会计 外文翻译

会计外文翻译

Master's thesis, University of LondonInformation technology and accounting management with the use is the relevant value of information analysis and use, and various factors of production based on the value creation of corporate accounting and management contributions to the study of accounting will be the main content. No use of information technology, there is any enterprise information and accounting information to promote the implementation of value chain management will lose technical support, there is no theory of innovation value chain management, accounting, and information technology development, there is no power. In this paper, the meaning of information to start, leads to the meaning of accounting information, accounting information describes the development process, the second part of the analysis of the status quo of accounting information, analysis of its use in theproblems, the third part of the proposed accounting information on the implementation of the strategic analysis.Keywords: accounting, information technology strategyI. Introduction(A) BackgroundThe development of accounting information in China has gone through more than 20 years, accounting information theory and practical application of talent, the accounting information system software has gradually matured, and, and theproduction, supply and marketing, human resources management, cost control and other aspects of the formation of an integrated management information system software. But the company found accounting information in the status of the development of enterprises is extremely uneven, a lot of strength and standardized management of large enterprises have been using the integrated accounting information system "ERP" is the management software, and the introduction of new ideas with the value of the supply chain management chain management system, and also the majority of the total business is still in the initial stage of the use of computerized accounting, or even manually. Enterprise management is still in the coexistence of traditional and modern, our corporate accounting information so early, the senior co-existence of the phenomenon will not surprise. Accounting information must be improved to facilitate the management of change. The essence of the value chain to value chain to implement the core business processes node changes, if companies choose the value chain as the core business process change, business management will enable a major step forward, it promotes corporate accounting development of information technology.(B) SignificanceWhile accounting information in China's time is not long, its nature and content to be further studied, but it is undeniable, with the advent of the information society, accounting, information technology will be an irresistible inevitable trend of the accounting information The current accounting both in theory and in practice will have a huge impact.First, to achieve after the accounting information, accounting information system will truly become a business management information system, a subsystem. The business enterprise is able to automatically capture the enterprise's internal and external information related to accounting, and together with the company's internal accounting information system for real-time processing. Accounting from the limitations of traditional accounting afterwards freed, and thus play a greater management control of accounting functions, business and information so that users can readily use the corporate accounting information to the business of the future financial situation to make a reasonable forecast, management and development of enterprises to make the right decisions. Second, the accounting assumptions, in particular, is no longer the traditional accounting entity with real money and plant business, it will include some of the online virtual companies and network companies,which for the common goal, in short time together, when the completion of specificgoals will soon dissolve, and its continuing operations, accounting, staging and monetary measures the basic premise of all will be affected. Implementation of accounting information, the enterprise network and external networks to achieve the Internet, users of accounting information can always obtain the relevant accounting information. Comprehensive application of information technology has greatly improved the timeliness of the information, the predictive value of information and feedback is also greatly enhance the value of information flow is also much faster, can contribute positively to the improvement of economic management. Other accounting information systems through direct access to relevant data and analysis, reducing theman-made fraud, thus greatly improving the reliability of accounting information and the quality of information.Third, today's accounting software processes basically simulate manual accounting processes and design. Implementation of accounting information, the accounting system is no longer isolated, but with a real-time processing, highly automated system, which with other business systems and external connections, you can directly read data from other systems, and a series of processing, processing, storage and transmission. Accounting reports can also be used for real-time electronic means associated newspaper report, the user can always obtain useful accounting information for decision-making, improve efficiency, promote economic development.21st century will be an information-oriented society, today's society is the "knowledge economy" era forward, In today's competitive environment, the accounting officer must not only well versed in the basic principles of accounting, computerized accounting techniques to master , but also learn some sense of organization, behavioral factors, decision-making process and communication technology and other aspects of the basic theory. Accounting information representsnew accounting ideas and concepts, the traditional accounting theory and modern information technology, network technology, a combination of product development is the inevitable trend of modern accounting. It must seize opportunities, meet challenges, and strive to promote the development of China's accounting information.II An overview of the accounting information(A) the meaning of informationBegan in the 1940s wave of information technology, beginning aroused great attention in all aspects, from the 1960s, scholars began to have "information" and "information society" and so on. 1963 Japanese scholars Tidal plum out in its "Information Industry science" for the first time that "information technology" concept. As information technology there is not long, the actual development and very rapid development of information society itself changes, the understanding of information technology are not the same. For example, "information is the communication of modern, computer and rationalize the general term", "information is computerized, modern communication and network technology", "information is e-commerce" and "information is computerized," " information is information technology and information industry in the economic and social development andplay a leading role in increasing the process ", and so on. Information technologyrevolution and the industrial revolution is the result of information from the three aspects, namely, the digitization of information, information networks, information and intelligent. "Digital information is the basis of information, the information network is the basic characteristics of information technology, information, and information technology is the development of intelligent features."(B) The information content of accountingThe concept of accounting information in 2000, the Shenzhen Municipal Finance Bureau and the Shenzhen Kingdee Software Technology Co., Ltd in Shenzhen's "new situation, management accounting software market, Information Theory Symposiumaccounting expert forum" on the make is the accounting computerized product development to a new stage. Theoretical understanding of information technology sector have different views, such as technical concept, the process concept, elements and outlook, and thus the concept of accounting information will have a different set, HU Ran star of accounting information as defined by the use of more the status quo. "Accounting information is based on the system in the enterprise of science, management science, application of modern information technology, integration of enterprise business processes and accounting processes, the establishment of accounting information systems; full development and use of accounting information resources, timely and accurate to the enterprise internal and external users of accounting information to provide useful support to strengthen the role of accounting to reflect and monitor the overall process. "As can be seen from this statement, the accounting information is the process of concept, it conveys such meanings: First, the means of access to information networks, communications and databases; Second, business processes and accounting processes to be re- whole, to better reflect the timeliness of information provided; third-to-business cash flow, physical flow and information flow throughout theimplementation of real-time control; Fourth, the spatial extent of the accounting information to expand information coverage, including information and currency non-monetary information internal information and external information, and so on. Professor Yang Zhou Nan the study of accounting information has its own unique, she will be introduced to the theory of value chain management accounting information in the field, made a "value chain management, accounting, information technology," the new concept, and that the "value chain management accounting information is the value chain to achieve important environmental accounting management and technology base. " And discussed the value chain management accounting information in the target location, technology platform, business process management models, standards, audit system, and in ten areas of change. Expand the meaning of accounting information.(C) The development of accounting information1 era of computerized accountingFunding from the Ministry of Finance in 1978, Chinches First Automobile Works began a pilot computerized accounting, accounting information in China's development has gone through more than 20 years, in its early stage of developmentthat the era of computerized accounting, computer applications accounting in the accounting field to produce a major change, the accounting staff work from reimbursement heavy afterwards freed, so that participants are management accounting staff time, improve the quality of accounting information and timeliness of the initial training of accounting software boom market, develop a group of composite talent, creating a number of accounting software company, to the standardization of computerized accounting, commercial, universal, professional development, and for corporate information and provide a good experience, and promote enterprise management software development. But the rapid development of modern information technology on the traditional computerized accounting system had a tremendousimpact on the theoretical basis of accounting, the timeliness of accounting reports and other challenges. Xiao ravioli the traditional computerized accounting of the main problems are summarized as follows: "First, the traditional manual accounting, computerized accounting simulation only, although the financial accounting software to improve the efficiency and quality of accounting information, but accounting processing procedures and methods are basically just a set of procedures to move the hand up the computer; Second, the traditional accounting information system is the internal information 'islands' in the computerized implementation, financial data and business can not be shared, resulting in confined to the financial sector financial software to use, and internal business units are not well connected. other departments can not directly access to financial data; Third, the traditional accounting information system and outside the enterprise information system isolation and all business transactions or to open by hand, according to the paper documents the first, and then entered into the computer; Fourth, the traditional accounting information system lags behind the development of modern information technology now INTERNET-INTRANET technology has reached the stage that we can not imagine, if we are still deal with isolated cases of the PC, then the business of managementdecision-making, budgeting, investment and production decisions will be errors due to insufficient amount of information; the fifth, only in the most traditional computerized accounting electronic data processing stage. China's implementation of accounting computing of the unit, most just use computerized accounting basic accounting, and a large number of financial management and financial analysis, is still a manual process; the sixth, in place of traditional computerized software development, function is not fully, to use the resulting inconvenient. "(2) Accounting information ageWhen the network technology and the maturity of domestic accounting software, financial, and timely exchange of business data has a technical support, and therefore the accounting information age has arrived. 2000, accounting information theorists first proposed the term is, and has been widely recognized. This reference is to the service management functions of accounting on the present and future information environment into account, is changing attitudes, is to seek greater development. Accounting information on the target even pay attention to accounting in business management on the central role; more dependent on the technology of modern network technology; focus on the functional areas of management accountinginformation and decision analysis; status in the system as a management systemintegral part; in the information transmission on the basis of authorization to acquire or output the information in the internal and external systems.Time accounting information more open and diversity. Openness is the high degree of sharing of accounting information resources, large amounts of data information between the departments within the enterprise, between enterprises within the group and between groups and external corporate unlimited or limited authorization of information exchange. Diversity performance of accounting information is no longer a single financial account table data, but also a lot of non-monetary forms of information; is no longer the only direct data or after a simplesummary of the data, but also includes many qualitative and quantitative analysis after can respond to different information needs of those recycling information; not only by Rose-year tradition of staging statistics accounting information, more of a point in time information, that is its real-time.Third, the use of accounting information Analysis(A) the status of the use of accounting informationImplementation of information technology in business process, the software provider to the enterprise managers have always praised their own software in the technical structure and how the information model is refined, is how the demand for enterprise management, and that enterprises should make what change in order to play the software management functions. But it did, most did not use information technology for the enterprise software providers to create the initial promised value. Even companies and managers think that the use of information systems management in the past rigid, not as labor management more convenient and flexible. This information management system is a failure of management systems; it is only concerned about the use of technology, while ignoring the way people access to information and requirements. U.S. information technology specialist Thomas. H •Davenport claims, in order to change the unsatisfactory status of information technology, must be people-oriented principle. Effective information management must first focus on how people think about the application of information, rather than how to use the machine. In people-oriented information management strategy, the reality of diversity to be concerned about the information; to emphasize the effective use of information and wide sharing; to make information technology solutions to solve current practical problems; to allow for different interpretations of the same message; to that enterprises to obtain the desired effect is considered the ultimate success; to specific problems to establish the appropriate structure; to promote and strengthen the method by adjusting the behavior of members of the organization; to the user's need to design their own applications. Body belongs to large enterprises, has been large-scale enterprise management, and financial strength. Before the introduction of the enterprise, there are three companies will have to implement ERP management system, and is part of the implementation of these enterprises are large-scale department stores and supermarket chains. Both with 16 companies have at least one financial software business management software companies, one of the six companies of the business management software such as inventory managementsoftware and financial software to achieve the integration, these companies are outside the supermarket. Local department stores and supermarket chains do little to achieve integration.Large supermarket chains in spite of the ERP management system, but and foreign retail giants such as Wal-Mart, Carrefour, B & Q, in comparison, China's domestic retail business of information technology still in its infancy. For example, Wal-Mart is the first use of computers to track inventory in retail enterprises (1969), is the earliest use of bar code (1980), the use of EDI with suppliers for better coordination (1985), launch its own communication satellite (1986) and use the wireless scanning guns (late 1980s) of retail companies. Now, Wal-Mart is the world'smost spare no effort to implement RFID Technology Company. Our domestic retail enterprises and applications providers are basically in a bystander.(B) The use of accounting information the problems1 lack of capital investmentAccording to the survey, not the type of business is accounting information in capital investment are also significant differences, in general, in terms of information technology also significantly less capital investment. Some small retail businesses, especially those franchise retail stores, its turnover of 100 million or less, the profit of 10 million or less. These companies invest in information technology capital is almost zero. For example, there is a franchise of computer accessories supplies store, operated by no less than one thousand kinds of varieties of goods, commodities Invoicing also only manual bookkeeping, the occurrence of errors is often a matter, but in a short time do not want to invest in this area. Manager believes that the purchase of small Invoicing software is several thousand to more than a million, do not necessarily apply to buy back their own and do not find someone to develop such talent. This situation represents the general attitude of some small businesses. Some of the economic benefits of better information technology in the retail business is also aserious shortage of capital investment. Local department store is a large-scale, high-profile retailer, sales of 4 billion last year, more than 300 million annual profit. This year is expected to increase by 1 million sales. So far the company has a network version of the UF of a financial accounting software and a software company developing your inventory management software, for a total capital of less than 30 million, if $ 1 million plus investment in hardware terms, the company's information construction accounts for the year total investment capital ratio of .325% of sales. According to statistics, the total number of enterprises in China accounted for 99.6% of the 40 million SMEs, of which 74% of enterprise information into sales revenue accounted for less than 1%, usually abroad, 2% -3%. Defined in accordance with the latest standards for SMEs to divide, retail enterprises with annual sales of more than 150 million people or more than 500 the number of workers should belong to large-scale retail enterprises. In other words, the department stores are large retail companies, invested in information technology should be more than 1% of the funds, but the fact is much lower than the ratio. From the survey found the same with the size of the retail mall business investment in information technology is basically the same proportion.(2) For their own interests and resist cooperation with upstream and downstreambusinessesSome retailers believe that if the composition of upstream and downstream enterprises and their value chain, then this value chain to increase the total value is given, other means to make their own alliance to get more companies will get less. Therefore, the value chain between the various value chains Alliance is a competitive relationship. In such a concept under the guidance of the retail business is often not the whole value chain from the perspective of value-added, but rather in order to pursue their own interests at the expense of maximizing the interests of the entire value chain. Therefore, in the retail business and corporate transactions in theupstream, suppliers repeatedly lower prices, even the ones who enjoy the suppliers as their main source of profit; the supplier is to conceal their true costs, even as the retail price increases in disguise counterattack. The two sides are not creating value chain from the overall effectiveness of view, but to build their own profit loss in the value chain based on the Alliance. This is clearly not the goal of value chain management. Retailers should change their ideas, we must seek to maximize their own interests into the overall interests of the pursuit of maximizing the value chain, and clear corporate profits should manage to get through the value chain, value chain, rather than from the body to acquire Alliance.Other retailers do not want their business data, or other important sales information and customer information available to the supplier, even if the enterprise also needs to control access rights, let alone to disclose outside the enterprise. This deep-rooted tradition of understanding between suppliers and retailers so that the lack of a good spirit of cooperation. The basic goal of value chain management is the management process by improving the transparency of the entire value chain to improve the efficiency of resource allocation and profit levels, sharing of information resources. This will not only make the core of the value chain within the enterpriseand value chain alliances between enterprises can receive timely, flexible and actionable information resources to enable them to fully grasp the value chain cooperation between the Alliance information, market information, other business decision-making information, but also enables the company starting from the global value chain to arrange production and services.Management rather than the promoterLearned in the survey had had some local retailers, accounting information for what is not understood, was 67.19% in visitors who do not know what is accounting information, never heard of value chain management, the company has implemented a complete information technology solutions tend to say, very often referred to our information management staff to answer. Managers of these companies as the information because of competitive pressures is a helpless and passive choice, their knowledge of information technology know much, but not condescending and general staff to receive formal training, and such of the lack of knowledge of information technology initiative to accept the manager's attitude will inevitably lead to the loss of authority in this regard, they naturally will not be a promoter of information technology, and will be the task entrusted to the information management staff.Regardless of the information management company executives in the company'sposition that tall, and its authority is inferior to general manager, when stakeholders hinder the process of information, the information management staff had no ability to advance the information technology revolution. In addition, information management staffs are often professional and technical personnel, their lack of business knowledge and management capabilities, enterprise information process will be based more on business instead of computer hardware and software technical problems. In this case, information management will become powerless. If you rely on information technology to promote information management, failure becomes inevitable.Positioned correctly in the accounting functions of informationOne view is that the accounting functions will be limited to record a variety of business information behind them, while in charge of foreign tax returns and financial statements submitted to the traditional. Hold this view tend to be small retail business managers. They see the accounting for tax accounting and treasury accounting, they need to get that information from the accounting major is the number of day and monthly cash flow to pay the tax number. For the case of commodity stocks more business managers to ask, but regardless of the amount of inventory accounting and inventory carrying costs. This is because much small retail business to avoid taxes from the perspective of the book to create a false inventory, accounting, accounts payable data is the tax department. Based on this purpose, the managers of these enterprises will not consider business management systems and financial accounting system for data sharing. Learned from the survey 62.5% of the enterprises is not the business management software and financial accounting software and docking. Managers first consider the purchase of inventory management system is more than the amount due to the types of products, often caused by hand-billing and out of the workload and error rate increased only alternative. In the early stages of business development, accounting information for managers attitude and understanding of theaccounting function to reduce the tax burden may have a role, but this effect is not really benefit from the long-term stable development of enterprises to consider, once the risk of tax laws increased, the negative effect caused by low-would offset the tax benefits.Accounting, information technology implementation strategy analysis(A) Strategic and tactical implementation services for enterpriseFirm's strategic goal is to guide the development of accounting information based strategy; it must be its direction. In the absence of this direction, it will not clear the company's future direction, it is impossible to the accounting information to provide a clear strategic goal orientation, so the implementation of accounting information in the development of strategy must first clear the overall development strategy. Such enterprises to implement low-cost competitive strategy in the case of the accounting information of the implementation strategy will have a significant impact. The purpose of this strategy is to provide quality low cost products, and use price advantage over competitors. The accounting information in order to meet the strategic needs to be broken down by value chain analysis of cost control point, the development of procurement, production process, the operational procedures,marketing and other aspects of cost control standards, the design of cost control pointof cost information collection, transmission, aggregation, evaluation methods, to establish the accounting staff in the cost assessment in the central position, the establishment of cost control, reward and punishment system, and so on.(B) The implementation of management concepts update strategyManagers and internal employees know a lot of information technology is superficial, is generally believed that is a documentation of business processes and translate into something the computer can use to help companies accelerate the transmission of information; solutions manual has been the basis of the business can not solve management problems, but did not think for management improvement.Managers tend to think only of the benefits of information into management, but has not been established to promote information technology and management thinking in need of change, not concerned about the information technology business processes are likely to face adjustment and the adjustment of rules. Managers must also recognize that while changes in the general population and also including employees, their thoughts must also go to follow the changes in business, change from passive acceptance to active acceptance. Thus thinking of updating educational enterprise information has become an indispensable step in the process. Haier's Zhang proposed a "re-process reengineering first person who first recycling recycling concept." In order to promote the implementation of information technology in the process change, reversing the employees, especially the concept of corporate management, Zhang himself as a teacher, teaching stage process reengineering to promote the guiding ideology, and the formation of discussion of the program to verify in practice. Total number of trained close to 20,000.Some people think that advanced management information system implies a system of advanced management concepts, this argument has some truth, but the use of advanced information systems and management concepts to improve the。

公司各个部门英文翻译

市场营销部: SALES&MARKETING DEPARTMENT计财部:ACCOUNTING DEPARTMENT人力资源部: HUMAN RESOURCE DEPARTMENT工程部: ENGINEERING DEPARTMENT保安部: SECURITY DEPARTMENT行政部: EXECUTIVE DEPARTMENT前厅部: FRONT OFFICE客房部: HOUSEKEEPING DEPARTMENT餐饮部: FOOD&BEVERAGE DEPARTMENT外销部: EXPORT DEPARTMENT财务科: FINANCIAL DEPARTMENT党支部: BRANCH OF THE PARTY会议室: MEETING ROOM会客室: RECEPTION ROOM质检科: QUALITY TESTING DEPARTMENT内销部: DOMESTIC SALES DEPARTMENT厂长室: FACTORY DIRECTOR'S ROOM行政科: ADMINISTRATION DEPARTMENT技术部: TECHNOLOGY SECTION档案室: MUNIMENT ROOM生产科: MANUFACTURE SECTION总公司: Head Office分公司: Branch Office营业部: Business Office人事部: Personnel Department总务部: General Affairs Department财务部: General Accounting Department销售部: Sales Department促销部: Sales Promotion Department国际部: International Department出口部: Export Department进口部: Import Department公共关系: Public Relations Department广告部: Advertising Department企划部: Planning Department产品开发部: Product Development Department研发部: Research and Development Department (R&D) 秘书室: Secretarial Poo市场部Marketing Department技术服务部 Technical service Department人事部 Personnel Department(人力资源部)Human Resources DepartmentAccounting Assistant 会计助理Accounting Clerk 记帐员Accounting Manager 会计部经理Accounting Stall 会计部职员Accounting Supervisor 会计主管Administration Manager 行政经理Administration Staff 行政人员Administrative Assistant 行政助理Administrative Clerk 行政办事员Advertising Staff 广告工作人员Airlines Sales Representative 航空公司定座员Airlines Staff 航空公司职员Application Engineer 应用工程师Assistant Manager 副经理Bond Analyst 证券分析员Bond Trader 证券交易员Business Controller 业务主任Business Manager 业务经理Buyer 采购员Cashier 出纳员Chemical Engineer 化学工程师Civil Engineer 土木工程师Clerk/Receptionist 职员/接待员Clerk Typist & Secretary 文书打字兼秘书Computer Data Input Operator 计算机资料输入员Computer Engineer 计算机工程师Computer Processing Operator 计算机处理操作员Computer System Manager 计算机系统部经理Copywriter 广告文字撰稿人Deputy General Manager 副总经理Economic Research Assistant 经济研究助理Electrical Engineer 电气工程师Engineering Technician 工程技术员English Instructor/Teacher 英语教师Export Sales Manager 外销部经理Export Sales Staff 外销部职员Financial Controller 财务主任Financial Reporter 财务报告人F.X. (Foreign Exchange) Clerk 外汇部职员F.X. Settlement Clerk 外汇部核算员Fund Manager 财务经理General Auditor 审计长General Manager/President 总经理General Manager Assistant 总经理助理General Manager‘s Secretary 总经理秘书Hardware Engineer (计算机)硬件工程师Import Liaison Staff 进口联络员Import Manager 进口部经理Insurance Actuary 保险公司理赔员International Sales Staff 国际销售员Interpreter 口语翻译Legal Adviser 法律顾问Line Supervisor 生产线主管Maintenance Engineer 维修工程师Management Consultant 管理顾问Manager 经理Manager for Public Relations 公关部经理Manufacturing Engineer 制造工程师Manufacturing Worker 生产员工Market Analyst 市场分析员Market Development Manager 市场开发部经理Marketing Manager 市场销售部经理Marketing Staff 市场销售员Marketing Assistant 销售助理Marketing Executive 销售主管Marketing Representative 销售代表Marketing Representative Manager 市场调研部经理Mechanical Engineer 机械工程师Mining Engineer 采矿工程师Music Teacher 音乐教师Naval Architect 造船工程师Office Assistant 办公室助理Office Clerk 职员Operational Manager 业务经理Package Designer 包装设计师Passenger Reservation Staff 乘客票位预订员Personnel Clerk 人事部职员Personnel Manager 人事部经理Plant/Factory Manager 厂长Postal Clerk 邮政人员Private Secretary 私人秘书Product Manager 生产部经理Production Engineer 产品工程师Professional Staff 专业人员Programmer 电脑程序设计师Project Staff (项目)策划人员Promotional Manager 推销部经理Proof-reader 校对员Purchasing Agent 采购(进货)员Quality Control Engineer 质量管理工程师Real Estate Staff 房地产职员Recruitment Coordinator 招聘协调人Regional Manger 地区经理Research & Development Engineer 研究开发工程师Restaurant Manager 饭店经理Office Assistant 办公室助理Office Clerk 职员Operational Manager 业务经理Package Designer 包装设计师Passenger Reservation Staff 乘客票位预订员Personnel Clerk 人事部职员Personnel Manager 人事部经理Plant/Factory Manager 厂长Postal Clerk 邮政人员Private Secretary 私人秘书Product Manager 生产部经理Production Engineer 产品工程师Professional Staff 专业人员Programmer 电脑程序设计师Project Staff (项目)策划人员Promotional Manager 推销部经理Proof-reader 校对员Purchasing Agent 采购(进货)员Quality Control Engineer 质量管理工程师Real Estate Staff 房地产职员Recruitment Coordinator 招聘协调人Regional Manger 地区经理Research & Development Engineer 研究开发工程师Restaurant Manager 饭店经理Sales and Planning Staff 销售计划员Sales Assistant 销售助理Sales Clerk 店员、售货员Sales Coordinator 销售协调人Sales Engineer 销售工程师Sales Executive 销售主管Sales Manager 销售部经理Salesperson 销售员Seller Representative 销售代表Sales Supervisor 销售监管School Registrar 学校注册主任Secretarial Assistant 秘书助理Secretary 秘书Securities Custody Clerk 保安人员Security Officer 安全人员Senior Accountant 高级会计Senior Consultant/Adviser 高级顾问Senior Employee 高级雇员Senior Secretary 高级秘书Service Manager 服务部经理Simultaneous Interpreter 同声传译员Software Engineer (计算机)软件工程师Supervisor 监管员Systems Adviser 系统顾问Systems Engineer 系统工程师Systems Operator 系统操作员Technical Editor 技术编辑Technical Translator 技术翻译Technical Worker 技术工人Telecommunication Executive 电讯(电信)员Telephonist/Operator 电话接线员、话务员Tourist Guide 导游Trade Finance Executive 贸易财务主管Trainee Manager 培训部经理Translation Checker 翻译核对员Translator 翻译员Trust Banking Executive 银行高级职员Typist 打字员Word Processing Operator 文字处理操作员文案编辑词条B 添加义项?文案,原指放书的桌子,后来指在桌子上写字的人。

会计学毕业论文的外文翻译

会计学毕业论文外文翻译and Countermeasure of Accounting CausesInformation DistortionHuang Xian LingSchool of Management South-Central University For Nationalities , PR.China, 430074Abstract: In recent years, the accounting information distortion hasaffected social economy order. This article mainly discusses on the causesand countermeasure of accounting information distortion in China.Keywords: Accounting Information Distortion Causes Countermeasure1 IntroductionIn recent years, it happens sometimes that the accounting information distort. It will affect information users such asinvestors and creditors correctly judge and deicide the management of enterprise, result in the national macroeconomic regulation and control and the microscopic policy-making fault, and affect the social economy order normally operate. This article mainly discusses on the causes and countermeasure of accounting information distortion in China.2 The reason of the accounting information distortionThere arevarious reasons of accounting information distortion: the enterprise internal factor and also exterior factor; the objective reason and alsothe subjective reason. Summarily, it mainly has following several points:2.1 The limitation of accountant laws and regulations systemTheaccounting guide line and business accounting system are all the basic standards of accounting work, the concrete prescribe of businessaccounting principles, the accounting service processing method and the accounting information disclosure method and so on. As the basic standardsof accounting work, the limitation of the accounting guide line and business accounting system is reason of accounting information distortion.It mainly displays in: First, the inherent estimate and the specialized judgment of the accounting guide line and business accounting system willcause the accounting information distortion. Second, the flexibility of accounting method may cause the accounting information distortion. Third,the hysteretic quality of the accounting guide line and businessaccounting system will also cause the accounting informationdistortion2.2 The accountancy faultThe accountancy fault refers tounconsciousness fault made in the accountancy as a result of the fault of measure, confirmation, record, report and so on. The accountancy faultis also an important reason of accounting information distortion. It mainly displays in: 1. Understood and applied the accounting guide line and and business business business accounting accounting accounting system system system mistakenly mistakenly mistakenly will will will lead lead lead accounting accountinginformation distortion. In the accounting guide line and businessaccounting system, certain economic work or the phenomenon calculationis compares principled, which calls for appropriate calculation method by purse bearer specialized analysis. If the purse bearer is not certainabout the accounting guide line and business accounting system, he will not account economic work correctly, and then it becomes possible to makedistorted accounting information 2. Unconsciousness fault made in the accountancy leads to accounting information distortion. Even if the accountant can understand and grasp accounting guide line and business accounting system accurately, some mistakes unavoidably in the work willmistake ofcause the accounting information distortion. Such as theaccount category, accountant miscalculation, miss record the business occurred2. 3 Occupational ethics deviatingAccountant occupational ethicsdeviating from the norm refers to accountant lack or lose the professional standard. Since reform and opening-up, the reform of accountant has filledwith vitality and vigor and obtained the huge achievement in our country.But at the same time, original accountant standards encounter serious destruction or the denial by a certain extent, gradually lose restraint of 481 accountant. And form accountant occupational ethics standardauthority losing. In practical work, some accountants fail to resist enticement or the instruction of higher authority, and intentionally manufacture the distorting accounting information seeking the benefit2.4 The imperfect government mechanismAt present, our country has practicedthe market economy system, but in the reality, dislocation mechanism thatthe government manage enterprise extremely was still prevails, andgovernment's behavior was not according to the market economy rule. The government manages enterprise directly in many place, as a result it always leads to a complexion that the leader of enterprise “revolving around government”. Some local government manages the lead leader er ofenterprise by target inspection, responsibility audit, rewards theexcellent and punishes the inferior. But the head of enterprise hide theprofit when getting good benefit, and forge the profit when not achieve the goal in order to go through a strategic pass. As the matter stands, the accounting information inevitably distorts3. The Countermeasure of Accounting Information DistortionThe accounting information is thepublic public product product product and and and influence influence influence widespread, widespread, widespread, the the the user user user of of of which which which is ismultitudinous. Currently, accounting information distortion is tooserious to harness. Generally speaking, it will be resolved from followingseveral aspects:3.1 Standard accounting guide line and strengthen the construction of accounting systemWhen the country formulates accountant criterion andrelated laws and regulations, it should be comprehensively, necessary, prompt and feasibility as possible as we can, normalize the using of uncertainty wording, and gradually accord to international accounting system. When choosing accountant processing method, we should identicallyuse the most effective method as possible as we can, and clear about thesituation and the elastic sector of each processing method. Consummatingthe accounting method, stopping up loophole of the accounting informationdistorts. At the same time, enhancing enterprise internal control systemconstruction, displaying system restraint mechanism, reducing theopportunity of uncertainty and fuzziness3.2 Establishing and perfecting enterprise internal control system Currently the root of many distortingaccounting information depends on insufficient internal control system of enterprise, so that some illegal leader and accountant use the systemloophole to seek the benefit for themselves. The internal control systema complex system involves various departments, various levels, various links in the enterprise, the move of people, property and substance of enterprise and also involves assignment and arrangement of right,responsibility and benefit of enterprise. Therefore, it is important to establish and perfect an effective internal control system, which can guarantee the enterprise property security and integrity, the accountinginformation legitimate and fair and economic work legality, and enhance the management efficiency of the enterprise3.3 Perfecting accountant supervises system, enhancing punishment 1 Establishing accounting managesystem with the central of strengthening the internal management. In orderto establishing a good accountant the foundation of providing the real accounting information, we should enhance internal control, formulate finance finance supervision supervision and and internal internal internal investigation investigation system, system, perfect perfectenterprise interior accounting system, rigorously enforce accountingmain routine, perfect examination and approval system of each kind of property commodity and the financial revenue and expenditure Carrying out the accountant delegate system. Currently many accountants are unableto resist the leader’s instruct and conduct to corrupt practices, mostlybecause their own status and treatment have a very close relation with the the leader's leader's leader's opinion. opinion. opinion. Accountant Accountant Accountant delegate delegate delegate system system system may may may reduce reduce reduce the theattachment of accountant to the leader, thus strengthen accountantsupervise and improves the accounting information quality Chartered accountant should be developed vigorously, enterprise financial report audit verification system should be carrying out comprehensively,unaudited reports are illegally. Simultaneously we should strengthen legal liability surveillance of chartered accountant, urge chartered accountant to raise their occupational ethics level and service quality,clear about legal liability of accounting information examinationverification by chartered accountant, and establish concrete punishment measure for those482 chartered accountant who is derelict of duty or violates the occupational ethics3.4 Consummating employed qualifications system,enhancing enhancing following following following education, education, education, improving improving improving the the the accountant accountant accountant quality qualitycomprehensively Accountant’s quality will not only affec affect tthe effect of carrying out accounting guide line and business accounting system, butalso affects the accountancy quality, therefore, improving the accountant quality is the key of reducing accounting information distorts 1 Enforcing accountant employed qualifications system, enhancing the standard of present accountant employed qualifications. The people provided with corresponding qualifications are able to be engaged in the accountancy. accountancy. Strengthening Strengthening Strengthening accountant accountant accountant ranks ranks ranks from from from the the the source source source 2 Strengthening accountant's concept of legal system and occupationalethics idea. The accountant should be provided with intense sense of responsibility, disciplined and probity while line of duty, and never lose the principle and never scheme the personal gain whatever kind of situationMoreover, accountant must certainly observe accountant occupational ethics standard, namely loves the work, probity andself-discipline, objective fair, conservative secret, honest and keep faith, insistence criterion and enhances skill and so on, they should keeps these standard firmly in mind and the implementation in the routine work 3 Pay special attention to accountant's following education. first,opening up the content of following education, which include management and operation, occupational ethics and finance and economics law and discipline educations besides new accountant criterion and accounting system; second, pay attention to effect and quality of following education,preventing goes through the motions; third, closely unifies following education and professional qualifications management, practicescompulsory following educational system4 ConclusionsIn summary, there are various reasons of accounting information distortion; it will affect the fairness of public wealth assignment, the efficiency of social resources disposition, the establishment of social credit system. Therefore, we must establish and consummates accountant supervise system, establish and perfect enterprise internal control system, further standard standard accountant accountant accountant criterion, criterion, criterion, strengthen strengthen strengthen the the the accounting accounting accounting system system construction, Strengthens the the following following education, improve improve the the accountant’s accountant’s quality quality quality comprehensively. comprehensively. comprehensively. Then Then Then we we can guarantee guarantee the the authenticity, validity and legality of accounting information, and realize the goal of administer accounting information distortionReferences[1] Yang Hong. On the Reason and Countermeasure of Accountant Information Fault. Science &technology information. 2006.4[2]Jiang Yi biao. The formations of accountant information distortion. Finance & Accounting ForCommunications. 2003.2[3]Zhao Jing Ting. the countermeasures of accountant information distortion. Friends of accounting.2006.6[4]Cheng Shao Hua. Interior accounting control and accountingprofessional moral education. FuJian publishing company of Xia Men University. 2004.1 会计信息失真的原因与对策会计信息失真的原因与对策黄贤玲黄贤玲中南民族大学管理学院中南民族大学管理学院,,中国武汉中国武汉 430074 430074摘要摘要::这些年这些年,,会计信息失真已经影响到了社会经济秩序会计信息失真已经影响到了社会经济秩序,,本文主要分析了我国会计信息失真产生的原因国会计信息失真产生的原因,,及其对策。

会计英文文献及翻译

IMPLEMENTING ENVIRONMENTAL COSTACCOUNTING IN SMALL AND MEDIUM-SIZEDCOMPANIES1.ENVIRONMENTAL COST ACCOUNTING IN SMESSince its inception some 30 years ago, Environmental Cost Accounting (ECA) has reached a stage of development where individual ECA systems are separated from the core accounting system based an assessment of environmental costs with (see Fichter et al., 1997, Letmathe and Wagner , 2002).As environmental costs are commonly assessed as overhead costs, neither the older concepts of full costs accounting nor the relatively recent one of direct costing appear to represent an appropriate basis for the implementation of ECA. Similar to developments in conventional accounting, the theoretical and conceptual sphere of ECA has focused on process-based accounting since the 1990s (see Hallay and Pfriem, 1992, Fischer and Blasius, 1995, BMU/UBA, 1996, Heller et al., 1995, Letmathe, 1998, Spengler and H.hre, 1998).Taking available concepts of ECA into consideration, process-based concepts seem the best option regarding the establishment of ECA (see Heupel and Wendisch , 2002). These concepts, however, have to be continuously revised to ensure that they work well when applied in small and medium-sized companies.Based on the framework for Environmental Management Accounting presented in Burritt et al. (2002), our concept of ECA focuses on two main groups of environmentally related impacts. These are environmentally induced financial effects and company-related effects on environmental systems (see Burritt and Schaltegger, 2000, p.58). Each of these impacts relate to specific categories of financial and environmental information. The environmentally induced financial effects are represented by monetary environmental information and the effects on environmental systems are represented by physical environmental information. Conventional accounting deals with both – monetary as well as physical units – but does not focus on environmental impact as such. To arrive at a practical solution to the implementation of E CA in a company’s existing accounting system, and to comply with the problem of distinguishing between monetary and physical aspects, an integrated concept is required. As physical information is often the basis for the monetary information (e.g. kilograms of a raw material are the basis for the monetary valuation of raw material consumption), the integration of this information into the accounting system database is essential. From there, the generation of physical environmental and monetary (environmental) information would in many cases be feasible. For many companies, the priority would be monetary (environmental) information for use in for instance decisions regarding resource consumptions and investments. The use of ECA in small andmedium-sized enterprises (SME) is still relatively rare, so practical examples available in the literature are few and far between. One problem is that the definitions of SMEs vary between countries (see Kosmider, 1993 and Reinemann, 1999). In our work the criteria shown in Table 1 are used to describe small and medium-sized enterprises.Table 1. Criteria of small and medium-sized enterprisesNumber of employees TurnoverUp to 500employees Turnover up to EUR 50mManagement Organization- Owner-cum-entrepreneur -Divisional organization is rare- Varies from a patriarchal management -Short flow of information style in traditional companies and teamwork -Strong personal commitmentin start-up companies -Instruction and controlling with- Top-down planning in old companies direct personal contact- Delegation is rare- Low level of formality- High flexibilityFinance Personnel- family company -easy to survey number of employees- limited possibilities of financing -wide expertise-high satisfaction of employeesSupply chain Innovation-closely involved in local -high potential of innovationeconomic cycles in special fields- intense relationship with customersand suppliersKeeping these characteristics in mind, the chosen ECA approach should be easy to apply, should facilitate the handling of complex structures and at the same time be suited to the special needs of SMEs.Despite their size SMEs are increasingly implementing Enterprise Resource Planning (ERP) systems like SAP R/3, Oracle and Peoplesoft. ERP systems support business processes across organizational, temporal and geographical boundaries using one integrated database. The primary use of ERP systems is for planning and controlling production and administration processes of an enterprise. In SMEs however, they are often individually designed and thus not standardized making the integration of for instance software that supports ECA implementation problematic. Examples could be tools like the “eco-efficiency” approach of IMU (2003) or Umberto (2003) because these solutions work with the database of more comprehensive software solutions like SAP, Oracle, Navision or others. Umberto software for example (see Umberto, 2003) would require large investments and great background knowledge of ECA – which is not available in most SMEs.The ECA approach suggested in this chapter is based on an integrative solution –meaning that an individually developed database is used, and the ECA solution adopted draws on the existing cost accounting procedures in the company. In contrast to other ECA approaches, the aim was to create an accounting system that enables the companies to individually obtain the relevant cost information. The aim of the research was thus to find out what cost information is relevant for the company’s decision on environmental issues and how to obtain it.2.METHOD FOR IMPLEMENTING ECASetting up an ECA system requires a systematic procedure. The project thus developed a method for implementing ECA in the companies that participated in the project; this is shown in Figure 1. During the implementation of the project it proved convenient to form a core team assigned with corresponding tasks drawing on employees in various departments. Such a team should consist of one or two persons from the production department as well as two from accounting and corporate environmental issues, if available. Depending on the stage of the project and kind of inquiry being considered, additional corporate members may be added to the project team to respond to issues such as IT, logistics, warehousing etc.Phase 1: Production Process VisualizationAt the beginning, the project team must be briefed thoroughly on the current corporate situation and on the accounting situation. To this end, the existing corporate accounting structure and the related corporate information transfer should be analyzed thoroughly. Following the concept of an input/output analysis, how materials find their ways into and out of the company is assessed. The next step is to present the flow of material and goods discovered and assessed in a flow model. To ensure the completeness and integrity of such a systematic analysis, any input and output is to be taken into consideration. Only a detailed analysis of material and energy flows from the point they enter the company until they leave it as products, waste, waste water or emissions enables the company to detect cost-saving potentials that at later stages of the project may involve more efficient material use, advanced process reliability and overview, improved capacity loads, reduced waste disposal costs, better transparency of costs and more reliable assessment of legal issues. As a first approach, simplified corporate flow models, standardizedstand-alone models for supplier(s), warehouse and isolated production segments were established and only combined after completion. With such standard elements and prototypes defined, a company can readily develop an integrated flow model with production process(es), production lines or a production process as a whole. From the view of later adoption of the existing corporate accounting to ECA, such visualization helps detect, determine, assess and then separate primary from secondary processes. Phase 2: Modification of AccountingIn addition to the visualization of material and energy flows, modeling principal and peripheral corporate processes helps prevent problems involving too high shares of overhead costs on the net product result. The flow model allows processes to be determined directly or at least partially identified as cost drivers. This allows identifying and separating repetitive processing activity with comparably few options from those with more likely ones for potential improvement.By focusing on principal issues of corporate cost priorities and on those costs that have been assessed and assigned to their causes least appropriately so far, corporate procedures such as preparing bids, setting up production machinery, ordering (raw) material and related process parameters such as order positions, setting up cycles of machinery, and order items can be defined accurately. Putting several partial processes with their isolated costs into context allows principal processes to emerge; these form the basis of process-oriented accounting. Ultimately, the cost drivers of the processes assessed are the actual reference points for assigning and accounting overhead costs. The percentage surcharges on costs such as labor costs are replaced by process parameters measuring efficiency (see Foster and Gupta, 1990).Some corporate processes such as management, controlling and personnel remain inadequately assessed with cost drivers assigned to product-related cost accounting. Therefore, costs of the processes mentioned, irrelevant to the measure of production activity, have to be assessed and surcharged with a conventional percentage.At manufacturing companies participating in the project,computer-integrated manufacturing systems allow a more flexible and scope-oriented production (eco-monies of scope), whereas before only homogenous quantities (of products) could be produced under reasonable economic conditions (economies of scale). ECA inevitably prevents effects of allocation, complexity and digression and becomes a valuable controlling instrument where classical/conventional accounting arrangements systematically fail to facilitate proper decisions. Thus, individually adopted process-based accounting produces potentially valuable information for any kind of decision about internal processing or external sourcing (e.g. make-or-buy decisions).Phase 3: Harmonization of Corporate Data – Compiling and Acquisition On the way to a transparent and systematic information system, it is convenient to check core corporate information systems of procurement and logistics, production planning, and waste disposal with reference to their capability to provide the necessary precise figures for the determined material/energy flow model and for previously identified principal and peripheral processes. During the course of the project, a few modifications within existing information systems were, in most cases, sufficient to comply with these requirements; otherwise, a completely new softwaremodule would have had to be installed without prior analysis to satisfy the data requirements.Phase 4: Database conceptsWithin the concept of a transparent accounting system, process-based accounting can provide comprehensive and systematic information both on corporate material/ energy flows and so-called overhead costs. To deliver reliable figures over time, it is essential to integrate a permanent integration of the algorithms discussed above into the corporate information system(s). Such permanent integration and its practical use may be achieved by applying one of three software solutions (see Figure 2).For small companies with specific production processes, an integrated concept is best suited, i.e. conventional andenvironmental/process-oriented accounting merge together in one common system solution.For medium-sized companies, with already existing integrated production/ accounting platforms, an interface solution to such a system might be suitable. ECA, then, is set up as an independent software module outside the existing corporate ERP system and needs to be fed data continuously. By using identical conventions for inventory-data definitions within the ECA software, misinterpretation of data can be avoided.Phase 5: Training and CoachingFor the permanent use of ECA, continuous training of employees on all matters discussed remains essential. To achieve a long-term potential of improved efficiency, the users of ECA applications and systems must be able to continuously detect and integrate corporate process modifications and changes in order to integrate them into ECA and, later, to process them properly.。

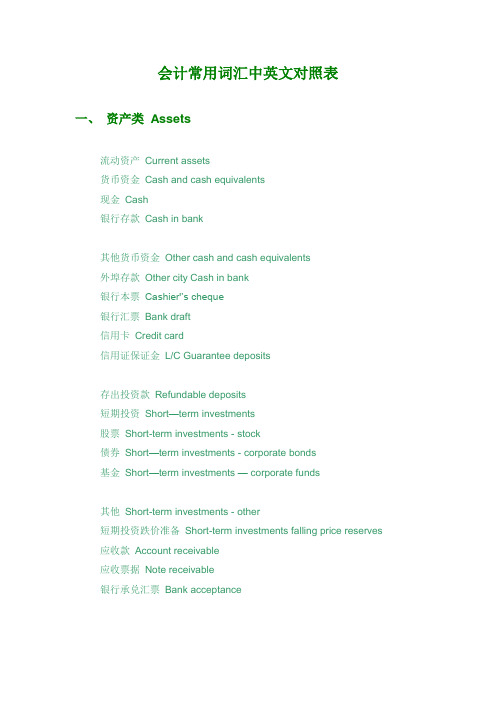

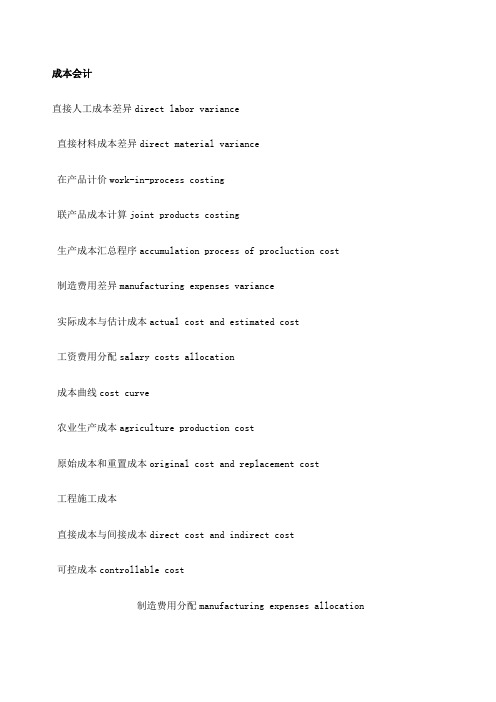

会计中英文对照[定稿]

![会计中英文对照[定稿]](https://img.taocdn.com/s3/m/1eb0f22abb1aa8114431b90d6c85ec3a87c28bdd.png)

会计中英文对照[定稿]第一篇:会计中英文对照[定稿]财会常见名词英汉对照表(1)会计与会计理论会计accounting 决策人Decision Maker 投资人Investor 股东Shareholder 债权人Creditor 财务会计Financial Accounting 管理会计Management Accounting 成本会计Cost Accounting 私业会计Private Accounting 公众会计 Public Accounting 注册会计师 CPA Certified Public Accountant 国际会计准则委员会IASC 美国注册会计师协会AICPA 财务会计准则委员会FASB 管理会计协会IMA 美国会计学会AAA 税务稽核署IRS 独资企业Proprietorship 合伙人企业Partnership 公司 Corporation 会计目标 Accounting Objectives 会计假设Accounting Assumptions 会计要素Accounting Elements 会计原则Accounting Principles 会计实务过程Accounting Procedures 财务报表Financial Statements 财务分析Financial Analysis 会计主体假设Separate-entity Assumption 货币计量假设Unit-of-measure Assumption 持续经营假设Continuity(Going-concern)Assumption 会计分期假设 Time-period Assumption 资产Asset 负债Liability 业主权益Owner's Equity 收入Revenue 费用Expense 收益 Income 亏损 Loss 历史成本原则 Cost Principle 收入实现原则 Revenue Principle 配比原则 Matching Principle 全面披露原则Full-disclosure(Reporting)Principle 客观性原则Objective Principle 一致性原则Consistent Principle 可比性原则Comparability Principle 重大性原则 Materiality Principle 稳健性原则Conservatism Principle 权责发生制Accrual Basis 现金收付制Cash Basis 财务报告 Financial Report 流动资产 Current assets 流动负债Current Liabilities 长期负债Long-term Liabilities 投入资本Contributed Capital 留存收益 Retained Earning(2)会计循环会计循环Accounting Procedure/Cycle 会计信息系统Accounting information System 帐户 Ledger 会计科目 Account 会计分录 Journal entry 原始凭证 Source Document 日记帐 Journal 总分类帐General Ledger 明细分类帐Subsidiary Ledger 试算平衡Trial Balance 现金收款日记帐 Cash receipt journal 现金付款日记帐Cash disbursements journal 销售日记帐 Sales Journal 购货日记帐Purchase Journal 普通日记帐 General Journal 工作底稿 Worksheet 调整分录 Adjusting entries 结帐 Closing entries(3)现金与应收帐款现金 Cash 银行存款 Cash in bank 库存现金 Cash in hand 流动资产 Current assets 偿债基金 Sinking fund 定额备用金 Imprest petty cash 支票 Check(cheque)银行对帐单 Bank statement 银行存款调节表 Bank reconciliation statement 在途存款 Outstanding deposit 在途支票Outstanding check 应付凭单Vouchers payable 应收帐款Account receivable 应收票据 Note receivable 起运点交货价 F.O.B shipping point 目的地交货价F.O.B destination point 商业折扣Trade discount 现金折扣Cash discount 销售退回及折让Sales return and allowance 坏帐费用Bad debt expense 备抵法Allowance method 备抵坏帐 Bad debt allowance 损益表法 Income statement approach 资产负债表法 Balance sheet approach 帐龄分析法 Aging analysis method 直接冲销法 Direct write-off method 带息票据Interest bearing note 不带息票据 Non-interest bearing note 出票人 Maker 受款人 Payee 本金 Principal 利息率 Interest rate 到期日Maturity date 本票Promissory note 贴现Discount 背书Endorse 拒付费Protest fee(4)存货存货Inventory 商品存货Merchandise inventory 产成品存货 Finished goods inventory 在产品存货Work in process inventory 原材料存货Raw materials inventory 起运地离岸价格F.O.B shipping point 目的地抵岸价格F.O.B destination 寄销Consignment 寄销人Consignor 承销人Consignee 定期盘存Periodic inventory 永续盘存Perpetual inventory 购货 Purchase 购货折让和折扣 Purchase allowance and discounts 存货盈余或短缺 Inventory overages and shortages 分批认定法 Specific identification 加权平均法 Weighted average 先进先出法First-in, first-out or FIFO 后进先出法Lost-in, first-out or LIFO 移动平均法 Moving average 成本或市价孰低法 Lower of cost or market or LCM 市价 Market value 重置成本 Replacement cost 可变现净值 Net realizable value 上限 Upper limit 下限 Lower limit 毛利法Gross margin method 零售价格法Retail method 成本率Cost ratio(5)长期投资长期投资 Long-term investment 长期股票投资 Investment on stocks 长期债券投资 Investment on bonds 成本法 Cost method 权益法Equity method 合并法Consolidation method 股利宣布日Declaration date 股权登记日Date of record 除息日Ex-dividend date 付息日 Payment date 债券面值 Face value, Par value 债券折价Discount on bonds 债券溢价Premium on bonds 票面利率Contract interest rate, stated rate 市场利率 Market interest ratio, Effective rate 普通股 Common Stock 优先股 Preferred Stock 现金股利Cash dividends 股票股利Stock dividends 清算股利Liquidating dividends 到期日 Maturity date 到期值 Maturity value 直线摊销法 Straight-Line method of amortization 实际利息摊销法Effective-interest method of amortization(6)固定资产固定资产 Plant assets or Fixed assets 原值 Original value 预计使用年限 Expected useful life 预计残值 Estimated residual value 折旧费用 Depreciation expense 累计折旧 Accumulated depreciation 帐面价值 Carrying value 应提折旧成本 Depreciation cost 净值 Net value 在建工程 Construction-in-process 磨损 Wear and tear 过时Obsolescence 直线法 Straight-line method(SL)工作量法 Units-of-production method(UOP)加速折旧法Accelerated depreciation method 双倍余额递减法 Double-declining balance method(DDB)年数总和法Sum-of-the-years-digits method(SYD)以旧换新Trade in 经营租赁Operating lease 融资租赁Capital lease 廉价购买权Bargain purchase option(BPO)资产负债表外筹资Off-balance-sheet financing 最低租赁付款额 Minimum lease payments(7)无形资产无形资产 Intangible assets 专利权 Patents 商标权 Trademarks, Trade names 著作权Copyrights 特许权或专营权Franchises 商誉Goodwill 开办费Organization cost 租赁权Leasehold 摊销Amortization(8)流动负债负债 Liability 流动负债 Current liability 应付帐款Account payable 应付票据Notes payable 贴现票据Discount notes 长期负债一年内到期部分Current maturities of long-term liabilities 应付股利Dividends payable 预收收益Prepayments by customers 存入保证金 Refundable deposits 应付费用 Accrual expense 增值税 value added tax 营业税 Business tax 应付所得税 Income tax payable 应付奖金 Bonuses payable 产品质量担保负债 Estimated liabilities under product warranties 赠品和兑换券Premiums, coupons and trading stamps 或有事项Contingency 或有负债 Contingent 或有损失 Loss contingencies 或有利得 Gain contingencies 永久性差异 Permanent difference 时间性差异 Timing difference 应付税款法 Taxes payable method 纳税影响会计法Tax effect accounting method 递延所得税负债法Deferred income tax liability method(9)长期负债长期负债 Long-term Liabilities 应付公司债券 Bonds payable 有担保品的公司债券Secured Bonds 抵押公司债券Mortgage Bonds 保证公司债券 Guaranteed Bonds 信用公司债券 Debenture Bonds 一次还本公司债券 Term Bonds 分期还本公司债券 Serial Bonds 可转换公司债券 Convertible Bonds 可赎回公司债券 Callable Bonds 可要求公司债券 Redeemable Bonds 记名公司债券 Registered Bonds 无记名公司债券 Coupon Bonds 普通公司债券 Ordinary Bonds 收益公司债券 Income Bonds 名义利率,票面利率 Nominal rate 实际利率Actual rate 有效利率 Effective rate 溢价 Premium 折价 Discount 面值Par value 直线法Straight-line method 实际利率法Effective interest method 到期直接偿付Repayment at maturity 提前偿付Repayment at advance 偿债基金 Sinking fund 长期应付票据 Long-term notes payable 抵押借款 Mortgage loan(10)业主权益权益Equity 业主权益 Owner's equity 股东权益 Stockholder's equity 投入资本 Contributed capital 缴入资本 Paid-in capital 股本Capital stock 资本公积 Capital surplus 留存收益 Retained earnings 核定股本 Authorized capital stock 实收资本 Issued capital stock 发行在外股本Outstanding capital stock 库藏股Treasury stock 普通股Common stock 优先股Preferred stock 累积优先股Cumulative preferred stock 非累积优先股 Noncumulative preferred stock 完全参加优先股Fully participating preferred stock 部分参加优先股Partially participating preferred stock 非部分参加优先股Nonpartially participating preferred stock 现金发行 Issuance for cash 非现金发行 Issuance for noncash consideration 股票的合并发行 Lump-sum sales of stock 发行成本 Issuance cost 成本法 Cost method 面值法 Par value method 捐赠资本 Donated capital 盈余分配Distribution of earnings 股利Dividend 股利政策Dividend policy 宣布日 Date of declaration 股权登记日 Date of record 除息日 Ex-dividend date 股利支付日 Date of payment 现金股利 Cash dividend 股票股利 Stock dividend 拨款 appropriation(11)财务报表财务报表 Financial Statement 资产负债表 Balance Sheet 收益表 Income Statement 帐户式 Account Form 报告式 Report Form 编制(报表)Prepare 工作底稿 Worksheet 多步式 Multi-step 单步式 Single-step(12)财务状况变动表财务状况变动表中的现金基础 SCFP.Cash Basis(现金流量表)财务状况变动表中的营运资金基础SCFP.Working Capital Basis (资金来源与运用表)营运资金Working Capital 全部资源概念 All-resources concept 直接交换业务Direct exchanges 正常营业活动Normal operating activities 财务活动 Financing activities 投资活动Investing activities(13)财务报表分析财务报表分析Analysis of financial statements 比较财务报表Comparative financial statements 趋势百分比 Trend percentage 比率 Ratios 普通股每股收益 Earnings per share of common stock 股利收益率 Dividend yield ratio 价益比 Price-earnings ratio 普通股每股帐面价值Book value per share of common stock 资本报酬率Return on investment 总资产报酬率 Return on total asset 债券收益率 Yield rate on bonds 已获利息倍数 Number of times interest earned 债券比率 Debt ratio 优先股收益率 Yield rate on preferred stock 营运资本Working Capital 周转Turnover 存货周转率Inventory turnover 应收帐款周转率 Accounts receivable turnover 流动比率 Current ratio 速动比率 Quick ratio 酸性试验比率 Acid test ratio(14)合并财务报表合并财务报表Consolidated financial statements 吸收合并Merger 创立合并 Consolidation 控股公司 Parent company 附属公司Subsidiary company 少数股权Minority interest 权益联营合并Pooling of interest 购买合并Combination by purchase 权益法Equity method 成本法 Cost method(15)物价变动中的会计计量物价变动之会计 Price-level changes accounting 一般物价水平会计 General price-level accounting 货币购买力会计 Purchasing-power accounting 统一币值会计 Constant dollar accounting 历史成本 Historical cost 现行价值会计 Current value accounting 现行成本Current cost 重置成本Replacement cost 物价指数Price-level index 国民生产总值物价指数 Gross national product implicit price deflator(or GNP deflator)消费物价指数Consumer price index(or CPI)批发物价指数Wholesale price index 货币性资产Monetary assets 货币性负债 Monetary liabilities 货币购买力损益 Purchasing-power gains or losses 资产持有损益 Holding gains or losses 未实现的资产持有损益 Unrealized holding gains or losses 现行价值与统一币值会计 Constant dollar and current cost accounting oracle的应用软件版本11提供了45个集成的软件模块。

会计外文翻译---设定收益制养老金会计新准则

原文2New Accounting Rules for Defined Benefit Pension Plans MARCH 2008 - Issued in September 2006, Statement of Financial Accounting Standards (SFAS) 158, Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans—An Amendment of FASB Statements No. 87, 88, 106, and 132(R), significantly changes the balance-sheet reporting for defined benefit pension plans. Before SFAS 158, the effects of certain events, such as plan amendments or actuarial gains and losses, were granted delayed balance-sheet recognition. As a result, a plan’s funded status (plan assets minus obligations) was rarely reported on the balance sheet. SFAS 158 requires companies to report their plans’ funded status as either an asset or a liability on their balance sheets, which will cause reported pension liabilities to rise significantly. Although SFAS 158 also applies to postretirement benefit plans other than pensions and to not-for-profit entities, the focus below is on for-profit businesses with defined benefit pension plans.Balance-Sheet Reporting Under SFAS 158Under SFAS 87, prepaid or accrued pension cost, which is the net of a firm’s pension assets, liabilities, and unrecognized amounts, is reported on the balance sheet. SFAS 158 arguably improves financial reporting by more clearly communicating the funded status of defined benefit pension plans. Previously, this information was reported only in the detailed pension footnotes.Under SFAS 158, companies with defined benefit pension plans must recognize the difference between the plan’s projected benefit obligation and its fair value of plan assets as either an asset or a liability. The projected benefit obligation is the actuarial present value of the benefits attributed by the pension plan benefit formula for services already provided. As a result, the complex and conceptually unsound ―minimum pension liability‖ rules, which are used when the accumulated benefit obligation is less than the fair value of pension plan assets, has been eliminated. (The accumulated benefit obligation is similar to the projected benefit obligation but does not include expected future salary increases in the calculation of the present value of actuarial benefits.) In addition, the unrecognized prior service costs and actuarial gains and losses that were previously relegated to the footnotes are now recognized on the balance sheet, with an offsetting amount in accumulated other comprehensive income under shareholders’ equity.Income Reporting Under SFAS 158SFAS 158 does not change the computation of periodic pension cost, which remains a function of service cost, interest cost, expected return on pension plan assets, and amortization of unrecognized items. It does, however, impact the reporting of comprehensive income. Specifically, actuarial gains or losses and prior service costs that arise during the period are recognized as components of comprehensive income. In addition, the amortization of actuarial gains or losses, prior service costs, and transition amounts recognized before implementing SFAS 158 require a reclassification adjustment to comprehensive income.Applying SFAS 158Exhibit 1presents pension footnote data for three companies: Lockheed Martin, Glatfelter, and AMR Corp. Lockheed Martin represents a classic example of a scenario SFAS 158 is designed to eliminate: namely, reporting a pension asset when the pension plan is actually underfunded. Specifically, Lockheed Martin’s pension obligation ($28,421 million) exceeds its plan assets ($23,432 million), meaning the plan is underfunded by the difference, $4,989 million. Previously, Lockheed Martin’s unrecognized net losses and unr ecognized prior service costs (totaling $7,108 million) enabled it to report a pension asset of $2,119 million ($7,108 – $4,989).The data for Glatfelter and AMR in Exhibit 1 indicate other likely scenarios under SFAS 158. Glatfelter, while overfunded by $155.3 million, would reduce its reported pension asset by $90 million under SFAS 158. Although AMR currently recognizes a pension liability of $882 million, SFAS 158 would require AMR to significantly increase its reported pension liability to $3,225 million.An Illustration of the Transition to SFAS 158The following example uses the actual 2005 data from Exhibit 1 to illustrate how each of these companies would record the transition to the new rules. Because SFAS 158 is generally first effective for fiscal years ending after December 15, 2006, the actual numbers these companies record upon transition to SFAS 158 will differ from those in this example. For simplicity, the illustration ignores tax effects.Exhibit 1 shows that each of the three companies reports additional minimum liabilities and related intangible assets on its balance sheet. These items are eliminated under SFAS 158. In addition, pension assets and liabilities and accumulated other comprehensive income are adjustedso that their ending balances conform to the amounts required under SFAS 158. The necessary journal entries to accomplish the transition, using 2005 data, are presented in Exhibit 2.Exhibit 3 shows the balance-sheet reporting for each company after posting the entries in Exhibit 2, and exposes several important points. First, each company reports its funded status as either a pension asset or liability. Second, the balance in accumulated other comprehensive income equals the amount of previously unrecognized items. In this example, and likely for many companies with defined benefit plans, the amount of this contra-shareholders’ equity will increase under SFAS 158, even potentially generating negative shareholders’ equity. The transition to SFAS 158 might impose costs on leveraged firms due to the increased likelihood of tightening restrictive debt covenants. Finally, the balance-sheet presentation, and each company’s funded status, should be easier to understand after SFAS 158 is implemented.Subsequent Application of SFAS 158SFAS 158 does not impact the amount of periodic pension cost reported on the income statement, but it does impact the reporting of comprehensive income. For example, assume that after implementing SFAS 158 Lockheed Martin were to report the financial results in Exhibit 4. Again, these amounts are for illustrative purposes only.Exhibit 5 shows the required journal entries. The first entry records the service cost, interest cost, and expected return on plan assets components of periodic pension cost. The second entry reclassifies the amortization items from accumulated other comprehensive income to periodic pension cost, and the third entry adjusts the pension liability and accumulated other comprehensive income for the difference in actual pension returns above expectations during the year.Author: Kenneth W. ShawNationality: ColumbiaOriginate from: The CPA Journal译文二设定收益制养老金会计新准则2008年3月SFAS颁布了158号《雇主对既定福利养老金和其他退休后计划的会计处理》对FASB第87、88、106号准则做了修订,显著改变了资产负债表对设定收益制下养老金的列报。

会计术语中英文对照表