安达信咨询方法与工具资料库WPLAN-08

安达信咨询方法与工具资料库00_NEW

What ' s New in 1997Several changes have been made to the January 1997 release of the Business Consulting Engagement Quality Assurance (EQA) Procedures & Guidelines. These changes are based primarily on the feedback provided by BC practitioners, the results of our 1996 practice reviews, and input from the Firm ' s Legal Group. Identified below are these changes.Risk SMARTRisk SMART has been automated. Key features include the on line entry of risk indicators, on line entry ofaction steps for high risk items and the automated preparation of the Risk Management Action Plan.Automation of the risk assessment process will facilitate the completion of the required forms and in obtainingthe required consultation from the mandated BC partners.The automated Risk SMART is available from the BC KnowledgeSpace. The Word documents will continueto be available in the EQA manual to allow for a smooth transition to the automated system.InterimAgreement On occasion it may not be possible to get a contract fully negotiated before the scheduled commencement date of AA ' s services. In these cases, we now have anInterim Agreement (See Appendix 21). An Interim Agreement is a short contract that documents the fact thatthe parties are working toward, but have not yet finalized, a definitive agreement. Specific usage guidance isincluded in the appendix.Changes to theJobArrangement Letter and Consulting Services Agreement There have been several changes to the standard terms and conditions associated with our Job Arrangement Letter (Appendix 14) and our Consulting Services Agreement (Appendix 15). These changes are defined below and have been included in the appendices.These new contracts must be used on all new engagements.Remember, these appendices are based on the laws of the United States. Countries outside the U.S. will need to work with their Area Legal Group (Nancy Laben in Hong Kong and Michael Hughes in Paris) to make the appropriate changes based on local laws and regulations.Ownership ofWork ProductIt has been our initial position that the client retains ownership of the work product. This has raised questionsregarding knowledge capital and the reuse of developed products on subsequent engagements, particularlyon custom systems development engagements. Consequently, we have changed the initial position in ourcontracts so that AA retains the ownership of the work products and the client has a non-exclusive license touse the work products. Optional provisions continue to be offered in the Consulting Services Agreement. Year 2000Potential risks to the Firm associated with the “ Year 2000 ” problem have beenaddressed in our standard contracts. Areas affected include the limits of liability, indemnification andwarranty. Please note the inclusion of the appropriate legal language and guidance for usage.Warranty Government Contracts (U.S. only) The default warranty period offered in our standard contracts has been reduced from 90 days to 30 days. In some instances, such as custom systems development, this time frame may be insufficient. Changes to the warranty period are a matter of business and you should involve your Country/Regional Quality Leader in these discussions.In the past we have offered alternate limit of liability, indemnification, and warranty language for contracts with any government agencies. Our experience has been that contracts with government agencies go far beyond these three areas and typically require the involvement of the Firm ' s legal group. In gaodvdeitrionnm,ent clients tend to present us with their contract to sign thereby creating the need to include the Firm ' s legal group.Therefore, this alternate language has been removed and it is now recommended that all government contracts be reviewed with th e Firm ' s legal group.。

安达信咨询方法与工具资料库ILVER

Item Processing

Investments

SILVERLAKE N

FINSER 1987

Safe Deposit SILVERLAKE

N

MEMO POST Y AS/400 BASED

N/A RPG400

Stockholder Accounting

SILVERLAKE 1987

N

IPS 1987

Y

Fixed Assets

General Ledger

SILVERLAKE N

1987

MEMO POST Y AS/400 BASED

Additional Comments:

1627738039.xls, SILVER

2020/11/12, 1:15

Service Bureau/In-house System Survey

Appendix A

Arthur Andersen

Name of Package? How old is the Program? Third Party ( Y/N/Partly)

Asset Liability Management

Customer Profitability

Product Profitability

安达信咨询方法与工具资料库TRANACT

Med. Record Lookup

Total Req Records

Pharmacy

Total Req Records

Employer Profile

Total Req Records

Employer Lookup

Total Req Records

Center Status

body_part retrieve: body_part insert: body_part update: body_part delete:

case retrieve: case insert: case update: case delete:

center retrieve: center insert: center update: center delete:

Total Req Records

Patient Checkout

Total Req Records

Charge Entry

Total Req Records

Med. Record Maintenance

Total Req Records

Med. Record Lookup

Total Req Records

Total Req Records

1

2

1

2

3

120

1

6

1

1

Page 7

Date: 2020/11/14 Time: 0:25

guarantor delete:

hsm retrieve: hsm insert: hsm update: hsm delete:

hsm_clinic retrieve: hsm_clinic insert: hsm_clinic update: hsm_clinic delete:

安达信咨询方法与工具资料库PLANNING

1.4

CREAR EL PLAN DE PROYECTO.

1 Crear el Plan de Trabajo del Proyecto. 2 Asignar fechas de realizaci髇 de las tareas. 3 Asignar responsables a las tareas.

4 Preparar los datos. 5 Preparar la documentaci髇 para los usuarios. 6 Mostrar el prototipo a usuarios y direcci髇. 7 Revisar la lista de puntos de calidad de la fase de Dise駉

FASE 2: DISE袿 DETALLADO Y PARAMETRIZACI覰

SD DISE袿 DETALLADO SD Dise馻r modelo de organizaci髇 Determinar datos b醩icos Dise馻r modelo de procedimientos Identificar procesos recurrentes Implementar interfases Configurar formularios Configurar reporting Determinar autorizaciones

安达信咨询方法与工具资料库CPWORK

Page 8

Sheet1

Org aniz atio n char - ts

Syst ems doc ume ntati - on Pro duct liter atur -e Rep orts from prev ious wor k, eith er by inter nal or exte rnal con sult - ants Bro chur - es Audi t tea m blue bac ks (if an audi t clie - nt)

b. ysis

Page 3

Sheet1

Con duct oneonone inter view s with key stak ehol ders to und erst and their curr ent visio n of the futur 2 e.

Und erst and the exte nt to whic h the visio n is shar ed amo ng pote ntial key stak ehol ders 3.

Time to Completion

Co

ns

Met hod olog y Deli vera bles : No Deli vera bles .

Pha se Na me: Ass ess Syst emi c Nee ds

Pha seΒιβλιοθήκη Deli vera bles : Co mpl eted Que stio n Pyr ami d CP 1 Deli vera ble List

Tas ks:

Sheet1

Page 2

Sheet1

安达信咨询方法与工具资料库PAPER

INDUSTRY ANALYSIS FRAMEWORK -- A Global PerspecivePaper and Forest Products Industry -- March 1995(Source:Daniel H. Wick, Forest Products Segment Director)PURPOSEThe purpose of the Industry Analysis Framework is to describe the fundamental forces driving an industry. It presents our auditors with a good framework with which to evaluate global industry risks and issues and, in turn, determine the applicability of these risks to specific clients. The Industry Analysis Framework accomplishes these objectives by:∙Presenting a brief description of the industry from a global perspective∙Discussing the critical elements of the Business Analysis Framework affecting the industry∙Presenting available global resourcesDESCRIPTION OF THE INDUSTRYThe Paper and Forest Products Industry consists of different companies that operate in two distinct segments: paper and pulp or forest products. Many of the largest diversified companies in the industry operate in both of these segments. The companies in this industry share the common characteristic of utilizing input materials that were originally derived from trees.Some specific Forest Product types are:∙Hardwood and Softwood Logs∙Wood Chips∙Lumber∙Structural and Non-structural Panels∙Specialty Products (doors, windows, moulding and millwork, etc.)The construction sector (primarily residential) is the main end-use market for most of this segment of the industry's products. Other end-use markets include furniture, cabinets and fixtures, and pallets and skids.The Paper and Pulp segment has two distinct subsegments: Primary Products and Converted Products. Primary Products encompasses pulp, paper and paperboard manufacturing. Some specific Primary Product types are:∙Market Pulp∙Printing and Writing Papers∙Sanitary Tissues∙Industrial-grade Papers∙Containerboard∙BoxboardCompanies in the Primary Products subsegment operate capital intensive mills that transform cellulose fibers from timberlands or purchased virgin and recycled fibers into the above products.The Converted Products subsegment uses Primary Paper Products as inputs to manufacture value-added finished goods. Some Converted Products are:∙Coated Paper∙Paper Bags∙Boxes∙Envelopes∙Sanitary Tissues∙Corrugated Shipping Containers∙Folding Cartons∙Flexible PackagingThe largest firms in the Converted Products subsegment are affiliated with Primary Products firms. These companies have a cost advantage over the more numerous, small independent shops due to the strength of the relationship with their largest vendor.INTRODUCTION TO THE FRAMEWORKThe Industry Analysis Framework for the Paper and Forest Products Industry is intended to assist us in thinking more strategically and operationally about a client. It has been developed to contribute to: (1) gaining an in-depth understanding of the client’s business as a whole and (2) identifying and evaluating critical business issues and changes affecting the company and industry. The framework is intended to focus on the external and internal influences that affect a client’s opportunity for success, and thus, to deal with the matterns of concern to the chief executive officer, the owners, the community and the employees. The Industry Analysis Framework for the Paper and Forest Products Industry is illustrated below:The elements of this framework are intended to be applicable to any Paper and Forest Products company anywhere in the world as they deal with the fundamentals of this industry. While these business elementsare common, the specific environment within which each of these elements operates will obviously vary significantly from country to country. Depending on the type of Paper and Forest Products company, its location and other factors, the specific environment will vary due to differences in factors such as the regulatory environment, the status of the overall economy, and the availability of qualified labor. OVERVIEW OF BUSINESS ELEMENTSThe purpose of this section is to identify and describe the basic business elements that are fundamental to the Paper and Forest Products Industry, using the framework described above.A. Environment1. Domestic and Global EconomyPaper and Forest Products companies have the ability to sell goods in both domestic and globalmarkets. The companies in most of the segments cited above have sales which are largelydependent on gross domestic product in served markets.The drivers of demand differ for the Paper segment and the Forest Products segment in otherrespects.Demand for forest products is linked closely to the health of the residential construction industry.Residential construction accounts for 70% of sales of wood products. New housing starts are very interest rate sensitive which causes wood product sales to share this sensitivity. Remodeling and rehabilitation activity can compensate for weak new home starts in times of high interest rates.Paper product demand is mostly independent of the level of interest rates because unit prices arelow to end users. Although sensitive to cycles in domestic GDP, the market for paper products is quite mature in the industrialized nations. Consequently, most companies are looking to exportmarkets as the best available growth opportunity.The export market is also a good method for Paper and Forest Product companies to insulate sales and profits from country specific business cycles. Foreign sales already comprise a sizablepercentage of sales for some of the larger companies (anywhere from 10-50%). However,exchange rate fluctuations, unless hedged against properly, can quickly destroy profits fromforeign sales.2. Government RegulationGovernment has a direct impact on many areas of Paper and Forest Products company operations.While regulation is a reality in every country, the details can vary significantly.Wood product companies can be subject to regulations about how, where and when they canharvest timber on both public and private lands. Harvesting regulations have tended to becomemore restrictive over time as society grows more environmentally conscious. Forest productscompanies are also subject to government regulations about the export of product and theavailability and cost of competing imported product.Paper and pulp primary product manufacturers have regulatory constraints similar to forestproducts firms to the extent they integrated into virgin fiber production. Other areas ofgovernment influence in this segment are environmental discharge regulations, import tariffs,export ceilings and specifications for recycled product sold to government offices.Paper and pulp converted product firms are the least affected by government of the three mainsegments of this industry. The impact of government has historically been limited to areas which apply to all companies: worker safety and taxes. Recently the European Community has begun an initiative to reduce solid waste from packaging materials, increase the amount of packagingmaterials that are recycled and minimize the amount of this type of waste going for final disposal.3. TechnologyTechnological advancements influence each segment of this industry in varying ways.Technology is most likely to improve capital intensive production processes.The forest products segment has experienced moderate technological advancement since theintroduction of the gas powered chain saw. Recent advances in genetic engineering capabilitieshave accelerated the rate of development of hybrids and genetically customized trees with disease, weather and pest resistant traits and shorter growing periods. Other advances include automated delimbers and harvesting machines.The converted paper products segment will need to adapt to the changing technological climate in several ways. Computers improve the ordering, production and distribution processes. Specificexamples include lighter weight, more colorful folding cartons and on-line customer orderfacilities.The main focuses for technological improvement in the primary paper and pulp segment is toward finding substitutes for chlorine in the fiber bleaching process, improvements in the brightness ofbleaching processes, efficient energy use and improved cleaning and processing of recycled fiber.4. Ecological ConcernsPaper and Forest Products is an industry with numerous issues related to ecological impact. This is apparent as these issues appear in quite a few of the sections of this document. Recycling hasgrown in popularity rapidly in the past 10 years. Environmental groups are pushing harder thanever to preserve the few remaining old growth forests in the world. Alternatives to chlorine in the bleaching of pulp fiber are sought with vigor. Ecologically friendly packaging design may bemandated by government. The biodegradability of disposable baby diapers is an issue as sanitary landfill space fills up in large urban areas. Government controls on emission levels continue totighten.B. OwnersThe two basic types of ownership in the Paper and Forest Products industry are:∙Publically Traded Companies- The publically held firms dominate the paper and pulp segment of the industry due to the capital requirements.∙Private Companies- Some companies are private and closely or family held. They tend to be more prevalent in forest and converted paper products.The o wners’ main goal is the generation of profits. Consistent profitability in this industry hasbeen acheived by firms which are best at managing their cost levels through valleys in thedomestic economic cycle.Although profits are the main goal of ownership, the company can not lose sight of its duty as acorporate citizen to temper the pursuit of profits with responsible behavior in the community.Sensitivity to ecological impacts from waste disposal practices is an example of corporateresponsibility that makes sense in business practice. Legislation in many industrialized nations ismaking the economic consequences of contaminating the environment costly to businesses.C. CustomersThe customers of Paper and Forest Products companies vary by segment. Although thesecustomers are a diverse group, they all have three basic needs, quality products supplemented witha high level of service at a reasonable cost.∙Forest products customers are primarily in the construction industry. Other customers served include furniture, cabinets, pallets and skids, and wood chips.∙Paper and pulp primary product manufacturers serve customers in need of printing and writing paper, sanitary tissue, industrial paper stocks, commodity grades of wood pulp,containerboard and boxboard. Obviously, other primary product manufacturers withoutadequate pulp supplies would be net purchasers of commodity pulp. Most of the otherproducts supplied are used primarily by the converted products segment. Finally, industrialusers, advertisers, printers and publishers make up the balance of large customer types.∙Paper and pulp converted product manufacturers sell product to industrial and consumer non-durable goods manufacturers for use as shipping and packaging material. In the case ofsanitary tissues, the consumer (or commercial firm) is the direct end user of the product.Durable goods customers’ share of industry output purchased has been in decline for fiveyears and now comprises about 20% compared to non-durables’ 80%. Consu mer non-durablecustomers are demanding more value added products with enhanced, multicolor graphics foruse in point of purchase displays and in product packaging.The outlook for each of these groups of potential customers varies widely from country to country.The more companies and countries served in its client base, the more a company’s revenue stream is insulated from a single industry or country business decline.D. CompetitorsCompetition in this industry is split between the two major segments, forest products and paperand pulp. Forest products require less capital in production than do primary paper and pulpproduct firms whose production process converts fiber into product. This lowers the capitalbarrier to entry and allows more small, private enterprises to operate in the forest productssegment. The converted paper product segment is not as capital intensive as primary products.These differences in capital needs impacts the basis on which firms in this industry compete.Forest ProductsCompetion in wood products takes place on two levels: securing supplies of logs and pricingproduct. Many of the old growth forests of the world have been logged and those that have nottend to be in remote, undeveloped areas and/or protected by government regulation. Supplies ofimported logs can compete against local supply only if available and at a favorable price. Accessto harvestable timber is a key determinant of a company’s ability to survive.Forest products do have the advantage of having relatively few substitutes, although steel andconcrete have had considerable success as building materials.Paper and Pulp- PrimaryWith the large amount of capital required for capacity growth and the focus on output volumeefficiencies in this segment, competition is on the basis of price. Capacity expansion can occursimultaneously and the excess supply created will bring prices to the level of marginal cost.New state of the art plants brought on line in Latin America and Africa have become factors in the competitive market for pulp. Plants in these countries enjoy several advantages. Supplies ofwood are fast growing and abundant. Labor, environmental and general overhead costs are lower than in more developed countries.The continuing rise in demand for recycled product has produced a race to introduce more types of primary paper stocks with recycled fiber content. Firms able to react quickly to this marketdevelopment have had a competitive advantage.Paper demand has also been impacted by the substitution of electronic media in the form oftelevision, radio and the growth of the trend towards a paperless office.Paper and Pulp- ConvertedCompetition in this sector is largely on the basis of price. This makes proximity to major markets an advantage by holding down transportation costs. Since the production process is more laborand less capital intense, price competitiveness is also dependent on the ability to hold down labor costs.Market share competition in the sanitary tissue segment is intense and firms are spending heavily on advertising new and existing products to consumers. Competition has been particularly keen in the disposable diaper segment which does have significant capital cost and proprietary technology barriers to entry. The race to discover a new biodegradable disposable diaper is commanding a lot of resources from firms in this market.Substitute plastic products are a factor in the box, carton and bag segments. Firms have sought to replace demand lost to plastic alternatives by expanding end use applications. For example,cartons traditionally used to package milk have found use as packages for fruit juices, nondairyflavored drinks, dry pet foods, laundry detergents and hardware.E. ResourcesThe most significant resources used and challenges faced by Paper and Forest Product companymanagement include:∙Labor - A competitive factor in the forest products segment which is less capital intense. Labor makes up 10-20% of the operating costs of firms across the industry. Labor unions are wellorganized as evidenced by the United Paper Workers International in the U.S. As the automation of production equipment and processes advances, the computer skill levels required of theworkforce will need to increase.∙Raw Materials - Includes logs, virgin and recycled pulp fiber sources and primary paper products for the converting segment. Depending on the product mix, raw material costs can be verysignificant to all firms in the industry and run from 40% of sales to as high as 70%. Holding down raw material costs while maintaining steady supplies is a challenge.∙Energy - Energy sources such as electricity are essential to the production process and can be a significant component of the cost structure. The goal is managing utility costs by conserving and negotiating with suppliers. Severe problems can be caused by disruptions to the supply of energy or massive price increases which have occurred from time to time in worldwide and local markets.∙Capital - A more significant issue in primary paper and pulp production where marginal capacity comes in large volume and is expensive. Debt comprises 40-60% of capital for these companiesand most of them have tapped the public equity market. Other sources of capital needs includeplant upgrades to handle recycled fiber and pollution control equipment.∙Plant and Equipment - Paper and pulp primary product manufacturers need to successfully upgrade production lines to handle the increasing use of recycled fiber, meet environmentalemissions regulations and increase productivity. Some firms are realizing significant savings byrebuilding or adding onto existing machinery and equipment rather than purchasing new.F. OperationsThe essence of Paper and Forest Products operations is conversion of raw or primary materialsinto end product to fill orders. This process can be divided into distinct areas such as--purchasing, production, sales and marketing, research and development, quality control, andshipping and receiving. Continuous improvement is necessary in all aspects of operations toenhance quality, improve productivity and financial performance, meet established workplace and environmental regulations, meet product specification requirements and meet just-in-time delivery schedules.Key challenges for operations management across the industry include:∙Modernizing Manufacturing Systems - Both segments of paper and pulp need to consider adapting “Just in Time” production processes with shorter runs and sophi sticated machinery with minimal set-up times and high quality output. Upgrades by primary paper and pulp companies forenvironmental compliance and to convert recycled fibers are a growing use of capitalexpenditures.∙Implementation of Total Quality Management (TQM) - TQM programs have total customer satisfaction as their goal. This includes on-time delivery and competitive pricing, much more than the typical quality measures of compliance with product design and specifications. Leadershipfrom management is necessary to effective implementation of TQM.∙Improvement of the Product Development Process - Rapid new product development can be used to gain new business and retain existing clients. Converting firms can utilize cross-functionalteams, computer-aided design and manufacturing (CAD/CAM), design for manufacturing (DFM) and concurrent engineering (suppliers’ assistance) to speed development and lower costs.∙Reinforcing Vendor Relationships - The concurrent engineering and design for manufacturing movements depend upon the participation and support from key suppliers. Leveraging tradedollars spent with suppliers is becoming more common.Some of the above considerations are more relevant to specific segments of the industry than toothers. For example, the product development process for forest products companies is not socomplex as to require CAD/CAM.G. ManagementManagement must steer operations through the challenges cited above in competitors, resources, operations and other areas.Management priorities include:∙Strategic Planning - Management must establish a strategic planning process that includes monitoring and evaluating the environment and other external forces, organize keymanagement positions to support the process, direct operations responsibility and authoritytoward achieving the goals set by the strategic plan and monitor results.∙Customer and Supplier Relationship Management- Very important in the context of Just-in-Time, Design for Manufacturing and concurrent engineering.∙Provide Leadership- Management’s effectiveness is linked closely to establishment of a role as leader. Management must have the ability to assume and manage business and financialrisk, particularly with respect to potential changes in government regulation and thecompetitive environment. Management must also have the ability to recognize strategicopportunities, not just risks.H. ValueA successful organization determines the values of its stakeholders and sets about satisfying those values. The various stakeholders and some basic value considerations are:∙Owners - Providing a reasonable rate of return on investment to ownership.∙Workers - Providing secure jobs with decent pay, benefits and working conditions.∙Customers -Providing the “right product at the right place at the right time at the right price”.∙Vendors - Providing the opportunity to establish long-term healthy relationships that are “win-win”.∙Community - Providing jobs, a tax base and economic stimulus in a non-obtrusive manner. ADDITIONAL RESOURCESPersonnel ReferencesWorldwide Manufacturing Industry Director: Steven M. Hronec, Los Angeles (213) 614-8512Deputy Manufacturing Industry Director: James M. Eberle, Washington, D.C. (202) 862-6440Paper and Forest Products Segment Director: Daniel H. Wick, Seattle (206) 386-8674Area Industry Directors:Americas Steven M. Hronec, Los Angeles (213) 614-8512EMEIA Steven M. Hronec, Los Angeles (213) 614-8512Asia/Pacific Alfonso (Tito) Aliga, Manila (2) 812-8166Manufacturing Industry Audit Practice Directors:Americas Gary N. McKinley, San Francisco (415) 546-8767EMEIA Claus-Peter Weber, Hamburg (40) 35-60-7100Asia/Pacific T.M. Chung, Taipei (2) 545-9988For additional industry personnel, consult the Directory of Industry Teams Additional Reference SourcesU.S. Industrial Outlook, 1994, the U.S. Commerce Department Amadeus company reports, Bureau Van Dyck, January 1995 discINDUSTRY BUSINESS ENVIRONMENT -- A U.S. PerspectivePaper & Forest Products Industry -- March 1995(Source: Daniel H. Wick, Forest Products Segment Director)PURPOSEThe purpose of the Industry Business Environment is to describe the critical forces driving an industry domestically. It presents our auditors with a good framework with which to evaluate industry risks and issues and, in turn, determine the applicability of these risks to specific clients. The Industry Business Environment accomplishes these objectives by:∙Presenting a brief description of the industry, current performance information and a future outlook from a U.S. perspective.∙Discussing the critical factors affecting the industry.∙Outlining additional resources available to our personnel.OVERVIEW AND OUTLOOKScope of the Industry: The paper and forest products industry comprises two broad segments: forest products, and pulp and paper. Forest products include logs, wood chips, lumber, structural and nonstructural panels, and specialty products (moulding and millwork, doors, windows, etc.) Most of the lumber and wood products industry is concentrated in the Pacific Northwest and the Southeast. Secondaryconcentrations are found across the Midwest and Northeast and in Appalachia. The construction sector (primarily residential) is the main end-use market for most of the industry's products. Other end-usemarkets include furniture, cabinets and fixtures, wood chips, and pallets and skids.The pulp and paper segment includes a number of sectors that process wood, wastepaper, other cellulose fiber, and plastic film into thousands of end products. The primary-products sector encompasses pulp, paper, and paperboard manufacturing. These capital-intensive industries obtain cellulose fibers fromtimberlands or from purchased virgin and recycled fibers. They produce commodity grades of wood pulp, printing and writing papers, sanitary tissue, industrial-type papers, containerboard, and boxboard. The more labor-intensive converting sector uses primary products, such as paper and paperboard, in the manufacture of coated papers, bags, boxes, and envelopes.Paper and forest products is one of the largest U.S. manufacturing industries, with yearly shipments of more than $200 billion.Key industry fundamentals are as follows:∙There is little industry concentration, with the result that many firms compete in each segment.∙With few exceptions, most of the industries' products are commodities, and prices are established within almost purely competitive markets (via the intersection of supply and demand). There isalmost no pricing power. Consequently, imbalances in supply and demand can lead to enormous price changes. Indeed, during periods of excess supply, prices can decline to the cash cost of the marginalproducer.∙In an attempt to escape somewhat the extreme price volatility to which commodity products are subjected, many smaller manufacturers have attempted to differentiate their products. This avenue isnot available to the larger firms. Value-added grades include premium coated free sheet, somerecycled grades, and premium grades of bristols and bleached board. Likewise, the establishment ofclose customer relationships through premium service helps alleviate some of the vagaries of finding markets for products.∙Substantial international trade affects the balance of supply and demand in certain products. For example, the U.S. is a net importer of softwood lumber and newsprint and a net exporter of logs,market pulp, and paperboard.∙The factors that affect supply and demand in paper are quite different from those that affect supply and demand in forest products. (The common element is dependence of demand growth on GDP.) Because of these differences, the performance of the two sectors can be quite divergent.∙Maintenance of a lean cost structure is of paramount importance for producers of commodities that compete on the basis of price. In this regard, the U.S. industry ranks as one of the most efficient in the world. Advantages include relatively low-cost fiber, access to capital, relatively advantageous labor costs, and management committed to maintaining the cost competitiveness of the industry.∙Growth in demand and capacity are each strongly cyclical. With respect to capacity growth, strong operating rates and prices are the market's cue for additional capacity. Indeed, strong periods of free cash flow are typically followed by a surge in capacity. However, increasing capital requirements to meet new environmental regulations could eat up a great deal of cash generated by operations. This could serve to restrain future capacity growth, which has implications for pricing and competitive positions.∙In the paper segment, substantial operating leverage further adds to the volatility of earnings. Indeed, the industry operates very costly equipment in the production of low-value products. Consequently, there are strong disincentives for reducing production, even during periods of excess supply. Current Performance: Aggregate shipments in 1994 were $140 billion for paper products and $103 billion for forest products, increases of 5% and 3%, respectively. Paper markets exploded as 1994 progressed due to strong growth in the U.S. economy combined with relatively healthy demand from overseas. These two factors boosted prices for the majority of paper products. The unexpected boom, which is likely to continue in 1995 as long as growth of GDP remains on track, follows several years of extremely depressed conditions for paper producers. On the wood products side, higher interest rates have contributed to a decline in lumber pricing, but wood markets continue to be fairly healthy despite a slowdown in profit growth for suppliers of building materials.Outlook: Following several years of depressed prices and weak or nonexistent profits, most paper producers are expected to report sharply higher earnings in 1995 as extremely tight supplies and strong demand continues to boost pricing. As of January 1, 1995, newsprint prices were about 30% higher than they were at the beginning of 1994, linerboard was 50% higher, corrugating medium was 60% more expensive, and most other paper categories were 10% to 30% higher in price than a year earlier. Assuming the Federal Reserve's monetary policy doesn't result in a recession in 1995, paper production should rise more than 3%. More importantly, due to the higher operating and financial leverage in the paper industry, profits are likely to surge.Capacity growth in the paper segment is projected to be rather modest (averaging only 1.9% annually over the 1994-1996 period). Historically, when the industry experienced strong demand and pricing, as it is currently, producers raced to add capacity, invariably making the next down cycle even more severe. In fact, in the last boom period for the industry in the late 1980s, most large, integrated paper manufacturers took on high levels of debt to support capacity expansion projects. The current expectation is that a few lessons were learned in the past several years, and the industry's plans to add capacity may be modified by memories of the most recent downturn in paper market conditions as well as by the need to spend available funds to upgrade papermaking equipment for environmental reasons.。

安达信咨询方法与工具资料库MISSION

I. SERVICE DEFINITI ON

New Product Development is the process of creating, developing and commercializing new products/services, including generation of the initial idea, investigation of the product/service concept and its market feasibility, screening and select of the highest potential product/service development projects, design and development of the product (including all technical, operational, manufacturing, marketing, sales, distribution, financial, service and warranty plans) through launc of the new product/service in the marketplace. It begins with formulation of a product strategy (driven by the overall corporate strategy) and includes management of the entire product portfolio.

Page 1

安达信咨询方法与工具资料库avcalc

Total Hrs/Wk.

N

e

t

A

n

n

u

a

l

S

a

v

i

n

g

10

s

$868,920

$10.40 $6.37

(plus 10% to make lead assoc. position)

Incremental Difference

$4.03

Outsourcing Maintenance:

Stores Currently Monthly Fee Outsourcing (*less 10%)

12 - 24 months Changes

Average hrs/wk

Less Percent

of Reinvest

Net hourly savings

Average Hourly Weeks Rate per Year

Store Mutiplier

Net Annual Savings

40

70%

12

Savings per square foot per month per store Average selling square footage per store

Number of Months per Year Avg. Annual savings per store Estimate d stores in-house mainten ance

1

0%

1

$9.00

52

300

$140,400

1

0%

1

$6.85

52

300

$106,860

1

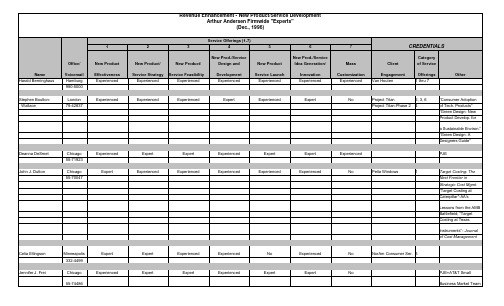

安达信咨询方法与工具资料库EXPERTS

New Product

New Prod./Service Idea Generation/

Service Strategy Service Feasibility

Expert

Expert

Development Expert

Service Launch Experienced

Innovation Expert

Development

Service Launch

Innovation

7

Mass Customization

CREDENTIALS

Client

Category of Service

Engagement

Offerings

Other

Moore Business Forms

Experienced

Experienced

Lessons from the AMB Battlefield; "Target Costing at Texas

Instruments"- Journal of Cost Management

Celia Ellingson Jennifer J. Frei

Minneapolis 332-4499

Chicago 55-74486

Expert Experienced

Expert Expert

Experienced Expert

Experienced Experienced

No Expert

Experienced Expert

No

NorAm Consumer Ser. 3

No

PJE=AT&T Small Business Market Team

安达信咨询方法与工具资料库QMWORK

Sheet1

Page 10

C on du ct th e Q ua lit y Le ad er S es si on to en su re ev er yo ne ha s a si mi lar st 2 ar

Sheet1

Page 11

A s pa rt of th e Q ua lit y Le ad er S es si on , co nd uc t an int ell ec tu all y ho ne 3 st

St ep D eli ve ra bl es : N o D eli ve ra bl es .

T as ks

Sheet1

Page 16

R ev ie w th e C us to mi zi ng Cl ie nt Tr ai ni ng to ol as w ell as ea ch of th e su gg 1 es

Sheet1

Page 5

M ee t wi th st ee rin g co m mi tte e m e m be rs to ex pl ai n th eir re sp on si bil iti 3 es

Sheet1

Page 6

S pe nd ti m e an d eff or t in di sc us si on s wi th th e st ee rin g co m mi tte e to 4m

St ep D eli ve ra bl es : N o D eli ve ra bl es .

T as ks

Sheet1 Page 9

S ch ed ul e a ti m e to m ee t wi th le ad er sh ip (t hi s m ay be th e st ee rin g 1 co

安达信咨询方法与工具资料库BRWOR

Sheet1

Page 12

Pha se Deli vera bles : No Deli vera bles .

Ste p Na me: Car e Abo ut Peo ple

Ste p Deli vera bles : No Deli vera bles .

Tas ks: No Tas ks.

Tas ks: No Tas ks.

Sheet1

Page 8

Ste p Na me: Deli ver On Pro mis es

Ste p Deli vera bles : No Deli vera bles .

Tas ks: No Tas ks.

Ste p Na me: Rec ogni ze Deg ree of Clie nt Trus t in the Rel atio nshi p

Tas ks: No Tas ks.

Sheet1

Page 6

Ste p Na me: Be Ethi cal

Ste p Deli vera bles : No Deli vera bles .

Tas ks: No Tas ks.

Pha se Na me: Cre ate Trus t

Pha se Deli vera bles : No Deli vera bles .

Sቤተ መጻሕፍቲ ባይዱeet1

Page 5

Ste p Deli vera bles : No Deli vera bles .

Tas ks: No Tas ks.

Ste p Na me: De mon strat e Skill s and Acc omp lish men ts

Ste p Deli vera bles : No Deli vera bles .

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Init. ID#ORG01 - Customer Development Initiative:Define Critical Process Flows1.0Identify all critical processes and related activities20 (5 to 7per area)Relating to new organizational structure1.1Generate list of critical processes and activitiesthat support new organization structure1.2Map critical processes1.3Identify value added activities1.4Rank/prioritize critical process activities1.5Gain understanding of how processes areinterrelated1.6Achieve consensus from stakeholders/key processowners2.0Benchmark recommended process designs withAA experts 8Identify similar businessprocess designs within andoutside of industry2.1Confirm with AA marketing experts3.0Identify barriers/enablers to achieve new processdesign 5Determining barriers regardingthe flow of critical processesthat will hinder performance3.1Conduct brainstorming session to identify barriers3.2Identify potential impacts on processes3.3Conduct brainstorming session to identify enablers3.4Utilize Expert/Best Practices information3.5Confirm action plans and primary responsibilities4.0Finalize recommended processes withstakeholders/key process owners104.1Ensure understanding of critical process flows4.2Achieve consensus from stakeholders/key processownersInit. ID#ORG01 - Customer Development Initiative:Define Critical Process Flows5.0Communicate redesigned processes toorganization 10Communicating the transitionto the future organizationalstate5.1Develop information materials for organization5.2Customize communication plan5.3Communicate process design to organization6.0Integrate revised processes5Merge initiative with initiativesin other focus areas6.1Coordinate with other implementation teams6.2Identify implementation dates for redesignedbusiness processesInit. ID#ORG02 - Customer Development Initiative:Define Roles/Responsibilities1.0Review organizational needs based on projectfindings 2Assess the current availabilityand positioning of resources1.1Identify resource gaps 1.2Prioritize resource needs2.0Identify jobs and associated roles/responsibilitiesneeded for new organization design 15Managerial, professional,clerical (Key Acct. Mgrs, E/WMgrs for W&R, VP CD, DirCS, Inside Sales people, W&RMktg Mgrs)2.1Identify key positions2.2Detail all positions and determine staffing totals byposition/job type2.3Define reporting relationships (particularly cross-functional)2.4Assess the ability to relocate non-value addedactivities to support functions2.5Communicate the necessity to reduce non-valueadded activities3.0Develop draft job descriptions103.1Identify skill requirements for all key positions3.2Assign "weighting" ranks3.3Provide clearly defined and understoodresponsibilities and accountabilities4.0Identify all stakeholders/key process owners3HR involvement4.1Review list of key positions4.2Confirm job assignments as determined by skillsassessment initiative5.0Identify and allocate resources (FTEs & $s) to thecritical processes 5May follow skills assessmentphase5.1Confirm primary (high-impact or high resource)business processesInit. ID#ORG02 - Customer DevelopmentInitiative:Define Roles/Responsibilities5.2Allocate FTEs and associated $s based onidentified roles/responsibilities and findings fromthe skills assessment26.0Gain consensus from stakeholders/key processowners6.1Ensure understanding of organization structure6.2Finalize roles/responsibilities needed for newprocess design7.0Communicate roles/responsibilities to organization5Communicating the transitionto the future organizationalstate7.1Develop communication plan7.2Communicate roles/responsibilities to organizationInit. ID#ORG03 - Customer DevelopmentInitiative:Perform Skills Assessment1.0Conduct employee focus groups and interviews51.1Confirm necessary and desired skill sets1.2Confirm skill weightings1.3Review and utilize initial project interviewinformation1.4Conduct management and non-managementinterviews for additional information2.0Create skills assessment survey52.1Use focus groups and interview results to designsurvey2.2Review designed survey with stakeholders3.0Perform skills assessment203.1Conduct one, or a combination of, the followingskills assessment techniques:To be filled out by supervisors, and Departmental employeesA) Skills assessment survey (See workstep 3.0)Those surveyed may be askedto rate the organization andthemselves against theirperception of competitorcapabilities - Supervisory evaluation- Peer evaluations- Interdepartment evaluations- Self-assessmentsB) Individual skills assessment based on historicalperformance reviews, and downward and upwardevaluation trends3.2Identify gaps in skill sets3.3Identify positions that provide a strong fit withindividual's skill sets3.4Identify candidates that need training to fit certainpositions (trainable)3.5Identify candidates that should be assigned toother areas (non-trainable)Init. ID#ORG03 - Customer DevelopmentInitiative:Perform Skills Assessment3.6Assess need to procure outside resources/skills3.7Assign individuals to key positions4.0Communicate findings34.1Analyze survey and assessment findings4.2Finalize recommendations of personnel that arebest suited for each position4.3Review with stakeholders/key process owners4.4Finalize development opportunities for personnel5.0Plan curriculum35.1Identify improvement options to addressdevelopment needs5.2Stakeholders ensure that development candidatesare trained in the need areas6.0Develop coaching program5Build into organization duringimplementation phase6.1Create personal development instrument todetermine employee's strengths and developmentopportunities6.2Launch a coaching programInit. ID#ORG04 - Customer Development Initiative:Develop Performance Measures1.0Review corporate mission, vision, strategies, andKPIs 2Information from Strategyarticulation and KPI session1.1Confirm that overall corporate strategy issupported by new process design2.0Set performance targets for CustomerDevelopment, Marketing, and Customer Service 20Focus groups from keystakeholders2.1Align customer needs and develop objectives2.2Align targets to critical process flows2.3Develop performance measures that aremeasurable, actionable, linked to objectives,controllable, simple, credible, and integrated2.4Review effective performance measures fromother organizations2.5Prioritize the performance measures2.6Ensure that performance measures are balancedwith respect to cost, quality, and time2.7Review first draft of measures with stakeholders3.0Identify performance barriers53.1Identify skills, attitudes, and behaviors3.2Confirm clarity of roles3.3Determine communication effectiveness4.0Overcome performance barriers54.1Assign responsibility for overcoming barriers4.2Develop action plans to overcome barriers4.3Implement continuous learning plan4.4Leadership development4.5Develop communication model5.0Finalize performance measures with stakeholders55.1Gain consensus, and refine if necessaryInit. ID#ORG04 - Customer DevelopmentInitiative:Develop Performance Measures6.0Determine tools to monitor and evaluate10performance6.1Track results vs. targets6.2Manage future performance6.3Take corrective action7.0Reward and coach107.1Review existing performance appraisals7.2Integrate new performance measures intoappraisal process7.3Reward and incent desired behaviors7.4Review the coaching process for effectiveness7.5Develop recruiting and selection process criteria8.0Conduct cross-functional working sessions to5refine performance measures and developconsensus9.0Compensation review20Primary involvement from HR9.1Review existing compensation practices Key Account Mgrs, E/W MgrsW&R, Inside Sales people,DSMs, VP CD9.2Review Best Practices/alternatives9.3Design new compensation plans9.4Review with stakeholders9.5Determine transition plan9.6Roll-out。