经济学原理(英文)第13章 曼昆

曼昆微观经济学chapter13

0

Production function

1

2

3

4

5Number of Workers Hired

Copyright © 2019 South-Western

The Production Function

● Diminishing Marginal Product

Copyright © 2006 Nelson, a division of Thomson Canada Ltd.

Total Revenue, Total Cost, and Profit

● Total Revenue

The amount a firm receives for the sale of its output.

Copyright © 2006 Nelson, a division of Thomson Canada Ltd.

The Production Function

● Diminishing Marginal Product

Diminishing marginal product is the property whereby the marginal product of an input declines as the quantity of the input increases. • Example: As more and more workers are hired at a firm, each additional worker contributes less and less to production because the firm has a limited amount of equipment.

曼昆微观经济学chapter13讲义资料

Copyright © 2006 Nelson, a division of Thomson Canada Ltd.

Fixed and Variable Costs

PART 5

FIRM BEHAVIOR AND THE ORGANIZATION OF INDUSTRY

The Costs of Production

Copyright © 2006 Nelson, a division of Thomson Canada Ltd.

13

Learning Objectives

Copyright © 2006 Nelson, a division of Thomson Canada Ltd.

Figure 1 Economic versus Accountants

How an Economist Views a Firm

How an Accountant Views a Firm

● Total Cost

➢ The market value of the inputs a firm uses in production.

Copyright © 2006 Nelson, a division of Thomson Canada Ltd.

Total Revenue, Total Cost, and Profit

● Accountants measure the accounting profit as the firm’s total revenue minus only the firm’s explicit costs.

曼昆《经济学原理(微观经济学分册)》(第6版)【核心讲义】(第13章 生产成本)

第13章生产成本跨考网独家整理最全经济学考研真题,经济学考研课后习题解析资料库,您可以在这里查阅历年经济学考研真题,经济学考研课后习题,经济学考研参考书等内容,更有跨考考研历年辅导的经济学学哥学姐的经济学考研经验,从前辈中获得的经验对初学者来说是宝贵的财富,这或许能帮你少走弯路,躲开一些陷阱。

以下内容为跨考网独家整理,如您还需更多考研资料,可选择经济学一对一在线咨询进行咨询。

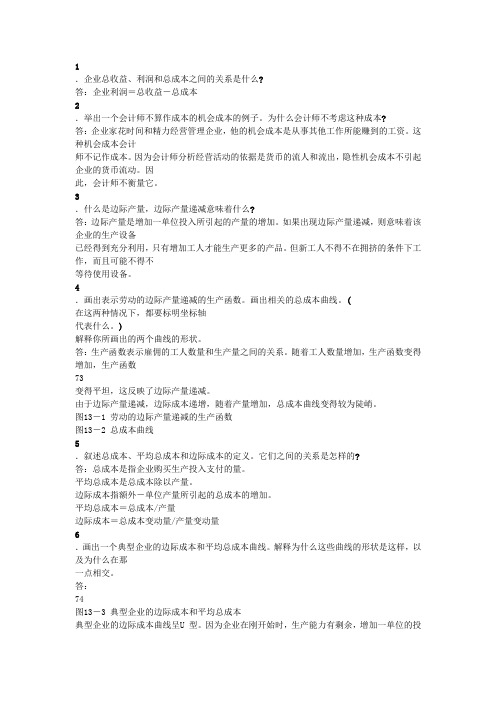

一、成本1.总收益、总成本和利润总收益(total revenue):企业从销售其产品中得到的货币量。

总成本(total cost):企业用于生产的投入品的市场价值。

利润(profit):企业的总收益减去其总成本。

经济学家通常假设,企业的目标是利润最大化,而且这个假设在大多数情况下都能很好地发挥作用。

2.作为机会成本的成本一种东西的机会成本是指为了得到某种东西所必须放弃的所有东西。

当经济学家提到某个企业的生产成本的时候,它们包括该企业生产其物品与劳务的所有机会成本。

显性成本(explicit costs):需要企业支出货币的投入成本。

隐性成本(implicit costs):不需要企业支出货币的投入成本。

经营的总成本是显性成本和隐性成本之和。

经济学家关注于研究企业如何做出生产和定价决策。

由于这些决策既考虑了显性成本又考虑了隐性成本,因此,经济学家在衡量企业的成本时就包括了这两种成本。

与此相反,会计师的工作是记录流入企业和流出企业的货币。

因此,他们衡量显性成本,但往往忽略隐性成本。

3.作为一种机会成本的资本成本几乎每一个企业都有一项重要的隐性成本,那就是已经投资于企业的金融资本的机会成本。

经济学家和会计师以不同的方式来看待和处理成本。

4.经济利润与会计利润由于经济学家和会计师用不同的方法衡量成本,他们也用不同的方法衡量利润。

经济学家衡量企业的经济利润(economic profit),即企业的总收益减去生产所销售物品与劳务的总机会成本(显性的与隐性的)。

曼昆经济学原理英文书

曼昆经济学原理英文书The Economics Principles by MankiwChapter 1: Ten Principles of EconomicsChapter 2: Thinking Like an EconomistChapter 3: Interdependence and the Gains from Trade Chapter 4: The Market Forces of Supply and Demand Chapter 5: Elasticity and Its ApplicationChapter 6: Supply, Demand, and Government Policies Chapter 7: Consumers, Producers, and Efficiency of Markets Chapter 8: Application: The Costs of TaxationChapter 9: Application: International TradeChapter 10: ExternalitiesChapter 11: Public Goods and Common Resources Chapter 12: The Design of the Tax SystemChapter 13: The Costs of ProductionChapter 14: Firms in Competitive MarketsChapter 15: MonopolyChapter 16: Monopolistic CompetitionChapter 17: OligopolyChapter 18: The Markets for Factors of Production Chapter 19: Earnings and DiscriminationChapter 20: Income Inequality and PovertyChapter 21: Introduction to MacroeconomicsChapter 22: Measuring a Nation's IncomeChapter 23: Measuring the Cost of LivingChapter 24: Production and GrowthChapter 25: Saving, Investment, and the Financial System Chapter 26: The Basic Tools of FinanceChapter 27: UnemploymentChapter 28: The Monetary SystemChapter 29: Money Growth and InflationChapter 30: Open-Economy Macroeconomics: Basic Concepts Chapter 31: A Macroeconomic Theory of the Open Economy Chapter 32: Aggregate Demand and Aggregate SupplyChapter 33: The Influence of Monetary and Fiscal Policy on Aggregate DemandChapter 34: The Short-Run Trade-Off between Inflation and UnemploymentChapter 35: The Theory of Consumer ChoiceChapter 36: Frontiers of MicroeconomicsChapter 37: Monopoly and Antitrust PolicyChapter 38: Oligopoly and Game TheoryChapter 39: Externalities, Public Goods, and Environmental Policy Chapter 40: Uncertainty and InformationChapter 41: Aggregate Demand and Aggregate Supply Analysis Chapter 42: Understanding Business CyclesChapter 43: Fiscal PolicyChapter 44: Money, Banking, and Central BankingChapter 45: Monetary PolicyChapter 46: Inflation, Disinflation, and DeflationChapter 47: Exchange Rates and the International Financial SystemChapter 48: The Short - Run Trade - Off between Inflation and Unemployment RevisitedChapter 49: Macroeconomic Policy: Challenges in the Twenty - First CenturyEpilogue: 14 Big IdeasNote: The chapter titles have been abbreviated for simplicity and brevity purposes.。

曼昆经济学原理英文版文案加习题答案13章

221WHAT’S NEW IN THE S EVENTH EDITION:There are no major changes to this chapter.LEARNING OBJECTIVES:By the end of this chapter, students should understand:➢ what items are included in a firm’s costs of production.➢ the link between a f irm’s production process and its total costs.➢ the meaning of average total cost and marginal cost and how they are related.➢ the shape of a typical firm’s cost curves.➢ the relationship between short-run and long-run costs.CONTEXT AND PURPOSE:Chapter 13 is the first chapter in a five-chapter sequence dealing with firm behavior and the organization of industry. It is important that students become comfortable with the material in Chapter 13 because Chapters 14 through 17 are based on the concepts developed in Chapter 13. To be more specific, Chapter 13 develops the cost curves on which firm behavior is based. The remaining chapters in thissection (Chapters 14-17) utilize these cost curves to develop the behavior of firms in a variety of different market structures —competitive, monopolistic, monopolistically competitive, and oligopolistic.The purpose of Chapter 13 is to address the costs of production and develop the firm’s cost curves. These cost curves underlie the firm’s supply curve. In previous chapters, we summarized the firm’s production decisions by starting with the supply curve. While this is suitable for answering manyquestions, it is now necessary to address the costs that underlie the supply curve in order to address the part of economics known as industrial organization —the study of how firms’ decisions about prices and quantities depend on the market conditions they face.KEY POINTS:•The goal of firms is to maximize profit, which equals total revenue minus total cost.THE COSTS OF PRODUCTION13222 ❖Chapter 13/The Costs of Production• When analyzing a firm’s behavior, it is important to include all the opportunity costs of production.Some of the opportunity costs, such as the wages a firm pays its workers, are explicit. Otheropportunity costs, such as the wages the firm owner gives up by working at the firm rather than taking another job, are implicit. Economic profit takes both explicit and implicit costs into account, whereas accounting profits consider only explicit costs.• A firm’s costs reflect its production process. A typical firm’s production function gets flatter as the quantity of an input increases, displaying the property of diminishing marginal product. As a result, a firm’s total-cost curve gets steeper as the quantity produced rises.• A firm’s total costs can be divided between fixed costs and variable costs. Fixed costs are costs that do not change when the firm alters the quantity of output produced. Variable costs are costs that change when the firm alters the quantity of output produced.• From a firm’s total cost, two related measures of cost are derived. Average total cost is total cost divided by the quantity of output. Marginal cost is the amount by which total cost rises if output increases by one unit.• When analyzing firm behavior, it is often useful to graph average total cost and marginal cost. For a typical firm, marginal cost rises with the quantity of output. Average total cost first falls as output increases and then rises as output increases further. The marginal-cost curve always crosses the average-total-cost curve at the minimum of average total cost.• A firm’s costs often depend on the time horizon considered. In particular, many costs are fixed in the short run but variable in the long run. As a result, when the firm changes its level of production, average total cost may rise more in the short run than in the long run.CHAPTER OUTLINE:I. What Are Costs?A. Total Revenue, Total Cost, and Profit1. The goal of a firm is to maximize profit.Chapter 13/The Costs of Production ❖ 2232. Definition of total revenue: the amount a firm receives for the sale of its output.3. Definition of total cost: the market value of the inputs a firm uses in production.4. Definition of profit: total revenue minus total cost.B. Costs as Opportunity Costs1. Principle #2: The cost of something is what you give up to get it.2. The costs of producing an item must include all of the opportunity costs of inputs used inproduction. 3. Total opportunity costs include both implicit and explicit costs.a. Definition of explicit costs: input costs that require an outlay of money by thefirm .b. Definition of implicit costs: input costs that do not require an outlay of moneyby the firm .c. The total cost of a business is the sum of explicit costs and implicit costs.d. This is the major way in which accountants and economists differ in analyzing theperformance of a business. e. Accountants focus on explicit costs, while economists examine both explicit and implicitcosts.C. The Cost of Capital as an Opportunity Cost 1. The opportunity cost of financial capital is an important cost to include in any analysis of firmperformance. 2. Example: Caroline uses $300,000 of her savings to start her firm. It was in a savings accountpaying 5% interest.3. Because Caroline could have earned $15,000 per year on this savings, we must include thisopportunity cost. (Note that an accountant would not count this $15,000 as part of the firm's costs.)224 ❖ Chapter 13/The Costs of Production4. If Caroline had instead borrowed $200,000 from a bank and used $100,000 from her savings,the opportunity cost would not change if the interest rate stayed the same (according to the economist). But the accountant would now count the $10,000 in interest paid for the bank loan.D. Economic Profit versus Accounting Profit1. Figure 1 highlights the differences in the ways in which economists and accountants calculateprofit. 2. Definition of economic profit: total revenue minus total cost, including both explicitand implicit costs .a. Economic profit is what motivates firms to supply goods and services.b. To understand how industries evolve, we need to examine economic profit. 3. Definition of accounting profit: total revenue minus total explicit cost .4. If implicit costs are greater than zero, accounting profit will always exceed economic profit.II. Production and CostsA. The Production Function1. Definition of production function: the relationship between quantity of inputs usedto make a good and the quantity of output of that good.2. Example: Caroline's cookie factory. The size of the factory is assumed to be fixed; Carolinecan vary her output (cookies) only by varying the labor used.Chapter 13/The Costs of Production ❖ 2253. Definition of marginal product: the increase in output that arises from an additionalunit of input.a. As the amount of labor used increases, the marginal product of labor falls.b. Definition of diminishing marginal product: the property whereby the marginalproduct of an input declines as the quantity of the input increases.4. We can draw a graph of the firm's production function by plotting the level of labor (x -axis)against the level of output (y -axis).226 ❖Chapter 13/The Costs of ProductionFigure 2a. The slope of the production function measures marginal product.b. Diminishing marginal product can be seen from the fact that the slope falls as theamount of labor used increases.B. From the Production Function to the Total-Cost Curve1. We can draw a graph of the firm's total cost curve by plotting the level of output (x-axis)against the total cost of producing that output (y-axis).a. The total cost curve gets steeper and steeper as output rises.b. This increase in the slope of the total cost curve is also due to diminishing marginalproduct: As Caroline increases the production of cookies, her kitchen becomesovercrowded, and she needs a lot more labor.Chapter 13/The Costs of Production ❖227III. The Various Measures of CostA. Example: Conrad’s Coffee Shop228 ❖Chapter 13/The Costs of ProductionB. Fixed and Variable Costs1. Definition of fixed costs: costs that do not vary with the quantity of outputproduced.2. Definition of variable costs: costs that do vary with the quantity of output produced.3. Total cost is equal to fixed cost plus variable cost.C. Average and Marginal Cost1. Definition of average total cost: total cost divided by the quantity of output.2. Definition of average fixed cost: fixed costs divided by the quantity of output.3. Definition of average variable cost: variable costs divided by the quantity of output.4. Definition of marginal cost: the increase in total cost that arises from an extra unitof production.Chapter 13/The Costs of Production ❖ 2295. Average total cost tells us the cost of a typical unit of output and marginal cost tells us thecost of an additional unit of output.D. Cost Curves and Their Shapes1. Rising Marginal Costa. This occurs because of diminishing marginal product.b. At a low level of output, there are few workers and a lot of idle equipment. But as outputincreases, the coffee shop gets crowded and the cost of producing another unit of output becomes high.2. U-Shaped Average Total Costa. Average total cost is the sum of average fixed cost and average variable cost.b. AFC declines as output expands and AVC typically increases as output expands. AFC ishigh when output levels are low. As output expands, AFC declines pulling ATC down. As fixed costs get spread over a large number of units, the effect of AFC on ATC falls and ATC begins to rise because of diminishing marginal product. c. Definition of efficient scale: the quantity of output that minimizes average totalcost. 3. The Relationship between Marginal Cost and Average Total Costa. Whenever marginal cost is less than average total cost, average total cost is falling.Whenever marginal cost is greater than average total cost, average total cost is rising.b. The marginal-cost curve crosses the average-total-cost curve at minimum average totalcost (the efficient scale).230 ❖ Chapter 13/The Costs of Production4. Typical Cost Curvesa. Marginal cost eventually rises with output.b. The average-total-cost curve is U-shaped.c. Marginal cost crosses average total cost at the minimum of average total cost.Activity 2—Average and Marginal GradesType: In-class demonstration Topics: Relationship between marginal and average cost Materials needed: None Time: 5 minutes Class limitations: Works in any size classPurposeThis quick exercise uses an analogy to illustrate to students that they already know the relation between marginal values and averages.InstructionsTell the class that two twins (Miley and Hannah) are enrolled in Principles of Economics. They each had a “B” average (GPA = 3.0) before taking the class.Miley gets a “C” in the course. What happens to her GPA?Hannah gets an “A” in the class. What happens to her GPA?Common Answers and Points for DiscussionStudents will likely know that Miley will have a lower GPA and Hannah a higher GPA. A “marginal” grade lower than the average will pull down the average. A “marginal” grade higher than the average will increase the average.The same is true of marginal cost and average costs. If marginal cost is less than average cost, average cost will fall. If marginal cost is higher than average cost, average cost will rise. Figure 5IV. Costs in the Short Run and in the Long RunA. The division of total costs into fixed and variable costs will vary from firm to firm.B. Some costs are fixed in the short run, but all are variable in the long run.1. For example, in the long run a firm could choose the size of its factory.2. Once a factory is chosen, the firm must deal with the short-run costs associated with thatplant size.C. The long-run average-total-cost curve lies along the lowest points of the short-run average-total-cost curves because the firm has more flexibility in the long run to deal with changes in production.D. The long-run average-total-cost curve is typically U-shaped, but is much flatter than a typicalshort-run average-total-cost curve.E. The length of time for a firm to get to the long run will depend on the firm involved.F. Economies and Diseconomies of Scale1. Definition of economies of scale: the property whereby long-run average total costfalls as the quantity of output increases.2. Definition of diseconomies of scale: the property whereby long-run average totalcost rises as the quantity of output increases.3. Definition of constant returns to scale: the property whereby long-run average totalcost stays the same as the quantity of output changes.Figure 6 Emphasize that these cost curves include ALL costs for the resources needed toproduce the good. Thus, both explicit costs and implicit costs are included.4. FYI: Lessons from a Pin Factorya. In The Wealth of Nations, Adam Smith described how specialization in a pin factoryallowed output to be greater than it would have been if each worker attempted toperform many different tasks.b. The use of specialization allows firms to achieve economies of scale.V. Table 3 provides a summary of all of the various cost definitions used throughout this chapter.Table 3SOLUTIONS TO TEXT PROBLEMS:Quick Quizzes1. Farmer McDonald’s opportunity c ost is $300, consisting of 10 hours of lessons at $20 an hourthat he could have been earning plus $100 in seeds. His accountant would only count theexplicit cost of the seeds ($100). If McDonald earns $200 from selling the crops, thenMcDonald earns a $100 accounting profit ($200 sales minus $100 cost of seeds) but incursan economic loss of $100 ($200 sales minus $300 opportunity cost).2. Farmer Jones’s production function is shown in Figure 1 and his total-cost curve is shown inFigure 2. The production function becomes flatter as the number of bags of seeds increasesbecause of the diminishing marginal product of seeds. The total-cost curve gets steeper asthe amount of production increases. This feature is also due to the diminishing marginalproduct of seeds, since each additional bag of seeds generates a lower marginal product, andthus, the cost of producing additional bushels of wheat rises.Figure 1 Figure 23. The average total cost of producing 5 cars is $250,000/5 = $50,000. Since total cost rosefrom $225,000 to $250,000 when output increased from 4 to 5, the marginal cost of the fifthcar is $25,000.The marginal-cost curve and the average-total-cost curve for a typical firm are shown inFigure 3. They cross at the efficient scale because at low levels of output, marginal cost isbelow average total cost, so average total cost is falling. But after the two curves cross,marginal cost rises above average total cost, and average total cost starts to rise. So thepoint of intersection must be the minimum of average total cost.Figure 34. The long-run average total cost of producing 9 planes is $9 million/9 = $1 million. The long-run average total cost of producing 10 planes is $9.5 million/10 = $0.95 million. Since thelong-run average total cost declines as the number of planes increases, Boeing exhibitseconomies of scale.Questions for Review1. The relationship between a firm's total revenue, profit, and total cost is profit equals totalrevenue minus total costs.2. An accountant would not count the owner’s opportunity cost of alternative employment as anaccounting cost. An example is given in the text in which Caroline runs a cookie business, butshe could instead work as a computer programmer. Because she's working in her cookiefactory, she gives up the opportunity to earn $100 per hour as a computer programmer. Theaccountant ignores this opportunity cost because money does not flow into or out of the firm.But the cost is relevant to Caroline’s decision to run the cookie factory.3. Marginal product is the increase in output that arises from an additional unit of input.Diminishing marginal product means that the marginal product of an input declines as thequantity of the input increases.4. Figure 4 shows a production function that exhibits diminishing marginal product of labor.Figure 5 shows the associated total-cost curve. The production function is concave becauseof diminishing marginal product, while the total-cost curve is convex for the same reason.Figure 4 Figure 55. Total cost consists of the costs of all inputs needed to produce a given quantity of output. Itincludes fixed costs and variable costs. Average total cost is the cost of a typical unit ofoutput and is equal to total cost divided by the quantity produced. Marginal cost is the cost of producing an additional unit of output and is equal to the change in total cost divided by the change in quantity. An additional relation between average total cost and marginal cost is that whenever marginal cost is less than average total cost, average total cost is declining;whenever marginal cost is greater than average total cost, average total cost is rising.Figure 66. Figure 6 shows the marginal-cost curve and the average-total-cost curve for a typical firm.There are three main features of these curves: (1) marginal cost is U-shaped but risessharply as output increases; (2) average total cost is U-shaped; and (3) whenever marginal cost is less than average total cost, average total cost is declining; whenever marginal cost is greater than average total cost, average total cost is rising. Marginal cost is increasing for output greater than a certain quantity because of diminishing returns. The average-total-cost curve is downward-sloping initially because the firm is able to spread out fixed costs over additional units. The average-total-cost curve is increasing beyond some output levelbecause as quantity increases, the demand for important variable inputs increases; therefore, the cost of these inputs increases. The marginal-cost and average-total-cost curves intersect at the minimum of average total cost; that quantity is the efficient scale.7. In the long run, a firm can adjust the factors of production that are fixed in the short run; forexample, it can increase the size of its factory. As a result, the long-run average-total-costcurve has a much flatter U-shape than the short-run average-total-cost curve. In addition,the long-run curve lies along the lower envelope of the short-run curves.8. Economies of scale exist when long-run average total cost decreases as the quantity ofoutput increases, which occurs because of specialization among workers. Diseconomies ofscale exist when long-run average total cost rises as the quantity of output increases, whichoccurs because of the coordination problems inherent in a large organization.Quick Check Multiple Choice1. a2. d3. d4. c5. b6. aProblems and Applications1. a. opportunity cost; b. average total cost; c. fixed cost; d. variable cost; e. total cost; f.marginal cost.2. a. The opportunity cost of something is what must be given up to acquire it.b. The opportunity cost of running the hardware store is $550,000, consisting of $500,000to rent the store and buy the stock and a $50,000 implicit cost, because your aunt wouldquit her job as an accountant to run the store. Because the total opportunity cost of$550,000 exceeds the projected revenue of $510,000, your aunt should not open thestore, as her economic profit would be negative.3. a. The following table shows the marginal product of each hour spent fishing:b. Figure 7 graphs the fisherman's production function. The production function becomesflatter as the number of hours spent fishing increases, illustrating diminishing marginalproduct.Figure 7c. The table shows the fixed cost, variable cost, and total cost of fishing. Figure 8 showsthe fisherman's total-cost curve. It has an upward slope because catching additional fish takes additional time. The curve is convex because there are diminishing returns tofishing time because each additional hour spent fishing yields fewer additional fish.Figure 84. Here is the completed table:Workers Output MarginalProduct TotalCostAverageTotal CostMarginalCost0 0 --- $200 --- ---1 20 20 300 $15.00 $5.002 50 30 400 8.00 3.333 90 40 500 5.56 2.504 120 30 600 5.00 3.335 140 20 700 5.00 5.006 150 10 800 5.33 10.007 155 5 900 5.81 20.00a. See the table for marginal product. Marginal product rises at first, then declines becauseof diminishing marginal product.b. See the table for total cost.c. See the table for average total cost. Average total cost is U-shaped. When quantity is low,average total cost declines as quantity rises; when quantity is high, average total costrises as quantity rises.d. See the table for marginal cost. Marginal cost is also U-shaped, but rises steeply asoutput increases. This is due to diminishing marginal product.e. When marginal product is rising, marginal cost is falling, and vice versa.f. When marginal cost is less than average total cost, average total cost is falling; the costof the last unit produced pulls the average down. When marginal cost is greater thanaverage total cost, average total cost is rising; the cost of the last unit produced pushesthe average up.5. At an output level of 600 players, total cost is $180,000 (600 × $300). The total cost ofproducing 601 players is $180,901. Therefore, you should not accept the offer of $550,because the marginal cost of the 601st player is $901.6. a. The fixed cost is $300, because fixed cost equals total cost minus variable cost. At anoutput of zero, the only costs are fixed cost.Marginal cost equals the change in total cost for each additional unit of output. It is also equal to the change in variable cost for each additional unit of output. This relationshipoccurs because total cost equals the sum of variable cost and fixed cost and fixed costdoes not change as the quantity changes. Thus, as quantity increases, the increase intotal cost equals the increase in variable cost.7. The following table illustrates average fixed cost (AFC), average variable cost (AVC), andaverage total cost (ATC) for each quantity. The efficient scale is 4 houses per month,because that minimizes average total cost.Quantity VariableCost FixedCostTotalCostAverageFixed CostAverageVariable CostAverageTotal Cost0 $0.00 $200.00 $200.00 --- --- ---1 10.00 200.00 210.00 $200.00 $10.00 $210.002 20.00 200.00 220.00 100.00 10.00 110.003 40.00 200.00 240.00 66.67 13.33 80.004 80.00 200.00 280.00 50.00 20.00 70.005 160.00 200.00 360.00 40.00 32.00 72.006 320.00 200.00 520.00 33.33 53.33 86.677 640.00 200.00 840.00 28.57 91.43 120.008. a. The lump-sum tax causes an increase in fixed cost. Therefore, as Figure 10 shows, onlyaverage fixed cost and average total cost will be affected.Figure 10b. Refer to Figure 11. Average variable cost, average total cost, and marginal cost will all begreater. Average fixed cost will be unaffected.Figure 119. a. The following table shows average variable cost (AVC), average total cost (ATC), andmarginal cost (MC) for each quantity.Quantity VariableCost TotalCostAverageVariable CostAverageTotal CostMarginalCost0 $0.00 $30.00 --- --- ---1 10.00 40.00 $10.00 $40.00 $10.002 25.00 55.00 12.50 27.50 15.003 45.00 75.00 15.00 25.00 20.004 70.00 100.00 17.50 25.00 25.005 100.00 130.00 20.00 26.00 30.006 135.00 165.00 22.50 27.50 35.00b. Figure 12 shows the three curves. The marginal-cost curve is below the average-total-cost curve when output is less than four and average total cost is declining. Themarginal-cost curve is above the average-total-cost curve when output is above four and average total cost is rising. The marginal-cost curve lies above the average-variable-cost curve.Figure 1210. The following table shows quantity (Q), total cost (TC), and average total cost (ATC) for thethree firms:Firm A Firm B Firm CQuantity TC ATC TC ATC TC ATC1 $60.00 $60.00 $11.00 $11.00 $21.00 $21.002 70.00 35.00 24.00 12.00 34.00 17.003 80.00 26.67 39.00 13.00 49.00 16.334 90.00 22.50 56.00 14.00 66.00 16.505 100.00 20.00 75.00 15.00 85.00 17.006 110.00 18.33 96.00 16.00 106.00 17.677 120.00 17.14 119.00 17.00 129.00 18.43Firm A has economies of scale because average total cost declines as output increases. Firm B has diseconomies of scale because average total cost rises as output rises. Firm C has economies of scale from one to three units of output and diseconomies of scale for levels of output beyond three units.。

曼昆经济学原理课后答案第十三章生产成本

1.企业总收益、利润和总成本之间的关系是什么?答:企业利润=总收益-总成本2.举出一个会计师不算作成本的机会成本的例子。

为什么会计师不考虑这种成本?答:企业家花时间和精力经营管理企业,他的机会成本是从事其他工作所能赚到的工资。

这种机会成本会计师不记作成本。

因为会计师分析经营活动的依据是货币的流人和流出,隐性机会成本不引起企业的货币流动。

因此,会计师不衡量它。

3.什么是边际产量,边际产量递减意味着什么?答:边际产量是增加一单位投入所引起的产量的增加。

如果出现边际产量递减,则意味着该企业的生产设备已经得到充分利用,只有增加工人才能生产更多的产品。

但新工人不得不在拥挤的条件下工作,而且可能不得不等待使用设备。

4.画出表示劳动的边际产量递减的生产函数。

画出相关的总成本曲线。

(在这两种情况下,都要标明坐标轴代表什么。

)解释你所画出的两个曲线的形状。

答:生产函数表示雇佣的工人数量和生产量之间的关系。

随着工人数量增加,生产函数变得增加,生产函数73变得平坦,这反映了边际产量递减。

由于边际产量递减,边际成本递增,随着产量增加,总成本曲线变得较为陡峭。

图13-1 劳动的边际产量递减的生产函数图13-2 总成本曲线5.叙述总成本、平均总成本和边际成本的定义。

它们之间的关系是怎样的?答:总成本是指企业购买生产投入支付的量。

平均总成本是总成本除以产量。

边际成本指额外-单位产量所引起的总成本的增加。

平均总成本=总成本/产量边际成本=总成本变动量/产量变动量6.画出一个典型企业的边际成本和平均总成本曲线。

解释为什么这些曲线的形状是这样,以及为什么在那一点相交。

答:74图13-3 典型企业的边际成本和平均总成本典型企业的边际成本曲线呈U 型。

因为企业在刚开始时,生产能力有剩余,增加一单位的投入量,边际产量会高于前一单位的投入,这样就出现一段边际成本下降。

生产能力全部被利用之后,再增加边际投入,就会出现边际产量递减,边际成本递增。

曼昆《经济学原理》英文版完整讲义丛elasticity

Demand

2. At exactly $4, consumers will buy any quantity.

0 3. At a price below $4, quantity demanded is infinite.

Quantity

Total Revenue and the Price Elasticity of Demand • Total revenue is the amount paid by buyers and

Copyright © 2004 South-Western/Thomson Learning

Computing the Price Elasticity of Demand • The price elasticity of demand is computed as

the percentage change in the quantity demanded divided by the percentage change in price.

formula, would be calculated as:

(10 8)

(10 8) / 2 (2.20 2.00)

22% 2.32 9.5%

(2.00 2.20) / 2

Copyright © 2004 South-Western/Thomson Learning

The Variety of Demand Curves

Demand

0

90 100

Quantity

2. . . . leads to an 11% decrease in quantity demanded.

Figure 1 The Price Elasticity of Demand

微观经济学原理(第七版)-曼昆-名词解释(带英文)

微观经济学原理曼昆名词解释1.需求价格弹性(price elasticity of demand):2.蛛网模型():对于生产周期较长的商品供给的时滞性,需求的不是动态模型分类,画图3.|4.边际效用递减(diminishing marginal utility)——基数效用论不违反边际效用递减规律。

因为边际效用是指物品的消费量每增加(或减少)一个单位所增加(或减少)的总效用的量。

这里的“单位”是指一完整的商品单位,这种完整的商品单位,是边际效用递减规律有效性的前提。

比如,这个定律适用于一双的鞋子,但不适用于单只的鞋子。

对于四轮车而言,必须是有四个轮子的车才成为一单位。

三个轮子不能构成一辆四轮车,因而每个轮子都不是一个有效用的物品,增加一个轮子,才能使车子有用。

因此,不能说第四个轮子的边际效用超过第三个轮子(2)特征:凸向原点越远越大不相交6.边际替代率(marginal rate of :——序数效用论7.预算线(Budget line/ budget constraint)8.吉芬物品(Giffen good):价格上升引起需求量增加的物品。

9.柯布道格拉斯生产函数稀缺性(scarcity):社会资源的有限性。

\经济学(economics):研究社会如何管理自己的稀缺资源。

效率(efficiency):社会能从其稀缺资源中得到最多东西的特性。

平等(equality):经济成果在社会成员中公平分配的特性。

机会成本(opportunity cost):为了得到某种东西所必须放弃的东西。

理性人(rational people):系统而有目的地尽最大努力实现起目标的人。

【边际变动(marginal change):对行动计划微小的增量调整。

激励(incentive):引起一个人做出某种行为的某种东西。

市场经济(market economy):当许多企业和家庭在物品与劳务市场上相互交易时,通过他们的分散决策配置资源的经济。

曼昆经济学原理微观名词解释13(中英)

CHAPTER 13The Costs of Productiontotal revenue: the amount a firm receives for the sale of its output总收益:企业出售其产品所得到的货币量total cost: the market value of the inputs a firm uses in production总成本:企业用于生产的投入品的市场价值profit: total revenue minus total cost利润:总收益减去总成本explicit costs: input costs that require an outlay of money by the firm显性成本:需要企业支出货币的投入成本implicit costs: input costs that do not require an outlay of money by the firm隐性成本:不需要企业支出货币的投入成本economic profit: total revenue minus total cost, including both explicit and implicit costs经济利润:总收益减总成本,包括显性成本与隐性成本accounting profit: total revenue minus total explicit cost会计利润:总收益减总显性成本production function: the relationship between the quantity ofinputs used to make a good and the quantity of output of that good生产函数:用于生产一种物品的投入量与该物品产量之间的关系marginal product: the increase in output that arises from an additional unit of input边际产量:增加一单位投入所引起的产量增加diminishing marginal: product the property whereby the marginal product of an input declines as the quantity of the input increases边际产量递减:一种投入的边际产量随着投入量增加而减少的特征fixed costs: costs that do not vary with the quantity of output produced固定成本:不随着产量变动而变动的成本variable costs: costs that vary with the quantity of output produced可变成本:随着产量变动而变动的成本average total cost: total cost divided by the quantity of output 平均总成本:总成本除以产量average fixed cost: fixed cost divided by the quantity of output 平均固定成本:固定成本除以产量average variable cost: variable cost divided by the quantity of output平均可变成本:可变成本除以产量marginal cost: the increase in total cost that arises from an extra unit of production边际成本:额外一单位产量所引起的总成本的增加efficient scale: the quantity of output that minimizes average total cost有效规模:使平均总成本最小的产量economies of scale: the property whereby long-run average total cost falls as the quantity of output increases规模经济:长期平均总成本随产量增加而减少的特性diseconomies of scale: the property whereby long-run average total cost rises as the quantity of output increases规模不经济:长期平均总成本随产量增加而增加的特性constant returns to scale: the property whereby long-run average total cost stays the same as the quantity of output changes规模收益不变:长期平均总成本在产量变动时保持不变的特性。

经济学原理 Chapter 13

It can be represented by a table, equation, or

graph.

Example 1: • Farmer Jack grows wheat. • He has 5 acres of land. • He can hire as many workers as he wants.

8

The Production Function

A production function shows the relationship

between the quantity of inputs used to produce a good, and the quantity of output of that good.

Comparing them helps Jack decide whether he

would benefit from hiring the worker.

CHAPTER 13

THE COSTS OF PRODUCTION

14

Why MPL Diminishes

Farmer Jack’s output rises by a smaller and

1

In this chapter, look for the answers to these questions: What is a production function? What is marginal

prre the various costs, and how are they

13

The Costs of Production

PRINCIPLES OF

ECONOMICS

《经济学原理·曼昆·第三版》第13章

called industrial organization—the study of how firms’ decisions regarding prices

and quantities depend on the market conditions they face. The town in which you live, for instance, may have several pizzerias but only one cable television company. How does this difference in the number of firms affect the prices in these markets

买面粉花了1000美元

糕点工人的工资

海伦放弃程序员工作(100美元/小时)

13.1.3 作为机会成本的资本成本 Costs as Opportunity Costs

资本成本核算

购买糕点厂的方案

economist 动用储蓄30万元 存款利率5% 动用储蓄10万元,贷款20 万元,存贷利率5% accountant

Prologue

In previous chapters we used the supply curve to summarize firms’ production

decisions. According to the law of supply, firms are willing to produce and sell a

投入总成本 (工厂成本+工人成本) (美元) 30 40 50 60 70

5

150

10

30Байду номын сангаас

曼昆微观经济学ch13

THE COSTS OF PRODUCTION

15

THE COSTS OF PRODUCTION

16

The slope of the production function

measures the marginal product of a worker. As the number of workers increases, the marginal product declines, and the production function becomes flatter.

THE COSTS OF PRODUCTION

2

What Are Costs?

The firm’s objective

The economic goal of the firm is to

maximize profits.

THE COSTS OF PRODUCTION

3

Total Revenue, Total Cost, Profit

工人 数量 0 1 2 3

总成本函数

产量 0 50 90 120

工厂 成本 30 30 30 30

工人 成本 0 10 20 30

总成 本 30 40 50 60

4

5

10 20 30 40 50 60 70

We assume that the size of facቤተ መጻሕፍቲ ባይዱory is fixed

and we can vary the quantity of goods produced only by changing the number of workers. This assumption is realistic in the short run, but not in the long run.

第13章 总供给总需求动态模型

rt

t t*

E t t 1 t*

it t*

产出和实际利率=自然水平 通胀和预期通胀=通胀目标值

名义利率=自然利率+目标通胀率 古典二分法:目标通胀率只影响通 胀率、预期通胀率和名义利率; 货币中性:实际变量(产出和实际 利率)不依赖于货币政策。 动态总供给曲线 短期 两个主要变量的图形: 产出 (横轴) , 通胀率(纵轴) 从 5 个方程推出 2 个变量的方程, 消去 rt ,it ,E t 1t 。 把适应性预期代入菲利普斯曲线

曲线

E t t 1 t

it t t t* Y Yt Yt 货

适应性预期

币政策规则 内生变量 Yt 产出 πt rt it 通胀率 实际利率 名义利率

Et πt+1 预期通胀率

外生变量

Yt

自然产出水平 央行的通胀目标 需求冲击 供给冲击

rt it E t t 1

实际利率=名义利率-预期通胀率。 实际利率是事前实际利率。 利率是 t 和 t+1 之间的回报率。 通胀率是 t-1 和 t 之间价格水平的百 分比变动。 下标表示变量是什么时候决定的。 期望算子下标表示期望形成的时

间。 3.通货膨胀:菲利普斯曲线 通胀由包括预期通胀和供给冲击的 菲利普斯曲线决定:

t t 1 Yt Yt v t DAS

图 13-2

π DASt

Y

DAS 是在过去的通胀率、自然产出 水平和供给冲击给定的情况下做出 的。 动态总需求曲线 需求

Yt Yt rt t

为消除内生变量实际利率,应用费 雪方程,用 it

Yt Yt it Et t 1 t

曼昆《经济学原理第三版》第1-12章(上)微观分册原版中英文双语PPT课件(很经典)

1.人们面临权衡取舍

为了得到我们喜爱的一件东西,我们 通常不得不放弃另一件喜爱的东西。

大炮 vs.黄油 食物 vs. 衣服 休闲 vs. 工作 效率 vs. 平等

作决策时需要在两个目标之间权衡取舍

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Principles of Economics

Third Edition by

N. Gregory Mankiw

经济学原理

(第三版)

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

1

INTRODUCTION 导言

Guns v. butter Food v. clothing Leisure time v. work Efficiency v. equity

Making decisions requires trading off one goal against another.

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Ten Principles of Economics

经济学十大原理

Chapter 1

Economy. . . 经济…

. . . The word economy comes from a Greek word for ―one who manages a household.‖

经济一词来源于希腊语,意思是 “tems and derived items copyright © 2001 by Harcourt, Inc.

经济学原理曼昆课后答案chapter13

经济学原理曼昆课后答案chapter13 Problems and Applicat ions1. a. opportunity cost; b. average total cost; c. fixed cost; d. variable cost; e. total cost;f. marginal cost.2. a. The opportunity cost of something is what must be forgone to acquire it.b. The opportunity cost of running the hardware store is $550,000, consisting of $500,000 to rent the store and buy the stock and a $50,000 opportunity cost,since your aunt would quit her job as an accountant to run the store. Sincethe total opportunity cost of $550,000 exceeds revenue of $510,000, your aunt shouldn't open the store, as her profit would be negative she would losemoney.3. a. Since you'd have to pay for room and board whether you went to college or not, that portion of your college payment is not an opportunity cost.b. The explicit opportunity cost is the cost of tuition.c. An implicit opportunity cost is the cost of your time. You could work at a jobfor pay rather than attend college. The wages you give up represent an opportunity cost of attending college.4. a. The following table shows the marginal product of each hour spent fishing:b. Figure 13-7 graphs the fisherman's production function. The production function becomes flatter as the number of hours spent fishing increases, illustrating diminishing marginal product.Figure 13-7c. The table shows the fixed cost, variable cost, and total cost of fishing. Figure 13-8 shows the fisherman's total-cost curve. It slopes up because catching additional fish takes additional time. The curve is convex because there are diminishing returns to fishing time each additional hour spent fishing yields fewer additional fish.5. Here’s the table of costs:a. See table for marginal product. Marginal product rises at first, then declinesbecause of diminishing marginal product.b. See table for total cost.c. See table for average total cost. Average total cost is U-shaped. Whenquantity is low, average total cost declines as quantity rises; when quantity ishigh, average total cost rises as quantity rises.d. See table for marginal cost. Marginal cost is also U-shaped.e. When marginal product is rising, marginal cost is falling, and vice versa.f. When marginal cost is less than average total cost, average total cost is falling;when marginal cost is greater than average total cost, average total cost isrising.6. Fixed costs include the cost of owning or renting a car to deliver the bagels and thecost of advertising; they're fixed costs because they don't vary with output. Variable costs include the cost of the bagels and gas for the car, sincethose costs will increase as output increases.7. a. The fixed cost is 300, since fixed cost equals total cost minus variable cost. b.Marginal cost equals the change in total cost or the change in variable cost. That's because total cost equals variable cost plus fixed cost and fixed cost doesn't change as the quantity changes. So as quantity increases, the increase in total cost equals the increase in variable cost and both are equal to marginal cost.8. a. The fixed cost of setting up the lemonade stand is $200. The variable cost per cup is 50 cents.Figure 13-9b. The following table shows total cost, average total cost, and marginal cost. These are plotted in Figure 13-9.9. The following table illustrates average fixed cost (AFC), average variable cost (AVC), and average total cost (ATC) for each quantity. The efficient scale is 4 houses per month, since that minimizes average total cost.10. a. The following table shows average variable cost (AVC), average total cost (ATC), and marginal cost (MC) for each quantity.b. Figure 13-10 graphs the three curves. The margi nal cost curve is below the average total cost curve when output is less than 4, as average total cost is declining. The marginal cost curve is above the average total cost curvewhen output is above 4, as average total cost is rising. The marginal costcurve is always above the average variable cost curve, and average variablecost is always increasing.Figure 13-1011. The following table shows quantity (Q), total cost (TC), and average total cost (ATC)for the three firms:Firm A has economies of scale since average total cost declines as output increases.Firm B has diseconomies of scale since average total cost rises as output rises. Firm C has economies of scale for output from 1 to 3, then diseconomies of scale for greater levels of output.。

曼昆《经济学原理》(宏观经济学分册)英文原版

Con ps riin uc d m P eer o e x b if rcae o s g fk o a eo s n td e dr s 1 v0 ic Pr ob ifcae is b nk a ye s ete ar

© 2007 Thomson South-Western

THE CONSUMER PRICE INDEX

• The consumer price index (CPI) is a measure of the overall cost of the goods and services bought by a typical consumer.

© 2007 Thomson South-Western

How the Consumer Price Index Is Calculated • The inflation rate is calculated as follows:

I n f l a t i o n R a t e i n Y e a r 2 = C P I i n Y e a r 2 C P I i n Y e a r 1 1 0 0 C P I i n Y e a r 1

© 2007 Thomson South-Western

How the Consumer Price Index Is Calculated

4. Choose a base year and compute the index.

经济学原理 曼昆 英文

经济学原理曼昆英文1. Economics as a Social Science: In this chapter, the author introduces the study of economics as a social science that explores how individuals, firms, and societies make decisions about resource allocation.2. The Role of Incentives: This chapter explores how individuals respond to incentives and how they influence decision-making in economics. Various types of incentives, such as financial rewards and punishments, are discussed.3. Supply and Demand: The concept of supply and demand is explained in this chapter. It delves into how the interaction between buyers and sellers in a market determines the equilibrium price and quantity of a product.4. Elasticity and Its Applications: Elasticity, a measure of responsiveness, is discussed in this chapter. The various types of elasticity, including price elasticity of demand and income elasticity of demand, are explained and their applications are explored.5. Consumer Choice: This chapter explores how individuals make choices as consumers, considering factors such as preferences, constraints, and budget constraints. Utility theory and indifference curves are introduced as tools to understand consumer choice.6. Production and Costs: The author discusses how firms make decisions regarding production and cost in this chapter. Topics covered include production functions, costs of production, and theconcept of economies of scale.7. Perfect Competition: This chapter explores the characteristics of perfect competition, including the large number of buyers and sellers, homogenous products, and ease of entry and exit. It also examines the implications of perfect competition on market outcomes.8. Monopoly: The concept of monopoly, where a single firm controls the market, is discussed in this chapter. The author analyzes the sources of monopoly power and its implications for prices and output in the market.9. Market Failures and Government Intervention: This chapter examines market failures, situations where the market fails to allocate resources efficiently. Different types of market failures, such as externalities and public goods, are explained, along with the role of government intervention in correcting these failures.10. Externalities: Externalities, or the consequences of economic activities on third parties, are explored in this chapter. The author discusses positive and negative externalities and their implications for resource allocation.11. Public Goods and Common Resources: This chapter focuses on the characteristics of public goods and common resources. It discusses the free-rider problem and the challenges in providing public goods efficiently.12. Markets for Factors of Production: The author explores themarkets for factors of production, including labor and capital, in this chapter. Wage determination, discrimination, and other factors influencing the prices of these factors are analyzed.13. The Economics of Income Inequality: Income inequality and its causes are discussed in this chapter. The author explores different theories and factors that contribute to income inequality, as well as its implications for society and policy considerations.14. The Theory of Consumer Choice: This chapter delves deeper into the theory of consumer choice, examining topics such as consumer preferences, budget constraints, and the concept of utility maximization.15. Frontiers of Microeconomics: The final chapter explores the frontiers of microeconomics, including topics such as behavioral economics, game theory, and the economics of information. The author discusses how these fields have expanded our understanding of economic behavior.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Economic Profit versus Accounting Profit

How an Economist Views a Firm

Economic profit Accounting profit

How an Accountant Views a Firm

Revenue

Implicit costs Total opportunity costs

explicit and implicit costs, the firm earns economic profit.

Economic

profit is smaller than accounting profit.

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

the

relationship between short-run and long-run costs. the meaning of average total cost and marginal cost and how they are related.

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Costs as Opportunity Costs

A firm’s cost of production includes all the opportunity costs of making its output of goods and services.

b. Annual implicit costs: salary foregone: investment income foregone: rent foregone: total implicit costs:

$ 3,600 25,000 10,000 $ 50 x 12 = 600 $ 39,200

The Costs of Production

Chapter 13

Copyright © 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College Publishers, 6277 Sea Harbor Drive, Orlando, Florida 32887-6777.

Explicit costs involve a direct money outlay for factors of production. Implicit costs do not involve a direct money outlay.

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

LEARNING OBJECTIVES:

By the end of this chapter, students should understand:

what

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

a. Annual explicit costs: cost of office equipment: programmer’s salary: hardware heat and light: total explicit costs:

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

A Firm’s Profit

Profit is the firm’s total revenue minus its total cost. Profit = Total revenue - Total cost

A Firm’s Total Revenue and Total Cost

Total

The

Revenue

amount that the firm receives for the sale of its output.

Total

The

Cost

amount that the firm pays to buy inputs.

$ 35,000 $10,000 x .05 = 500 $250x12 = 3,000 $ 38,500

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

c.Congratulations

are not in order since economic profit for the year is $55,000 – ($39,200 + $38,500) = –$22,700.

items are included in a firm’s costs of production. the link between a firm’s production process and its total costs. the shape of a typical firm’s cost curves.

Economic Profit versus Accounting Profit

measure a firm’s economic profit as total revenue minus all the opportunity costs (explicit and implicit). Accountants measure the accounting profit as the firm’s total revenue minus only the firm’s explicit costs. In other words, they ignore the implicit costs.

0 50 90 120 140 150

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

The Production Function

The production function shows the relationship between quantity of inputs used to make a good and the quantity of output of that good.

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

A Production Function and Total Cost

Number of Workers 0 1 2 3 4 5 Output Marginal Product of Labor 50 40 30 20 10 Cost of Factory $30 30 30 30 30 30 Cost of Workers $0 10 20 30 40 50 Total Cost of Inputs $30 40 50 60 70 80

The Costs of Production

The Law of Supply: Firms are willing to produce and sell a greater quantity of a good when the price of the good is high. This results in a supply curve that slopes upward.

Revenue

Explicit costs

Explicit costs

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Exercises

You work for a firm earning $35000 a year. But you like to have your own software Business and cashed in $ 10,000 saving account (i=5% ) and use the money to buy Hardware and software for your business. You also convert a basement apartment in your house, which has been renting for $250 per month, into a work space of your firm. You lease some equipment for $3,600 a year and hire two part time programmers, whose combined salary is $25,000 a year. Office lighting charges is $50 a month. a. What are the total annual explicit costs of your new business? b. What are the total annual implicit costs? c. At the end of the 1st year, your accountant cheerily informs you that your total sales for the year amounted to $ 55,000. She congratulates you on a profitable year. Are her congratulates warranted? Why or why not?