会计英语PPT(完成版) Chapter 10- Liabilities

合集下载

财务会计assets-liabilities-and-equityppt课件

later for costs that have been incurred to earn revenue. – salaries and wages – electricity and gas – supplies used – advertising

Accounting for Business Transactions

Economic Resources

Claims to Economic Resources

Assets

What is an asset? It is something a company owns or controls which has

future economic value. – land – building – equipment – goodwill

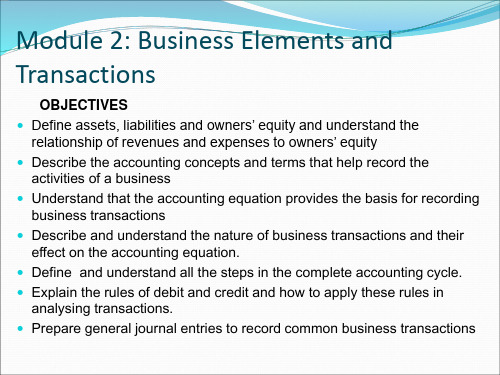

effect on the accounting equation. Define and understand all the steps in the complete accounting cycle. Explain the rules of debit and credit and how to apply these rules in

Module 2: Business Elements and Transactions

OBJECTIVES Define assets, liabilities and owners’ equity and understand the

relationship of revenues and expenses to owners’ equity Describe the accounting concepts and terms that help record the

Accounting for Business Transactions

Economic Resources

Claims to Economic Resources

Assets

What is an asset? It is something a company owns or controls which has

future economic value. – land – building – equipment – goodwill

effect on the accounting equation. Define and understand all the steps in the complete accounting cycle. Explain the rules of debit and credit and how to apply these rules in

Module 2: Business Elements and Transactions

OBJECTIVES Define assets, liabilities and owners’ equity and understand the

relationship of revenues and expenses to owners’ equity Describe the accounting concepts and terms that help record the

会计学英语电子版ppt课件

Land Buildings Vehicles Computers Furniture Equipment

15

Operating Activities

Primary activity of business

Selling goods Providing services Manufacturing Cost of Sales Advertising Paying employees Paying utilities

3. Explain the three principal types of business activity.

4. Describe the content and purpose of each of the financial statements.

3

Study Objectives

5. Explain the meaning of assets, liabilities, and stockholders’ equity, and state the basic accounting equation.

6. Describe the components that supplement the financial statements in an annual report.

4

111 Forms of Business Organization

Sole proprietorship Partnership Corporation

11

Users of Financial Information

External Users Ask?

12

311

Types of Business Activity

15

Operating Activities

Primary activity of business

Selling goods Providing services Manufacturing Cost of Sales Advertising Paying employees Paying utilities

3. Explain the three principal types of business activity.

4. Describe the content and purpose of each of the financial statements.

3

Study Objectives

5. Explain the meaning of assets, liabilities, and stockholders’ equity, and state the basic accounting equation.

6. Describe the components that supplement the financial statements in an annual report.

4

111 Forms of Business Organization

Sole proprietorship Partnership Corporation

11

Users of Financial Information

External Users Ask?

12

311

Types of Business Activity

财务会计英语ppt课件

Assets =Liabilities + Owner’s equity

Accounting element :

➢ Asset ➢ Liability ➢ Owner’s equity ➢ Revenue ➢ Expense ➢ Profit

Accrual vs Cash Accounting

Accrual Accounting权责发生制.

Similarly, accrual basis accounting requires expenses be recorded in the period in which the related revenues were recognized. Accrual basis accounting differs from cash basis accounting, where revenue and expense are recorded when cash is received or paid.

The definition of accrual basis

Accrual basises revenues and expenses, respectively, to the period they were earned and incurred. Under accrual basic accounting, revenue is recorded when product is hipped or service provided.

Time-Period Concept.会计期间

➢The time-period concept ensures that accounting information is reported at regular intervals.

Accounting element :

➢ Asset ➢ Liability ➢ Owner’s equity ➢ Revenue ➢ Expense ➢ Profit

Accrual vs Cash Accounting

Accrual Accounting权责发生制.

Similarly, accrual basis accounting requires expenses be recorded in the period in which the related revenues were recognized. Accrual basis accounting differs from cash basis accounting, where revenue and expense are recorded when cash is received or paid.

The definition of accrual basis

Accrual basises revenues and expenses, respectively, to the period they were earned and incurred. Under accrual basic accounting, revenue is recorded when product is hipped or service provided.

Time-Period Concept.会计期间

➢The time-period concept ensures that accounting information is reported at regular intervals.

会计英语(第三版)(ppt课件)

net book value 账面净值

worksheet 工作底稿

closing entries 结账分录

学习交流课件

27

income summary 收益汇总

bookkeeping procedures

账务处理程序

summarized vouchers

汇总记账凭证

categorized accounts summary

nominal account 虚账户

chart of accounts 科目表

学习交流课件

17

general ledger 总分类账

normal balance 正常余额

journalizing 记日记账

compound journal entry

复合分录

学习交流课件

18

general journal 普通日记账

posting 过账

accounting cycle 会计循环

trial balance 试算表

学习交流课件

19

adjustment 账项调整

adjusted trial balance

调整后试算表

closing 结账

post-closing trail balance

22

Chapter 3

学习交流课件

23

time period 会计期间

fiscal year 财政年度

calendar year 日历年度

natural business year

自然经营年度

学习交流课件

24

adjustments 账项调整

cash basis 现金制、收付实现制

会计英语

worksheet 工作底稿

closing entries 结账分录

学习交流课件

27

income summary 收益汇总

bookkeeping procedures

账务处理程序

summarized vouchers

汇总记账凭证

categorized accounts summary

nominal account 虚账户

chart of accounts 科目表

学习交流课件

17

general ledger 总分类账

normal balance 正常余额

journalizing 记日记账

compound journal entry

复合分录

学习交流课件

18

general journal 普通日记账

posting 过账

accounting cycle 会计循环

trial balance 试算表

学习交流课件

19

adjustment 账项调整

adjusted trial balance

调整后试算表

closing 结账

post-closing trail balance

22

Chapter 3

学习交流课件

23

time period 会计期间

fiscal year 财政年度

calendar year 日历年度

natural business year

自然经营年度

学习交流课件

24

adjustments 账项调整

cash basis 现金制、收付实现制

会计英语

《会计英语》PPT课件

② Accounting is a measure used by an entity (profit or non-profit) to accumulate, dispose, communicate and convey economic inf ormation. The gathered and settled data should communicate e fficiently with relevant groups outside by the using standard acc ounting statements (in the sense of types, forms and contents).

13. Accounts receivable应收帐款 14. Realized profits实现的利润 15. Financial accounting财务会计 16. Financial position财务状况 17. Operating results经营结果 18. Cash flow现金流量 19. Double entry复式记帐 20. Accounting entity会计主体 21. Going-concern持续经营 22. Accounting period会计期间 23. Accrual system权责发生 24. Cash basis accounting收付实现制

on 会计前提/假设 4. Accounting principles会计原则 5. Accounting elements会计要素 6. Assets资产 7. Liabilities负债 8. Owner’s equity所有者权益 9. Revenue收入 10.Profit利润 11.Expenses费用 12.Entity经营单位、实体单位

13. Accounts receivable应收帐款 14. Realized profits实现的利润 15. Financial accounting财务会计 16. Financial position财务状况 17. Operating results经营结果 18. Cash flow现金流量 19. Double entry复式记帐 20. Accounting entity会计主体 21. Going-concern持续经营 22. Accounting period会计期间 23. Accrual system权责发生 24. Cash basis accounting收付实现制

on 会计前提/假设 4. Accounting principles会计原则 5. Accounting elements会计要素 6. Assets资产 7. Liabilities负债 8. Owner’s equity所有者权益 9. Revenue收入 10.Profit利润 11.Expenses费用 12.Entity经营单位、实体单位

会计英语10

Categories

Defined as debts or obligations arising from past transactions or events. Maturity = 1 year or less Current Liabilities Maturity > 1 year Non-current Liabilities

(2) Bonds

Definition of Bonds

Bonds are a form of interest-bearing notes payable.

Three advantages over common stock:

a) Stockholder control is not affected. b) Tax savings result. c) Earnings per share may be higher.

Composition

Current liabilities include notes payable, accounts payable, unearned revenues, and accrued liabilities such as taxes, salaries and wages, and interest payable.

• Accounting of Interest Payable

Dr. Interest Expense Cr. Interest Payable

(8) Cash dividends Payable • Definition

Cash dividends declared but not yet paid are reported as a current liability. Declared dividends are reported as a liability between the date of declaration and payment--- because declaration gives rise to an enforceable contact.

会计学英文版ppt课件

managers and other users of its financial statements.The

accounts within the chart of accounts are numbered for use

as references.

Balance Sheet Accounts

accounts.

Prepare an unadjusted trial

balance and explain how it can be used to discover errors.

Using Accounts to Record Transactions

As a result,accounting systems are designed to show the increases and decreases in each accounting equation element as a separate record.This record is

accounts.

Describe and illustrate

journalizing transaction using the double-entry

accounting system.

Describe and illustrate the journalizing and

posting of transactions to

Examples ——wages expense, rent expense, utilities expense, supplies expense, and miscellaneous expense.

A chart of accounts should meet the needs of a company’s

accounts within the chart of accounts are numbered for use

as references.

Balance Sheet Accounts

accounts.

Prepare an unadjusted trial

balance and explain how it can be used to discover errors.

Using Accounts to Record Transactions

As a result,accounting systems are designed to show the increases and decreases in each accounting equation element as a separate record.This record is

accounts.

Describe and illustrate

journalizing transaction using the double-entry

accounting system.

Describe and illustrate the journalizing and

posting of transactions to

Examples ——wages expense, rent expense, utilities expense, supplies expense, and miscellaneous expense.

A chart of accounts should meet the needs of a company’s

大学课程《会计英语》PPT课件:Chapter 10 Unit 6

The dollar amount of change from year to year is significant, but expressing the change in percentage terms adds perspective.

Trend Percentages

The changes in financial statement items from a base year to following years are often expressed as trend percentages to show the extent and direction of change. Two steps are necessary to compute trend percentages.

Quickratio Quickassets Currentliabilities

Accounts Receivable Turnover

Accounts receivable turnover indicates reasonableness of accounts receivable balance and effectiveness of collections.

statements analysis. Explain the uses and limitations of dollar and

percentage changes, trend percentages, and component percentages. Compute dollar and percentage changes, trend percentages, and component percentages from a set of comparative financial statements. Identify the widely used ratios. Compute each of them and explain what they may indicate and measure.

Trend Percentages

The changes in financial statement items from a base year to following years are often expressed as trend percentages to show the extent and direction of change. Two steps are necessary to compute trend percentages.

Quickratio Quickassets Currentliabilities

Accounts Receivable Turnover

Accounts receivable turnover indicates reasonableness of accounts receivable balance and effectiveness of collections.

statements analysis. Explain the uses and limitations of dollar and

percentage changes, trend percentages, and component percentages. Compute dollar and percentage changes, trend percentages, and component percentages from a set of comparative financial statements. Identify the widely used ratios. Compute each of them and explain what they may indicate and measure.

财务会计assets-liabilities-and-equityppt课件

Module 2: Business Elements and Transactions

OBJECTIVES

Define assets, liabilities and owners’ equity and understand the relationship of revenues and expenses to owners’ equity

equation; some affect both sides.

精品课件

Double-Entry Accounting

Double entry bookkeeping means to record the dual effects of each business transaction.

Assets = Liabilities + Ownersቤተ መጻሕፍቲ ባይዱ Equity

精品课件

Affect Owners’ Equity

OWNERS’ EQUITY INCREASES

OWNERS’ EQUITY DECREASES

Owner Investments in the Business

Owner Drawings from the Business

Owners’ Equity

精品课件

Accounting for Business Transactions

What is a transaction? It is any event that both affects the financial

position of the business and can be reliably recorded.

精品课件

Expenses

OBJECTIVES

Define assets, liabilities and owners’ equity and understand the relationship of revenues and expenses to owners’ equity

equation; some affect both sides.

精品课件

Double-Entry Accounting

Double entry bookkeeping means to record the dual effects of each business transaction.

Assets = Liabilities + Ownersቤተ መጻሕፍቲ ባይዱ Equity

精品课件

Affect Owners’ Equity

OWNERS’ EQUITY INCREASES

OWNERS’ EQUITY DECREASES

Owner Investments in the Business

Owner Drawings from the Business

Owners’ Equity

精品课件

Accounting for Business Transactions

What is a transaction? It is any event that both affects the financial

position of the business and can be reliably recorded.

精品课件

Expenses

会计英语财务会计(ppt版)

executives 高级(gāojí)管理人员

professional judgment

职业判断力

第六页,共八十四页。

ethical standard 道德(dàodé)准那么

integrity 整合性

AICPA

美国(měi ɡuó)注册会计师 协会

第七页,共八十四页。

Chapter 2

第四十六页,共八十四页。

weight average

加权平均

(píngjūn)

第四十七页,共八十四页。

Chapter 7

第四十八页,共八十四页。

accumulated depletion

累计折耗(shéhào)

accumulated depreciation

累计折旧

acquisition cost 取得(qǔdé)本钱

第二十九页,共八十四页。

bad debt recovery 已确认(quèrèn)坏账的收

回

bed debt expense 坏账费用

bank charges 银行(yínháng)手续费

bank credit memorandum

银行贷项通知

第三十页,共八十四页。

bank debit memorandum

closing the accounts

结账

(jié zhànɡ)

closing entry 结账分录

credit balance 贷方余额

第十八页,共八十四页。

debit balance 借方余额

depreciation expense 折旧费用

double-entry accounting

第二十七页,共八十四页。

会计英语课件:Liabilities

▪ Interest—the cost of borrowing— accrues with the passage of time.

▪ When companies enter into long-term financing agreements, they may become committed to paying large amounts of interest for many years to come. At any balance sheet date, however, only a small portion of this total interest obligation represents a “liability”.

2

n/a = 466.7 + (466.7) n/a - 466.7 = (466.7) n/a

Assets Cash (1)9 300 Bal. 9 300

=

Liabilities

+

Equity

Notes Payable

Interest Expense

(1)10 000

(2)466.7

Bal. 10 000

▪ Amounts owed to someone else which are payable after one year. Examples include:

▪ (1) Long term loans;

▪ (2) Debentures, which are long term loans secured on the business assets. This means if the business fails to repay back the loan on time the business assets are at risk.

会计英语—基础会计PPT课件

• entry • 会计分录

• general journal • 普通日记账

• journalizing • 记日记账

第20页/共38页

• ledger • 分类账

• posting • 过账

• special journals • 特种日记账

• source document • 原始凭证

第21页/共38页

• accounting period • 会计分期

• cash-basis • 现金收付制

• accrual-basis • 权责发生制(应计制)

第8页/共38页

• cost principle • 成本原则

• realization principle • 实现原则

• matching principle • 配比原则

• adjusted trial balance • 调整后试算平衡

• contra-asset account • 备抵账户

第24页/共38页

• closing entries • 结账分录

• capital stock • 股本

• depreciation expense • 折旧费用

• post-closing trial balance • 结账后试算平衡

• objective principle • 客观性原则

第9页/共38页

• consistency principle • 一致性原则

• full disclosure • 充分反映

• materiality • 重要性

• conservatism • 稳健性

第10页/共38页

Chapter 3

• subsidiary ledgers • 明细分类账

• general journal • 普通日记账

• journalizing • 记日记账

第20页/共38页

• ledger • 分类账

• posting • 过账

• special journals • 特种日记账

• source document • 原始凭证

第21页/共38页

• accounting period • 会计分期

• cash-basis • 现金收付制

• accrual-basis • 权责发生制(应计制)

第8页/共38页

• cost principle • 成本原则

• realization principle • 实现原则

• matching principle • 配比原则

• adjusted trial balance • 调整后试算平衡

• contra-asset account • 备抵账户

第24页/共38页

• closing entries • 结账分录

• capital stock • 股本

• depreciation expense • 折旧费用

• post-closing trial balance • 结账后试算平衡

• objective principle • 客观性原则

第9页/共38页

• consistency principle • 一致性原则

• full disclosure • 充分反映

• materiality • 重要性

• conservatism • 稳健性

第10页/共38页

Chapter 3

• subsidiary ledgers • 明细分类账

会计英语PPT(完成版) Chapter 1- An Overview of Accounting

Accounting is the process of analyzing, classifying, summarizing, and interpreting business transactions in financial or monetary terms.

5

of

12

A Brief History of Accounting

International Accounting Standards (IAS) (now called International Financial Reporting Standards—IFRS)

7

of

12

3

The Reform of China’s Accounting System

In 1957,own accounting system was established. It was mostly copied from the former USSR and failed to take into account the actual conditions of our country. In 1985, the first Accounting Law of our country was promulgated. Serve its open-door policy and the modernization. In 1993, Accounting Standards for Business Enterprises and General Financial Rules for Business Enterprises— were finally enacted and came into effect.

MBA教材课件英文版 会计 CHAP10 Liabilities

Slide 10-1

Liabilities

Chapter 10

Slide 10-2

The Nature of Liabilities

Defined as debts or obligations arising from past transactions or

events.

Maturity = 1 year or less

Maturity > 1 year

Current Liabilities

Noncurrent Liabilities

I.O.U.

Slide

10-3 Distinction Between Debt and

Equity

The acquisition of assets is financed from two sources:

and has an annual interest rate of 8%.

Is this a current liability or a noncurrent liability?

Slide

10-5

Liabilities

Question

Devon Mfg. borrows $100,000 from First Bank. The loan will be repaid in 20 years

As the earnings process is

completed . . .

Cash is received

in advance.

Deferred revenue is recorded.

Earned revenue is recorded.

Slide 10-21

Liabilities

Chapter 10

Slide 10-2

The Nature of Liabilities

Defined as debts or obligations arising from past transactions or

events.

Maturity = 1 year or less

Maturity > 1 year

Current Liabilities

Noncurrent Liabilities

I.O.U.

Slide

10-3 Distinction Between Debt and

Equity

The acquisition of assets is financed from two sources:

and has an annual interest rate of 8%.

Is this a current liability or a noncurrent liability?

Slide

10-5

Liabilities

Question

Devon Mfg. borrows $100,000 from First Bank. The loan will be repaid in 20 years

As the earnings process is

completed . . .

Cash is received

in advance.

Deferred revenue is recorded.

Earned revenue is recorded.

Slide 10-21

会计学(第21版)课件:Current Liabilities

20 000 00 20 000 00

Contingent Liabilities

Product Liability

On June 30, a company sells a product for $60,000 on which there is a 36-month warranty. Past

experience indicates that repairs of defects cost 5% of the sales price over the warranty period.

June 30 Product Warranty Expense Product Warranty Liability Warranty expenses projected for June, 5% of $60,000.

The Nature of Current Liabilities

Liabilities that are to be paid out of current assets and are due within a short time, usually within one year,

are called current liabilities.

Record Liability

Disclose Liability

Disclose Liability

Payroll and Payroll Taxes

Liability for Employee Earnings

Payroll is the amount paid to employees for services provided. Payrolls are important because--

相关主题

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

A term loan is a monetary loan that is repaid in regular payments over a set period of time. The lender is usually a bank or an insurance company. A term loan usually involves an unfixed interest rate that will add additional balance to be repaid.

2

of

10

1

Current Liabilities

Current liabilities are those that are due or payable within one year or current operation cycle, whichever is longer. For instance, accounts payable, notes payable, taxes payable, accrued expenses, deferred revenues, and current portions of long-term debts are all current liabilities.

Accounts payable are money owed by a business to its suppliers shown as a liability on a company’s balance sheet.

Accounts payable mainly refer to trade payables, payables for the purchase of physical goods that are recorded in inventory.

4

of

10

Accrued expenses are expenses to be paid for goods or services received in a period but have not yet been invoiced for by the suppliers.

A deferred revenue (also called unearned revenue) is money that is received before the entity delivers goods or provides services. A current portion of long-term debt represents the part of a noncurrent liability that is due within the next twelve months. That amount is considered a current liability.

6

of

10

For a company, bonds are a more significant source of noncurrent liabilities. A bond is a form of interest-bearing note payable, representing money that a corporation borrows from the investing public.

Notes payable are often used instead of accounts payable because they give the lender formal proof of the obligation.

Taxes payable represent the amounts the entity owes to the government for taxes. Taxation usually sets rules for an entity different from financial accounting rules.

Chapter 10. Liabilities

1 Current Liabilities 2

Noncurrent Liabilities

1

of

10

Liabilities

Liabilities are the existing obligations of an enterprise as a result of past transactions or other past events which will sacrifice future economic benefits of the enterprise. Examples of liabilities are amounts owed to a supplier for goods bought on credit, amounts owed to a lender, tax payable and so on. Some liabilities are due to be repaid fairly quickly. Other liabilities may take some years to repay. Thus, liabilities can be classified as current liabilities and noncurrent liabilities.urrent Liabilities

2

Debts that do not meet the criteria for being classified as current liabilities are called noncurrent liabilites or long-term liabilities.

3

of

10

Accounts payable and Notes payable There is a distinction between accounts payable and notes payable, which are debts owed to financial institutions such as a bank and created by formal legal instrument documents.