新编金融英语教程 Chapter1 Money

[教材]高等院校金融英语教科书第一单元翻译

![[教材]高等院校金融英语教科书第一单元翻译](https://img.taocdn.com/s3/m/39ee830453d380eb6294dd88d0d233d4b14e3fca.png)

货币(Money)1,1货币的定义:货币是指在支付购买商品和服务的款项方面以及在清偿债务方面为人们所普遍接受的事物。

currency(指纸币和硬币)显然符合这一定义,是money的一种类型。

然而,money仅仅是被定义为currency对于现在的人们来说太狭隘了,因为事实上不仅可以通过currency(货币,指硬币和纸币)进行支付,还可以通过支票转账和电子转账来进行支付。

因此,支票也作为被接受的用于购买的支付工具,支票账户存款也被认为是种货币。

有时,就有必要使用货币(money)的广义定义,因为如果money可以很便捷的转换为currency,那么像储蓄存款等实际上也可以发挥货币的作用。

1.2货币的类型1.2.1商品货币:商品货币或者实物货币是一种其价值来源于制作商品的货币,制作商品货币或实物货币的商品本身也拥有价值同时也可作为货币来使用。

曾被用来作为交换媒介的商品有金、银、铜、盐、大的石头、装饰的腰带、贝壳、酒、烟、大麦等。

实际上,在过去的4000年期间,主要的商品货币是贵金属:大多数是银、金,也称为足值货币,贵金属货币阶段是商品货币的阶段之一。

几乎所有的国家都曾经经历过贵金属货币(是货币的一种完美的形式)阶段。

1.2.2代用货币:代用货币或者代用足值货币是指完全有贵金属作为支持的货币。

代用货币的价值与商品有着直接固定的关系,然而它们本身并不是由商品构成。

在20世纪30年代,经济与金融危机爆发,纸币不再能兑换为贵金属,金本位制或者银本位制瓦解,主要的西方国家不得不脱离金属本位制。

因此,纸币不能再被兑换为黄金。

自那时开始,代用货币退出流通领域,信用货币就出现了。

1.2.3信用货币:信用货币既不是由特定的有价值的商品构成的也不代表特定的有价值的商品。

信用货币的价值取决于其普遍接受程度(而普遍接受程度又是以发行者的信用为基础的),信用货币是通过信用流程发行的。

信用货币有两个特征:一是和贵金属的联系,另一个其价值是基于国家政府和银行的信用。

金融英语课件(unit 1)

教学重点(Emphases and difficult points) :

some important vocabulary: banknote, joint stock company, acquisition, monetary polices, lender of last resort, liquidity, bank run, IMF, IBRD, financial institution, etc.; transformation, empower, directives, comply (with), implement, oversee, supervisory, registration ;the understanding about the history and function of the Bank of England. the brief knowledge of the banking system in China. Some specialized English words.

Exercises and Key to Exercises

(1)1.英格兰银行 Bank of England 2.银行营业部 Banking Department 3.股份公司joint stock company 4.接 受存款机构 deposit-talking institution 5.规章制度 rules and regulations 6.执行货币政策 implement monetary policy 7.贴现行 discount house 8.公众利益 public interest 9.国际货币基金组织 International Monetary policy 10.世界银行 World Bank (2)ACBCD (3) Some questions: What are the functions of the central bank? When was the Bank of England founded?

金融专业英语 Unit 1 Money

Learning Targets

After learning this unit, you will be able to: understand the general definition of money; explain the functions of money; explain the forms of money; describe the contents of monetary system.

0 9 International Financing

1 0 Financial Derivatives

1 1 International Financial Institution

12

International Banking Regulatory Framework

Unit 1 Money

1.1 Introduction 1.2 Functions of Money 1.3 Forms of Money 1.4 Monetary System

1.1.1 History of Money

简单或偶然的价值形式

扩大的价值形式

一般价值形式

货币形式

Simple or Accidental Expanded Form of

Form of Value

Value

General Form of Value

Currency Form

1.1.1.1 Simple or Accidental Form of Value

1.1 Introduction

1.1.1 History of Money

Human society has existed for millions of years, but the emergence of money is only a few thousand years. There are many theories about the origin of money in history, but none of them have formed a complete theoretical system. Until Marx, from the view of dialectical materialism (辩证唯物 主义) and historical materialism (历史唯物 主义), explained the essence of money— the labor theory of value (劳动价值论). Marx believed that money originated from commodity exchange, and its economic root was private ownership. It was formed spontaneously in the process of commodity exchange.

Financial English 金融英语教程chapter 1 money-张铁军教材版本

2. Compound Interest S=P(I+R)n I=S-P

Page 24

1.4.2 Nominal and Real Interest Rates

1. The definition of nominal interest. P7, 1.4.2, L1-2 2. The definition of real interest. P7, 1.4.2, L3-4

Page 2

Benefits

Financial English course will provide you with:

- Greater confidence when discussing financial documents and data

- Increased verbal fluency for face-to-face negotiations

Assignment

20%

Exam

50%

Total

100%

Page 4

Part 1 Money

1. Definition of Money 2. Types of Money 3. Functions of Money 5. Interest and Interest Rate 6. Money Supply 7. China’s Monetary System

Page 5

Chapter 1 Money

Professional Terms

1.monetary area货币区 货币区是货币一体化的较高层次,它是指成员国之间的货

币建立紧密联系的地理区域。 货币区的初级阶段是固定汇率制度,包括货币局制度和美

120新编金融英语教程

CONTENTS

1.1 L e a d - i n 1.2 K e y Po i n t s 1.3 L a n g u a g e N o t e s 1.4 F o l l o w - u p Ta s k s 1.5 E x t e n d e d Ta s k s

M1

M1 is the measure that corresponds most closely to the definition of money. It consists of currency held by the public and checkable deposits.

M2

M2 consists of everything in M1 plus some highly liquid assets which can be converted to the items in M1 very easily without the loss of value for the principal. The other highly liquid assets are small savings, time deposits, MMDAs, and individual money market mutual funds.

最新金融英语课件(unit 1)

外汇清算 multilateral/bilateral clearing 多边/双边清算

Exercises and Key to Exercises

(1)1.英格兰银行 Bank of England 2.银行营业部

the central bank system in the United States : FED ---- The Federal Reserve System.

the central bank system in Britain (part A):

Bank of England

Now, let’s turn to the FED. Please try to find out the differences between the central bank system in British and the United States.

Language Points(语言点)

6. acquisition knowledge acquisition 知识收集 language acquisition 语

言习得 lump-sum acquisition 总价采购 real estate acquisition

不动产购置 7. finance n. 财务;金融;资金v.为(计划等)提供资金,

Language Points(语言点)

9. discount n. 折扣,贴现 bank discount 银行折扣,银行贴现 cash discount 付

现折扣 compound discount 复利贴现 customary discount 行

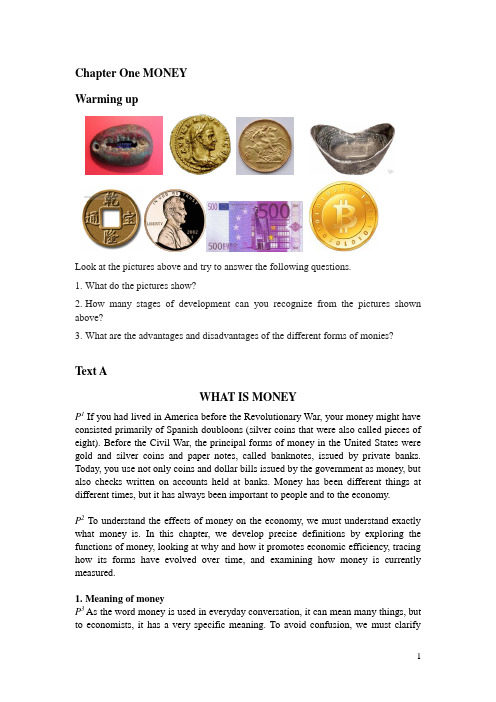

财经英语ChapterOneMoney

Chapter One MONEYWarming upLook at the pictures above and try to answer the following questions.1.What do the pictures show?2.How many stages of development can you recognize from the pictures shown above?3.What are the advantages and disadvantages of the different forms of monies? Text AWHAT IS MONEYP1 If you had lived in America before the Revolutionary War, your money might have consisted primarily of Spanish doubloons (silver coins that were also called pieces of eight). Before the Civil War, the principal forms of money in the United States were gold and silver coins and paper notes, called banknotes, issued by private banks. Today, you use not only coins and dollar bills issued by the government as money, but also checks written on accounts held at banks. Money has been different things at different times, but it has always been important to people and to the economy.P2 To understand the effects of money on the economy, we must understand exactly what money is. In this chapter, we develop precise definitions by exploring the functions of money, looking at why and how it promotes economic efficiency, tracing how its forms have evolved over time, and examining how money is currently measured.1.Meaning of moneyP3 As the word money is used in everyday conversation, it can mean many things, but to economists, it has a very specific meaning. To avoid confusion, we must clarifyhow economists’ use of the word money differs from conventional usage.P4 Economists define money (also referred to as the money supply) as anything that is generally accepted in payment for goods or services or in the repayment of debts. Currency, consisting of dollar bills and coins, clearly fits this definition and is one type of money. When most people talk about money, they’re talking about currency (paper money and coins). If, for example, someone comes up to you and says, “Your money or your life,” you should quickly hand over all your currency rather than ask, “What exactly do you mean by ‘money’?”P5 To define money merely as currency is much too narrow for economists. Because checks are also accepted as payment for purchases, checking account deposits are considered money as well. An even broader definition of money is often needed, because other items such as savings deposits can, in effect, function as money if they can be quickly and easily converted into currency or checking account deposits. As you can see, no single, precise definition of money or the money supply is possible, even for economists.P6To complicate matters further, the word money is frequently used synonymously with wealth. When people say, “Joe is rich—he has an awful lot of money,”they probably mean that Joe not only has a lot of currency and a high balance in his checking account but also has stocks, bonds, four cars, three houses, and a yacht. Thus, while“currency”is too narrow a definition of money, this other popular usage is much tooP7broad. Economists make a distinction between money in the form of currency, demand deposits, and other items that are used to make purchases and wealth, the total collection of pieces of property that serve to store value. Wealth includes not only money but also other assets such as bonds, common stock, art, land, furniture, cars, and houses.2.Functions of MoneyP8Whether money is shells or rocks or gold or paper, it has three primary functions in any economy: as a medium of exchange, as a unit of account, and as a store of value. Of the three functions, its function as a medium of exchange is what distinguishes money from other assets such as stocks, bonds, and houses.2.1 Medium of ExchangeP9In almost all market transactions in our economy, money in the form of currency or checks is a medium of exchange; it is used to pay for goods and services. The use of money as a medium of exchange promotes economic efficiency by minimizing the time spent in exchanging goods and services. To see why, let’s look at a barter economy, one without money, in which goods and services are exchanged directly for other goods and services.P10Take the case of Ellen the Economics Professor, who can do just one thing well: give brilliant economics lectures. In a barter economy, if Ellen wants to eat, she must find a farmer who not only produces the food she likes but also wants to learn economics. As you might expect, this search will be difficult and time-consuming, and Ellen might spend more time looking for such an economics-hungry farmer than she will teaching. It is even possible that she will have to quit lecturing and go into farming herself. Even so, she may still starve to death.P11The time spent trying to exchange goods or services is called a transaction cost. In a barter economy, transaction costs are high because people have to satisfy a “double coincidence of wants”—they have to find someone who has a good or service they want and who also wants the good or service they have to offer.P12Let’s see what happens if we introduce money into Ellen the Economics Professor’s world. Ellen can teach anyone who is willing to pay money to hear her lecture. She can then go to any farmer (or his representative at the supermarket) and buy the food she needs with the money she has been paid. The problem of the double coincidence of wants is avoided, and Ellen saves a lot of time, which she may spend doing what she does best: teaching.P13As this example shows, money promotes economic efficiency by eliminating much of the time spent exchanging goods and services. It also promotes efficiency by allowing people to specialize in what they do best. Money is therefore essential in an economy: It is a lubricant that allows the economy to run more smoothly by lowering transaction costs, thereby encouraging specialization and division of labor.P14The need for money is so strong that almost every society beyond the most primitive invents it. For a commodity to function effectively as money, it has to meet several criteria: (1) It must be easily standardized, making it simple to ascertain its value; (2) it must be widely accepted; (3) it must be divisible, so that it is easy to “make change”; (4) it must be easy to carry; and (5) it must not deteriorate quickly. Objects that have satisfied these criteria have taken many unusual forms throughout human history, ranging from wampum (strings of beads) used by Native Americans; to tobacco and whiskey, used by the early American colonists; to cigarettes, used in prisoner-of-war camps during World War II. The diverse forms of money that have been developed over the years is as much a testament to the inventiveness of the human race as the development of tools and language.2.2 Unit of AccountP15The second role of money is to provide a unit of account; that is, it is used to measure value in the economy. We measure the value of goods and services in terms of money, just as we measure weight in terms of pounds or distance in terms of miles. P16 To see why this function is important, let’s look again at a barter economy, in which money does not perform this function. If the economy has only three goods—say, peaches, economics lectures, and movies—then we need to know only three prices to tell us how to exchange one for another: the price of peaches in terms of economics lectures (that is, how many economics lectures you have to pay for a peach), the price of peaches in terms of movies, and the price of economics lectures in terms of movies. If there were 10 goods, we would need to know 45 prices to exchange one good for another; with 100 goods, we would need 4,950 prices; and with 1,000 goods, 499,500 prices.P17 Imagine how hard it would be in a barter economy to shop at a supermarket with 1,000 different items on its shelves and be faced with deciding whether chicken or fish is a better buy if the price of a pound of chicken were quoted as 4 pounds of butter and the price of a pound of fish as 8 pounds of tomatoes. To make it possible to compare prices, the tag on each item would have to list up to 999 different prices, and the time spent reading them would result in very high transaction costs.P18 The solution to the problem is to introduce money into the economy and have all prices quoted in terms of units of that money, enabling us to quote the price of economics lectures, peaches, and movies in terms of, say, dollars. If there were only three goods in the economy, this would not be a great advantage over the barter system, because we would still need three prices to conduct transactions. But for 10 goods we would need only 10 prices; for 100 goods, 100 prices; and so on. At the 1,000-goods supermarket, now only 1,000 prices need to be looked at, not 499,500!P19 We can see that using money as a unit of account lowers transaction costs in an economy by reducing the number of prices that need to be considered. The benefits of this function of money grow as the economy becomes more complex.2.3 Store of ValueP20Money also functions as a store of value; it is a repository of purchasing power over time. A store of value is used to save purchasing power from the time income is received until the time it is spent. This function of money is useful, because most of us do not want to spend our income immediately upon receiving it, but rather prefer to wait until we have the time or the desire to shop.P21Money is not unique as a store of value; any asset—whether money, stocks, bonds, land, houses, art, or jewelry—can be used to store wealth. Many such assets have advantages over money as a store of value: They often pay the owner a higher interest rate than money, experience price appreciation, and deliver services such as providing a roof over one’s head. If these assets are a more desirable store of value than money, why do people hold money at all?P22The answer to this question relates to the important economic concept of liquidity, the relative ease and speed with which an asset can be converted into a medium of exchange. Liquidity is highly desirable. Money is the most liquid asset of all becauseit is the medium of exchange; it does not have to be converted into anything else to make purchases. Other assets involve transaction costs when they are converted into money. When you sell your house, for example, you have to pay a brokerage commission (usually 4–6% of the sales price), and if you need cash immediately to pay some pressing bills, you might have to settle for a lower price if you want to sell the house quickly. Because money is the most liquid asset, people are willing to hold it even if it is not the most attractive store of value.P23How good a store of value money is depends on the price level. A doubling of all prices, for example, means that the value of money has dropped by half; conversely, a halving of all prices means that the value of money has doubled. During inflation, when the price level is increasing rapidly, money loses value rapidly, and people will be more reluctant to hold their wealth in this form. This is especially true during periods of extreme inflation, known as hyperinflation, in which the inflation rate exceeds 50% per month.P24 Hyperinflation occurred in Germany after World War I, with inflation rates sometimes exceeding 1,000% per month. By the end of the hyperinflation in 1923, the price level had risen to more than 30 billion times what it had been just two years before. The quantity of money needed to purchase even the most basic items became excessive. There are stories, for example, that near the end of the hyperinflation, a wheelbarrow of cash would be required to pay for a loaf of bread. Money was losing its value so rapidly that workers were paid and given time off on several occasions during the day to spend their wages before the money became worthless. No one wanted to hold on to money, so the use of money to carry out transactions declined and barter became more and more dominant. Transaction costs skyrocketed, and, as we would expect, output in the economy fell sharply.3.Evolution of the Payments SystemP25We can obtain a better picture of the functions of money and the forms it has taken over time by looking at the evolution of the payments system, the method of conducting transactions in the economy. The payments system has been evolving over centuries, and with it the form of money. At one point, precious metals such as gold were used as the principal means of payment and were the main form of money. Later, paper assets such as checks and currency began to be used in the payments system and viewed as money. Where the payments system is heading has an important bearing on how money will be defined in the future.3.1 Commodity MoneyP26To obtain perspective on where the payments system is heading, it’s worth exploring how it has evolved. For any object to function as money, it must be universally acceptable; everyone must be willing to take it in payment for goods and services. An object that clearly has value to everyone is a likely candidate to serve as money, and a natural choice is a precious metal such as gold or silver. Money made upof precious metals or another valuable commodity is called commodity money, and from ancient times until several hundred years ago, commodity money functioned as the medium of exchange in all but the most primitive societies. The problem with a payments system based exclusively on precious metals is that such a form of money is very heavy and is hard to transport from one place to another. Imagine the holes you’d wear in your pockets if you had to buy things only with coins! Indeed, for large purchases such as a house, you’d have to rent a truck to transport the money payment.3.2 Fiat MoneyP27The next development in the payments system was paper currency (pieces of paper that function as a medium of exchange). Initially, paper currency carried a guarantee that it was convertible into coins or into a fixed quantity of precious metal. However, currency has evolved into fiat money, paper currency decreed by governments as legal tender (meaning that legally it must be accepted as payment for debts) but not convertible into coins or precious metal. Paper currency has the advantage of being much lighter than coins or precious metal, but it can be accepted as a medium of exchange only if there is some trust in the authorities who issue it and if printing has reached a sufficiently advanced stage that counterfeiting is extremely difficult. Because paper currency has evolved into a legal arrangement, countries can change the currency they use at will. Indeed, this is what many European countries did when they abandoned their currencies for the euro in 2002.P28Major drawbacks of paper currency and coins are that they are easily stolen and can be expensive to transport in large amounts because of their bulk. To combat this problem, another step in the evolution of the payments system occurred with the development of modern banking: the invention of checks.3.3 ChecksP29 A check is an instruction from you to your bank to transfer money from your account to someone else’s account when she deposits the check. Checks allow transactions to take place without the need to carry around large amounts of currency. The introduction of checks was a major innovation that improved the efficiency of the payments system. Frequently, payments made back and forth cancel each other; without checks, this would involve the movement of a lot of currency. With checks, payments that cancel each other can be settled by canceling the checks, and no currency need be moved. The use of checks thus reduces the transportation costs associated with the payments system and improves economic efficiency. Another advantage of checks is that they can be written for any amount up to the balance in the account, making transactions for large amounts much easier. Checks are also advantageous in that loss from theft is greatly reduced and because they provide convenient receipts for purchases.P30 Two problems arise, however, with a payments system based on checks. First, it takes time to get checks from one place to another, a particularly serious problem ifyou are paying someone in a different location who needs to be paid quickly. In addition, if you have a checking account, you know that it often takes several business days before a bank will allow you to make use of the funds from a check you have deposited. If your need for cash is urgent, this feature of paying by check can be frustrating. Second, the paper shuffling required to process checks is costly; currently, the cost of processing all checks written in the United States is estimated at over $10 billion per year.3.4 Electronic PaymentP31The development of inexpensive computers and the spread of the Internet now make it cheap to pay bills electronically. In the past, you had to pay bills by mailing a check, but now banks provide websites at which you just log on, make a few clicks, and thereby transmit your payment electronically. Not only do you save the cost of the stamp, but paying bills becomes (almost) a pleasure, requiring little effort. Electronic payment systems provided by banks now even spare you the step of logging on to pay the bill. Instead, recurring bills can be automatically deducted from your bank account. Estimated cost savings when a bill is paid electronically rather than by a check exceed one dollar per transaction. Electronic payment is thus becoming far more common in the United States.3.5 E-MoneyP32Electronic payments technology can substitute not only for checks but also for cash, in the form of electronic money (or e-money)—money that exists only in electronic form. The first form of e-money was the debit card. Debit cards, which look like credit cards, enable consumers to purchase goods and services by electronically transferring funds directly from their bank accounts to a merchant’s account. Debit cards are used in many of the same places that accept credit cards and are now often becoming faster to use than cash. At most supermarkets, for example, you can swipe your debit card through the card reader at the checkout station, press a button, and the amount of your purchases is deducted from your bank account. Most banks and companies such as Visa and Master-Card issue debit cards, and your ATM card typically can function as a debit card.P33A more advanced form of e-money is the stored-value card. The simplest form of stored-value card is purchased for a preset dollar amount that the consumer pays up front, like a prepaid phone card. The more sophisticated stored-value card is known as a smart card. It contains a computer chip that allows it to be loaded with digital cash from the owner’s bank account whenever needed. In Asian countries, such as Japan and Korea, cell phones now have a smart card feature that raises the expression “pay by phone” to a new level. Smart cards can be loaded from ATM machines, personal computers with a smart card reader, or specially equipped telephones.P34A third form of electronic money is often referred to as e-cash, which is used on the Internet to purchase goods or services. A consumer gets e-cash by setting up anaccount with a bank that has links to the Internet and then has the e-cash transferred to her PC. When she wants to buy something wiThe-cash, she surfs to a store on the Web and clicks the “buy”option for a particular item, whereupon the e-cash is automatically transferred from her computer to the merchant’s computer. The merchant can then have the funds transferred from the consumer’s bank account to his before the goods are shipped.P35Given the convenience of e-money, you might think that we would move quickly to a cashless society in which all payments are made electronically. However, this hasn’t happened.4. Measuring MoneyP36The definition of money as anything that is generally accepted in payment for goods and services tells us that money is defined by people’s behavior. What makes an asset money is that people believe it will be accepted by others when making payment. As we have seen, many different assets have performed this role over the centuries, ranging from gold to paper currency to checking accounts. For that reason, this behavioral definition does not tell us which assets in our economy should be considered money. To measure money, we need a precise definition that tells us exactly which assets should be included.The Federal Reserve’s Monetary AggregatesP37The Federal Reserve System (the Fed), the central banking authority responsible for monetary policy in the United States, has conducted many studies on how to measure money. The problem of measuring money has recently become especially crucial because extensive financial innovation has produced new types of assets that might properly belong in a measure of money. Since 1980, the Fed has modified its measures of money several times and has settled on the following measures of the money supply, which are also referred to as monetary aggregates (see Table 1).P38The narrowest measure of money that the Fed reports is M1, which includes the most liquid assets: currency, checking account deposits, and traveler’s checks. The components of M1 are shown in Table 1. The currency component of M1 includes only paper money and coins in the hands of the nonbank public and does not include cash held in ATMs or bank vaults. Surprisingly, more than $3,000 cash is in circulation for each person in the United States. The traveler’s checks component of M1 includes only traveler’s checks not issued by banks. The demand deposits component includes business checking accounts that do not pay interest, as well as traveler’s checks issued by banks. The other checkable deposits item includes all other checkable deposits, particularly interest-bearing checking accounts held by households. These assets are clearly money because they can be used directly as a medium of exchange.P39Until the mid-1970s, only commercial banks were permitted to establish checkingaccounts, and they were not allowed to pay interest on them. With the financial innovation that has occurred, regulations have changed so that other types of banks, such as savings and loan associations, mutual savings banks, and credit unions, can also offer checking accounts. In addition, banking institutions can offer other checkable deposits, such as NOW (negotiated order of withdrawal) accounts and ATS (automatic transfer from savings) accounts, which do pay interest on their balances.P40 The M2 monetary aggregate adds to M1 other assets that are not quite as liquid as those included in M1: assets that have check-writing features (money market deposit accounts and money market mutual fund shares) and other assets (savings deposits and small-denomination time deposits) that can be turned into cash quickly at very little cost. Small-denomination time deposits are certificates of deposit with a denomination of less than $100,000 that can be redeemed only at a fixed maturity date without a penalty. Savings deposits are nontransaction deposits that can be added to or taken out at any time. Money market deposit accounts are similar to money market mutual funds, but are issued by banks. The money market mutual fund shares are retail accounts on which households can write checks.Table 1[Frederic S. Mishkin. The Economics of Money, Banking, and Financial Markets, 10The d., Chapter 3 What Is Money? 2013, pp.52-59]Listening Signpost words/phrases to listen forWhether in a lecture or a speech, there is much information and it’s impossible (nor is it necessary) for an English-as-a-foreign-language (EFL) student to understand every single word and phrase used by the lecturer or the speaker. Being able to listen for and catch certain signal words and phrases may help an EFL student to better get the big picture and the key points of the lecture or speech.There are two types of signal words and phrases often used by a speaker to either summarize the point(s) already elaborated or wake up and attract (or re-attract) the attention of the audience. These signal words and phrase include, but not limited to, so, therefore, but you know what, let me show you something, etc. Once these words and phrases are used, the audiences will know what comes next will be a brief summary or repetition and clarification of some previously mentioned point(s), or something important such as a new point of view, or a piece of evidence, or a keen observation, etc.Task 1 Watch the video titled Hidden Secrets of Money, from 9:00 minutes to 21:00 minutes. Listen for and write down the signpost words and phrases you have got and appreciate their function in the talk.Task 2 Below is a summary of the designated part of the video on money. Please fill in the missing words from the video.The American dollar is viewed as unreliable as __________(1) of value because it has lost much of its purchasing power since its creation as __________(2) money in 1913. It’s not backed by gold like it used to be in the past. Actually it becomes a __________(3) check against nothing. Instead of maintaining value, the dollar is said to be a __________(4), and __________(5) away people’s wealth, their purchasing power. On the other hand, __________(6) is praised as the _________(7) form of gold because it is divisible, permanent, and cannot be manipulated.Inflation is the result of __________(8) currency supply. With the __________(9) system replaced with a single currency, and without the constraint of gold, every government is racing to increase their ___________(10) currency by printing money to allow for deficit spending and bailouts of troubled institutions. As a result, inflation runs out of control and leads to revolutions in certain parts of the world.ReadingTask 1Read the text and choose the best answer from the choices for the following questions.1.The example of “Your money or your life” in para.? is meant toA.warn readers of the danger of taking currency while going out.B.point out a setback of coins and paper money.C.demonstrate how people understand money in daily life.D.suggest that economist would respond differently from common people in such a situation.2.Which of the following is NOT a purpose of the example of “Joe is rich--he has an awful lot of money” in para. ?? toA.show that people sometimes confuse money with wealth.B.disapprove a certain definition of money.C.give the word richness a new definition.D.clarify the differences between money and wealth.3.The author mentions the barter economy in para.?? mainly toA.prove that ancient people aren’t as smart as people today.B.explain the necessity of introducing a better form of exchange.C.indicate that barter should have never been used by any society.D.imply that the more specialized people are, the cheaper products will be.4.Which of the following statements about money as a store of value is the LEAST likely to be true ?A.Money is the most attractive form of store of value.B.A person who is bullish on gold may not want to hold money as a store of value.C.A person expecting deflation may want to hold on to his/her money.D.Rapid price increases may lead people to lose confidence in money as a store of value.5.In Where the payments system is heading has an important bearing on how money will be defined in the future in para.25, the word “bearing” is closest in meaning to which of the following words?A.enduranceB.supportC.mannerD.interconnection6.Which of the following is NOT one of the prerequisites to fiat money?A.advanced printing technologyB.confidence in the issuing authoritiesC.Convertibility into precious metalsernment order7.The first form of e-money isA.credit cardsB.debit cardsC.stored-valued cards。

金融英语 chapter 1 money

Course Structure

• Chapter 1 Money, the Functions of Money and the Financial System • Chapter 2 The Banking system • Chapter 3 Interest Rate and Interest Rate Policies • Chapter 4 Money Market

• 铸币税(Seigniorage) • 也称为“货币税”。发行货币的组织或 国家的政府可以不需任何补偿地用纸制 货币向自己的居民换取实际经济资源, 从中攫取发行货币所产生的特定收益。 这部分由货币发行主体垄断性地享受 “通货币面价值超出生产成本”的收益, 就被定义为“铸币税”。Professional源自TermsQuestion

• When you buy a pair of jeans or a CD, for example, you never wonder whether the merchant will accept the bills and coins in your wallet as payment. • But suppose money didn't exist. How would you pay for the things you want to buy?

• 45.fund obligation基金负担

• 基金负担或称基金总数是指当时发行在 外的基金的总量

Professional Terms

• 58.monetary ease银根松动 • 银根monetary situation 指金融市场上的 资金供应。因中国1935年法币改革以前 曾采用银本位制,市场交易一般都用白 银,所以习惯上称资金供应为银根。 • 银根有紧松之分,判断依据是资金供需 状况。如果市场上资金供不应求,称为 “银根紧俏”或“银根紧”;市场上资 金供过于求,称为“银根松疲”或“银 根松”

(完整版)金融英语名词解释

Chapter 1The international money market trades short-term claims with an original maturity of one year or less.The international capital market trades capital market instruments with an original maturity greater than one year.The foreign exchange market is the one where foreign currencies are bought and sold in the course of trading goods, services, and financial claims among countries. Chapter 21.Money:Economists define money (also referred to as the money supply) asanything that is generally accepted in payment for goods or services or in the repayment of debts.2.Currency:One type of money:dollar bills and coins3.Medium of Exchange:In almost all market transactions in an economy, money inthe form of currency or checks is a medium of exchange; it is used to pay for goods and services.4.Transaction Cost:The time spent trying to exchange goods and services is called atransaction cost.5.Store of Value:Money also functions as a store of value; it is a repository ofpurchasing power over time. A store of value is used to save purchasing power from the time income is received until the time it is spent.6.Liquidity:Liquidity is a measure of the ease with which an asset can be turnedinto a means of payment, namely money.7.Inflation:Inflation is a sustained rise in the general price level—that is, the priceof everything goes up more or less at the same time.8.Money aggregates: We have drawn the line in a number of different places andcomputed several measures of money, called the money aggregates: M1, M2, and M3.M1=currencycurrency and various deposit accounts on which people can write checks +Traveler’s checks+Demand deposits+Other checkable depositsM2=M1M2 equals all of M1 plus assets that cannot be used directly as a means of payment and are difficult to turn into currency quickly+Small-denomination time deposits+Savings deposits and money market deposit accounts+Money market mutual fund shares (non-institutional)M3=M2M3 adds to M2 a number of other assets that are important to large institutions but not to individuals.+Large-denomination time deposits+Money market mutual fund shares (institutional)+Repurchase agreements+EurodollarsChapter 31. Depository institutions:Depository institutions are financial institutions that accept deposits from savers and make loans to borrowers .W e use the term “banks” as an alternative.2.bank:A bank is a financial institution where you can deposit your money.mercial Banks:A commercial bank is an institution that accepts deposits anduses the proceeds to make consumer, commercial, and mortgage loans. Originally established to meet the needs of businesses, many of these banks now serve individual customers as well4.holding company:A holding company is a corporation that owns a group of otherfirms.munity Banks:Small banks—those with assets of less than $1 billion—thatconcentrate on serving consumers and small businesses.These are the banks that take deposits from people in the local area and lend them back to local businesses and consumers.6.Regional and Super-Regional Banks:larger than community banks and muchless local. Besides consumer and residential loans, these banks also make commercial and industrial loans.7.Money Center Banks:do not rely primarily on deposit financing. These banks relyinstead on borrowing for their funding8.Savings Institutions:Savings institutions, which are sometimes referred to as“thrift institutions” or “thrifts”, are financial intermediaries that were established to serve households and individuals.9.Credit Union:Credit unions (CUs) are nonprofit organizationsThey are composed of members with a common bond, such as an affiliation with a particular labor union, church, university, or even residential area.Chapter 4Insurance Companies: Insurance companies are intermediaries whose primary function is to allow households and businesses to shed specific risks by buying contracts called insurance policies that pay cash compensation if certain specified events occur.1.Insurance:Insurance is a financial arrangement that redistributes the costs ofunexpected losses.2.Insurance System: An insurance system accomplishes the redistribution of thecost of losses by collecting a premium payment from every participant in the system.Marine Insurance —The large majority of ship owners resort to marine insurance for the protection of their ships, freight and other interests against marine perils.Life Insurance—Life insurance pays a stated amount of money on the death of the insured individualFire Insurance —Fire insurance covers losses due to fireProperty Insurance —property insurance covers damage to the properties of the assured subject to an agreed limit.Motor Insurance—a legally required insurance covering the driver of a car for potential damages to other road users or their vehicles from accidents caused through their fault.Accident Insurance—this type of insurance provides compensation in the event of an accident causing death or injury.Liability Insurance —this type of insurance is to protect the policyholder who is sued for damages arising from negligence.Property and casualty insurance--- Policies that cover accidents, theft, or fire are called property and casualty insurance.Health and disability insurance--- Policies that cover sickness or the inability to work are called health and disability insuranceLife insurance---Policies that cover death are called life insurance3.Premiums: Payments made to insurance companies for the insurance they provideare called premiums.4.Reinsurance: Insurance companies commonly obtain reinsurance, whicheffectively allocates a portion of their return and risk to other insurance companies.(1)Pension Funds: Like an insurance company, a pension fund offers people the ability to make premium payments today in exchange for promised payments under certain future circumstances.(2)Pension plan: A pension plan is an asset pool that accumulates over an individual’s working years and is paid out during the nonworking years.5.Installment Loans: Consumer finance firms provide small installment loans toindividual consumers.This kind of consumer credit allows people without sufficient savings to purchase appliances such as television sets, washing machines, and microwave ovens6.Mutual Funds:A mutual fund is a portfolio of stocks, bonds, or other assetspurchased in the name of a group of investors and managed by a professional investment company or other financial institution.7.Open-end mutual funds: Open-end mutual funds are willing to repurchase theshares they sell from investors at any time.8.Closed end: Closed-end mutual funds do not repurchase the shares they sell.9.Investment Bank:It is a financial institution that helps corporations raise funds.10.Securities Brokers:Securities brokers and dealers conduct trading in secondarymarkets.11.Brokers: Brokers are pure intermediaries who act as agents for investors in thepurchase or sale of securities.12.Securities Dealers: Security dealers link buyers and sellers by standing ready tobuy and sell securities at given prices.anized Exchange: An organized exchange actually functions as a hybrid of anauction market (in which buyers and seller trade with each other in a central location14.dealer market: A dealer market (in which dealers make the market by buying andselling securities at given prices)Chapter 51.Interest rate:The willingness to postpone purchases into the future is a function ofthe reward.2.Future Values: future value is the value on some future date of an investmentmade today.3.Present Value:Present value is the value in the present of a payment that ispromised to be made in the future.4.Nominal Interest Rates: interest rate that is adjusted for expected changes in theprice level so that it more accurately reflects the true cost of borrowing.补:The interest rate before taking inflation into account. The nominal interest rate is the rate quoted in loan and deposit agreements. The equation that links nominal and real interest rates is:(1 + nominal rate) = (1 + real interest rate) (1 + inflation rate).It can be approximated as nominal rate = real interest rate + inflation rate.5.Real Interest Rates: (补)An interest rate that has been adjusted to remove theeffects of inflation to reflect the real cost of funds to the borrower, and the real yield to the lender. The real interest rate of an investment is calculated as the amount by which the nominal interest rate is higher than the inflation rate.Real Interest Rate = Nominal Interest Rate - Inflation (Expected or Actual) Chapter 6Money Market:Money market is the market for short-term creditMoney market provides short term debt financing and investment.1.Treasury Bills:A short-term debt obligation backed by the U.S. government witha maturity of less than one year. T-bills are sold in denominations of $1,000 up toa maximum purchase of $5 million and commonly have maturities of one month(four weeks), three months (13 weeks) or six months (26 weeks).2.Negotiable Certificates of Deposit (CDs):The term CD stands for Certificate ofDeposit. A CD is simply a short- to medium-length investment. Most CDs have a maturity of 1-12 months.mercial Paper:Commercial paper securities are unsecured promissory notes,issued by corporations that mature in no more than 270 days.4.Banker’s Acceptance:Banker’s acceptances are money market instrumentscreated in the course of financing international trade.An acceptance is a financial instrument designed to shift the risk of international trade to a third party willing to take on that risk for a known cost.5.Repurchase Agreements:Repurchase agreements (repos) are short-termagreements in which the seller sells a government security to a buyer and simultaneously agrees to buy the government security back on a later date at a higher price.6.Money Market Mutual Funds:MMMFs are funds that aggregate money from agroup of small investors and invest it in money market instruments.7.open-ended fund:An open-ended fund is one that invests in securities and sellsdirect claims on the securities to investors.Chapter 71.Central Bank:The central bank is the financial institution designed to regulateand control the money supply of a nation, with the goal of fostering economic growth without inflation.2.expansionary policy:lower interest rates, raises both growth and inflation over theshort run3.restrictive policy:Higher interest rates, reduces both growth and inflation.4.Dollar hegemony: dollar hegemony means that managing the US dollar thereforenot only affects the US economy but all economies.Chapter 81.Monetary policy:Defined as the use of various tools by the central bank tocontrol the availability of loanable funds in an effort to achieve national economic goals, such as full employment and reasonable price stability.2.Reserve Requirements: Reserve requirements are a percentage of depositoryinstitutions' demand deposit liabilities that must be kept on deposit at the central bank as a requirement of banking regulations.3.Discount Rate:Discount rate is the interest rate charged by a central bank on loansto commercial banks.4.Open Market Operations:Open market operations, the central ban k’s purchase orsale of bonds in the open marketOpen market purchases:Open market purchases expand reserves and the monetary base, thereby raising the money supply and lowering short-term interest rates.Open market sales:Open market sales shrink reserves and the monetary base, lowering the money supply and raising short-term interest rates.Chapter 9Capital Market:The capital market is the market in which long-term debt (generally those with original maturity of one year or greater) and equity instruments are traded.1.The primary market:The primary market is where new issues of stocks and bondsare introduced. Investment funds, corporations, and individual investors can purchase all securities offered in the primary market.anized Securities Exchanges:Exchange rules govern trading to ensure theefficient and legal operation of the exchange, and the exchange’s board constantly reviews these rules to ensure that they result in competitive trading.3.Over-the-Counter Markets:Securities that are not listed on one of the exchangestrade in the over-the-counter market. This market is not organized in the sense of having a building where trading takes place.4.NSADAQ:shows bid and asked prices for thousands of OTC-traded securities onvideo screens hooked up to a central computer system.5.Bonds:Bonds are securities that represent a debt owed by the issuer to theinvestorMunicipal bonds:These are issued by state and local governments or their agencies to pay for public improvements, reducing debt, or other purposesCorporate bonds:These are issued by corporations that want to raise money for their business venture, ranging from balancing their cash flow to buying new equipment, building new facilities, or spending on new research.Government bonds:Issued by the Federal government or one of the its agencies.6.Treasuries: Treasuries bills, notes and bonds are collectively called “Treasuries”.Treasury Bills (T-bills): These are short-term securities that mature in a year or less. You buy them at a discount price and at the end of the term, you are repaid the full price.Treasury Notes: Theses are issued for the intermediate term, such as 2 years up to10 years. Expect to earn a little higher interest rate than what you could get from aT-bill. Interest is paid every 6 months.Treasury Bonds: Theses are issued for the long term, generally from 10 years to30 years. Expect to earn a higher interest rate than what you could get from aT-note. Interest is paid every 6 months.Savings Bonds: They are government bonds designed especially for individual investors. As such, they can generally only be redeemed by their original owner, except in limited circumstances.7.Primary market:bonds sold for the first time.Secondary market: the resale of bonds some time after their initial offering.8.Face Value: The face value, or par value, of a bond is the value of the bond atmaturity, the date when the loan is paid off. A common face value is $1,000 per bond.9.Coupon Rate: A bond’s coupon rate refers to the amount of interest that will bepaid based on the face value of the bond.10.Yield:The yield is the discount rate or interest rate that an investor wants frominvesting in a bond.11.Stocks:A share of stock in a firm represents ownershipCommon stock:makes up the majority of stocks. As a common stock holder, you have a right to claim dividends and get to have one vote per share when electing board of directors.Preferred stock:does not usually include voting rights and pays a specified dividend, because of which the stock price does not rise and fall along with the company profits.Bull Market: indicates the constant upward movement of the stock market.Bear Market: indicates the continuous downward movement of the stock market.12.Mortgages: Mortgages are loans to households or firms to purchase housing, land,or other real structure, where the structure or land itself serves as collateral for the loans.13.Discount points: Discount points are interest payments made at the beginning of aloanChapter 10Financial derivatives:Financial derivatives are financial contracts, or financial instruments, whose values are derived from the value of something else ( known as the underlying).1.Exchange-traded derivatives (ETD): are those derivatives products that are tradedvia specialized derivatives exchanges or other exchanges.Over-the counter (OTC) derivatives:They are contracts that are traded ( and privately negotiated) directly between two parties, without going through an exchange or other intermediary.2.Forward: A forward, or forward contract, is an agreement between a buyer and aseller to exchange a commodity or financial instrument for a specified amount of cash on a prearranged future date.3.Future: a future, or futures contract, is a forward contract that has beenstandardized and sold through an organized exchange.Hedger: tries to minimize risk by buying or selling now in an effort to avoid risking or declining futures pricesSpeculator: try to profit from the risks by buying or selling now in anticipation of rising or declining future prices4.Initial margin: represents a good faith deposit that serves to cover losses if pricesmove against the trader.5.Options:Options are contracts that give the purchaser the right to buy or sell theunderlying financial instrument at a specified price within a specific period of time(1)There are two basic options: puts and calls:A call gives the holder the right to buy an asset at a certain price within a specificperiod of timeA put option gives the holder the right to sell an asset at a certain price within aspecific period of time.(2)There are two types of option contracts:American options can be exercised at any time up to the expiration date of the contract,European options can be exercised only on the expiration date(3)How to Read An Option TableColumn 1: Strike price: This is the stated price per share for which an underlying stock may be purchased (for a call) or sold ( for a put) upon the exercise of the option contract. Option strike prices typically move by incrementsof $2.50 or $5 (even though in the above example it moves in $2. increments).Column 2: Expiry date: This shows the termination date of an option contract.Remember that US listed options expire on the third Friday of the expiry month.Column 3: Call or Put: This column refers to whether the option is a call or put.Column 4: V olume: This indicates the total number of options contracts traded for the day. This volume of all contracts is listed at the bottom of each table.Column 5: Bid: This indicates the price someone is willing to pay for the options contract.Column 6: Ask:This indicates the price at which someone is willing to sell an options contract.Column 7: Open Interest: Open interest is the number of options contracts that are open; these are contracts that have neither expired nor been exercised.6.Swaps: A swap is an agreement between two parties to exchange sequences ofcash flows for a set period of time.Interest Rate Swap:Interest rate swaps involve the exchange of one set of interest payments for another set of interest payments, all denominated in the same currency.Currency Swap:It involves exchanging principal and fixed interest payments on a loan in one currency for principal and fixed interest payments on a similar loan in another currency.Chapter 11foreign exchange rates:The prices of foreign currencies expressed in terms of other currencies are called foreign exchange rates.1.Spot Transaction:A spot transaction is a straightforward (or “outright”) exchange of one currency for another. (This trade represents a “direct exchange” between two currencies and has the shortest time frame2.Outright Forwards:An outright forward transaction, like a spot transaction, is a straightforward single purchase/sale of one currency for another3.FX Swaps:A swap is an agreement between two parties to exchange payments based onidentical notional principle. In a swap, two parties exchange currencies for a certain length of time and agree to reverse the transaction at a later dateIn the FX swap market, one currency is swapped for another for a period of time, and then swapped back, creating an exchange and re-exchange.short-dated swap:both dates are less than one month from the deal dateforward swap:one or both dates are one month or more from the deal date5.Currency Swaps:In a typical currency swap, counterparties will(1)exchange equal initial principal amounts of two currencies at the spot exchangerate,(2)exchange a stream of fixed or floating interest rate payments in their swappedcurrencies for the agreed period of the swap, and then(3)re-exchange the principal amount at maturity at the initial spot exchange rate.6.Over-the-Counter Currency Options:A foreign exchange or currency option contract gives the buyer the right, but notthe obligation, to buy (or sell) a specified amount of one currency for another at a specified price on (in some cases, on or before) a specified date.6.Exchange-Traded FuturesIn the U.S. exchanges, a foreign exchange futures contract is an agreement between two parties to buy/sell a particular (non-U.S. dollar) currency at a particular price on a particular future date, as specified in a standardized contract common to all participants in that currency futures exchange.7.Exchange-Traded Currency OptionsExchange-traded currency options, like exchange-traded futures, utilize standardized contracts—with respect to the amount of the underlying currency, the exercise price, and the expiration date.The option buyer—who has no further financial obligation after he has paid the premium—is not required to make margin payments.The option writer—who has all of the financial risk—is required to put up initial margin and to make additional (maintenance) margin payments if the market price moves adversely to his position.Chapter 12Balance of Payments:A country’s balance of payments is commonly defined as the record of transactions between its residents and foreign residents over a specified period.A debit entry records a transaction that results in a domestic resident making apayment abroad. A debit entry has a negative value in the balance-of-payments account.A credit entry records a transaction that results in a domestic resident receiving apayment from abroad. A credit entry has a positive value in the balance-of-payment account.1.The Current Account:The current account measures the flow of goods, services,and income across national borders.(1)Goods:The goods category includes imports and exports of tangible goods such as cars, computers, clothes, televisions, etc.If a country’s imports more than it exports in this category, then it is said to have a trade deficit.If a country’s exports more than imports it in this category, then it is said to have a trade surplus.(2)Services:The services category includes flows of payment in exchange for services countries provide to each other: transportation, insurance, banking, tourism, etc.(3)income: The income category measures cross-border compensation of employees.(4)Transfer Payments:Transfer payments include unilateral gifts or payments from private citizens and government of a country to people living abroad or vice versa.3.The Capital and Financial Account:The capital and financial account includes a variety of sub-accounts all dealing with purchases and sales of financial assets or real estate (stocks, bonds, land, buildings, businesses, etc.).4.The Official Settlements Balance:The official settlements balance measures the transactions of financial assets and deposits by official government agencies.5.Deficits and Surpluses in the Balance of Payments:The so-called balance-of-payments deficit or surplus is something other than the overall balance of payments.A balance-of-payments deficit refers to a situation in which the official settlements balance is positive.A balance-of-payments surplus:A situation where the sum of the debits and credits in the current and the capital and financial account is positive means that private payments received from foreigners exceed private payments made to foreigners. In this case, the official settlements balance is negative, and there is a balance-of-payments surplus.A balance-of-payments equilibrium refers to a situation where the sum of the debits and credits in the current account and capital and financial account is zero, and thus the official settlements balance is zero.Chapter 131.Letters of Credit A letter of credit is an internat ional bank’s future promise to payfor goods stored overseas or for goods shipped between two countries。

新编金融英语教程 Chapter1 Money

• depository institutions

the U.S. Treasury 美国财政部

• fiat money

unit of account计量单位

• financial claim

• medium of exchange

• monetary aggregate

• money market deposit accounts (MMDAs)

M3

M3 consists of everything in M2 plus some illiquid assets. The assets include large deposits, repurchase agreements, European dollars, institutional money, and market mutual funds.

1.3 Language Notes

III. Sentences

1. It occurred because gold and silver merchants or banks would issue receipts to their depositors – redeemable for the commodity money deposited. 2. Economists make a distinction between money in the form of currency, demand deposits, and other items that are used to make purchases and wealth, the total collection of property to store value. 3. They consist of demand deposits, which are non-interest-earning checking accounts issued by banks, and other checkable deposits, which are interest-earning checking accounts issued by some depository institutions. 4. Even though these other assets are not used to make transactions, they are all highly liquid, so they are often referred to as near monies. 5.In other words, in a barter system, the exchange can take place only if there is a double coincidence of wants between two transacting parties.

金融英语第一章答案

Chapter1Ⅰ.1. Money and risk and how they are interrelated.2. Recently a number of websites have been created to give consumers basic price comparisons for services.3. Allows a company to determine how much credit it can extend to customers before it begins to have liquidity problems.4. refer to money used by entrepreneurs and businesses to buy what they need to make their products or provide their services or to that sector of the economy based on its operation, i.e., retail, corporate, investment banking.5. A new discipline that uses mathematical and statistical methodology to understand behavioral biases in conjunction with valuation.6. An area of finance dealing with the financial decisions corporations make and the tools and analysis used to make these decisions.7. A main branch of applied mathematics concerned with the financial markets.8. The application of the principles of finance to the monetary decisions of an individual or family unit.Ⅱ.1.maximize risks2. mathematics statistics3. money offering4. determine liquidity5. aggregates accepts6. economics behavioralⅢ.translate the following sentences into English.1.The commercial management is the important aspects of the business management,Do not have the appropriate financial plan, the enterprise is not likely to be successful.2. Financial institutions is the basic aim of the public welcome by the financial assets into they can accept financial assets.3. Enterprise management is risky, so financial manager must evaluate the risks and management.4. Investment decision first refers to the investment opportunity, often referring to capital investment projects.5. Cash budget is often used to assess whether is the enterprise have enough cash to maintain the daily operation of the enterprise operation and if there is too much cash surplus.6. According to the view of finance, capital is the enterprise to the purchase of goods to produce other goods or provide services of currencyⅣ. Translate the following sentences into chinese.1.现金预算非常重要,特别是为小型企业,因为它允许公司确定多少信用可以向客户开始之前就有流动性问题。

金融英语Lecture 1 Money资料

金融英语L e c t u r e1M o n e yMoneyIf you can actually count your money, then you are not really a rich man.——American oil billionaire J. Paul GettyWhat is money?Economists define money as anything that is generally accepted in payment for goods or services or in the repayment of debts.Types of moneyA. Commodity moneyB. Convertible paper moneyC. Fiat money(or fiat currency):Usually paper money, is a type of currency whose only value is that a government made a fiat that the money is a legal method of exchange. Unlike commodity money or representative money it is not based in another commodity such as gold or silver and is not covered by a special reserve.D. Private debt moneyE. Electronic moneyPrivate debt moneyA loan that the borrower promises to repay in currency on demand. E.g. IOU the checkable deposit at commercial banks and other financial institutions.Commercial notes(商业票据):Short-term, unsecured, discounted, and negotiable notes sold by one company to another in order to satisfy immediate cash needs.Include: promissory note (期票,拮据) draft (汇票) check and so on. Electronic money: Electronic Check, Internet Payment System, Credit Card ServiceWhat does money do?A. Medium of ExchangeIn almost all market transactions in our economy, money in the form of currency or checks is a medium of exchange; it is used to pay for goods and services. The use of money as a medium of exchange promotes economic efficiency by eliminating much of the time spent in exchanging goods and services.Terms: Transaction cost, Time value of moneyB. Unit of AccountThe second role of money is to provide a unit of account; that is, it is used to measure value in the economy. We measure the value of goods and services in terms of money, just as we measure weight in terms of pounds or distance in terms of miles.Note: Fiat money has not only no particular value in use; it doesn't even really have a value in exchange except that which is decreed that it would have.Terms: Good money, Bad moneyC. Store of ValueMoney also functions as a store of value: it is a repository of purchasing power over time. It is an asset. It 's something that we can use to store value away to be retrieved at a later point in time. So we can not consume today, we can hold money instead - and transfer that consumption power to some point in the future.Term: Hard currencyMeasuring Monetary Aggregates1. Measure as “money” only those assets that are most liquid, hence that function best as a medium of exchange.2. Include all financial assets in the measure of money, but weight them in proportion to their liquidity.1. M1 = Most Narrow Measure (Most Liquid)M1 = currency + traveler’s checks + demand deposits + other checkable deposits2. M2 = M1 + Less Liquid AssetsM2 = M1 + small denomination time deposits + savings deposits + money market deposit accounts + money market mutual fund shares3. M3 = M2 + Less Liquid AssetsMoney supplyThe revenue raised through the printing of money. When thegovernment prints money to finance expenditure, it increases the money supply. The increase in the money supply, in turn, causes inflation. Printing money to raise revenue is like imposing an inflation tax.To expand the money supply:The Federal Reserve buys Treasury Bonds and pays for them with new money.To reduce the money supply:The Federal Reserve sells Treasury Bonds and receives the existing dollars and then destroys them.InflationInflation is an increase in the average level of prices, and a price is the rate at which money is exchanged for a good or service.Here is a great illustration of the power of inflation:In 1970, the New York Times cost 15 cents, the median price of a single-family home was $23,400, and the average wage in manufacturing was $3.36 per hour. In 2008, the Times cost $1.50, the price of a home was $183,300, and the average wage was $19.85 per hour.Hyperinflation is defined as inflation that exceeds 50 percent per month, which is just over 1 percent a day.Questions1. Money is not unique as a store of value; any asset, be it money, stocks, bonds, land, houses, art, or jewelry, can be used to store wealth.Many such assets have advantages over money as a store of value: They often pay the owner a higher interest rate than money, experience price appreciation, and deliver services such as providing a roof over one's head. If these assets are a more desirable store of value than money, why do people hold money at all?The answer to this question relates to the important economic concept of liquidity.2. Rank the following assets from most liquid to least liquid:a.Checking account depositsb. Housesc. Currencyd. Washing machinese. Savings depositsf. Common stock3. Why have some economists described money during a hyperinflation as a “hot potato” that is quickly passed from one person to another?4. Was money a better store of value in the United States in the 1950s than it was in the 1970s? Why or why not? In which period would you have been more willing to hold money?5. In Brazil, a country that was undergoing a rapid inflation before 1994, many transactions were conducted in dollars rather than in Reals, the domestic currency. Why?Quiz1. Fiat money is:A. credit card chargesB. CoinsC. not convertible into precious metals.D. checksAnswer: C2. Which of these is not a function of money in an economy?A. Store of valueB. Medium of exchangeC. Source of incomeD. Unit of accountAnswer:C3. Which of the following is not part of M1?A. checking accountsB. traveler's checksC. savings accountsD. currencyAnswer:C4. If Mary deposits $100 of her currency in her checking account, then:A. M1 will increase by $100.B. M2 will fall by $100.C. M1 and M2 will not change.D. M2 will increase by $100. Answer:C5. If Mary moves $100 from her savings account to her checking account, then:A. M1 will not change.B. M2 will not change.C. M1 will fall by $100.D. M2 will fall by $100. Answer:B6. Which of the following is not part of M2?A. Small time depositsB. CurrencyC. Institutional money market mutual fundsD. Saving accounts Answer:C7. Inefficiencies that are created when using checks as money include:A. Checks can transfer funds slowly.B. There are too many bad checks written.C. Checkbooks can be stolen.D. Checks can be written for any amount.Answer:A8. The liquidity of an asset is:A. the ability of an asset to earn interest income.B. the amount of an asset sold at discount or premium.C. the relative ease with which an asset can be converted into a medium of exchange.D. the relative ease with which an asset can be converted into a common stock.Answer:C9. For a commodity to function effectively as money, it mustA. Be widely accepted.B. Be backed by gold or silver.C. Be indestructible.D. Be printed by the government. Answer:A10. Money supply data is generated by:A. The Department of CommerceB. The Federal Deposit Insurance Corporation (FDIC)C. The Federal Reserve System (the Fed)D. The Treasury DepartmentAnswer:C11. Which of the following correctly shows the evolution of the payments system?A. Commodity money, fiat money, checks, electronic money.B. Commodity money, fiat money, electronic money, checks.C. Commodity money, checks, fiat money, electronic money.D. Fiat money, commodity money, checks, electronic money. Answer:A12.Which of the following is true regarding money's store of value function?A. money does not allow a person to hold purchasing power from the time income is earned until it is spent.B. money is the only store of value available.C. money is the most liquid store of value available.D. money is superior to all other stores of value during periods of inflation.Answer:C13. Which of the following is not a disadvantage of electronicmoney?A. People are concerned about the privacy and security of e-money transactions.B. E-money transactions cost more than paper check transactions.C. The cost of setting up a system for processing e-money payments is high.D. E-money does not allow people to take advantage of float. Answer:B14. Wealth isA. Generally accepted for the repayment of debtsB. A flow of earnings per unit of timeC. A stock conceptD. The total collection of pieces of property that serve to store value Answer:D15. The Fed's measurements of monetary aggregatesA. Are more reliable in the short run than the long run.B. Are revised once a year.C. Does not depend on the definition of money.D. Are more reliable in the long run than the short run.Answer:D。

[转载]金融英语01

![[转载]金融英语01](https://img.taocdn.com/s3/m/ca070f2742323968011ca300a6c30c225801f059.png)

[转载]⾦融英语01 ⾦融数字原⽂地址:⾦融英语01 ⾦融数字作者:空⼼菜MaxUnit 1 Money1.1 FiguresAmerican oil billionaire J. Paul Getty has a very famous saying, that is “ If you can actually count your money, then you are not really a rich man.” Well, the sentence is interesting, but actually we must know how to count the money before we get rich, especially in English. So, in today’s class, we would first learn to say English numbers.Let’s talk about the different ways to say 0 in English.Usually, we have the following 5 ways to say 0 in English.They are: OH, ZERO, LOVE, NOUGHT, NIL!We say ohafter a decimal point 6.03 six point oh threein telephone numbers 84 08 32 13 eight four oh eight three two one threein bus numbers No. 708 get the seven oh eightin hotel room numbers Room 308 I'm in room three oh eight.in years 1905 nineteen oh fiveWe say noughtbefore the decimal point 0.201 nought point two oh oneWe say zerofor the number 0 the number zerofor temperature -5~C five degrees below zeroWe say nilin football scores 5-0 Spain won five nil.We say lovein tennis 15- 0 The score is fifteen love.Now say the following:1. The exact figure is 0.002.before the decimal point, read nought;after a decimal point, read oh.Nought point oh oh two.2. Can you get back to me on 010 – 5175 – 0123 ? I'll be here all morning.in telephone numbers, say oh.Oh one oh five one seven five oh one two three3. Can you put that on my bill? I'm in room 804.in hotel room numbers, say oh. Eight oh four4. The temperature in north-east China is very low in winter. Usually, it's 20 degrees below 0!for temperature, say zero.5. Basically, tennis scoring proceeds from 0 to 15 to 30 to 40 to game.love(0), fifteen(15), thirty(30), forty(40), game(胜局)。

英语(Money)PPT课件

• 5. But people didn’t think gold and silver were convenient if they had to buy something expensive. 人们认为要买贵重的商品,使用金银币也不方便。

The first metal coin of China

They were round and had a square hole in the center. People strung them together

Let’s discuss

History of money

Is money everything?

ThWiinthgms omneoynweeyccaannbudyoa lot oTf hthiinnggss. mWeocnaenybcuaynd’etlidcoous food, nice clothes, beautiful flowers, comfortable houses. 1B.eIsticdaens,bwuey cdaenliceinojuosyfaolol dkinds o1.f seItrvciacne’st .buy a real friend. anHdonwiecveecrl,oetvheersy. coin has two sides. There are also many 2th. ings that money can’t do. We c2a. n’t buy a real friend with 3m.oney. We can’t buy a healthy b3o. dy. We can’t buy a comfortable sleep. We can’t buy happiness. ...So In my opinion, money isn’t .e..verything.

金融英语教程 第一章

Be tempered with 使调和,使缓和

Risk has clearly not disappeared financial market. Global imbalances, sustained high oil prices and soaring levels of household indebtedness - each alone, or in combination- could impair future global growth. However, they are unlikely to materialize any time soon.

before class 课前预习 Preparation for the class

preview

Reading the text Finding out the new words Checking out the meanings of new words Trying to understand the main idea of the text Examining the Chinese concept of the professional financial term

Ordinary time study performance

2 If you don’t have 24 points (40%×60 points) for this part , you will not allowed to take the final exam.

What should you write on the cover of the exercise book as required:

金融英语课文翻译chapter1 money class1 new

第1页张盼青刘嘉瑞货币的历史最初:物物交换物物交换是一种对资源或服务的交换,用来得到共同的利益,这也许要追溯到人类的开始。

有的人甚至争辩说这不仅仅是人类的活动。

植物和动物一直在物物交换——在共生的关系中——维持了几千年。

无论如何,人类的物物交换是要先于货币的使用的。

今天,个体,组织和政府依旧使用也经常更喜欢用物物交换来作为物品和服务的形式。

公元前9000~600年:牲畜牲畜是第一个,也是最古老的货币形式,包括了任何牛,羊,骆驼。

随着农业的出现有了谷物的使用和其他蔬菜或植物生产在文化中作为物物交换的标准形式。

公元前1200年:贝壳币(或直接写贝币)贝币是一种可在太平洋和印度洋的浅水区可得到的软体动物的外壳,第一次使用贝币是在中国。

历史上,许多社会已经用贝壳当做货币。

尽管最近是在上世纪的中叶,贝壳已经在一些非洲地区使用。

在历史上贝币是最广泛和最长使用时间的货币。

第3页王凌云王云霞公元前1000年,第一个金属货币在石器时代末期,制造了青铜和铜仿制品。

中国第一个使用了像刀和铁楸这样的金属货币工具。

这些早期的金属货币是圆形货币的初始形式。

中国的硬币是以常用金属为基础制造的。

通常有孔,因此可以把他们穿成一串。

公元前500年,现代货币在中国以外,最早的货币是由银块发展成的。

他们与今天的圆形非常相似,而且,被充满各种上帝和皇帝的图像来标志他们的真实性。

这些最早的货币出现在吕底亚(是现在土耳其的一部分),但是这种工艺很快被Greek, Persian, Macedonian和罗马帝国复制和进一步的改进。

不像依赖于基础金属的中国货币,这些货币由像银,铜,金这样的珍稀金属制造,内在价值更高。

公元前118年,皮革货币皮革货币在中国以带有彩色镶边的一平方英尺的白色鹿皮当做货币使用,它可能是第一个看做有证明文件的纸币类型。

公元806年,纸币第一个纸币出现在中国。

中国使用早期纸币总共经历了500多年之久,它贯穿了第九世纪到第十五世纪。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

( ) 1. a means of payment ( ) 2. checkable deposits ( ) 3. payment tool ( ) 4. debt repayments ( ) 5. common stock ( ) 6. liquid assets ( ) 7. near monies ( ) 8. a given point in time ( ) 9. stock of money ( ) 10. financial claims

Chapter 1

Money

CONTENTS

1.1 L e a d - i n 1.2 K e y Po i n t s 1.3 L a n g u a g e N o t e s 1.4 F o l l o w - u p Ta s k s 1.5 E x t e n d e d Ta s k s

• depository institutions

the U.S. Treasury 美国财政部

• fiat money

unit of account计量单位

• financial claim

• medium of exchange

• monetary aggregate

• money market deposit accounts (MMDAs)

Money, as a repository of purchasing power over time, also functions as a store of value. It is an asset which can be used to store value for the future. When we don’t consume the money now, we can save it and transfer the consumption power to some point in the future.

A. 债务偿还 B. 普通股 C. 一种支付手段 D. 金融要求权 E. 可支取的存款账户 F. 一个给定的时间点 G. 货币存量 H. 支付工具 I. 流动资产 J. 准货币

1.4 Follow-up Tasks

II. Judgments Directions: Decide whether each of the following statements is true (T) or false (F).

M1

M1 is the measure that corresponds most closely to the definition of money. It consists of currency held by the public and checkable deposits.

M2

M2 consists of everything in M1 plus some highly liquid assets which can be converted to the items in M1 very easily without the loss of value for the principal. The other highly liquid assets are small savings, time deposits, MMDAs, and individual money market mutual funds.

1.1Lead-in

In this chapter, we will first of all examine the definition of money, then introduce the meaning of monetary aggregate, and finally discuss the main

functions of money.

1.2 Key Points

1.2.1 Definition of Money

¥$

Money

Money is defined as anything that is commonly used to pay for goods and services.

Economists make a distinction between money in the form of currency, demand deposits, and other items that are used to make purchases and wealth, the total collection of property to store v money, but also other assets such as bonds, common stock, art, land, furniture, cars, and houses.

1.4 Follow-up Tasks

III. Short Answer Questions Directions: Answer each of the following questions briefly.

1. What assets have acted as payment tools in the history of mankind? 2. What are the differences between wealth and currency? 3. What is the relationship between M1, M2 and M3? 4. What is the major problem of making transactions by barter? 5. What are the advantages and disadvantages of money as the store of value?

1.4 Follow-up Tasks

I. Matching

Directions: Match the English words and phrases in the left column with the proper Chinese equivalents in the right column.

1.3 Language Notes

II. Phrases

• barter economy

• narrow money

• checking account

• paper money

• commodity money

• store of value

• demand deposits

• the Federal Reserve System ( the Fed)

1.3 Language Notes

III. Sentences

1. It occurred because gold and silver merchants or banks would issue receipts to their depositors – redeemable for the commodity money deposited. 2. Economists make a distinction between money in the form of currency, demand deposits, and other items that are used to make purchases and wealth, the total collection of property to store value. 3. They consist of demand deposits, which are non-interest-earning checking accounts issued by banks, and other checkable deposits, which are interest-earning checking accounts issued by some depository institutions. 4. Even though these other assets are not used to make transactions, they are all highly liquid, so they are often referred to as near monies. 5.In other words, in a barter system, the exchange can take place only if there is a double coincidence of wants between two transacting parties.

M3

M3 consists of everything in M2 plus some illiquid assets. The assets include large deposits, repurchase agreements, European dollars, institutional money, and market mutual funds.

1.M1 is not the narrowest measure of money. ( ) 2.Demand deposits are more profitable than the traveler’s checks. ( ) 3.Money market deposit accounts (MMDAs) have more checkingwriting privileges than checking accounts. ( ) 4.Not all components of M1 can be used as means of payment. ( ) 5.Only money has the store of value. ( )