保险文本译件

养老保险改革最新外文文献翻译

养老保险改革最新外文文献翻译This article aims to compare the endowment insurance system in different countries。

The endowment insurance system is a type of life insurance that XXX in China。

the United States。

and the United Kingdom.In China。

the endowment insurance system is XXX system covers all employees。

XXX。

the system XXX.In the United States。

XXX individuals can choose to participate。

The system has XXX。

it also e individuals.In the United Kingdom。

the endowment insurance system XXX。

it also XXX.Overall。

the study shows that the endowment insurance system varies in different countries and has XXX countries.XXX is a common social problem that is XXX society。

It has XXX to set up a system to support the elderly。

The old-ageinsurance system was XXX。

with the development of social economy。

the system has XXX strata of the elderly。

汽车保险中英文对照外文翻译文献

汽车保险中英文对照外文翻译文献(文档含英文原文和中文翻译)汽车保险汽车保险是在事故后保证自己的财产安全合同。

尽管联邦法律没有强制要求,但是在大多数州(新罕布什和威斯康星州除外)都要求必须购买汽车保险;在各个州都有最低的保险要求。

在鼻腔只购买汽车保险的两个州,如果没有足够的证据表明车主财力满足财务责任法的要求,那么他就必须买一份汽车保险。

就算没有法律规定,买一份合适的汽车保险对司机避免惹上官和承担过多维修费用来说都是非常实用的。

依据美国保险咨询中心的资料显示,一份基本的保险单应由6个险种组成。

这其中有些是有州法律规定,有些是可以选择的,具体如下:1.身体伤害责任险2.财产损失责任险3.医疗险或个人伤害保护险4.车辆碰撞险5.综合损失险6.无保险驾驶人或保额不足驾驶人险责任保险责任险的投保险额一般用三个数字表示。

不如,你的保险经纪人说你的保险单责任限额是20/40/10,这就代表每个人的人身伤害责任险赔偿限额是2万美元,每起事故的热身上海责任险赔偿限额是4万美元,每起事故的财产损失责任险的赔偿限额是1万美元。

人身伤害和财产损失责任险是大多数汽车保险单的基础。

要求汽车保险的每个州都强令必须投保财产损失责任险,佛罗里达是唯一要求汽车保险但不要求投保人身伤害责任险的州。

如果由于你的过错造成了事故,你的责任险会承担人身伤害、财产损失和法律规定的其他费用。

人身伤害责任险将赔偿医疗费和误工工资;财产损失责任险将支付车辆的维修及零件更换费用。

财产损失责任险通常承担对其他车辆的维修费用,但是也可以对你的车撞坏的灯杆、护栏、建筑物等其他物品的损坏进行赔偿。

另一方当事人也可以决定起诉你赔偿精神损失。

看看汽车责任险的最低投保要求,你就会发现在你居住的地方哪些保险是必须的。

记住,如果你引起了一场严重的交通事故,最低限度的保险可能不足以支付你造成的损失。

因此最好在州要求的最低限度外再买一些保险。

如果你已经拥有了家庭或者拥有养老或存储账户,你应该更多地考虑责任险。

汽车保险丝英文译中文

汽车保险丝英文译中文腾骅自动变速箱维修丰田车系统保险丝中英文名称及相关的系统对照情况见下表FUSE 保险丝、熔断丝2 DOME 保险丝室内灯系统3 STOP 保险丝停车灯系统4 HORN 保险丝喇叭5 ST 保险丝起动机6 DEFOG 保险丝除雾器系统7 TRUN 保险丝转向信号灯系统8 PANEL 保险丝仪表板9 GAUGE 保险丝组合仪表10 ENGINE 保险丝发动机11 RADIO 保险丝音响系统12 CHARGE 保险丝充电系统13 IGN 保险丝点火系统14 FOG 保险丝防雾灯系统15 WIPER 保险丝刮水器和洗涤器系统16 CIG 保险丝点烟器17 TAIL 保险丝尾灯18 A/C 保险丝空调系统19 EFI 保险丝电子控制燃油喷射系20 AIR SUS 保险丝空气悬架系统21 ABS 保险丝防抱死制动系统22 SRS 保险丝辅助乘员保护系统23 ECU 保险丝电子控制单元24 HAZ-HORN 保险丝危险-喇叭25 POWER 保险丝电动车窗控制系统26 CB DOOR 保险丝电动门锁控制系统27 FL RAD FAN 保险丝散热器风扇28 HTR 保险丝加热器系统29 HEAD RH-LWR 保险丝右前照灯近光30 HEAD LH-LWR 保险丝左前照灯近光31 HEAD RH-UPR 保险丝右前照灯远光32 HEAD LH-UPR 保险丝左前照灯远光33 TEMP 温度34 O/D 超速35 A/T 自动变速器36 TDCL 故障诊断连接器37 TEL 车载电话38 RR A/C 保险丝后空调系统39 RR SEAT-HTR 保险丝后座加热器系统40 SEAT-HTR 保险丝前座加热器系统41 ECU-IG 保险丝巡航控制系统、电动倾斜和伸缩控制系统、ABS 系统42 ECU-B 保险丝安全气囊警告灯43 DOME-CLOCK 保险丝车内照明系统、液晶车内后视镜、电子表。

保险自固文言文翻译

夫保险者,国之大计,民之保障也。

古之圣贤,未尝不重其道。

是以,今日之世,吾辈当深究其理,以图自固。

insurance, it is the great cause of the country, the guarantee of the people. The ancient sages, never not important their way. Therefore, in today's world, we should deeply study its theory, in order to self-fortification.盖保险之始,起于人心之善。

人之生也,各有其志,各有其欲。

欲求其利,必先避其害。

是以,保险者,所以避害而得利也。

然保险之道,非一日之功,非一人之力。

必众志成城,众力合一,而后能自固。

The origin of insurance, starts from the kindness of the people.People's lives, each has its aspirations, each has its desires. Want to seek their interests, must first avoid their harm. Therefore, insurance is to avoid harm and get benefit. However, the way of insurance, is not a day's work, not one person's strength. Must be united as one, the strength of unity, then can self-fortification.古之智者,知其然也。

故设仓储以蓄积,置仓库以储藏。

积之既久,财货充盈,民之利也。

保险合同翻译

保险合同翻译

合同标题,保险合同翻译范本。

合同翻译范本。

甲方,(保险公司名称)。

乙方,(被保险人名称)。

鉴于甲方为乙方提供保险服务,双方经协商一致,达成以下保险合同翻译范本:第一条保险责任。

1.1 甲方在保险期限内,对乙方在保险范围内因意外事故或其他风险所导致的

损失承担保险责任。

1.2 保险范围包括但不限于财产损失、人身伤害、第三者责任等。

第二条保险金额及费用。

2.1 保险金额为(具体金额),保险费用为(具体金额),乙方应在约定时间

内支付保险费用。

2.2 如乙方未按时支付保险费用,甲方有权暂停或终止保险责任。

第三条索赔和理赔。

3.1 乙方在保险事故发生后应及时通知甲方,并提供相关证明和资料。

3.2 甲方收到索赔通知后,将及时进行理赔审核,并在法定期限内给予答复。

第四条合同解除。

4.1 若乙方提供虚假信息或故意隐瞒重要事实,甲方有权解除保险合同并不承担保险责任。

4.2 除非双方另有约定,保险合同解除后,甲方应返还乙方已支付的未到期保险费用。

第五条其他约定。

5.1 本合同未尽事宜,由双方协商解决。

5.2 本合同一式两份,甲乙双方各执一份,具有同等法律效力。

甲方(盖章):乙方(盖章):

日期:日期:

以上为保险合同翻译范本,具体内容以实际合同约定为准。

如有任何疑问,请随时与合同范本专家联系。

人寿保险外文翻译文献

人寿保险外文翻译文献(文档含英文原文和中文翻译)Is Life Insurance Good for Retirement Planning?At first glance, the life insurance industry appears to be in trouble as it faces the millennium. As the large baby boomer market ages, these consumers have shifted their financial focus away from life insurance and towards assuring their future comfort.Although the industry has long recognized that its future lies in more in financial products than in life insurance, it has lately been losing its share of the retirement market. Between 1992 and 1994 alone, insurers' share of 401(k) plans slipped from 34% to 30%,while mutual funds' share leaped from 26% to 37%. Tax-deferred annuities sold by insurance companies fell in share of Americans' total retirement assets to 16.61% in 1996 from its peak in 1990 of 22.56%. In individual retirement accounts, while banks' market share fell dramatically from 61% in 1985 to 18.4% in 1996, insurance companies saw mutual funds and brokerage houses gain the fattest slices of the banks' loss.Such developments can, however, be misleading. Two experts who believe that the life insurance industry's picture is far brighter than it firstappears are Paul Hoffman and Anthony M. Santomero of the Wharton School's Financial Institutions Center. Their paper, "Life Insurance Firms in the Retirement Market: Is the News All Bad?" answers their own titular question with a decided "no." Hoffman and Santomero point to a number of facts that, while not completely reassuring to the industry, definitely show some profitable opportunities. A revised version of this paper appeared in the Journal of the American Society of CLU and ChFC. First of all, retirement planning is a huge and growing market. Contrary to reports that have appeared in the past, baby boomers are saving more rapidly than their parents. And, face it, they have to: The decline of defined benefit plans, which Americans once counted on so heavily for their golden years, demands that they look to other financial instruments to protect their futures. That opens up new sales opportunities for group and individual retirement plans sold by financial companies, including insurers. And annuities, which are insurers' biggest retirement-oriented product, are growing in importance as a share of Americans' wealth. Moreover, annuities have remained stable as a percentage of retirement assets.Second, while mutual funds and brokerage houses have been expanding their market share, their inroads have been mostly at the expense ofdepository institutions, not life insurance companies.Third, the retirement market is a growing financial feast, even if insurers do have to compete a little harder for their share of the bounty. By the end of 1996, total private retirement assets in the U.S. stood at almost $5.1 trillion, having increased as a share of total national wealth from 10.6% in 1983 to 13.6%.There has also been a decided shift in the nature of the nation's retirement assets. In 1980, total defined benefit assets in the U.S. were 2.5 times defined contribution assets (mostly, 401(k) plans). By 1993, the latest date for which figures are available, total funds of both types of plans were almost equal. From 1984 to 1993, total U.S. 401(k) assets alone grew from about $92 billion to $616 billion, increasing from 0.74% of Americans' total wealth to 2.18%. As a share of total retirement capital, 401(k)s rose from about 7% in1984 to 16.6% in 1993, according to the U.S. Department of Labor. Individual retirement accounts, although no longer as attractive as a saving vehicle due to the loss of most tax advantages in 1986, still capture a huge amount of total retirement assets. By the end of 1996, savings in IRAs had swollen to $1.35 trillion, representing around 3% of U.S. wealth. Most of the growth was from gains in the equity market rather than in newcontributions. Meanwhile, mutual funds and brokerage firms picked up more than 43% of the depository institutions' drop in IRA market share, increasing their own share from 15.8% to 37.9% for mutual funds and 14.7% to 35.8% in the case of brokerages. Insurers' share of the IRA market actually fell from 10.4% in 1990 to 7.8% in 1996.The annuity market represent insurers' best hopes to retain a significant share of the retirement market. In 1993, annuities represented almost 20% of the market, following IRAs' 23.4%. Insurance companies' share of this huge financial stash stood at almost 76% in 1993, equal to more than $1 trillion, of which about $734 billion was earmarked for retirement. (These figures only include tax-advantaged annuities).Life insurance carriers, then, are likely to retain significant sales and profit growth in the retirement market. Still, the industry needs to find new ways to grow. Its recent binge of mergers and acquisitions has improved cost efficiency and diminished competition among carriers, but is scarcely enough to offset inroads by brokers and mutual funds. Even banks have declared their intentions to market competitive new instruments in the annuities market. A disturbing development for insurance companies is their lossof share of revenue, from 55% of sales fees for variable annuities in 1994to only 43% the next year. The Wall Street Journal has predicted that insurers' share of these fees could fall to 30% by the year 2000.With these developments in mind, strategy for life insurance firms in the decade ahead need to aim at stopping their skid out of the retirement market, where they have fallen from a 22.7% market share in 1983 to 18% in 1996. Elements of a successful strategy might include:1. Retain dominance in annuities by increasing cost efficiency in delivery and holding down fees, to maintain competitiveness with other financial services.2. Slow down loss of market share for IRA accounts. While this market has diminished in terms of new contributions, financial returns on existing IRA assets have grown to 12% of insurance company pension assets as of 1996, from3.3% in 1983.3. Jump with both feet into the exploding 401(k) market, with particular emphasis on pursuing the fat market for rollover accounts.For the life insurance industry, the stakes are clear. While its decline in competitiveness is not as serious as widely proclaimed, its share of the retirement market has been falling by more than 1% a year in recent years. Because its income from annuities has surpassed its income from life insurance since 1985, clearly it must continue to pursue the retirementsegment. Now, however, it also needs to look to ways of solidifying and perhaps expanding its share of the 401(k) and IRA niches.Insurers' strength is that they can leverage a wide spectrum of products to help them to protect their presence in the retirement marketplace. For example, they can offer one-stop shopping for a combination of retirement income, long-term care coverage and estate protection. By offering consumers products that blend traditional risk protection with asset management, insurers may be able to protect their own future.人寿保险是否有利于退休金计划乍看之下,寿险业出现了已面临了千年的麻烦。

商务英语情景对话保险带翻译(2)完整篇.doc

商务英语情景对话保险带翻译(2)ATake a seat inside and see what you think.So you will take the Porsche then, sir?坐进去看看感觉如何。

那么你要租这辆保时捷啰?BYes, and I want to buy the insurance too. I think it s necessary.是的,并且我要买保险,这是需要的。

AYou re smart to buy it. At 45 dollars for three days, it is a good deal.你很聪明。

保三天,四十五元,蛮合理的。

BCan I return the car in San Francisco?我可以在旧金山还车吗?ASan Francisco? No, sir.We only have this office here. You will have to return it here.旧金山?不行。

我们只在这里有公司,你必须把车交还到这里。

BReally? I heard in America you can return rental cars in different cities.这样啊?我听说在美国你可以把车交还到不同的城市。

ANo, sir. That s only with the very big companies.I m sorry, but this car must be returned to this lot.只有大公司才可以。

我很抱歉,这辆车只能交还到这个车厂。

BWell, I guess I will have to drive back down then. Hmm. I didn t think of that.那么到时我必须把车开下来,我还没想到这点。

ADo you still want the car, sir?你还是想租这辆车吗?BYes. It will be fun. Driving back down the coast. My girlfriend will like it.是的,沿着海边开下来应该很有意思,我女朋友应该会喜欢的。

保险翻译

I'm looking for insurance from your company.我是到贵公司来投保的。

Mr. Zhang met Mr. William in the office of the People' Insurance Company of China.张先生在中国人民保险公司的办公室接待了威廉先生。

After loading the goods on board the hip, I go to the insurance company to have them insured. 装船后,我到保险公司去投保。

When should I go and have the tea insured?我什么时候将这批茶叶投保?All right. Let's leave insurance now.好吧,保险问题就谈到这里。

I have come to explain that unfortunate affair about the insurance.我是来解释这件保险的不幸事件的。

I must say that you've corrected my ideas about the insurance.我该说你们已经纠正了我对保险的看法。

This information office provides clients with information on cargo insurance.这个问讯处为顾客提供大量关于货物投保方面的信息。

The underwriters are responsible for the claim as far as it is within the scope of cover.只要是在保险责任范围内,保险公司就应负责赔偿。

The loss in question was beyond the coverage granted by us.损失不包括在我方承保的范围内。

保险单翻译模板

保险单翻译模板篇一:保险单英语翻译练习Put the insurance policy into Chinese:The People’s Insurance Company of ChinaORIGINALHead Office: BEIJING Established 1949MARINE CARGO TRANSPORTATION INSURANCE POLICYPolicy No.WH74/23002This policy of Insurance witnesses that the People’s Insurance Company of China (hereinafter called “The Company”),at the Request of CHINA IMPORT & EXPORT WUHAN CORP. OF STATE FARMS(hereinafter called the “insured”)and in consideration of the agreed premium being paid to the Company by the Insured,undertakes to insure the under-mentioned goods in transportation subject to the conditions of this policy as perthe ClausesT otalAmount Insured? U.S.DOLLARS NINETEEN THOUSAND THREE HUNDRED AND SIXTY ONLY perconv eyance S. S. “EASTWIND”V.33Slg. on or abt. ?AS PERB/L From WUHAN to PUSANConditionsCOVERING ALL RISKS AS PER OCEAN MARINE CARGOCLAUSES AND W AR RISKS CLAUSES(1/1/1981) OF PICC.Claims, if any, payable on surrender of the First Original of the Policy together with other relevant documents.In the event of accident whereby loss or damage may result in a claim under this Policy immediate notice applying for survey must be given to the Company’s Agent as mentioned hereunder. HYOPSUNG SHIPPING CORPORATION12TH FLOOR YUCHANG BLUG? 25-2, 4-KACHUNGANG-DONG, THE PEOPLE’S INSURANCE COMPANY OF CHINACHUNG;KU, PUSAN, KOREA P.O.OX 75 TEL:463 6551 TI 6553 WUHAN BRANCHClaim payable at? PUSAN, KOREA IN USDGeneral ManagerFAX: 027-******** TEL027-******** Date JUN. 06,2003篇二:保险英语词汇(已排版)保险英语词汇Aabandonment 委付abandonment clause委付条款accident 意外事故accounting period 结算期act of god 不可抗力actual total loss 实际全损actuarial method 精算法actuary 保险精算师additional premium 附加保险费additional risk 附加险advance profit 预期利润aggregate limit 累积限额aggregated loss 累积损失all-risks policy 一切险保单antis election 逆选择applicant 投保人application 投保单approved 承保assignment clause转让条款average 海损、海损分摊average adjuster 海损理算人average clause共同海损分担条款保险英语词汇Bbalance所欠款项beneficiary受益人binder 暂保单binding slip 暂保单breakage of packing 包装破碎险保险英语词汇Cbroker 经纪人capacity 承保能力captive 自保公司captive pools 自保组合cargo damage adjustment 货损理算cargo damage inspection 货损检验cargo damage prevention 货损预防cargo damage report货损报告cargo damage survey货损检查,货物损坏检验cargo insurance premium 货物保险费cargo insurance rate 货物保险费率cargo insurer 货物承保人cargo policy 货物保单,货物保险单cargo premium货运保险费,货物保险费cargo underwriter货物保险承保人(商),货险承保人,货物承保人cash loss 现金赔款cash value 现金价值catastrophe巨灾catastrophe excess of loss(CXL)巨灾超赔\巨灾超赔分保categories of insurance保险类别ceding company 分出公司ceding(insurance)company 分保公司ceding, retrocession(for reinsurance) 分保certificate of cargo damage货损证明certificate of insurance 保险证明、保险凭证- 1 -cession limit 分保限额China Insurance Clause (CIC) 中国保险条款claim索赔claim assessor索赔人claim settlement 理赔claim-prone容易出险claims and arbitration 索赔与仲裁claims assistance理赔协助clash and breakage 碰损,破碎险clean cut结清方式coinsurance 共保co-insurance 共同保险co-insurance company 共同保险公司combined ratio综合赔付率commencement and termination起讫concurrent insurance 同时保险consequential loss (CL) 后果损失constructive total loss 推定全损contingent liquidity 或有流动性continued insurance 继续保险co-related risks 关联风险cover承保、责任额cover note 保险证明书,承保单,保险证明cover note 暂保单(证明同意承保的临时文件)coverage受保范围保险英语词汇Ddamage 损坏赔偿金damage cargo clerk 理残员,货损管理员damage cargo list货损单,残货单damage certificate 损坏证明书damage claim 损坏索赔damaged by other cargo 由其他货物损害damaged cargolist 受损货物单damaged cargo report受损货物报告书,货物损害报告deductibles 免赔额deposit premium 预付保费destroyed 毁坏disbursement policy (船舶)驶费保险单dividend system 红利制度double insurance 双保险dual valuation clause 双重价值条款保险英语词汇Eemployer业主Endorsement批单endorsement: 签注endowment insurance养老保险endowment policy人寿定期保险单event limit事件限额ex gratia payments通融赔款excess loss 超额赔款excess of loss cover 超额赔偿excess of loss(XL) 超赔分保exclusion 除外责任EXL protection 超赔保障exposed areas 风险承受区域- 2 -exposure rating风险评估extended-term insurance 过期保险extra charges 额外费用extra premium额外保险费extraneous risks (additional risks) 附加险group insurance 团体保险guarantee of insurance 保险担保书保险英语词汇H保险英语词汇Ffacultative business 临分保facultative reinsurance 临时分保fault liability 过失责任financial quota shares成数分保fine print 细则finite risk 有限制的风险finite risk transfer 有限风险转移floating policy 浮动保险单franchise (deductible)免赔额;免赔率free of all average (FAA) 全损赔偿freight insurance运费保险freight policy 运费保险单full coverage全额承保full insurance全额保险full insurance value 足额保险价值full liability 全部责任保险英语词汇Ggeneral average(GA)共同海损grace period宽限期gross net premium income(GNPI)总净保费收入hazard 危险因素health insurance 疾病保险,健康保险heavy damage 严重破坏holistic risk transfer 整体风险转移hook damage 勾(钩)损险hour clause小时条款保险英语词汇IIBRN reserve已发生但未报的损失储备金,IBRN储备金import cargo insurance进口货物保险increased value clause 增值条款increased value insurance 增值保险increasing coverage, extending coverage 加保Incurred but not reported losses(IBRN)已发生但未报的损失indemnitylimit 赔偿期限indemnity period 赔偿期individuallosses单一损失industrial insurance 产业保险inflated claim 超额索赔inherent nature of cargo 货物的固有性inherent vice 内在缺陷inherent vice of cargo货物固有缺陷inspection of cargo 积货鉴定,货物检验,检查货物- 3 -inspection of cargo GA or PA 海损(单独海损或共同海损)鉴定inspection on damaged cargo 货物残损检验installment insurance 分期付款保险Institute Cargo Clauses (ICC,I.C.C.) 协会货物(保险)条款insurability 可保性insurance 保险,保险费,保险金额insurance act 保险条例insurance against risk 保险insurance agent(s) 保险代理,保险代理人insurance amount 保险金额\保险额insurance applicant 投保人insurance assessor保险公估人insurance broker 保险经纪人insurance business保险企业\保险业insurance capacity 承保能力insurance certificate保险凭证\保险证书insurance claim 保险索赔insurance clause保险条款insurance commission保险佣金insurance company 保险公司insurance conditions 保险条件\保险契约约定条款insurance contract保险合同insurance corporation保险公司insurance coverage保险范围,保额insurance declaration sheet(bordereau) 保险申报单(明细表) insurance division 保险部insurance document 保险单据insurance expense保险费insurance fond 保险基金insurance industry 保险业insurance instruction 投保通知,投保须知insurance law保险法insurance on last survivor 长寿保险insurance period 保险期限insurance policy保险单\保单insurance premium保险费insurance proceeds 保险金(保险收入),保险赔偿金,保险赔款insurance rate保险费率表insurance securitization 保险证券化insurance slip投保单\投保申请书insurance subject 保险标的insurance treaty 保险合同insurance underwriter 保险承保人insurance value(insurance amount) 保险金额insurant 被保险人,受保人insure保险、投保、保证insured 被保险人insured amount保险金额insured loss保险损失insured property 参保物业Insured Value保险价值insurer保险人、保险公司,保险商insurer (underwriter) 承保人、保险人investment insurance 投资保险保险英语词汇J-L Jjettison 投弃- 4 -Llaw of insurance 保险法law of large numbers 大数法则leaflet说明书less exposed 损失可能性小letter of guarantee 保函,保证书liability 责任liability insurance 责任保险license bond 执照保险life assured 人寿保险投保人life expectancy 平均余命life fund 人寿保险基金life insurance 人寿保险life insurance actuary 人寿保险精算师life insurance reserve 人寿保险责任准备金life T able 生命表light damage 轻度破坏limits 投保限额line slips 分保条liquidity support 提供流动资金Lloyd 劳合社loading 附加费loading人寿保险附加费loss adjuster损失理算人loss occurrence 损失发生loss occurring basis 损失发生基础loss of profit 利损险loss participation 分担损失loss ratio 损失率loss ratio赔付率loss settlement 损失赔付保险英语词汇Mmail contractor承包商main risks主险maintenance 保证期malicious damage 恶意损害marine insurance 海上运输保险,水险marine losses海损medical insurance 医疗保险mortality tables 死亡率表(用于计算保险风险)multiple claim多次(重复)索赔multiple insurance 重复保险mutual insurance 相互保险mutual insurance company相互保险公司保险英语词汇NNatCat pooling 自然灾害共保natural catastrophe (NatCat)自然灾害natural premium 自然纯保费net retained lines净自留额net retained losses 损失净自赔额no profit commission 无纯益风险no-claims bonus无索偿奖金non-life 非寿险non-proportional reinsurance 非比例再保险notification 告知- 5 -篇三:保险单英语翻译练习(1)Put the insurance policy into Chinese:The People’s Insurance Company of ChinaORIGINALHead Office: BEIJING Established 1949MARINE CARGO TRANSPORTATION INSURANCE POLICYPolicy No.WH74/23002This policy of Insurance witnesses that the People’s Insurance Company of China (hereinafter called “The Company”),(万晨可、周雪雪、江琦、王心悦、杨琴、羊青)at the Request of CHINA IMPORT & EXPORT WUHAN CORP. OF STATE FARMS(hereinafter called the “insured”)and in consideration of the agreed premium being paid to the Company by the Insured,undertakes to insure the under-mentioned goods in transportation subject to the conditions of this policy as per the Clauses杜娟、杨星耀、陈朝莉、钟雅玮、杨朕T otalAmount Insured? U.S.DOLLARS NINETEEN THOUSAND THREE HUNDRED AND SIXTY ONLY (刘芬、严娇娇、刘梦尧)perconveyance S. S. “EASTWIND”V.331Slg. on or abt. ?AS PERB/L From WUHAN to PUSANConditionsCOVERING ALL RISKS AS PER OCEAN MARINE CARGO CLAUSES AND W AR RISKS CLAUSES(1/1/1981) OF PICC.赵静、刘小娟、黄敏、王艳萍、司婧祎)Claims, if any, payable on surrender of the First Original of the Policy together with other relevant documents.In the event of accident whereby loss or damage may result in a claim under this Policy immediate notice (李妍、孟佳媛)applying for survey must be given to the Company’s Agent as mentioned hereunder. HYOPSUNG SHIPPING CORPORATION12TH FLOOR YUCHANG BLUG? 25-2, 4-KA CHUNGANG-DONG, THE PEOPLE’S INSURANCE COMPANY OF CHINA(巩洁、王杰、向金凤、王浪珍、刘思)CHUNG;KU, PUSAN, KOREA P.O.OX 75 TEL:463 6551 TI 6553 WUHAN BRANCHClaim payable at? PUSAN, KOREA IN USDGeneral ManagerFAX: 027-******** TEL027-******** Date JUN. 06,2003(詹苏美、蒙勇、贺欢欢、李雅筠、牛雅娜、梁帅帅2。

养老保险制度中英文对照外文翻译文献

养老保险制度中英文对照外文翻译文献(文档含英文原文和中文翻译)翻译:重新引入代际均衡:波兰养老保险制度摘要:波兰于1999 年通过了新的养老金制度。

这种新的养老保险制度允许波兰,以减少退休金支出(占GDP 的百分比),而不是增加它-正如预计的经合组织其他大多数国家。

本文介绍了概念背景的新系统的设计。

新系统的长期目的是确保人口代际平衡,不论情况。

这需要稳定的国内生产总值的份额分配给整个退休一代。

传统的养老金制度的目的,相反,在稳定的份额人均国内生产总值退休人员。

在人口结构的变化观察到,在过去的一夫妻几十年,这历史性的尝试,以稳定为首占GDP 的比重为退休人员严重的财政问题和经济增长负外部性,如观察许多国家。

许多国家曾试图改革其养老金制度不同的方法来尝试解决这些不断增加的费用问题。

虽然波兰改革采用了其他地方应用技术,它的设计不同于典型的做法和教训,结果是有希望的所有经合组织国家。

本文介绍了这一理论和实际应用另一种方法,因此,新的波兰养老保险制度主要特点设计。

导言人口结构的转型与政策过于短视一起造成了严重的问题在全世界许多国家地区的养老金。

传统的要素养老金制度的设计包括对捐款的薄弱环节和利益缺乏超过该系统的成本控制。

这些因素列入养老保险制度导致爆炸的设计成本,造成了负增长的外部因素和导致失业率持续高企。

因此,养老金改革的追求现已在世界各地,特别是在欧洲的政策议程的顶部。

然而,很少有国家能够在引进根本性的改革面积到了这个时候养老金。

在这种情况下,改革的定义是至关重要的。

对于本文的目的,“改革”是指改变系统,以消除而不是仅仅在边缘玩的贡献率- 结构性效率低下和退休年龄调整为短期财政和系统的参数政治传统的养老金制度已被证明是低效率的提供与社会保障。

在同一时间试图治愈这些系统阻碍了缺乏共识什么可以取代传统的制度。

讨论这问题涉及混乱的思想背景下产生的讨论参与者,以及从这些概念作为过度使用“支付即用即付”与“资金”,即“公” 与“私”,而在同一时间,忽略了数重要的经济问题。

常用保险翻译

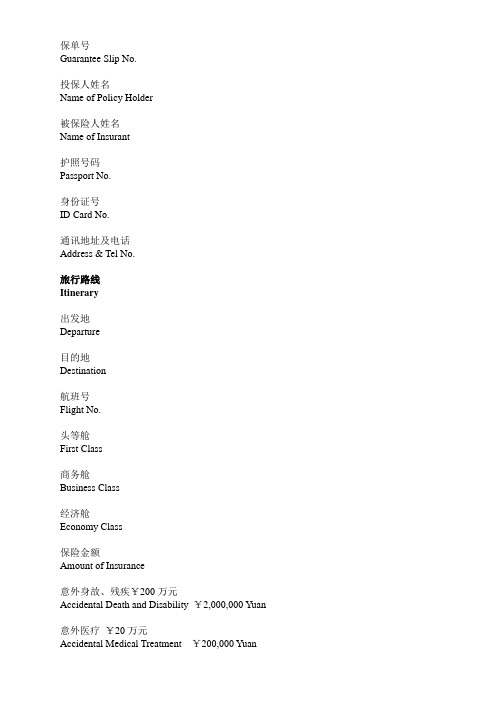

保单号Guarantee Slip No.投保人姓名Name of Policy Holder被保险人姓名Name of Insurant护照号码Passport No.身份证号ID Card No.通讯地址及电话Address & Tel No.旅行路线Itinerary出发地Departure目的地Destination航班号Flight No.头等舱First Class商务舱Business Class经济舱Economy Class保险金额Amount of Insurance意外身故、残疾¥200万元Accidental Death and Disability ¥2,000,000 Yuan意外医疗¥20万元Accidental Medical Treatment ¥200,000 Yuan意外住院津贴¥200元/日Accidental Hospitalization Benefit ¥200 Yuan/day保险费Insurance Premium保险期间:壹年内一次往返有效。

Insurance Period: It is valid for one trip within one year.特别约定:乘客以有效行程单上列明的出境航程改期或签转航班继续有效(最长有效期一年),非因乘客本人原因造成的机票签转或转乘下一航班时继续有效。

Special Stipulation: Emigration flight modified date or flight signed for extension listed on effective trip sheet by passenger goes on taking effect (maximum effective period is one year). Ticket signed for extension or transfer to take the next flight due to no reason of passenger goes on taking effect.保险责任:自踏入出发地航班舱门时起,至踏出目的地航班舱门时止,被保险人在乘坐本保单上列明的民航班机时,因意外伤害事故导致180日内身故,或下落不明、经人民法院宣告死亡的,本公司按保险金额给付身故保险金。

陆上货物运输保险合同双语范本

陆上货物运输保险合同双语范本陆上货物运输保险合同(中英双语范本)LC No: xxxxxxxxxxxxx保险合同编号:xxxxxxxxxxxxxInsured: xxxxxxxxxxxx被保险人姓名:xxxxxxxxxxxxxInsurer: xxxxxxxxxxxx保险人姓名:xxxxxxxxxxxxxEffective Date: xxxxxxxxxxxx生效日期:xxxxxxxxxxxxx1. 险种及保额:货物运输保险风险:所有直接由意外事故及交通意外的破碎、丢失或受损所引起的损失或损害。

保额:本保险的保险金额为xxxxxxxxxxx人民币。

2. 保险期限:本保险自指定日期起至指定日期止。

3. 责任责任:本保险保证在保险期限内,由保险人承担本保单的范围内货物运输途中发生的意外事故造成的损失或损害。

然而,本保险不包括以下情况造成的损失或损害:-牢固固定在运输工具上的物品-货物的浸泡、受潮或发霉-损坏或灭失的包装件-货物的不合适堆放或存放不当所引起的损失4. 赔偿申请:在发生保险事故后,被保险人应及时向保险人提出赔偿申请,提供详细的账单、损失清单、损坏货物的照片等证据。

保险人将在接收到完整的赔偿申请后,审查并在合理时间内进行赔偿。

5. 保险费用:被保险人应按照约定的金额和支付方式向保险人支付保险费用。

6. 生效与终止:本保险合同自生效日期起生效,至指定日期止。

然而,双方均有权在提前通知对方的情况下终止本保险合同。

本保险合同以中文和英文书写,两种文字具有同等效力。

任何有关本保险合同的争议应通过友好协商解决。

如果争议不能解决,应提交至被保险人所属地的仲裁机构进行仲裁。

被保险人签名:___________________日期:___________________保险人签名:___________________日期:___________________。

最新保险单的中英文范例

W.பைடு நூலகம்A.

War Risk

Claims, if any, payable on surrender of this policy together with other relevant documents.

In the event of accident whereby loss or damage may result in a claim under this policy immediate notice applying for survey must be given to the Company’s Agent as mentioned hereunder:

Marks & Nos. No. of Package Quantity Description of Goods Amount Insured

SOUTHAMPTON25 cartons Porcelain Figures US$ 2035.00

JSS1/25

Total Amount Insured: US Dollars Two Thousand and Thirty Five only, Premium…..Rate…..per conveyance S. S. WULIN Slg. On or abt. 25 April 1986 From Whompoa to Southampon

保险单的中英文范例

保险单(Insurance Policy)

保险人和被保险人之间成立保险合同的凭证。下列为货物保险单。在CIF合同中,保险单是卖方必须向买方提供的单据之一。

THE PEOPLE’S INSURANCE COMPANY OF CHINA

产品质量保证保险条款参考(中英双语)

产品质量保证保险条款Clauses of Product Quality Bond Insurance总则General Provisions第一条为促进产品生产者、销售者重视和提高产品质量,维护企业产品声誉,保护消费者的合法权益,特开办本保险。

Clause I This insurance is specially set up to promote producers and distributors to pay attention to and improve product quality, so as to maintain the reputation of products, protect the legal rights and interest of consumers.第二条凡经国家产品质量检验机构检验合格、批准生产和销售的产品,生产和销售企业(以下称被保证人)都可以按本条款规定向本公司投保。

Clause II All the products that have been accredited and authorized by Product Quality Inspection Unit to be manufactured and freely sold on the market, producers as well as distributors, hereafter referred to as the warrantee, can apply for insurance to our company.保险责任Insurance Liabilities第三条在保险期限内,被保证人对其当年生产销售的产品,依照《中华人民共和国产品质量法》。

对由下列原因产生的,应由其承担的修理、更换、退货责任,本公司对被保证人负责赔偿80%的损失,累计最高赔偿金额在保险金额10%以内赔付,具体赔偿限额在特别约定中列明。

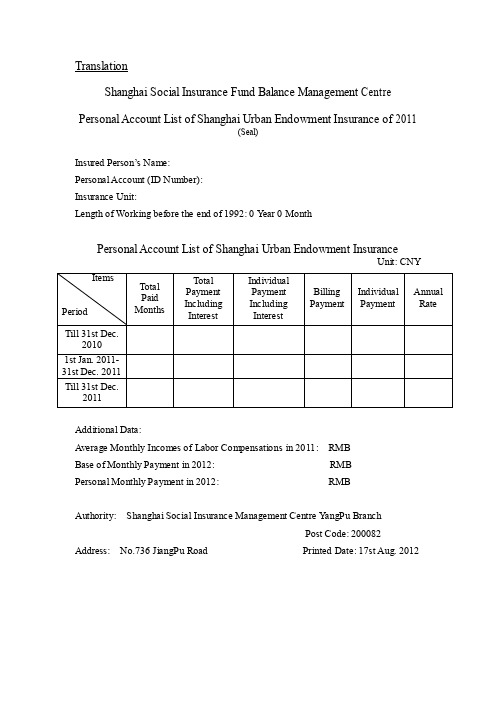

【最新公文】上海养老保险个人权益记录单英文翻译模板

TranslationShanghai Social Insurance Fund Balance Management Centre Personal Account List of Shanghai Urban Endowment Insurance of 2011(Seal)Insured Person’s Name:Personal Account (ID Number):Insurance Unit:Length of Working before the end of 1992: 0 Y ear 0 MonthPersonal Account List of Shanghai Urban Endowment InsuranceUnit: CNYAdditional Data:Average Monthly Incomes of Labor Compensations in 2011: RMBBase of Monthly Payment in 2012: RMBPersonal Monthly Payment in 2012: RMBAuthority: Shanghai Social Insurance Management Centre Y angPu BranchPost Code: 200082 Address: No.736 JiangPu Road Printed Date: 17st Aug. 2012Shanghai Social Insurance Fund Balance Management Centre Personal Account List of Shanghai Urban Endowment Insurance of 2012(Seal)Insured Person’s Name:Personal Account (ID Number):Insurance Unit:Length of Working before the end of 1992: 0 Y ear 0 MonthPersonal Account List of Shanghai Urban Endowment InsuranceUnit: CNYAdditional Data:1, Average Monthly Incomes of Labor Compensations in 2012: RMB2, Base of Monthly Payment in 2013: RMB3, Personal Monthly Payment in 2013: RMB4, Overdue Payment from 1st Jan. 2012- 31st Dec. 2012:Overdue Month: --- Overdue Amount: ---Authority: Shanghai Social Insurance Management Centre Y angPu BranchPost Code: 200082 Address: No.736 JiangPu Road Printed Date: 31st Jul. 2013以下是附加文档,不需要的朋友下载后删除,谢谢高二班主任教学工作总结5篇高二班主任工作总结1本学期,我担任高二(14)班班主任。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

综合责任险

责任范围:

本综合责任险涵盖由第三方在投保人的工作场地而引发的与投保人利益相关,在本保险中细化的各项法律责任。

保险支付:-

关于损失及投保人的成本和支出的法律责任:

a.任何人的人身意外伤害;

b.财产的意外损害;

前提条件:

●事故发生在所约定的工作生产地点,和约定的时期内。

●在保险终止前的12个月内采取正规的法律手段和途径。

责任限度:

本保险之下,有两种责任的限度:

a.关于任何事故或意外意外的保险责任(AOA);

b.关于保险期内的任何年份,任何时间内的保险责任(AOY)。

标准除外项目:

●雇佣工人的赔偿;

●投保人涉及专业性的责任;

●分包商的责任;

●战争,恐怖主义活动,核反应而产生的后果;

●惩罚和罚款产生的相应的损失。

投保人须知:

如有责任界限和自负额,按照双方协定的计划执行。

1.保险所规定的特例情况,条款和各条件是针对投保方和承保方所

制定的。

2.如果因意外情况而有可能进行索赔,投保方应该:

a.在第一时间以正式的书面信函的形式通报承保方,并且将索赔上报。

b.提供承保方所需的信息和协助,以便于办理索赔手续。

综合责任险

作为一家联合保险公司,本保险公司受公司章程的约束。

沙印保险公司(以下简称“公司”)会将年度保险经营的全部或者部分盈余分配给投保方。

具体的分配金额,时间和资格将会根据公司的规章制度来决定,或者由公司董事会来决定安置。

(此段有异议,不建议参考。

)由投保方出具或宣布的书面协议或者信息将会基于并且成为本保险协议的一部分。

对投保方的损害赔偿

基于投保方缴纳的保费,承保方有义务根据法律及其相关条款,特例及其他条件针对投保方所产生的损失和其他费用而进行赔付,具体包括:

a.人身意外伤害;

b.财产意外受损。

在保期内,如在协定的工作地点内发生了意外事故,一切按照约定的条款,诉诸于正规的法律途径来解决,在保期内或在保险结束前12个月内进行损害的索赔。

由同一原因引发的一个或者一系列的事故,承保方将根据协议的规定而进行赔付,不能超出协议规定的损害赔偿的具体范围和期限。

协定的事故具体的损害赔偿保险责任包括:

a.投保方进行索赔和申诉所产生的相关成本和费用;

b.同承保方书面的协定中所涉及以及包括的成本及费用。

针对其他人员的损害赔偿:

针对以下保险条款,承保方也会进行损害赔偿:

1.对于投保方明确给予可以获得保险赔付资格的直接合作伙伴或者

雇员,承保方可以在其申请索赔后进行赔付。

2.如发生人员意外死亡的情况,其个人法律代表可以根据本保险的

条例获得相关的损害赔偿。

司法条款:

本损害赔偿条例是诉诸于由沙特阿拉伯法庭来鉴定和实现的。

其他地点不能够强制进行损害赔偿的鉴定和相关命令。

例外情况

承保方对一下特殊情况将不承担责任:

1.双方基于道义上的,但非协议条款所规定的责任;

2.与投保方签订过雇佣合同的服务或是学徒身份的人员,由于从事

的职业的原因而死亡,受伤或者生病的情况;

3.属于投保方所有,及其管辖、看管范围的财产,人员破坏或者受

损的情况;

4.有损害或者事故引发的投保方的雇员或者其他机构的财产损失;

5.由投保方或能够代表投保方的相关人员的有意的行为或者疏忽而

造成的死亡,伤病,损失或者毁坏,或是投保方能够预测到的可能出现此种行为或者疏忽的情况;

6.有以下情况引发的死亡,伤病,损失或者毁坏:

a.正处于动物,机动车辆,火车,飞机,气垫船,汽艇,拖车,电梯,自动扶梯,吊车等属于投保方所拥有,或是能够代表

投保方的物品或者设备之内。

b.处于机动车辆,摩托车(自行车除外),火车飞机,气垫船,汽艇或者拖车的装卸过程中。

c.锅炉或者其他压力设备的爆裂。

d.刺激气体,烟尘,毒气,空气和水污染,地下水或者噪声。

e.投保方进行的货品的销售,供给,维修,检测工程。

f.涉及由投保方或其代表人给出的处理规范及意见的专业性责任。

g.投保人,其雇员或者及其其他机构的分包商。

h.对地面建筑或者其他财产的薄弱处进行振动或者拆除。

7.由以下情况而引起的后果:

a.战争,侵略活动,外国军队的活动,敌对势力或好战分子的活动(无论宣布战争与否),内战,叛乱,内部骚乱,大规

模人群引发的骚乱,军队造反,叛变,谋反,革命或篡权,

军事法,政府或者其他政权要求的征用或国有化等引起的财

产毁坏或损失。

b.代表或与某组织有联系的一人或多人以暴力为途径,为达到某种政治目的而将民众或部分民众置于恐怖之中的恐怖主

义活动。

在任何诉讼行为中,当承保人声称根据保险例外条款,承保人认为可能适用于本保单或保单延伸下的任何财产损失、人身伤害或相关责任,不在理赔之列时,投保人有义务去证明这些财产损失和人身伤害等属于赔付之列。

最主要例外应适用于本保单或保单下的延伸,不管这些延伸是产生在这一主要例外之前或之后下列情况产生的后果。

8.以下情况而产生的任何后果:

c.由核燃料或者核垃圾燃烧产生的电子辐射或者放射性污染,此特例要求核分裂反应应当包括独立支撑系统。

d.核武器材料。

9.罚款,惩罚性损坏或自然引发的损失。

条款

1.保险单和清单将当做一份合同一起读。

任何单词或表达的特定含

义已附在本保单或清单中,并且不管出现在什么地方,含义相同。

2.只有在投保人的理赔符合本保单下的条款下,承保人才履行赔付

责任。

索赔陈述和建议回复的真实性以及提供给承保人的风险信息,将是承保人付款前要求的先决条件。

3.如果投保物的风险出现变动,投保人必须以书面方式立刻通知承

保人,从而进一步对保险费用做相应的调整。

4.投保方必须自费采取合理的预防措施来防止事故的发生,保护保

养好标的物,并且遵守政府机构制定的法律法规。

保险代理人可以在合理次数内检查标的物。

5.倘若发生意外,出现本保单下的索赔,投保方应做出以下行为:

a.立刻以书面方式通知承保人,费用自理,并向承保人提供所有相关信息和支持,从而使承保人能对索赔进行赔付或抗辩或提起诉讼。

b.立刻以书面形式通知承保人关于将发生的起诉或者非常重要的调查,以便承保人对此有所了解。

c.投保方在收到任何形式的索赔信后,须转交给承保人。

d.采取合理措施最大程度的减少损失。

e.在承保人没有书面同意下,对于任何索赔,采取不协商,不赔付或不驳回的办法。

6.倘若投保方对本保单下的一项或多项索赔负有过失,承保人有权

以投保方的名义做出以下行为:

7.对任何索赔和法律诉讼的行为、控制和仲裁,承担责任。

8.为了追讨赔偿或者免受任何个人或多人的索赔,保护自身利益,

可以自费提起诉讼。

9.如果本保单下的标的物发生索赔时,投保人或其代理人对该标的

物还投保了其他保险,涵盖了同样的人身伤亡、疾病、财产损失的全部或部分,那么承保人将不负责赔付或者按比例只赔付一部分。

10.在一项或多项索赔解决后,承保人可以随时对投保人进行赔付(须

扣去已付的赔偿金额)。

11.承保人可以根据投保方提供的地址,通过以电传、传真、挂号信

的方式,提前七天发送通知给投保方,从而取消保单。

承保人应在维护投保方权益的基础上,在没有出现人身伤亡、疾病、财产损失等前提下,可以在保险期限内返还给投保方一定比例的保险费。

12.如果保险费是基于投保人对保险额的全部或部分估计,投保方必

须准确记录所有相关细节,以便承保人随时可以检查这些记录。

在保险到期一个月内,投保方必须提供给承保人要求的这些详细信息。

从而使该期的保险费在规定的最低保险额上做相应的调整。

13.任何缘于本保单或与本保单相关争论的解决办法,将参照本保险

公司Co-Operative Insurance Companies 操作法的应用条款、执行规则和其他沙特法律法规及其相应补充条款。