audit report

Examples of audit report

Examples of audit report(审计报告英文样本)Examples of audit report(审计报告英文样本)1.Following is an example of an audit report containing an unqualified opinion Audit reportTo: The Board of Directors (or Shareholders) of ABC company ltd:We have audited the accom panying balance sheet of ABC Co., Ltd. (“ the Company”) as of December 31, 2002, and the related statements of income and cash flows for the year then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an audit opinion on these financial statements based on our audit.We conducted our audit in accordance with the Independent Auditing Standards for Certified Public Accountants. Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.In our opinion, the financial statements give a true and fair view( or are presented fairly, in all material respects, ) the financial position as of December 31, 2002 , and the results of its operations and its cash flows for the years then ended in accordance with the requirements of both the Accounting Standard for Business Enterprises and other relevant financial and accounting laws and regulations promulgated by the State.Certified Public Accountant: liliCertified Public Accountant: zhanghua**Certified Public Accountants(name and stamp of the firm)Beijing, People’s Republic of ChinaFebruary 26, 20032.Following is an example of an audit report containing an unqualified opinion with an explanatory paragraphAudit ReportTo: The Board of Directors (or Shareholders) of ABC company ltd.:We have audited the accompanying balance sheet of ABC Co., Ltd. (“ the Company”) as of December 31, 2002, and the related statements of income and cash flows for the year then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an audit opinion on these financial statements based on our audit.We conducted our audit in accordance with the Independent Auditing Standards for Certified Public Accountants. Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting theamounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.In our opinion, the financial statements give a true and fair view( or are presented fairly, in all material respects, ) the financial position as of December 31, 2002 , and the results of its operations and its cash flows for the years then ended in accordance with the requirements of both the Accounting Standard for Business Enterprises and other relevant financial and accounting laws and regulations promulgated by the State.In the course of our audit, we have reminded the management that, due to the sharp price decline in the stock market since January 2003, an investment loss totaling RMB5 700 000 would be incurred if the short-term equity securities held by your Company were sold out on March 10Certified Public Accountant: liliCertified Public Accountant: zhanghua**Certified Public Accountants (name and stamp of the firm)Beijing, People’s Republic of China February 26, 2003Audit report3.Following is an example of an audit report containing an qualified opinion Audit ReportTo: The Board of Directors (or Shareholders)of ABC company ltd.:We have audited the accompanying balance sheet of ABC Co., Ltd. (“ the Company”) as of December 31, 2002, and the related statements of income and cash flows for the year then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an audit opinion on these financial statements based on our audit.We conducted our audit in accordance with the Independent Auditing Standards for Certified Public Accountants. Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.The accompanying balance sheet at December 31, 2002 includes project service fees receivable of RMB17,309,667 and other long-term receivables of RMB160,599,155 . These amounts are owing by one of the joint venture investors of the Company and certain business partners of that investor. As described in Notes 5 and 6 to the financial statements, there is uncertainty about the collectibility of these receivables. Because the ability of the debtors to repay these receivables is dependent upon the success of future operations of certain projects and upon the ability of the debtors to comply with the terms of their agreements with the Company, it is not possible to estimate the amount which ultimately will be collected. Provision for loss relating to the project service fees receivable has been made at approximately 3% of the year-end balance, and no provision is made forother long-term receivables.In our opinion, except for the possible effects of the uncertainty about the collectibility of the project service fees and other long-term receivables, the financial statements referred above give a true and fair view( or are presented fairly, in all material respects, ) the financial position as of December 31, 2002 , and the results of its operations and its cash flows for the years then ended in accordance with the requirements of both the Accounting Standard for Business Enterprises and other relevant financial and accounting laws and regulations promulgated by the State.The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. However, as explained in Note 10 to the financial statements, the Company has been unable to negotiate an extension of its borrowings with its foreign joint venture investor beyond December 31, 2003. Further, as described above, there is uncertainty about the collectibility of project service fees receivable and other long-term receivables. Because of this uncertainty, and without the continued financial support of the foreign investor, there is substantial doubt that the Company will be able to continue as a going concern beyond 2003. Consequently, adjustments may be required to the recorded asset amounts. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.Certified Public Accountant: liliCertified Public Accountant: zhanghua**Certified Public Accountants (name and stamp of the firm)Beijing, People’s Republic of China February 26, 20034.Following is an example of an audit report containing an adverse opinion Audit ReportTo: The Board of Directors (or Shareholders)of ABC company ltd.:We hav e audited the accompanying balance sheet of ABC Co., Ltd. (“ the Company”) as of December 31, 2002, and the related statements of income and cash flows for the year then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an audit opinion on these financial statements based on our audit.We conducted our audit in accordance with the Independent Auditing Standards for Certified Public Accountants. Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.The inventory costing method as in Note XX and the valuation method for fixed assets as in Note XX do not follow the historical cost principle. This departure from the accounting standards has caused a RMBY XX decrease in the inventory value as well as a RMBY XX increase in the original value of fixed assets, which has a material impact on the correctness of the income determination.In our opinion, due to the material impact of the matters mentioned above, the financial statements referred above give a true and fair view( or are presented fairly, in all material respects, ) the financial position as of December 31, 2002 , and the results of its operations and its cash flows for the years then ended in accordance with the requirements of both the Accounting Standard for Business Enterprises and other relevant financial and accounting laws and regulations promulgated by the State.Certified Public Accountant: liliCertified Public Accountant: zhanghua**Certified Public Accountants(name and stamp of the firm)Beijing, People’s Republic of ChinaFebruary 26, 20035.Following is an example of an audit report containing a disclaimer of opinion Audit ReportTo: The Board of Directors (or Shareholders)of ABC company ltd.:We were engaged to audit the balance sheet of your Company as of December 31, 2002 and the related statements of income and cash flows for the year then ended. There financial statement are the responsibility of the Company’s management.According to our examination, most of the inventory purchases and product sales of your Company are, as disclosed in the accompanying Note XX, transactions between related parties. However, we were unable, as a result of the limits imposed by management, to perform the necessary audit procedures on those transactions. Thus we were unable to conclude whether these transactions were fair and reasonable.Because of the inability to perform the necessary audit procedures on the related party transaction mentioned above and the impossibility to determine their impact on the financial statements as a whole, we are unable to express an audit opinion whether the financial statements referred to above comply with the requirements of both the Accounting Standard for Business Enterprises and other relevant financial and accounting laws and regulations promulgated by the State, or whether these financial statements present fairly the financial position as of December 31, 2002 , and the results of its operations and its cash flows for the years then ended.Certified Public Accountant: liliCertified Public Accountant: zhanghua**Certified Public Accountants(name and stamp of the firm)Beijing, People’s Republic of China February 26, 20036.Following is an example of an audit report containing special purpose engagementsAudit ReportTo: The Board of Directors (or Shareholders)of ABC company ltd.:We have audited the accompanying statement of expenditures of ABC Limited Beijing Representative Office (the “Office”) for the year ended December 31, 2002 which has been prepared on the tax basis. This statement is the responsibility of the Office’s management. Our responsibility is to express an opinion on this statement based on ouraudit.We conducted our audit in accordance with the Independent Auditing Standards for Certified Public Accountants. Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.In our opinion, the statement of expenditures referred to above has been properly prepared on the tax basis, and presents fairly, in all material respects, the expenditures of the Office for the year ended December 31, 2002.This report is intended solely for the purpose of filing with the tax authorities and should not be used for any other purpose.Certified Public Accountant: lili Certified Public Accountant: zhanghuaBeijing, the PRC Febrary 25, 20037.Following is an example of an audit report containing the consolidated financial statementsAudit ReportTo: The Board of Directors (or Shareholders)of ABC company ltd.:We have audited the consolidated balance sheets of ABC Co., Ltd. and its subsidiaries (the “Group”) as of December 31, 2002 and the consolidated statements of income and retained earnings and cash flows for the years then ended. We did not audit the financial statements of Tianjin D Co., Ltd., the financial statements of which reflected total assets and total net sales accounting for 18 percent and 16 percent in 2000, respectively, of the corresponding consolidated totals. Those financial statements were audited by other CPAs whose report has been furnished to us, and our opinion, insofar as it relates to the amounts included for that entity, is based solely on the report of the other CPAs. These financial statements are the responsibility of the Group’s management. Our responsibility is to express an opinion on these financial statements based on our audits.We conducted our audit in accordance with the Independent Auditing Standards for Certified Public Accountants. Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.In our opinion, based on our audits and the report of other CPAs, the financial statements referred to above comply with the requirements of both the Accounting Standard for Business Enterprises and other relevant financial and accounting laws and regulations promulgated by the State, and present fairly, in all material respects, the consolidatedfinancial position of the Group as of December 31, 2002 and the consolidated results of its operations and its cash flows for the years then ended.Certified Public Accountant: liliCertified Public Accountant: zhanghua**Certified Public Accountants (name and stamp of the firm)Beijing, People’s Republic of China February 26, 2001Audit repor。

审计情况报告

审计情况报告审计情况报告(Audit Status Report)是指审计工作的进展情况、具体指标、发现的问题和未来的发展方向等内容的总结性报告。

该报告旨在向审计委员会、管理层、股东和其他相关利益相关者提供审计的最新概况和情况。

审计情况报告通常包含以下内容:1. 审计范围和目标:概述审计的范围、目标和时间表等基本信息。

2. 进展情况:介绍审计工作的进展情况,如已完成的工作和下一步的计划。

3. 发现的问题:列举及分析发现的问题,以及给出解决方案和建议。

4. 风险评估:对所发现的问题进行风险评估,并给出相应的管理建议。

5. 报告结论:总结审计的结论和建议,以及后续跟进工作。

下面列举三个实际案例,以便更好地理解审计情况报告的具体内容。

案例一:某电商公司财务审计情况报告该报告主要围绕公司财务管理展开,包括检查财务账目准确性和合规性、检验成本核算、现金管理控制等。

审计结果显示该公司财务管理存在多种问题,包括记录不准确、预算管理、现金控制等。

审计团队为管理层提供了改进建议,并推荐在下一次审计中持续关注财务管理的情况。

案例二:某银行IT审计情况报告该报告主要围绕银行IT系统的审计展开,包括信息安全管理、系统运行稳定性、数据备份等方面的评估。

审计结果显示该银行IT系统存在多个风险,如过多的数据访问权限、系统存储容量不足等。

审计团队向管理层提供了一系列的改进建议,并推荐在下一次审计中重点关注技术风险管理。

案例三:某制药公司生产工艺审计情况报告该报告主要围绕制药公司的生产工艺展开,包括生产安全控制、产品质量控制等方面的评估。

审计结果显示该公司生产工艺存在多个问题,如产品不合格率高、操作规程不规范等。

审计团队向管理层提供了改进建议,并推荐在下一次审计中重点关注生产安全和产品质量问题。

总之,审计情况报告对企业的管理和发展至关重要。

通过全面、客观的评估,能够揭示企业内部存在的问题,并提供明确的改进方向,从而帮助企业追求更加优秀的运营和管理。

Audit Report审计报告

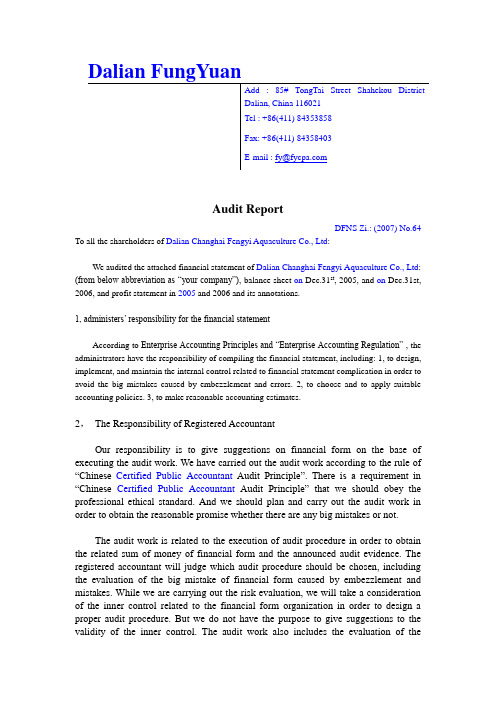

Audit ReportDFNS Zi.: (2007) No.64 To all the shareholders of Dalian Changhai Fengyi Aquaculture Co., Ltd:We audited the attached financial statement of Dalian Changhai Fengyi Aquaculture Co., Ltd: (from below abbreviation as “your company”), balance sheet on Dec.31st, 2005, and on Dec.31st, 2006, and profit statement in 2005 and 2006 and its annotations.1, administers’ responsibility for the financial statementAccording to Enterprise Accounting Principles and “Enterprise Accounting Regulation” , the administrators have the responsibility of compiling the financial statement, including: 1, to design, implement, and maintain the internal control related to financial statement complication in order to avoid the big mistakes caused by embezzlement and errors. 2, to choose and to apply suitable accounting policies. 3, to make reasonable accounting estimates.2,The Responsibility of Registered AccountantOur responsibility is to give suggestions on financial form on the base of executing the audit work. We have carried out the audit work according to the rule of “Chinese Certified Public Accountant Audit Principle”. There is a requirement in “Chinese Certified Public Accountant Audit Principle” that we should obey the professional ethical standard. And we should plan and carry out the audit work in order to obtain the reasonable promise whether there are any big mistakes or not.The audit work is related to the execution of audit procedure in order to obtain the related sum of money of financial form and the announced audit evidence. The registered accountant will judge which audit procedure should be chosen, including the evaluation of the big mistake of financial form caused by embezzlement and mistakes. While we are carrying out the risk evaluation, we will take a consideration of the inner control related to the financial form organization in order to design a proper audit procedure. But we do not have the purpose to give suggestions to the validity of the inner control. The audit work also includes the evaluation of theappropriation of the accountant policy that the managers use to choose an accountant and the rationality of an account decision that they make. And it also includes the whole list of estimating the financial form.3, Audit OpinionWe think that the provided accounting statements are in conformity with the regulations of <<Company Accounting Principles and Copmany Accounting Regulation>>, which can objectively reflect the financial status as from Dec. 31, 2005 to Dec. 31, 2006, and business achievements of Year 2005 and Year 2006 of the company.Enclosed:1.Balance Sheet of Dec. 31, 2005 and Profit Statement of Year 20052.Balance Sheet of Dec. 31, 2006 and Profit Statement of Year 2006Dalian FundYuan Certified Public Accountants Co., Ltd. (Seal)Dalian ChinaCertified Public Accountant of the People’s Republic of China: Yuan Shichun (Seal)Certified Public Accountant of the People’s Republic of China: Yu Hongwei (Seal)Jun.20th, 2007。

Audit Reports

Materiality Decisions

Failure to follow GAAP

Audit report

Unqualified

Qualified opinion only

Adverse

Materiality Decisions

Materiality Decisions

Scope limitation

Auditor’s Decision Process

Determine whether any condition exists requiring a departure from a standard unqualified report.

Decide the materiality for each condition. Decide the appropriate type of report. Write the audit report.

Audit Reports

Learning Objective 1

Describe the parts of the standard unqualified

audit report.

Parts of the Standard Unqualified Audit Report

1. Report title 2. Audit report address 3. Introductory paragraph 4. Scope paragraph 5. Opinion paragraph 6. Name of CPA firm 7. Audit report date

Consistency versus Comparability

Changes that affect comparability but not consistency:

audit_report

TRAINING MATERIALTHE AUDIT REPORTINTRODUCTIONThe audit report is the written document presented to the principal, authorizer or other statutory recipients by the auditors or audit institution responsible for fulfilling an audit assignment.It is an integrated reflection of the audit work and its results and an important way to exhibit audit achievements. As the subjects of audit, types of audit assignments and recipients of reports differ, audit reports also differ in nature, contents, binding force and methods of preparation. The audit report referred to herein is the audit report that is prepared by the audit team and submitted to the audit institution in the conduct of government audits. It is a written document that the audit team presents to its dispatching audit institution at the completion of field audit about the fulfillment of audit tasks and achievement of audit results.The Role of the Audit ReportAs a summary of audit work and its achievements, the audit report is of great significance to the audit institution, the audited body and other users of the report. The audit report is the essential basis for the top management of the audit institution to learn about the conduct of audit, make relevant judgment and handle audit issues. According to the Audit Law, after auditing the audit items, auditors should submit their audit report to the audit institution within the prescribed time limit explaining audit work and results, evaluating audit items and putting forward audit recommendations. Consequently, the audit institution can use the report to understand work done by the audit team, including timing, scope and methods of audit, basic situation and business operation/results of the audited body and problems discovered in the course of audit.The audit report is the foundation for audit opinions and decisions. After the audit team completes the audit assignment, the audit institution needs to evaluate the truthfulness, compliance and effectiveness of the audit items, produce its audit opinion, and make its audit decision on punitive measures (such measures are to be imposed on the audited body against its irregular actions of revenues and expenditures that are discovered in audit). Only by relying on the audit report presented by the audit team can the audit institution understand the economic activities of the auditedbody or project, learn about the latter’s compliance with relevant laws and regulations and then evaluate the audit items and mete out appropriate penalties or punishments. The audit report is an important source for the audit institution to prepare audit information for the government’s macroscopic decision making. By summarizing, integrating and analyzing information provided by each individual audit report from the perspective of macroscopic operation and management, the audit institution can play its role in promoting and strengthening macroscopic management within a certain scope by providing the government and relevant organizations with factual, analytical and suggestive audit informationThe audit report is an important reference for the audited body to improve its management. In the audit report, auditors evaluate the financial position, profitability and liquidity of the audited body, evaluate and analyze causes for errors in financial activities and defects in internal control, disclose existing problems and shortcomings and put forward recommendations for reference of competent authorities. Such information and comments provided by the auditors are of great reference value for the audited body to improve its internal control and management.CONTENTS OF THE AUDIT REPORTAs a type of documentation employed in the audit institution, the audit report possesses all the basic elements of an official document, including title, major recipient, subjects of report, signature by the audit team leader, date of reporting, etc. ∙The title of the audit report should include the name of the audited body, major contents and timing of the audit items.∙Major recipient of the audit report usually refers to the audit institution that dispatches the audit team to do the audit assignment.∙Subjects of report are main component of the audit report reflecting the audit work and its results.∙Signature of the audit team leader means that the team leader assumes responsibility for the truthfulness and lawfulness of the contents reported by his team.∙Date of reporting refers to the date when field audit is completed.To be more specific, the audit report includes the following aspects:Explanation of audit tasksThe audit report should provide a concise explanation about the relevant audit tasks. Such an explanation covers the following∙Audit basis;∙Name of the audit subject, i.e., name of the audited body or project;∙Scope and contents of audit, i.e., time limit, audit scope and specific audit items; ∙Audit approaches adopted in the audit;∙Areas requiring sampling or extended audit;∙Explanation about the handling of material issues;∙Cooperation and assistance provided by the audited body.Explanation of these aspects can help users of the audit report to gain a basic understanding of the nature and tasks of the audit assignment.Explanation about accounting and auditing responsibilitiesThe audit report should clarify the accounting responsibility of the audited body and auditing responsibility of the auditors so that the users can understand and use the report correctly. It is the responsibility of the audited body to ensure that accounting information is true, complete and lawful while responsibility of the auditors is to express opinions as to the truthfulness, compliance and effectiveness of revenues and expenditures of the audited body.Basic information about the audited bodyThe audit report should briefly explain the basic situation of the audited body so that the report users can gain an understanding of the latter. Such explanation covers the following∙Business nature, management system, evolution, organizational set-up, business scope and scale of the audited body;∙Financial affiliation and accounting system of the audited body;∙Major economic indicators of the fiscal year under audit;∙Material issues related to audit items;∙Changes of business and legal context in which the audited body operates;∙Impact of state macroscopic economic situ ation on the audited body’s revenues and expenditures.The conduct of the auditThe conduct of audit covers two aspects:∙Information about the audit including work done by the audit team, audit procedure and methods adopted by the audit team, adjustments made to the audit programs and fulfillment of audit tasks.∙Confirmation of facts related to audit items after the completion of audit such as disclosure of revenues and expenditures of the audited body.Audit evaluationAudit evaluation covers∙Evaluation of truthfulness, compliance and effectiveness of the audited items;∙Evaluation of internal control related to the audited body’s revenues and expenditures;∙Evaluation of the audited body’s accountability.Audit findingsDisclosure of problems existing in audit items is an important component of the audit report and a concrete reflection of audit achievements. Audit findings refer to irregular actions of revenues and expenditures that are committed by the audited body and discovered by the auditors in the course of audit. In the report, auditors should explain such findings, covering the following aspects:∙Details about revenues and expenditures that are in violation of relevant state laws and regulations;∙Causes for such irregularities;∙Details of provisions that have been violated;∙Impacts or consequences of the irregularities.Audit opinions and recommendationsFor the above-mentioned audit findings, the audit report should put forward corresponding audit opinions or recommendations. Audit opinions mentioned herein refer to opinions on imposing penalties and punishments on the audited body against its irregular actions of revenues and expenditures that have violated relevant laws andregulations to the point of being liable to such punitive measures. Where the audited body falls behind standards in its business activities and is weak in management, the auditors should put forward recommendations for improvement. For audit findings that go beyond the mandate of the audit institution and should be subject to punitive measures imposed by other relevant organizations, the audit report should produce recommendations that such relevant organizations should mete out the appropriate penalties or punishments.PROCEDURE FOR PREPARING, REVIEWING AND FINALIZING THE AUDIT REPORTThe audit report is usually prepared according to the following steps:∙Sorting out and analyzing audit working papersAudit working papers are historical records about the auditors’ audit work and the direct basis for preparing the audit report. However, as each working paper is prepared for an individual item, the information contained in such papers ispiecemeal thereby unable to give a comprehensive reflection of the entire audit assignment. Therefore, prior to the preparation of the audit report, auditors should sum up, sort out, classify and analyze various audit working papers. Such work mainly cover the following aspects:o To examine whether the audit tasks as laid down in the audit program have been fulfilled with corresponding working papers providing supportinginformation;o To sort out all audit findings, and then classify and summarize according to their different nature;o To review whether facts about audit findings are clear with sufficient and appropriate corresponding audit evidence;o To analyze audit items within the audit scope and judge whether the facts are clarified, whether relevant audit evidence has been obtained andwhether audit conclusions are correctly drawn.∙Screening audit information to select audit evidenceAs a government audit report should give a separate disclosure of audit findings, it is necessary for auditors to select the key information related to problems found in audit before they prepare the report in accordance with the audit objectives and thenature of audit findings. Afterward, they should classify and sort out the selected information.First, auditors should classify audit findings into different types according to their different nature and arrange them in order of amounts or according to the degree of seriousness.Secondly, the selection of audit evidence should be able to support the disclosed problems.Evidence should be chosen according to the principles of sufficiency, relevance, objectivity and lawfulness.∙Outlining and drafting the audit reportAfter summarizing and sorting out the audit findings, the audit team can discuss the outline of the audit report focusing on the following:o Whether the outline has a clear theme and reasonable structure;o Whether the outline lists clear subjects and reflects major issues to be resolved by the report;o Whether the outline contains clear facts, sufficient evidence and correct conclusions for the problems listed and whether further investigation isneeded for collection of evidence.After determining the outline, auditors can draft the audit report, discuss andrevise the draft within the audit team and ask the audit team leader to reviewand approve the draft, thereby forming the exposure draft of the audit report. ∙Soliciting opinions from the audited body and revising the audit report Before submitting the audit report to the audit institution, the audit team should solicit opinions from the audited body as to whether facts acknowledged by the audit team are correct, whether the right laws and regulations are applied, whether the audit evaluation is objective, whether audit opinions and recommendations are reasonable and effective.The audited body should present its written comments to the audit team or audit institution 10 days within its receipt of the audit report. Where the audited body fails to do so within the prescribed time limit, it is regarded that the audited body has no objection to the audit report. Upon receipt of comments from the audited body, however, the audit team should study them in an earnest manner.For disagreements with the audit report due to obscure facts and insufficientevidence, the audit team should make further verification and supplementation.Where the audited body holds that the audit report makes inappropriate reference to laws and regulations, necessary adjustments should be made. For the audited body’s disagreement with the audit team’s evaluation, audit opinions andrecommendations, auditors should adopt the audited body’s reasonable comments.The audit team should also explain its reasons for not adopting certain writtencomments made by the audited body.In conclusion, the audit team should produce an explanation on the audited body’s feedback on the exposure draft and submit it to the audit institution together with the report itself for review and approval.Reviewing the audit reportAfter receiving the audit report submitted by the audit team, the audit institution should ask full-time reviewers or organization to review the report and produce review opinions.Examining and approving the audit report by the audit institutionAfter the reviewing process, the audit institution will examine and approve the audit report. For audit reports on ordinary audit items, competent members of the top management of the audit institution can carry out this job while audit panel meetings will examine and approve reports on material items. In this process, the audit institution focuses on the following:∙Whether facts related to the audit items are clear and whether audit evidence is solid;∙Whether the audited body gives right comments on the audit report and whether the review organizations or reviewers produce correct review opinions;∙Whether audit evaluation is appropriate;∙Whether judgmental opinions and recommendations for punitive measures concerning irregular actions are correct, lawful and appropriate.REQUIREMENTS FOR A QUALITY REPORTTo ensure that the audit report is of high quality and plays an effective role, auditors should meet the following requirements in preparing the report:∙Clear facts and true dataFacts listed in the audit report should be clear while data should be accurate, true and reliable. Origins and causal relations should be clarified. These will enable the audit institution to carry out correct evaluation and draw correct conclusion of the audit items and the report users to gain a correct understanding of the report. ∙Complete contents and clear prioritiesThe audit report must contain complete contents so as to give a complete andaccurate reflection of the audit results and make correct evaluation of thetruthfulness, compliance and effectiveness of the audited body’s revenues and expenditures within a certain period. To begin with, the report must be complete in its basic elements. Secondly, details of the report should be able to reflect the actual situation of the audited body. Meanwhile, the audit report should focus on priorities.∙Clear arrangement of ideas and reasonable structureTo promote its readability and enable the users to make correct judgments and decisions, the audit report should arrange ideas in a clear and reasonable structure.Clear arrangement of ideas means summarization of the contents and arrangement in a logical way. Each paragraph should focus on a single main idea whileinterrelated to other paragraphs. Issues of the same type should be stated in the same paragraph or section instead of scattered among several paragraphs.Similarly, the same paragraph should not attempt to explain several differentissues.Reasonable structure means that the framework of the report should meet standard requirements with reasonable arrangements of major and minor issues. In general, major issues are stated first followed by minor ones. When stating an issue, facts should be given first, followed by the judgement on their nature, production of recommendations for punitive measure. In other words, the actual situation is put forward at the beginning, followed by evaluation, opinions and recommendations. ∙Sufficient evidence and correct judgmentThe audit report should be based on facts using evidence to prove such facts.Relevant laws and regulations should be regarded as the criteria for judgement.Evidence used in the report must be reliable and sufficient to support the audit opinions. To make judgments on the nature of the audit items, auditors mustgrasp the fundamental features of the items and refer to appropriate laws andregulations. If using references, they should quote the relevant legal article in addition to the name and reference number of the document so that theirevaluation and recommendations can be more convincing.∙Concise wording and accurate expressionThe audit report is an official document of the audit institution. Therefore, reports should be concise and correct in wording and conform to the format of auditdocumentation. Sticking to the principle of making clear explanations forconcerned issues, auditors should use qualitative, quantitative, judgmental and reflective words in preparing the audit report. In short, the report should use plain words to help the users understand. Obscurity and exaggeration should be strictly avoided.∙Compliance with principles and adherence to factsCompliance with principles means that the audit report should make fairevaluation of the truthfulness, compliance and effectiveness of audit itemsaccording to relevant laws and regulations. A firm attitude should be maintained in this process. To be more specific, auditors should make their judgment of the nature of audit findings and produce their recommendations for punitive measures strictly on the basis of facts and with the use of legal criteria. They should neither withdraw in the face of contradictions nor avoid heavier responsibilities to assume lighter tasks.Adherence to facts means that the audit report should disclose the true situation and problems of the audited body without overstatement or understatement. Audit evaluation should be appropriate, i.e., pointing out shortcomings while affirming achievements. For problems existing in the audited body, the audit report should analyze their causal relations and the larger context in a fair and objective manner instead of imposing punitive measures in simplistic ways.。

Audit Reports(英文版)(ppt 55页)

Standard unqualified

Qualified

Unor modified wording

Adverse or disclaimer

3-9

Components of Auditors’ Report

Three paragraphs ➢ Introductory ➢ Scope ➢ Opinion

the audit.

3 - 12

Scope Paragraph

F/S are on auditor’s letterhead Produced by accountant’s computer F/S state that they are the auditors.

3-2

3-3

Assurance F/S Audits

An auditor's opinion on financial statements is an explicit statement of the auditor's conclusion.

All reports except disclaimer are positive assurance. Examples of positive assurance reports:

Unqualified Qualified Adverse

3-4

Negative Assurance

Negative assurance is a statement that the auditor is not aware of any material departures from GAAP

Audit Reports(英文 版)(ppt 55页)

3-1

Audit Report(1)

Audit ReportTo the board of directors of ×××××:We have audited the accompanying balance sheets of the Company and the Group as of 31 December 2004 and the related statements of income and income appropriation and cash flows of the Company and the Group for the year then ended. The preparation of these financial statements is the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audit.We planed and performed our audit in accordance with China’s Independent Auditing Standards to obtain reasonable assurance as to whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assess ing the accounting policies adopted and significant accounting estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our auditprovides a reasonable basis for our opinion.In our opinion, the financial statements on pages×to×,comply with the requirements of the Accounting Standards for Business Enterprises and the Accounting System for Business Enterprises promulgated by the State, and present fairly, in all material respects, the financial position of the Company as at 31 December 2004 and the results of its operation and cash flows for the year then endedCertified Public Accountants Chinese CPAChina Nanjing Chinese CPAReporting Date。

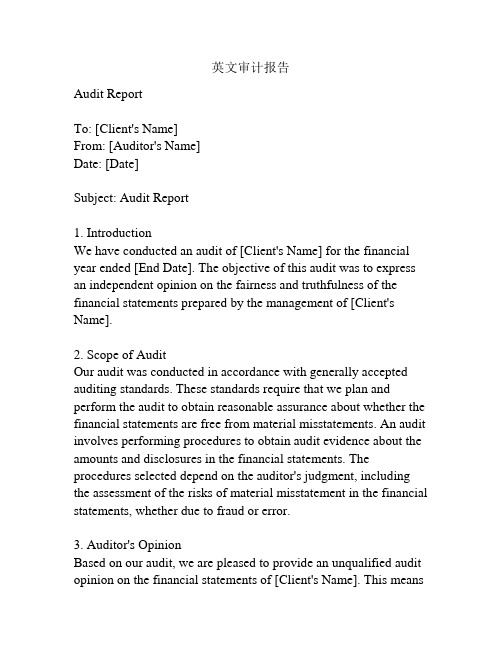

英文审计报告

英文审计报告Audit ReportTo: [Client's Name]From: [Auditor's Name]Date: [Date]Subject: Audit Report1. IntroductionWe have conducted an audit of [Client's Name] for the financial year ended [End Date]. The objective of this audit was to express an independent opinion on the fairness and truthfulness of the financial statements prepared by the management of [Client's Name].2. Scope of AuditOur audit was conducted in accordance with generally accepted auditing standards. These standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatements. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement in the financial statements, whether due to fraud or error.3. Auditor's OpinionBased on our audit, we are pleased to provide an unqualified audit opinion on the financial statements of [Client's Name]. This meansthat, in our opinion, the financial statements present fairly, in all material respects, the financial position of [Client's Name] as of [End Date] and the results of its operations and its cash flows for the year then ended in accordance with the applicable financial reporting framework.4. Key Audit FindingsDuring the course of our audit, we identified certain significant matters that we believe should be brought to your attention:a) Revenue Recognition: We noted that the company recognized revenue on a percentage of completion basis for long-term contracts. We reviewed the contracts and found that the method of revenue recognition was appropriate and in accordance with accounting standards.b) Accounts Receivable: We examined the company's procedures for recording accounts receivable and found them to be adequate. We also tested a sample of accounts receivable and found no material misstatements.c) Inventory: We tested the company's inventory reconciliation process and found it to be accurate. The company has controls in place to prevent any material misstatements.5. management's ResponseManagement has reviewed our audit findings and provided us with their responses, which we believe adequately address the matters raised during the audit. They have agreed to take corrective actions where necessary to strengthen internal controls and improvefinancial reporting.6. ConclusionBased on our audit procedures and the evidence obtained, we believe that the financial statements of [Client's Name] present fairly, in all material respects, the financial position of the company as of [End Date], and the results of its operations and cash flows for the year then ended.We appreciate the cooperation and assistance provided by the management throughout the audit process. If you have any questions or require further information, please feel free to contact us.Yours faithfully,[Auditor's Name][Position][Company Name]。

审计报告AuditReport

审计署国外贷援款项目审计服务中心Audit Service Center of China National Audit Office for Foreign Loan and Assistance Projects审计报告Audit Report审外中报〔2016〕23号AUDIT REPORT〔2016〕NO. 23项目名称:世界银行贷款中国节能融资项目–中国进出口银行Project Name:China Energy Efficiency Financing Project Financed by the World Bank –the Export-Import Bank ofChina贷款编号:7529–CNLoan No.:7529–CN项目执行单位:中国进出口银行Project Entity: The Export-Import Bank of China会计年度:2015Accounting Year: 2015目录Contents一、审计师意见 (1)Ⅰ. Auditor’s Opinion (3)二、财务报表及财务报表附注 (5)II. Financial Statements and Notes to the Financial Statements (5)(一)资金平衡表 (5)i. Balance Sheet (5)(二)项目进度表 (7)ii. Summary of Sources and Uses of Funds by Project Component (7)(三)贷款协定执行情况表 (11)iii. Statement of Implementation of Loan Agreement (11)(四)财务报表附注 (12)iv. Notes to the Financial Statements (15)三、审计发现的问题及建议 (18)III. Audit Findings and Recommendations (20)一、审计师意见审计师意见中国进出口银行:我们审计了世界银行贷款中国节能融资项目2015年12月31日的资金平衡表及截至该日同年度的项目进度表、贷款协定执行情况表等特定目的财务报表及财务报表附注(第5页至第17页)。

Audit Reports(英文版)(ppt 55页)

Negative Assurance - based on our review, we are not aware of any material modifications. Used for reviews.

No assurance - disclaimer of opinion, no opinion at all. Used for compilations.

Standard unqualified

Qualified

Unqualified with explanatory paragraph or modified wording

Adverse or disclaimer

Components of Auditors’ Report

Three paragraphs ➢ Introductory ➢ Scope ➢ Opinion

for opinions other than unqualified

Auditors Assurance of GAAP

Financial Statements are:

In accordance with GAAP Accounting principles are appropriate for

审计报告英文

审计报告英文As an auditor, it is essential to prepare an audit report that accurately reflects the findings and conclusions of the audit process. The audit report serves as a communication tool between the auditor and the stakeholders, providing them with an understanding of the audit scope, objectives, methodology, and the results of the audit.The purpose of an audit report is to provide an independent, objective assessment of the financial statements and internal controls of an organization. It is important for the report to be clear, concise, and accurate, in order to effectively communicate the audit findings to the stakeholders. The report should also include recommendations for improvement, if any, to help the organization address any identified weaknesses or deficiencies.In preparing the audit report, the auditor should adhere to professional standards and guidelines, ensuring that the report is based on sufficient and appropriate evidence gathered during the audit process. The report should also be free from any bias or conflicts of interest, maintaining the independence and objectivity of the audit findings.The audit report typically includes the following sections:1. Introduction: This section provides an overview of the audit objectives, scope, and methodology. It also includes a brief description of the audited entity and the period covered by the audit.2. Executive Summary: The executive summary provides a high-level overview of the audit findings, conclusions, and recommendations. It is designed to provide the stakeholders with a quick understanding of the key points of the audit report.3. Scope of the Audit: This section outlines the specific areas and processes that were included in the audit, as well as any limitations or restrictions that may have affected the audit scope.4. Audit Findings: This section presents the detailed findings of the audit, including any significant issues or deficiencies identified during the audit process. The findings should be presented in a clear and organized manner, with supporting evidence and documentation.5. Conclusion: The conclusion section summarizes the overall results of the audit and provides the auditor's opinion on the fairness and accuracy of the financial statements and the effectiveness of the internal controls.6. Recommendations: This section includes any recommendations for improvement or corrective actions that the organization should consider in response to the audit findings.In conclusion, the audit report is a critical component of the audit process, providing stakeholders with an independent assessment of the organization's financial statements and internal controls. It is important for the report to be clear, concise, and accurate, in order to effectively communicate the audit findings and recommendations. By adhering to professional standards and guidelines, the auditor can ensure the quality and integrity of the audit report, ultimately contributing to the credibility and reliability of the audit process.。

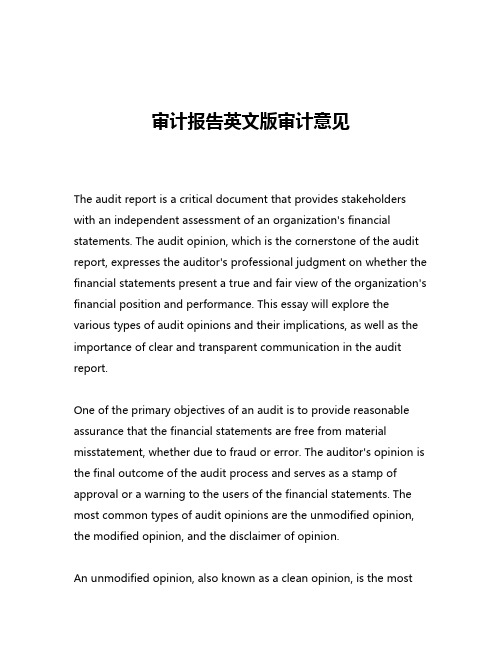

审计报告英文版审计意见

审计报告英文版审计意见The audit report is a critical document that provides stakeholders with an independent assessment of an organization's financial statements. The audit opinion, which is the cornerstone of the audit report, expresses the auditor's professional judgment on whether the financial statements present a true and fair view of the organization's financial position and performance. This essay will explore the various types of audit opinions and their implications, as well as the importance of clear and transparent communication in the audit report.One of the primary objectives of an audit is to provide reasonable assurance that the financial statements are free from material misstatement, whether due to fraud or error. The auditor's opinion is the final outcome of the audit process and serves as a stamp of approval or a warning to the users of the financial statements. The most common types of audit opinions are the unmodified opinion, the modified opinion, and the disclaimer of opinion.An unmodified opinion, also known as a clean opinion, is the mostfavorable audit opinion. It indicates that the auditor has obtained sufficient and appropriate audit evidence to conclude that the financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework. This opinion conveys that the financial statements present a true and fair view of the organization's financial position and performance, and that the auditor has not identified any significant issues or concerns.In contrast, a modified opinion is issued when the auditor has encountered one or more issues that affect the financial statements. There are three main types of modified opinions: the qualified opinion, the adverse opinion, and the disclaimer of opinion. A qualified opinion is issued when the auditor has identified a matter that, while not pervasive, is material to the financial statements. This could be due to a limitation in the scope of the audit, a departure from the applicable financial reporting framework, or a disagreement with management. An adverse opinion is the most severe form of modified opinion, and it is issued when the auditor concludes that the financial statements are materially misstated and do not present a true and fair view. A disclaimer of opinion is issued when the auditor is unable to obtain sufficient appropriate audit evidence to form an opinion on the financial statements, usually due to significant limitations in the scope of the audit.The language and structure of the audit report, including the auditopinion, are crucial in conveying the auditor's findings to the users of the financial statements. The audit report should be clear, concise, and easy to understand, with the audit opinion prominently displayed. The report should also include a description of the auditor's responsibilities, the scope of the audit, and any significant matters that arose during the audit process.One of the key challenges in audit reporting is ensuring that the communication is transparent and understandable to a wide range of stakeholders, from financial analysts to the general public. The auditor must strike a balance between providing technical details and using plain language that can be readily understood by non-experts. This is particularly important in the case of modified opinions, where the auditor must clearly explain the reasons for the modification and its potential impact on the financial statements.In recent years, there have been calls for greater transparency and enhanced communication in audit reporting. This has led to the development of new reporting standards, such as the International Auditing and Assurance Standards Board's (IAASB) revised auditor's report, which includes the introduction of key audit matters (KAMs). KAMs are areas that, in the auditor's professional judgment, were of most significance in the audit of the current period's financial statements. By highlighting these matters, the auditor can provide users with a better understanding of the audit process and the areasthat required significant auditor attention.The importance of clear and transparent communication in the audit report cannot be overstated. The audit opinion is a critical piece of information that informs the decisions of a wide range of stakeholders, from investors and lenders to regulators and the general public. By providing a clear and unambiguous assessment of the financial statements, the auditor can help to build trust in the financial reporting process and contribute to the overall transparency and accountability of the organization.In conclusion, the audit report and the audit opinion are essential components of the financial reporting ecosystem. The auditor's opinion serves as a stamp of approval or a warning to the users of the financial statements, and the language and structure of the report play a crucial role in conveying the auditor's findings. As the demands for greater transparency and enhanced communication in audit reporting continue to grow, it is incumbent upon auditors to ensure that their reports are clear, concise, and easily understood by all stakeholders.。

audit_report

KPMG – BARENTS GROUP LLC 2001 NOVEMBER ADB CNAO AUDIT STANDARDS PROJECT TRAINING MATERIALTHE AUDIT REPORTINTRODUCTIONThe audit report is the written document presented to the principal, authorizer or other statutory recipients by the auditors or audit institution responsible for fulfilling an audit assignment.It is an integrated reflection of the audit work and its results and an important way to exhibit audit achievements. As the subjects of audit, types of audit assignments and recipients of reports differ, audit reports also differ in nature, contents, binding force and methods of preparation. The audit report referred to herein is the audit report that is prepared by the audit team and submitted to the audit institution in the conduct of government audits. It is a written document that the audit team presents to its dispatching audit institution at the completion of field audit about the fulfillment of audit tasks and achievement of audit results.The Role of the Audit ReportAs a summary of audit work and its achievements, the audit report is of great significance to the audit institution, the audited body and other users of the report. The audit report is the essential basis for the top management of the audit institution to learn about the conduct of audit, make relevant judgment and handle audit issues. According to the Audit Law, after auditing the audit items, auditors should submit their audit report to the audit institution within the prescribed time limit explaining audit work and results, evaluating audit items and putting forward audit recommendations. Consequently, the audit institution can use the report to understand work done by the audit team, including timing, scope and methods of audit, basic situation and business operation/results of the audited body and problems discovered in the course of audit.The audit report is the foundation for audit opinions and decisions. After the audit team completes the audit assignment, the audit institution needs to evaluate the truthfulness, compliance and effectiveness of the audit items, produce its audit opinion, and make its audit decision on punitive measures (such measures are to be imposed on the audited body against its irregular actions of revenues and expenditures that are discovered in audit). Only by relying on the audit report presented by the audit team can the audit institution understand the economic activities of the auditedKPMG – BARENTS GROUP LLC 2001 NOVEMBER ADB CNAO AUDIT STANDARDS PROJECT body or project, learn about the latter’s compliance with relevant laws and regulations and then evaluate the audit items and mete out appropriate penalties or punishments. The audit report is an important source for the audit institution to prepare audit information for the government’s macroscopic decision making. By summarizing, integrating and analyzing information provided by each individual audit report from the perspective of macroscopic operation and management, the audit institution can play its role in promoting and strengthening macroscopic management within a certain scope by providing the government and relevant organizations with factual, analytical and suggestive audit informationThe audit report is an important reference for the audited body to improve its management. In the audit report, auditors evaluate the financial position, profitability and liquidity of the audited body, evaluate and analyze causes for errors in financial activities and defects in internal control, disclose existing problems and shortcomings and put forward recommendations for reference of competent authorities. Such information and comments provided by the auditors are of great reference value for the audited body to improve its internal control and management.CONTENTS OF THE AUDIT REPORTAs a type of documentation employed in the audit institution, the audit report possesses all the basic elements of an official document, including title, major recipient, subjects of report, signature by the audit team leader, date of reporting, etc. ∙The title of the audit report should include the name of the audited body, major contents and timing of the audit items.∙Major recipient of the audit report usually refers to the audit institution that dispatches the audit team to do the audit assignment.∙Subjects of report are main component of the audit report reflecting the audit work and its results.∙Signature of the audit team leader means that the team leader assumes responsibility for the truthfulness and lawfulness of the contents reported by his team.∙Date of reporting refers to the date when field audit is completed.To be more specific, the audit report includes the following aspects:KPMG – BARENTS GROUP LLC 2001 NOVEMBER ADB CNAO AUDIT STANDARDS PROJECT Explanation of audit tasksThe audit report should provide a concise explanation about the relevant audit tasks. Such an explanation covers the following∙Audit basis;∙Name of the audit subject, i.e., name of the audited body or project;∙Scope and contents of audit, i.e., time limit, audit scope and specific audit items;∙Audit approaches adopted in the audit;∙Areas requiring sampling or extended audit;∙Explanation about the handling of material issues;∙Cooperation and assistance provided by the audited body.Explanation of these aspects can help users of the audit report to gain a basic understanding of the nature and tasks of the audit assignment.Explanation about accounting and auditing responsibilitiesThe audit report should clarify the accounting responsibility of the audited body and auditing responsibility of the auditors so that the users can understand and use the report correctly. It is the responsibility of the audited body to ensure that accounting information is true, complete and lawful while responsibility of the auditors is to express opinions as to the truthfulness, compliance and effectiveness of revenues and expenditures of the audited body.Basic information about the audited bodyThe audit report should briefly explain the basic situation of the audited body so that the report users can gain an understanding of the latter. Such explanation covers the following∙Business nature, management system, evolution, organizational set-up, business scope and scale of the audited body;∙Financial affiliation and accounting system of the audited body;∙Major economic indicators of the fiscal year under audit;∙Material issues related to audit items;∙Changes of business and legal context in which the audited body operates;∙Impact of state macroscopic economic situation on the audited body’s revenues and expenditures.KPMG – BARENTS GROUP LLC 2001 NOVEMBER ADB CNAO AUDIT STANDARDS PROJECTThe conduct of the auditThe conduct of audit covers two aspects:∙Information about the audit including work done by the audit team, audit procedure and methods adopted by the audit team, adjustments made to the audit programs and fulfillment of audit tasks.∙Confirmation of facts related to audit items after the completion of audit such as disclosure of revenues and expenditures of the audited body.Audit evaluationAudit evaluation covers∙Evaluation of truthfulness, compliance and effectiveness of the audited items;∙Evaluation of internal control related to the audited body’s revenues and expenditures;∙Evaluation of the audited body’s accountability.Audit findingsDisclosure of problems existing in audit items is an important component of the audit report and a concrete reflection of audit achievements. Audit findings refer to irregular actions of revenues and expenditures that are committed by the audited body and discovered by the auditors in the course of audit. In the report, auditors should explain such findings, covering the following aspects:∙Details about revenues and expenditures that are in violation of relevant state laws and regulations;∙Causes for such irregularities;∙Details of provisions that have been violated;∙Impacts or consequences of the irregularities.Audit opinions and recommendationsFor the above-mentioned audit findings, the audit report should put forward corresponding audit opinions or recommendations. Audit opinions mentioned herein refer to opinions on imposing penalties and punishments on the audited body against its irregular actions of revenues and expenditures that have violated relevant laws andKPMG – BARENTS GROUP LLC 2001 NOVEMBER ADB CNAO AUDIT STANDARDS PROJECT regulations to the point of being liable to such punitive measures. Where the audited body falls behind standards in its business activities and is weak in management, the auditors should put forward recommendations for improvement. For audit findings that go beyond the mandate of the audit institution and should be subject to punitive measures imposed by other relevant organizations, the audit report should produce recommendations that such relevant organizations should mete out the appropriate penalties or punishments.PROCEDURE FOR PREPARING, REVIEWING AND FINALIZING THE AUDIT REPORTThe audit report is usually prepared according to the following steps:∙Sorting out and analyzing audit working papersAudit working papers are historical records about the auditors’ audit work and the direct basis for preparing the audit report. However, as each working paper is prepared for an individual item, the information contained in such papers ispiecemeal thereby unable to give a comprehensive reflection of the entire audit assignment. Therefore, prior to the preparation of the audit report, auditors should sum up, sort out, classify and analyze various audit working papers. Such work mainly cover the following aspects:o To examine whether the audit tasks as laid down in the audit program have been fulfilled with corresponding working papers providing supportinginformation;o To sort out all audit findings, and then classify and summarize according to their different nature;o To review whether facts about audit findings are clear with sufficient and appropriate corresponding audit evidence;o To analyze audit items within the audit scope and judge whether the facts are clarified, whether relevant audit evidence has been obtained andwhether audit conclusions are correctly drawn.∙Screening audit information to select audit evidenceAs a government audit report should give a separate disclosure of audit findings, it is necessary for auditors to select the key information related to problems found in audit before they prepare the report in accordance with the audit objectives and theKPMG – BARENTS GROUP LLC 2001 NOVEMBER ADB CNAO AUDIT STANDARDS PROJECT nature of audit findings. Afterward, they should classify and sort out the selected information.First, auditors should classify audit findings into different types according to their different nature and arrange them in order of amounts or according to the degree of seriousness.Secondly, the selection of audit evidence should be able to support the disclosed problems.Evidence should be chosen according to the principles of sufficiency, relevance, objectivity and lawfulness.∙Outlining and drafting the audit reportAfter summarizing and sorting out the audit findings, the audit team can discuss the outline of the audit report focusing on the following:o Whether the outline has a clear theme and reasonable structure;o Whether the outline lists clear subjects and reflects major issues to be resolved by the report;o Whether the outline contains clear facts, sufficient evidence and correct conclusions for the problems listed and whether further investigation isneeded for collection of evidence.After determining the outline, auditors can draft the audit report, discuss andrevise the draft within the audit team and ask the audit team leader to reviewand approve the draft, thereby forming the exposure draft of the audit report.∙Soliciting opinions from the audited body and revising the audit report Before submitting the audit report to the audit institution, the audit team should solicit opinions from the audited body as to whether facts acknowledged by the audit team are correct, whether the right laws and regulations are applied, whether the audit evaluation is objective, whether audit opinions and recommendations are reasonable and effective.The audited body should present its written comments to the audit team or audit institution 10 days within its receipt of the audit report. Where the audited body fails to do so within the prescribed time limit, it is regarded that the audited body has no objection to the audit report. Upon receipt of comments from the audited body, however, the audit team should study them in an earnest manner.For disagreements with the audit report due to obscure facts and insufficientKPMG – BARENTS GROUP LLC 2001 NOVEMBER ADB CNAO AUDIT STANDARDS PROJECT evidence, the audit team should make further verification and supplementation.Where the audited body holds that the audit report makes inappropriate reference to laws and regulations, necessary adjustments should be made. For the audited body’s disagreement with the audit team’s evaluation, audit opinions andrecommendations, auditors should adopt the audited body’s reasonable comments.The audit team should also explain its reasons for not adopting certain writtencomments made by the audited body.In conclusion, the audit team should produce an explanation on the audited body’s feedback on the exposure draft and submit it to the audit institution together with the report itself for review and approval.Reviewing the audit reportAfter receiving the audit report submitted by the audit team, the audit institution should ask full-time reviewers or organization to review the report and produce review opinions.Examining and approving the audit report by the audit institutionAfter the reviewing process, the audit institution will examine and approve the audit report. For audit reports on ordinary audit items, competent members of the top management of the audit institution can carry out this job while audit panel meetings will examine and approve reports on material items. In this process, the audit institution focuses on the following:∙Whether facts related to the audit items are clear and whether audit evidence is solid;∙Whether the audited body gives right comments on the audit report and whether the review organizations or reviewers produce correct review opinions;∙Whether audit evaluation is appropriate;∙Whether judgmental opinions and recommendations for punitive measures concerning irregular actions are correct, lawful and appropriate.REQUIREMENTS FOR A QUALITY REPORTTo ensure that the audit report is of high quality and plays an effective role, auditors should meet the following requirements in preparing the report:KPMG – BARENTS GROUP LLC 2001 NOVEMBER ADB CNAO AUDIT STANDARDS PROJECT ∙Clear facts and true dataFacts listed in the audit report should be clear while data should be accurate, true and reliable. Origins and causal relations should be clarified. These will enable the audit institution to carry out correct evaluation and draw correct conclusion of the audit items and the report users to gain a correct understanding of the report.∙Complete contents and clear prioritiesThe audit report must contain complete contents so as to give a complete andaccurate reflection of the audit results and make correct evaluation of thetruthfulness, compliance and effectiveness of the audited body’s revenues and expenditures within a certain period. To begin with, the report must be complete in its basic elements. Secondly, details of the report should be able to reflect the actual situation of the audited body. Meanwhile, the audit report should focus on priorities.∙Clear arrangement of ideas and reasonable structureTo promote its readability and enable the users to make correct judgments and decisions, the audit report should arrange ideas in a clear and reasonable structure.Clear arrangement of ideas means summarization of the contents and arrangement in a logical way. Each paragraph should focus on a single main idea whileinterrelated to other paragraphs. Issues of the same type should be stated in the same paragraph or section instead of scattered among several paragraphs.Similarly, the same paragraph should not attempt to explain several differentissues.Reasonable structure means that the framework of the report should meet standard requirements with reasonable arrangements of major and minor issues. In general, major issues are stated first followed by minor ones. When stating an issue, facts should be given first, followed by the judgement on their nature, production of recommendations for punitive measure. In other words, the actual situation is put forward at the beginning, followed by evaluation, opinions and recommendations.∙Sufficient evidence and correct judgmentThe audit report should be based on facts using evidence to prove such facts.Relevant laws and regulations should be regarded as the criteria for judgement.Evidence used in the report must be reliable and sufficient to support the audit opinions. To make judgments on the nature of the audit items, auditors mustKPMG – BARENTS GROUP LLC 2001 NOVEMBER ADB CNAO AUDIT STANDARDS PROJECT grasp the fundamental features of the items and refer to appropriate laws andregulations. If using references, they should quote the relevant legal article in addition to the name and reference number of the document so that theirevaluation and recommendations can be more convincing.∙Concise wording and accurate expressionThe audit report is an official document of the audit institution. Therefore, reports should be concise and correct in wording and conform to the format of auditdocumentation. Sticking to the principle of making clear explanations forconcerned issues, auditors should use qualitative, quantitative, judgmental and reflective words in preparing the audit report. In short, the report should use plain words to help the users understand. Obscurity and exaggeration should be strictly avoided.∙Compliance with principles and adherence to factsCompliance with principles means that the audit report should make fairevaluation of the truthfulness, compliance and effectiveness of audit itemsaccording to relevant laws and regulations. A firm attitude should be maintained in this process. To be more specific, auditors should make their judgment of the nature of audit findings and produce their recommendations for punitive measures strictly on the basis of facts and with the use of legal criteria. They should neither withdraw in the face of contradictions nor avoid heavier responsibilities to assume lighter tasks.Adherence to facts means that the audit report should disclose the true situation and problems of the audited body without overstatement or understatement. Audit evaluation should be appropriate, i.e., pointing out shortcomings while affirming achievements. For problems existing in the audited body, the audit report should analyze their causal relations and the larger context in a fair and objective manner instead of imposing punitive measures in simplistic ways.。

审计报告审计准则英文版

审计报告审计准则英文版Audit Report Audit Standards English VersionAuditing is a critical process that ensures the accuracy, reliability, and integrity of financial information. It is a systematic examination of an organization's accounts and records, conducted by an independent party, to verify the validity and reliability of the financial statements. The audit report is the culmination of this process, providing a comprehensive assessment of the organization's financial position, performance, and compliance with relevant laws and regulations.The audit report is a crucial document that serves as a communication tool between the auditor and the stakeholders, including management, shareholders, and regulatory authorities. It presents the auditor's findings, opinions, and recommendations based on the audit procedures performed. The report should be clear, concise, and easy to understand, ensuring that the stakeholders can make informed decisions based on the information provided.The audit report is guided by a set of established standards and principles, known as audit standards. These standards are developedand maintained by various professional organizations, such as the International Federation of Accountants (IFAC) and the American Institute of Certified Public Accountants (AICPA). The audit standards provide a framework for the auditor to conduct the audit process, ensuring consistency, reliability, and quality in the audit work.The International Standards on Auditing (ISAs) are a set of standards developed by the IFAC's International Auditing and Assurance Standards Board (IAASB). These standards are widely recognized and adopted globally, providing a common framework for auditing practices. The ISAs cover various aspects of the audit process, including planning, risk assessment, evidence gathering, reporting, and quality control.One of the key components of the ISAs is the requirement for the auditor to express an opinion on the financial statements. The auditor's opinion can be unmodified (also known as an unqualified opinion), which indicates that the financial statements are presented fairly and in accordance with the applicable financial reporting framework. Alternatively, the auditor may issue a modified opinion, such as a qualified opinion, adverse opinion, or a disclaimer of opinion, depending on the nature and extent of the issues identified during the audit.The audit report should also include a description of the auditor'sresponsibilities, the scope of the audit, and the basis for the auditor's opinion. This information helps the stakeholders understand the auditor's role and the limitations of the audit process.In addition to the ISAs, there are other standards and guidelines that may be applicable to specific industries or jurisdictions. For example, the Public Company Accounting Oversight Board (PCAOB) in the United States has its own set of auditing standards for publicly traded companies.The effective implementation of audit standards is crucial to ensuring the quality and reliability of the audit process. Auditors must have a thorough understanding of the applicable standards and must adhere to them throughout the audit engagement. This includes maintaining independence, exercising professional skepticism, and collecting sufficient and appropriate audit evidence to support their conclusions.In conclusion, the audit report and the underlying audit standards play a vital role in ensuring the transparency, accountability, and reliability of financial information. The audit report provides stakeholders with an independent and objective assessment of an organization's financial position and performance, enabling them to make informed decisions. The adherence to established auditstandards, such as the ISAs, is essential for maintaining the integrity and credibility of the audit process.。

Chapter03AuditReports(审计学-英文版)

3-8

Sarbanes-Oxley Act

This Act requires the auditor of a public company to attest to management’s report on the effectiveness of internal control over financial reporting. PCAOB Auditing standard 2 requires the audit of internal control to be integrated with the audit of the financial statements.

3-9

©2006 Prentice Hall Business Publishing, Auditing 11/e, Arens/Beasley/Elder

Sarbanes-Oxley Act

Combined Report on Financial Statements and Internal Control Over Financial Reporting 1. Introductory paragraph 2. Scope paragraph 3. Definition paragraph 4. Inherent limitations paragraph 5. Opinion paragraph

Audit Reports

Chapter 3

©2006 Prentice Hall Business Publishing, Auditing 11/e, Arens/Beasley/Elder

审计术语——内部审计报告

审计术语——内部审计报告审计术语——内部审计报告审计术语——内部审计报告内部审计报告(Internal Audit Reports)[1] 什么是内部审计报告内部审计报告是指内部审计人员,根据审计计划对被审计单位实施必要的审计程序后,就被审计单位经营活动和内部控制的适当性、合法性和有效性出具的书面文件。

[2] 内部审计报告撰写的基本原则客观性原则《内部审计具体准则第7号——审计报告》第四条规定:“内部审计人员应在审计实施结束后,以经过核实的审计证据为依据,形成审计结论与建议,出具审计报告”。

即审计报告应实事求是、不偏不倚地反映审计事项。

审计依据、标准不明确的事项,以及由各种原因导致模棱两可,事实不清的问题都不应该在审计报告中评价。

重要性原则审计报告应突出重点,以点采面,充分考虑审计风险水平,不遗漏审计中发现的重大事项。

审计评价要围绕预定的审计目标开展,不可扩大审计范围。

简洁易懂原则审计报告文字措辞要“明确、简练”。

从内部审计报告的利用来看,“明确”是指写出的报告要让大多数人能看懂,所提出的审计意见或建议具有可操作性,被审计单位一看就知道怎么做,“简练”是指内部审计报告一定要主次分明,繁简得体,能短则短,把主要方面讲清楚则可。

说明审计立项依据、审计目的和范围、审计重点和审计标准等内容。

[2] 内部审计报告的结构和主要内容1(审计概况说明审计立项依据、审计目的和范围、审计重点和审计标准等内容。

2(审计依据说明在审计过程中遵守的国家制定的相关法律、法规、上级单位制定的制度等外部依据。

3(审计结论根据已查明的事实,对被审计单位经营活动和内部控制所作的评价,结论要正确、客观、公正、实事求是,该肯定就肯定,该否定就否定,不能含糊不清,更不能掺杂任何个人意志。

4(审计决定及审计建议针对审计发现的主要问题提出的处理、处罚意见或合理化建议。

审计建议要确保可行性,不仅要体现一定的政策性和指导性,符合有关法规和制度要求,同时也要结合实际情况有较强的针对性和可操作性,否则被审计单位难以达到整改要求。