平安营业中断保险条款

营业中断险投保单-2009

12.保险合同争议解决方式选择:

□提交仲裁委员会仲裁;□诉讼。

13.特别约定:

投保人声明:保险人已向本人提供并详细介绍了《中国人寿财产保险股份有限公司营业中断保险条款》及其附加险条款内容(若投保附加险),并对其中免除保险人责任的条款(包括但不限于责任免除、投保人被保险人义务、赔偿处理、其他事项等),以及本保险合同中付费约定和特别约定的内容向本人做了明确说明,本人已充分理解并接受上述内容,同意以此作为订立保险合同的依据,自愿投保本保险。

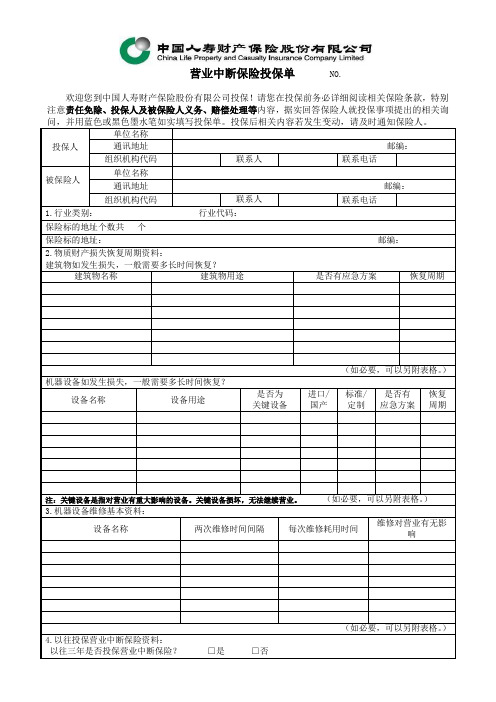

邮编:

组织机构代码

联系人

联系电话

被保险人

单位名称

通讯地址

邮编:

组织机构代码

联系人

联系电话

1.行业类别:行业代码:

保险标的地址个数共个

保险标的地址:邮编:

2.物质财产损失恢复周期资料:

建筑物如发生损失,一般需要多长时间恢复?

建筑物名称

建筑物用途

是否有应急方案

恢复周期

(如必要,可以另附表格。)

机器设备如发生损失,一般需要多长时间恢复?

以下为投保信息

7.物质财产损失保险资料:

险别:保单号:

8.投保基本资料:

保险金额

毛利润元¥

赔偿限额

审计费用元¥

最大赔偿期

免赔额/免赔期

请填写约定的维持费用资料项目名称、所属会计一、二级科目名称和其他必要说明:

(1)

(2)

(3)

(4)

(5)

(如必要,可另有附页)

9.附加险情况:

□附加通道堵塞保险:

保险金额:

以往三年是否投保营业中断保险?□是□否

保险期间

是否发生

保险事故

平安高新技术企业营业中断保险条款

平安高新技术企业营业中断保险条款总则第一条本保险合同由保险条款、投保单、保险单以及批单组成。

凡涉及本保险合同的约定,均应采用书面形式。

第二条本保险合同的被保险人是指经过国家主管部门认定的从事高新技术研发、生产的企业或机构。

保险责任第三条在保险期间内,由于下列原因造成保险单明细表中列明的关键研发设备损毁、灭失或丧失使用功能以及存储于其中的科研资料丢失,导致研发项目的研发工作中断,保险人依照本保险合同的约定,负责赔偿被保险人能够恢复到损失发生前研发状态所需要的合理必要的研发费用:(一)火灾、爆炸;(二)雷电、暴雨、洪水、暴风、龙卷风、冰雹、台风、飓风、暴雪、冰凌;(三)突发性滑坡、崩塌、泥石流;(四)飞行物体及其他空中运行物体坠落。

第四条本保险合同所指研发项目是保险明细表中列明的向国家有关管理部门申请财政补贴并获书面批准的新技术、新工艺或新产品的研究开发课题或项目。

第五条本保险合同所指研发费用是被保险人在产品、技术、材料、工艺、标准的研究、开发过程中发生的如下费用:(一)研发活动直接消耗的材料、燃料和动力费用;(二)被保险人在职研发人员的工资;(三)用于中间试验和产品试制的模具、工艺装备开发及制造费,设备调整及检验费,样品、样机及一般测试手段购置费,试制产品的检验费;(四)研发成果的知识产权申请费、注册费、代理费;(五)通过外包、合作研发等方式,委托其他单位或与之合作进行研发而支付的费用。

下列不属于本保险所称研发费用:(一)用于研发活动的仪器、设备、房屋等固定资产的建造费用、改造费用、购置费用、安装费用或租赁费用以及相关固定资产的运行维护、维修等费用;(二)用于研发活动的软件,专利权、非专利技术等无形资产的购置和摊销费用;(三)与研发活动相关的其他费用,包括技术图书资料费、资料翻译费、会议费、差旅费、办公费、外事费、研发人员培训费、培养费、专家咨询费等。

责任免除第六条由于下列原因造成研发项目的研发工作中断的,保险人不负责赔偿:(一)投保人、被保险人的故意或重大过失行为;(二)战争、敌对行动、军事行为、武装冲突、罢工、骚乱、暴动、恐怖活动;(三)核辐射、核爆炸、核污染及其他放射性污染;(四)地震、海啸;(五)行政行为或司法行为;(六)大气污染、土地污染、水污染及其他各种污染,但因本保险合同责任范围内的事故造成的污染不在此限。

营业中断保险条款

营业中断保险条款总则第一条本保险合同由保险条款、投保单、保险单或其他保险凭证以及批单组成。

凡涉及本保险合同的约定,均应采用书面形式。

第二条投保人应将被保险人在本保险合同载明的营业处所从事载明的经营业务(以下简称“营业”)所使用的物质财产向保险人投保相关的物质财产损失保险。

物质财产损失保险合同(以下简称“物质损失保险合同”)号应在本保险合同中载明。

保险责任第三条在保险期间内,被保险人因物质损失保险合同主险条款所承保的风险造成营业所使用的物质财产遭受损失(以下简称“物质保险损失”),导致被保险人营业受到干扰或中断,由此产生的赔偿期间内的毛利润损失,保险人按照本保险合同的约定负责赔偿。

本保险合同所称赔偿期间是指自物质保险损失发生之日起,被保险人的营业结果因该物质保险损失而受到影响的期间,但该期间最长不得超过本保险合同约定的最大赔偿期。

本保险合同所称毛利润是指按照下述公式计算的金额:毛利润=营业利润+约定的维持费用或毛利润=约定的维持费用-营业亏损×约定的维持费用/全部的维持费用本保险合同所称维持费用是指被保险人为维持正常的营业活动而发生的、不随被保险人营业收入的减少而成正比例减少的成本或费用。

约定的维持费用由投保人自行确定,经保险人确认后在保险合同中载明。

除另有约定外,上述公式所用的会计措辞的含义与被保险人会计账表中的含义一致。

第四条发生第三条约定的保险事故后,被保险人申请赔偿时,按照保险人的要求提供有关账表、账表审计结果或其他证据所付给被保险人聘请的注册会计师的合理的、必要的费用(以下简称“审计费用”),保险人在本保险合同约定的赔偿限额内也负责赔偿。

责任免除第五条保险人不负责赔偿下列损失:(一)投保人、被保险人的故意或重大过失行为产生或扩大的任何损失;(二)由于物质损失保险合同主险条款责任范围以外的原因产生或扩大的损失;(三)地震、海啸及其次生灾害产生或扩大的损失;(四)由于政府对受损财产的修建或修复的限制而产生或扩大的损失;(五)恐怖主义活动产生或扩大的损失;(六)本保险合同载明的免赔额或本保险合同约定的免赔期内的损失。

电厂营业中断保险费率 保险条款开发

XXX财产保险股份有限公司电厂营业中断保险费率表目录一、总则二、术语定义三、纯风险损失率表构成四、使用原则和方法五、纯风险损失率表六、保险费计算一、总则为准确识别电厂在营运过程中的风险,合理确定承保条件,在测算电厂经营数据,研究电厂生产特征的基础上,特制定本损失率表。

在开展实际业务时,应在纯风险损失率的基础上附加合理的费用及利润比例,得到实际费率。

本表适用于电厂在生产经营过程中面临的物质损失风险、机损险风险和营业中断险损失风险。

本表所称电厂包括常规燃煤电厂、燃气轮机电厂、柴油机电厂、水电厂和风电厂,但不包括核电站。

本表仅适用于电厂整体投保的业务,不适用于电厂投保专门设备的业务(投保专门设备的不得低于本表中的基准损失率)。

二、术语定义1、常规燃煤电厂以煤为燃料,通过锅炉中煤粉的燃烧,把煤的化学能转化成热能,加热锅炉给水使其变成高温高压蒸汽,在蒸汽轮机中膨胀做功,推动蒸汽轮机转子旋转,同时带动发电机发电。

2、燃气轮机电厂以燃油或燃气为燃料,通过燃烧在燃机中形成高温高压的烟气,在透平中膨胀做功,推动燃气轮机转子旋转,同时带动发电机发电。

3、柴油机电厂以燃油为燃料,通过燃烧在柴油机中形成高温高压的烟气,在燃烧室中做功,再通过机械传动把往复式活塞运动转换成转动,同时带动发电机发电。

4、水电厂利用水能推动水轮机旋转,同时带动发电机发电。

5、风电厂利用风能推动叶片旋转,同时带动发电机发电。

三、纯风险损失率表构成《电厂纯风险损失率表》分为“电厂财产险纯风险损失率”、“电厂营业中断险纯风险损失率(财产险项下)”和“电厂机器损坏险纯风险损失率”、“电厂营业中断险纯风险损失率(机损险项下)”四部分,每个部分又分为“平均风险损失率和基准免赔”及“纯风险损失率调整系数”两部分。

四、使用原则和方法对于电厂财产险和机器损坏险纯风险损失率的拟定,主要通过对平均风险损失率、风险偏离因子和纯风险损失率调整系数的确定、计算获得。

以上分类参数主要参照了有关公司历年在该行业承保和理赔的相关数据,同时利用保险公司在电力领域长期承保经验,通过综合考虑得到。

营业中断保险附加险条款

营业中断保险附加险条款本条款是《XXXXXXXX公司营业中断保险》(以下简称“主险”)的附加险条款。

本附加险合同未约定事项,以主险合同为准;主险合同与本附加险合同相抵触之处,以本附加险合同为准。

投保人可以选择其中的某一个、某几个或全部附加险投保。

一、扩展类K01.包括全部营业额条款K02.未保险的维持费用条款K03.通道堵塞条款K04.谋杀等条款K05.公众事业设备扩展条款K06.遗失欠款账册条款K07.恢复保险金额条款K08.每月预付赔款扩展条款K09.调整保险费条款K10.保单取消条款K11.不得进入条款K12.承包商/供应商条款 K13.顾客/供应商/承包商条款K14.物质损失放弃免赔条款K15.关闭营业处所/设施条款K16.审计师条款 K17.通道受阻条款 K18.炸弹恐吓条款 (只适用于财产利润损失险)K19.政府法令条款 (不超过连续10星期)K20.营业费用增加条款K21.相关性条款K22.累积存货条款二、规范类G01.部门条款G02.账目分类条款G03.会计师条款G04.违反保险条件条款G05.错误及遗漏描述条款G06.保费调整条款G07.保险人90天通知取消保险或拒绝续保条款G08.新业务条款G09.产量条款G10.经营部门条款G11.新营业条款G12.预付赔款条款G13.不具名供应商及顾客扩展条款G14.放弃代位权条款一、扩展类K01.包括全部营业额条款在赔偿期限内如果为获得营业收入,被保险人或他人代其在营业处所以外的地点,销售货物或提供服务,则有关这项销售或服务所给付或应给付的金额,在计算赔偿期限的营业额时应包括在内。

K02.未保险的维持费用条款如本保险合同未承保经营业务的维持费用(根据本保险合同规定对毛利润的定义,在计算毛利润时已予减除),在计算本保险合同项下,可以取得补偿的营业费用增加的赔偿金额时,只赔偿营业费用增加乘以按毛利润与毛利润加上未保的维持费用之比例所得的那一部分额外费用。

保险公司倒闭了保单怎么办

一、保险公司倒闭了保单怎么办根据《保险法》规定,经营有人寿保险业务的保险公司被依法撤销的或者被依法宣告破产的,其持有的人寿保险合同及准备金,必须转移给其他经营有人寿保险业务的保险公司;不能同其他保险公司达成转让协议的,由保险监督管理机构指定经营有人寿保险业务的保险公司接受。

转让或者由保险监督管理机构指定接受前款规定的人寿保险合同及准备的,应当维护被保险人、受益人的合法权益。

保险公司被撤销或者被宣告破产,其清算财产不足以偿付保单利益的,保险保障基金按照下列规则对非人寿保险合同的保单持有人提供救济:(一)保单持有人的损失在人民币5万元以内的部分,保险保障基金予以全额救济;(二)保单持有人为个人的,对其损失超过人民币5万元的部分,保险保障基金的救济金额为超过部分金额的90%;保单持有人为机构的,对其损失超过人民币5万元的部分,保险保障基金的救济金额为超过部分金额的80%。

前款所称保单持有人的损失,是指保单持有人的保单利益与其从清算财产中获得的清偿金额之间的差额。

二、破产后具体赔付是怎样的根据《保险法》第九十一条破产财产在优先清偿破产费用和共益债务后,按照下列顺序清偿:(一)所欠职工工资和医疗、伤残补助、抚恤费用,所欠应当划入职工个人账户的基本养老保险、基本医疗保险费用,以及法律、行政法规规定应当支付给职工的补偿金;(二)赔偿或者给付保险金;(三)保险公司欠缴的除第(一)项规定以外的社会保险费用和所欠税款;(四)普通破产债权。

三、投保人的保险合同解除权是什么《保险法》第15条规定,"除本法另有规定或者保险合同另有约定外,保险合同成立后,投保人可以解除保险合同"。

根据上述法律规定,除了法律另有规定或者保险合同另有约定外,投保人享有任意解除保险合同的法定权利。

这种权利是法律赋予保险合同投保人的一项特权,与普通民商事合同有较大的不同。

《保险法》之所以作出这样规定,其法理是:保险合同是一种保障性合同,投保人为保障自己的保险利益与保险人签定保险合同,保险利益是基于投保人对保险标的的权利而产生,投保人有权在法律规定的范围内任意处分自己的民事权利,他可以选择保险或不保险、可以选择此时保险而彼时不保险,也可以自由选择保险人。

太平财险条款太平财产保险有限公司营业中断保险条款

本保险合同所称毛利润是指按照下述公式计算的金额:

毛利润=营业利润+约定的维持费用

或

毛利润=约定的维持费用-营业亏损×约定的维持费用/全部的维持费用

本保险合同所称维持费用是指被保险人为维持正常的营业活动而发生的、不随被保险人营业收入的减少而成正比例减少的成本或费用。约 定的维持费用由投保人自行确定,经保险人确认后在保险合同中载明。

第十八条 除另有约定外,投保人应在保险合同成立时一次性支付全部保险费。保险费交付前发生的保险事故,保险人不承担赔偿责 任。

第十九条 被保险人应当遵守国家有关消防、安全、生产操作、劳动保护等方面规定,加强管理,采取合理的预防措施,尽力避免或减少 责任事故的发生,维护保险标的的安全。

保险人可以对被保险人遵守前款约定的情况进行检查,向投保人、被保险人提出消除不安全因素和隐患的书面建议,投保人、被保险人应 该认真付诸实施。

除另有约定外,上述公式所用的会计措辞的含义与被保险人会计账表中的含义一致。

第四条 发生第三条约定的保险事故后,被保险人申请赔偿时,按照保险人的要求提供有关账表、账表审计结果或其他证据所付给被保险 人聘请的注册会计师的合理的、必要的费用(以下简称“审计费用”),保险人在本保险合同约定的赔偿限额内也负责赔偿。

总则

第一条 本保险合同由保险条款、投保单、保险单或其他保险凭证以及批单组成。凡涉及本保险合同的约定,均应采用书面形式。

平安(备案)[2009]N47号-公众责任保险(1994版)条款

![平安(备案)[2009]N47号-公众责任保险(1994版)条款](https://img.taocdn.com/s3/m/c3895a6fcaaedd3383c4d318.png)

中国平安财产保险股份有限公司公众责任保险(1994版)条款一、责任范围(一)在本保险期间内,被保险人在本保险单明细表列明的范围内,因在其经营业务范围内的经营行为发生意外事故,造成第三者的人身伤亡和财产损失,依法应由被保险人承担的经济赔偿责任,保险人按下列条款的规定负责赔偿。

(二)对被保险人因上述原因而支付的诉讼费用以及事先经保险人书面同意而支付的其他费用,保险人亦负责赔偿。

(三)保险人对每次事故引起的赔偿金额以法院或政府有关部门根据现行法律裁定的应由被保险人偿付的金额为准。

但在任何情况下,均不得超过本保险单明细表中对应列明的每次事故赔偿限额。

在本保险期间内,保险人在本保险单项下对上述经济赔偿的最高赔偿责任不得超过本保险单明细表中列明的累计赔偿限额。

定义:意外事故:指不可预料的并且被保险人无法控制并造成物质损失或人身伤亡的突发性事件。

二、除外责任保险人对下列各项不负赔偿责任:(一)被保险人根据与他人的协议应承担的责任,但即使没有这种协议,被保险人仍应承担的责任不在此限;(二)对于为被保险人服务的任何人所遭受的人身伤亡或财产损失的责任;(三)对下列财产损失的责任:1.被保险人或其代表或其雇佣人员所有的财产或由其保管或由其控制的财产;2.被保险人或其代表或其雇佣人员因经营业务一直使用和占用的任何物品、土地、房屋或建筑。

(四)由于下列各项引起的损失或伤害责任:1.对于未载入本保险单明细表而属于被保险人的或其所占有的或以其名义使用的任何牲畜、脚踏车、车辆、火车头、各类船只、飞机、电梯、升降机、自动梯、起重机、吊车或其他升降装置;2.火灾、地震、爆炸、洪水、烟熏;3.大气、土地、水污染及其他污染;4.有缺陷的卫生装置或任何类型的中毒或任何不洁或有害的食物或饮料;5.由被保险人作出的或认可的医疗措施或医疗建议。

(五)由于震动、移动或减弱支撑引起任何土地、财产、建筑物的损坏责任;(六)由于战争、类似战争行为、敌对行为、武装冲突、恐怖活动、谋反、政变直接或间接引起的任何后果所致的责任;(七)由于罢工、暴动、民众骚乱或恶意行为直接或间接引起的任何后果所致的责任;(八)被保险人及其代表的故意行为或重大过失;(九)由于核裂变、核聚变、核武器、核材料、核辐射及放射性污染所引起的直接或间接责任;(十)罚款、罚金或惩罚性赔款;(十一)保险单明细表或有关条款中规定的应由被保险人自行负担的免赔额。

中国大地财产保险营业中断保险条款

中国大地财产保险股份有限公司营业中断保险条款总则第一条 本保险合同由保险条款、投保单、保险单或其他保险凭证以及批单组成。

凡涉及本保险合同的约定,均应采用书面形式。

第一条第二条 投保人应将被保险人在本保险合同载明的营业处所从事载明的经营业务(以下简称“营业”)所使用的物质财产向保险人投保相第二条关的物质财产损失保险。

物质财产损失保险合同(以下简称“物质损失保险合同”)号应在本保险合同中载明。

保险责任第三条 在保险期间内,被保险人因物质损失保险合同主险条款所承保的风险造成营业所使用的物质财产遭受损失(以下简称“物质保险第三条损失”),导致被保险人营业受到干扰或中断,由此产生的赔偿期间内的毛利润损失,保险人按照本保险合同的约定负责赔偿。

本保险合同所称赔偿期间是指自物质保险损失发生之日起,被保险人的营业结果因该物质保险损失而受到影响的期间,但该期间最长不得超过本保险合同约定的最大赔偿期。

本保险合同所称毛利润是指按照下述公式计算的金额:毛利润=营业利润+约定的维持费用或毛利润=约定的维持费用-营业亏损×约定的维持费用/全部的维持费用本保险合同所称维持费用是指被保险人为维持正常的营业活动而发生的、不随被保险人营业收入的减少而成正比例减少的成本或费用。

约定的维持费用由投保人自行确定,经保险人确认后在保险合同中载明。

除另有约定外,上述公式所用的会计措辞的含义与被保险人会计账表中的含义一致。

第四条第四条 发生第三条约定的保险事故后,被保险人申请赔偿时,按照保险人的要求提供有关账表、账表审计结果或其他证据所付给被保险人聘请的注册会计师的合理的、必要的费用(以下简称“审计费用”),保险人在本保险合同约定的赔偿限额内也负责赔偿。

责任免除第五条 保险人不负责赔偿下列损失:(一)投保人、被保险人的故意或重大过失行为产生或扩大的任何损失;;(二)由于物质损失保险合同主险条款责任范围以外的原因产生或扩大的损失;(二)由于物质损失保险合同主险条款责任范围以外的原因产生或扩大的损失(三)地震、海啸及其次生灾害产生或扩大的损失;(四)由于政府对受损财产的修建或修复的限制而产生或扩大的损失;(五)恐怖主义活动产生或扩大的损失;产生或扩大的损失;(五)恐怖主义活动(六)本保险合同载明的免赔额或本保险合同约定的免赔期内的损失。

电厂营业中断保险险条款

中华财险电厂营业中断保险附加险条款一、扩展类:1.附加新企业条款经保险合同双方特别约定,假设被保险人在保险期间内发生保险事故时其营业时间尚未超过一年的,保险人按照对毛利润率、标准营业收入和年度营业收入的如下约定计算毛利润损失:一、毛利润率按照被保险人从其营业开始至发生物质保险损失之日止的期间内的毛利润与营业收入的比例计算;二、标准营业收入按照被保险人从其营业开始至发生物质保险损失之日止的期间内的营业收入,乘以赔偿期间与前述期间的比例计算;三、年度营业收入按照被保险人从其营业开始至发生物质保险损失之日止的期间内的营业收入,乘以十二个月与前述期间的比例计算。

被保险人、保险人应根据被保险人营业趋势及情况的变化、物质保险损失发生前后营业受影响的情况或假设未发生物质保险损失原会影响营业的其他情况对毛利润率、标准营业收入以及年度营业收入进行必要的调整,使调整后的数额尽可能合理地接近在赔偿期间内假设未发生损失被保险人原可以取得的经营成果。

本附加险条款与主险条款内容相悖之处,以本附加险条款为准;未尽之处,以主险条款为准。

2.附加通道堵塞条款经保险合同双方特别约定且投保人已支付相应的附加保险费,假设本保险合同载明的营业处所临近的财产因发生物质财产损失保险合同主险条款责任范围内的事故遭受物质损失,造成该营业处所无法使用或堵塞进出该营业处所的通道,使被保险人营业受到干扰或中断,无论被保险人在该营业处所的财产是否发生物质保险损失,保险人均将其视为保险事故并对被保险人的损失按照保险合同约定进行赔偿。

但是对于临近本保险合同载明的营业处所并向该营业处所供气或供水的燃〔煤〕气厂或自来水厂,因其财产发生物质财产损失保险合同主险条款责任范围内的事故遭受物质损失而无法向该营业处所供气或供水,造成该营业处所无法使用或堵塞进出该营业处所的通道,使被保险人营业受到干扰或中断,则保险人不负责赔偿被保险人因此而遭受的损失。

保险人在本附加险条款项下的赔偿责任最高不得超过保险合同约定的相应的分项保险金额。

中国平安财产保险股份有限公司 保险产品目录

条款名称平安个人抵押商品住房综合保险平安个人购置住房抵押贷款保证保险平安国内贸易信用保险平安国内特定合同贸易信用保险平安国内贸易贷款信用保险外派劳务人员履约保证保险雇员忠诚保证保险雇员忠诚保证保险附加险平安产品质量保证保险平安产品质量保证保险境外产品扩展平安机动车辆道路救援保险机动车辆保险机动车单程提车保险摩托车,拖拉机保险电话营销专用机动车辆保险财产基本险财产综合险财产一切险财产险附加险财产一切险,财产综合险附加机器设备损坏保险营业中断保险营业中断保险附加险现金保险(1994版) 平安现金保险平安计算机综合保险平安锅炉压力容器综合保险平安电梯安全综合保险平安电梯安全综合保险附加电梯乘员精神损害赔偿责任保险平安银行业综合保险活动意外取消保险艺术品保险平安电子设备保险平安高尔夫球场(俱乐部)综合保险平安恒利达企业综合保险平安汽车生产商成品车损失保险平安汽车生产商成品车损失保险附加险平安珠宝一切险平安码头综合保险平安码头综合保险附加险平安展览会财产保险平安展览会财产保险附加险平安工程机械设备保险平安工程机械设备保险附加险平安企业贷款综合保险备案险种保证保险保证保险信用保险信用保险信用保险保证保险保证保险保证保险保证保险保证保险其他车险车险车险车险企业财产保险。

永安保险(备案)[2009]N7号-营业中断保险附加险

![永安保险(备案)[2009]N7号-营业中断保险附加险](https://img.taocdn.com/s3/m/48f6be7858fafab069dc02fb.png)

永安财产保险股份有限公司营业中断保险附加险条款本条款是《永安财产保险股份有限公司营业中断保险》(以下简称“主险”)的附加险条款。

本附加险合同未约定事项,以主险合同为准;主险合同与本附加险合同相抵触之处,以本附加险合同为准。

投保人可以选择其中的某一个、某几个或全部附加险投保。

一、扩展类K01.包括全部营业额条款K02.未保险的维持费用条款K03.通道堵塞条款K04.谋杀等条款K05.公众事业设备扩展条款K06.遗失欠款账册条款K07.恢复保险金额条款K08.每月预付赔款扩展条款K09.调整保险费条款K10.保单取消条款K11.不得进入条款K12.承包商/供应商条款K13.顾客/供应商/承包商条款K14.物质损失放弃免赔条款K15.关闭营业处所/设施条款K16.审计师条款K17.通道受阻条款K18.炸弹恐吓条款 (只适用于财产利润损失险)K19.政府法令条款 (不超过连续10星期)K20.营业费用增加条款K21.相关性条款K22.累积存货条款二、规范类G01.部门条款G02.账目分类条款G03.会计师条款G04.违反保险条件条款G05.错误及遗漏描述条款G06.保费调整条款G07.保险人90天通知取消保险或拒绝续保条款G08.新业务条款G09.产量条款G10.经营部门条款G11.新营业条款G12.预付赔款条款G13.不具名供应商及顾客扩展条款G14.放弃代位权条款一、扩展类K01.包括全部营业额条款在赔偿期限内如果为获得营业收入,被保险人或他人代其在营业处所以外的地点,销售货物或提供服务,则有关这项销售或服务所给付或应给付的金额,在计算赔偿期限的营业额时应包括在内。

K02.未保险的维持费用条款如本保险合同未承保经营业务的维持费用(根据本保险合同规定对毛利润的定义,在计算毛利润时已予减除),在计算本保险合同项下,可以取得补偿的营业费用增加的赔偿金额时,只赔偿营业费用增加乘以按毛利润与毛利润加上未保的维持费用之比例所得的那一部分额外费用。

营业中断险附加险条款(英文)[精选.]

![营业中断险附加险条款(英文)[精选.]](https://img.taocdn.com/s3/m/d48f305b763231126edb1191.png)

PICC Property and Casualty Company Limited Additional Clauses for Business Interruption InsuranceThe following clauses are the Additional Clauses for Business Interruption Insurance Policy (2009 Version), which is hereinafter called Policy. The terms , conditions and exclusions of the Policy shall apply except to the extent that they are expressly varied by the Additional Clauses. Any one of the Additional Clause(s) could be chosen by the Applicant to be attached to and forming part of the Policy.1.Extension ClausesK01. Scope of Cover (A)K06. Denial of Access (A)K07. Denial of Access (B)K08. Murder, Infectious Disease, and Food Contamination Extension (A)K09. Murder, Infectious Disease, and Food Contamination Extension (B)K10. Murder, Infectious Disease, and Food Contamination Extension (C)K11. Infectious Disease ExtensionK12. Closure of Operation FacilityK13. Public Utilities Extension (A)K14. Public Utilities Extension (B)K15. Loss of Book DebtsK16. Suppliers Extension ( A)K20. Customers/Suppliers /ContractorsK21. Unnamed Suppliers/CustomersK22. Bomb Scare (only applied to PDBI)K23. Government action (Not exceeding __ consecutive weeks)K24. Public Authority ExtensionK33. Departmental extensionK34. Au ditor’s FeesK35. Accountant’s/Auditor’s FeesK36. Errors & Omissions (A)K37. Errors & Omissions (B)2.Restriction ClausesX01. War and Terrorism ExclusionX02. IT ClarificationX03. Total Asbestos ExclusionX04. Mold & Fungi ExclusionX05. Y2K EXCLUSION CLAUSE3.Clarification ClausesG01. DesignationG02. Premium AdjustmentG03. Premium AdjustmentG04. Increase in Cost of WorkingG05. OutputG06.New BusinessG07. Monthly Payment on AccountG08. Payment on AccountG09. Gross Profit Difference BasisG13. Inclusion of All TurnoverG14. Uninsured Standing ChargesG15. Accumulated StocksG16. Breach of Condition and WarrantyG21. Automatic Reinstatement of Sum InsuredG22. __Days’ CancellationG23. __Days’ Notify Cancella tion or Refuse to RenewalG24. Nomination of Loss AdjusterG28. Co-InsuranceG32. Waiver of Subrogation (A)1.Extension ClausesK01. Scope of Cover(A)It is agreed and understood that, subject to the Applicant having paid the agreed additional premium, the Insurer shall indemnify the Insured in respect of loss of Gross Profit resulting from interruption of or interference with the business at the premises in consequence of physical damage to the property used in business operation caused by perils or hazards covered under the Physical Damage Insurance during the period of insurance.Provided that the Insurer shall not be liable for any loss due to causes as following:1.willful act and/or gross negligence of the Applicant and/or the Insured; and/or2.earthquake or tsunami and/or secondary disasters so caused; and/or3.strike, riot, civil commotion, malicious damage an/or act of terrorism; and/or4.confiscation, temporary or permanent requisition by order of the government de jure orde facto or by any public authority; and/or5.nuclear radiation, nuclear fission, nuclear fusion, nuclear pollution or contamination andother radioactive pollution or contamination; and/or6.pollution of atmosphere, soil, water and other non-radioactive pollution; and/or7.other exclusions which agreed by the Insurer and the Insured.This Clause is subject otherwise to the terms, Conditions and Exclusions of this Policy.K06. Denial of Access (A)It is agreed and understood that, subject to the Applicant having paid the agreed additional premium, loss as insured by this Policy resulting from interruption of or interference with the business in consequence of the damage (as within define) to property in the vicinity of the Premises which shall prevent or hinder the use thereof of access thereto, whether the Premises or property of the Insured therein shall be damaged or not, shall be deemed to be loss resulting from damage to property used by the Insured at the Premises.This Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K07. Denial of Access (B)It is agreed and understood that, subject to the Applicant having paid the agreed additional premium, loss as insured by this Policy resulting from interruption of or interference with the business in consequence of the damage (as within define) to property in the vicinity of the Premises which shall prevent or hinder the use thereof of access thereto, whether the Premises or property of the Insured therein shall be damaged or not, shall be deemed to be loss resulting from damage to property used by the Insured at the Premises.Provided, however, that the Insurer shall not be liable for any loss if the aforesaid prevention of the use of the premise or the hinder of the access thereto is contributed to the failure of gas and/or water supply in the vicinity of Insured premises resulting from the property damage thereof.The indemnity limit under this clause shall not exceed the relevant sub limits stated in the Policy.This Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K08. Murder, Infectious Disease, and Food Contamination Extension Clause (A)It is agreed and understood that, subject to the Applicant having paid the agreed additional premium, this Policy is extended to cover loss as insured hereunder resulting from interruption of or interference with the Business carried on by the Insured at the Premises in consequences of:1. Murder or suicide occurring at the Premises stated in the Policy;2. Closure &/or quarantine of the Premises stated in the Policy by order of a competent public authority due to Notifiable Infectious Disease manifested by any person at the Premises;3. Closing of the whole or part of the premises by order of a competent pulblic authority consequent upon defects in the drains and other sanitary facilities at the Premises stated in the Policy.4. Injury or illness sustained by any guest arising from spoilage of or infectious matter in food or drinks provided at the Premises stated in the Policy.In respect of each and every occurrence of the damage giving rise to a claim under this Clause, the Insurer shall not be liable for the first seventy-two (72) hours of such loss.It is a condition precedent to any liability of the Insurer that the Insured shall observe and fulfill relevant laws, regulations and requirements on security, sanitation and health, and shall exercise due diligence to avoid the occurrence of the contingencies aforementioned.The indemnity limit under this clause shall not exceed the relevant sub limits stated in the Policy.This Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K09. Murder, Infectious Disease, and Food Contamination Extension (B)It is agreed and understood that, subject to the Applicant having paid the agreed additional premium, this Policy is extended to cover loss as insured hereunder resulting from interruption of or interference with the Business carried on by the Insured at the Premises in consequences of:1. The cancellation of or inability to accept bookings for accommodation at the premises as a result of an outbreak of an infectious or contagious disease occurring at the Premises;2. Murder or suicide occurring at the Premises;3. Injury or illness sustained by any guest arising from spoilage of or infectious matter in food or drinks provided at the Premises;4. Closing of the whole or part of the Premises by order of a competent public authority consequent upon defects in the drains and other sanitary facilities at the Premises.It is a condition precedent to liability on the part of the Insurer that the Insured shall make sure every article is appropriately used and shall exercise due diligence to avoid the occurrence of the contingencies aforementioned.The indemnity limit under this clause shall not exceed __.This Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K10. Murder, Infectious Disease, and Food Contamination Extension (C)It is agreed and understood that, subject to the Applicant having paid the agreed additional premium, this Policy is extended to cover loss as insured hereunder resulting from interruption of or interference with the Business carried on by the Insured at the Premises in consequences of:1. The cancellation of or inability to accept bookings for accommodation at the premises as a result of an outbreak of an infectious or contagious disease occurring at the Premises;2. Murder or suicide occurring at the Premises;3. Injury or illness sustained by any guest arising from spoilage of or infectious matter in food or drinks provided at the Premises;4. Closing of the whole or part of the premises by order of a competent public authorityconsequent upon defects in the drains and other sanitary facilities at the Premises.In respect of each and every occurrence of the damage giving rise to a claim under this Clause, the Insurer shall not be liable for the first three (3) days of such loss.It is a condition precedent to liability on the part of the Insurer that the Insured shall make sure every article is appropriately used and shall exercise due diligence to avoid the occurrence of the contingencies aforementioned.This Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K11. Infectious Disease ExtensionIt is agreed and understood that, subject to the Applicant having paid the agreed additional premium, this policy is extended to cover loss resulting from interruption of or interference with the business as the direct and sole result of Notifiable Infectious Disease manifested by any person at the Insured Premises which results in the total closure &/or quarantine of the Insured Premises by order of a competent government authority.For the purpose of this insurance, Notifiable Infectious Disease means illness sustained by any person resulting from any human infectious or human contagious disease (excluding Acquired Immune Deficiency Syndrome (AIDS)), the outbreak of which should be notified to the competent public authorities.For the purpose of this insurance ,(1)Indemnity Period means the period during which the results of the business shall be affected in consequence of the Notifiable Infectious Disease, beginning with effective date of the order issued by the competent government authority and ending not later than the Maximum Indemnity Period thereafter.(2) Notwithstanding any provision to the contrary within any other additional clauses or endorsements thereto , it is agreed that this insurance shall only be liable for interruption of or interference with the Insured’s business as a result of an insured event occurred within the locations as specified in the schedule , wherein the insured carries on his business .Provided that the Insurers’ liability under this extension shall not exceed ___ per occurrence for all insured parties in respect of all premises stated in the policy and ___ in aggregate under this extension during any one period of insurance and subject to the time excess of this policy.Occurrence means a loss or series of loss arising out of the event of Notifiable Infectious Disease occurring during the period of insurance.This Clause is subject otherwise to other terms and conditions of this Policy.K12. Closure of Operation FacilityIt is agreed and understood that, subject to the Applicant having paid the agreed additionalpremium, any loss resulting from interruption of or interference with the Insured’s business due to shut-down of operation facility by order of the Health Authorities as a result of food spoilage or contamination, shall be considered as the loss resulting from the physical damage to the insured property, regardless whether the insured property are damaged or not.For the purpose of this extension, Indemnity Period means the period during which the results of the business shall be affected, beginning with 72 hours after the occurrence of the loss and ending not later than 12 months thereafter.It is a condition precedent to liability on the part of the Insurer that the Insured shall make sure every article is appropriately used and shall exercise due diligence to avoid the occurrence of the contingencies aforementioned.This Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K13. Public Utilities ExtensionIt is agreed and understood that, subject to the Applicant having paid the agreed additional premium, loss as insured by this Policy resulting from interruption of or interference with the Business carried on by the Insured at the Premises in consequence of failure of electricity, gas or water supply at the terminal ends of the electricity service feeders/Gas Works/Water Works from which the Insured obtained electric supply/Gas/water at the Premises directly due to the damage (as within defined) to property at an Electricity Station or Sub-station of Public Electricity Supply Undertaking from which the Insured obtained electric supply/Gas/water shall be deemed to be loss resulting from the damage to property used by the Insured at the Premises.Provided, however, that the Insurer shall not be liable for any loss occasioned by the deliberate act of the Government, Municipal or Local Authority or Supply Authority not performed for the sole purpose of safeguarding life or protecting any part of the supply undertaking's system or by the exercise by any such authority of its power to withhold or restrict or ration supply not necessitated solely by the damage to the supply undertaking's generating or supply equipment by an insured perils.For the purpose of the this insurance , the Indemnity Period in respect of each damage or of series of damages consequent on or attributable to one source or original cause shall be as follows:The period beginning with the occurrence of the damage and ending not later than sixty (60) days thereafter during which the result of the business shall be affected in consequence of the damage.Provided that the Insurer shall not be liable for any loss unless the duration of each such failure exceeds twenty-four (24) hours and the Insurer shall not be liable for any loss for the first twenty-four (24) hours of each such failure.In any action, suit or other proceedings where the Insurer alleges that by reason of the provisionsof this condition any loss or damage is not covered by this insurance, the burden proving that this loss or damage is covered shall be upon the Insured.This Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K14. Public Utilities Extension (B)It is hereby agreed and understood that, subject to the Applicant having paid the agreed additional premium, the Insurer shall indemnify the Insured for the loss resulting from interruption of or interference with the Business carried on by the Insured at the premises stated in the Policy in consequence of failure of gas or water supply at the terminal ends of the Gas Works/Water Works from where the Insured obtained gas/water supply, if such failure is directly due to the physical damage (as within defined) to property therein.For the purpose of this insurance, maximum indemnity period in respect of each occurrence shall be sixty (60) days since the date of such failure.The limit of indemnity under this clause shall be determined by the Applicant and specified in the Policy. The limit of indemnity shall not exceed:___In no case shall the insurer be liable for any loss occurred in the first twenty-four(24) hours of each such failure covered hereinThis Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K15. Loss of Book DebtsIt is agreed and understood that, subject to the Applicant having paid the agreed additional premium, within the respective limits of sums insured under this Policy, in the event of the records of accounts receivable kept on the premises being lost, destroyed or damaged by any of the perils insured against under this Policy the Insurer shall indemnify the Insured in respect of: 1) all sums due to the Insured from customers, provided the Insured is unable to effect collection thereof as a direct result of such loss,2) any collection expense in excess of normal collection cost and made necessary because of such loss,3) auditor’s charges necessarily and reasonably incurred in substantiating any claim under this extensionProvided that the Insured can substantiate the loss by documentary evidence by an Auditor and the Insurer's maximum liability under this extension shall not exceed_______.This extension applies only with respect to loss of or damage to records of accounts receivable and occurring during the period of insurance.This Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K16. Suppliers Extension (A)It is agreed and understood that, subject to the Applicant having paid the agreed additional premium, loss as insured by this Policy resulting from interruption of or interference with the business in consequence of the property damage at the premises of the suppliers of the Insured, which leads to the suppliers’ failure to provide the raw materials, commodities or goods in process necessarily for the Insured’s business, shall be deemed to be loss resulting from damage to property used by the Insured at the premises, and the Insurer shall be liable for such loss subject to the conditions of this Policy.For the purpose of this insurance ,Supplier means any individual ,firm ,company, corporation , joint venture or entity from which the Insured directly obtains supplies of commodities, materials, components, goods or services, other than suppliers of public energy and other public facilities.T he Insurer’s liability under this extension shall not exceed ___ for any one supplier and ___ in aggregate during the period of insurance.This Clause is subject otherwise to the terms, Conditions and Exclusions of this Policy.K20. Customers/Suppliers /ContractorsIt is agreed and understood that, subject to the Applicant having paid the agreed additional premium, loss as insured resulting from interruption of and interference with the business in consequence of property damage at the customers/suppliers/toll manufacturers’ premises or in the course of construction executed by the contractors shall be deemed to be loss resulting from damage to property used by the insured at the premises.The Insurer’s liability under this extension shall not exceed ___ during the period of insurance.This Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K21. Unnamed Suppliers/CustomersIt is agreed and understood that, subject to the Applicant having paid the agreed additional premium, loss as insured resulting from interruption of and interference with the business in consequence of damage to the property of the I nsured’s customers or suppliers at their premises in PRC, shall be deemed to be loss resulting from damage to property used by the insured at the premises.The limit of indemnity under this extension clause shall not exceed______.This Clause is subject otherwise to the terms, Conditions and Exclusions of this Policy.K22. Bomb Scare (only applied to PDBI)It is agreed and understood that, subject to the Applicant having paid the agreed additional premium, loss as insured by this Policy resulting from interruption of or interference with Business in consequence of bomb scare shall be deemed to be loss resulting from damage toproperty used by the Insured at the Premises.This clause is subject otherwise to the terms, conditions and exclusions of this Policy.K23. Government action (Not exceeding __ consecutive weeks)It is agreed and understood that, subject to the Applicant having paid the agreed additional premium, this Policy is extended to cover the loss as insured hereunder resulting directly from the interruption of or interference with the business, due to that the access to any insured premises is prohibited by order of civil authority as a direct result of damage to or destruction of property adjacent to the premises herein described by the peril(s) insured under physical damage insurance (Policy No.: ). T he Insurer’s liability under this extension shall not exceed ___ consecutive weeks, during the period of insurance .This Clause is subject otherwise to the terms, conditions and exclusions of this Policy.K24. Public Authority ExtensionIt is agreed and understood that, subject to the Applicant having paid the agreed additional premium, in the event of loss or damage to Property insured under the physical damage insurance, this Policy shall be extended to cover the loss of Gross Profit as may be incurred or expanded solely by reason of the necessity to comply with building or other regulations under or framed in pursuance of any ordinance law, statute, rules or with bye-laws of any relative public authority in the course of repair, reconstruction, or reinstatement.This Clause is subject otherwise to the terms, Conditions and Exclusions of this Policy.K33. Departmental ClauseIt is agreed and understood that if the business be conducted in departments the independent trading results of which are ascertainable, the provisions of the item on gross profit shall apply separately to each department affected by the damage except that if the Sum Insured by the said item be less than the aggregate of the sums produced by applying the rate of gross profit for each department of the business (Whether affected by the damage or not) to its relative annual turnover (or to a proportionately increased multiple thereof where the maximum indemnity period exceed twelve (12) months the amount payable shall be proportionately reduced.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.K34. Auditor’s FeesIt is agreed and understood that the auditor of the Insured is authorized to provide the necessary accounting records or any extract or detail of the accounting records for the purpose of the insurer to investigate or verify the claim under this policy. If the auditor happens to be performing seasonal works related with foresaid documents, the accounting/audit report shall be the preliminary supporting documents.This clause is subject otherwise to the terms, conditions and exclusions of this Policy.K35. Accountant’s/Auditor’s FeesIt is agreed and understood that any particulars or details contained in the Insured's books of account or other business books or documents which may be required by the Insurers for the purpose of investigating or verifying any claim hereunder may be produced by professional accountants if at the time they are regularly acting as such for the insured and their report shall be prima facie evidence of the particulars and details to which such report relates.The Insurer shall indemnify the Insured for the reasonable fees aforesaid payable to professional accounts or auditors provided that the sum of the amount payable under this extension shall in no case exceed_____.This clause is subject otherwise to the terms, conditions and exceptions of this Policy.K36. Errors &Omissions (A)It is agreed and understood that the interest of the Insured under this Policy shall not be prejudiced in the event of any unintentional delay or error or omission in reporting new locations acquired or occupied or in reporting any alteration of values of property or in reporting increase of hazard of the property insured or other material facts, provided that such delay, error or omission shall be immediately reported to the Insurer upon such alteration coming to the Insured’s knowledge.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.K37. Errors & Omissions (B)It is agreed and understood that the interest of the Insured under this Policy shall not be prejudiced in the event of any unintentional delay or error or omission in reporting new locations acquired or occupied or in reporting any alteration of values of property or in reporting increase of hazard of the property insured or other material facts, provided that such delay, error or omission shall be immediately reported to the Insurer upon such alteration coming to the Insured’s knowledge and additional premium, if any, shall be charged from the date of such increase of hazard to the expiration of this Policy.Incorrect, defect or wrong valuation shall not be deemed as unintentional errors and omissions.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.2.Restriction ClausesX01. War and Terrorism ExclusionNotwithstanding any provision to the contrary within this insurance or any Endorsement thereto it is agreed that this insurance excludes damage, cost or expense of whatsoever nature directly or indirectly caused by, resulting from or in connection with any of the following regardless ofany other cause or event contributing concurrently or in any other sequence to the loss:(1) War, invasion, acts of foreign enemies, hostilities or warlike operations (whether war be declared or not), civil war, rebellion, revolution, insurrection, assuming the proportions of or amounting to an uprising, military or usurped power; or(2) Any act of terrorism.For the purpose of this insurance an act of terrorism means an act, including but not limited to the unlawful use of force or violence and/or the threat thereof, of any person or group(s) of persons, whether acting along or on behalf of or in connection with any organization(s) or government(s), committed for political, religious, ideological, or similar purposes including the intention to influence any government, and/or to put the public, or any section of the public, in fear for such purpose ..This Endorsement also excludes damage, cost or expense of whatsoever nature directly or indirectly caused by, resulting from or in connection with any action taken in controlling, preventing, suppressing or in any way relating to (1) and /or (2) above.In the event any portion of this Endorsement is found to be invalid or unenforceable, the remainder shall remain in full force and effect.This Clause is subject otherwise to the terms, Conditions and Exclusions of this Policy.X02. IT Clarification ClauseProperty damage covered under this Policy means physical damage to the substance of property. Physical damage to the substance of property shall not include damage to data or software, in particular any detrimental change in data, software or computer programs that is caused by a deletion corruption or a deformation of the original structure.Consequently the following are excluded from this Policy:Loss of or damage to data or software, in particular any detrimental change in data, software or computer programs that is caused by a deletion, a corruption or a deformation of the original structure, and any business interruption losses resulting from such loss or damage. Notwithstanding this exclusion, loss of or damage to data or software which is the direct consequence of insured physical damage to the substance of property shall be covered.Loss or damage resulting from an impairment in the function, availability, range of use or accessibility of data, software or computer programs, and any business interruption losses resulting from such loss or damage.This Clause is subject otherwise to the terms, Conditions and Exclusions of this Policy.X03. Total Asbestos ExclusionIt is hereby understood and agreed that this Policy shall not apply to and does not cover any actual or alleged liability whatsoever for any claim or claims in respect of loss or losses directly。

安联财产保险(中国)有限公司营业中断保险附加条款I

附件一营业中断保险条款附加条款扩展类及规范类条款一、扩展类 (3)1.附加新企业条款 (3)2.附加通道堵塞条款 (3)3.附加公共事业设备条款 (3)4.附加供应商条款 (4)5.附加购买商条款 (4)6.附加谋杀、传染病和污染条款A (5)7.附加谋杀、传染病和污染条款B (5)8.包括全部营业额条款 (5)9.未保险的维持费用条款 (6)10.共保条款(90%) (6)11.遗失欠款帐册条款 (6)12.当局禁止条款 (6)13.机损险2000年问题除外责任条款 (7)14.营业费用增加条款 (7)15.保险金额自动恢复条款 (7)16.编辑记录及索赔准备费用条款 (7)17.持续损失条款 (7)18.关闭营业处所/设施条款 (8)19.损失确定的费用条款 (8)20.公共设备供应中断条款 (8)21.审计专业费用条款 (8)22.累积存货条款 (9)23.免赔额豁免条款 (9)24.MR811Hull Risk for Mobile Equipment on Premises only (9)25.MR812 Hull Risk for Mobile Equipment Including Inland Transit (9)26.MR813 Internal Fire, Internal Chemical Explosion and Direct Lightning (10)27.MR817 Underground Machinery and Equipment (10)28.MR829 Machinery Breakdown during Guarantee Period (10)29.MR855 Radioactive Isotopes in Instruments (11)30.MR856 Deterioration of Raw Materials, Intermediate or Finished Products, orOperating Media (11)31.MR857 Prolongation of the Interruption Period due to Deterioration (12)32.MR861 Increased Cost of Electricity, Water, Gas or Steam Supply (12)33.MR862 Maximum Demand Charges (12)34.MR863 Additional Expenditure other than Increase in Cost of Working (13)35.MR866 Failure of Public Power, Water, Gas or Steam Supply (13)36.Denial of Access Clause (14)37.Extra Charges Clause (15)38.Failure of Public Utilities Clause (15)d and Unnamed Customers/Suppliers Extension Clause (16)40.Molten Material Clause (16)二、规范类 (17)1.错误和遗漏条款 (17)2.产量条款 (17)3.自动恢复保险金额条款 (17)4.分部门条款 (18)5.每月预付赔款 (18)6.调整保险费条款 (18)7.物质损失放弃免赔条款 (18)8.六十天取消保单条款 (18)9.指定公估人条款 (19)10.独立被保险人条款 (19)11.财务利益关系方条款 (19)12.损失的赔款支付条款 (20)13.损失受益人条款 (20)14.专业会计师条款 (20)15.延迟支付条款 (20)16.预付赔款条款 (20)17.MR842 Non-Destructive Testing (NDT) of Presses, Shears and Similar items withFrames or other Components exposed to High Stresses (21)18.MR843 Overhaul of Electric Motors and Generators (21)19.MR844 Overhaul of Steam, Water and Gas Turbines and Turbo-Generator Sets (22)20.MR845 Inspection and Overhaul of Boilers (23)21.MR891 Delay in Repair (24)22.MR892 Indemnity Period Limits Exceeding 12 Months (24)23.MR893 Proportional Time Excess (24)24.MR894 Sum insured on Unit Price Basis (24)25.Inclusion of All Turnover Clause (25)26.Interdependency Clause (25)27.Premium Adjustment Clause (25)28.Automatic Reinstatement of Sum Insured Clause (26)29.Average Relief Clause (26)30.Loss Notification Clause (26)31.Non-Invalidation Clause (26)32.Payment on Account Clause (27)33.Premium Payment Warranty (60 days) (27)34.30 Days Notice of Cancellation by Insurer Clause (27)一、 扩展类1.附加新企业条款经保险合同双方特别约定,若被保险人在保险期间内发生保险事故时其营业时间尚未超过一年的,保险人按照对毛利润率、标准营业收入和年度营业收入的如下约定计算毛利润损失:一、毛利润率按照被保险人从其营业开始至发生物质保险损失之日止的期间内的毛利润与营业收入的比例计算;二、标准营业收入按照被保险人从其营业开始至发生物质保险损失之日止的期间内的营业收入,乘以赔偿期间与前述期间的比例计算;三、年度营业收入按照被保险人从其营业开始至发生物质保险损失之日止的期间内的营业收入,乘以十二个月与前述期间的比例计算。

营业中断险附加险

中国人民财产保险股份营业中断保险附加险条款(2009版)本条款是《中国人民财产保险股份营业中断保险(2009版)》(以下简称“主险”)的附加险条款。

本附加险合同未约定事项,以主险合同为准;主险合同与本附加险合同相抵触之处,以本附加险合同为准。

投保人可以选择其中的某一个、某几个或全部附加险投保。

一、扩展类K01.包括全部营业额条款K02.未保险的维持费用条款K03.通道堵塞条款K04.谋杀等条款K05.公众事业设备扩展条款K06.遗失欠款账册条款K07.恢复保险金额条款K08.每月预付赔款扩展条款K09.调整保险费条款K10.保单取消条款K11.不得进入条款K12.承包商/供应商条款K13.顾客/供应商/承包商条款K14.物质损失放弃免赔条款K15.关闭营业处所/设施条款K16.审计师条款K17.通道受阻条款K18.炸弹恐吓条款(只适用于财产利润损失险)K19.政府法令条款(不超过连续10星期)K20.营业费用增加条款K21.相关性条款K22.累积存货条款二、规类G01.部门条款G02.账目分类条款G03.会计师条款G04.违反保险条件条款G05.错误及遗漏描述条款G06.保费调整条款G07.保险人90天通知取消保险或拒绝续保条款G08.新业务条款G09.产量条款G10.经营部门条款G11.新营业条款G12.预付赔款条款G13.不具名供应商及顾客扩展条款G14.放弃代位权条款一、扩展类K01.包括全部营业额条款在赔偿期限如果为获得营业收入,被保险人或他人代其在营业处所以外的地点,销售货物或提供服务,则有关这项销售或服务所给付或应给付的金额,在计算赔偿期限的营业额时应包括在。

K02.未保险的维持费用条款如本保险合同未承保经营业务的维持费用(根据本保险合同规定对毛利润的定义,在计算毛利润时已予减除),在计算本保险合同项下,可以取得补偿的营业费用增加的赔偿金额时,只赔偿营业费用增加乘以按毛利润与毛利润加上未保的维持费用之比例所得的那一部分额外费用。

营业中断保险所需材料

机损险项下营业中断保险所需材料

上海东大保险经纪有限责任公司:

关于河北建投集团的营业中断保险案件,请尽快提供以下材料。

以便尽快处理相关赔案。

1.索赔申请书

2.报损清单

3.受损设备运行报告(控制系统内故障停机截图)

4.受损设备停机时间证明(控制系统内截图)

5.维修厂家的正式事故原因分析报告以及维修报告

6.受损设备的投保清单

7.被保险人的三证(组织机构代码证、税务登记证、营业执照)

8.受损风机临近2台风机,在受损风机停机期间的发电量记录,

需提供控制系统内的电子记录或者截图

9.受损设备的投产记录,或者是竣工的记录或者文件,因为前

期被保险人称去年没有投产运营,那么计算方式与保单约定不符,因此需要提供相关证明,证实去年没有发电

10.出险风机出险故障前一天的正常运行记录(控制系统内截图)

11.出险前最近一次与电网的结算单,或者是与电网的销售合同

复印件

12.经了解,被保险人的部分报损案件中的设备,生产厂家已经

免费更换,沧州1月8日和2月21日风机电机损失案件、蔚县12月25日电容受损案件、3月9日蔚县风机折断案件。

请被保险人提供情况说明。

13.被保险人的开户行以及银行帐号

中国平安财产险保险股份有限公司秦皇岛中心支公司

2011-3-14。

营业中断保险特点及法律问题探究——兼论疫情营业中断指数保险可保性

致损失往往被列入营业中断保险的责任免 除事项。为助力企业复工复产,多地政府联 合保险公司推出一些疫情防控保险,这类保 险由政府主导推出,保险费由政府和企业分 担,采取定额补贴方式对企业利润损失进行 补偿,如海南推出的“复工复产企业疫情防 控综合保险”,保障企业因封闭或隔离等疫 情防控行为导致的营业中断损失、员工工资 及隔离费用支出;宁波推出的“小微企业政

营业中断保险的索赔方式类似于责任 保险的“期内发生式”,事故必须发生在保险 期限内。赔偿期间可以超出保险期限,从岀 险之日起计算,至恢复正常营业之日止,考 虑了受到影响的财务指标。损失核定必须 以被保险人会计核算资料为基础。

(二)营业中断保险也作为机器损坏保 险的附加险

机器损坏保险是从传统财产保险中分 离并扩展出来的险种,主要承保机械或人为 因素造成的机器损坏,属于物质损失保险。 机损利损险(即机器损坏保险项下的营业中 断保险)主要保障机器设备在遭受意外事故 损失时,由于修复或重置受损机器设备造成 营业中断而产生的利润损失,跟随机器损坏 保险投保,以机器损坏保险责任成立为理赔 基础,属于附加险。

我国营业中断保险往往存在于一揽子 保险协议中,不同于一般的附加险形式,它 有单独的承保明细表、保险责任、责任免除、 特别约定和附加条款,承保理赔基础也不同 于财产保险,但承保实务中又不允许单独投 保。这主要是因为利润损失具有不确定性, 难以预估,容易产生道德风险。保险人通常 要求投保人在投保企业财产保险或机器损 坏保险基础上附加投保营业中断保险,附加 投保有助于保险人控制理赔风险。

根据《中国人民财产保险股份有限公司 营业中断保险条款(2009版)》第三条和第四 条,保险责任是指被保险人因财产保险(即 物质损失保险)条款所承保的风险造成营业 所使用的物质财产遭受损失,导致被保险人 营业受到干扰或中断,由此产生的赔偿期间 内的毛利润损失和审计费用,保险人按照保 险合同的约定负责赔偿;赔偿期间是指自物 质保险损失发生之日起,被保险人的营业结 果因该损失而受到影响的期间,但该期间最 长不得超过保险合同约定的最大赔偿期。 第二十三条规定,被保险人在物质损失保险 合同主险条款项下取得赔款或其保险责任 已获保险人认定,是保险人承担保险合同项 下赔偿责任的前提条件。可见,我国营业中

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

营业中断保险条款中国平安财产保险股份有限公司营业中断保险条款总则第一条本保险合同由保险条款、投保单、保险单或其他保险凭证以及批单组成。

凡涉及本保险合同的约定,均应采用书面形式。

第二条投保人应将被保险人在本保险合同载明的营业处所从事载明的经营业务(以下简称“营业”)所使用的物质财产向保险人投保相关的物质财产损失保险。

物质财产损失保险合同(以下简称“物质损失保险合同”)号应在本保险合同中载明。

保险责任第三条在保险期间内,被保险人因物质损失保险合同主险条款所承保的风险造成营业所使用的物质财产遭受损失(以下简称“物质保险损失”),导致被保险人营业受到干扰或中断,由此产生的赔偿期间内的毛利润损失,保险人按照本保险合同的约定负责赔偿。

本保险合同所称赔偿期间是指自物质保险损失发生之日起,被保险人的营业结果因该物质保险损失而受到影响的期间,但该期间最长不得超过本保险合同约定的最大赔偿期。

本保险合同所称毛利润是指按照下述公式计算的金额:毛利润=营业利润+约定的维持费用或毛利润=约定的维持费用-营业亏损×约定的维持费用/全部的维持费用本保险合同所称维持费用是指被保险人为维持正常的营业活动而发生的、不随被保险人营业收入的减少而成正比例减少的成本或费用。

约定的维持费用由投保人自行确定,经保险人确认后在保险合同中载明。

除另有约定外,上述公式所用的会计措辞的含义与被保险人会计账表中的含义一致。

第四条发生第三条约定的保险事故后,被保险人申请赔偿时,按照保险人的要求提供有关账表、账表审计结果或其他证据所付给被保险人聘请的注册会计师的合理的、必要的费用(以下简称“审计费用”),保险人在本保险合同约定的赔偿限额内也负责赔偿。

责任免除第五条保险人不负责赔偿下列损失:(一)投保人、被保险人的故意或重大过失行为产生或扩大的任何损失;(二)由于物质损失保险合同主险条款责任范围以外的原因产生或扩大的损失;(三)地震、海啸及其次生灾害产生或扩大的损失;(四)由于政府对受损财产的修建或修复的限制而产生或扩大的损失;(五)恐怖主义活动产生或扩大的损失;(六)本保险合同载明的免赔额或本保险合同约定的免赔期内的损失。

保险金额与赔偿限额第六条毛利润损失保险金额由投保人自行确定并在保险合同中载明。

第七条审计费用赔偿限额由投保人自行确定并在保险合同中载明。

保险期间与最大赔偿期第八条除另有约定外,保险期间为一年,以保险单载明的起讫时间为准。

第九条最大赔偿期由投保人自行确定并在保险合同中载明。

免赔额与免赔期第十条免赔额或免赔期由投保人与保险人在订立保险合同时协商确定,并在保险合同中载明。

保险人义务第十一条订立保险合同时,采用保险人提供的格式条款的,保险人向投保人提供的投保单应当附格式条款,保险人应当向投保人说明保险合同的内容。

对保险合同中免除保险人责任的条款,保险人在订立合同时应当在投保单、保险单或者其他保险凭证上作出足以引起投保人注意的提示,并对该条款的内容以书面或者口头形式向投保人作出明确说明;未作提示或者明确说明的,该条款不产生效力。

第十二条本保险合同成立后,保险人应当及时向投保人签发保险单或其他保险凭证。

第十三条保险人依据第十七条所取得的保险合同解除权,自保险人知道有解除事由之日起,超过三十日不行使而消灭。

自保险合同成立之日起超过二年的,保险人不得解除合同;发生保险事故的,保险人承担赔偿责任。

保险人在合同订立时已经知道投保人未如实告知的情况的,保险人不得解除合同;发生保险事故的,保险人应当承担赔偿责任。

第十四条保险人按照第二十二条的约定,认为被保险人提供的有关索赔的证明和资料不完整的,应当及时一次性通知投保人、被保险人补充提供。

第十五条保险人收到被保险人的赔偿保险金的请求后,应当及时作出是否属于保险责任的核定;情形复杂的,应当在三十日内作出核定,但保险合同另有约定的除外。

保险人应当将核定结果通知被保险人;对属于保险责任的,在与被保险人达成赔偿保险金的协议后十日内,履行赔偿保险金义务。

保险合同对赔偿保险金的期限有约定的,保险人应当按照约定履行赔偿保险金的义务。

保险人依照前款约定作出核定后,对不属于保险责任的,应当自作出核定之日起三日内向被保险人发出拒绝赔偿保险金通知书,并说明理由。

第十六条保险人自收到赔偿保险金的请求和有关证明、资料之日起六十日内,对其赔偿保险金的数额不能确定的,应当根据已有证明和资料可以确定的数额先予支付;保险人最终确定赔偿的数额后,应当支付相应的差额。

投保人、被保险人义务第十七条订立保险合同,保险人就保险标的或者被保险人的有关情况提出询问的,投保人应当如实告知。

投保人故意或者因重大过失未履行前款规定的如实告知义务,足以影响保险人决定是否同意承保或者提高保险费率的,保险人有权解除保险合同。

投保人故意不履行如实告知义务的,保险人对于合同解除前发生的保险事故,不承担赔偿责任,并不退还保险费。

投保人因重大过失未履行如实告知义务,对保险事故的发生有严重影响的,保险人对于合同解除前发生的保险事故,不承担赔偿责任,但应当退还保险费。

第十八条除另有约定外,投保人应在保险合同成立时一次性支付全部保险费。

保险费交付前发生的保险事故,保险人不承担赔偿责任。

第十九条被保险人应当遵守国家有关消防、安全、生产操作、劳动保护等方面规定,加强管理,采取合理的预防措施,尽力避免或减少责任事故的发生,维护保险标的的安全。

保险人可以对被保险人遵守前款约定的情况进行检查,向投保人、被保险人提出消除不安全因素和隐患的书面建议,投保人、被保险人应该认真付诸实施。

投保人、被保险人未按照约定履行其对保险标的的安全应尽责任的,保险人有权要求增加保险费或者解除合同。

第二十条在保险期间内,如被保险人在保险合同载明的营业处所经营的业务发生变化、被进行清算或由清算人或财产管理人接管经营,或营业所用的物质财产的风险加大,以及足以影响保险人决定是否继续承保或是否增加保险费的保险合同重要事项变更,被保险人应及时书面通知保险人,保险人有权要求增加保险费或者解除合同。

被保险人未履行前款约定的通知义务的,因保险标的的危险程度显著增加而发生的保险事故,保险人不承担赔偿责任。

第二十一条知道保险事故发生后,被保险人应当:(一)尽力采取必要、合理的措施以修理、修复营业所用的受损的物质财产,尽快恢复营业以防止或减少因营业受到干扰或中断所造成的损失,否则,对因此扩大的损失,保险人不承担赔偿责任;(二)立即通知保险人,并书面说明事故发生的原因、经过和损失情况;故意或者因重大过失未及时通知,致使保险事故的性质、原因、损失程度等难以确定的,保险人对无法确定的部分,不承担赔偿责任,但保险人通过其他途径已经及时知道或者应当及时知道保险事故发生的除外;(三)保护事故现场,允许并且协助保险人进行事故原因和损失情况的调查,以及对被保险人相关的会计凭证和账表的检查;对于拒绝或者妨碍保险人进行上述调查或检查导致无法确定事故原因或核实损失情况的,保险人对无法核实的部分不承担赔偿责任。

第二十二条被保险人请求赔偿时,应向保险人提供下列证明和资料:(一)保险单正本、索赔申请、财产损失清单、技术鉴定证明、事故报告书、救护费用发票、相关的会计凭证及账表、单据和有关部门的证明;(二)投保人、被保险人所能提供的与确认保险事故的性质、原因、损失程度等有关的其他证明和资料。

投保人、被保险人未履行前款约定的单证提供义务,导致保险人无法核实损失情况的,保险人对无法核实的部分不承担赔偿责任。

赔偿处理第二十三条发生保险事故后,被保险人在物质损失保险合同主险条款项下取得赔款或其保险责任已获保险人认定,是保险人承担本保险合同项下赔偿责任的前提条件。

如被保险人因物质损失保险合同主险条款项下的免赔额而无法获得该合同项下的赔款,则不受本条前款约定所限。

第二十四条赔偿期间内的毛利润损失为分别按照营业收入的减少和经营费用的增加计算的损失之和,扣除在赔偿期间内被保险人因保险事故的发生而从毛利润中减少或停止支付的费用:(一)因营业收入减少导致的损失为毛利润率乘以赔偿期间内的实际营业收入与标准营业收入的差额,即:毛利润率×(标准营业收入-赔偿期间内的实际营业收入)本保险合同所称营业收入是指被保险人在营业过程中,因销售商品、提供劳务或者让渡资产使用权等实现的收入金额。

本保险合同所称毛利润率是指发生物质保险损失之日前最近一个完整的会计年度内的毛利润与营业收入的比率。

本保险合同所称标准营业收入是指发生物质保险损失之日前十二个月中与赔偿期间对应的日历期间的营业收入。

在赔偿期间内,被保险人或他人代其在保险合同载明的营业处所以外的地点从事保险合同载明的经营业务而取得的营业收入,应计算在赔偿期间内的实际营业收入内。

(二)经营费用增加导致的损失是指被保险人专门为避免或降低赔偿期间内营业收入的减少而额外支出的必要的、合理的经营费用或成本;如果不予支出,则赔偿期间内的营业收入就会因保险事故的发生而降低。

但该项损失以不超过毛利润率乘以因花费该经营费用而避免降低的营业收入为限。

若投保人确定的维持费用仅包括营业所需的部分维持费用,则保险人对额外增加的经营费用的赔偿金额按照该经营费用乘以毛利润与毛利润加上未承保的维持费用的比例计算,即:增加的经营费用×毛利润/(毛利润+未承保的维持费用)第二十五条若最大赔偿期小于或等于十二个月,且保险金额低于毛利润率与年度营业收入的乘积,则保险人对毛利润损失的赔偿金额应按保险金额和前述乘积的比例计算确定,即:赔偿金额=毛利润损失×保险金额/(毛利润率×年度营业收入)若最大赔偿期大于十二个月,且保险金额低于毛利润率与年度营业收入及最大赔偿期与十二个月的比例的乘积,则保险人对毛利润损失的赔偿金额应按保险金额和前述乘积的比例计算确定,即:赔偿金额=毛利润损失×保险金额/(毛利润率×年度营业收入×最大赔偿期/12)。

本保险合同所称年度营业收入是指发生物质保险损失之日前十二个月内的营业收入。

第二十六条被保险人、保险人应根据被保险人营业趋势及情况的变化、物质保险损失发生前后营业受影响的情况或若未发生物质保险损失原本会影响营业的其他情况对毛利润率、标准营业收入以及年度营业收入进行必要的调整,使调整后的数额尽可能合理地接近在赔偿期间内若未发生损失被保险人原本可以取得的经营成果。

第二十七条若保险合同约定了免赔额,保险人按照第二十四条、第二十五条计算的毛利润损失扣除保险合同约定的免赔额计算毛利润损失赔偿金额。

若保险合同约定了免赔期,则免赔额为免赔期和赔偿期间的比例与按照本条款第二十四条、第二十五条计算出的毛利润损失的乘积。

第二十八条因保险事故而发生的保险责任约定的审计费用,保险人按费用实际发生数予以赔偿,但最高不超过保险合同中载明的相应赔偿限额。