid financial assets(such as residential mortgages, auto loans, and credit card receivables), which have typically been the main business of banking institutions, into marketable capital market securities.19. What’s time-inconsistency problem? 时间不一致问题The time -inconsistency problem is some thing we deal with continually in everyday life. We often have a plan that we know will produce a good outcome in the long run, but when tomorrow comes, we just can't help ourselves and we deny our plan because doing so has short-run gains. In other words, we find ourselves unable to consistently follow a good plan over time, and the good plan is said to be time-inconsistent and will soon be abandoned .20. Political Business Cycle 政治经济周期Political business cycle is a process that can be illustrated in the following example. Just before an election, expansionary policies are pursued to lower unemployment and interest rates. After the election, the bad effects of these policies, that is high inflation and high interest rates, come home to roost,requiring contractionary policies that politicians hope the public will forget before the next election.21. What’s money multiplier and what are the factors that affect it? 货币乘数及其影响因素?(1)The money multiplier, denoted by m, tells us how much the money supply changes for a given change in the monetary base. The relationship between the money supply, the money multiplier and the monetary base is described by the following equation: M = m ×MB(2)The money multiplier is a function of the currency ratio set by depositor c, the excess reserves ratio set by banks e, and the required reserve ratio set by the Fed r. The money multiplier m is thus22. What are the tools of monetary policy? 货币政策工具There are three tools of monetary policy that can be conducted by the central bank, such as open market operations, discount lending and reserve requirements.(1)Open market operations (公开市场操作) are the most important monetary policy tool, because they are the primary determinants of changes in interest rates and the monetary base, the main source of fluctuations in the money supply. Open market purchases expand reserves and the monetary base, thereby increasing the money supply and lowering short-term interest rates. Open market sales shrink reserves and the monetary base, decreasing the money supply and raising short-term interest rates.Open market operations have four advantages over the other tools of monetary policy: ①Open market operations occur at the initiative of the Fed, which has complete control over their volume. ②Open market operations are flexible and precise, and they can be used to any extent. ③Open market operations are easily reversed.④Open market operations can be implemented quickly, since they involve no administrative delays. (2)The facility at which banks can borrow reserves from the Fed is called the discount window (贴现窗口). The facility is intended to be a backup source of liquidity for banks during financial crisis.The most important advantage of discount policy is that the Fed can use it to perform its role of lender of last resort (最后贷款人). The disadvantage of discount policy is that the decisions to take out discount loans are made by banks and are therefore not completely controlled by the Fed.(3)Changes in reserve requirements (法定存款准备金) affect the money supply by causing the money supply multiplier to change. A rise in reserve requirements reduces the amount of deposits that can be supported by a given level of the monetary base and will lead to a contraction of the money supply. A rise in reserve requirements also increases the demand for reserves and raises the federal funds rate. Conversely, a decline in reserve requirements leads to an expansion of the money supply and a fall in the federal funds rate.Reserve requirements have at least three disadvantages: ①Owing to financial innovation, reserve requirements are no longer binding for most banks, so this tool is much less effective than it once was. ②Raising the requirements can cause immediate liquidity problems for banks where reserve requirements are binding. ③Continually fluctuating reserve requirements would also create more uncertainty for banks and make their liquidity management more difficult.23. Law of One Price and Theory of Purchasing Power Parity一价定理与购买力评价理论(1)The law of one price states that if two countries produce an identical good, and transportation costs and trade barriers are very low, the price of the good should be the same throughout the world no matter which country produces it.(2)T he theory of purchasing power parity (PPP) states that exchange rates between any two currencies will adjust to reflect changes in the price levels of the two countries. The theory of PPP is simply an application of the law of one price to national price levels rather than to individual prices. The statement that exchange rates equal relative price levels is sometimes referred to as absolute PPP (绝对购买力平价). Relative PPP (相对购买力平价) states that the percentage change in the exchange rate between two currencies over any period equals the difference between the percentage changes in national price levels.24. Real Exchange Rate 实际汇率The real exchange rate refers to the rate at which domestic goods can be exchanged for foreign goods. In effect, it is the price of domestic goods relative to the price of foreign goods denominated in the domestic currency. For example, if a basket of goods in New York costs $50, while the cost of the same basket of goods in Tokyo costs $75 because it costs 7500 yen while the exchange rate is at 100 yen per dollar, then the real exchange rate is 0.66 (=$50/$75). The real exchange rate is below l, indicating that it is cheaper to buy the basket of goods in the United States than in Japan.25. Why the theory of purchasing power parity cannot fully explain exchange rates? 购买力平价的缺陷(1)Contrary to the assumption of the law of one price, transport costs and restrictions on trade certainly do exist. These trade barriers may be high enough to prevent some goods from being traded between countries.(2)Monopolistic practices in goods markets may interact with transport costs and other trade barriers to weakenfurther the link between the prices of similar goods sold in different countries.(3)Because the inflation data reported in different countries are based on different commodity baskets, there is no reason for exchange rate changes to offset official measures of inflation differences, even when there are no barriers to trade and all products are tradable.26. Monetary Neutrality 货币中性Monetary neutrality states that in the long run, a one-time percentage rise in the money supply is matched by the same one-time percentage rise in the price level, leaving unchanged the real money supply and all other real variables such as real interest rates.27. Exchange Rate Overshooting 汇率超调The phenomenon that the exchange rate falls by more in the short run than it does in the long run when the money supply increases is called exchange rate overshooting. It can help explain why exchange rates exhibit so much volatility.Exchange rate overshooting is a direct consequence of the short-run rigidity of the price level. In a hypothetical world where the price level could adjust immediately to its new, long-run level after a money supply increase, the interest rate would not fall because prices would adjust immediately and prevent the real money supply from rising. Thus, the exchange rate would maintain equilibrium simply by jumping to its new, long-run level right away.28. Interest Parity Condition 利率平价条件(1)The uncovered interest parity condition(非抛补利率平价) states that the domestic interest rate equals the foreign interest rate minus the expected appreciation of the domestic currency, or equivalently, the domestic interest rate equals the foreign interest rate plus the expected appreciation of the foreign currency.For example, If the domestic interest rate is higher than the foreign interest rate, there is a positive expected appreciation of the foreign currency, which compensates for the lower foreign interest rate. This condition can be rewritten as(2)The covered interest parity condition(抛补利率平价) states that the rates of return on dollar deposits and “covered” foreign deposits must be the same. Suppose you want to buy a euro deposit with dollars but would like to be certain about the number of dollars it will be worth at the end of a year. You can avoid exchange rate risk by buying a euro deposit and, at the same time, selling the proceeds of your investment forward. We say you have “covered” yourself, that is, avoided the possibility of an unexpected depreciation of the euro.29. Unsterilized Foreign Exchange Intervention and Sterilized Foreign Exchange Intervention(1)A foreign exchange intervention in which a central bank allows the purchase or sale of domestic currency to have an effect on the monetary base, is called an unsterilized foreign exchange intervention (非冲销式干预). An unsterilized intervention in which domestic currency is sold to purchase foreign assets leads to a gain in international reserves, an increase in the money supply, and a depreciation of the domestic currency. An unsterilized intervention in which domestic currency is purchased by selling foreign assets leads to a drop in international reserves, a decrease in the money supply, and an appreciation of the domestic currency.(2)A foreign exchange intervention with an offsetting open market operation that leaves the monetary base unchanged is called a sterilized foreign exchange intervention (冲销式干预). A sterilized intervention leaves the money supply unchanged and so has no direct way of affecting interest rates or the expected future exchange rate.30. Fixed Exchange Rate Regime, Floating Exchange Rate Regime and Managed Float Regime(1)In a fixed exchange rate regime(固定汇率制), the value of a currency is pegged relative to the value ofone other currency, which is called the anchor currency (锚货币), so that the exchange rate is fixed in terms of the anchor currency.(2)In a floating exchange rate regime (浮动汇率制), the value of a currency is allowed to fluctuate against all other currencies.(3)When countries intervene in foreign exchange markets in an attempt to influence their exchange rates by buying and selling foreign assets, the regime is referred to as a managed float ing regime (管理浮动汇率制)ora dirty floating (肮脏浮动).31. What are the advantages and disadvantages of Gold Standard? 金本位的利与弊?(1)Before World War I, the world economy operated under the gold standard, a fixed exchange rate regime in which the currency of most countries was convertible directly into gold at fixed rates, so exchange rates between currencies were also fixed.(2)The fixed exchange rates under the gold standard had the important advantage of encouraging world trade by eliminating the uncertainty that occurs when exchange rates fluctuate.(3)There are disadvantages of gold standard as follows: ①Adherence to the gold standard meant that a country had no control over its monetary policy, because its money supply was determined by gold flows between countries. ②Monetary policy throughout the world was greatly influenced by the production of gold and gold discoveries.32. Currency Board and Dollarization 货币局制度与美元化(1)Currency board (货币局制度) means that the domestic currency is backed 100% by a foreign currency and in which the note-issuing authority, whether the central bank or the government, establishes a fixed exchange rate to this foreign currency and stands ready to exchange domestic currency for the foreign currency at this rate whenever the public requests it. A currency board is just a variant of a fixed exchange-rate target in which the commitment to the fixed exchange rate is especially strong because the conduct of monetary policy is in effect put on autopilot, and taken completely out of the hands of the central bank and the government.(2)Dollarization(美元化) means the adoption of a sound currency, like the U.S. dollar, as a country’s money.Indeed, dollarization is just another variant of a fixed exchange-rate target with an even stronger commitment mechanism than a currency board provides.The common disadvantage of both regimes is that a country that ties its exchange rate to an anchor currency of a larger country loses control of its monetary policy.33. Quantity Theory of Money 货币数量论The quantity theory of money states that nominal income is determined solely by movements in the quantity of money. We can derive the conclusion from the equation of exchange (交易方程式): MV=PY.Since the institutional and technological features of the economy would affect velocity of money (货币流通速度) only slowly over time, so velocity V would normally be reasonably constant in the short run.Because the classical economists thought that wages and prices were completely flexible, they believed that the level of aggregate output Y produced in the economy during normal times would remain at the full-employment level, so Y in the equation of exchange could also be treated as reasonably constant in the short run.So, for the classical economists, the quantity theory of money provided an explanation of movements in the price level: movements in the price level result solely from changes in the quantity of money.34. Liquidity Preference Theory 流动性偏好理论The liquidity preference theory of John Maynard Keynes pointed out that there are three motives behind the demand for money: the transactions motive, the precautionary motive, and the speculative motive. The demand of money for transaction and precautionary motives is proportional to income, while the demand of money forspeculative motive is negatively related to the level of interest rate. So the demand for real money balances is a function of interest rate and income as follow35. Friedman’s Modern Quantity Theory of Money 弗里德曼的现代货币数量论Friedman stated that the demand for money should be a function of the resources available to individuals (their wealth) and the expected returns on other assets relative to the expected return on money. From this reasoning, Friedman expressed his formulation of the demand for money as follows:Unlike Keynes’s theory, which indicates that interest rates are an important determinant of the demand for money, Friedman's theory suggests that changes in interest rates should have little effect on the demand for money.36. Crowding Out Effect of Fiscal Policy 财政政策的挤出效应Expansionary fiscal policy will crowd out investment and net exports, which decrease because of the rise in the interest rate. This situation is called crowding out (挤出效应).When the demand for money is unaffected by the interest rate, the LM curve is vertical. An expansionary fiscal policy does not lead to a rise in output but a sharp in interest rate, which means the increased government spending have completely crowed out investment and net exports. This situation is called complete crowding out (完全挤出).37. Transmission Mechanisms of Monetary Policy 货币政策传导机制(1)Traditional Interest-Rate Channel 利率机制An expansionary monetary policy leads to a fall in real interest rates, which in turn lowers the cost of capital, causing a rise in investment spending, thereby leading to an increase in aggregate demand and a rise in output.(2)Exchange Rate Channel 汇率机制An expansionary monetary policy leads to a fall in real interest rates, which in turn the currency depreciates, causing a rise in net exports, thereby leading to an increase in aggregate demand and a rise in output.(3)Tobin’s q Theory 托宾q理论Tobin defines q as the market value of firms divided by the replacement cost of capital. If q is high, the market price of firms is high relative to the replacement cost of capital, and new plant and equipment capital is cheap relative to the market value of firms. Investment spending will rise, because firms can buy a lot of new investment goods with only a small issue of stock. Conversely, when q is low, firms will not purchase new investment goods because the market value of firms is low relative to the cost of capital. Investment spending, the purchase of new investment goods, will then be very low。

复旦大学 研究生投资学讲义 CHPT12-1-Modern portfolio Theory

i =1 n n

ERP = ∑ ω i ERi = ϖ ' E ( R)

i =1

var(RP ) = ϖ ' Σϖ Σ = (σ ij )

Portfolio optimization without riskless asset 1 min 2 ϖ ' Σϖ {ω }

[

]

=

1 δ pδ q 1 A B ⎛ B⎞ + D = + ( µ p − )⎜ µ q − ⎟ A AB 2 A D A⎝ A⎠

Portfolio correlation

• For any minimum-variance portfolio P except the global-minimumvariance portfolio, there exists a unique minimum-variance portfoliodenoted by Z which has zero covariance with P; Consider P and Z 1 A B B cov( R p , Rz ) = + ( µ p − )( µ z − ) A D A A when µ z satisfies

• First-order condition ∂L

∂ϖ

v v = 0 ⇒ Σϖ = λ ( µ − R f 1) v v

v ∂L v v = 0 ⇒ R f + ϖ ' ( µ − R f 1) = µ p ∂λ

v ϖ * = λΣ ( µ − R f 1) v

−1

v

µ p − Rf v −1 v v λ= v ( µ − R f 1)' Σ ( µ − R f 1)

【复旦大学 投资学】Section4 FamaEMH

2.The Main Areas of Research

❖ 1970 review: weak-form tests; semi-strong form tests and strong-form tests

Returns ❖ 4.Cross-Sectional Return Predictability ❖ 5.Event Studies ❖ 6.Tests for Private Information ❖ 7.Conclusions

1. The Theme

❖ Strong version of market efficiency hypothesis: information and trading costs are 0

New tests remain suspicious but give us some new methodologies.

❖ Event studies are discussed next briefly. Its most advantage is allowing a break between market efficiency and equilibrium-pricing issues

Efficient Capital Markets:Ⅱ

The Journal of Finance, Vol 46,No. 5(Dec,1991)

By Eugene F.Fama

Menu

❖ 1.The Theme ❖ 2.The Main Areas of Research ❖ 3.Return Predictability: Time-Varying Expected

投资学精要(博迪)(第五版)习题答案英文版chapter5综述

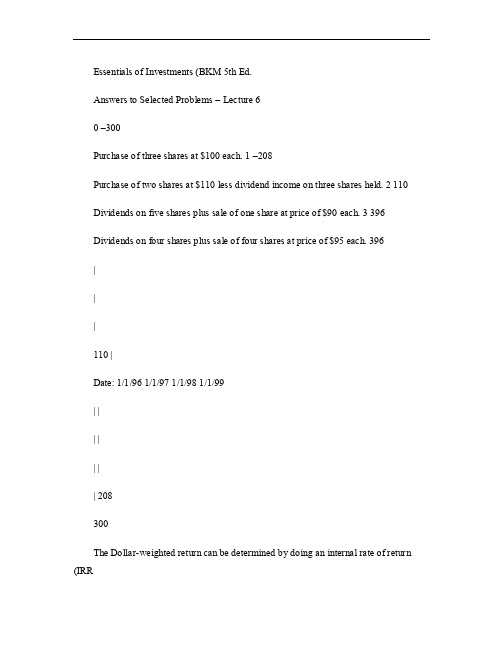

Essentials of Investments (BKM 5th Ed.Answers to Selected Problems – Lecture 60 –300Purchase of three shares at $100 each. 1 –208Purchase of two shares at $110 less dividend income on three shares held. 2 110 Dividends on five shares plus sale of one share at price of $90 each. 3 396Dividends on four shares plus sale of four shares at price of $95 each. 396|||110 |Date: 1/1/96 1/1/97 1/1/98 1/1/99| || || || 208300The Dollar-weighted return can be determined by doing an internal rate of return (IRRcalculation. In other words, set the present value of the outflows equal to the presentvalue of the inflows (or the net present value to zero: %1661. 0001661. 01(396 1(110 1(208300321−=−=+++=++R R R3. b.5. We need to distinguish between timing and selection abilities. The intercept of the scatterdiagram is a measure of stock selection ability. If the manager tends to have a positive excess return even when the market’s performance is merely ‘neutral’ (i.e., has zero excess return, then we conclude that the manager has on average made good stock picks – stock selection must be the source of the positive excess returns.Timing ability is indicated by curvature in the plotted line. Lines that become steeper as you move to the right of the graph show good timing ability. An upward curvedrelationship indicates that the portfolio was more sensitive to market moves when the market was doing well and less sensitive to market moves when the market was doingpoorly -- this indicates good market timing skill. A downward curvature would indicate poor market timing skill.We can therefore classify performance ability for the four managers as follows:a. Bad Goodb. Good Goodc. Good Badd. Bad Bad9. The manager’s alpha is:10 - [6 + 0.5(14-6] = 010. a α(A = 24 - [12 + 1.0(21-12] = 3.0%α(B = 30 - [12 + 1.5(21-12] = 4.5%T(A = (24 - 12/1 = 12T(B = (30-12/1.5 = 12As an addition to a passive diversified portfolio, both A and B are candidates because they both have positive alphas.b (i The funds may have been trying to time the market. In that case, the SCL of the funds may be non-linear (curved.(ii One year’s worth of data is too small a sample to make clear conclusions.(iii The funds may have significantly different levels of diversification. If both have the same risk-adjusted return, the fund with the less diversified portfolio has a higher exposure to risk because of its higher firm-specific risk. Since the above measure adjusts only for systematic risk, it does not tell the entire story.11. a Indeed, the one year results were terrible, but one year is a short time period from whichto make clear conclusions. Also, the Board instructed the manager to give priority to long-term results.b The sample pension funds had a much larger share in equities compared to Alpine’s. Equities performed much better than bonds. Also, Alpine was told to hold down risk investing at most 25% in equities. Alpine should not be held responsible for an asset allocation policy dictated by the client.c Alpine’s alpha measures its risk-adjusted performance compared to the market’s:α = 13.3 - [7.5 + 0.9(13.8 - 7.5] = 0.13%, which is actually above zero!d Note that the last five years, especially the last one, have been bad for bonds – and Alpine was encouraged to hold bonds. Within this asset class, Alpine did much better than the index funds. Alpine’s performance within each asset class has been superior on a risk-adjusted basis. Its disappointing performance overall was due to a heavy asset allocation weighting toward bonds, which was the Board’s –not Alpine’s – choice.e A trustee may not care about the time-weighted return, but that return is moreindicative of the manager’s performance. After all, the manager has no control over the cash inflow of the fund.。

复旦大学精品课程《.投资学原理》课件,第三章资产组合理论课件复习精品

资产B

概率 1/2 1/2 110 150 130

资产C

收益 概率 1/2 1/2

资产A期望收益率

130 1 30% 100

1 120 1 140 1 32.5% 2 98 2 98

1 110 1 150 1 37% 2 95 2 95

五、均值-方差准则(MVC) Markowitz(1952)提出“期望收益-收益方差” (expected return-variance of return)准则, 认为投资者在实际中按照这一法则进行投资。 其现实基础: 1、投资者的风险厌恶性 2、投资者的不满足性 其理论形式:均值-方差准则

(二)证券市场风险的种类 市场风险 利率风险 汇率风险 通胀风险 财务(违约)风险 经营风险 流动性风险

Байду номын сангаас

信用违约掉期——次贷危机引发全球 金融风暴的真正元凶

金融资产的违约保险:信用违约掉期(CDS,Credit Default Swap)

按期支付固定费用 标 的 资 产

信用 违约 保险 购买 方

i 1 n

期望收益率的两大要素:各种状态下可能收益 率及其发生概率。

(三)风险的度量——方差与标准差 方差:对资产实际收益率与期望收益率的偏离的测 度方法。单一风险资产的方差:

2 pi [ri E (r )]2

i 1

n

标准差(standard deviation):方差的平方根。

第三节 最优资产组合选择

问题的提出: 当面临多个不同风险-收益关系的资产组合时, 投资者应该如何进行分析与选择? 构建最优资产组合的基本要素: 1、基本方法:马科维茨的均值-方差理论 2、主观判断标准:无差异曲线

投资学精要Chap012

30-46

Example

再投资资金的收益率ROE

∞

∞

11-46

固定增长模型( 固定增长模型(Constant growth model)——Gordon ) model

若 股 息 d t = d t −1 (1 + g ), 则 d t = d 0 (1 + g ) v0 =

t

∑

t =1

∞

∞ dt (1 + g ) t = d0 ⋅ ∑ t (1 + k ) (1 + k ) t t =1

dt vT - = ∑ (1+ k)t t =1 dt dt +1 vT + = ∑ = t T (k − g)(1+ k) t =T (1+ k )

T dt +1 dt v0 = +∑ T (k − g)(1+ k) t =1 (1+ k)t ∞

T

(k > g)

18-46

Intrinsic Value内在价值 and Market Price市场价格 内在价值 市场价格

=

∑

t =1 n t =1 n

=∑ =∑

t =1

d 0 (1 + g 1 ) t d n +1 + t (1 + k ) (1 + k ) n ( k − g 2 )

其 中 , d n +1 = d n (1 + g )

15-46

三阶段增长模型

两阶段模型假设公司的股利在头n年以每年 的速率增长, 两阶段模型假设公司的股利在头 年以每年g1的速率增长, 年以每年 个从g 从(n+1)年起由 1立刻降为 2,而不是稳定地有 个从 1 )年起由g 立刻降为g 而不是稳定地有1个从 的过渡期,这是不合理的,为此, 到g2的过渡期,这是不合理的,为此,Fuller(1979)提 ( ) 出了三阶段模型

复旦大学 研究生投资学讲义 CHPT15- the equity market cross-section and time-series properties

Chapter 15 the equity market (cross-section patternsand time-series patterns)Fan LongzhenIntroduction•In this class, we again look at the stock return data, but with a very different view point;•Previously, we examined the data through the “eyes”of CAPM. We had a noble intension, although it didn’t work very well;•Now we are going to get our hands “dirty”, and plunge right into the data, without a formal model;•In particular, we will look at some well-established patterns---size,value, and momentum—that have beensuccessful in explaining the cross-sectional stock returns.Multifactor-regressions•For each asset i, we use a multi-factor time-series regression to quantify the asset’s tendency to move with multiple risk factors:• 1. Systematic factors:•:risk premium•:risk premium • 2 idiosyncratic factors:•: no risk premium • 3. Factor loadings:•beta(i): sensitivity to market risk;•: sensitivity to the factor risk.i tt i f t M t i i f t i t e F f r r r r ++−+=−)(βαM t r )(f t M t M r r E −=λtF )(t F F E =λi t e 0)(=i t e E i fThe pricing relation•Given the risk premia of the systematic factors, the determinants of expected returns:•What are the additional systematic factors?FiM i f t i t f r r E λλβ+=−)(Size: small or big•We sort the socks by their market capitalization: share price* number of shares outstandingValue or growth•We can sort the cross-section of stocks by their book-to-market ratios: growth stocks:firm with low book-to-market ratios;•Value stocks:firms with high book-to-market ratios.Other factors•Price-to-earining ratios,•The market skewness fcator•---Havey and Siddique(JF,2000) report that systematic skewness is economically important and commands an average risk premium of 3.6% per year.Time-series behavior•For the time-series behavior of stock returns, we focus in particular on the time-varying nature of expected return and volatility;•We are interested in building dynamic models that explicitly incorporate conditioning information to best describe the behavior of future stock returns.Predictability and marketefficiency•In addition to the random walk test, there is mounting evidence that stock returns are predictable;•Some argue that predictability implies market inefficiency. What do you think?•Others contend it is simple a result of rational variation in expected returns;•Suppose this is true. Can we find a coherent story that relates the variation through time of expected returns to business conditionsWhat cause expected returns to vary?•Using the intuition of CAPM, expected returns canvary for two reasons:• 1. Varying risk aversion;• 2. Varying exposure to market risk, or varying market risk.•When income is high, investor want save more, higher saving lead to lower expected returns;•Empirical implication?Variables related to business condition •Default spreads: difference in yields between defaultable bonds and treasury bonds with similar maturities. When the business condition is bad, the systematic default risk increases, widening the default spread.•Term premiums: difference in yields between long-and short-term treasury bonds. This is a forward-looking variable predictive of future inflation, and is found to be important in forecasting real economic activity.•Financial ratios: book-to-market, dividend yields, ect. Variables that are important in fundamental valuationTime-varying volatility---volatility also changes with time •If the rate of information arrival is time-varying, so is the rate of price adjustment, causing the volatility to change over time;•The time-varying volatility of the market return is related to the time-varying volatility of a variety of economic variables, includinginflation, money growth, and industrial production;•Stock market volatility increases with financial leverage: a decrease in stock price causes an increase in financial leverage, cause volatility to increase;•Investors’s sudden changes of risk attitudes, changes in market liquidity, and temporary imbalance of supply and demand could all cause market volatility to change over time.•What are the testable empirical implications?Stochastic volatility•More generally, volatility is a stochastic process of its own, this is an active area of research in academics and in industry.•Some well-known facts about stochastic volatility:• 1. It is persistent: volatile periods are followed by volatile periods;• 2. It is mean-reverting: over time, volatility converges to its long-run mean.• 3. There is a negative correlation between volatility and return: large negative price jumps are coupled with large positive volatility jumps.。

复旦大学投资学课件Section3 Returns equity mutual funds

❖ Several caveats: ❖ The results are not robust ❖ The strategy worked during the 1970s for

the 8% load charges and survivorship bias

4.B strategies involving the purchase of Forbes “Honor Roll” Funds.

❖ Jensen(1968): performance of mutual funds was inferior to randomly selected portfolios with equivalent risk

❖ Henriksson(1984): fund managers have enough private information to offset expenses.

❖ Good performance continue: two cautions; survivorship bias; not robust since the strong persistence in 1970s does not exist during the 1980s

are not independent and correlated over time. The predictability of returns ❖ Most efficiency test are joint tests ❖ Eugene Fama:”Sequels are rarely as good as the originals.”

❖ Positive relationship between advisory expenses and performance

投资学英文课件 (3)

International Issues

Problems when using multipliers for international company valuation

• Problem1: what do stock prices mean in different countries?

Dividend Discount Models

Expected Holding Period Return

• The return on a stock investment comprises cash dividends and capital gains or losses – Assuming a one-year holding period

Estimating Dividend Growth Rates

g = growth rate in dividends ROE = Return on Equity for the firm b = plowback or retention percentage rate

(1- dividend payout percentage rate)

• Market Price – Consensus value of all potential traders

• Trading Signal – PrV > MP Buy – PrV < MP Sell or Short Sell – PrV = MP Hold or Fairly Priced

Relative valuation

Goal: Assign a value to a non-listed company Evaluate whether a listed company is under-

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Burton G. Malkiel JOF 1995

Introduction

❖ Early 1970s, EMH accepted ❖ By the early 1980s, several cracks: returns

❖ The numbers of positive alpha and negative alpha are approximately equal.

❖ Table 3

❖ Grossman and Stiglitz(1980): positive alphas for pre-expense returns confirm that mutual funds do earn gross returns to cover expenses

❖ High returns: the funds failed have been dropped out of the sample

❖ Tendency of more successful funds to survive, overstated.

❖ “incubator” funds ❖ Funds quity

❖ Hot hand: mutual funds that achieved above average returns continue to enjoy superior performance.

❖ Expense ratios will also influence

❖ Analyze the predictability of performance by two-way tables showing successful performance over successive periods.

❖ The 1980s: small stocks tended to underperform the S&P stock index.

❖ 10-year sample limited

❖ There is relationship between returns and betas in mutual funds. The betas are stable

Weaker during the 1980s

4 simulations of strategies based on the persistence

❖ Whether the persistence of performance is economically significant.

expenses ❖ conclude

1 Survivorship bias and the data set employed

❖ Today’s investors are not interested in the funds that no longer exist, which creates the biases in the figures.

funds sold to the public. ❖ Quarterly total returns.

Some survivorship in table 1

The differences is big

2. A closer look at performance

❖ The t is only -0.21, so it is indistinguishable from 0. even surviving funds do not produce excess returns for investors after expenses.

❖ Over 20 year period 1971 to 1991, the relationships between betas and total returns disappear.

3. The “Hot Hand” Phenomenon: the persistence of mutual fund returns

❖ hot hand phenomenon

❖ Section 1: data ❖ Section 2: performance of the equity mutual

funds ❖ Section 3: hot hand phenomenon ❖ Section 4: simulate investment strategies ❖ Section 5: relation between returns and

❖ Jensen(1968): performance of mutual funds was inferior to randomly selected portfolios with equivalent risk

❖ Henriksson(1984): fund managers have enough private information to offset expenses.

❖ But positive alphas are small and insignificant. EGDH(1993): inappropriate benchmarks, if corrects for the non-S&P stocks, the positive alphas disappear.

are not independent and correlated over time. The predictability of returns ❖ Most efficiency test are joint tests ❖ Eugene Fama:”Sequels are rarely as good as the originals.”