巴塞尔新资本协议_中文版

巴塞尔资本协议中英文完整版(首封)

概述导言1. 巴塞尔银行监管委员会(以下简称委员会)现公布巴塞尔新资本协议(BaselII,以下简称巴塞尔II)第三次征求意见稿(CP3,以下简称第三稿)。

第三稿的公布是构建新资本充足率框架的一项重大步骤。

委员会的目标仍然是在今年第四季度完成新协议,并于2006年底在成员国开始实施。

2. 委员会认为,完善资本充足率框架有两方面的公共政策利好。

一是建立不仅包括最低资本而且还包括监管当局的监督检查和市场纪律的资本管理规定。

二是大幅度提高最低资本要求的风险敏感度。

3. 完善的资本充足率框架,旨在促进鼓励银行强化风险管理能力,不断提高风险评估水平。

委员会认为,实现这一目标的途径是,将资本规定与当今的现代化风险管理作法紧密地结合起来,在监管实践中并通过有关风险和资本的信息披露,确保对风险的重视。

4. 委员会修改资本协议的一项重要内容,就是加强与业内人士和非成员国监管人员之间的对话。

通过多次征求意见,委员会认为,包括多项选择方案的新框架不仅适用于十国集团国家,而且也适用于世界各国的银行和银行体系。

5. 委员会另一项同等重要的工作,就是研究参加新协议定量测算影响分析各行提出的反馈意见。

这方面研究工作的目的,就是掌握各国银行提供的有关新协议各项建议对各行资产将产生何种影响。

特别要指出,委员会注意到,来自40多个国家规模及复杂程度各异的350多家银行参加了近期开展的定量影响分析(以下称简QIS3)。

正如另一份文件所指出,QIS3的结果表明,调整后新框架规定的资本要求总体上与委员会的既定目标相一致。

6. 本文由两部分内容组成。

第一部分简单介绍新资本充足框架的内容及有关实施方面的问题。

在此主要的考虑是,加深读者对新协议银行各项选择方案的认识。

第二部分技术性较强,大体描述了在2002年10月公布的QIS3技术指导文件之后对新协议有关规定所做的修改。

第一部分新协议的主要内容7. 新协议由三大支柱组成:一是最低资本要求,二是监管当局对资本充足率的监督检查,三是信息披露。

巴塞尔资本新协议(doc 14页)

巴塞尔资本新协议(doc 14页)概述导言1. 巴塞尔银行监管委员会(以下简称委员会)现公布巴塞尔新资本协议(Basel II, 以下简称巴塞尔II)第三次征求意见稿(CP3,以下简称第三稿)。

第三稿的公布是构建新资本充足率框架的一项重大步骤。

委员会的目标仍然是在今年第四季度完成新协议,并于2006年底在成员国开始实施。

2. 委员会认为,完善资本充足率框架有两方面的公共政策利好。

一是建立不仅包括最低资本而且还包括监管当局的监督检查和市场纪律的资本管理规定。

二是大幅度提高最低资本要求的风险敏感度。

3. 完善的资本充足率框架,旨在促进鼓励银行强化风险管理能力,不断提高风险评估水平。

委员会认为,实现这一目标的途径是,将资本规定与当今的现代化风险管理作法紧密地结合起来,在监管实践中并通过有关风险和资本的信息披露,确保对风险的重视。

4. 委员会修改资本协议的一项重要内容,就是加强与业内人士和非成员国监管人员之间的对话。

通过多次征求意见,委员会认为,包括多项选择方案的新框架不仅适用于十国集团国家,而且也适用于世界各国的银行和银行体系。

5. 委员会另一项同等重要的工作,就是研究参加新协议定量测算影响分析各行提出的反馈意见。

这方面研究工作的目的,就是掌握各国银行提供的有关新协议各项建议对各行资产将产生何种影响。

特别要指出,委员会注意到,来自40多个国家规模及复杂程度各异的350多家银行参加了近期开展的定量影响分析(以下称简QIS3)。

正如另一份文件所指出,QIS3的结果表明,调整后新框架规定的资本要求总体上与委员会的既定目标相一致。

6. 本文由两部分内容组成。

第一部分简单介绍新资本充足框架的内容及有关实施方面的问题。

在此主要的考虑是,加深读者对新协议银行各项选择方案的认识。

第二部分技术性较强,大体描述了在2002年10月公布的QIS3技术指导文件之后对新协议有关规定所做的修改。

第一部分新协议的主要内容7. 新协议由三大支柱组成:一是最低资本要求,二是监管当局对资本充足率的监督检查,三是信息披露。

巴塞尔新资本协议第三版(中文版)-232页

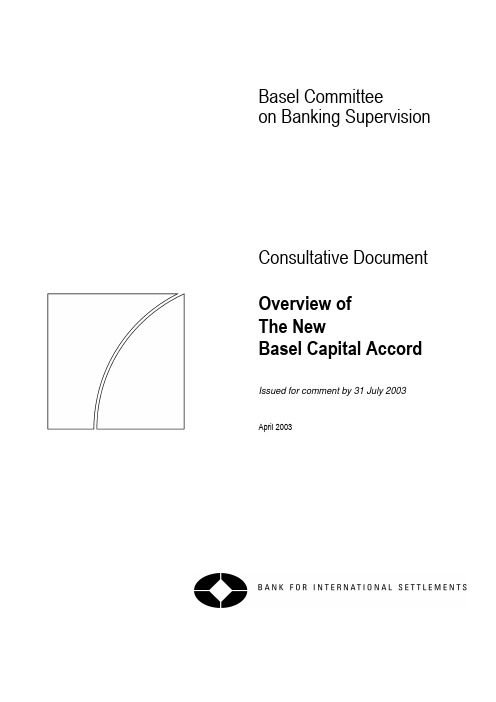

巴塞尔委员会Basel Committeeon Banking Supervision征求意见稿(第三稿)巴塞尔新资本协议The NewBasel Capital Accord 中国银行业监督管理委员会翻译目录概述 (10)导言 (10)第一部分新协议的主要内容 (11)第一支柱:最低资本要求 (11)信用风险标准法 (11)内部评级法(Internal ratings-based (IRB) approaches) (12)公司、银行和主权的风险暴露 (13)零售风险暴露 (14)专业贷款(Specialised lending) (14)股权风险暴露(Equity exposures) (14)IRB法的实施问题 (15)证券化 (15)操作风险 (16)第二支柱和第三支柱:监管当局的监督检查和市场纪律 (17)监管当局的监督检查 (17)市场纪律 (18)新协议的实施 (18)朝新协议过渡 (18)有关前瞻性问题 (19)跨境实施问题 (20)今后的工作 (20)第二部分: 对QIS3技术指导文件的修改 (21)导言 21允许使用准备 (21)合格的循环零售风险暴露(qualifying revolving retail exposures,QRRE)..22住房抵押贷款 (22)专业贷款(specialised lending, SL) (22)高波动性商业房地产(high volatility commercial real estate ,HVCRE).23信用衍生工具 (23)证券化 (23)操作风险 (24)缩写词 (26)第一部分:适用范围 (28)A.导言 (28)B.银行、证券公司和其他附属金融企业 (28)C.对银行、证券公司和其他金融企业的大额少数股权投资 (29)D.保险公司 (29)E.对商业企业的大额投资 (30)F.根据本部分的规定对投资的扣减 (31)第二部分:第一支柱-最低资本要求 (33)I. 最低资本要求的计算 (33)II.信用风险-标准法(Standardised Approach) (33)A.标准法 — 一般规则 (33)1.单笔债权的处理 (34)(i)对主权国家的债权 (34)(ii)对非中央政府公共部门实体(public sector entities)的债权 (35)(iii)对多边开发银行的债权 (35)(iv) 对银行的债权 (36)(v)对证券公司的债权 (37)(vi)对公司的债权 (37)(vii)包括在监管定义的零售资产中的债权 (37)(viii) 对居民房产抵押的债权 (38)(ix)对商业房地产抵押的债权 (38)(x)逾期贷款 (39)(xi)高风险的债权 (39)(xii)其他资产 (40)(xiii) 资产负债表外项目 (40)2.外部评级 (40)(i)认定程序 (40)(ii)资格标准 (40)3.实施中需考虑的问题 (41)(i)对应程序(mapping process) (41)(ii)多方评级结果的处理 (42)(iii)发行人评级和债项评级(issuer versus issues assessment) (42)(iv)本币和外币的评级 (42)(v)短期和长期评级 (43)(vi)评级的适用范围 (43)(vii)被动评级(unsolicited ratings) (43)B. 标准法—信用风险缓释(Credit risk mitigation) (44)1.主要问题 (44)(i)综述 (44)(ii) 一般性论述 (44)(iii)法律确定性 (45)2.信用风险缓释技术的综述 (45)(i)抵押交易 (45)(ii) 表内净扣(On-balance sheet netting) (47)(iii)担保和信用衍生工具 (47)(iv) 期限错配 (47)(v) 其他问题 (48)3.抵押品 (48)(i)合格的金融抵押品 (48)(ii) 综合方法 (49)(iii)简单方法 (56)(iv) 抵押的场外衍生工具交易 (57)4.表内净扣 (57)5.担保和信用衍生工具 (58)(i)操作要求 (58)(ii)合格的担保人/信用保护提供者的范围 (60)(iii)风险权重 (60)(iv)币种错配 (60)(v)主权担保 (61)6.期限错配 (61)7.与信用风险缓释相关的其他问题的处理 (62)(i)对信用风险缓释技术池(pools of CRM techniques)的处理 (62)(ii) 第一违约的信用衍生工具 (62)(iii)第二违约的信用衍生工具 (62)III. 信用风险——IRB法 (62)A.概述 (62)B.IRB法的具体要求 (63)1.风险暴露类别 (63)(i) 公司暴露的定义 (63)(ii) 主权暴露的定义 (65)(iii) 银行暴露的定义 (65)(iv) 零售暴露的定义 (65)(v)合格的循环零售暴露的定义 (66)(vi) 股权暴露的定义 (67)(vii)合格的购入应收账款的定义 (68)2.初级法和高级法 (69)(i)公司、主权和银行暴露 (69)(ii) 零售暴露 (70)(iii) 股权暴露 (70)(iv) 合格的购入应收账款 (70)3. 在不同资产类别中采用IRB法 (70)4.过渡期安排 (71)(i)采用高级法的银行平行计算资本充足率 (71)(ii) 公司、主权、银行和零售暴露 (72)(iii) 股权暴露 (72)C.公司、主权、及银行暴露的规定 (73)1.公司、主权和银行暴露的风险加权资产 (73)(i)风险加权资产的推导公式 (73)(ii) 中小企业的规模调整 (73)(iii) 专业贷款的风险权重 (74)2.风险要素 (75)(i)违约概率 (75)(iii)违约风险暴露 (79)(iv) 有效期限 (80)D.零售暴露规定 (82)1.零售暴露的风险加权资产 (82)(i) 住房抵押贷款 (82)(ii) 合格的循环零售贷款 (82)(iii) 其他零售暴露 (83)2.风险要素 (83)(i)违约概率和违约损失率 (83)(ii) 担保和信贷衍生产品的认定 (83)(iii) 违约风险暴露 (83)E.股权暴露的规则 (84)1.股权暴露的风险加权资产 (84)(i)市场法 (84)(ii) 违约概率/违约损失率方法 (85)(iii) 不采用市场法和违约概率/违约损失率法的情况 (86)2. 风险要素 (87)F. 购入应收账款的规则 (87)1.违约风险的风险加权资产 (87)(i)购入的零售应收账款 (87)(ii) 购入的公司应收账款 (87)2.稀释风险的风险加权资产 (89)(i)购入折扣的处理 (89)(ii) 担保的认定 (89)G. 准备的认定 (89)H.IRB法的最低要求 (90)1.最低要求的内容 (91)2.遵照最低要求 (91)3.评级体系设计 (91)(i)评级维度 (92)(ii) 评级结构 (93)(iv) 评估的时间 (94)(v)模型的使用 (95)(vi) 评级体系设计的记录 (95)4.风险评级体系运作 (96)(i) 评级的涵盖范围 (96)(ii) 评级过程的完整性 (96)(iii) 推翻评级的情况(Overrides) (97)(iv) 数据维护 (97)(v)评估资本充足率的压力测试 (98)5. 公司治理和监督 (98)(i)公司治理(Corporate governance) (98)(ii) 信用风险控制 (99)(iii) 内审和外审 (99)6. 内部评级的使用 (99)7.风险量化 (100)(i)估值的全面要求 (100)(ii) 违约的定义 (101)(iii) 重新确定帐龄(Re-ageing) (102)(iv) 对透支的处理 (102)(v) 所有资产类别损失的的定义 (102)(vi) 估计违约概率的要求 (102)(vii) 自行估计违约损失率的要求 (104)(viii) 自己估计违约风险暴露的要求 (104)(ix) 评估担保和信贷衍生产品成熟性效应的最低要求 (106)(x)估计合格的购入应收账款违约概率和违约损失率的要求 (107)8. 内部评估的验证 (109)9. 监管当局确定的违约损失率和违约风险暴露 (110)(i)商用房地产和居民住房作为抵押品资格的定义 (110)(ii) 合格的商用房地产/居民住房的操作要求 (110)(iii) 认定金融应收账款的要求 (111)10.认定租赁的要求 (113)11.股权暴露资本要求的计算 (114)(i)内部模型法下的市场法 (114)(ii) 资本要求和风险量化 (114)(iv) 验证和形成文件 (116)12.披露要求 (118)IV.信用风险--- 资产证券化框架 (119)A.资产证券化框架下所涉及交易的范围和定义 (119)B. 定义 (120)1. 银行所承担的不同角色 (120)(i)银行作为投资行 (120)(ii) 银行作为发起行 (120)2. 通用词汇 (120)(i) 清收式赎回(clean-up call) (120)(ii) 信用提升(credit enhancement) (120)(iii) 提前摊还(early amortisation) (120)(iv) 超额利差(excess spread) (121)(v)隐性支持(implicit support) (121)(vi) 特别目的机构(Special purpose entity (SPE)) (121)C. 确认风险转移的操作要求 (121)1.传统型资产证券化的操作要求 (121)2.对合成型资产证券化的操作要求 (122)3.清收式赎回的操作要求和处理 (123)D. 对资产证券化风险暴露的处理 (123)1.最低资本要求 (123)(i)扣减 (123)(ii) 隐性支持 (123)2. 使用外部信用评估的操作要求 (124)3. 资产证券化风险暴露的标准化方法 (124)(i) 范围 (124)(ii) 风险权重 (125)(iii) 对于未评级资产证券化风险暴露一般处理方法的例外情况 (125)(iv) 表外风险资产的信用转换系数 (126)(v)信用风险缓释的确认 (127)(vi) 提前摊还规定的资本要求 (128)(viii)对于非控制型具有提前摊还特征的风险暴露的信用风险转换系数的确定 (130)4.资产证券化的内部评级法 (131)(i)范围 (131)(ii) KIRB定义 (131)(iii) 各种不同的方法 (132)(iv) 所需资本最高限 (133)(v) 以评级为基础的方法 (133)(vi) 监管公式 (135)(vii)流动性便利 (137)(viii) 合格服务人现金透支便利 (138)(ix) 信用风险缓释的确认 (138)(x) 提前摊还的资本要求 (138)V. 操作风险 (139)A. 操作风险的定义 (139)B. 计量方法 (139)1.基本指标法 (139)2.标准法 (140)3.高级计量法(Advanced Measurement Approaches ,AMA) (141)C.资格标准 (142)1.一般标准 (142)2.标准法 (142)3. 高级计量法 (143)D.局部使用 (147)VI.交易账户 (148)A.交易账户的定义 (148)B.审慎评估标准 (149)1.评估系统和控制手段 (149)2.评估方法 (149)3.计值调整(储备) (150)C.交易账户对手信用风险的处理 (151)D.标准法对交易账户特定风险资本要求的处理 (152)1.政府债券的特定风险资本要求 (152)2.对未评级债券特定风险的处理原则 (152)3. 采用信用衍生工具套做保值头寸的专项资本要求 (152)4.信用衍生工具的附加系数 (153)第三部分:监督检查 (155)A.监督检查的重要性 (155)B.监督检查的四项主要原则 (155)C.监督检查的具体问题 (161)D:监管检查的其他问题 (167)第四部分:第三支柱——市场纪律 (169)A.总体考虑 (169)1.披露要求 (169)2.指导原则 (169)3.恰当的披露 (169)4. 与会计披露的相互关系 (169)5.重要性(Materiality) (170)6.频率 (170)B.披露要求 (171)1.总体披露原则 (171)2.适用范围 (171)3.资本 (173)4.风险暴露和评估 (175)(i)定性披露的总体要求 (175)(ii)信用风险 (175)(iii)市场风险 (183)(iv)操作风险 (184)(v)银行账户的利率风险 (184)附录1 创新工具在一级资本中的上线为15% (185)附录2 标准法-实施对应程序 (186)附录3 IRB法风险权重的实例 (190)附录4 监管当局对专业贷款设定的标准 (193)附录5 按照监管公式计算信用风险缓释的影响 (207)附录 6 (211)附录7 损失事件分类详表 (215)附录8 (220)概 述导言1.巴塞尔银行监管委员会(以下简称委员会)现公布巴塞尔新资本协议(Basel II, 以下简称巴塞尔II)第三次征求意见稿(CP3,以下简称第三稿)。

巴塞尔协议3(中文版)

巴塞尔银行监管委员会增强银行体系稳Array健性征求意见截至2010年4月16日2009年12月目录I 摘要 (3)1. 巴塞尔委员会改革方案综述及其所应对的市场失灵 (3)2. 加强全球资本框架 (5)(a)提高资本基础的质量、一致性和透明度 (5)(b)扩大风险覆盖范围 (6)(c)引入杠杆率补充风险资本要求 (8)(d)缓解亲周期性和提高反周期超额资本 (8)(e)应对系统性风险和关联性 (11)3. 建立全球流动性标准 (11)4. 影响评估和校准 (12)II加强全球资本框架 (14)1. 提高资本基础的质量、一致性和透明度 (14)(a)介绍 (14)(b)理由和目的 (15)(c)建议的核心要点 (16)(d)具体建议 (18)(e)一级资本中普通股的分类 (19)(f)披露要求 (28)2. 风险覆盖 (29)交易对手信用风险 (29)(a)介绍 (29)(b)发现的主要问题 (29)(c)政策建议概览 (31)降低对外部信用评级制度的依赖性,降低悬崖效应的影响 (53)3. 杠杆率 (59)(a)资本计量 (60)(b)风险暴露计量 (60)(c)其它事宜 (63)(d)计算基础建议概述 (64)4. 亲周期效应 (65)(a)最低资本要求的周期性 (65)(b)具有前瞻性的拨备 (65)(c)通过资本留存建立超额资本 (66)(d)信贷过快增长 (69)缩写词增强银行体系稳健性I. 摘要1.巴塞尔委员会改革方案综述及其所应对的市场失灵1. 本征求意见稿提出巴塞尔委员会1关于加强全球资本监管和流动性监管的政策建议,目标是提升银行体系的稳健性。

巴塞尔委员会改革的总体目标是改善银行体系应对由各种金融和经济压力导致的冲击的能力,并降低金融体系向实体经济的溢出效应。

2. 本文件提出的政策建议是巴塞尔委员会应对本轮金融危机而出台全面改革规划的关键要素。

巴塞尔委员会实施改革的目的是改善风险管理和治理以及加强银行的透明度和信息披露2。

巴塞尔新资本协议_中文版

内部程序

系统

外部事件

操作风险的度量方法

基本指标法、标准法、高级计量法

操作风险的度量方法:基本指标法 基本指标法

银行持有的操作风险资本应等于前三年总收入的平均值 乘上一个固定比例(用α表示)。资本计算公式如下:

KBIA = GI * α

其中,KBIA = 基本指标法需要的资本, GI = 前三年总收入的平均值, α = 15%,由巴塞尔委员会设定。 总收入定义为:净利息收入加上非利息收入。这种 计算方法旨在(1)反映所有准备(例如,未付利息的准备)的 总额;(2)不包括银行账户上出售证券实现的利润(或损失) ; (3)不包括特殊项目以及保险收入。

资本充足率 = 信用风险, ƒ (信用风险, 市场风 操作风险) 险, 操作风险)

市场风险的衡量方法

标准法

对市场风险的最低资本要求=利率风险+股权投 资风险+外汇风险+大宗商品风险+期权风险

内部模型法

对市场风险的最低资本要求=前一个交易日的 VAR 或 3*前六十个交易日的平均VAR

(以高者为准)

操作风险

操作风险的定义 操作风险的度量方法

操作风险的定义

由于内部操作流程不完善、人为过失、系统故 障或外部突发事件造成的损失。 操作风险事件分类

内部欺诈 外界欺诈 雇佣事项及工作场所安全性 客户、产品及业务方式 有形资产的损坏 业务中断及系统故障 操作流程管理

BBA关于操作风险的界定

第一级: 第一级:因素 人 第二级: 第二级:定义 (1)雇员欺诈、犯罪;(2)越权行为、欺诈交 易、操作失误 (3)违反用工法;(4)劳动力中断; (5)关键人员流失或缺乏 (1)支付清算、传输风险;(2)文件、合同风 险;(3)估价、定价风险;(4)内部、外部报 告风险;(5)执行风险;(6)策略风险、管理 变动;(6)出售风险;(7)科技投资风险 (1)系统开发和执行;(2)系统功能; (3)系统失败;(4)系统安全 (1)法律、公共责任;(2)犯罪;(3)外部 采购、供应商风险;(4)外部开发风险;(5) 灾难、基础设施;(6)政策调整(7)政治、政 府风险

巴塞尔资本协议中英文完整版(13附录5)

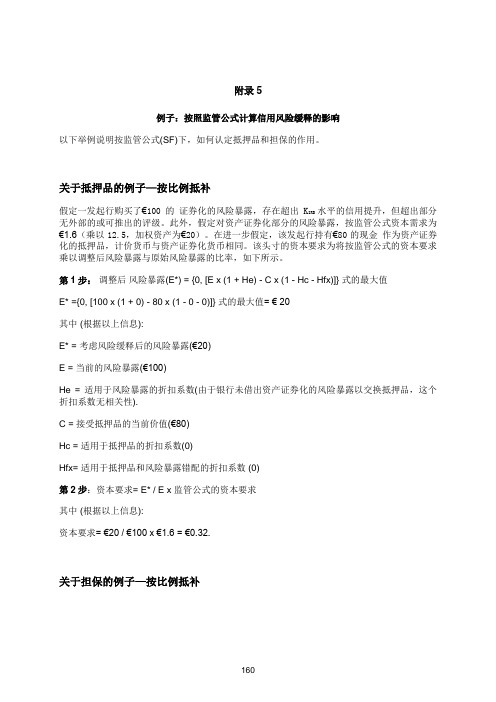

附录5例子:按照监管公式计算信用风险缓释的影响以下举例说明按监管公式(SF)下,如何认定抵押品和担保的作用。

关于抵押品的例子—按比例抵补假定一发起行购买了€100 的证券化的风险暴露,存在超出K IRB 水平的信用提升,但超出部分无外部的或可推出的评级。

此外,假定对资产证券化部分的风险暴露,按监管公式资本需求为€1.6(乘以12.5,加权资产为€20)。

在进一步假定,该发起行持有€80的现金作为资产证券化的抵押品,计价货币与资产证券化货币相同。

该头寸的资本要求为将按监管公式的资本要求乘以调整后风险暴露与原始风险暴露的比率,如下所示。

第1步:调整后风险暴露(E*) = {0, [E x (1 + He) - C x (1 - Hc - Hfx)]} 式的最大值E* ={0, [100 x (1 + 0) - 80 x (1 - 0 - 0)]} 式的最大值= € 20其中 (根据以上信息):E* = 考虑风险缓释后的风险暴露(€20)E = 当前的风险暴露(€100)He = 适用于风险暴露的折扣系数(由于银行未借出资产证券化的风险暴露以交换抵押品,这个折扣系数无相关性).C = 接受抵押品的当前价值(€80)Hc = 适用于抵押品的折扣系数(0)Hfx= 适用于抵押品和风险暴露错配的折扣系数 (0)第2步:资本要求= E* / E x 监管公式的资本要求其中 (根据以上信息):资本要求= €20 / €100 x €1.6 = €0.32.关于担保的例子—按比例抵补除信用风险缓释工具外,该例子中所有涉及抵押品的假设条件均适用。

假定发起行持有其他银行提供的合格,无抵押品的担保,金额为80€。

因此,货币错配的折扣系数不适用。

资本要求如下所示:∙ 资产证券化的保护部分(80€ )的风险权重为保护提供者的风险权重。

保护提供者的风险权重与提供给担保银行无担保贷款的风险权重相同,在内部评级法下也是如此。

假定风险权重是10%。

巴塞尔资本协议中英文完整版(10附录2(英文))

Annex 2Standardised Approach - Implementing the Mapping Process1. Because supervisors will be responsible for assigning eligible ECAI’s credit risk assessments to the risk weights available under the standardised approach, they will need to consider a variety of qualitative and quantitative factors to differentiate between the relative degrees of risk expressed by each assessment. Such qualitative factors could include the pool of issuers that each agency covers, the range of ratings that an agency assigns, each rating’s meaning, and each agency’s definition of default, among others.2. Quantifiable parameters may help to promote a more consistent mapping of credit risk assessments into the available risk weights under the standardised approach. This annex summarises the Committee’s proposals to help supervisors with mapping exercises. The parameters presented below are intended to provide guidance to supervisors and are not intended to establish new or complement existing eligibility requirements for ECAIs. Evaluating CDRs: two proposed measures3. To help ensure that a particular risk weight is appropriate for a particular credit risk assessment, the Committee recommends that supervisors evaluate the cumulative default rate (CDR) associated with all issues assigned the same credit risk rating. Supervisors would evaluate two separate measures of CDRs associated with each risk rating contained in the standardised approach, using in both cases the CDR measured over a three-year period.∙To ensure that supervisors have a sense of the long-run default experience over time, supervisors should evaluate the ten-year average of the three-year CDR when this depth of data is available.150 For new rating agencies or for those that have compiled less than ten years of default data, supervisors may wish to ask rating agencies what they believe the 10-year average of the three-year CDR would be for each risk rating and hold them accountable for such an evaluation thereafter for the purpose of risk weighting the claims they rate.∙The other measure that supervisors should consider is the most recent three-year CDR associated with each credit risk assessment of an ECAI4. Both measurements would be compared to aggregate, historical default rates of credit risk assessments compiled by the Committee that are believed to represent an equivalent level of credit risk.5. As three-year CDR data is expected to be available from ECAIs, supervisors should be able to compare the default experience of a particular ECAI’s assessments with t hose issued by other rating agencies, in particular major agencies rating a similar population.150 In 2002, for example, a supervisor would calculate the average of the three-year CDRs for issuers assigned to each rating grade (the “cohort”) for each of the ten years 1990-1999.170Mapping risk ratings to risk weights using CDRs6. To help supervisors determine the appropriate risk weights to which an ECAI’s risk ratings should be mapped, each of the CDR measures mentioned above could be compared to the following reference and benchmark values of CDRs:∙For each step in an ECAI’s rating scale, a ten-year average of the three-year CDR would be compared to a long run “reference” three-year CDR that would represent a sense of the long-run international default experience of risk assessments.∙Likewise, for each step in the ECAI’s rating scale, the two most recent three-year CDR would be compared to “benchmarks” for CDRs. This comparison would be intended to determine whether the ECAI’s most recent record of assessing credit risk remains within the CDR supervisory benchmarks.7. Table 1 below illustrates the overall framework for such comparisons.Table 1Comparisons of CDR Measures1511. Comparing an ECAI’s long-run average three-year CDR to a long-run“reference” CDR8. For each credit risk category used in the standardised approach of the New Accord, the corresponding long-run reference CDR would provide information to supervisors on what its default experience has been internationally. The ten-year average of an eligible ECAI’s particular assessment would not be expected to match exactly the long-run reference CDR. The long run CDRs are meant as guidance for supervisors, and not as “targets” that ECAIs would have to meet. The recommended long-run “reference” three-year CDRs for each of the Committee’s credit risk categories are presented in Table 2 below, based on the Committee’s observations of the default experience reported by major rating agencies internationally.151 It should be noted that each major rating agency would be subject to these comparisons as well, in which its individual experience would be compared to the aggregate international experience.171Table 2Proposed long run "reference" three-year CDRs2. Comparing an ECAI’s most recent three-year CDR to CDR Benchmarks9. Since an ECAI’s own CDRs are not intended to match the reference CDRs exactly, it is important to provide a better sense of what upper bounds of CDRs are acceptable for each assessment, and hence each risk weight, contained in the standardised approach. 10. It is the Committee’s general sense that the upper bounds for CDRs should serve as guidance for supervisors and not necessarily as mandatory requirements. Exceeding the upper bound for a CDR would therefore not necessarily require the supervisor to increase the risk weight associated with a particular assessment in all cases if the supervisor is convinced that the higher CDR results from some temporary cause other than weaker credit risk assessment standards.11. To assist supervisors in interpreting whether a CDR falls within an acceptable range for a risk rating to qualify for a particular risk weight, two benchmarks would be set for each assessment, namely a “monitoring” level benchmark and a “trigger” level benchmark.(a) “Monitoring” level benchmark12. Exceeding the “monitoring” level CDR benchmark implies that a rating agency’s current default experience for a particular credit risk-assessment grade is markedly higher than international default experience. Although such assessments would generally still be considered eligible for the associated risk weights, supervisors would be expected to consult with the relevant rating agency to understand why the default experience appears to be significantly worse. If supervisors determine that the higher default experience is attributable to weaker standards in assessing credit risk, they would be expected to assign a higher risk category to the agency’s credit risk assessment.(b) “Trigger” level13. Exceeding the “trigger” level benchmark implies that a rating agency’s default experience is considerably above the international historical default experience for a p articular assessment grade. Thus there is a presumption that the ECAI’s standards for assessing credit risk are either too weak or are not applied appropriately. If the observed three-year CDR exceeds the trigger level in two consecutive years, supervisors would be expected to move the risk assessment into a less favourable risk category. However, if supervisors determine that the higher observed CDR is not attributable to weaker 172assessment standards, then they may exercise judgement and retain the original risk weight.15214. In all cases where the supervisor decides to leave the risk category unchanged, it may wish to rely on Pillar 2 of the New Accord and encourage banks to hold more capital temporarily or to establish higher reserves.15. When the supervisor has increased the associated risk category, there would be the opportunity for the assessment to again map to the original risk category if the ECAI is able to demonstrate that its three-year CDR falls and remains below the monitoring level for two consecutive years.(c) Calibrating the benchmark CDRs16. After reviewing a variety of methodologies, the Committee decided to use Monte Carlo simulations to calibrate both the monitoring and trigger levels for each credit risk assessment category. In particular, the proposed monitoring levels were derived from the 99.0th percentile confidence interval and the trigger level benchmark from the 99.9th percentile confidence interval. The simulations relied on publicly available historical default data from major international rating agencies. The levels derived for each risk assessment category are presented in Table 3 below, rounded to the first decimal:Table 3Proposed three-year CDR benchmarks152 For example, if supervisors determine that the higher default experience is a temporary phenomenon, perhaps because it reflects a temporary or exogenous shock such as a natural disaster, then the risk weighting proposed in the standardised approach could still apply. Likewise, a breach of the trigger level by several ECAIs simultaneously may indicate a temporary market change or exogenous shock as opposed to a loosening of credit standards. In either scenario, supervisors would be expected to monitor the ECAI’s assessments to ensure that the higher default experience is not the result of a loosening of credit risk assessment standards.173。

巴塞尔资本协议中英文完整版(17附录9)

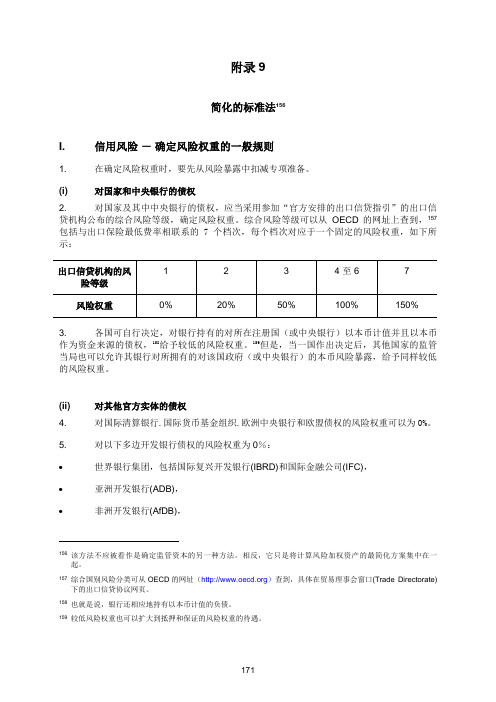

附录9简化的标准法156I. 信用风险-确定风险权重的一般规则1. 在确定风险权重时,要先从风险暴露中扣减专项准备。

(i) 对国家和中央银行的债权2. 对国家及其中中央银行的债权,应当采用参加“官方安排的出口信贷指引”的出口信贷机构公布的综合风险等级,确定风险权重。

综合风险等级可以从OECD的网址上查到,157包括与出口保险最低费率相联系的7个档次,每个档次对应于一个固定的风险权重,如下所示:3. 各国可自行决定,对银行持有的对所在注册国(或中央银行)以本币计值并且以本币作为资金来源的债权,158给予较低的风险权重。

159但是,当一国作出决定后,其他国家的监管当局也可以允许其银行对所拥有的对该国政府(或中央银行)的本币风险暴露,给予同样较低的风险权重。

(ii) 对其他官方实体的债权4. 对国际清算银行.国际货币基金组织.欧洲中央银行和欧盟债权的风险权重可以为0%。

5. 对以下多边开发银行债权的风险权重为0%:∙世界银行集团,包括国际复兴开发银行(IBRD)和国际金融公司(IFC),∙亚洲开发银行(ADB),∙非洲开发银行(AfDB),156该方法不应被看作是确定监管资本的另一种方法。

相反,它只是将计算风险加权资产的最简化方案集中在一起。

157综合国别风险分类可从OECD的网址()查到,具体在贸易理事会窗口(Trade Directorate)下的出口信贷协议网页。

158也就是说,银行还相应地持有以本币计值的负债。

159较低风险权重也可以扩大到抵押和保证的风险权重的待遇。

∙欧洲复兴开发银行(EBRD),∙泛美开发银行(IADB),∙欧洲投资银行(EIB),∙北欧投资银行(NIB),∙加勒比海开发银行(CDB),∙伊斯兰开发银行(IDB),∙欧洲开发银行理事会(CEDB)6. 对其他多边开发银行债权的标准风险权重为100%。

7. 对国内公共部门实体的债权,可以采用对银行债权风险权重的方案,确定风险权重。

巴塞尔新资本协议

概述导言1. 巴塞尔银行监管委员会(以下简称委员会)现公布巴塞尔新资本协议(Basel II, 以下简称巴塞尔II)第三次征求意见稿(CP3,以下简称第三稿)。

第三稿的公布是构建新资本充足率框架的一项重大步骤。

委员会的目标仍然是在今年第四季度完成新协议,并于2006年底在成员国开始实施。

2. 委员会认为,完善资本充足率框架有两方面的公共政策利好。

一是建立不仅包括最低资本而且还包括监管当局的监督检查和市场纪律的资本管理规定。

二是大幅度提高最低资本要求的风险敏感度。

3. 完善的资本充足率框架,旨在促进鼓励银行强化风险管理能力,不断提高风险评估水平。

委员会认为,实现这一目标的途径是,将资本规定与当今的现代化风险管理作法紧密地结合起来,在监管实践中并通过有关风险和资本的信息披露,确保对风险的重视。

4. 委员会修改资本协议的一项重要内容,就是加强与业内人士和非成员国监管人员之间的对话。

通过多次征求意见,委员会认为,包括多项选择方案的新框架不仅适用于十国集团国家,而且也适用于世界各国的银行和银行体系。

5. 委员会另一项同等重要的工作,就是研究参加新协议定量测算影响分析各行提出的反馈意见。

这方面研究工作的目的,就是掌握各国银行提供的有关新协议各项建议对各行资产将产生何种影响。

特别要指出,委员会注意到,来自40多个国家规模及复杂程度各异的350多家银行参加了近期开展的定量影响分析(以下称简QIS3)。

正如另一份文件所指出,QIS3的结果表明,调整后新框架规定的资本要求总体上与委员会的既定目标相一致。

6. 本文由两部分内容组成。

第一部分简单介绍新资本充足框架的内容及有关实施方面的问题。

在此主要的考虑是,加深读者对新协议银行各项选择方案的认识。

第二部分技术性较强,大体描述了在2002年10月公布的QIS3技术指导文件之后对新协议有关规定所做的修改。

第一部分新协议的主要内容7. 新协议由三大支柱组成:一是最低资本要求,二是监管当局对资本充足率的监督检查,三是信息披露。

新资本协议全文

巴塞尔新的资本协议强调,银行仅通过资本充足率的规定无法实现安全性和稳健性的目标,应通过一些更加全面、具体的约束加以实现。

为此,该协议提出三大支柱,即最低资本要求、监管当局检查评估和市场纪律约束,并作为该协议的主要内容。

1.最低资本要求。

这是该协议的基础,主要包括三方面的内容,即监管部门对资本的定义、风险头寸的计量及根据风险程度计算的最低资本要求。

其中监管部门对资本的定义和8%的最低资本充足比率,维持原资本协议的规定不变。

但在风险头寸的计量方面,新资本协议提出了更高的要求。

对于风险资产的计算,在调整了原有“标准法”计算风险资产的同时,强调对于十分先进的银行可以采用内部评级法计算风险资产,对于一些高度发达的银行,在进行风险管理时,可以运用信用组合风险模型。

此外,在风险管理的范围上,除须涵盖原协议要求的信用风险和市场风险外,对于银行所面临的其他风险,如利率风险、操作风险、法律风险等也应特别关注。

2.监管部门对资本充足率的评估检查。

这方面要求加大监管机构对银行的监管力度,确保各家商业银行建立起行之有效的内部程序,借以评估银行在认真分析风险的基础上设定的资本充足率。

具体原则包括:银行应参照其承担风险的程度,建立资本充足总体情况的内部评价机制,制定维持资本水平的战略;监管当局对资本充足情况的内部评价机制、维持战略、资本充足情况进行检测和评价;监管部门要求银行保持高于最低资本监管要求的资本充足率;监管当局对银行资本充足率下滑的状况进行及早干预,防止风险的扩散,如果资本得不到恢复,则应及时采取补救措施。

3.市场纪律约束。

这方面要求发挥市场的力量来促使银行稳健、高效地经营以及保持较高的资本充足率。

市场纪律有助于促使银行合理进行资本调节和控制内部风险。

有效的市场约束要求银行建立一定的信息披露制度。

新协议要求银行及时披露包括资本结构、资本充足率、对资本的内部评价机制、风险预测及战略管理等内容。

新资本协议的借鉴与启示新资本协议虽然不是国际法规,也不属于国际公约,对各国政府、银行监管当局及商业银行不具有强制的约束力。

巴塞尔资本协议中英文完整版(03目录)

目录第一部分:适用范围 (1)A. 导言 (1)B. 银行、证券公司和其他金融企业 (1)C. 对银行、证券公司和其他金融企业的大额少数股权投资 (2)D. 保险公司 (2)E. 对商业企业的大额投资 (3)F. 根据本部分的规定对投资的扣减 (4)第二部分:第一支柱-最低资本要求 (6)I. 最低资本充足率的计算 (6)II. 信用风险-标准法 (6)A. 标准法-一般规则 (6)1. 单笔债权的的处理 (7)(i) 对主权的债权 (7)(ii) 对非中央政府公共部门实体的债权 (7)(iii) 对多边开发银行的债权 (8)(iv) 对银行的债权 (8)(v) 对证券公司的债权 (9)(vi) 对公司的债权 (9)(vii) 包括在监管定义的零售资产中的债权 (10)(viii) 以居民房产抵押的债权 (10)(ix) 以商业房地产抵押的债权 (11)(x) 逾期贷款 (11)(xi) 高风险的债权 (11)(xii) 其他资产 (12)(xiii) 资产负债表外项目 (12)2. 外部评级 (12)(i) 认定程序 (12)(ii) 资格标准 (12)3. 实施中需考虑的问题 (13)(i) 对应程序 (13)(ii) 多方评级结果的处理 (13)(iii) 发行人评级和债项评级 (14)(iv) 本币和外币评级 (14)(v) 短期/长期评级 (14)(vi) 评级的适用范围 (15)(vii) 被动评级 (15)B. 标准法-信用风险缓释 (15)1. 主要问题 (15)(i) 综述 (15)(ii) 一般性论述 (16)(iii) 法律确定性 (16)2. 信用风险缓释技术的综述 (16)(i) 抵押交易 (16)(ii) 表内净扣 (18)(iii) 担保和衍生工具 (18)(iv) 期限错配 (18)(v) 其他问题 (19)3. 抵押 (19)(i) 合格的金融抵押品 (19)(ii) 综合法 (20)(iii) 简单法 (27)(iv) 抵押的场外衍生工具交易 (27)4. 表内净扣 (28)5. 担保和衍生工具 (28)(i) 操作要求 (28)(ii) 合格的担保人/信用保护提供者的范围 (30)(iii) 风险权重 (30)(iv) 币种错配 (30)(v) 国家担保 (31)6. 期限错配 (31)(i) 期限的定义 (31)(ii) 期限错配的风险权重 (31)7. 与信用风险缓释相关的其他问题的处理 (32)(i) 对信用风险缓释技术库的处理 (32)(ii) 第一违约的信用衍生工具 (32)(iii) 第二违约的信用衍生工具 32 III. 信用风险——IRB法 (32)A. 概述 (32)B. IRB法的具体要求 (32)1. 风险暴露类别 (33)(i) 公司暴露的定义 (33)(ii) 主权暴露的定义 (35)(iii) 银行暴露的定义 (35)(iv) 零售暴露的定义 (35)(v) 合格的循环零售风险暴露的定义 (35)(vi) 股权暴露的定义 (36)(vii) 合格的购入应收帐款的定义 (36)2. 初级法和高级法 (37)(i) 公司、主权和银行暴露 (38)(ii) 零售暴露 (38)(iii) 股权暴露 (39)(iv) 合格的购入应收帐款 (39)3. 在不同资产类别中采用IRB法 (39)4. 过渡期安排 (39)(i) 采用高级法的银行平行计算资本充足率 (40)(ii) 公司、主权、银行和零售暴露 (40)(iii) 股权暴露 (40)C. 公司、主权、及银行暴露的规定 (41)1. 公司、主权和银行暴露的风险加权资产 (41)(i) 风险加权资产的推导公式 (41)(ii) 中小企业的规模调整 (41)(iii) 专业贷款的风险权重 (42)2. 风险要素 (42)(i) 违约概率(PD) (43)(ii) 违约损失率 (LGD) (43)(iii) 违约风险暴露(EAD) (43)(iv) 有效期限(M) (47)D. 零售暴露规定 (48)1. 零售暴露的风险加权资产 (49)(i) 住房抵押贷款 (49)(ii) 合格的循环零售贷款 (49)(iii) 其他零售暴露 (49)2. 风险要素 (50)(i) 违约概率(PD) 和违约损失率 (LGD) (50)(ii) 担保和信贷衍生产品的认定 (50)(iii) 违约风险暴露 (EAD) (50)E. 股权暴露的规则 (50)1. 股权暴露的风险加权资产 (51)(i) 市场法 (51)(ii) 违约概率/违约损失率法 (51)(iii) 不采用市场法和违约概率/违约损失率法的情况 (52)2. 风险要素 (52)F. 购入应收帐款的规则 (53)1. 违约风险的风险加权资产 (53)(i) 购入的零售应收帐款 (53)(ii) 购入的公司应收帐款 (53)2. 稀释风险的风险加权资产 (54)(i) 购入折扣的处理 (54)(ii) 担保的认定 (55)G. 准备的认定 (55)H. IRB法的最低要求 (55)1. 最低要求的内容 (56)2. 遵照最低要求 (56)3. 评级体系设计 (57)(i) 评级维度 (57)(ii) 评级结构 (57)(iii) 评级标准 (58)(iv) 评估的时间 (59)(v) 模型的使用 (60)(vi) 评级体系设计的记录 (60)4. 风险评级体系运作 (60)(i) 评级的涵盖范围 (61)(ii) 评级过程的完整性 (61)(iii) 推翻评级的情况 (61)(iv) 数据维护 (61)(v) 评估资本充足率的压力测试 (62)5. 公司治理和监督 (62)(i) 公司治理 (63)(ii) 信用风险控制 (63)(iii) 内审和外审 (63)6. 内部评级的使用 (64)7. 风险量化 (64)(i) 估值的全面要求 (64)(ii) 违约的定义 (65)(iii) 重新确定帐龄 (66)(iv) 对透支的处理 (66)(v) 所有资产类别损失的的定义 (66)(vi) 估计违约概率的要求 (66)(vii) 自行估计违约损失率的要求 (67)(viii) 自己估计违约风险暴露的要求 (68)(ix) 评估担保和信贷衍生产品效应的最低要求 (69)(x) 估计违约概率、违约损失率(或预期损失)的最低要求......................... . 718. 内部评估的验证 (72)9. 监管当局确定的违约损失率和违约风险暴露 (73)(i) 商用房地产和住宅用房地产作为抵押品资格的定义 (73)(ii) 合格的商用房地产/住宅用房地产的操作要求 (73)(iii) 认定金融应收账款的要求 (74)10. 认定租赁的要求 (76)11. 股权暴露资本要求的计算 (76)(i) 内部模型法下的市场法 (76)(ii) 资本要求和风险量化 (76)(iii) 风险管理过程和控制 (78)(iv) 验证和形成文件 (78)12. 披露要求 (80)IV. 信用风险–资产证券化框架 (80)A. 资产证券化框架下所涉及交易的范围和定义 (80)B. 定义 (80)1. 银行所承担的不同角色 (80)(i) 投资行 (80)(ii) 发起行 (81)2. 通用词汇 (81)(i) 清除式召回 (81)(ii) 信用提高 (81)(iii) 提前摊还 (81)(iv) 超额利差 (81)(v) 隐性支持 (82)(vi) 特别目的机构 (SPE) (82)C. 确认风险转移的操作要求 (82)1. 传统型资产证券化的操作要求 (82)2. 合成型资产证券化的操作要求 (83)3. 清除式召回的操作要求和处理 (83)D. 对资产证券化风险暴露的处理 (84)1. 最低资本要求 (84)(i) 扣减 (84)(ii) 隐性支持 (84)2. 使用外部信用评估的操作要求 (84)3. 资产证券化风险暴露的标准化方法 (85)(i) 范围 (85)(ii) 风险权重 (85)(iii) 未评级资产证券化风险暴露一般处理方法的例外情况 (86)(iv) 表外风险资产的信用转换系数 (86)(v) 信用风险缓释的确认 (87)(vi) 提前摊还规定的资本要求 (88)(vii) 具有控制型提前摊还特征的信用转换系数的确定 (89)(viii) 对于非控制型具有提前摊还特征的风险暴露的信用风险转换系数的确定. 904. 资产证券化的内部评级法 (91)(i) 范围 (91)(ii) K IRB的定义 (92)(iii) 各种不同的方法 (92)(iv) 所需资本最高限 (93)(v) 以评级为基础的方法 (RBA) (93)(vi) 监管公式 (SF) (95)(vii) 流动性便利 (97)(viii) 合格服务人现金透支便利 (98)(ix) 信用风险缓释的确认 (98)(x) 提前摊还的资本要求 (98)V. 操作风险 (98)A. 操作风险定义 (98)B. 计量方法 (98)1. 基本指标法 (99)2. 标准法 (99)3. 高级计量法 (AMA) (100)C. 资格标准 (101)1. 一般标准 (101)2. 标准法 (101)3. 高级计量法 (102)(i) 定性标准 (102)(ii) 定量标准 (102)(iii) 风险缓释 (105)D. 局部使用 (106)VI. 交易账户 (106)A. 交易账户定义 (106)B. 审慎评估标准 (107)1. 评估系统和控制手段 (107)2. 评估方法 (107)(i) 按照市场价格计值 (107)(ii) 按照模型计值 (108)(iii) 价格独立验证 (108)3. 计值调整,又称储备 (108)C. 交易账户对手方信用风险的处理 (109)D. 标准法对交易账户特定风险资本要求的处理 (109)1. 政府债券的特定风险资本要求 (110)2. 对未评级债券特定风险的处理原则 (110)3. 采用信用衍生工具套做保值头寸的专项资本要求 (110)4. 信用衍生工具的附加系数 (111)Part 3: 第二支柱——监督检查 (113)A. 监督检查的重要性 (113)B. 监督检查的四项主要原则 (113)C. 监督检查的具体问题 (119)D. 监督检查的其他问题 (124)Part 4: 第三支柱——市场纪律 (126)A. 总体考虑 (126)1. 披露要求 (126)2. 指导原则 (126)3. 恰当的披露 (126)4. 与会计披露的相互关系 (126)5. 重要性 (127)6. 频率 (127)7. 内部和保密信息 (127)B. 披露要求 (128)1. 总体披露原则 (128)2. 使用范围 (128)3. 资本 (129)4. 风险暴露和评估 (130)(i) 定性披露的总体要求 (130)(ii) 信用风险 (131)(iii) 市场风险 (136)(iv) 操作风险 (137)(v) 银行账户的利率风险 (137)附录 1 创新工具在一级资本中的上线为15% (138)附录2 标准法-实施对应程序 (139)附录 3 IRB 法风险权重的实例 (143)附录4 监管当局对专业贷款设定的标准 (145)附录5 例子:按照监管公式计算信用风险缓释的影响 (159)附录6 产品线对应表 (163)附录7 损失事件分类详表 (165)附录8 按照标准法和内部评级法的规定,计算金融抵押品担保交易的资本要求的方法概述 (168)附录9 简化的标准法 (170)。

最新巴塞尔协议三中英对照

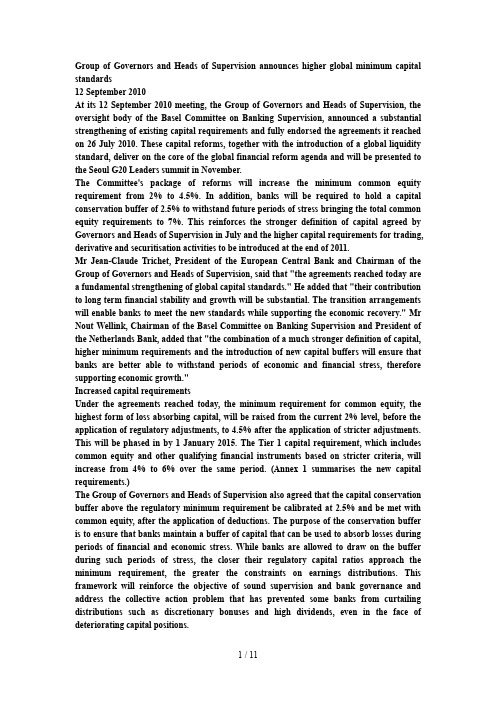

Group of Governors and Heads of Supervision announces higher global minimum capital standards12 September 2010At its 12 September 2010 meeting, the Group of Governors and Heads of Supervision, the oversight body of the Basel Committee on Banking Supervision, announced a substantial strengthening of existing capital requirements and fully endorsed the agreements it reached on 26 July 2010. These capital reforms, together with the introduction of a global liquidity standard, deliver on the core of the global financial reform agenda and will be presented to the Seoul G20 Leaders summit in November.The Committee's package of reforms will increase the minimum common equity requirement from 2% to 4.5%. In addition, banks will be required to hold a capital conservation buffer of 2.5% to withstand future periods of stress bringing the total common equity requirements to 7%. This reinforces the stronger definition of capital agreed by Governors and Heads of Supervision in July and the higher capital requirements for trading, derivative and securitisation activities to be introduced at the end of 2011.Mr Jean-Claude Trichet, President of the European Central Bank and Chairman of the Group of Governors and Heads of Supervision, said that "the agreements reached today are a fundamental strengthening of global capital standards." He added that "their contribution to long term financial stability and growth will be substantial. The transition arrangements will enable banks to meet the new standards while supporting the economic recovery." Mr Nout Wellink, Chairman of the Basel Committee on Banking Supervision and President of the Netherlands Bank, added that "the combination of a much stronger definition of capital, higher minimum requirements and the introduction of new capital buffers will ensure that banks are better able to withstand periods of economic and financial stress, therefore supporting economic growth."Increased capital requirementsUnder the agreements reached today, the minimum requirement for common equity, the highest form of loss absorbing capital, will be raised from the current 2% level, before the application of regulatory adjustments, to 4.5% after the application of stricter adjustments. This will be phased in by 1 January 2015. The Tier 1 capital requirement, which includes common equity and other qualifying financial instruments based on stricter criteria, will increase from 4% to 6% over the same period. (Annex 1 summarises the new capital requirements.)The Group of Governors and Heads of Supervision also agreed that the capital conservation buffer above the regulatory minimum requirement be calibrated at 2.5% and be met with common equity, after the application of deductions. The purpose of the conservation buffer is to ensure that banks maintain a buffer of capital that can be used to absorb losses during periods of financial and economic stress. While banks are allowed to draw on the buffer during such periods of stress, the closer their regulatory capital ratios approach the minimum requirement, the greater the constraints on earnings distributions. This framework will reinforce the objective of sound supervision and bank governance and address the collective action problem that has prevented some banks from curtailing distributions such as discretionary bonuses and high dividends, even in the face of deteriorating capital positions.A countercyclical buffer within a range of 0% - 2.5% of common equity or other fully loss absorbing capital will be implemented according to national circumstances. The purpose of the countercyclical buffer is to achieve the broader macroprudential goal of protecting the banking sector from periods of excess aggregate credit growth. For any given country, this buffer will only be in effect when there is excess credit growth that is resulting in a system wide build up of risk. The countercyclical buffer, when in effect, would be introduced as an extension of the conservation buffer range.These capital requirements are supplemented by a non-risk-based leverage ratio that will serve as a backstop to the risk-based measures described above. In July, Governors and Heads of Supervision agreed to test a minimum Tier 1 leverage ratio of 3% during the parallel run period. Based on the results of the parallel run period, any final adjustments would be carried out in the first half of 2017 with a view to migrating to a Pillar 1 treatment on 1 January 2018 based on appropriate review and calibration.Systemically important banks should have loss absorbing capacity beyond the standards announced today and work continues on this issue in the Financial Stability Board and relevant Basel Committee work streams. The Basel Committee and the FSB are developing a well integrated approach to systemically important financial institutions which could include combinations of capital surcharges, contingent capital and bail-in debt. In addition, work is continuing to strengthen resolution regimes. The Basel Committee also recently issued a consultative document Proposal to ensure the loss absorbency of regulatory capital at the point of non-viability. Governors and Heads of Supervision endorse the aim to strengthen the loss absorbency of non-common Tier 1 and Tier 2 capital instruments.Transition arrangementsSince the onset of the crisis, banks have already undertaken substantial efforts to raise their capital levels. However, preliminary results of the Committee's comprehensive quantitative impact study show that as of the end of 2009, large banks will need, in the aggregate, a significant amount of additional capital to meet these new requirements. Smaller banks, which are particularly important for lending to the SME sector, for the most part already meet these higher standards.The Governors and Heads of Supervision also agreed on transitional arrangements for implementing the new standards. These will help ensure that the banking sector can meet the higher capital standards through reasonable earnings retention and capital raising, while still supporting lending to the economy. The transitional arrangements, which are summarised in Annex 2, include:National implementation by member countries will begin on 1 January 2013. Member countries must translate the rules into national laws and regulations before this date. As of 1 January 2013, banks will be required to meet the following new minimum requirements in relation to risk-weighted assets (RW As):3.5% common equity/RW As;4.5% Tier 1 capital/RW As, and8.0% total capital/RW As.The minimum common equity and Tier 1 requirements will be phased in between 1 January 2013 and 1 January 2015. On 1 January 2013, the minimum common equity requirement will rise from the current 2% level to 3.5%. The Tier 1 capital requirement will rise from4% to 4.5%. On 1 January 2014, banks will have to meet a 4% minimum common equity requirement and a Tier 1 requirement of 5.5%. On 1 January 2015, banks will have to meet the 4.5% common equity and the 6% Tier 1 requirements. The total capital requirement remains at the existing level of 8.0% and so does not need to be phased in. The difference between the total capital requirement of 8.0% and the Tier 1 requirement can be met with Tier 2 and higher forms of capital.The regulatory adjustments (ie deductions and prudential filters), including amounts above the aggregate 15% limit for investments in financial institutions, mortgage servicing rights, and deferred tax assets from timing differences, would be fully deducted from common equity by 1 January 2018.In particular, the regulatory adjustments will begin at 20% of the required deductions from common equity on 1 January 2014, 40% on 1 January 2015, 60% on 1 January 2016, 80% on 1 January 2017, and reach 100% on 1 January 2018. During this transition period, the remainder not deducted from common equity will continue to be subject to existing national treatments.The capital conservation buffer will be phased in between 1 January 2016 and year end 2018 becoming fully effective on 1 January 2019. It will begin at 0.625% of RW As on 1 January 2016 and increase each subsequent year by an additional 0.625 percentage points, to reach its final level of 2.5% of RWAs on 1 January 2019. Countries that experience excessive credit growth should consider accelerating the build up of the capital conservation buffer and the countercyclical buffer. National authorities have the discretion to impose shorter transition periods and should do so where appropriate.Banks that already meet the minimum ratio requirement during the transition period but remain below the 7% common equity target (minimum plus conservation buffer) should maintain prudent earnings retention policies with a view to meeting the conservation buffer as soon as reasonably possible.Existing public sector capital injections will be grandfathered until 1 January 2018. Capital instruments that no longer qualify as non-common equity Tier 1 capital or Tier 2 capital will be phased out over a 10 year horizon beginning 1 January 2013. Fixing the base at the nominal amount of such instruments outstanding on 1 January 2013, their recognition will be capped at 90% from 1 January 2013, with the cap reducing by 10 percentage points in each subsequent year. In addition, instruments with an incentive to be redeemed will be phased out at their effective maturity date.Capital instruments that no longer qualify as common equity Tier 1 will be excluded from common equity Tier 1 as of 1 January 2013. However, instruments meeting the following three conditions will be phased out over the same horizon described in the previous bullet point: (1) they are issued by a non-joint stock company 1 ; (2) they are treated as equity under the prevailing accounting standards; and (3) they receive unlimited recognition as part of Tier 1 capital under current national banking law.Only those instruments issued before the date of this press release should qualify for the above transition arrangements.Phase-in arrangements for the leverage ratio were announced in the 26 July 2010 press release of the Group of Governors and Heads of Supervision. That is, the supervisory monitoring period will commence 1 January 2011; the parallel run period will commence 1January 2013 and run until 1 January 2017; and disclosure of the leverage ratio and its components will start 1 January 2015. Based on the results of the parallel run period, any final adjustments will be carried out in the first half of 2017 with a view to migrating to a Pillar 1 treatment on 1 January 2018 based on appropriate review and calibration.After an observation period beginning in 2011, the liquidity coverage ratio (LCR) will be introduced on 1 January 2015. The revised net stable funding ratio (NSFR) will move to a minimum standard by 1 January 2018. The Committee will put in place rigorous reporting processes to monitor the ratios during the transition period and will continue to review the implications of these standards for financial markets, credit extension and economic growth, addressing unintended consequences as necessary.The Basel Committee on Banking Supervision provides a forum for regular cooperation on banking supervisory matters. It seeks to promote and strengthen supervisory and risk management practices globally. The Committee comprises representatives from Argentina, Australia, Belgium, Brazil, Canada, China, France, Germany, Hong Kong SAR, India, Indonesia, Italy, Japan, Korea, Luxembourg, Mexico, the Netherlands, Russia, Saudi Arabia, Singapore, South Africa, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States.The Group of Central Bank Governors and Heads of Supervision is the governing body of the Basel Committee and is comprised of central bank governors and (non-central bank) heads of supervision from member countries. The Committee's Secretariat is based at the Bank for International Settlements in Basel, Switzerland.Annex 1: Calibration of the Capital Framework (PDF 1 page, 19 kb)Annex 2: Phase-in arrangements (PDF 1 page, 27 kb)Full press release (PDF 7 pages, 56 kb)--------------------------------------------------------------------------------1 Non-joint stock companies were not addressed in the Basel Committee's 1998 agreement on instruments eligible for inclusion in Tier 1 capital as they do not issue voting common shares.最新巴塞尔协议3全文央行行长和监管当局负责人集团1宣布较高的全球最低资本标准国际银行资本监管改革是本轮金融危机以来全球金融监管改革的重要组成部分。

新资本协议全文范文

巴塞尔新的资本协议强调,银行仅通过资本充足率的规定无法实现安全性和稳健性的目标,即最低资本要求、为此,该协议提出三大支柱,应通过一些更加全面、具体的约束加以实现。

监管当局检查评估和市场纪律约束,并作为该协议的主要内容。

最低资本要求。

这是该协议的基础,主要包括三方面的内容,即监管部门对资本的定 1.的计量及根据风险程度计算的最低资本要求。

其中监管部门对资本的定义和义、风险头寸新资本的最低资本充足比率,维持原资本协议的规定不变。

但在风险头寸的计量方面,8%计算风险资产的同时,”在调整了原有“标准法协议提出了更高的要求。

对于风险资产的计算,在对于一些高度发达的银行,强调对于十分先进的银行可以采用内部评级法计算风险资产,时,可以运用信用组合风险模型。

此外,在风险管理的范围上,除须涵盖原协风险管理进行法、、操作风险外,对于银行所面临的其他风险,如议要求的信用风险和市场风险利率风险。

等也应特别关注律风险确对银行的监管力度,这方面要求加大监管机构 2.监管部门对资本充足率的评估检查。

借以评估银行在认真分析风险的基础上设定的,建立起行之有效的内部程序保各家商业银行建立资本充足总体情况的内部具体原则包括:银行应参照其承担风险的程度,资本充足率。

维持战略、制定维持资本水平的战略;监管当局对资本充足情况的内部评价机制、评价机制,资本充足情况进行检测和评价;监管部门要求银行保持高于最低资本监管要求的资本充足如果资本得不监管当局对银行资本充足率下滑的状况进行及早干预,防止风险的扩散,率;到恢复,则应及时采取补救措施。

高效地经营以及保持较市场纪律约束。

这方面要求发挥市场的力量来促使银行稳健、 3.有效的市场高的资本充足率。

市场纪律有助于促使银行合理进行资本调节和控制内部风险。

资本充足、资本结构信息披露制度。

新协议要求银行及时披露包括约束要求银行建立一定的等内容。

率、对资本的内部评价机制、风险预测及战略管理新资本协议的借鉴与启示当局及商业银行监管也不属于国际公约,对各国政府、新资本协议虽然不是国际法规,银行不具有强制的约束力。

巴塞尔资本协议中英文完整版(02概述(英文))

Basel Committeeon Banking SupervisionConsultative Document Overview ofThe NewBasel Capital Accord Issued for comment by 31 July 2003 April 2003Introduction1. The Basel Committee on Banking Supervision (the Committee) is releasing this overview paper as an accompaniment to its third consultative paper (CP3) on the New Basel Capital Accord (also known as Basel II). The issuance of CP3 represents an important step in putting the new capital adequacy framework in place. The Committee‟s goal continues to be to finalise the New Accord by the fourth quarter of this year with implementation to take effect in member countries by year-end 2006.2. The Committee believes that important public policy benefits can be obtained by improving the capital adequacy framework along two important dimensions. First, by developing capital regulation that encompasses not only minimum capital requirements, but also supervisory review and market discipline. Second, by increasing substantially the risk sensitivity of the minimum capital requirements.3. An improved capital adequacy framework is intended to foster a strong emphasis on risk management and to encourage ongoing improvements in banks‟ risk assessment capabilities. The Committee believes this can be accomplished by closely aligning banks‟ capital requirements with prevailing modern risk management practices, and by ensuring that this emphasis on risk makes its way into supervisory practices and into market discipline through enhanced risk- and capital-related disclosures.4. A critical component of the Committee‟s efforts to revise the Basel Accord has been its extensive dialogue with industry participants and with supervisors from outside member countries. As a result of these consultations, the Committee believes the new framework with its various options will be suitable not only within the G10 but also for banks and for countries around the world to apply to their banking systems.5. An equally important aspect to the Committee‟s work has been the feedback received from banks participating in its impact studies. The aim of these studies has been to gather information from banks worldwide on the impact of the capital proposals on their existing portfolios. In particular, the Committee recognises the tremendous effort of the more than 350 banks of varying size and levels of complexity from more than 40 countries that participated in the most recent quantitative exercise known as QIS 3. As discussed in a separate paper, the QIS 3 results confirmed that the framework as currently calibrated produces capital requirements broadly consistent with the Committee‟s objectives.6. This overview paper is structured in two parts. The first part provides a summary of the new capital adequacy framework and also touches upon implementation considerations. It is targeted to readers that would like to increase their familiarity with the options available to banks in Basel II. The second part is more technical in nature. It outlines the specific modifications to the New Accord relative to the proposals embodied in the QIS 3 Technical Guidance released in October 2002.Part I: Key Elements of the New Accord7. The New Accord consists of three pillars: (1) minimum capital requirements, (2) supervisory review of capital adequacy, and (3) public disclosure. The proposals comprising each of the three pillars are summarised below.Pillar 1: Minimum capital requirements8. While the proposed New Accord differs from the current Accord along a number of dimensions, it is important to begin with a description of elements that have not changed. The current Accord is based on the concept of a capital ratio where the numerator represents the amount of capital a bank has available and the denominator is a measure of the risks faced by the bank and is referred to as risk-weighted assets. The resulting capital ratio may be no less than 8%.9. Under the proposed New Accord, the regulations that define the numerator of the capital ratio (i.e. the definition of regulatory capital) remain unchanged. Similarly, the minimum required ratio of 8% is not changing. The modifications, therefore, are occurring in the definition of risk-weighted assets, that is in the methods used to measure the risks faced by banks. The new approaches for calculating risk-weighted assets are intended to provide improved bank assessments of risk and thus to make the resulting capital ratios more meaningful.10. The current Accord explicitly covers only two types of risks in the definition of risk-weighted assets: (1) credit risk and (2) market risk. Other risks are presumed to be covered implicitly through the treatments of these two major risks. The treatment of market risk arising from trading activities was the subject of the Basel Committee‟s 1996 Amendment to the Capital Accord. The proposed New Accord envisions this treatment remaining unchanged. 11. The pillar one proposals to modify the definition of risk-weighted assets in the New Accord have two primary elements: (1) substantive changes to the treatment of credit risk relative to the current Accord; and (2) the introduction of an explicit treatment of operational risk that will result in a measure of operational risk being included in the denominator of a bank‟s capital ratio. The discussions below will fo cus on these two elements in turn.12. In both cases, a major innovation of the proposed New Accord is the introduction of three distinct options for the calculation of credit risk and three others for operational risk. The Committee believes that it is not feasible or desirable to insist upon a one-size-fits-all approach to the measurement of either risk. Instead, for both credit and operational risk, there are three approaches of increasing risk sensitivity to allow banks and supervisors to select the approach or approaches that they believe are most appropriate to the stage of development of banks‟ operations and of the financial market infrastructure. The following table identifies the three primary approaches available by risk type.Standardised approach to credit risk13. The standardised approach is similar to the current Accord in that banks are required to slot their credit exposures into supervisory categories based on observable characteristics of the exposures (e.g. whether the exposure is a corporate loan or a residential mortgage loan). The standardised approach establishes fixed risk weights corresponding to each supervisory category and makes use of external credit assessments to enhance risk sensitivity compared to the current Accord. The risk weights for sovereign, interbank, and corporate exposures are differentiated based on external credit assessments. For sovereign exposures, these credit assessments may include those developed by OECD export credit agencies, as well as those published by private rating agencies.14. The standardised approach contains guidance for use by national supervisors in determining whether a particular source of external ratings should be eligible for banks to use.The use of external ratings for the evaluation of corporate exposures, however, is consideredto be an optional element of the framework. Where no external rating is applied to anexposure, the standardised approach mandates that in most cases a risk weighting of 100%be used, implying a capital requirement of 8% as in the current Accord. In such instances,supervisors are to ensure that the capital requirement is adequate given the defaultexperience of the exposure type in question. An important innovation of the standardised approach is the requirement that loans considered past-due be risk weighted at 150%,unless a threshold amount of specific provisions has already been set aside by the bankagainst that loan.15. Another important development is the expanded range of collateral, guarantees, andcredit derivatives that banks using the standardised approach may recognise. Collectively,Basel II refers to these instruments as credit risk mitigants. The standardised approachexpands the range of eligible collateral beyond OECD sovereign issues to include most typesof financial instruments, while setting out several approaches for assessing the degree of capital reduction based on the market risk of the collateral instrument. Similarly, thestandardised approach expands the range of recognised guarantors to include all firms thatmeet a threshold external credit rating.16. The standardised approach also includes a specific treatment for retail exposures.The risk weights for residential mortgage exposures are being reduced relative to the currentAccord, as are those for other retail exposures, which will now receive a lower risk weightthan that for unrated corporate exposures. In addition, some loans to small- and medium-sized enterprises (SMEs) may be included within the retail treatment, subject to meetingvarious criteria.17. By design the standardised approach draws a number of distinctions betweenexposures and transactions in an effort to improve the risk sensitivity of the resulting capitalratios. The same can also be said of the IRB approaches to credit risk and those forassessing the capital requirement for operational risk where capital requirements are moreclosely linked to risk. In order to assist banks and national supervisors where circumstancesmay not warrant a broad range of options, the Committee has developed the …simplified st andardised approach‟ outlined in Annex 9 of CP3. The annex collects in one place thesimplest options for calculating risk weighted assets. Banks intending to adopt the simplifiedstandardised methods are also expected to comply with the corresponding supervisoryreview and market discipline requirements of the New Accord.Internal ratings-based (IRB) approaches18. One of the most innovative aspects of the New Accord is the IRB approach to creditrisk, which includes two variants: a foundation version and an advanced version. The IRB approach differs substantially from the standardised approach in that banks‟ internal assessments of key risk drivers serve as primary inputs to the capital calculation. Because the approach is based on banks‟ internal assess ments, the potential for more risk sensitive capital requirements is substantial. However, the IRB approach does not allow banks themselves to determine all of the elements needed to calculate their own capital requirements. Instead, the risk weights and thus capital charges are determined through the combination of quantitative inputs provided by banks and formulas specified by the Committee.19. The formulas, or risk weight functions, translate a bank‟s inputs into a specificcapital requirement. They are based on modern risk management techniques that involve astatistical and thus quantitative assessment of risk. Ongoing dialogue with industryparticipants has confirmed that use of such methods represents an important step forward for developing a meaningful assessment of risk at the largest most complex banking organisations in today‟s market.20. The IRB approaches cover a wide range of portfolios with the mechanics of the capital calculation varying somewhat across exposure types. The remainder of this section highlights the differences between the foundation and advanced IRB approaches by portfolio, where applicable.Corporate, bank and sovereign exposures21. The IRB calculation of risk-weighted assets for exposures to sovereigns, banks, or corporate entities uses the same basic approach. It relies on four quantitative inputs: (1) Probability of default (PD), which measures the likelihood that the borrower will default over a given time horizon; (2) Loss given default (LGD), which measures the proportion of the exposure that will be lost if a default occurs; (3) Exposure at default (EAD), which for loan commitments measures the amount of the facility that is likely to be drawn if a default occurs; and (4) Maturity (M), which measures the remaining economic maturity of the exposure. 22. Given a value for each of these four inputs, the corporate IRB risk-weight function described in CP3 produces a specific capital requirement for each exposure. In addition, for exposures to SME borrowers defined as those with annual sales of less than 50 million of Euros, banks will be permitted to make use of a firm size adjustment to the corporate IRB risk weight formula.23. The foundation and advanced IRB approaches differ primarily in terms of the inputs that are provided by the bank based on its own estimates and those that have been specified by the supervisor. The following table summarises these differences.24. The table makes clear that for corporate, sovereign, and interbank exposures, all IRB banks must provide internal estimates of PD. In addition, advanced IRB banks must provide internal estimates of LGD and EAD, while foundation IRB banks will make use of supervisory values contained in CP3 that depend on the nature of the exposure. Advanced IRB banks will generally provide their own estimates of remaining maturity for theseexposures, although there are some exceptions where supervisors can allow fixed maturity assumptions to be used instead. For foundation IRB banks, supervisors can choose on a national basis whether all such banks are to apply fixed maturity assumptions described in CP3 or to provide their own estimates of remaining maturity.25. Another major element of the IRB framework pertains to the treatment of credit risk mitigants, namely, collateral, guarantees and credit derivatives. The IRB framework itself, particularly the LGD parameter, provides a great deal of flexibility to assess the potential value of credit risk mitigation techniques. For foundation IRB banks, therefore, the different supervisory LGD values provided in CP3 reflect the presence of different types of collateral. Advanced IRB banks have even greater flexibility to assess the value of different types of collateral. With respect to transactions involving financial collateral, the IRB approach seeks to ensure that banks are using a recognised approach to assessing the risk that such collateral could change in value, and thus a specific set of methods is provided, as in the standardised approach.Retail exposures26. For retail exposures, there is only a single, advanced IRB approach and no foundation IRB alternative. The key inputs to the IRB retail formulas are PD, LGD and EAD, all of which are to be provided by the bank based on its internal estimates. In contrast to the IRB approach for corporate exposures, these values would not be estimated for individual exposures, but instead for pools of similar exposures.27. In light of the fact that retail exposures address a broad range of products with each exhibiting different historical loss experiences, the framework divides retail exposures into three primary categories: (1) exposures secured by residential mortgages, (2) qualifying revolving retail exposures (QRRE), and (3) other non-mortgage exposures also known as …other retail.‟ Generally speaking, the QRRE category captures unsecured revolving credits that exhibit appropriate loss characteristics, which would include many credit card relationships. All other non-mortgage consumer lending including exposures to small businesses falls into the …other retail‟ category. A separate risk-weight formula for each of the three categories is provided in CP3.Specialised lending28. Basel II distinguishes several sub-categories of wholesale lending from other forms of corporate lending and refers to them as specialised lending. The term specialised lending is associated with the financing of individual projects where the repayment is highly dependent on the performance of the underlying pool or collateral. For all but one of the specialised lending sub-categories, if banks can meet the minimum criteria for the estimation of the relevant data inputs, they can simply use the corporate IRB framework to calculate the risk weights for these exposures. However, in recognition that the hurdles for meeting these criteria for this set of exposures may be more difficult in practice, CP3 also includes an additional option that only requires that a bank be able to classify such exposures into five distinct quality grades. CP3 provides a specific risk weight for each of these grades.29. For one sub-category of specialised lending, …high volatility commercial real estate‟ (HVCRE), IRB banks that can estimate the required data inputs will use a separate risk-weight formula that is more conservative than the general corporate risk-weight formula in light of the risk characteristics of this type of lending. Banks that cannot estimate the required inputs will classify their HVCRE exposures into five grades, for which CP3 also provides specific risk weights.Equity exposures30. IRB banks will be required to separately treat their equity exposures. Two distinctapproaches are described in CP3. One approach builds on the PD/LGD approach forcorporate exposures and requires banks to provide own PD estimates for the associatedequity exposures. This approach, however, mandates the use of a 90% LGD value and alsoimposes various other limitations, including a minimum risk weight of 100% in manycircumstances. The other approach is intended to provide banks with the opportunity tomodel the potential decrease in the market value of their equity holdings over a quarterly holding period. A simplified version of this approach with fixed risk weights for public andprivate equities is also included.Implementation of IRB31. By relying on internally generated inputs to the Basel II risk weight functions, there isbound to be some variation in the way in which the IRB approach is carried out. To ensuresignificant comparability across banks, the Committee has established minimum qualifyingcriteria for use of the IRB approaches that cover the comprehensiveness and integrity ofbanks‟ internal credit risk assessment c apabilities. While banks using the advanced IRB approach will have greater flexibility relative to those relying on the foundation IRB approach,at the same time they must also satisfy a more stringent set of minimum standards.32. The Committee believes that banks‟ internal rating systems should accurately andconsistently differentiate between different degrees of risk. The challenge is for banks todefine clearly and objectively the criteria for their rating categories in order to providemeaningful assessments of both individual credit exposures and ultimately an overall riskprofile. A strong control environment is another important factor for ensuring that banks‟ rating systems perform as intended and the resulting ratings are accurate. An independent ratings process, internal review and transparency are control concepts addressed in the minimum IRB standards.33. Clearly, an internal rating system is only as good as its inputs. Accordingly, banksusing the IRB approach will need to be able to measure the key statistical drivers of creditrisk. The minimum Basel II standards provide banks with the flexibility to rely on data derivedfrom their own experience, or from external sources as long as the bank can demonstrate therelevance of such data to its own exposures. In practical terms, banks will be expected to have in place a process that enables them to collect, to store and to utilise loss statistics over time in a reliable manner.Securitisation34. Basel II provides a specific treatment for securitisation, a risk management technique that the current Accord does not fully contemplate. The Committee recognises that securitisation by its very nature relates to the transfer of ownership and/or risks associated with the credit exposures of a bank to other parties. In this respect, securitisation is important in helping to provide better risk diversification and to enhance financial stability.35. The Committee believes that it is essential for the New Accord to include a robust treatment of securitisation. Otherwise the new framework would remain vulnerable to capital arbitrage, as some securitisations have enabled banks under the current Accord to avoid maintaining capital commensurate with the risks to which they are exposed. To address this concern, Basel II requires banks to look to the economic substance of a securitisation transaction when determining the appropriate capital requirement in both the standardised and IRB treatments.36. As elsewhere in the standardised approach to credit risk, banks must assign supervisory risk weights to securitisation exposures based on various criteria. Onenoteworthy point is the difference in treatment of lower quality and unrated securitisationsvis-à-vis comparable corporate exposures. In a securitisation, such positions are generallydesigned to absorb all losses on the underlying pool of exposures up to a certain level.Accordingly, the Committee believes this concentration of risk warrants higher capitalrequirements. In particular, for banks using the standardised approach, unrated securitisationpositions must be deducted from capital.37. For IRB banks that originate securitisations, a key element of the framework is thecalculation of the amount of capital that the bank would have been required to hold on theunderlying pool had it not securitised the exposures. This amount of capital is referred to asK IRB. If an IRB bank retains a position in a securitisation that obligates it to absorb losses upto or less than K IRB before any other holders bear losses (i.e. a first loss position), then thebank must deduct this position from capital. The Committee believes that this requirement iswarranted in order to provide strong incentives for originating banks to shed the riskassociated with highly subordinated securitisation positions that inherently contain the greatest risks. For IRB banks that invest in highly rated securitisation exposures, a treatmentbased on the presence of an external rating, the granularity of the underlying pool, and thethickness of an exposure has been developed.38. Because of their importance in ensuring the smooth functioning of commercial papermarkets and their importance to corporate banking generally, the Basel II securitisationframework includes an explicit treatment of liquidity facilities provided by banks. In the IRBframework, the capital requirement for a liquidity facility is dependent upon a number of factors including the asset quality of the underlying pool and the degree to which creditenhancements are available to absorb losses prior to use of the facility. Each is a criticalinput to the supervisory formula designed for use by originating banks to calculate capitalrequirements for unrated positions, such as liquidity facilities. A treatment of liquidity facilitiesin the standardised approach is also provided which sets out various criteria for ensuring thatmore preferential treatment is only provided to those liquidity facilities where the risks arelower.39. Many securitisations of revolving retail exposures contain provisions that call for the securitisation to be wound down if the quality of securitised assets begins to deteriorate. TheBasel II proposals include a specific treatment of securitisations with these …earlyamortisation‟ features, given that suc h mechanisms can in effect partly shield investors fromfully sharing in the losses of the underlying accounts. The Committee‟s approach is based ona measure of the quality of the underlying assets in the pool. When this is high, the approachimplies a zero capital requirement associated with the securitised exposures. As the qualitydeteriorates, however, the bank must increasingly hold capital as if future draws on existing credit card lines would remain on its balance sheet.Operational risk40. The Committee believes that operational risk is an important risk facing banks andthat banks need to hold capital to protect against losses from it. Within the Basel IIframework, operational risk is defined as the risk of losses resulting from inadequate or failedinternal processes, people and systems, or external events. This is another area where theCommittee has developed a new regulatory capital approach. As with credit risk, theCommittee builds on banks‟ rapidly developing internal assessment techniques and seeks to provide incentives for banks to improve upon those techniques, and more broadly, theirmanagement of operational risk over time. This is particularly true of the AdvancedMeasurement Approaches (AMA) to operational risk described below.41. Approaches to operational risk are continuing to evolve rapidly, but are not likely in the near term to attain the precision with which market and credit risk can be quantified. This situation has posed obvious challenges to the incorporation of a measure of operational risk within pillar one of the New Accord. Nevertheless, the Committee believes that such inclusion is essential to ensure that there are strong incentives for banks to continue to develop approaches to operational risk measurement and to ensure that banks are holding sufficient capital buffers for this risk. It is clear that a failure to establish a minimum capital requirement for operational risk within the New Accord would reduce these incentives and result in a reduction of industry resources devoted to operational risk.42. The Committee is prepared to provide banks with an unprecedented amount of flexibility to develop an approach to calculate operational risk capital that they believe is consistent with their mix of activities and underlying risks. In the AMA, banks may use their own method for assessing their exposure to operational risk, so long as it is sufficiently comprehensive and systematic. The extent of detailed standards and criteria for use of the AMA are limited in order to accommodate the rapid evolution in operational risk management practices that the Committee expects to see over the coming years.43. The Committee intends to review progress in regard to operational risk approaches on an ongoing basis. It has been strongly encouraged by the advances made at those banks that have been developing operational risk frameworks consistent with the spirit of the AMA. Management at these banking organisations has concluded that it is possible to develop a flexible and comprehensive approach to operational risk measurement within their firms. 44. Internationally active banks and banks with significant operational risk exposure (for example, specialised processing banks) are expected to adopt over time the more risk sensitive AMA. Basel II contains two simpler approaches to operational risk: the basic indicator and the standardised approach, which are targeted to banks with less significant operational risk exposures. In general terms, the basic indicator and standardised approaches require banks to hold capital for operational risk equal to a fixed percentage of a specified risk measure.45. In the basic indicator approach, the measure is a bank‟s average annual gross income over the previous three years. This average, multiplied by a factor of 0.15 set by the Committee, produces the capital requirement. As a point of entry for the capital calculation, there are no specific criteria for use of the basic indicator approach. Nevertheless banks using this approach are encouraged to comp ly with the Committee‟s guidance on sound practices for the management and supervision of operational risk, which was released in February 2003.46. In the standardised approach, gross income again serves as a proxy for the scale ofa bank‟s business oper ations and thus the likely scale of the related operational risk exposure for a given business line. However, rather than calculate capital at the firm level as under the basic indicator approach, banks must calculate a capital requirement for each business line. This is determined by multiplying gross income by specific supervisory factors determined by the Committee. The total operational risk capital requirement for a banking organisation is the summation of the regulatory capital requirements across all of its business lines. As a condition for use of the standardised approach, it is important for banks to have adequate operational risk systems that comply with the minimum criteria outlined in CP3. 47. Banks using the basic indicator or standardised approaches to operational risk are not permitted to recognise the risk mitigating impact of insurance. As discussed in Part II of this overview paper, banks using the AMA are permitted to do so subject to certain conditions.。

巴塞尔新资本协议中文

巴塞尔新资本协议2010/7/28概述导言1. 巴塞尔银行监管委员会(以下简称委员会)现公布巴塞尔新资本协议(Basel II, 以下简称巴塞尔II)第三次征求意见稿(CP3,以下简称第三稿)。

第三稿的公布是构建新资本充足率框架的一项重大步骤。

委员会的目标仍然是在今年第四季度完成新协议,并于2006年底在成员国开始实施。

2. 委员会认为,完善资本充足率框架有两方面的公共政策利好。

一是建立不仅包括最低资本而且还包括监管当局的监督检查和市场纪律的资本管理规定。

二是大幅度提高最低资本要求的风险敏感度。

3. 完善的资本充足率框架,旨在促进鼓励银行强化风险管理能力,不断提高风险评估水平。

委员会认为,实现这一目标的途径是,将资本规定与当今的现代化风险管理作法紧密地结合起来,在监管实践中并通过有关风险和资本的信息披露,确保对风险的重视。

4. 委员会修改资本协议的一项重要内容,就是加强与业内人士和非成员国监管人员之间的对话。

通过多次征求意见,委员会认为,包括多项选择方案的新框架不仅适用于十国集团国家,而且也适用于世界各国的银行和银行体系。

5. 委员会另一项同等重要的工作,就是研究参加新协议定量测算影响分析各行提出的反馈意见。

这方面研究工作的目的,就是掌握各国银行提供的有关新协议各项建议对各行资产将产生何种影响。

特别要指出,委员会注意到,来自40多个国家规模及复杂程度各异的350多家银行参加了近期开展的定量影响分析(以下称简QIS3)。

正如另一份文件所指出,QIS3的结果表明,调整后新框架规定的资本要求总体上与委员会的既定目标相一致。

6. 本文由两部分内容组成。

第一部分简单介绍新资本充足框架的内容及有关实施方面的问题。

在此主要的考虑是,加深读者对新协议银行各项选择方案的认识。

第二部分技术性较强,大体描述了在2002年10月公布的QIS3技术指导文件之后对新协议有关规定所做的修改。

第一部分新协议的主要内容7. 新协议由三大支柱组成:一是最低资本要求,二是监管当局对资本充足率的监督检查,三是信息披露。

解读中国版巴塞尔新资本协议

解读中国版巴塞尔新资本协议近期,银监会发布了《商业银行资本管理办法(试行)》(以下简称《资本办法》),该办法相当于中国版的巴塞尔新资本协议,它将巴塞尔协议Ⅱ与巴塞尔协议Ⅲ统筹推进,于2013年1月1日起开始实施,商业银行应于2018年年底前全面达标。

我国银行业稳步实施新的资本监管标准,不仅符合国际金融监管改革的大趋势,也有助于增强中国银行业抵御风险的能力,加快商业银行经营管理的战略转型。

《资本办法》的基本框架《资本办法》整合了巴塞尔II和巴塞尔III在风险加权资产计算方面的核心要求,扩展了风险覆盖范围,提高了监管资本的风险敏感度,合理设计各类资产的风险权重体系,允许符合条件的银行采取内部评级法计量信用风险的资本要求,同时要求所有银行必须计提市场风险和操作风险的资本要求。

《资本办法》还明确了商业银行内部资本充足评估程序、资本充足率监管检查等内容,规定银监会有权增加高风险资产组合和高风险银行的资本要求,并依据资本充足率水平对商业银行实施分类监管,采取一整套具有针对性和操作性的差异化监管措施。

《资本办法》将商业银行资本充足率监管要求分为四个层次:第一层次为最低资本要求,即核心一级资本充足率、一级资本充足率和资本充足率分别为5%、6%和8%;第二层次为储备资本要求和逆周期资本要求,分别为2.5%和0-2.5%;第三层次为系统重要性银行附加资本要求,为1%;第四层次为根据单家银行风险状况提出的第二支柱资本要求。

《资本办法》实施后,我国大型银行和中小银行的资本充足率监管要求分别为11.5%和10.5%,符合巴塞尔最低监管标准,并与国内现行监管要求保持一致。

多层次的监管资本要求既符合巴塞尔III确定的资本监管新要求,又增强了资本监管的审慎性和灵活性,确保资本充分覆盖国内银行面临的系统性风险和个体风险。

总体看,《资本办法》在资本要求、资本定义、风险加权资产计量和全面风险治理等各方面都保持了与国际新资本监管标准的基本一致。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

操作风险的度量方法:高级计量法

高级计量法是指,银行用定量和定性标准,通过内部操作 风险计量系统计算监管资本要求。与信用风险的估测相似,操 作风险发生的事件的概率乘以操作风险的违约的损失乘以操作 风险的暴露的敞口. 内部衡量法(IMA) 损失分布法(LDA) 极值原理法(EVT) 贝叶斯网络法(BBN) 记分卡法(SCA)

操作风险的度量方法:标准法

总资本要求是各产品线监管资 本的简单加总。总资本要求如 下所示: KTSA = Σ (GI1-8 x β1-8)

KTSA = 用标准法计算的资本要求; GI1-8 = 按基本指标法的定义,8 个产品线中各产品线过去三年的 年均总收入;β1-8 = 由委员会设 定的固定百分数, 建立8个产品 线中各产品线的总收入与资本要 求之间的联系。β值详见下表: 业务部门 公司金融 (β1) 交易和销售 (β2) 零售银行业务(β3) 商业银行业务 (β4) 支付和清算 (β5) 代理服务 (β6) 资产管理 (β7) 零售经纪 (β8) β系数 18% 18% 12% 15% 18% 15% 12% 12%

操作风险

操作风险的定义 操作风险的度量方法

操作风险的定义

由于内部操作流程不完善、人为过失、系统故 障或外部突发事件造成的损失。 操作风险事件分类

内部欺诈 外界欺诈 雇佣事项及工作场所安全性 客户、产品及业务方式 有形资产的损坏 业务中断及系统故障 操作流程管理

BBA关于操作风险的界定

第一级: 第一级:因素 人 第二级: 第二级:定义 (1)雇员欺诈、犯罪;(2)越权行为、欺诈交 易、操作失误 (3)违反用工法;(4)劳动力中断; (5)关键人员流失或缺乏 (1)支付清算、传输风险;(2)文件、合同风 险;(3)估价、定价风险;(4)内部、外部报 告风险;(5)执行风险;(6)策略风险、管理 变动;(6)出售风险;(7)科技投资风险 (1)系统开发和执行;(2)系统功能; (3)系统失败;(4)系统安全 (1)法律、公共责任;(2)犯罪;(3)外部 采购、供应商风险;(4)外部开发风险;(5) 灾难、基础设施;(6)政策调整(7)政治、政 府风险

新巴塞尔协议在我国实施的可能性

我国银行业如何实施新巴塞尔协议

新巴塞尔协议的背景及演进阶段

巴塞尔协议的提出 巴塞尔协议的内容 巴塞尔协议的缺陷 新巴塞尔协议的发展历程

巴塞尔协议的提出

•70年代国际大型商业银行的业务呈 70年代国际大型商业银行的业务呈 现出全球化, 现出全球化,金融工具创新和投机活 动等三个特点。1974年德国赫斯德特 动等三个特点。1974年德国赫斯德特 银行、纽约富兰克林国民银行和英国 银行、 -以色列银行相继倒闭。 以色列银行相继倒闭。

资本结构

风险的测量和评估

资本充足性

三大支柱之间的相互联系

三大风险

信用风险 市场风险 操作风险

信用风险

信用风险的确定方法

标准法的原理及方法 内部评级法的基本框架

标准法VS内部评级法

信用风险的确定方法

信用风险

标准法

内部评级法

一般规则 信用风险缓冲

初级法

高级法

标准法:一般规则

在计算信用风险的标准法中,新协议采用评级机 构的评级结果确定风险权重,废除以往以经合组 织成员确定风险权重的做法。 使用于风险管理体系并不十分复杂的银行 评级机构:外部评级与出口信用机构评级相结合 新协议将最大风险权重由100%提高到150%

内部程序

系统

外部事件

操作风险的度量方法

基本指标法、标准法、高级计量法

操作风险的度量方法:基本指标法 基本指标法

银行持有的操作风险资本应等于前三年总收入的平均值 乘上一个固定比例(用α表示)。资本计算公式如下:

KBIA = GI * α

其中,KBIA = 基本指标法需要的资本, GI = 前三年总收入的平均值, α = 15%,由巴塞尔委员会设定。 总收入定义为:净利息收入加上非利息收入。这种 计算方法旨在(1)反映所有准备(例如,未付利息的准备)的 总额;(2)不包括银行账户上出售证券实现的利润(或损失) ; (3)不包括特殊项目以及保险收入。

巴塞尔协议的缺陷

不能反映银行面临的真实风险 资本套利交易引发资产质量下降 缺乏激励模式 存在歧视性政策

新巴塞尔协议发展历程

1988 1992

1988 年巴 塞尔协议 实施:信 用风险资 本要求

1996

市场风险的 修订案:市 场风险资本 要求

1998.9

1999.6

新资本协 议第一次 征询意见 稿

资本充足率 = 信用风险, ƒ (信用风险, 市场风 操作风险) 险, 操作风险)

市场风险的衡量方法

标准法

对市场风险的最低资本要求=利率风险+股权投 资风险+外汇风险+大宗商品风险+期权风险

内部模型法

对市场风险的最低资本要求=前一个交易日的 VAR 或 3*前六十个交易日的平均VAR

(以高者为准)

新巴塞尔协议专题讲座

谢家智

教授 博导

西南大学经济管理学院副院长 重庆市政府决策专家咨询委员 重庆市金融学学术带头人

金融危机演变的逻辑变化特征

传统:经济危机 现代:金融危机 金融危机 社会危机 经济危机 社会危机

银行风险

→ 金融风险 → 经济风险 → 国家风险

主要内容

新巴赛尔协议的背景及演进阶段 新巴塞尔协议的内容框架 新巴塞尔协议的创新

内部评级法的基本框架

内部评级法的四个要素:违约概率、违约损失 率、期限、风险暴露

内部评级方法

初级法:要求比较简单,银行只需计算违约概 率,其余要素只要依照监管机构的参数即可 高级法:高级法相对复杂得多,银行需要自行 计算上述4个要素,且受监管机构限制的地方 较少。巴塞尔委员会除了对使用高级法的银行 有较高的要求外,同时对第二支柱及第三支柱 提出加强规范,亦规定银行在使用高级法前要 先得到监管机构的认可。

信息披露的内容

最低资本要求的适 最低资本要求的适用范围

银行集团中适用资本充足要求的成员范围 资本的结构和組成 资本工具的期限、条件、 资本工具的期限、条件、主要特征 资产负债、 资产负债、拨备及收益使用的会计政策 风险资产的分布和测算: 风险资产的分布和测算: 信用风险(银行帐 市场风 银行帐)、 作风险、 信用风险 银行帐 、市场风、操作风险、利 率风险(银行帐 银行帐) 率风险 银行帐

银行资产规模 是否可以无 限制扩张? 限制扩张?

巴塞尔协议

巴塞尔协议的内容

1987年,美联储和英格兰银行联合提出建立共 同的资本体系,限制在资本不足的情况下过度 扩张;1988年,西方十国的央行经过多轮谈判, 达成了巴塞尔资本协议

界定资本充足率:资本充足率不得低于8%,核 界定资本充足率:资本充足率不得低于8%,核 心资本充足率不得低于4 心资本充足率不得低于4%。 界定了风险资产RWA assets) 界定了风险资产RWA (risk wave assets) 界定了资本

并表资本充足率及其相关信息; 并表资本充足率及其相关信息; 险敞口的测算方法; 风险敞口的测算方法; 影响资本充足率的因素分析; 影响资本充足率的因素分析; 不同类别风险的资本要求; 不同类别风险的资本要求; 补充资本的紧急方案; 补充资本的紧急方案; 经济资本提取方法; 经济资本提取方法; 比较“总经济资本需要” 实际资本” 比较“总经济资本需要”、“实际资本”、“监管资本 要求” 要求”

信用风险缓释

银行可以采用多种技术对贷款进行信用风险缓释 (Credit Risk Mitigation)。标准法确定的风险缓 释工具包括抵押、表内净扣、担保和信用衍生工具。 信用风险缓释工具得到认可后,在计算风险暴露时 就要扣除信用风险缓释工具的影响。

简单法:将抵押或担保部分与风险暴露部分分开计算风险 权重。在计算资本充足率时,贷款中被抵押或担保的部分, 采用抵押品或担保人的风险权重,风险暴露部分采用借款 人的风险权重。 综合法:计算风险权重时要考虑抵押部分在未来贷款期限 内抵押价值的波动性,及由此导致的抵押部分价值的变化 和风险暴露部分价值的变化。

内部评级高级法

首先选择适当的信用风险管理模型估计或根据监管标 准确定输入参数PD, LGD, EAD,M 其次,由参数PD, LGD, M确定风险权重RW;由EAD和RW 之积确定各资产风险暴露的风险加权资产 对各类资产风险暴露的风险加权资产求和,确定资本 要求。

内部评级法存在的问题影响 强化亲周期性效应

2001.1

新协议 第二次 征询意 见稿

2003.5

新协议第 三次征询 意见稿

2004.6

巴塞尔协 议II正式 出台实施

2006.12

引入操 作风险 管理

Basel I实 实 施的最后 期限

操作风险的定量分析

Basel II 实施的 最后期 限

新巴塞尔协议的内容框架

新巴塞尔协议的框架

三大支柱 三大风险

原则4 原则4

监管者应在尽早的阶段介入可能出现风险资本额小于最低标准 的银行, 的银行,要求即时进行补充

三大职责

全面监管银行资本充足状况 培育银行的内部信用评估体系 加快制度化进程

第三支柱:市场约束

市场约束的含义 信息披露内容

市场约束的含义

也称市场纪律,又称为信息披露。巴塞尔委员 会力求鼓励市场纪律发挥作用。要求银行提高信 息的透明度,使外界对它的财务、管理等有更好 的了解。对银行在应用范围、资本构成、风险评 估和管理过程及资本充足性方面提出了定性和定 量的信息披露要求:大银行每季度进行一次信息披 露,一般银行每半年披露一次信息。

新巴塞尔协议的创新

风险计量的创新。一是在信用风险领域允许银行采用外部 评级机构所提供的信用等级计算其资本要求,具有高级风 险管理能力的银行运用其IRR制度评定信用风险,即以内 部评级代替对何一种类资产的标准化的风险加权; 资本对风险的敏感程度方面大大增强; 全面风险管理理念。操作风险首次被纳入资本充足率框架 之下; 三大支柱的提出。以监管审查和市场约束两大支柱作为原 来数量标准的补充手段,其目的是减少对第一大支柱数量 标准的过度依赖,为资产评估确立一个更均衡的标准。