2019年互联网造车新势力蔚来汽车分析报告

造车新势力之蔚来市场情况与产品情况分析

Auto Pilot 自动监测停车位是否符合泊车

结论

检测停车位时间长, 实现条件和要求高, 改进空间很大

自动辅助 导航驾驶

允许车辆在特定条件下按照导航规划的路径实现自动进 出高速公路匝道功能,可以实现主动超车、并线、巡航 行驶等功能(20年4月推出)

车辆自动驶入驶出高速公路匝道或立 交桥岔路口功能,能在行驶中超过行 驶缓慢的车辆(19年5月推出)

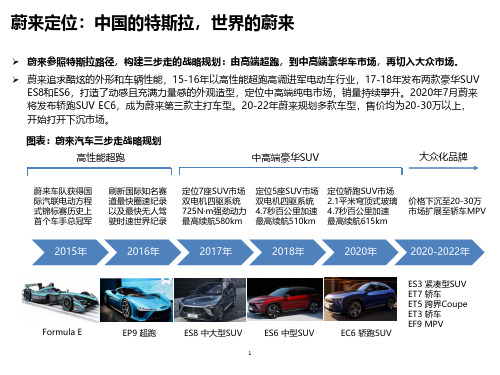

定位轿跑SUV市场 2.1平米穹顶式玻璃 4.7秒百公里加速 最高续航615km

价格下沉至20-30万 市场扩展至轿车MPV

2015年

2016年

2017年

2018年

2020年

2020-2022年

Formula E

EP9 超跑

ES8 中大型SUV

ES6 中型SUV

1

EC6 轿跑SUV

ES3 紧凑型SUV ET7 轿车 ET5 跨界Coupe ET3 轿车 EF9 MPV

术副总裁。

2

图表:蔚来主要投资者

李斌 联想

刘强东 腾讯

高瓴资本红杉李想 资本顺为高举高打(1):研发投资巨大,打造电动车核心技术

➢ 前期研发投资巨大,20年有所收缩。蔚来高举高打,从设计、结构到辅助驾驶系统都是自主研发完成,因 此前期研发中大量投入, 17-19年研发投入26/40/44亿,其中18Q4单季度高达15亿元,20年以来蔚来在 设计开发上的费用投入有所收缩,Q1研发投入为5.22亿元,同比-51.58%,创历史新低。

特斯拉技术领先1年以 上

召唤功能

可通过手机APP控制车辆前后移动一定距离,特定场景下 控制车辆行驶至车主所在的或指定的

方便上下车和停泊(尚未推出)

位置,可以按需躲避障碍物和停车。

蔚来客户调研分析报告

蔚来客户调研分析报告根据最近对蔚来(NIO)的客户进行的调研,我们对他们的反馈和意见进行了分析,并撰写了以下报告。

这份报告将提供有关蔚来客户对其产品、服务和品牌的看法,以及他们的购买决策和未来的期望。

1. 产品质量和性能根据调研结果,蔚来客户普遍认为其产品的质量和性能出色。

客户对蔚来的电动汽车的操控、性能和耐久性给予了高度评价。

他们认为蔚来在创新和技术方面的努力是其优势之一,特别是在电池技术和智能驾驶方面。

2. 充电设施和服务蔚来的充电设施和服务也得到了客户的积极反馈。

客户普遍认为蔚来的充电站点覆盖面积广,便于使用,并且充电速度快。

另外,蔚来提供的免费充电服务也受到了客户的欢迎。

然而,一些客户提到了充电点的拥堵问题,呼吁蔚来进一步优化充电网络以提高使用的便捷性。

3. 客户服务和售后支持大部分客户对蔚来的客户服务和售后支持表示满意。

他们认为蔚来的销售代表和工作人员专业且友好,在购车过程中提供了有效的帮助和建议。

同时,蔚来的售后服务响应及时,解决问题的速度也得到了客户的认可。

4. 品牌形象和口碑蔚来在客户中建立了良好的品牌形象和口碑。

调研结果显示,大部分客户对蔚来的品牌认知度很高,并将其与创新、科技和环保等特点联系在一起。

客户普遍对蔚来的品牌形象表示赞赏,并认为它是一个值得信赖的汽车品牌。

5. 购买决策和未来期望调研结果显示,客户购买蔚来的主要原因是其产品的性能和环保特点。

他们认为蔚来的电动汽车是一种具有未来感和可持续发展的购车选择。

此外,客户还希望蔚来继续加强技术创新,提升电池续航里程,并进一步改善充电设施以满足日益增长的用户需求。

综上所述,蔚来的客户调研分析显示出客户对其产品质量、性能、充电设施、客户服务和品牌形象的满意度较高。

然而,为了进一步满足客户的需求,蔚来应不断改进充电网络,加强技术创新,提高产品的竞争力,并与客户保持良好的沟通和关系,以维持其在市场的领先地位。

蔚来调研报告

蔚来调研报告蔚来是中国新能源汽车制造商,成立于2014年。

作为一家中国民族品牌,蔚来致力于推动车辆电动化和智能化,并为用户提供更加绿色、智能、高效的出行解决方案。

以下是对蔚来的调研报告。

蔚来在新能源汽车市场的竞争力不断增强。

根据国内汽车销售数据,蔚来在2021年完成了超过10万辆的销量,超过了多个传统汽车制造商。

蔚来的市场份额持续增长,其中引人注目的是其产品的高品质和技术创新。

蔚来智能汽车的研发技术十分先进。

蔚来在电动汽车技术、智能驾驶技术以及电池技术等方面都有出色表现。

蔚来的电动汽车拥有长续航里程和强大的动力系统,可满足用户对性能和续航的需求。

同时,智能驾驶技术使得蔚来的车辆具备自动驾驶的能力,提高了驾驶的安全性和便捷性。

此外,蔚来开发了具有自主知识产权的电池技术,大大提升了电池的安全性和寿命,为用户提供了更好的使用体验。

蔚来在用户体验方面非常注重。

蔚来将用户需求放在首位,致力于提供优质的售后服务和良好的用户体验。

蔚来建立了全国范围内的服务中心和售后网点,为用户提供快速、便捷的服务。

此外,蔚来还为用户提供了智能充电设施和智能汽车应用程序,方便用户进行充电和车辆管理。

蔚来也不断与各大地方政府合作,在城市建设中推广电动汽车和充电设施的使用,为用户创造更便捷的出行环境。

蔚来的市场定位和发展战略也十分明确。

蔚来在产品定位上主打高端市场,为高收入人群提供豪华电动汽车解决方案。

同时,蔚来还推出了更为亲民的产品,如蔚来EC6等,以满足不同消费群体的需求。

蔚来也正在积极开展海外合作,进军全球市场。

蔚来在挑战传统汽车制造商的同时,也在应对来自特斯拉等国际竞争对手的竞争压力。

总体来说,蔚来作为一家新兴的中国新能源汽车制造商,具备强大的技术实力和竞争力。

蔚来的产品质量和用户体验受到了用户的认可,销量不断攀升。

随着政府对新能源汽车的政策支持和消费者环保意识的提高,蔚来有望在未来市场中脱颖而出,并成为中国新能源汽车行业的领军企业。

2019造车新势力模式分析及其对汽车产业的影响

2019 造车新势力模式分析及其对汽车产业的影响转自未来智库2018-12-10 08:16:002015 年起,大量造车新势力开始涌现。

以下是对造车新势力发展模式及其战略影响的分析。

一、新势力与新市场的共鸣新能源乘用车大类下已经形成了两大不同细分市场:消费市场与出行市场。

二者产品属性、服务属性有着较大不同且未来分化有望加大,一定程度上降低了新进入者细分领域突破的难度。

细分市场的分化一方面导致了现有整车巨头在持续优化新能源产品,发力消费市场的同时,纷纷布局出行市场,如上汽整合Evcard 、吉利旗下曹操专车、滴滴大众组建合资公司、众泰福特成立智能出行等;另一方面,造车新势力也在两大市场中做出了选择,如蔚来、奇点、前途等主打消费市场,而车和家、新特等主打出行市场;另外,也有如威马汽车一般,在发布主打消费市场产品的同时,推出出行合作版车型。

整车巨头布局出行市场:电动乘用车与出行服务天然契合,出行市场是新能源乘用车崛起阻力最小的方向,未来运营用车将大规模采用新能源车型。

三年来,这一观点在逐步被产业所验证,但出行市场较之消费市场亦有很多天然的不足。

我们判断,出行市场同样是新造车势力向上突破阻力最小的方向。

但成也萧何败也萧何,制造环节行业护城河尚不清晰。

另一方面,消费市场直面巨头的竞争阻力较大,但有望做出品牌效应,进而影响全产业链价值分配。

1、出行市场:驾乘体验的分离(1)电动车与出行服务天然契合出行服务平台的本质是高效连接运力提供者与运力使用者的撮合平台。

其中,运力的直接提供者可以是车辆提供商(分时租赁公司)、兼职司机、专职司机,也可以是专业的重资产运营用车租赁公司(与专业司机签订租赁协议并负责司机管理,类似于出租车公司的份子钱模式)。

随着运力提供者的逐步专业化,后者有望占到越来越大的份额。

运力供给端成本极度敏感,使用成本方面更低的电动车很快打开市场。

公开资料显示,截至2017 年,滴滴平台之上已有26 万辆新能源车,占纯电动汽车总量接近三分之一。

2019年一季度新能源乘用车市场分析

60秒快速阅读:1、在整体车市不景气的背景下,新能源汽车一季度销量25.3万辆,同比增长116%,但伴随着国六实施、补贴退坡等因素,新能源车市下半年存在不确定性。

2、一季度,比亚迪元EV、北汽新能源EU系列、比亚迪e5是销量三强。

此外,造车新势力销售车型也已达到13款,蔚来ES8处于上牌量第一的位置。

3、从车企角度来看,比亚迪依然是市场最大的玩家,北汽新能源是跟随其后的亚军,吉利、上汽乘用车、长城是新能源销量排行榜上的第二梯队企业。

■新能源行情出挑,后市增速可能放缓今年第一季度,国内中国品牌新能源乘用车累计实现销量25.3万辆,同比去年一季度增长了116%,其中,纯电动车型累计销售20万辆,插电式混合动力车型累计销售5.3万辆,同比增幅分别为151.5%和42.1%。

受国家政策导向和企业产品策略的推动,国内新能源乘用车市场的纯电动车型比重已经接近了80%。

新能源车的这一表现在整体仍处低迷的乘用车市场中显得非常突出。

乘联会数据显示,今年一季度国内乘用车累计零售507.8万辆,同比下降了10.5%;而中汽协数据显示,一季度国内乘用车实现销量526.3万辆,同比下降了13.7%。

今年7月开始,国六排放标准将在各地渐次开始实施,后市一定时期内选择持币观望的消费者会增多,然而,下调增值税又为市场带来了积极因素,各大车纷纷降价让利于消费者进行促销,因此未来整体车市的走向仍将处于多力角逐之中。

与此同时,今年新能源汽车的补贴过渡期也即将结束,行业发展驱动力即将由政策主导转为市场主导。

国际上,中美贸易争端旷日持久、韩国民间呼吁取消对中国产电动汽车的补贴;国内,对纯电动汽车的驾乘安全性、充电便利性、保值水平等的探讨和质疑声也不绝于耳。

在这种复杂的经济与消费环境中,新能源乘用车市场继续保持高歌猛进的不确定性也会进一步增加,增速放缓和阶段性的调整是必然事件。

■新能源车型黑马现身,新势力在售车型13款那么,今年以来国内新能源乘用车市场上,哪些车卖的比较好呢?纯正中国血统的当然首推比亚迪家族。

蔚来汽车发展中存在问题及对策

蔚来汽车发展中存在问题及对策蔚来汽车是一家中国新能源汽车公司,成立于2014年,并于2018年在美国上市。

蔚来汽车在电动汽车领域取得了一定的成就,但同时也面临着一些问题。

以下是蔚来汽车发展中存在的问题及对策。

1.建设充电基础设施不足充电基础设施是电动汽车普及的关键。

蔚来汽车在中国建设了一定数量的充电桩,但仍远远不足以满足用户的需求。

对策是加快充电基础设施的建设,与充电设施提供商合作,提高充电桩的建设速度和数量。

2.续航里程短电动汽车的续航里程是用户选择的重要指标。

蔚来汽车的续航里程相对较短,无法满足长途驾驶需求。

对策是提升蔚来汽车的续航里程,研发更高效的电池技术,或者引入更多充电站,以便用户在行程中进行充电。

3.产品价格高昂蔚来汽车的产品定位高端市场,价格相对较高,无法满足普通消费者的需求。

对策是研发更多价格亲民的产品,打造更多入门级的电动汽车,以吸引更多消费者购买。

4.售后服务不完善蔚来汽车的售后服务存在一定的问题。

用户反映,在售后保养、维修和配件供应方面存在不便。

对策是加强售后服务体系建设,培训更多的维修技术人员,提高维修服务的质量,确保用户的售后需求得到及时满足。

5.市场竞争压力大蔚来汽车面临着来自国内外众多电动汽车品牌的竞争,如特斯拉、小鹏汽车等。

对策是加强研发创新,提升产品和技术的竞争力,同时加大市场营销力度,提升品牌知名度,树立蔚来汽车在电动汽车领域的领导地位。

6.公共充电桩不统一在中国,公共充电桩的接口和支付方式多样化,用户使用不便。

对策是积极参与制定充电标准,推动不同充电桩的互联互通,提供更加便捷的充电服务,同时与支付平台合作,提供更多支付方式,方便用户使用。

总之,蔚来汽车在发展中面临诸多问题,包括充电基础设施不足、续航里程短、产品价格高昂、售后服务不完善、市场竞争压力大和公共充电桩不统一等。

为解决这些问题,蔚来汽车需要加快充电基础设施建设,提升续航里程,研发更多价格亲民的产品,提升售后服务质量,加强研发创新,加大市场营销力度,并推动充电标准、支付方式的统一化,提供更加便捷的充电服务。

蔚来汽车竞争力分析

蔚来汽车竞争力分析介绍本文档旨在对蔚来汽车的竞争力进行分析。

蔚来汽车是中国的一家新能源汽车制造商,致力于推动电动汽车的发展。

通过对蔚来汽车的市场地位、品牌优势、技术创新和战略规划进行分析,我们可以了解蔚来汽车在竞争激烈的汽车市场中的优势和挑战。

市场地位蔚来汽车是中国新能源汽车市场的领先品牌之一。

根据最新的销售数据,蔚来汽车在中国新能源汽车市场的销售占有率稳定增长。

同时,蔚来汽车还计划扩大其市场份额,进军国际市场,提升其全球竞争力。

品牌优势蔚来汽车建立了强大的品牌形象。

蔚来汽车在设计和制造方面注重品质和创新,并提供高端电动汽车产品。

消费者对蔚来汽车的品牌印象较好,对其产品的质量和性能有很高的期望。

技术创新蔚来汽车在技术创新方面具有竞争优势。

该公司专注于新能源汽车技术的研发和创新,并在电池技术、自动驾驶技术和智能互联技术方面取得了显著进展。

蔚来汽车致力于提供更安全、更智能的驾驶体验,不断推动整个行业的创新发展。

战略规划蔚来汽车的战略规划着眼于未来的可持续发展。

该公司计划在产品线扩展、全球市场拓展和生态系统建设等方面进行投资和发展。

蔚来汽车还推出了一系列战略合作伙伴关系,以增强其在新能源汽车领域的竞争力。

挑战与展望尽管蔚来汽车在竞争激烈的汽车市场中有着一定的竞争优势,但它仍面临着一些挑战。

包括市场竞争的加剧、技术创新的速度和成本控制等方面的挑战。

然而,蔚来汽车凭借其市场地位、品牌优势和技术创新能力,有望在未来保持竞争力,并成为新能源汽车领域的领军企业。

结论蔚来汽车在竞争力分析中展示出了其在新能源汽车市场的优势与挑战。

通过不断的技术创新和战略规划,蔚来汽车有望进一步巩固其市场地位,并在全球范围内扩大其影响力。

然而,蔚来汽车也需要应对市场竞争和技术快速发展的挑战,以保持其竞争优势。

蔚来汽车竞争优势分析

蔚来汽车竞争优势分析

蔚来汽车是中国一家新能源汽车制造商,致力于提供高品质、

高性能和智能化的电动汽车。

蔚来汽车在竞争激烈的汽车市场中具

有一定的竞争优势。

技术创新是蔚来汽车的重要竞争优势之一。

作为一家新能源汽

车制造商,蔚来汽车在电动汽车领域进行了大量的技术研发,并取

得了一系列的创新成果。

例如,蔚来汽车推出了可更换式电池技术,解决了传统充电时间长、续航里程短的问题,大幅提高了电动汽车

的使用便利性和续航能力。

此外,蔚来汽车还大力发展自动驾驶技术,通过引入人工智能和大数据分析,提升了汽车的安全性和智能

化水平,赢得了消费者的青睐。

品牌形象是蔚来汽车的另一个竞争优势。

蔚来汽车注重品牌营

销和推广,并与众多知名品牌进行合作,提高了品牌的知名度和影

响力。

蔚来汽车在产品设计和外观上也非常注重细节,形成了独特

的品牌风格和辨识度。

这些创新的设计和突出的品牌形象使蔚来汽

车在市场竞争中具有一定的竞争力。

供应链管理是蔚来汽车的另一个竞争优势。

蔚来汽车建立了完善的供应链网络和合作伙伴关系,并通过有效管理和优化供应链,提高了生产效率和成本控制能力。

这使得蔚来汽车能够更好地满足市场需求并提供具有竞争力的产品和服务。

综上所述,蔚来汽车在技术创新、品牌形象和供应链管理等方面具有竞争优势。

随着新能源汽车市场的不断发展和竞争加剧,蔚来汽车需要继续加大创新力度,提高产品质量和服务水平,以保持竞争优势并赢得更多市场份额。

蔚来企业结构分析报告论文

蔚来企业结构分析报告论文1.引言1.1 概述概述蔚来企业是中国领先的新能源汽车制造商,其创立于2014年,总部位于上海。

作为新能源汽车行业的领军企业,蔚来致力于提供高品质的电动汽车和创新的智能交通解决方案。

本报告旨在对蔚来企业的结构进行深入分析,以揭示其组织架构、管理层及特点,并评价其现有结构,展望其未来发展方向。

通过本报告的撰写,我们希望能够为蔚来企业的发展提供有益的参考和建议。

1.2 文章结构文章结构部分的内容:本论文将主要从三个方面对蔚来企业的结构进行分析,分别是蔚来企业背景分析、蔚来企业组织结构分析和蔚来企业管理层分析。

在蔚来企业背景分析部分,将分析蔚来企业的发展历程、市场定位和竞争优势;在蔚来企业组织结构分析部分,将深入探讨蔚来企业的组织架构、部门设置和工作流程;在蔚来企业管理层分析部分,将对蔚来企业的高管团队成员进行介绍,并分析其管理风格和决策能力。

通过对这三个方面的分析,可以更全面地了解蔚来企业的结构特点和运营模式,为对蔚来企业的结构评价和未来发展展望提供有力支持。

1.3 目的本报告的目的在于对蔚来企业的结构进行深入分析,旨在全面了解蔚来企业在组织架构、管理层和企业特点方面的特点和优势,并对其进行评价。

通过对蔚来企业结构的分析,可以帮助我们更好地理解该企业的运营模式和管理方式,为投资者、管理者和相关研究人员提供参考和借鉴。

同时,本报告也旨在展望蔚来企业结构的发展趋势,指出可能存在的问题和改进的方向,为蔚来企业未来的发展提供建议和指导。

通过本报告的撰写,希望能够对蔚来企业的发展和未来走向有所贡献。

2.正文2.1 蔚来企业背景分析蔚来是一家在中国成立的汽车制造公司,成立于2014年,总部位于上海。

公司创立的初衷是生产和销售电动汽车以及相关的电池交换服务。

蔚来公司的目标是成为世界领先的汽车制造商,致力于推动电动汽车的发展。

蔚来在短短几年内就取得了巨大的成功,成为了中国电动汽车市场的领军者之一。

新能源与智能并行剖析蔚来ES在中国市场的优劣特点

新能源与智能并行剖析蔚来ES在中国市场的优劣特点随着全球对环境问题的关注日益增加,新能源汽车作为传统燃油汽车的替代品,逐渐成为汽车产业的热点。

在中国市场上,蔚来ES作为一款新能源智能汽车,备受关注。

本文将对蔚来ES在中国市场上的优劣特点进行剖析。

一、新能源汽车的优势新能源汽车以电能驱动为特点,相较于传统燃油汽车,具有以下优势。

1. 环保节能:新能源汽车采用电能作为驱动,不会产生尾气排放,并且电动机的效率更高,可以更好地利用能源,从而减少能源的消耗,减少空气污染。

2. 低运营成本:相较于传统燃油汽车,新能源汽车的能源成本更低。

以蔚来ES为例,其使用电能作为能源,相比于传统燃油车的油费,更为经济。

3. 噪音更低:新能源汽车采用电动驱动,噪音较低,可以提供更为舒适的驾驶环境。

二、蔚来ES的优势作为一款新能源智能汽车,蔚来ES在中国市场上具有以下优势。

1. 高续航里程:蔚来ES采用了先进的电池技术,拥有较高的续航里程。

其在一次充电下能行驶的里程数比一些竞争对手更远,满足了用户对长途驾驶的需求。

2. 智能化驾驶体验:蔚来ES搭载了先进的智能驾驶辅助系统,包括自动驾驶、自动泊车、智能导航等功能,提升了驾驶体验和安全性。

3. 丰富的服务和充电网络:蔚来公司在中国建立了完善的充电网络,用户可以便捷地进行充电,并在相关的应用上享受到丰富的在线服务。

4. 创新设计和良好的品质:蔚来ES以其独特的设计风格和出色的品质获得了用户的认可。

其外观造型时尚动感,内部配置精致舒适,全方位提升了驾乘体验。

三、蔚来ES的劣势虽然蔚来ES在中国市场上具备了许多优势,但也存在一些劣势。

1. 充电基础设施不完善:尽管蔚来公司在中国建立了一定数量的充电桩,但在全国范围内的充电基础设施还相对不完善。

这给用户在长途驾驶时可能带来一定的不便。

2. 价格相对较高:作为一款新能源智能汽车,蔚来ES的价格相对较高,对于一些普通消费者来说可能有一定的门槛。

蔚来财务评价分析报告(3篇)

第1篇一、引言蔚来(NIO)作为中国新能源汽车行业的领军企业,自成立以来,凭借其独特的品牌定位、创新的技术和优质的服务,在市场上赢得了较高的知名度和市场份额。

本报告将对蔚来公司的财务状况进行深入分析,旨在评估其财务健康状况、盈利能力、偿债能力以及发展潜力。

二、蔚来公司概况蔚来成立于2014年,总部位于中国上海,是一家专注于研发、生产和销售高性能、智能化电动汽车的企业。

蔚来产品线包括蔚来ES8、蔚来ES6和蔚来EC6等车型,同时提供电池换电、充电服务等增值服务。

截至2023,蔚来在全球范围内已拥有超过30,000名员工,产品销售覆盖中国、美国、欧洲等市场。

三、财务评价分析(一)财务状况分析1. 资产负债表分析(1)资产结构分析截至2023年12月31日,蔚来总资产为人民币2,686.42亿元,其中流动资产为人民币1,331.86亿元,非流动资产为人民币1,354.56亿元。

流动资产中,货币资金为人民币47.69亿元,占总流动资产的3.58%;应收账款为人民币92.31亿元,占总流动资产的6.89%;存货为人民币706.42亿元,占总流动资产的53.16%。

非流动资产中,固定资产为人民币335.74亿元,占总非流动资产的24.77%;无形资产为人民币616.92亿元,占总非流动资产的45.63%。

(2)负债结构分析截至2023年12月31日,蔚来总负债为人民币1,905.85亿元,其中流动负债为人民币1,514.85亿元,非流动负债为人民币389.95亿元。

流动负债中,短期借款为人民币14.93亿元,占总流动负债的0.99%;应付账款为人民币548.93亿元,占总流动负债的36.35%。

非流动负债中,长期借款为人民币227.14亿元,占总非流动负债的58.44%。

2. 利润表分析(1)收入分析截至2023年12月31日,蔚来营业收入为人民币633.54亿元,同比增长70.7%。

其中,汽车销售收入为人民币596.47亿元,同比增长71.2%;服务及其他收入为人民币37.07亿元,同比增长63.9%。

蔚来 NIO 2019年第二季度财报

NIO Inc. Reports Unaudited Second Quarter 2019 Financial ResultsSeptember 24, 2019Quarterly Total Revenues reached RMB1,508.6 million (US$219.7 million)Quarterly Deliveries of the ES8 and the ES61were 3,553 vehiclesSHANGHAI, China, Sept. 24, 2019 (GLOBE NEWSWIRE) -- NIO Inc. (“NIO” or the “Company”) (NYSE: NIO), a pioneer in China’s premium electric vehicle market, today announced its unaudited financial results for the second quarter ended June 30, 2019.Operating Highlights for the Second Quarter of 2019Deliveries of the ES8 were 3,140 in the second quarter of 2019, compared with 3,989 vehicles delivered in the firstquarter of 2019.Deliveries of the ES6 reached 413 in the second quarter of 2019.Key Operating Results2019 Q22019 Q1DeliveriesES83,1403,989ES6413—Total3,5533,989Financial Highlights for the Second Quarter of 2019Vehicle sales were RMB1,414.5 million (US$206.1 million) in the second quarter of 2019, representing a decrease of7.9% from the first quarter of 2019.Vehicle margin2 was negative 24.1%, compared with negative 7.2% in the first quarter of 2019. Excluding accrued recall costs, vehicle margin in the second quarter was negative 4.0%.Total revenues were RMB1,508.6 million (US$219.7 million) in the second quarter of 2019, representing a decrease of7.5% from the first quarter of 2019.Gross margin was negative 33.4%, compared with negative 13.4% in the first quarter of 2019. Excluding accrued recall costs, gross margin in the second quarter was negative 10.9%.Loss from operations was RMB3,226.1 million (US$469.9 million) in the second quarter of 2019, representing anincrease of 23.2% from the first quarter of 2019 and a 72.1% increase from the same period of 2018. Excluding accrued recall costs and expenses, loss from operations in the second quarter was RMB2,869.7 million (US$418.0 million).Excluding share-based compensation expenses, adjusted loss from operations (non-GAAP) was RMB3,133.9 million(US$456.5 million) in the second quarter of 2019, representing an increase of 25.5% from the first quarter of 2019 and a73.0% increase from the same period of 2018.Net loss was RMB3,285.8 million (US$478.6 million) in the second quarter of 2019, representing an increase of 25.2% from the first quarter of 2019 and an 83.1% increase from the same period of 2018. Excluding share-based compensation expenses, adjusted net loss (non-GAAP) was RMB3,193.6 million (US$465.2 million) in the second quarter of 2019,representing an increase of 27.5% from the first quarter of 2019 and an 84.5% increase from the same period of 2018.Net loss attributable to NIO’s ordinary shareholders was RMB3,313.7 million (US$482.7 million) in the second quarter of 2019, representing an increase of 24.9% from the first quarter of 2019 and a decrease of 45.8% from the same period of 2018. Excluding share-based compensation expenses and accretion on redeemable non-controlling interests toredemption value, adjusted net loss attributable to NIO’s ordinary shareholders (non-GAAP) was RMB3,189.9 million (US$464.7 million).Basic and diluted net loss per American depositary share (ADS)3 were both RMB3.23 (US$0.47) in the second quarter of 2019. Excluding share-based compensation expenses and accretion on redeemable non-controlling interests toredemption value, adjusted basic and diluted net loss per ADS (non-GAAP) were both RMB3.11 (US$0.45).Cash and cash equivalents, restricted cash and short-term investment were RMB3,455.6 million (US$503.4 million) as of June 30, 2019.Key Financial Results(in RMB million, except for per ordinary sharedata and percentage)2019 Q22019 Q12018 Q2% Change4QoQ YoY Vehicle Sales1,414.5 1,535.2 44.4 -7.9%3,086.0% Vehicle Margin-24.1%-7.2%-317.9%-16.9%293.8% Total Revenues1,508.6 1,631.2 46.0 -7.5%3,180.1% Gross Margin-33.4% -13.4%-333.1%-20.0%299.7% Loss from Operations(3,226.1)(2,617.7)(1,875.0)23.2%72.1% Adjusted Loss from Operations (non-GAAP)(3,133.9)(2,498.1)(1,811.5)25.5%73.0% Net Loss(3,285.8)(2,623.6)(1,794.5)25.2%83.1% Adjusted Net Loss (non-GAAP)(3,193.6)(2,504.0)(1,731.1)27.5%84.5% Net Loss Attributable to Ordinary Shareholders(3,313.7)(2,652.0)(6,110.6)24.9%-45.8% Net Loss per Ordinary Share-Basic and Diluted(3.23)(2.56)(204.93)25.9%-98.4% Adjusted Net Loss per Ordinary Share-Basic andDiluted (non-GAAP)(3.11)(2.42)(57.82)28.5%-94.6%Recent DevelopmentsDeliveries in July and August 2019Deliveries in July were 837 vehicles, consisting of 164 ES8s and 673 ES6s. Deliveries during the month were impacted by the Company’s voluntary battery recall for 4,803 ES8s, as the Company prioritized battery manufacturing capacity which significantly affected production and deliveries.Deliveries in August were 1,943 vehicles, consisting of 146 ES8s and 1,797 ES6s, and representing 132.1% sequential improvement.Convertible Note Subscription Agreements with Tencent and Bin LiThe Company has entered into convertible note subscription agreements with an affiliate of Tencent Holdings Limited(“Tencent”) and Mr. Bin Li, chairman and chief executive officer of the Company (together with Tencent, the “Investors”), pursuant to which NIO will issue and sell convertible notes (“Notes”) in an aggregate principal amount of US$200 million to the Investors through a private placement. Consummation of the placement of the Notes is subject to satisfaction ofcustomary closing conditions and is expected to close before the end of September.Tencent and Mr. Li will each subscribe for US$100 million principal amount of the convertible notes, each in two equally split tranches. The Notes issued in the first tranche will mature in 360 days, bear no interest, and require the Company to pay a premium at 2% of the principal amount at maturity. The Notes issued in the second tranche will mature in threeyears, bear no interest, and require the Company to pay a premium at 6% of the principal amount at maturity. The 360-day Notes will be convertible into Class A Ordinary Shares (or ADSs) of the Company at a conversion price of US$2.98 per ADS at the holder’s option from the 15th day immediately prior to maturity, and the 3-year Notes will be convertible into Class A Ordinary Shares (or ADSs) of the Company at a conversion price of US$3.12 per ADS at the holder’s option from the first anniversary of the issuance date. The holders of the 3-year Notes will have the right to require the Company to repurchase for cash all of the Notes or any portion thereof on February 1, 2022.CEO Comments“During the second quarter of 2019, we delivered a total of 3,553 ES8 and ES6 vehicles. This was followed by 837 units in July and 1,943 units in August, bringing our total aggregate deliveries to 21,670 as of August 31, 2019,” said William Bin Li, founder, chairman and chief executive officer of NIO. “Our ES6, the Company’s 5-seater high-performance premium electric SUV, beganrolling off the production line in June, and we are ramping up the production and deliveries for the coming months. In an environment of softer macro-economic and auto market conditions, we continue to work hard to expand our market penetration. Starting in October, we will begin delivering the ES6 and ES8 with an 84-kWh battery pack, extending their NEDC driving range to 510 km and 430 km, respectively. Going forward, we will continue to enhance sales by strengthening our value proposition through technology advancement.”“In response to the overall tempered market conditions, we are also working hard to maximize returns on our resources and have implemented comprehensive efficiency and cost control measures across the organization. These measures aim to further improve efficiency and streamline operations within our sales and service network and R&D activities. We target to reduce our global headcount to be around 7,800 by the end of the third quarter from over 9,900 in January 2019, and aim to further pursue a leaner operation through additional restructuring and spinning off some non-core businesses by year end,” Mr. Li concluded.Financial Results for the Second Quarter of 2019RevenuesVehicle sales in the second quarter of 2019 were RMB1,414.5 million (US$206.1 million), representing a decrease of7.9% from the first quarter of 2019. The decrease in vehicle sales over the first quarter of 2019 was mainly due to thedecrease in sales volume in the second quarter of 2019 caused by the electric vehicle (EV) subsidy reduction announced in late March and the slowdown of macro-economic conditions in China which has been exacerbated by the US-China trade war.Other sales in the second quarter of 2019 were RMB94.0 million (US$13.7 million), representing a decrease of 2.0% from the first quarter of 2019. The decrease in other sales over the first quarter of 2019 was mainly attributed to the salesdecline in charging piles, in line with the decline in vehicle sales.Total revenues in the second quarter of 2019 were RMB1,508.6 million (US$219.7 million), representing a decrease of7.5% from the first quarter of 2019.Cost of Sales and Gross MarginCost of sales in the second quarter of 2019 was RMB2,012.8 million (US$293.2 million), representing an increase of 8.8% from the first quarter of 2019. The increase in cost of sales over the first quarter of 2019 was mainly caused by accrued recall costs in relation to the Company’s voluntary recall of 4,803 vehicles announced on June 27, 2019. Total recall costs accrued in the second quarter of 2019 were RMB339.1 (US$49.4 million), including RMB283.3 million (US$41.3 million) recorded in cost of vehicle sales and RMB55.8 million (US$8.1 million) recorded in cost of other sales, respectively.Excluding accrued recall costs, cost of sales in the second quarter was RMB1,673.7 million (US$243.8 million),representing a decrease of 9.6% from the first quarter of 2019.Vehicle margin in the second quarter of 2019 was negative 24.1%, compared with negative 7.2% in the first quarter of 2019. The decrease of vehicle margin was mainly driven by the accrued recall costs in relation to the Company’s voluntary recall of 4,803 vehicles announced on June 27, 2019. Excluding accrued recall costs, vehicle margin in the second quarter was negative 4.0%.Gross margin in the second quarter of 2019 was negative 33.4%, compared with negative 13.4% in the first quarter of 2019, which was mainly influenced by the decrease of vehicle margin. Excluding accrued recall costs, gross margin in the second quarter was negative 10.9%.Operating ExpensesResearch and development expenses in the second quarter of 2019 were RMB1,300.5 million (US$189.4 million),representing an increase of 20.6% from the first quarter of 2019 and an increase of 70.0% from the second quarter of2018. Excluding share-based compensation expenses, adjusted research and development expenses (non-GAAP) were RMB1,281.7 million (US$186.7 million), representing an increase of 22.5% from the first quarter of 2019 and an increase of68.3% from the second quarter of 2018. The increase in research and development expenses over the first quarter of 2019was primarily attributed to increased rigorous testing activities of ES6 before its mass production in the second quarter of 2019.Selling, general and administrative expenses in the second quarter of 2019 were RMB1,421.4 million (US$207.0million), representing an increase of 7.7% from the first quarter of 2019 and an increase of 48.6% from the second quarter of 2018. Excluding share-based compensation expenses, adjusted selling, general and administrative expenses(non-GAAP) were RMB1,351.3 million (US$196.8 million), representing an increase of 9.5% from the first quarter of 2019 and an increase of 50.7% from the second quarter of 2018. The increase in selling, general and administrative expensesover the first quarter of 2019 was primarily driven by the Company’s marketing expenditure on the Shanghai auto show and ES6 test drive campaign in the second quarter.Loss from OperationsLoss from operations in the second quarter of 2019 was RMB3,226.1 million (US$469.9 million), representing anincrease of 23.2% from the first quarter of 2019 and an increase of 72.1% from the second quarter of 2018. Excluding accrued recall costs and expenses, loss from operations in the second quarter was RMB2,869.7 million (US$418.0 million).Excluding share-based compensation expenses, adjusted loss from operations (non-GAAP) was RMB3,133.9 million(US$456.5 million), representing an increase of 25.5% from the first quarter of 2019 and an increase of 73.0% from the second quarter of 2018.Share-based Compensation ExpensesShare-based compensation expenses in the second quarter of 2019 were RMB92.2 million (US$13.4 million),representing a decrease of 22.9% from the first quarter of 2019 and an increase of 45.3% from the second quarter of2018. The decrease in share-based compensation expenses over the first quarter of 2019 was primarily due to the part of the share-based compensation expenses that are recognized using the accelerated method, under which the expenses decrease gradually over the vesting period.Net Loss and Earnings Per ShareNet loss was RMB3,285.8 million (US$478.6 million) in the second quarter of 2019, representing an increase of 25.2% from the first quarter of 2019 and an increase of 83.1% from the second quarter of 2018. Excluding share-basedcompensation expenses, adjusted net loss (non-GAAP) was RMB3,193.6 million (US$465.2 million) in the second quarter of 2019, representing an increase of 27.5% from the first quarter of 2019 and an increase of 84.5% from the secondquarter of 2018.Net loss attributable to NIO’s ordinary shareholders in the second quarter of 2019 was RMB3,313.7 million (US$482.7 million), representing an increase of 24.9% from the first quarter of 2019 and a decrease of 45.8% from the second quarter of 2018. Excluding share-based compensation expenses and accretion on redeemable non-controlling interests toredemption value, adjusted net loss attributable to NIO’s ordinary shareholders (non-GAAP) was RMB3,189.9 million(US$464.7 million).Basic and diluted net loss per ADS in the second quarter of 2019 were both RMB3.23 (US$0.47). Excludingshare-based compensation expenses and accretion on redeemable non-controlling interests to redemption value, adjusted basic and diluted net loss per ADS (non-GAAP) were both RMB3.11 (US$0.45).Balance SheetsBalance of cash and cash equivalents, restricted cash and short-term investment was RMB3,455.6 million(US$503.4 million) as of June 30, 2019.On January 1, 2019, the Company adopted ASC 842, Leases and used the additional transition method to initially apply this new lease standard at the adoption date. Right-of-use assets and lease liabilities were recognized on the Company's consolidated financial statements.Business OutlookFor the third quarter of 2019, the Company expects:Deliveries of vehicles to be between 4,200 and 4,400 units, representing an increase of approximately 18.2% to 23.8% from the second quarter of 2019.Total revenues to be between RMB1,593 million (US$232.0 million) and RMB1,663million (US$242.2 million), representing an increase by approximately 5.6% to 10.3% from the second quarter of 2019.This business outlook reflects the Company’s current and preliminary view on the business situation and market condition, which is subject to change.Conference CallManagement will not hold its previously scheduled second quarter 2019 earnings conference call at 8:00 a.m. Eastern Time today, Tuesday, September 24, 2019 (8:00 p.m. Beijing Time on September 24, 2019).About NIO Inc.NIO Inc. is a pioneer in China’s premium electric vehicle market. Founded in November 2014, NIO’s mission is to shape a joyful lifestyle by offering premium smart electric vehicles and being the best user enterprise. NIO designs, jointly manufactures, and sells smart and connected premium electric vehicles,driving innovations in next generation technologies in connectivity, autonomous driving and artificial intelligence. Redefining the user experience, NIO provides users with comprehensive, convenient and innovative charging solutions and other user-centric services. NIO began deliveries of the ES8, a 7-seater high-performance premium electric SUV in China in June 2018, and its variant, the six-seater ES8, in March 2019. NIO officially launched the ES6, a 5-seater high-performance premium electric SUV, in December 2018 and began deliveries in June 2019.Safe Harbor StatementThis press release contains statements that may constitute “forward-looking” statements pursuant to the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. These forward-looking statements can be identified by terminology such as “will,” “expects,” “anticipates,” “aims,” “future,” “intends,” “plans,” “believes,” “estimates,” “likely to” and similar statements. Among other things, the Business Outlook and quotations from management in this announcement, as well as NIO’s strategic and operational plans, contain forward-looking statements. NIO may also make written or oral forward-looking statements in its periodic reports to the U.S. Securities and Exchange Commission (the “SEC”), in its annual report to shareholders, in press releases and other written materials and in oral statements made by its officers, directors or employees to third parties. Statements that are not historical facts, including statements about NIO’s beliefs, plans and expectations, are forward-looking statements. Forward-looking statements involve inherent risks and uncertainties. A number of factors could cause actual results to differ materially from those contained in any forward-looking statement, including but not limited to the following: NIO’s strategies; NIO’s future business development, financial condition and results of operations; NIO’s ability to develop and manufacture a car of sufficient quality and appeal to customers on schedule and on a large scale; its ability to grow manufacturing in collaboration with partners; its ability to provide convenient charging solutions to our customers; its ability to satisfy the mandated safety standards relating to motor vehicles; its ability to secure supply of raw materials or other components used in our vehicles; its ability to secure sufficient reservations and sales of the ES8 and ES6; its ability to control costs associated with our operations; its ability to build our NIO brand; general economic and business conditions globally and in China and assumptions underlying or related to any of the foregoing. Further information regarding these and other risks is included in NIO’s filings with the SEC. All information provided in this press release is as of the date of this press release, and NIO does not undertake any obligation to update any forward-looking statement, except as required under applicable law.Non-GAAP DisclosureThe Company uses non-GAAP measures, such as adjusted cost of sales (non-GAAP), adjusted research and development expenses(non-GAAP),adjusted selling,general and administrative expenses(non-GAAP),adjusted loss from operations (non-GAAP), adjusted net loss (non-GAAP), adjusted net loss attributable to ordinary shareholders (non-GAAP), adjusted basic and diluted net loss per share (non-GAAP) and adjusted basic and diluted net loss per ADS (non-GAAP), in evaluating its operating results and for financial and operational decision-making purposes.By excluding the impact of share-based compensation expenses, accretion on convertible redeemable preferred shares to redemption value and accretion on redeemable non-controlling interests to redemption value,the Company believes that the non-GAAP financial measures help identify underlying trends in its business and enhance the overall understanding of the Company’s past performance and future prospects. The Company also believes that the non-GAAP financial measures allow for greater visibility with respect to key metrics used by the Company’s management in its financial and operational decision-making.The non-GAAP financial measures are not presented in accordance with U.S. GAAP and may be different from non-GAAP methods of accounting and reporting used by other companies. The non-GAAP financial measures have limitations as analytical tools and when assessing the Company’s operating performance,investors should not consider them in isolation,or as a substitute for net loss or other consolidated statements of comprehensive loss data prepared in accordance with U.S. GAAP. The Company encourages investors and others to review its financial information in its entirety and not rely on a single financial measure.The Company mitigates these limitations by reconciling the non-GAAP financial measures to the most comparable U.S. GAAP performance measures, all of which should be considered when evaluating the Company’s performance.For more information on the non-GAAP financial measures, please see the table captioned “Unaudited Reconciliation of GAAP and Non-GAAP Results” set forth at the end of this press release.Exchange RateThis announcement contains translations of certain Renminbi amounts into U.S.dollars at specified rates solely for the convenience of the reader. Unless otherwise stated, all translations from Renminbi to U.S. dollars were made at the rate of RMB6.8650 to US$1.00, the noon buying rate in effect on June 28, 2019 in the H.10 statistical release of the Federal Reserve Board. The Company makes no representation that the Renminbi or U.S. dollars amounts referred could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all.Statement Regarding Preliminary Unaudited Financial InformationThe unaudited financial information set out in this earnings release is preliminary and subject to potential adjustments. Adjustments to the consolidated financial statements may be identified when audit work has been performed for the Company’s year-end audit, which could result in significant differences from this preliminary unaudited financial information.For more information, please visit: Contacts:NIO Inc.Investor RelationsTel: +86-21-6908-3681Email: ir@The Piacente Group, Inc.Brandi PiacenteTel: +1-212-481-2050Email: nio@Ross WarnerTel: +86-10-6508-0677Email: nio@Source: NIONIO INC.Consolidated Balance SheetsAmounts expressed in Renminbi (“RMB”), unless otherwise stated(in thousands, except for share and per share data)December 31, 2018June 30,2019June 30,2019(audited)(unaudited)(unaudited)(US$) ASSETSCurrent assets:Cash and cash equivalents3,133,8472,352,277342,648 Restricted cash57,01283,30012,134 Short-term investment5,154,7031,020,000148,580 Trade receivable756,5081,253,019182,523 Amounts due from related parties88,06653,3247,768 Inventory1,465,2391,390,696202,578 Prepayments and other current assets1,514,2571,842,886268,447Total current assets12,169,6327,995,5021,164,678Non-current assets:Long-term restricted cash33,52820,6083,002 Property, plant and equipment, net4,853,1575,612,717817,583 Intangible assets, net3,4702,839414 Land use rights, net213,662211,23830,770 Long-term investments148,303178,07425,939 Amounts due from related parties7,9707,9701,161 Right-of-use assets - operating lease—2,299,433334,950 Other non-current assets1,412,8301,874,537273,057Total non-current assets6,672,92010,207,4161,486,876 Total assets18,842,55218,202,9182,651,554LIABILITIESCurrent liabilities:Short-term borrowings1,870,0001,477,600215,237 Trade payable2,869,9532,059,674300,025 Amounts due to related parties219,583350,87951,111 Taxes payable51,31740,0035,827 Current portion of operating lease liabilities—524,67576,428 Current portion of long-term borrowings198,852291,70742,492 Accruals and other liabilities3,383,6813,501,979510,121Total current liabilities8,593,3868,246,5171,201,241Non-current liabilities:Long-term borrowings1,168,0126,514,508948,945 Non-current operating lease liabilities—1,932,100281,442 Other non-current liabilities930,8121,053,533153,464Total non-current liabilities2,098,8249,500,1411,383,851 Total liabilities10,692,21017,746,6582,585,092NIO INC.Consolidated Balance SheetsAmounts expressed in Renminbi (“RMB”), unless otherwise stated(in thousands, except for share and per share data)December 31, 2018June 30,2019June 30,2019(audited)(unaudited)(unaudited)(US$) MEZZANINE EQUITYRedeemable non-controlling interests1,329,197 1,391,972 202,764Total mezzanine equity1,329,197 1,391,972 202,764SHAREHOLDERS’ EQUITYOrdinary shares1,809 1,818 265 Treasury shares(9,186)——Additional paid in capital41,918,936 40,208,643 5,857,049 Accumulated other comprehensive loss(34,708)(165,432)(24,098) Accumulated deficit(35,039,810)(41,005,495)(5,973,124)Total NIO Inc. shareholders’ equity6,837,041 (960,466)(139,908) Non-controlling interests(15,896)24,754 3,606 Total shareholders’ equity6,821,145 (935,712)(136,302) Total liabilities, mezzanine equity and shareholders’ equity18,842,552 18,202,918 2,651,554NIO INC.Consolidated Statements of Comprehensive LossAmounts expressed in Renminbi (“RMB”), unless otherwise stated(in thousands, except for share and per share data)Three Months EndedJune 30, 2018March 31,2019June 30, 2019June 30, 2019(unaudited)(unaudited)(unaudited)(unaudited)(US$) Revenues:Vehicle sales44,399 1,535,190 1,414,533 206,050 Other sales1,592 95,971 94,037 13,698 Total revenues45,991 1,631,161 1,508,570 219,748 Cost of sales:Vehicle sales(185,531)(1,645,189)(1,755,017)(255,647) Other sales(13,648)(205,273)(257,737)(37,544) Total cost of sales(199,179)(1,850,462)(2,012,754)(293,191) Gross loss(153,188)(219,301)(504,184)(73,443) Operating expenses:Research and development(765,205)(1,078,448)(1,300,531)(189,444) Selling, general and administrative(956,568)(1,319,937)(1,421,392)(207,049)Total operating expenses(1,721,773)(2,398,385)(2,721,923)(396,493)Loss from operations(1,874,961)(2,617,686)(3,226,107)(469,936)Interest income21,128 62,738 46,519 6,776 Interest expenses(14,442)(68,118)(96,884)(14,113) Share of (losses)/income of equity investees(6,525)2,112 (28,214)(4,110)Other income/(loss), net82,778 (1,324)22,600 3,292 Loss before income tax expense(1,792,022)(2,622,278)(3,282,086)(478,091) Income tax expense(2,485)(1,341)(3,679)(536)Net loss(1,794,507)(2,623,619)(3,285,765)(478,627)Accretion on convertible redeemable preferred shares to redemptionvalue(4,323,154)———Accretion on redeemable non-controlling interests to redemptionvalue—(31,214)(31,561)(4,597) Net loss attributable to non-controlling interests7,036 2,804 3,670 535Net loss attributable to ordinary shareholders of NIO Inc.(6,110,625)(2,652,029)(3,313,656)(482,689)Net loss(1,794,507)(2,623,619)(3,285,765)(478,627) Other comprehensive (loss)/incomeForeign currency translation adjustment, net of nil tax1,217 (60,585)(70,139)(10,217) Total other comprehensive (loss)/income1,217 (60,585)(70,139)(10,217) Total comprehensive loss(1,793,290)(2,684,204)(3,355,904)(488,844)Accretion on convertible redeemable preferred shares to redemptionvalue(4,323,154)———Accretion on redeemable non-controlling interests to redemptionvalue—(31,214)(31,561)(4,597) Net loss attributable to non-controlling interests7,036 2,804 3,670 535Comprehensive loss attributable to ordinary shareholders ofNIO Inc.(6,109,408)(2,712,614)(3,383,795)(492,906)Weighted average number of ordinary shares used incomputing net loss per shareBasic and diluted29,818,067 1,034,648,189 1,026,505,444 1,026,505,444 Net loss per share attributable to ordinary shareholdersBasic and diluted(204.93)(2.56)(3.23)(0.47) Weighted average number of ADS used in computing netloss per shareBasic and diluted—1,034,648,189 1,026,505,444 1,026,505,444 Net loss per ADS attributable to ordinary shareholdersBasic and diluted—(2.56)(3.23)(0.47)NIO INC.Unaudited Reconciliation of GAAP and Non-GAAP ResultsAmounts expressed in Renminbi (“RMB”), unless otherwise stated(in thousands, except for share and per share data)。

【汽车】蔚来汽车公司经营情况分析

【汽车】蔚来汽车公司经营情况分析蔚来汽车公司经营情况分析 o 本文:零壹财经 xx 年 11 月,蔚来汽车在中国 ___创立,与同年诞生的小鹏汽车以及次年诞生的威马汽车等新能源汽车企业一道成为了“中国造车 ___”。

蔚来汽车从诞生之初就选择了跟特斯拉一样的策略,自上而下地推出产品,先是推出自己的高端车型,再逐步下探至中低端市场,因此蔚来汽车被部分人称为“中国版特斯拉”。

蔚来汽车由 ___、刘强东、李想、腾讯、高瓴资本、顺为资本等互联网企业、投资机构和企业家联合创立,并获得淡马锡、百度资本、红杉资本、厚朴、IDG、联想集团等数十家知名机构的投资,5 年内就在纽交所成功上市,彼时市场对蔚来汽车的前景十分乐观。

2018 年是蔚来汽车的巅峰之年,但进入 20XX 年后,这家车企的情况似乎开始急转直下。

糟糕的销售业绩、股价的大幅缩水以及巨额的亏损让蔚来汽车深陷财务泥潭,大家讨论这家车企的前景时更多 ___的已经是它还能撑多久? 9 月 24 日蔚来汽车发布 20XX 年第二季度财报,有分析表示这是蔚来汽车上市以来表现最糟糕的一个季度,蔚来并没有如预期一样交出一份让人满意的答卷,引起投资者恐慌性地抛售。

如今蔚来汽车的总市值仅剩16 亿美元,其股价比 IPO 时的 ___下跌去了 75.2%,较股价最高点减少了84.6%。

最新交付数据:挺不过最新交付数据:挺不过 20XX 第四季度?第四季度?10 月 8 日蔚来汽车公布了 20XX 年第三季度的交付数据,数据显示第三季度蔚来汽车共交付 4799 辆新能源汽车,其中包括 4196 辆 ES6和 603 辆 ES8。

与去年同期相比,第三季度的交付量增长了 46.9%;与 20XX 年第二季度相比,第三季度的交付量增长了35.1%。

表 1:蔚来汽车交付量与营收:蔚来汽车第三季度交付量报告如上表所示,在蔚来汽车第三季度的新车交付中,近 9 成的交付量是由ES6 型号贡献的。

蔚来汽车的工作总结怎么写

蔚来汽车的工作总结怎么写

蔚来汽车的工作总结。

蔚来汽车作为中国新能源汽车领域的领军企业,一直致力于研发、生产和销售

高品质的电动汽车。

在过去的一年里,蔚来汽车取得了许多令人瞩目的成就,为此我们进行了一次工作总结。

首先,蔚来汽车在产品研发方面取得了显著进展。

公司不断加大对新技术的研

发投入,推出了一系列高性能、高续航里程的电动汽车产品,受到了市场和消费者的广泛认可。

同时,蔚来汽车还在自动驾驶技术方面取得了重大突破,为未来的智能出行奠定了坚实基础。

其次,蔚来汽车在销售和营销方面也取得了令人瞩目的成绩。

公司通过多种渠

道扩大了产品的销售网络,提高了品牌知名度。

同时,蔚来汽车还开展了一系列的营销活动,吸引了大量消费者的关注和购买欲望。

此外,蔚来汽车在客户服务方面也表现出色。

公司建立了完善的售后服务体系,为消费者提供了全方位的服务保障。

同时,蔚来汽车还不断改进产品质量,提高了用户满意度和口碑。

总的来说,蔚来汽车在过去一年里取得了许多成绩,但也面临着一些挑战。

我

们相信,在公司领导和全体员工的共同努力下,蔚来汽车一定能够迎接更多的挑战,取得更大的成功。

2019-2020新能源汽车行业品牌企业蔚来调研分析报告

2019-2020新能源汽车行业品牌企业蔚来调研分析报告2019年10月1、蔚来——造车新势力先行者 (6)2、公司亮点 (11)2.1 、高端纯电SUV 市场前景可期 (11)2.2 、ES8/ES6 先发优势明确 (12)2.3 、技术研发持续储备 (14)3、公司潜在风险 (17)3.1 、补贴政策波动,销量/毛利率爬坡承压 (17)3.2 、行业竞争加剧,或弱化现有先发优势 (19)3.3 、融资需求 (22)4、盈利预测 (26)5、估值水平与投资评级 (27)6、风险分析 (28)图1:公司股权结构 (6)图2:公司发展历程 (6)图3:公司已发布车型及未来车型规划 (7)图4:ES8 月交付量数据 (7)图5:“线上+线下”直销模式 (9)图6:蔚来充电体系NIO Power (10)图7:蔚来服务体系NIO Service (10)图8:2012-2019 前5 月国内新能源汽车销量分拆 (11)图9:2012-2019 前5 月国内新能源汽车销量同比增速 (11)图10:2013-2019 前5 月传统燃油乘用车销量分拆 (12)图11:2019 前4 月国内新能源汽车销量分拆 (12)图12:2019 年前4 月国内传统燃油乘用车按品牌分拆 (12)图13:2019 年前4 月国内新能源汽车按品牌分拆 (12)图14:截止目前中国汽车市场主要新能源纯电SUV 定位及MSRP (13)图15:ES8 主要亮点 (14)图16:蔚来ES8 零部件供应商清单 (15)图17:2011-2021E 国内新能源汽车销量与同比增速 (15)图18:2011-2021E 国内新能源汽车渗透率 (15)图19:特斯拉国产化进程 (19)图20:主要造车新势力量产车车型、定价及开始交付时间 (21)图21:1Q19 全球前十大新能源汽车品牌销量vs.蔚来 (21)图22:2Q18-1Q19E 的公司营业成本分拆 (21)图23:2Q18-4Q21E 蔚来销量与汽车业务毛利率 (21)图24:2016-1Q19 Non-GAAP 研发费用占收入比例 (21)图25:2018 Non-GAAP 研发费用分拆 (21)图26:2016-1Q19 Non-GAAP SG&A 费用占收入比例 (21)图27:2018 Non-GAAP SG&A 费用分拆 (21)图28:2018-2021E 公司车型销量与同比增速 (26)图29:2018-2021E 公司收入与同比增速 (26)图30:2018-2021E 公司毛利率 (26)图31:2017-2021E Non-GAAP 归母净亏损与收入占比 (26)图32:蔚来上市至今vs. 特斯拉上市至今的不同发展阶段的PS 估值比较 (28)表1:蔚来与整车厂合作情况 (8)表2:蔚来生产基地布局 (8)表3:造车新势力普遍选择直销模式进行汽车销售 (9)表4:ES8/ES6 与对标高端豪华电动SUV 车型价格/性能比较 (13)表5:蔚来ES8 与部分主流车型关键零部件供应商对比 (14)表6:Mobileye 已发布的视觉芯片参数,ES8 为第一款搭载EyeQ4 车型 (16)表7:SAE 汽车自动驾驶分类 (16)表8:蔚来NIO Pilot 和特斯拉Auto Pilot 比较 (17)表9:2013-2019 中国新能源乘用车国家补贴政策 (17)表10:2018-2019 百公里电耗量的动态补贴标准 (17)表11:2018-2019 动力电池系统能量密度的动态补贴标准 (17)表12:2018 vs. 2019 年补贴政策对蔚来ES8/ ES6 购车成本影响分析 (18)表13:蔚来ES8/ES6 与特斯拉Model 3(国产)的比较 (19)表14:各主要品牌新能源汽车上市规划 (20)表15:公司银行授信及借款细节 (25)表16:公司历次股权融资、可转债、以及少数股东注资情况 (25)表17:可比公司估值表 (27)1、蔚来——造车新势力先行者蔚来成立于2014 年,为国内高端纯电动汽车制造商。

蔚来行业报告

蔚来行业报告蔚来是中国新能源汽车领域的领军企业之一,成立于2014年,总部位于上海。

蔚来致力于推动汽车行业的电动化和智能化发展,以及提供全面的出行解决方案。

本报告将对蔚来所在的新能源汽车行业进行分析,包括市场现状、竞争对手、发展趋势等方面的内容。

一、市场现状。

随着全球对环境保护和可持续发展的重视,新能源汽车市场逐渐崛起。

中国作为全球最大的汽车市场,也在积极推动新能源汽车的发展。

根据统计数据显示,2019年中国新能源汽车销量达到了143万辆,同比增长了3.1%。

而2020年受到新冠疫情的影响,整体汽车市场销量出现下滑,但新能源汽车却表现抢眼,销量同比增长了8.4%。

可以看出,新能源汽车市场具有巨大的发展潜力。

在这个市场中,蔚来作为新能源汽车企业的领军者之一,一直在不断创新和发展。

截至2021年底,蔚来已经在中国境内拥有超过100家直营门店,覆盖了全国30多个城市。

同时,蔚来还在欧洲市场进行了布局,计划在未来进军更多的海外市场。

可以说,蔚来在新能源汽车市场的地位已经较为稳固。

二、竞争对手。

在新能源汽车市场中,蔚来的竞争对手主要包括特斯拉、小鹏汽车、理想汽车等。

特斯拉作为全球新能源汽车领域的领军者,一直以来都是蔚来的主要竞争对手。

特斯拉凭借其先进的技术和强大的品牌影响力,一直在市场上占据着较大的份额。

小鹏汽车和理想汽车则是近年来崛起的新势力,它们也在新能源汽车市场上展现出了强大的竞争力。

在面对激烈的市场竞争时,蔚来不断加大研发投入,推出了一系列具有竞争力的新产品,如蔚来ES8、ES6、EC6等车型,以及蔚来的电池交换技术。

这些新产品和技术的推出,有力地提升了蔚来在市场上的竞争力。

三、发展趋势。

未来,新能源汽车市场将继续保持高速增长的态势。

政府对新能源汽车的政策支持力度不断增加,这将进一步刺激新能源汽车市场的发展。

同时,随着技术的不断进步和成本的不断下降,新能源汽车的性能和价格将会更加吸引消费者。

因此,新能源汽车市场具有很大的发展潜力。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2019年互联网造车新势力蔚来汽车分析报告

2019年8月

目录

一、最具竞争力的互联网造车新势力 (4)

1、生产端全铝车身精益求精,技术品控优良 (4)

(1)蔚来汽车是我国自主品牌第一条全铝生产线 (4)

(2)区别于传统制造商,客户可以进行定制化生产 (4)

(3)零库存及订金式生产有效减小资金压力 (5)

2、销售端注重用户生态搭建,中心地段建店,APP生态模式替代广告 (6)

(1)蔚来汽车采用直营模式 (6)

二、ES8销量靓丽,七座车差异化竞争取胜 (9)

1、2018年ES8位列新势力造车销量第一,在豪华品牌中位列第二 (9)

2、ES6针对五座车,市场空间打开期待再辉煌 (10)

三、盈利预测 (13)

四、主要风险 (14)

1、行业竞争加剧的风险 (14)

2、业绩的不确定性 (14)

ES6的陆续交付为公司带来新增长点。

区别于传统汽车生产、销售、服务各环节,蔚来以全新模式推进新能源汽车发展。

蔚来汽车采用定制化生产模式满足了客户不同类型要求,同时减轻企业资金成本压力。

一站式体验店区别于传统4S 店销售模式。

新公司打造新模式带来新期待。

预计公司2019~2021年收入分别为93亿元、107亿元、118亿元,同比增速为+65%、+15%、+10%,2019~2021年净利润分别为-103亿元、-59亿元、-23亿元,公司短期内无法实现盈利。

公司是互联网造车新势力,聚焦智能互联的高端电动汽车。

蔚来以电动赛车起家,具有一流的电动动力总成技术,可提供卓越的加速性能;公司开发了领先的NIO Pilot ADAS 自动辅助驾驶系统和NOMI 人工智能助手,并已大规模应用。

区别于传统汽车及4S店销售模式,蔚来汽车打造一站式全面服务:公司以汽车为核心,通过连接汽车、智能设备(手机、充电桩等),服务提供商和用户,以实现更高效和创新的用户体验,打造差异化竞争路线。

7座车细分市场寻求突破,打造差异化竞争。

根据机动车交强险数据,蔚来主打车型ES82018年全年上险11404辆,位列国内新一代新能源车车企销量榜首,同时售价也是竞品SUV中最高的,说明ES8的主要竞争对手并不是国内的新一代新能源车车企。

7座SUV及MPV 整体销量不及5座SUV,说明市场需求仍向五座SUV倾斜,凭借着优秀的产品力,蔚来新五座SUV ES6的表现更值得期待。

一、最具竞争力的互联网造车新势力

1、生产端全铝车身精益求精,技术品控优良

(1)蔚来汽车是我国自主品牌第一条全铝生产线

定位智能互联的高端电动汽车:公司以电动赛车起家,具有一流的电动动力总成技术,可提供卓越的加速性能;公司开发了领先的NIO Pilot ADAS 自动辅助驾驶系统和NOMI 人工智能助手,并已实现在生产汽车ES8、ES6上大规模应用。

蔚来汽车目前与江淮汽车合作建厂进行生产,工厂于2016年10

月动工,总投资额超过100亿元,2017年下半年正式投入使用,仅用了13个月便完成了年规划产能10万台的工厂的建造,其生产线也是中国三条全铝生产线之一,同时也是中国自主品牌的第一条全铝生产线。

(2)区别于传统制造商,客户可以进行定制化生产

不同于传统主流车企的库存化销售方式,蔚来目前主推的ES8以及ES6车型均采用全定制化生产模式,是国内唯一一家进行个性化定制的新能源车品牌。

客户可以通过手机APP 或者直营门店个性化选。