财务成本管理英语

财务管理英语词汇

financial management 财务管理chief financial officer 首席财务官hurdle rate 最低报酬率capital structure 资本结构cash dividend 现金股利dividend-payout ratio 股利支付率financial risk 财务风险earnings per share 每股盈余net present value 净现值stock option 股票期权earnings per share 每股收益time value of money 货币时间价值simple interest 单利annuity 年金future value 终值present value 现值compound interest 复利capital 本金d iscount rate 折现率opportunity cost 机会成本cost of capital 资本成本ordinary annuity 普通年金annuity due 先付年金deferred annuity 递延年金perpetuity 永续年金liquidity ratio 流动性比率nominal interest rate 名义利率marker value 市场价值intrinsic value 内在价值discounted cash flow valuation 折现现金流量模型earnings before interest and taxes 息税前利润par value 票面价值dividend payout 股利支付率dividend discount model 股利折现模型diversifiable risk可分散风险market risk 市场风险expected return 期望收益volatility 流动性权益融资equity financial债务融资debt financial利润最大化profit maximization股东财富最大化shareholders wealth maximization 每股收益最大化maximization of earning per share 11、投资报酬return on investment风险溢价risk premium货币市场money market偿债基金sinking fund1.financial markets 金融市场2.资本结构capital structure3.risk premium 风险报酬4.净现金流量net cash flow5.credit policy 信用政策6.终值future value7.moral hazard 道德风险8.收账政策collection policy1.chief financial officer 首席财务官2.财务管理financial management3.credit standard 信用标准4.流动性liquidity5.earnings before interest and taxes 息税前利润6.市场价值market value7.capital assets pricing model资本资产定价模型8.每股收益earnings per share。

财经英语单词--财务成本管理

PART I Fundamentals to Financial Management第一部分财务管理导论Section I Fundamentals to Financial Management第一节财务管理概述1.profit maximization*利润最大化1-1 EPS maximization* 每股收益最大化【讲解】EPS, earnings per share 每股收益1-2 Maximization of shareholders wealth* 股东财富最大化e.g. Shareholder wealth maximization is a fundamental principle of financial management. In financial management we assume that the objective of the business is to maximize shareholder wealth. This is not necessarily the same as maximizing profit.【讲解】(1)maximization[,mæksimai'zeiʃən]n.最大化,极大化(2)minimization [,minimai'zeiʃən, -mi'z-]n.最小化(3)maximize['mæksɪmaɪz]v. 最大化,取……最大值,达到最大值(4)minimize ['mɪnɪmaɪz] v. 最小化(5)minimum n.最小值,最小量 adj.最小的,最低的(6)maximum n. 极大,最大限度,最大量 adj.最高的,最多的(7)the same as 和……一样,与……相同学习成果回顾【译】股东财富最大化是财务管理的基本原则。

在财务管理中我们假定企业的目标就是实现股东财富最大化。

中英文对照,专业名词,财务成本管理

中英文对照,专业名词,财务成本管理第一部分财务治理导论Section I Fundamentals to Financial Management第一节财务治理概述1.profit maximization*利润最大化1-1 EPS maximization* 每股收益最大化【讲解】EPS, earnings per share 每股收益1-2 Maximization of shareholders wealth* 股东财宝最大化e.g. Shareholder wealth maximization is a fundamental principle of fi nancial management. In financial management we assume that the objectiv e of the business is to maximize shareholder wealth. This is not necessari ly the same as maximizing profit.【讲解】(1)maximization [,mæksimai'zeiʃən] n.最大化,极大化(2)minimization [,minimai'zeiʃən, -mi'z-] n.最小化(3)maximize ['mæksɪmaɪz] v. 最大化,取……最大值,达到最大值(4)minimize ['mɪnɪmaɪz] v. 最小化(5)minimum n.最小值,最小量adj.最小的,最低的(6)maximum n. 极大,最大限度,最大量adj.最高的,最多的(7)the same as 和……一样,与……相同学习成果回忆【译】股东财宝最大化是财务治理的差不多原则。

在财务治理中我们假定企业的目标确实是实现股东财宝最大化。

中英文对照,专业名词,财务成本管理(完整版)

PART I Fundamentals to Financial Management第一部分财务管理导论Section I Fundamentals to Financial Management第一节财务管理概述1.profit maximization*利润最大化1-1 EPS maximization* 每股收益最大化【讲解】EPS, earnings per share 每股收益1-2 Maximization of shareholders wealth* 股东财富最大化e.g. Shareholder wealth maximization is a fundamental principle of financial management. In financial management we assume that the objective of the business is to maximize shareholder wealth. This is not necessarily the same as maximizing profit.【讲解】(1)maximization[,mæksimai'zeiʃən]n.最大化,极大化(2)minimization [,minimai'zeiʃən, -mi'z-]n.最小化(3)maximize['mæksɪmaɪz]v. 最大化,取……最大值,达到最大值(4)minimize ['mɪnɪmaɪz] v. 最小化(5)minimum n.最小值,最小量 adj.最小的,最低的(6)maximum n. 极大,最大限度,最大量 adj.最高的,最多的(7)the same as 和……一样,与……相同学习成果回顾【译】股东财富最大化是财务管理的基本原则。

在财务管理中我们假定企业的目标就是实现股东财富最大化。

财务成本管理英语08

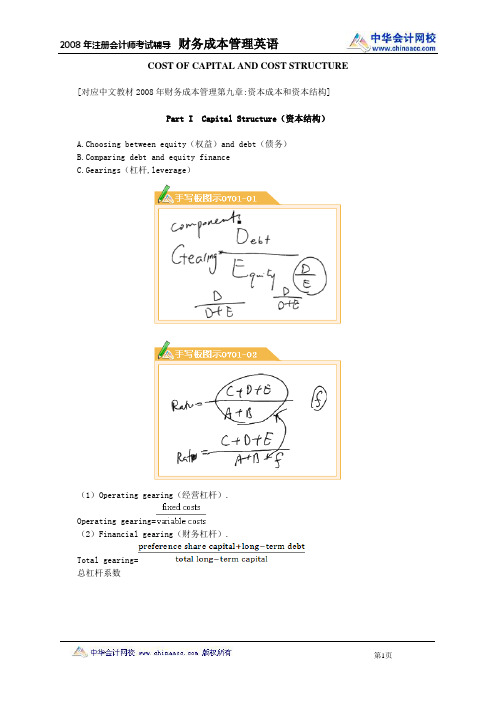

COST OF CAPITAL AND COST STRUCTURE [对应中文教材2008年财务成本管理第九章:资本成本和资本结构]Part I Capital Structure(资本结构)A.Choosing between equity(权益)and debt(债务)paring debt and equity financeC.Gearings(杠杆,leverage)(1)Operating gearing(经营杠杆).Operating gearing=(2)Financial gearing(财务杠杆).Total gearing=总杠杆系数Equity gearing=Income gearing=收入杠杆系数Here debt interest includes preference dividend.(利息金额包含优先股股利在内)D. Weighted Average Cost of Capital(WACC)(加权平均资本成本)Part II Cost of Capital(资本成本)1.The cost of equity, the cost of debt and the weighted average cost of capital1.1 The concept of a weighted average cost of capitalCost of equityCost of debtIrredeemableRedeemable K is the IRR of the related flows: initial market value, annual interestfinal redemption.1.2 Market or book weights(市值或账面价值)ExampleThe accounts of Apollo plc reveal(揭示)the following capital structure: Ordinary shares 2,000,000Reserves 3,000,00010% debentures 1,000,0006,000,000Market values of the above are as follows:Ordinary shares 3.75 each ex div(除权)Debenture stock 80The cost of equity is estimated to be 20%, the cost of debt is 7.5%(after tax).What is the weighted average cost of capital using book weights?SolutionEquity(ordinary shares+reserves)2000000+3000000 5000000Debt 1000000Total 6000000Proportions 5/6 Equity 1/6 DebtCombined cost of capital(5/6 x 20%)+(1/6 x 7.5%)= 17.92%3.Operating gearing(经营杠杆)Operating gearing(also called operational gearing)measures the cost structure(fixed and variable)of the firm. Firms with high levels of fixed costs are usually described as having high operating gearing.经营杠杆度量的是公司的成本结构,即固定成本和变动成本之间的关系.固定成本占比较大的公司称之为经营杠杆系数较高.Firms with high operating gearing are risky as fixed cost payments must be made no matter the level of contribution.具有较高经营杠杆系数的公司风险较大,原因在于无论边际贡献如何,均须承担相关固定成本.ExampleConsider two firms:Firm A Firm Bm mSales 5 5Variable costs 3 1Fixed costs 1 3EBIT(Earnings before interest and tax)1 1What would be the impact(影响)of a 10% increase in sales volume on the EBIT of each firm?Firm A New EBIT=(5m-3m)×1.1-1=1.2m i.e. a 20% increase.Firm B New EBIT=(5m-1m)×1.1-3=1.4m i.e. a 40% increase.Operating gearingFirmA FirmBAlternatively:FirmA FirmBB carries a higher operating gearing because it has higher fixed costs. Its operating earnings are more volume sensitive.公司B具有较高的经营杠杆系数,因为其固定成本占比较高.它的经营收入具有数量敏感性.Part III Further Aspects of WACC(加权平均成本的进一步探究)3 CAPM and the cost of capital3.1 Modigliani and Miller 1963In a world with corporation tax the benefit to the general company of the tax shield on debt interest must be included in our analysis. Thus:Assuming debt is risk free and that β debt is therefore zero:=0假定债务无风险,故βdebtDiscount rates for capital investment appraisal should be related to the systematic risk of the project in question. In a similar way it could also be argued that they ought also to be related to the gearing level of the project.资本投资评价使用的折现率应反映该项目的系统风险.同样地其也应反映该项目的杠杆水平.ExampleHubbard, an all equity(融资方式为权益资金))food manufacturing firm, is about to embark (转型)upon a major diversification in the consumer electronics industry(电子行业). Its current equity beta is 1.2, whilst the average equity βof electronics firms is 1.6. Gearing in the electronics industry averages 30% debt, 70% equity. Corporate debt is considered to be risk free.R m =25%, Rf=10%, corporation tax rate=30%(notation as before).Required:What would be a suitable discount rate for the new investment if Hubbard were to finance the new project in each of the following ways?问:若该公司采用下述融资结构以支持此新项目,则合适的折现率是多少?(a)Entirely by equity(b)By 30% debt and 70% equity(c)By 40% debt and 60% equity?SolutionIn all three situations the best approach is to treat the project as a 'mini-firm' and tailor(调整,修改)the discount rate to reflect its level of systematic business risk and financial risk(财务风险).(a)Project financed entirely by equityTo reflect the business risk of the new venture we should start with the equity ,βof the electronics industry, i.e. 1.6.As our project is to be ungeared we should then remove the financial risk element.The pure cost of equity(and hence WACC in the all equity ease)would then be:The project should be evaluated at a rate of 28.45%.(b)Project financed by 30% debt, 70% equityIn this case the observed equity beta of the electronics industry would reflect the level of business risk and financial risk of the project. No adjustments are therefore required.在此情况下电子行业的β系数反应了该项目的商业风险和财务风险.无需进一步调整.To obtain a suitable discount rate we must simply weight the cost of equity and the cost of debt, hence:Suitable discount rate for project=(34%×0.7)+(7%×0.3)=25.9%(c)Project financed by 40% debt and 60% equityIn this case the equity beta of the electronics industry reflects a lower level of gearing than that for the proposed project. The simplest procedure is to take a two step approach to the gearing adjustment.Step 1 Calculate the equity beta for an ungeared electronics company(as in(a)).β=1.23equity ungearedThis is a measure of the pure systematic risk of electronics companies.We now adjust this pure beta in the light of the given financial gearing ratio.Step 2 Work out the equation 'backwards' to calculate the cost of equity for an electronics company with 60% equity and 40% debtThe cost of equity for such a firm would then be:The cost of dcbt would be as before.And suitable discount rate for the project would be:风险调整后净现值(risk adjusted NPV)。

2021 年注册会计师《财务成本管理英语》资本成本与资本结构

第01讲资本成本与资本结构Part 1 核心词汇Part 2 重难点讲解—资本成本(一)普通股成本的估计(二)优先股成本的估计(三)债务成本的估计特殊债券的成本估计(四)加权平均资本成本(WACC)【例题·2017年考题】甲公司为扩大产能,拟平价发行分离型附认股权证债券进行筹资,方案如下:债券每份面值1000元,期限5年,票面利率5%。

每年付息一次。

同时附送20份认股权证。

认股权证在债券发行3年后到期,到期时每份认股权证可按11元的价格购买1股甲公司普通股股票。

甲公司目前有发行在外的普通债券,5年后到期,每份面值1000元,票面利率6%,每年付息一次,每份市价1020元(刚刚支付过最近一期利息)公司目前处于生产的稳定增长期,可持续增长率5%。

普通股每股市价10元。

公司企业所得税率25%。

要求:(1)计算公司普通债券的税前资本成本。

(2)计算分离型附认股权证债券的税前资本成本。

(3)判断筹资方案是否合理,并说明理由,如果不合理,给出调整建议。

『正确答案』(1)令税前资本成本为iAssume Pre-tax cost of capital is i1020=1000×6%×(P/A,i,5)+1000×(P/F,i,5)当i=4%时,等式右边=1000×6%×4.4518+1000×0.8219=1089When i equals 4%, the right side of the equation=1000×6%×4.4518+1000×0.8219=1089 continuing当i=6%时, 等式右边=1000×6%×4.2124+1000×0.7473=1000When i equals 6%, the right side of the equation =1000×6%×4.2124+1000×0.7473=1000 列出等式:Write out the equality :(i-4%)/(6%-4%)=(1020-1089)/(1000-1089)i=4%+[(1020-1089)/(1000-1089)]×(6%-4%)=5.55%(2)第3年末行权支出=11×20=220(元)Exercise expenditure at the end of the third year=11×20=220(yuan )取得股票的市价=10×(F/P,5%,3)×20=231.525(元)The market price of the acquired stock=10×(F/P,5%,3)×20=231.525(yuan )行权现金净流入=231.5325-220=11.525(元)Net cash inflow when option are exercised= 231.5325-220=11.525(yuan )令税前资本成本为k,Assume Pre-tax cost of capital is K1000=1000×5%×(P/A,K,5)+11.525×(P/F,K,3)+1000×(P/F,K,5)K=5%时,等式右边=1000×5%×4.3295+11.525×0.8638+1000×0.7835=1009.93(元)When K equals 5%, the right side of the equation =……K=6%时,等式右边=1000×5%×4.2124+11.525×0.8396+1000×0.7473=967.60(元)When K equals 6%, the right side of the equation =……(K-5%)/(6%-5%)=(1000-1009.93)/(967.60-1009.93)K=5%+[(1000-1009.93)/(967.60-1009.93)]×(6%-5%)=5.23%(3)该筹资方案不合理,原因是附认股权证债券的税前资本成本低于普通债券的税前资本成本。

财务管理专业英语(吐血整理)

Topic1:1、Financial management is an integrated decision-making process concerned with acquiring, financing, and managing assets to accomplish some overall goal within a business entity.财务管理是为了实现一个公司总体目标而进行的涉及到获取、融资和资产管理的综合决策过程。

2、Making financial decisions is an integral part of all forms and sizes of business organizations from small privately-hold forms to large publicly-traded corporations.做财务决策对于所有形式和规模的商业组织,无论是小型私人公司还是大型公开上市公司,都是不可分割的一部分。

3、In today’s rapidly changing environment, the financ ial manager must have the flexibility to adapt to external factors such as economic uncertainty, global competition, technological change, volatility of interest and exchange rates, changes in laws and regulations, and ethical concerns.在当今瞬息万变的环境中,财务经理必须具备足够的灵活性以适应外部因素,如经济的不确定性、国际竞争、技术变革、利息波动、汇率变动、法律法规变化以及商业道德问题。

财务成本管理英语

INVESTMENT APPRAISAL[对应中文教材2008年财务成本管理第五章:投资管理](已动用资本回报率)or ARR(会计收益率)(Accounting Rate of Return)(回收期法)Payback period=Initial payment/Annual cash inflow, payback is not always an exact number of years Most common formula:ROCE=EBIT (after depreciation)/ initial capital costsC NPV(净现值法)(1) Basic assumptions:·cash outlay occurs in year 0 (now).·cash flows occur at the end of the year.·if a cash flow occurs at the beginning of a year, it is assumed to occur at the end of the previous year.D IRR(内含报酬率法)(1)Basic principle: IRR is the cost of capital at which the NPV is zero, if the expected IRR is higher than a target rate of return; the project is financially worth undertaking.(2)Selection between IRR and NPV: when a choice has to be made between mutually exclusive projects, in such case the NPV should be selected, because higher NPV can maximize shareholder’s wealth.DefinitionThe discount rat which, when applied to the cash flows of a project, gives an NPV of zero.OrThe break-even interest rate for a project.It is the maximum rate of interest that you could afford to pay on a project without making a loss.FeaturesAdvantages -Takes into account the time value of money-Relative measure-More readily understood than NPVDisadvantages -May not be unique – projects can have more than one IRR- May rank projects incorrectly – for mutually exclusive projects or whenFunds are short supply- Cannot cope with changing rates of interestThe method of calculation depends upon whether or not the project has even cash flows.Even cash flowsConsider an investment of £ that generates net cash earnings of £10m for 5 years The IRR is the discount rate that gives a NPV of zero. This means that the IRR is the Rate that will discount five installments of £10m to a present value of £. This in turnMeans that the IRR is the discount rate for which the 5year annuity factor is . A The project’s IRR has been found via a cumulative discount fac tor (annuity factor)givenBy:Annuity factorat the IRR=for the life of the projectUneven cash flowsThese have to be found by trial and error or by estimating using two present values.Where:A=lower rate chosen=NPV at rate AB=higher rate=NPV at rate BIt helps to get A and B as close to the true IRR as possible, but it doesn’t matter whetherthe resultant NPVs are positive, negative or one of each.Some students prefer to use a common sense approach rather than a formula. Seeing by nowMuch NPV has fallen (from to) as the discount rate has risen from A to B, They find how much more the discount rate needs to rise to bring the NPV to zero.Whether the formula is used or common sense, the calculation assumes a linear relationshipBetween NPV and discount rate. In fact the relationship is not linear, hence the calculationIs only approximate and (unless you have been lucky when guessing which discount rates touse)you should not quote IRR’s calculated in this way to many, not to any,decimal places –unless the examiner asks you.IRR of a perpetuityThe present value of a perpetuity is the annual cash flow divided by the discount rate (expressed as a decimal. From this it follows that:the IRR of a perpetuity ==100Perpetuity: 永续年金Method of presentationA simple calculation such as those for Woods can be done on a single line. For larger projectstwo possibilities exist:(i) the cash budget approach(ii) the tabular approach.(1)Cash budget approachTime 0 1 2 3£’000£’000£’000£’000Investment (X)—— XAdvertising (X)(X) - -Working capital (X)- - XMaterials (X)(X)(X)-Labour —(X)(X)(X)Overheads —(X)(X)(X)Revenue ———X————Net cash flow (X)(X)(X) X————y% Discount factor 1 X X XPresent value (X)(X)(X)XNet present value (£’000)XThe cash budget approach is suitable for short projects with lots of different cash flowsWhich change from year to year.(2) Tabular approachTime Cash flow y% Discount Present value£’000£’000£’0000 Investment (X) 1 (X)0 and 1 Advertising (X)X (X)0 Working capital (X) 1 (X)0-9 Materials (X) 1 (X)1-10 Labour and overheads (X)X (X)1-10 Revenue X X X10 Sales proceeds X X X10 WC recovery X X X—Net present value (£’000)XThe tabular approach is suitable for long projects with lots of different cash flows that areThe same from year to year (enabling annuity factors to be used).Picking the right figuresWhen carrying out discounted cash flow analysis it is important to select the right figures.Ignore:costs – amounts that have already been spent– not a cash flowvalues – not a cash flow–incremental fixed costs (look out for the words “reapportioned fixed overheads”) costs – taken into account by the discounting processInclude:Those cash flows that are specifically received or incurred as a result of the acceptance of the project(future–incremental–cash flows).Asset replacement decisionFactors to be considered when making replacement decision are as follows:·capital cost of new equipment;·operating costs, increased repair and maintenance costs;loss of productivity;lower of quality and quantity of output;One application of discounted cash flow is to make decisions concerned with the replacement ofMachinery. This applies to short – life assets that will need to be replaced in perpetuity (. motorCars or photocopiers). As a machine gets older, it is likely to cost more to keep it running and itsScrap value will decrease. The aim is to find the optimal replacement cycle for the machine,. how often it should be replaced - before it becomes uneconomic to own.A simple approach would involve finding the total cost of keeping an asset for 1,2,3 years, etc,Then finding an average annual cost.DCF VersionNow, each possible replacement cycle is treated as a project (1-year, 2-year, or 3-year project).You calculate the NPV of each project (rather than just the total cost).Instead of dividing the NPV’s by 1,2,or 3, they’re divided by the 1,2, or 3-year annuity factorTo find an equivalent annual cost.Equivalent annual cost =。

财务成本管理英语12

Activity Based Costing (ABC)[对应中文教材2008年财务成本管理第十六章:作业成本计算与管理]1 Activity based costingAn alternative to absorption costing is activity based costing (ABC).ABC involves the identification of the factors (cost drivers)which cause the costs of an organization’s major activities.Support overheads are charged to products on the basis of their usage of an activity.For costs that vary with production level in the short term, the cost driver will be volume related (labor or machine hours).Overheads that vary with some other activity (and not volume of production)should be traced to products using transaction-based cost drivers such as production runs or number of orders received.1.1 Reasons for the development of ABCThe traditional cost accumulation system of absorption costing was developed in a time when most organizations produced only a narrow range of products(so that products underwent similar operations and consumed similar proportions of overheads).And overhead costs were only a very small fraction of total costs, direct labor and direct material costs accounting for the largest proportion of the costs.The benefits of more accurate systems for overhead allocation would probably have been relatively small.In addition, information processing costs were high.In recent years, however, there has been a dramatic fall in the costs of processing information.And, with the advent of advanced manufacturing technology (AMT),overheads are likely to be far more important and in fact direct labor may account for as little as 5% of a product’s cost.It therefore now appears difficult to justify the use of direct labor or direct material as the basis for absorbing overheads or to believe that errors made in attributing overheads will not be significant.Many resources are used in non-volume related support activities,(which have increased due to AMT)such as setting-up, production scheduling, inspection and data processing.These support activities assist the efficient manufacture of a wide range of products and are not, in general, affected by changes in production volume.They tend to vary in the long term according to the range and complexity of the products manufactured rather than the volume of output.The wider the range and the more complex the products, the more support services will be required. Consider, for example, factory X which produces 10,000 units of one product, the Alpha, and factory Y which produces 1000 units each of ten slightly different versions of the Alpha. Support activity costs in the factory Y are likely to be a lot higher than in factory X but the factories produce an identical number ofunits. For example, factor X will only need to set-up once whereas Factory Y will have to set-up the production run at least ten times for the ten different products. Factory Y will therefore incur more set-up costs for the same volume of production.Traditional costing systems, which assume that all products consume all resources in proportion to their production volumes, tend to allocate too great a proportion of overheads to high volume products (which cause relatively little diversity and hence use fewer support services)and too small a proportion of overheads to low volume products (which cause greater diversity and therefore use more support services). Activity based costing (ABC)attempts to overcome this problem.1.2 Definition of ABCThe major ideas behind activity based costing are as follows.(a)Activities cause costs. Activities include ordering, materials handling, machining, assembly, production scheduling and dispatching.(b)Producing products creates demand for the activities.(c)Costs are assigned to a product on the basis of the product's consumption of the activities.1.3 Outline an ABC systemAn ABC system operates as follows.Step 1 Identify an organization’s major activities.Step 2Identify the factors which determine the size of the costs of an activity/cause the costs of anLook at the following examples.Step 3 Collect the costs associated with each cost driver into what are known as cost pools.Step 4 Charge costs to products on the basis of their usage of the activity. A product's usage of an activity is measured by the number of the activity's cost driver it generates.2 Absorption costing versus ABCThe following example illustrates the point that traditional cost accounting techniques result in a misleading and inequitable division of costs between low-volume and high-volume products, and that ABC can provide a more meaningful allocation of costs.2.1 Example: Activity based costingSuppose that Cooplan manufactures four products, W, X, Y and Z. Output and cost data for the period justEnded are as follows.Number ofProductionruns in the Material cost Direct labour Machine Output units period per unit hours per unit hours per unit$W102201 1X1028O3 3Y1005201 1Z1005803 314Direct labour cost per hour$5Overhead costs$Short run variable costs3,080Set-up costs 10,920Expediting and scheduling costs9,100Materials handling costs7,70030,800 RequiredPrepare unit costs for each product using conventional costing and ABC.[答疑编号810110101]SolutionUsing a conventional absorption costing approach and an absorption rate for overheads based on either direct labour hours or machine hours, the product costs would be as follows.W X Y Z Total$ $$ $$ Direct material2008002,0008,000Direct labour501505001,500Overheads*7002,1007,00021,0009503,0509.50030,50044,000 Units produced1010100100Cost per unit$95$305$95$305* $30,800 ÷ 440 hours = $70 per direct labour or machine hour.Using activity based costing and assuming that the number of production runs is the cost driver for set-up costs, expediting([5ekspidait]v加速, 派出)and scheduling costs and materials handling costs and that machine hours are the cost drivers for short-run variable costs, unit costs would be as follows.W X Y ZTotal$ $$$$Direct material2008002,0008,000Direct labour 501505001,500Short-run variable overheads (W1)70210700 2,100Set-up costs (W2)1,5601,5603,9003,900Expediting, scheduling costs (W3)1,3001,3003,2503,250Materials handling costs (W4)1,1 O01,1 O0 2,750 2,7504,2805,12013,10021,50044,0O0Units produced1010100100Cost per unit$428$512$131$215Workings1. $3,080 ÷ 440 machine hours =$7 per machine hour2. $10,920 ÷ 14 production runs = $780 per run3. $9,100 ÷ 14 production runs =$650 per run4. $7,700 ÷ 14 production runs =$550 per runSummaryConventional costing ABC Difference per Difference in Product unit cost unit cost unit total$$$ $ W95428 + 333+3,330 X305512+ 207+2,070 Y95131+ 36+3,600 Z305215- 90-9,000The figures suggest that the traditional volume-based absorption costing system is flawed.A. It under-allocates overheads costs to low-volume products (here, W and X)and over-allocates overheads to higher-volume products (here Z in particular).B. It under-allocates overheads costs to smaller-sized products (here W and Y with just one hour of work needed per unit)and over-allocates overheads to larger products (here X and particularly Z).2.2 ABC versus traditional costing methodsBoth traditional absorption costing and ABC systems adopt the two stage allocation process.2.2.1 Allocation of overheadsABC establishes separate cost pools for support activities such as despatching. As the costs of these activities are assigned directly to products through cost driver rates, reapportionment of service department costs is avoided.2.2.2 Absorption of overheadsThe principal difference between the two systems is the way in which overheads are absorbed into products.(a)Absorption costing most commonly uses two absorption bases (labour hours and/or machine hours)to charge overheads to products.(b)ABC uses many cost drivers as absorption bases (e.g. number of orders or despatches). Absorption rates under ABC should therefore be more closely linked to the causes of overhead costs.2.3 Cost driversThe principal idea of ABC is to focus attention on what causes costs to increase, is the cost drivers.(a)The costs that vary with production volume, such as power costs, should be traced to products using production volume-related cost drivers, such as direct labour hours or direct machine hours.Overheads which do not vary with output but with some other activity should be traced to products using transaction-based cost drivers, such as number of production runs and number of orders received.(b)Traditional costing systems allow overheads to be related to products in rather more arbitrary ways producing, it is claimed, less accurate product costs.Question: Traditional costing versus ABCA company manufactures two products, L and M, using the same equipment and similar processes. An extract of the production data for these products in one period is shown below.L MQuantity produced (units)5,0007,000Direct labour hours per unit1 2Machine hours per unit3 1Set-ups in the period 1040Orders handled in the period1560Overhead costs$Relating to machine activity220,000Relating to production run set-ups20,000Relating to handling of orders45,000 285,000RequiredCalculate the production overheads to be absorbed by one unit of each of the products using the following costing methods.(a)A traditional costing approach using a direct labour hour rate to absorb overheads(b)An activity based costing approach, using suitable cost drivers to trace overheads to products [答疑编号810110102]Solution:(a)Traditional costing approachDirect labourhours Product L = 5,000 units × 1 hour5,000Product M = 7,000 units × 2 hours14,00019,000 ∴Overhead absorption rate= $285,00019,000= $15 per hourOverhead absorbed would be as follows.Product L 1 hour x $15 = $15 per unitProduct M 2 hours x $15 = $30 per unit(b)ABC approachMachine hoursProduct L= 5,000 units× 3 hours15.000Product M = 7,000 units × 1 hour7,00022,000 Using ABC the overhead costs are absorbed according to the cost drivers.$Machine-hour driven costs 220,000 ÷ 22,000 m/c hours = $10 per m/c hourSet-up driven costs20,000 ÷50 set-ups = $400 per set-upOrder driven costs45,000 ÷75 orders= $600 per orderOverhead costs are therefore as follows.Product L Product M$$ Machine-driven costs (15,000 hrs x $10)150,000 (7,000 hrs x $10)70,000Set-up costs (10 x $400)4,000 (40 x $400)16,000Order handling costs (15 x $600)9,000 (60 x $600)36,000163,000122,000 Units produced5,000 7,000Overhead cost per unit$32.60$17.43These figures suggest that product M absorbs an unrealistic amount of overhead using a direct labour hour basis. Overhead absorption should be based on the activities which drive the costs, in this casemachine hours, the number of production run set-ups and the number of orders handled for each product.3 Merits and criticisms of ABCABC has both advantages and disadvantages, and tends to be more widely used by larger organizations and the service sector.As you will have discovered when you attempted the question above, there is nothing difficult about ABC. Once the necessary information has been obtained it is similar to traditional absorption costing. This simplicity is part of its appeal. Further merits of ABC are as follows.A. The complexity of manufacturing has increased, with wider product ranges, shorter product life cycles and more complex production processes. ABC recognizes this complexity with its multiple cost drivers.B. In a more competitive environment, companies must be able to assess product profitability realistically. ABC facilitates a good understanding of what drives overhead costs.C. In modern manufacturing systems, overhead functions include a lot of non-factory-floor activities such as product design, quality control, production planning and customer services. ABC is concerned with all: overhead costs and so it takes management accounting beyond its 'traditional' factory floor boundaries.3.1 Criticisms of ABCIt has been suggested by critics that activity based costing has some serious flaws.A. Some measure of (arbitrary)cost apportionment may still be required at the cost pooling stage for items like rent, rates and building depreciation.B. Can a single cost driver explain the cost behavior of all items in its associated pool?C. Unless costs are caused by an activity that is measurable in quantitative terms and which can be related to production output, cost drivers will not be usable. What drives the cost of the annual external audit, for example?D. ABC is sometimes introduced because it is fashionable, not because it will be used by management to provide meaningful product costs or extra information. If management is not going to use ABC information, an absorption costing system may be simpler to operate.E. The cost of implementing and maintaining an ABC system can exceed the benefits of improved accuracy.F. Implementing ABC is often problematic.4 Implications of switching to ABC4.1 PricingAn ABC system gives management a good understanding of the cost structures of making and selling a wide range of products. Switching to ABC can change cost per unit calculations substantially. If an organization determines prices based on cost is using cost-plus pricing, greater costing information will be very useful and prices will change.Many organizations however price their products according to what the market will bear, so if costs are re-calculated, it is the profit margin for a product that will change rather than its price.Consider a business that produces a large volume standard product and a number of variants which are more refined versions of the basic product and sell in low volumes at a higher price. Such companies are common in practice in the modern business environment; also, such companies absorb fixed overheads on a conventional basis such as direct labour hours, and price their products by adding a mark up to full cost.In the situation described, the majority of the overheads would be allocated to the standard range, and only a small percentage to the up-market products. The result would be that the profit margin achieved on the standard range would be much lower than that on the up-market range.Thus the traditional costing and pricing system indicates that the firm might be wise to concentrate on its high margin, up-market products and drop its standard range. This is absurd, however. Much of the overhead cost incurred in such an organization is the cost of support activities like production scheduling: the more different varieties of product there are, the higher the level of such activities will become. The cost of marketing and distribution also increases disproportionately to the volume of products being made.The bulk of the overheads in such an organization are actually the costs of complexity'. Their arbitrary allocation on the basis of labour hours gives an entirely distorted view of production line profitability; many products that appear to be highly profitable actually make a loss if costs are allocated on the basis of what activities cause them.The problem arises with marginal cost-plus approaches as well as with absorption cost based approaches, particularly in a modern manufacturing environment, where a relatively small proportion of the total cost is variable. The implication in both cases is that conventional costing should be abandoned in favor of ABC.4.2 Sales strategyAs we have seen, the introduction of ABC has implications for the cost per unit, price and profit margin. For example, a product with few set-ups, material movements or inspections will have lower costs under ABC than traditional absorption costing. The organization could decide to reduce the product's selling price but if it is a high volume product, the number of units sold may not increase sufficiently to compensate for the loss in total revenue and contribution.ABC may result in a change in profit margins, with previously high margin products now being seen as less profitable. This can result in increased sales efforts on different products, especially if the sales department is rewarded on the basis of profits.4.3 Performance managementThe information provided by analyzing activities can support performance management provided it isused carefully and with full appreciation of its implications.4.3.1 PlanningBefore an ABC system can be implemented, management must analyze the organization’s activities, determine the extent of their occurrence and establish the relationships between activities,Products/services and their cost.The information database produced from such an exercise can then be used as a basis for forward planning and budgeting. For example, once an organization has set its budgeted production level, the database can be used to determine the number of times that activities will need to be carried out, thereby establishing necessary departmental staffing and machine levels. Financial budgets can then be drawn up by multiplying the budgeted activity levels by cost per activity.This activity-based approach may not produce the final budget figures but it can provide the basis for different possible planning scenarios.4.3.2 ControlThe information database also provides an insight into the way in which costs are structured and incurred in service and support departments. Traditionally it has been difficult to control the costs of such departments because of the lack of relationship between departmental output levels and departmental cost. With ABC, however, it is possible to control or manage the costs by managing the activities which underlie them by monitoring a number of key performance measures.4.4 Decision makingMany of ABC's supporters claim that it can assist with decision making in a number of ways.Provides accurate and reliable cost informationEstablishes a long-run product costProvides data which can be used to evaluate different ways of delivering business.It is therefore particularly suited to the following types of decision.PricingPromoting or discontinuing products or parts of the businessRedesigning products and developing new products or new ways to do business2008年注册会计师考试辅导 财务成本管理英语第11页Note, however, that an ABC cost is not a true cost, it is simply an average cost because some costs such as depreciation are still arbitrarily allocated to products. An ABC cost is therefore not a relevant cost for all decisions.。

cpa《财务成本管理》英语

cpa《财务成本管理》英语Cost Management in CPACost management is an essential aspect of financial management for Certified Public Accountants (CPAs). It involves the planning, monitoring, and control of organizational costs to maximize profitability and achieve strategic objectives. By effectively managing costs, CPAs can help businesses make informed decisions and optimize resource allocation.The first step in cost management is the identification and classification of costs. CPAs must understand the different types of costs incurred by an organization, such as direct costs (related to the production of goods or services) and indirect costs (not directly linked to production). By accurately categorizing costs, CPAs can analyze them and identify areas for potential cost reduction.Once costs have been identified, CPAs can proceed with cost planning. This involves setting targets for future costs and establishing budgets for various departments or projects within an organization. By setting realistic and achievable cost targets, CPAs can guide businesses towards their financial goals. They can also provide recommendations regarding cost reduction methods, such as streamlining processes or negotiating better prices with suppliers.Monitoring costs is another crucial aspect of cost management. CPAs need to continuously track actual costs against the budgeted amounts. This allows them to identify any variances and take corrective actions if necessary. Through detailed analysis, CPAs can uncover the underlying causes of cost variations and implement cost control measures to prevent future deviations.Furthermore, CPAs play a vital role in cost control by implementing effective internal controls and evaluating the efficiency of existing processes. This includes assessing the accuracy of financial records, ensuring compliance with regulations, and identifying potential risks that could impact the financial health of an organization. CPAs can also provide guidance on cost allocation methods, such as the use of activity-based costing, which helps allocate indirect costs based on the activities that drive them.In addition to cost planning, monitoring, and control, CPAs are responsible for cost analysis. This involves examining the cost structure of a business and assessing the profitability of different products or services. By analyzing costs relative to sales revenue, CPAs can identify areas where costs can be reduced or eliminated, leading to improved profitability. They can also conduct cost-volume-profit analysis to determine the breakeven point and evaluate the impact of changes in volume or pricing on the financial performance of a business.Overall, cost management is a fundamental aspect of financial management for CPAs. It encompasses various activities ranging from cost identification and planning to monitoring, control, and analysis. By effectively managing costs, CPAs can contribute to the financial success of an organization, provide valuable insights for decision-making, and help businesses achieve their strategic objectives.。

常见成本管理英语词汇

常见成本管理英语词汇成本管理是企业管理中的重要环节,以下是一些常见的成本管理相关的英语词汇。

1. Cost (成本)- Direct costs(直接成本)- Indirect costs(间接成本)- Fixed costs(固定成本)- Variable costs(变动成本)- Overhead costs(间接费用)- Operating costs(营运成本)2. Budget (预算)- Budget planning(预算编制)- Budget control(预算控制)- Budget variance(预算偏差)- Budget analysis(预算分析)- Budget performance(预算执行情况)3. Cost allocation (成本分摊)- Cost driver(成本驱动因素)- Cost pool(成本池)- Allocation base(分摊基数)- Activity-based costing(活动成本核算)4. Cost accounting (成本会计)- Cost center(成本中心)- Cost object(成本对象)- Job costing(作业成本核算)- Process costing(过程成本核算)- Standard costing(标准成本核算)5. Cost management techniques (成本管理技术)- Value chain analysis(价值链分析)- Cost-volume-profit analysis(成本-销售额-利润分析)- Break-even analysis(盈亏平衡分析)- Target costing(目标成本法)- Activity-based management(活动成本管理)6. Cost reduction (成本降低)- Cost optimization(成本优化)- Cost-saving measures(成本节约措施)- Cost-cutting strategies(成本削减策略)以上是关于常见成本管理的一些英语词汇,希望对您有所帮助。

财务成本管理英语05

WORKING CAPITAL MANAGEMENT[对应中文教材2008年财务成本管理第六章:流动资金管理]Part I Inventory/stock ManagementThe objective of stock management is to ensure sufficient levels of stock to maintain an acceptable level of availability on demand whilst minimizing the associated holding, administrative and stockout costs.1.1 Costs of holding stock(持有存货成本)Holding stock is an expensive business - it has been estimated that the cost of holding stock each year is one-third of its production or purchase cost.Holding costs include:interest on capitalstorage space and equipmentadministration and staff costsleasesOn the other hand, running out of stock (known as a stockout脱销) incurs a cost.Finally, order set-up costs(采购成本) are incurred each time a batch(批) of stock is ordered.Administrative costs and, where production is internal, costs of setting up machinery will be affected in total by the frequency of orders.The two major quantitative problems of determining re-order levels and order quantities are essentially problems of striking the optimum balance between holding costs, stockout costs and order set-up costs.the Economic Order Quantity (EOQ) model1.2 Stock management systemsTwo bin systemThis system utilizes two bins, e.g. A and B. Stock is taken from A until A is empty. An order for a fixed quantity is placed and, in the meantime, stock is used from B. The standard stock for B is the expected demand in the lead time(n.订货到收货时间间隔;n.前置时间)(the time between the order being placed and the stock arriving), plus some 'buffer' stock. When the new order arrives, B is filled up to its standard stock and the rest is placed in A. Stock is then drawn as required from A, and the process is repeated.Single bin systemThe same sort of approach is adopted by some firms for a single bin with a red line within the bin indicating the re-order level.1.3 Just in time (JIT) systemsJIT is a series of manufacturing and supply chain techniques that aim to minimize stock levels and improve customer service by manufacturing not only at the exact time customers require, but also in the exact quantities they need and at competitive prices.JIT extends much further than a concentration on stock levels. It centres around the elimination of waste. Waste is defined as any activity performed within a manufacturing company which does not add value to the product. Examples of waste are: raw material stockwork-in-progress stockfinished goods stockmaterials handlingquality problems (rejects and reworks etc)queues and delays on the shop-floorlong raw material lead-timeslong customer lead-timesunnecessary clerical and accounting proceduresJIT attempts to eliminate waste at every stage of the manufacturing process, notably by the elimination of:WIP, by reducing batch sizes (often to one)raw materials stock, by the suppliers delivering direct to the shop-floor just in time for usescrap and rework, by an emphasis on total quality control of the design, of the process, and of the materialsfinished goods stock, by reducing lead-times so that all products are made to order material handling costs, by re-design of the shop-floor so that goods move directly between adjacent work centersThe combination of these concepts in JIT results in:a smooth flow of work through the manufacturing planta flexible production process which is responsive to the customer's requirementsreduction in capital tied up in stocks1.4 Economic order quantity (EOQ) modelWe now turn to the theoretical side of stock control. Essentially, two stock problems need to be answered under either of two assumptions:when to re-orderhow much to re-orderPattern of stock levelsWhen new batches of an item in stock are purchased or made at periodic intervals the stock levels are assumed to exhibit the following pattern over time.When should stock be re-ordered?A gap (the lead-time) inevitably occurs between placing an order and its delivery. Where both that gap and the rate of demand are known with certainty, an exact decision on when to re-order can be made.In the real world both will fluctuate randomly and so the order must be placed so as to leave some buffer stock if demand and lead-time follow the average pattern. The problem is again the balancing of increased holding costs if the buffer stock is high, against increased stockout costs if the buffer stock is low.How much stock should be re-ordered?Large order quantifies cut order set-up and stockout costs each year. On the other hand, stock volumes will on average be higher and so holding costs increase. The problem is balancing one against the other.Economic order quantity (EOQ) is the quantity of stock ordered each time which minimises annual costs (order set-up + holding costs).ExampleWatallington Ltd is a retailer of barrels(桶). The company has an annual demand of 30,000 barrels. The barrels are purchased for stock in lots of 5,000 and cost 12 each. Fresh supplies can be obtained immediately, with ordering and transport costs amounting to 200 per order. The annual cost of holding one barrel in stock is estimated to be 1.20.The stock level situation could be represented graphically as follows:Thus Watallington Ltd orders 5,000 barrels at a time and these are used from stock at a uniform rate.Every two months stock is zero and a new order is made. The average stock level is 5,000/2 barrels, i.e. half the replenishment level.Watallington's total annual stock costs are made up as follows.Ordering costs 30,000/5000×2001,200Cost of holding stock 5000/2×1.2 3,000Total stock costs 4,2001.5 How much stock to be re-ordered: the EOQ formulaYou should remember from your previous studies that such situations offer minimum total stock costs when the order quantity is set at the economic order quantity or EOQ.Wbcte Co=fixed costs(order set-up costs)peJ ovdexD=expecicd annual sales volumeC H=bolding cost per stock unit per annumFor Warallington, EOQ==3,162barrelsTotal annual costs for the company will comprise holding costs plus re-ordering costs.=(Average stock×C H)+(Number of re-orders pa×Co)=(×£1.20)+(30000/3162×£200)=£1,897.20+£1,897.53=£3,794.731.6 The effect of large order discounts on EOQDiscounts may be offered for ordering in large quantities. If the order quantity to obtain the discount is above what would otherwise be the EOQ, is the discount still worth taking?This problem may be solved by the following procedure.Step 1 Calculate EOQ, ignoring discounts.Step 2 if this is below the level for discounts, calculate total annual stock costs.Step 3 Recalculate total annual stock costs using the order size required to just obtain the discount.Step 4 Compare the cost of steps 2 and 3 with the saving from the discount, and select the minimum cost alternative.Step 5 Repeat for all discount levels.ExampleIn the Watallington illustration, suppose that a 2% discount is available on orders of at least 5,000 barrels and that a 2.5% discount is available if the order quantity is 7,500 barrels or above. With this information, would the economic order quantity still be 3,162?SolutionSteps 1 and 2 have already been carried out, and it is known that total annual cost at 3,162 barrels/batch = 3795Step 3 At order quantity 5,000,total cost calculated as follows,4,200Extra costs of ordering in batcbes of 5,000 (405)Lcss:Saving on discount 2%×£12×30,000 7,200Step4 Net cosr saving 6,795Hence batches of 5,000 are worlhwhijc.Step3 At ordcr quantity 7,500,total costs are as follows.5,300Costs at 5,000 batch size 4,200Extra costs of ordering in batches of 7,500 (1,100)Less:Saving on extra discount(2.5-2)%×£12×30,0001,800Step4 Nct cost savingSo a further saving can be made by ordering in batches of 7,500.N.B. often the 'holding cost' will reduce where quantity discounts are taken - because this cost often relates to the original cost of buying an item.1.7 When to re-order stockHaving decided how much stock to re-order, the next problem is when to re-order. The firm needs to identify a level of stock which can be reached before an order needs to be placed. The re-order level (ROL) is the quantity of stock on hand when an order is placed. When demand and lead-time are known with certainty the re-order level may be calculated exactly.1.8 Re-order level with variable demand or variable lead timeWhen lead time and demand are known with certainty, ROL = demand during lead time. Where there is uncertainty, an optimum level of buffer stock must be found.If there were certainty, then the last unit of stock would be sold as the next delivery is made. In the real world, this ideal cannot be achieved. Demand will vary from period to period, and re-order levels must allow some buffer (or safety) stock, the size of which is a function of three factors:variability of demandcost of holding stockscost of stockouts.The problem may be solved by calculating costs at various decision levels, using the following procedure.Step 1 Estimate cost of holding one extra unit of stock for one year.Step 2 Estimate cost of each stockout.Step 3 Calculate expected number of stockouts per order associated with each level of stock.Step 4 Calculate EOQ, and hence number of orders per annum.Step 5 Calculate the total costs (stockout plus holding costs) per annum associated with each level of buffer stock, and select minimum cost options.ExampleAutobits Ltd is one of the few suppliers of an electronic ignition system for cars, and it sells 100 units each year. Each unit costs ~40 to buy in from the manufacturer, and it is estimated that each order costs ~10 to handle and that the cost of holding one unit in stock for one year is 25% of the cost price. The lead-time is always exactly one week.The weekly demand for units follows a probability distribution with a mean of 2, as follows:Demand Probability of demand0 0.141 0.272 0.273 0.184 0.095 0.046 0.01Auto bits estimates that the stockout cost is 20 per unit.Autobits must estimate when orders should be placed.SolutionStep 1 Cost of holding one unit: 10 (40 × 25%)Step 2 Cost of stockout: 20Step 3 Expected number of stockouts per orderThe normal level of demand in the lead-time is 2 (average, or mean, demand). Define buffer stock as re-order level minus 2. For example, if buffer stock were zero, re-ordering would take place when stock fell to 2.Buffer stock of 4 (6 - 2) would mean that, on the basis of the observations, a stockout would never occur. Thus, the range of buffer stock options is between 0 and 4 units i.e. re-order levels between 2 and 6.The pay-off table between buffer stock and actual demand in terms of stockouts is as follows:Pay-off table in terms of stockoutsRe-order level 2 3 4 5 6Actual densand durtng lead-time2or less 0 0 0 0 03 1 0 0 0 04 2 1 0 0 05 3 2 1 0 06 4 3 2 1 0Muhiplying lhcd,by the probabilify of that level of dcmand occurriug,tb cspcclcd numbcr of slockouts is as follows;Espected number of stockoutsRe-order levet 2 3 4 5 6Demand Probability2 or less 0.68* 0 0 0 0 03 0.18 0.18 0 0 0 04 0.09 0.18 0.09 0 0 05 0.04 0.12 0.08 0.04 0 06 0.01 0.04 0.03 0.02 0.01 0Total-Expeclcd 0.52 0.20 0.06 0.01 NilSrockoufs pcr order*calculated as 0.14+0.27+0.27=0.68Step4Ordcrs per annum==7.143Step 5(i) Re-order level 2 3 4 5 6(ii) Buffer stocks ((i) -2) 0 1 2 3 4(iii) Annual cost of holdingbuffer stock ((ii)× ~10) 0 10.00 20.00 30.00 40.00(iv) Stockouts per order (per step 3) 0.52 0.20 0.06 0.01 Nil(v) Annual cost of stockouts((iv)× 7.143 × ~20)74.29 28.57 8.57 1.43 Nil(vi) Total buffer stock cost((iii)+(v))74.29 38.57 28.57 31.43 40.00Therefore the minimum cost solution is to hold a buffer stock of 2 i.e. re-order when stocks fall to 4.From the above analysis, it is apparent that increasing buffer stock is worthwhile if the following conditions apply.Reduction in annual stockout costs > Unit holding cost orStockout cost x Orders per annum X Decrease in expected number of stockouts per order > Unit holding costPart II Cash ManagementCash and bank balances should be kept to a minimum, as they (usually) earn nothing for the firm, but care must be taken to ensure that activities are not restricted through shortage of ready cash to pay employees and creditors. Finance must obviously be set aside to meet taxation liabilities, pay dividends and invest in capital expenditure.However, until such payments become due, the cash may be profitably invested in short-term investments.1.1 Short-term cash investmentsCompanies may hold cash not only for transaction motives, but also for precautionary and speculative motives.precautionaryTransactions motive: the need to hold cash to meet day-to- day operational requirements. Precautionary motive: the holding of buffer stocks of cash to cover unexpected business requirements. Speculative motive: cash may be held to exploit unanticipated business or investment opportunities. The company's attitude to risk and working capital management will determine the planned cash holdings.Firms with an aggressive working capital policy will plan to minimize funds held, and borrow whenever cash is needed.Firms with a defensive policy will set aside cash in an investment portfolio, which can be drawn upon when the need arises.Objectives in the investment of surplus cashThe objectives can be categorized as follows:Liquidity: the cash must be available for use when needed.Safety: no risk of loss must be taken.Profitability: subject to the above, the aim is to earn the highest possible after tax returns.1.2 Borrowing from the bankBank overdraftsBank loansComparison of bank loans and overdrafts The difference can be shown as follows:1.3 Cash management modelsA number of different models have been developed for managing cash balances, in particular those developed by Baumol and by Miller-Orr.All models assume that a business will have a certain amount of ready cash available, in a bank current account(经常账户), for day-to-day transactions. In addition, an amount of buffer funds will be invested in deposit accounts, marketable securities, etc and these can be used to top up the current account, or absorb short-term surpluses from it, as appropriateCash management models attempt to minimise the total costs associated with cash movements between a current account and short-term investments - the ‘opportunity' cost of lost interest plus transaction costs - by determining when, and how much, cash should be transferred each time.ExampleIf the balances held in the current account are kept as low as possible by frequent movements of cash in and out, in order to minimise the holding costs, this may lead to excessive transaction costs.The models attempt to find an optimum cash management strategy that will minimize the total of these costs.Baumol cash management modelThe mechanics of this model are very similar to those of the EOQ model.If a company's cash resources are steadily used up by a constant daily demand for cash, Baumol suggested that the EOQ stock model could be applied to the situation so that the optimum regular cash injection, x, into the current account can be calculated.Where x = the optimum regular cash injection into the current account.ExampleA company faces a constant demand for cash totalling 200,000 pa. It replenishes its current account (which pays no interest) by selling constant amounts of gilts which are held as an investment earning 6% pa. The cost per sale of gilts as a fixed 15 per sale.The optimum amount of gilts sold, x, for each cash injection into the current account will be:=£10,000The Miller-Orr cash management modelThe model takes into account uncertainty in both receipts and payments of cash. It is best explained with reference to the following diagram.The Miller-Orr model controls irregular movements of cash by the use of upper and lower limits on cash balances.Part III Receivables Management1. Management of debtors1.1 Extending trade creditA firm must establish a policy for credit terms given to its customers. Ideally the firm would want to obtain cash with each order delivered, but that is impossible unless substantial settlement (or cash) discounts are offered as an inducement. It must be recognized that credit terms are part of the firm's marketing policy. If the trade or industry has adopted a common practice(行业惯例), then it is probably wise to keep in step with it.A lenient(宽大的,仁慈的;即宽松的) credit policy may well attract additional custom, but at a disproportionate increase in cost. The optimum level of trade credit extended represents a balance between two factors:profit improvement from sales obtained by allowing creditthe cost of credit allowedSettlement discountsA company may offer settlement discounts to its customers, by allowing debtors to pay less than their full debt if they pay sooner than the end of their credit period. The company must ensure that offering the discount is financially sensible, with the benefit of receiving the cash early exceeding the cost of the discount.1.3 Implementing credit policyAssessing creditworthinessPreventing credit limits from being exceededInvoicing promptlyDefinition of invoice: demand to pay.Collecting overdue(逾期) debtsFactor: 保理商Factoring: 保理Invoice discounting: 商票贴现Receivable aging: 账龄。

财务成本管理英语词汇

金融业术语,意为“不,无;不包 括,除,在外,不计算…在内;无权获 Ex dividend 无红利,无股息 Ex interest 无利息 Topic 04:patio analysis (interpretation of financial statements) 比率分析(财 务报分析) Paragraph 1 1 Window-dressing (财务报表)粉饰,弄虚作假 2 Creative accounting 创造性会计 3 Detriment 损害,伤害 4 Profit margin 利润率 Paragraph 2 1 Ascertain (动词)确定,查明,探知 2 Journalist 新闻工作者 3 Commentator 评论员 Paragraph 3 1 Liquidity 流动性,(金融术语)偿债能力 2 Scrutinize (动词)详细检查,彻查 3 Working capital 营运资本 4 Current liabilities 流动负债

第 3 页,共 5 页

财务成本管理篇 financial management and cost management

5 6 7 Current assets Quick/acid test ratio Statement of financial position Balance sheet Statement of financial position 流动资产 速动/酸性测试比率 财务状况表,即资产负债表

第 1 页,共 5 页

财务成本管理篇 financial management and cost management

11 Factoring 12 Expertise 13 Outsource Paragraph 3 1 Cite 2 Liable 3 Opportunity cost 4 In short 5 Neglect Paragraph 4 1 Core 2 Turnover 3 Unpredictable Paragraph 5 1 Insolvency 2 Express 3 Fund Paragraph 7 1 Holding cost 2 Theft 3 Obsolescence 4 Stockout 5 Stoppage 6 Strike 7 Trade-off 8 EOQ(economic order quantity) 9 Assumption 10 Lead time 11 Buffer Paragraph 9 1 Readily 2 Transaction motive 3 Precautionary motive 4 Speculative motive 5 Be aimed at 6 Associate with 7 Current account 8 Irregular 9 Incorporate 10 Return point Paragraph 10 1 Surce of finance 2 Option Topic 03:dividend poicy 股息分配政策 Paragraph 1 1 Rather than 2 Make up 3 Shortfall 4 Indifferent 5 Capital gain 6 Not…but… 7 Asymmetry 保理 专门知识,专门技术 外包 引用,引证 有责任的,有义务的 机会成本 简而言之 疏忽,忽视 核心,要点 营业额,流通量,人员流动 不可预知的,不定的,出乎意料的 破产,无力偿还,倒闭 (动词)表达 (动词)投资,资助 持有成本 盗窃 过时 缺货 停止 到达 权衡,取舍 经济采购量 假定,假设,假设条件 订货至交货的时间,提前期 缓冲 容易地,无困难地 交易性动机 预防性动机 投机性动机 旨在,为了,以…为目的 与…联系在一起 活期存款账户,经常账户 不规律的 包含,体现 现金返回线 融资渠道 选项,选择权,期权

财务成本管理英语04

[对应中文教材2008年财务成本管理第五章:投资管理]

A.ROCE(已动用资本回报率)orARR(会计收益率)(AccountingRateofReturn)

B.Payback(回收期法)

Paybackperiod

=Initialpayment/Annualcashinflow,paybackisnotalwaysanexactnumberofyears

twopossibilitiesexist:

(i)thecashbudgetapproach

(ii)thetabularapproach.

(1)Cashbudgetapproach

Time01 2 3

£’000 £’000 £’000 £’000

Investment (X) — — X

Advertising (X) (X)--

(expressedasadecimal.Fromthisitfollowsthat:

theIRRofaperpetuity= =100

Perpetuity:永续年金

Methodofpresentation

AsimplecalculationsuchasthoseforWoodscanbedoneonasingleline.Forlargerprojects

MuchNPVhasfallen(from to )asthediscountratehasrisenfromAtoB,

TheyfindhowmuchmorethediscountrateneedstorisetobringtheNPVtozero.

Whethertheformulaisusedorcommonsense,thecalculationassumesalinearrelationship

财务管理专业英语词汇表(很全面)

Chapter 1 An Overview of Financial Management business 企业,商业,业务finance 财务,理财management 管理,管理层revenue 收入return 回报shareholder 股东stakeholder 利益相关者stock 股票profit maximization 利润最大化shareholder wealth maximization 股东财富最大化enterprise value maximization 企业价值最大化hedge risks 规避风险inventory 存货current assets 流动资产current liabilities 流动负债financing 筹资corporation 股份公司earning per share(EPS)每股收益exchange rate 汇率inflation 通货膨胀contractual relations 契约关系equity 所有者权益dividend 股利CFO(Chief Financial Officer)首席财务官,财务总监Chapter 2 The Time Value of Money accrued 增值的,应计的annuity 普通年金annuity factor 年金系数compound interest 复利discounting 贴现future value 终值geometric series 等比数列mortgage 抵押ordinary annuity 普通年金perpetuity 永续年金present value 现值principal 本金reinvest 再投资simple interest 单利time value of money 货币时间价值compounding 复利计算Chapter 3 Risk and Rewardcapital asset pricing model(CAPM)资本资产定价模型diversification 分散化efficient capital market 有效资本市场expected return 期望回报market, systematic, or undiversifiable risk 市场风险、系统风险或不可分散风险portfolio 组合reward 收益,溢酬,溢价risk-aversion 风险厌恶risk-neutrality 风险中性risk preference 风险偏好risk premium 风险溢价security markets line(SML)证券市场线semi-strong capital market efficiency 半强式资本市场有效spread out 分散square root 平方根standard deviation 标准差strong capital market efficiency 强式资本市场有效transaction cost 交易成本unique, firm-specific, idiosyncratic, unsystematic, or diversifiable risk 特殊风险、特有风险、虚假风险、非系统风险或可分散风险variance 方差volatility 波动性weak capital market efficiency 弱式资本市场有效Chapter 4 Financial Assets and Their Valuation asset 资产security 证券issue (股票,钞票)分发,发行coupon rate 票面利率,息面利率annual 每年的,年度的,一年一次的obligate 使(某人)负有责任或义务outstanding 未解决的,未偿付的,杰出的calculate 估计,预测compensation 报酬,工资,补偿物perpetual 永久的,永恒的infinite 无限的,无穷的substitute 替代,取代yield 出产,产,出(果实、利润、结果)approximation 相似,近似trial-and-error 试误法illustrate 说明,阐明entitle 使人有权拥有……liability 负债intrinsic value 内在价值asymmetry 不对称constant 不变的,可靠的phase 阶段,时期preferred stock 优先股Chapter 5 Capital Budgeting and Investment Decision capital budgeting 资本预算estimating net present value 预期净现值the average accounting return 平均会计报酬率stand-alone principle 独立原则the internal rate of return 内部收益率the payback rule 回收期法erosion 侵蚀net working capital 净营运资本opportunity cost 机会成本hard rationing 硬约束soft rationing 软约束sunk cost 沉没成本incremental cash flow 增量现金流量pro forma financial statement 预估财务报表forecasting risk 预测风险scenario analysis 情景分析investment criteria 投资决策标准cash flow 现金流量project cash flow 项目现金流量depreciation 折旧capital spending 资本性支出garbage-in garbage-out system 垃圾进、垃圾出系统best case and worst case 最优情形和最差情形Chapter 6 Working Capital Management working capital 营运资本speculative 投机precautionary 预防的buffer 缓冲器invoice 发票deposit 存款disbursement 支付expenditure 消费trade-off 权衡attorney 代理人applicant 申请人utilization 应用dampen 使沮丧ordering cost 订货成本carrying cost 储存成本raw material 原材料insurance 保险linear 线性的bad-debt 坏账Chapter 7 Financing Modes debt financing 债务筹资equity financing 权益投资prospectus 招股说明书the general cash offer 普通现金发行the rights offer 配股发行initial public offering(IPO) 首次公开发行underwriting discount 承销折价the subscription price 认购价格collateral 抵押品mortgage securities 抵押债券debenture 信用债券sinking fund 偿债基金call provision 赎回条款call-protected 赎回保护operating leases 经营性租赁financial leases 融资租赁sale and lease-back 售后租回leveraged leases 杠杆租赁warrants 认股权证convertibles 可转换债券call options 看涨期权straight bond value 纯粹债券价值conversion value 转换价值secured loans 抵押贷款committed lines of credit 承诺式信贷额度compensating balances 补偿性余额trust receipt 信托收据Chapter 8 Capital Structure capital structure 资本结构optimal capital structure 最佳资本结构financial leverage 财务杠杆homemade leverage 自制杠杆payoff 回报proceeds 收益financial risk 财务风险interest tax shield 利息税盾direct bankruptcy costs 直接破产成本indirect bankruptcy costs 间接破产成本liquidation 清偿reorganization 重组absolute priority rule 绝对优先原则qualification 限定条件cost of equity 股权成本business risk 经营风险pie model 饼状模型break-even point 收益均衡点indifference point 无差异点Chapter 9 Dividend Distribution dividend irrelevance theory 股利无关理论retained earnings 留存收益capital surplus 资本公积earned surplus 盈余公积legal surplus 法定盈余公积free surplus reserves 任意盈余公积stockholder meeting 股东会declaration date 宣告日holder-of-record date 股权登记日ex-dividend date 除息日stock split 股票分割stock dividend 股票股利stock repurchase 股票回购declaration date 股利宣布日record date 股权登记日regular dividend 正常股利cash dividend 现金股利stock dividend 股票股利stock price appreciation 股价增值open market 公开市场payment date 股利支付日going concern 持续经营。

财务成本管理英语完整版

财务成本管理英语完整版财务成本管理英语 HEN system office room 【HEN16H-HENS2AHENS8Q8-HENH1688】INVESTMENT APPRAISAL[对应中⽂教材2008年财务成本管理第五章:投资管理](已动⽤资本回报率)or ARR(会计收益率)(Accounting Rate of Return)(回收期法)Payback period=Initial payment/Annual cash inflow, payback is not always an exact number of yearsMost common formula:ROCE=EBIT (after depreciation)/ initial capital costsC NPV(净现值法)(1) Basic assumptions:·cash outlay occurs in year 0 (now).·cash flows occur at the end of the year.·if a cash flow occurs at the beginning of a year, it is assumed to occur at the end of the previous year.D IRR(内含报酬率法)(1)Basic principle: IRR is the cost of capital at which the NPV is zero, if the expected IRR is higher than a target rate of return; the project is financially worth undertaking.(2)Selection between IRR and NPV: when a choice has to be made between mutually exclusive projects, in such case the NPV should be selected, because higher NPV can maximize sharehold er’s wealth.DefinitionThe discount rat which, when applied to the cash flows of a project, gives an NPV of zero.OrThe break-even interest rate for a project.It is the maximum rate of interest that you could afford to pay on a project without making a loss.FeaturesAdvantages -Takes into account the time value of money-Relative measure-More readily understood than NPVDisadvantages -May not be unique – projects can have more than one IRR- May rank projects incorrectly – for mutually exclusive projects or whenFunds are short supply- Cannot cope with changing rates of interestThe method of calculation depends upon whether or not the project has even cash flows.Even cash flowsConsider an investment of £ that generates net cash earnings of £10m for 5yearsThe IRR is the discount rate that gives a NPV of zero. This means that the IRR is theRate that will discount five installments of £10m to a present value of £. This in turnMeans that the IRR is the discount rate for which the 5year annuity factor is . A The project’s IRR has been found via a cumulative discount factor (annuity factor) givenBy:Annuity factorat the IRR=for the life of the projectUneven cash flowsThese have to be found by trial and error or by estimating using two present values.Where:A=lower rate chosen=NPV at rate AB=higher rate=NPV at rate BIt helps to get A and B as close t o the true IRR as possible, but it doesn’t matter whetherthe resultant NPVs are positive, negative or one of each.Some students prefer to use a common sense approach rather than a formula. Seeing by nowMuch NPV has fallen (from to) as the discount rate has risen from A to B, They find how much more the discount rate needs to rise to bring the NPV to zero.Whether the formula is used or common sense, the calculation assumes a linear relationshipBetween NPV and discount rate. In fact the relationship is not linear, hence the calculationIs only approximate and (unless you have been lucky when guessing which discount rates touse)you should not quote IRR’s calculated in this way to many, not toany,decimal places –unless the examiner asks you.IRR of a perpetuityThe present value of a perpetuity is the annual cash flow divided by the discount rate(expressed as a decimal. From this it follows that:the IRR of a perpetuity ==100Perpetuity: 永续年⾦Method of presentationA simple calculation such as those for Woods can be done on a single line. For larger projectstwo possibilities exist:(i) the cash budget approach(ii) the tabular approach.(1)Cash budget approachTime 0 1 2 3£’000£’000£’000£’000Investment (X)—— XAdvertising (X)(X) - -Working capital (X)- - XMaterials (X)(X)(X)-Labour —(X)(X)(X)Overheads —(X)(X)(X)Revenue ———X————Net cash flow (X)(X)(X) X————y% Discount factor 1 X X XPresent value (X)(X)(X)XNet present value (£’000)XThe cash budget approach is suitable for short projects with lots of different cash flows Which change from year to year.(2) Tabular approachTime Cash flow y% Discount Present value£’000£’000£’0000 Investment (X) 1 (X)0 and 1 Advertising (X)X (X)0 Working capital (X) 1 (X)0-9 Materials (X) 1 (X)1-10 Labour and overheads (X)X (X)1-10 Revenue X X X 10 Sales proceeds X X X10 WC recovery X X X—Net present value (£’000)XThe tabular approach is suitable for long projects with lots of different cash flows that are The same from year to year (enabling annuity factors to be used).Picking the right figuresWhen carrying out discounted cash flow analysis it is important to select the right figures. Ignore:costs – amounts that have already been spent– not a cash flowvalues – not a cash flow–incremental fixed costs (look out for the words “reapportioned fixed overheads”)costs – taken into account by the discounting processInclude:Those cash flows that are specifically received or incurred as a result of the acceptance of the project(future–incremental–cash flows).Asset replacement decisionFactors to be considered when making replacement decision are as follows:·capital cost of new equipment;·operating costs, increased repair and maintenance costs;loss of productivity;lower of quality and quantity of output;One application of discounted cash flow is to make decisions concerned with the replacement ofMachinery. This applies to short – life assets that will need to be replaced in perpetuity (. motorCars or photocopiers). As a machine gets older, it is likely to cost more to keep it running and itsScrap value will decrease. The aim is to find the optimal replacement cycle for the machine,. how often it should be replaced - before it becomes uneconomic to own.A simple approach would involve finding the total cost of keeping an asset for 1,2,3 years, etc,Then finding an average annual cost.DCF VersionNow, each possible replacement cycle is treated as a project (1-year, 2-year, or 3-year project).You calculate the NPV of each project (rather than just the total cost).Instead of dividing the NPV’s by 1,2,or 3, they’re divided by the 1,2, or 3-year annuity factorTo find an equivalent annual cost.Equivalent annual cost =。

{财务管理财务知识}引用社会经济类英语词汇