CFA一级笔记-第八部分 固定收益证券

CFA一级知识点完全总结

CFA一级知识点完全总结1.伦敦同业拆借市场(LIBOR):LIBOR是指银行之间短期借贷利率,是全球最重要的金融测量指标之一2.金融市场与市场参与者:掌握各种金融市场和市场参与者的特点和功能,包括股票市场、债券市场、货币市场、商品市场等。

3.财务报表分析:学习如何解析财务报表,包括资产负债表、利润表和现金流量表等。

4.企业财务管理:了解企业财务决策的原则和方法,包括资本预算、财务风险管理、股权和债权融资等。

5.市场和投资组合理论:掌握投资组合理论,包括投资组合构建、资本市场线、评估投资回报等。

6.证券分析与估值:学习企业估值方法和证券投资分析方法,包括技术分析和基本面分析等。

7.固定收益证券:了解债券的基本知识,包括债券定价、债券投资组合管理技巧等。

8.衍生品:学习如何分析和定价衍生品,包括期货、期权和互换等。

9.量化方法:熟悉统计学和数学方法在金融领域的应用,包括回归分析、概率分布、假设检验等。

10.宏观经济学:了解宏观经济学的基本原理和政策,包括经济增长、通货膨胀、货币供应等。

11.伦理与职业标准:了解金融行业的道德标准和职业操守,包括职业责任、尽职调查等。

此外,CFA一级考试的考试形式包括两种类型的题目:多项选择题和构建型题目。

多项选择题主要考察对知识的理解和应用,而构建型题目则要求候选人通过阐述问题、分析情况和展示解决方案来回答问题。

为了成功通过CFA一级考试,考生需要充分准备,掌握所有相关的知识点,并通过练习题和模拟考试来提高解题能力。

此外,良好的时间管理和复习计划也是成功的关键。

以上是CFA一级考试的主要知识点总结。

请考生根据实际情况有针对性地复习相关知识,并加以练习和实践,以便在考试中取得良好的成绩。

cfa一级十科笔记

cfa一级十科笔记CFA一级考试是金融行业中非常重要的职业资格认证,涵盖了广泛的金融知识领域。

下面是关于CFA一级考试十科的笔记,以帮助你更好地准备考试。

1. 伦理与专业标准(Ethics and Professional Standards):了解职业道德和行业规范的重要性。

理解与客户、公司和市场参与者之间的关系。

掌握投资专业人士应遵循的道德准则。

2. 数量方法(Quantitative Methods):熟悉基本的数学和统计概念。

掌握概率论和假设检验的基本原理。

理解回归分析和时间序列分析的基本概念。

3. 经济学(Economics):理解宏观经济和微观经济的基本原理。

掌握货币政策、财政政策和国际贸易的影响。

理解经济指标和金融市场之间的关系。

4. 金融报表分析(Financial Reporting and Analysis):理解财务报表的结构和内容。

掌握财务比率分析和财务报表的解读。

熟悉资产负债表、利润表和现金流量表之间的关系。

5. 公司金融(Corporate Finance):理解资本预算和资本结构的基本原理。

掌握投资决策和融资决策的方法。

熟悉公司治理和股权结构的影响。

6. 证券投资(Equity Investments):理解股票市场和股票投资的基本原理。

掌握股票估值和投资组合管理的方法。

熟悉股票投资的风险管理和绩效评估。

7. 固定收益投资(Fixed Income Investments):理解债券市场和债券投资的基本原理。

掌握债券估值和债券组合管理的方法。

熟悉利率风险和信用风险的评估和管理。

8. 衍生品投资(Derivative Investments):理解衍生品市场和衍生品投资的基本原理。

掌握期权、期货和其他衍生品的估值和交易策略。

熟悉衍生品投资的风险管理和绩效评估。

9. 另类投资(Alternative Investments):理解另类投资市场和另类投资的基本原理。

掌握房地产、私募股权和大宗商品等另类投资的特点和风险。

cfa一级笔记

cfa一级笔记(实用版)目录1.CFA 一级考试简介2.CFA 一级笔记的重要性3.如何高效利用 CFA 一级笔记4.CFA 一级笔记的具体内容5.结论正文1.CFA 一级考试简介CFA(Chartered Financial Analyst)一级考试是 CFA 认证考试的第一阶段。

该考试旨在为考生提供一个全面的金融知识体系,帮助他们在投资工具、公司金融、经济学、财务报表分析等领域建立坚实的基础。

通过 CFA 一级考试是迈向成为金融分析师、投资经理等职业的重要一步。

2.CFA 一级笔记的重要性CFA 一级笔记对于备考至关重要,因为它们可以帮助考生整理和梳理繁多的知识点,使学习过程更加有条理。

笔记还可以辅助考生进行复习,提高复习效率。

此外,良好的笔记还有助于考生在考试期间快速找到关键信息,从而提高答题速度和准确性。

3.如何高效利用 CFA 一级笔记(1)整理知识点:在学习过程中,将重要的概念、公式和方法整理成笔记,方便后续复习。

(2)梳理逻辑:按照课程模块,梳理各知识点之间的逻辑关系,帮助自己建立知识体系。

(3)对比分析:对比各知识点的异同,加深理解,提高记忆效果。

(4)总结归纳:在学习的过程中,不断总结和归纳自己的理解和心得,形成自己的观点。

(5)定期复习:按照艾宾浩斯遗忘曲线进行复习,提高记忆效果。

4.CFA 一级笔记的具体内容CFA 一级笔记应包括以下几个方面的内容:(1)投资工具:包括股票、债券、衍生品等金融产品的基本概念、特点和定价方法。

(2)公司金融:涉及资本预算、财务报表分析、现金流量预测等方面的知识。

(3)经济学:包括宏观经济学和微观经济学的基本原理和应用。

(4)财务报表分析:探讨财务报表的编制方法、财务比率分析、现金流量分析等技术。

5.结论CFA 一级笔记是备考过程中重要的学习工具,可以帮助考生梳理知识点、提高复习效率。

要想在 CFA 一级考试中取得好成绩,考生需要掌握笔记的整理方法和技巧,并定期进行复习。

cfa一级考试题库答案

cfa一级考试题库答案

1. 以下哪项是CFA一级考试中关于财务报表分析的主要内容?

A. 理解财务报表的结构和内容

B. 识别和分析财务报表中的异常情况

C. 预测未来财务报表的趋势

D. 所有以上选项

正确答案:D. 所有以上选项

2. 在CFA一级考试中,关于投资组合管理的哪项说法是正确的?

A. 投资组合管理只关注资产配置

B. 投资组合管理包括资产配置、选择证券和风险管理

C. 投资组合管理与市场时机无关

D. 投资组合管理只涉及股票投资

正确答案:B. 投资组合管理包括资产配置、选择证券和风险管理

3. 在CFA一级考试中,关于固定收益证券的以下哪项说法是错误的?

A. 固定收益证券的利息支付是固定的

B. 固定收益证券的价格与市场利率呈负相关

C. 固定收益证券的风险高于股票

D. 固定收益证券的到期收益率是固定的

正确答案:C. 固定收益证券的风险高于股票

4. 在CFA一级考试中,关于衍生品的以下哪项说法是正确的?

A. 衍生品的价值完全独立于标的资产

B. 衍生品可以用来对冲风险

C. 衍生品只能用于投机

D. 衍生品不能用于投资组合管理

正确答案:B. 衍生品可以用来对冲风险

5. 在CFA一级考试中,关于经济学的以下哪项说法是错误的?

A. 经济学研究资源的分配和利用

B. 宏观经济学关注整体经济的运行

C. 微观经济学研究个体经济单位的行为

D. 经济学只关注市场均衡状态

正确答案:D. 经济学只关注市场均衡状态

结束语:以上是CFA一级考试题库中的一些典型题目及其答案,希望能够帮助考生更好地准备考试。

CFA考试固定收益:资产证券化

CFA考试固定收益:资产证券化考点解析对于很多想参加CFA考试的同学来说,对于CFA的考试内容还不是很了解。

我就为大家分享一下CFA考试的考试科目:1、道德与职业行为标准(Ethics and Professional Standards)2、定量分析(Quantitative)3、经济学(Economics)4、财务报表分析(Financial Statement Analysis)5、公司理财(Corporate Finance)6、权益投资(Equity Investments)7、固定收益投资(Fixed Income)8、衍生工具(Derivatives)9、其他类投资(Alternative Investments)10、投资组合管理(Portfolio Management)固定收益投资考试中,资产证券化(securitization)是难点和重点。

资产证券化,就是指以基础资产未来所产生的现金流为偿付支持,通过结构化设计进行信用增级,在此基础上发行资产支持证券(Asset-backed Securities, ABS)的过程。

资产证券化流程一次完整的证券化融资的基本流程是:发起人(originator)将证券化资产出售给一家特殊目的机构(Special Purpose Vehicle, SPV),或者由SPV主动购买可证券化的资产,然后SPV将这些资产汇集成资产池(assets pool),再以该资产池所产生的现金流为支撑在金融市场上发行有价证券融资,最后用资产池产生的现金流来清偿所发行的有价证券。

可证券化的资产最大的特点是可以产生持续稳定的现金流,包括:居民住房抵押贷款、商业住房抵押贷款、汽车贷款、应收账款等等。

资产支持证券的投资者可以获得持续稳定的现金流,所以资产支持证券本质上就是一种结构化的债券。

居民住房抵押贷款居民住房抵押贷款(residential mortgage loans)是资产支持证券中最常见的一种基础资产,所以这里先来介绍一下居民住房抵押贷款的一些知识。

CFA一级:固定收益证券框架

CFA一级:固定收益证券框架许多考生感到CFA一级的固定收益证券(Fixed Income Analysis)考点较多较散,难以复习。

其实,固定收益证券的内容大致可以分为三大部分。

一、债券的合同条款1、基本条款:包括债券的maturity,par value,coupon rate。

这三条决定了债券未来的现金流,也就是债券定价模型的分子。

2、基本条款的衍生:由maturity的不同产生bill,notes,bond。

由coupon rate的不同产生Zero-coupon bond,Floating-rate bond等。

3、嵌入期权条款:包括债券发行人的权力(callable,prepayment等)和债券持有人的权力(puttable,convertible 等)。

4、嵌入期权条款的衍生:callable bond (MBS),puttable bond。

5、债券的发行人:根据发行人的不同,分为国债、机构债券、市政债券、企业债券等。

二、债券的风险1、Interest rate risk:yield curve平行移动为interest rate risk,非平行移动为Yield curve risk。

2、Yield curve risk:yield curve非平行移动为yield curve risk。

3、Call risk (Prepayment risk):callable bond利率下降有call risk。

4、Reinvestment risk:reinvestment risk与interest rate risk反相关。

5、Credit risk:包括Default risk,Credit spread risk,Downgrade risk。

外部信用增强的三个方法:第三方担保、银行信用证、债券保险。

6、Volatility risk:只有含有嵌入期权条款的债券(callable,puttable)才有volatility risk。

CFA一级笔记-第八部分 固定收益证券

CFA一级考试知识点第八部分固定收益证券债券五类主要发行人超国家组织supranational organizations,收回贷款和成员国股金还款主权(国家)政府sovereign/national governments,税收、印钞还款非主权(地方)政府non-sovereign/local governments(美国各州),地方税收、融资、收费。

准政府机构quasi-governments entities(房利美、房地美)公司(金融机构、非金融机构)经营现金流还款Maturity到期时间、tenor剩余到期时间小于一年是货币市场证券、大于一年是资本市场证券、没有明确到期时间是永续债券。

计算票息需要考虑付息频率,未明确的默认半年一次付息。

双币种债券dual-currency bonds支付票息时用A货币,支付本金时用B货币。

外汇期权债券currency option bongds给予投资人选择权,可以选择本金或利息币种。

本金偿还形式子弹型债券bullet bond,本金在最后支付。

也称为plain vanilla bond(香草计划债券)摊销性债券amortizing bond,分为完全摊销和部分摊销。

偿债基金条款sinking found provision,也是提前收回本金的方式,债券发行方在存续期间定期提前偿还部分本金,例如每年偿还本金初始发行额的6%。

票息支付形式固定票息债券fixed-rate coupon bonds,零息债券会折价发行,面值与发行价之差就是利息,零息债券也称为纯贴现债券pure discount bond。

梯升债券step – up coupon bonds票息上升递延债券deferred coupon bonds/split coupon bonds,期初几年不支付,后期才开始支付票息。

(前期资金紧张或研发型项目)实物支持债券payment-in-kind/PIK coupon bonds票息不是现金,而是实物。

cfa一级考试各科目介绍及重点解析

CFA一级考试各科目介绍及重点解析在CFA考试过程当中,许多考生都在自学的过程中走过些许弯路。

对往年的重点着重观望,对教材中仅有十几页的科目内容可能只是扫视几遍便匆匆翻篇。

为那些常年标着五角星的CFA重点刻苦钻研。

这样的备考方法并没有错,然而随着这几年CFA考试协会的出题更新,越来越多的考生反映,在实际考试当中会出现作为边角边料的小细节知识点出现。

偶偶考生们会此类题目打住考试的节奏,满脑袋转悠也只有稍许浅薄的印象。

针对历年变化的CFA考试,高顿财经CFA研究中心为考生们整理了在CFA一级考试中,经常会考到的一些重难点。

希望考生可以通过此类难点的归纳,调整自己的备考计划。

CFA一级考试中十大科目考试重点介绍:职业伦理:提高从业人员的职业和道德素养,特别是国际上对受托人的责任的要求,降低了公司内部人员职业违规方面的风险,同时提升公司内部的整体职业素养,由此提高公司整体的管治。

数量分析:定量分析就是以数量工具测算投资组合关联性,概率统计,为设定合理理性的投资规划提供技术支撑。

在一级二级考试中是考试占比比较大的考试科目,考察金融分析中的一些常用的计算方法。

经济学:经济学课程以经典宏观、微观经济学内容讲解弹性、价格曲线、生产者剩余、消费者剩余、垄断和市场形态,宏观金融政策和中央银行等知识,让考生了解经济运行的宏观和微观经济知识。

财务报表分析:财务报表是一级二级的考试重点,内容涉及三大会计报表,现金流量测控,养老会计、管理会计、税收规避FACC 等会计术语,考试难度不大,并且现在的考核方式更加灵活。

一级二级中财务报表是重点科目,占比考试20%左右的权重,权重较大。

公司理财:公司理财详细的介绍了资本的成本,使公司规划出最合适的资本结构,来获得资本的最优收益。

在制定资本预算时,可做出正确的现金流量估计和风险分析,从而作出正确的决定。

在决定股利政策时,充分了解其中的资讯和意义。

深入地了解如何实现公司融资结构与投资结构的最优化。

第八固定收益证券的价值分析文稿演示

第八固定收益证券的价值分析文稿演示引言:固定收益证券是投资者常用的一种投资工具,通过购买债券或其他固定收益证券来获取固定的利息或利息和本金。

本文将通过对固定收益证券的价值分析,帮助投资者更好地理解固定收益证券的特点和投资价值。

一、固定收益证券的种类及特点1.债券:债券是固定收益证券中最常见的一种,它是发行者募集资金的一种方式,投资者通过购买债券来提供资金。

债券的特点是有固定的利息和本金偿还期限。

债券通常有高信用评级,风险较低。

2.优先股:优先股是一种混合类型证券,具有固定的股息,在分配利润和资产清算时优先于普通股,但优先股不负有股票分红的权利。

优先股通常具有较长的固定收益期限。

3.可转换债券:可转换债券是一种特殊的债券,可以在一定条件下转换为普通股票,具有较高的灵活性。

二、固定收益证券的风险和收益1.风险:固定收益证券通常具有较低的风险,尤其是高信用评级的债券。

但不同种类的固定收益证券存在的风险因素不同,例如债券的违约风险、利率风险和市场风险等。

2.收益:固定收益证券的收益主要来自投资者持有证券期间所获得的固定利息。

收益率通常反映了证券的风险水平,收益率高的证券通常具有较高的风险。

三、固定收益证券的价值分析方法1.公司基本面分析:通过分析发行者的财务状况、行业前景等基本面因素,来评估固定收益证券的投资价值。

例如,对债券进行信用评级,评估发行公司的偿债能力。

2.利率分析:利率是固定收益证券的重要参考因素。

当利率上升时,固定利率证券的价值通常下降,因为持有固定利率证券的投资者放弃了其他投资机会。

投资者可以通过分析利率走势来预测固定收益证券的价格变动。

3.期限分析:固定收益证券的期限也会影响其价格和价值。

通常情况下,持有期限较长的债券价格波动较大,因为投资者需承担更长时间的风险。

投资者可以通过分析债券到期日来评估其投资价值。

四、固定收益证券的投资策略1.利用利差:不同发行者发行的债券利率可能存在差异,投资者可以通过选择利差较大的债券来获取更高的收益。

固定收益证券(一些需要背的知识点)

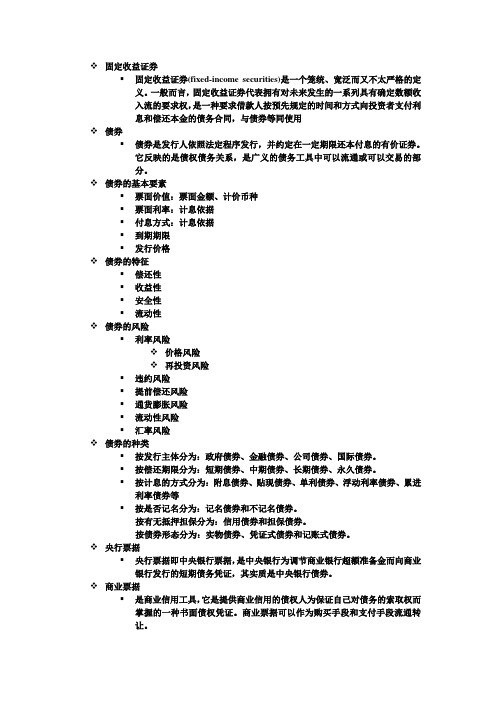

固定收益证券▪固定收益证券(fixed-income securities)是一个笼统、宽泛而又不太严格的定义。

一般而言,固定收益证券代表拥有对未来发生的一系列具有确定数额收入流的要求权,是一种要求借款人按预先规定的时间和方式向投资者支付利息和偿还本金的债务合同,与债券等同使用债券▪债券是发行人依照法定程序发行,并约定在一定期限还本付息的有价证券。

它反映的是债权债务关系,是广义的债务工具中可以流通或可以交易的部分。

债券的基本要素▪票面价值:票面金额、计价币种▪票面利率:计息依据▪付息方式:计息依据▪到期期限▪发行价格债券的特征▪偿还性▪收益性▪安全性▪流动性债券的风险▪利率风险价格风险再投资风险▪违约风险▪提前偿还风险▪通货膨胀风险▪流动性风险▪汇率风险债券的种类▪按发行主体分为:政府债券、金融债券、公司债券、国际债券。

▪按偿还期限分为:短期债券、中期债券、长期债券、永久债券。

▪按计息的方式分为:附息债券、贴现债券、单利债券、浮动利率债券、累进利率债券等▪按是否记名分为:记名债券和不记名债券。

按有无抵押担保分为:信用债券和担保债券。

按债券形态分为:实物债券、凭证式债券和记账式债券。

央行票据▪央行票据即中央银行票据,是中央银行为调节商业银行超额准备金而向商业银行发行的短期债务凭证,其实质是中央银行债券。

商业票据▪是商业信用工具,它是提供商业信用的债权人为保证自己对债务的索取权而掌握的一种书面债权凭证。

商业票据可以作为购买手段和支付手段流通转让。

▪当票据的持有者在票据未到偿还期而又需要资金时,票据持有人就可以背书,然后把它以一定的价格转让给金融机构,获得现款,这种活动称作票据贴现。

短期融资券▪短期融资券简称融资券,是指企业依照有关规定在银行间债券市场发行和交易并约定在一定期限内还本付息的有价证券。

▪发行市场化▪备案制债券回购▪债券回购是指债券持有人(卖方)在将债券卖给债券购买人(买方)时,买卖双方约定在将来某一日期以约定的价格,由卖方向买方买回相等数量的同品种债券的交易行为。

CFA一级学习重点记录

CFA一级学习重点记录Q uantitative methodP99、P253Continuous compounding: EAR=eRcc-1Continuous compounding of return (Rcc) = ln(1+EAR)P141:Time-weighted rate of return(分期计算收益率,然后相乘再开根,与投入资金的时间无关)Money-weighted rate of return(IRR)P143:Bank discount yield = D/F * 360/t 即把折扣率单利年化HPY holding period yieldEAY effective annual yield = (1+HPY)365/t – 1 即把HPY按照复利年化(365)MMY money market yield(CD equivalent yield )= HPY * 360/t 即把HPY单利年化(360)BEY bond-equivalent yield = HPY * 365 / t 即把HPY按照单利年化(365): (1 + BEY/2)2 = 1 + EAY切比雪夫不等式:在k standard deviation 以内的概率至少有1-1/k2 (k>1)夏普比率Sharpe ratio = ( portfolio return – risk-free return )/standard deviation of portfolio returns条件概率P(I|O) = P(O|I)*P(I) / P(O)置信区间:Two-tailed : 90% ? 1.65 , 95% ? 1.96 , 99% ? 2.58 .One-tailed : 90% ? 1.28 , 95% ? 1.65 , 99% ? 2.33 .SFR ratio SFR比率越大,越不可能小于threshold level ? P250 中央极限定理:Standard error of the sample mean isReliability factor is 置信区间的上界如90% (a=10%)? Z=1.65 , 95% (a=5%)? Z=1.96 , 99% ? 2.58 .假设检验:Type I error: H0 is true but reject it. = significance levelType II error: H0 is false but fail to reject it. Power of the test = 1 – P (Type II error)差异假设检验:正态分布、两变量有关联,用paired comparisons test (difference 的均值检验)正态分布、方差未知、方差可相等可不相等,两变量相互独立时,用t检验。

CFA考试一四大主要内容是:FSA、股权投资、固定收益、衍生品

CFA考试一级四大主要内容是:FSA、股权投资、固定收益、衍生品CFA考试一级四大主要内容是:FSA、股权投资、固定收益、衍生品。

如果考生在这四部分的正确率达到70%以上的话,通过CFA一级考试肯定是没有问题的。

这是一种说法,但是这种说法也是在最近几年得到了验证,当然,ETHICS一直就是个争议,我个人认为的话,这个是看评题人的,你不巧,碰到了那种特别对道德敏感的人的话,可能你就过不了了,如果你碰到的是一个觉得专业学识胜过一切的人的话,那么你的ETHICS不过也能够过,但是在这里,我们不能把结果赌在RP上面。

1、从 Equity入手,这部分容易一些,而且应该算是最不枯燥的一个,再没有底子总听说过股票,从这里入手可以兴趣会高一些,然后Fixed Income,Alternative Investment,最后Portfolio Management。

2、Financail Statement Analysis,建议直接用官方教材,讲得比较系统而且不枯燥,知识点比较多,教材在一级不用掌握很深的知识点上篇幅掌握很好,用notes 会疑问较多,因为会计知识相当深,很多一级考试不必要掌握。

但是这一部分是一级考试重中之重。

晚了看Corporate Finance,问题不大,其中Corporate Governance(公司治理部分)是一个独立的知识点,建议加强中文知识背景学习。

3、Economics 没有经济学基础要补充中文知识背景,这一块教材讲得不经典,市场有很多经济学原理的教材.4、Ethics只有死记,Quantitive部分学习一级不是很深。

各位考生,2015年CFA备考已经开始,为了方便各位考生能更加系统地掌握考试大纲的重点知识,帮助大家充分备考,体验实战,网校开通了全免费的高顿题库(包括精题真题和全真模考系统),题库里附有详细的答案解析,学员可以通过多种题型加强练习,通过针对性地训练与模考,对学习过程进行全面总结。

2021CFA一级总结(固定收益债券,金融衍生品和alternative inves

2021CFA一级总结(固定收益债券,金融衍生品和alternativeinves固定收益债券,金融衍生品和alternative investment部分一、FI1.债券1.债券合约:negative covenant(禁止借款人条款,as不能卖抵押资产,不能额外借款等),affirmative covenant(借款人承诺的action,as保持公司的负债率)付息结构:零息票债券,step-up notes(coupon rate以特定rate增长),deferred-coupon bonds,floating rate,inverse floater:coupon rate=12%-reference rate; inflation-indexed bond,cap, floor,collar(既有顶也有底)应计利息accrued interestCall price:maximum price for currently callable bond,可能有多个call,但call price越来越低 2.bond redemption and retirement 1)amortizing证券分期偿付2)prepayment optionCallable but Nonrefundable bond是指可以提前偿还但不能不能funded by 以更低的coupon rate 发行bond。

Sinking fund provisions---偿债基金条款---为了保护投资者,规定经过一段时间后,每年偿还一定金额的本金。

有两种方式进行:1. Cash payment---通过抽签形式进行2. Delivery of securities---购回债券---当债券价格下跌时候,回购债券的方式比较便宜!有利于发行者的条款:1. The right to Call2. Accelerated sinking fund provision---加速偿债条款―有利于发行者,发行者可以选择是否多还一些本金 3. Prepayment option4. A cap on floating coupon rate1有利于持有者的条款1. Conversion provision可转债2. Floor3. Put option购买债券融资的方式有两种1. Margin call从brokeror银行借款,债券作为抵押----保证金的利息要比rep agreement的利息要高!2. 回购交易repo agreement----实际上是一种抵押融资---大多数的bond-dealer融资采用repo agreement2.债券的风险1)利率风险用久期衡量 Duration---1. 在收益率发生变化的时候,债券的价格的变动的幅度,也就是收益率变化1%,债券的价格变化百分之几?=-价格变化百分比/收益率变化百分比2. 利率风险和久期的关系---从概念上来讲,久期本身就是衡量债券价格利率风险的指标!----正比关系,久期越大,利率风险越大! 3. 价格收益率曲线的斜率---价格收益率曲线的一阶导数!PYield 期限越长久期越大,息票利率越高久期越小,add a call久期变小,add a put,久期变小。

cfa固收知识点

cfa固收知识点哇塞,CFA的固定收益部分真的有好多超重要的知识点呢!固定收益证券的定义可不能忽视呀。

它就是一种承诺在未来特定日期支付固定金额或者按照一定公式计算的现金流的证券。

像债券就是最典型的固定收益证券啦。

债券有好多要素呢,发行人这个很关键哦。

发行人可以是政府,政府发行债券就像是一种融资手段,为了建设基础设施之类的项目筹集资金。

还有公司也可以发行债券,公司发行债券就是为了扩大生产或者进行其他的投资项目。

票面利率也超级重要。

这个利率决定了债券持有人定期能收到的利息金额。

比如说一张债券的票面金额是1000元,票面利率是5%,那每年就能收到1000乘以5%也就是50元的利息呢。

哎呀,这利息可是债券收益的一个重要组成部分。

债券的期限也不容忽视。

期限长的债券和期限短的债券在很多方面都有很大的不同。

期限长的债券面临的利率风险通常会更大。

为啥这么说呢?因为在较长的时间内,市场利率波动的可能性就更大。

如果市场利率上升,那债券价格就会下跌,期限长的债券价格下跌的幅度可能就更大。

再来说说债券的信用风险吧。

信用风险就是发行人可能无法按时支付本金和利息的风险。

政府债券的信用风险相对较低,尤其是一些发达国家的政府债券。

但是公司债券的信用风险就有高有低啦。

那些信用评级高的公司,债券的信用风险就低一些,而信用评级低的公司,债券的信用风险就比较高。

信用评级机构在评估债券信用风险方面起到了很重要的作用呢,它们会根据公司的财务状况、经营业绩等很多因素来给出信用评级。

债券价格的计算也是个大知识点。

债券价格和市场利率是反向关系,这一点一定要牢记哦。

当市场利率下降的时候,债券价格就会上升。

计算债券价格的公式虽然有点复杂,但是理解了原理之后也不是那么难。

它是把未来的现金流按照市场利率进行折现得到的现值之和。

还有收益率曲线这个概念。

收益率曲线就是把不同期限但风险、流动性和税收政策相同的债券收益率连接起来形成的曲线。

正常情况下,收益率曲线是向上倾斜的,这表示长期债券的收益率高于短期债券。

第八固定收益证券的价值分析演示文稿

固定收益证券(债券)定价

现金流贴现法(Discounted Cash Flow Method,DCF)又称收入法或收入资本化法。

DCF认为任何资产的内在价值(Intrinsic value) 取决于该资产预期的现金流的现值。

第十三页,共25页。

V0

C1 (1 i1)

C2 (1 i2 )2

3. 非常情况下的债权人的权利保障情况(债券契 约) 。

第十一页,共25页。

AAA是信用最高级别,表示无信用风险,信誉 最高,偿债能力极强,不受经济形势任何影响;

AA是表示高级,最少风险,有很强的偿债能力; A是表示中上级,较少风险,支付能力较强,在经

济环境变动时,易受不利因素影响;

BBB表示中级,有风险,有足够的还本付息能 力,但缺乏可靠的保证,其安全性容易受不确 定因素影响,这也是在正常情况下投资者所能 接受的最低信用度等级,或者说,以上这四种 级别一般被认为属投资级别,其债券质量相对 较高。

年金与分期偿还互为反函数。假设一笔现金流由 每期金额为C的n期(期末)支付组成,并在n期

结束。

01 2

12

n-1 n

n 时期

第十六页,共25页。

Annnity

v0

C[1/ i

1/ i (1 i)n

]

Amortization C i(1 i)n v0 (1 i)n 1

例:从银行按揭贷款100,000元,15年期每月等额还款,现行的年利率是 5.81%,计算每月还款额?

金融工具的首要条件:标准化

债券仍是反映债券债务关系。借款人出具债务凭 证是向很多不知名的投资者借钱,因此,每个人 的条件都是标准化的,格式相同、内容相同、责 任义务相同——这样债券才具有可分割、可转让。

CFA一级知识点总结最全

CFA一级知识点总结Ethics 部分Objective of codes and standard:永远是为了maintain public trust in1.Financial market2.Investment profession6个code of ethics1.Code 1—ethics and pertinent d personsa.2.Code 2---primacy of client’s interesta.Integrity with investment professionb.客户利益高于自身利益3.Code 3---reasonable and independenta.必须注意reasonable careb.必须exercise independent professional judgment---必须独立判断!4.Code 4---ethical culture in the professiona.不但自己要practice,而且要鼓励别人practice—不仅仅是自己一个人去做,要所有人共同去做5.Code 5---ethnical culture in the capital market!a.促进整个capital market的integrity,推广其相关法规---增强公众对资本市场的trust!b.Capital market是基于i.Fairly pricing of risky assets;ii.Investors‘ confidence6.有关competence—能力---competence7个standard of professional conduct1.Standard 1---professionalism---knowledge of lawa.不需要成为法律专家,但是必须understand和comply with applicable law;b.当两个law发生conflict,则要遵守更加严格的法律!c.Knowingly---know or should knowd.必须attempt to stop the violation,如果不能stop,then must dissociatefrom the violation!必须从其中分离出去!i.Remove name from the written report;ii.Ask for a different assignmente.并不要求向有关部门report!(do not require)f.向CFA 进行书面报告report--encouraged to so2. Standard 1 ---professionalism---integrity of capital marketa.Bias from client or other groups—listed company,controlling shareholder!b.Bias from sell side analystc.Buyer side client—d.Issuer paid report---只能接受flat fee for their worke.3.Standard 1 ---professionalism---misinterpretation—不能误导客户,不能剽窃其他人的研究成果4.Standard 1 ---professionalism---misconduct---5.Standard 2---integrity of capital marketa.不能使用非公开信息!---material nonpublic information---b.mosaic theory---conclusion from analysis of public and non-material nonpublicinformation6.standard 3—duties to clientsa.Loyalty, prudence and care---i.如何定义客户?---考虑最终受益人!---雇佣我们的人未必就是我们的客户,要考虑最终受益人!ii.Soft dollar---when a manager uses client brokerage to purchase research report to benefit the investment manager---比如,作为基金公司,使用证券公司的席位进行交易,肯定会支付一定的费用,这些费用来自客户,所以基金公司只能用这些soft dollar为客户服务!b.Fair dealing---i.对所有客户要公平客观ii.个别的客户要求,可以征收premium的费用之后,是可以做的!条件是,其他的分析都已经公布给其他客户了iii.More critical when changes recommendationiv.Investment action---taking investment action based on research recommendationv.Prorated the allocationc.Suitabilityi.了解客户的经验,风险和回报目标ii.要有书面目标—至少一年进行更新!iii.是否和客户的书面目标相符合?iv.是否符合客户的整个total portfolio的投资目标?v.必须理解其投资组合的constraints,只能进行符合其书面目标的投资推荐!1.Investment policy statement—IPS---risk tolerance,returnrequirement, investment2.Constraint---time horizon, liquidity needs, tax concerns, legaland regulatory factors, unique circumstancesd.Performance presentationi.这里有performance presentation的规定,同时在GIPS里面也有类似规定!其区别是1.一个是自愿的---GIPS,一个是必需的;2.一个是针对公司—firm wide,一个是针对个人member和candidate3.GIPS要求公司to use accurate input data and approvedcalculation method, to prevent the performance record inaccordance with a prescribed formate.Preservation of confidentiality---必须保密---可以不保密的情况i.违法行为ii.法律要求进行披露iii.Client或者prospective client同意披露iv.以现行法律为准v.CFA进行investigate固定收益债券,金融衍生品和alternative investment 部分Nonrefundable bond是指不能通过发行新的债券还旧债Sinking fund provisions---偿债基金条款---为了保护投资者,规定经过一段时间后,每年偿还一定金额的本金。

cfa一级固定收益知识点总结

cfa一级固定收益知识点总结嘿,朋友!咱今天来聊聊 CFA 一级里的固定收益这个让人又爱又恨的部分。

先来说说债券的基本概念吧。

债券就像是你借给别人钱的一个凭证,到期了对方得连本带利还给你。

你想想,这不就跟你把钱借给好朋友,然后约定啥时候还钱还多少利息一个道理嘛?再说说利率风险。

利率一变,债券价格可就跟着上蹿下跳啦!这就好比天气变化,一会儿晴一会儿雨,你穿衣服就得跟着变,不然就得着凉。

利率上升,债券价格下降;利率下降,债券价格上升。

这关系你可得搞清楚,不然投资就容易栽跟头。

还有久期这个概念,它可是衡量债券价格对利率变动敏感度的一把尺子。

久期越长,债券价格对利率变动就越敏感。

这就好像腿长的人步子大,走得快;久期长的债券,价格波动也大。

信用风险也不能忽视啊!发债的公司要是不靠谱,到期不还钱或者少还钱,那你不就亏了?这跟你找合作伙伴做生意一样,得看准对方的信誉和实力。

说到债券的种类,那也是五花八门。

国债就像是国家这个大老板发的借条,信用高,风险低;公司债呢,就是各个公司发的,质量参差不齐,得好好挑。

还有收益率曲线,它能反映不同期限债券的收益率情况。

这曲线就像人生的轨迹,有起有伏,有高有低。

在学习固定收益的时候,你得像个细心的侦探,不放过任何一个细节。

别觉得这东西枯燥,其实它就像一场解谜游戏,每解开一个谜题,你就离成功更近一步。

你说,要是连这些基础知识都掌握不好,怎么能在投资的海洋里畅游呢?怎么能让自己的钱生钱呢?所以啊,朋友们,加油学,认真记,固定收益这部分一定能被咱们拿下!。

2019年CFA一级notes整理固定收益习题

固定收益习题MODULE QUIZ50.1To best evaluate your performance,enter your quiz answers online.1.A dual-currency bond pays coupon interest in a currency:A.of the bondholder’s choice.B.other than the home currency of the issuer.C.other than the currency in which it repays principal.2.A bond’s indenture:A.contains its covenants.B.is the same as a debenture.C.relates only to its interest and principal payments.3.A clause in a bond indenture that requires the borrower to perform a certain action is most accurately described as:A.a trust deed.B.a negative covenant.C.an affirmative covenant.4.An investor buys a pure-discount bond,holds it to maturity,and receives its par value.For tax purposes, the increase in the bond’s value is most likely to be treated as:A.a capital gain.B.interest income.C.tax-exempt income.MODULE QUIZ50.2To best evaluate your performance,enter your quiz answers online.1.A10-year bond pays no interest for three years,then pays$229.25,followed by payments of$35semiannually for seven years,and an additional$1,000at maturity.This bond is:A.a step-up bond.B.a zero-coupon bond.C.a deferred-coupon bond.2.Which of the following statements is most accurate with regard to floating-rate issues that have caps and floors?A.A cap is an advantage to the bondholder,while a floor is an advantage tothe issuer.B.A floor is an advantage to the bondholder,while a cap is an advantage tothe issuer.C.A floor is an advantage to both the issuer and thebondholder,while a capis a disadvantage to both the issuer and the bondholder. 3.Which of the following most accurately describes the maximum price for a currently callable bond?A.Its par value.B.The call price.C.The present value of its par value.MODULE QUIZ51.1To best evaluate your performance,enter your quiz answers online.1.An analyst who describes a fixed-income security as being a structured finance instrument is classifying the security by:A.credit quality.B.type of issuer.C.taxable status.2.LIBOR rates are determined:A.by countries’central banks.B.by money market regulators.C.in the interbank lending market.3.In which type of primary market transaction does an investment bank sell bonds on a commission basis?A.Single-price auction.B.Best-efforts offering.C.Underwritten offering.4.Secondary market bond transactions most likely take place:A.in dealer markets.B.in brokered markets.C.on organized exchanges.5.Sovereign bonds are described as on-the-run when they:A.are the most recent issue in a specific maturity.B.have increased substantially in price since they were issued.C.receive greater-than-expected demand from auction bidders.6.Bonds issued by the World Bank would most likely be:A.quasi-government bonds.B.global bonds.C.supranational bonds.MODULE QUIZ51.2To best evaluate your performance,enter your quiz answers online.1.With which of the following features of a corporatebond issue does an investor most likely face the risk of redemption prior to maturity?A.Serial bonds.B.Sinking fund.C.Term maturity structure.2.A financial instrument is structured such that cash flows to the security holder increase if a specified reference rate increases.This structured financial instrument is best described as:A.a participation instrument.B.a capital protected instrument.C.a yield enhancement instrument.3.Smith Bank lends Johnson Bank excess reserves on deposit with the central bank for a period of three months. Is this transaction said to occur in the interbank market?A.Yes.B.No,because the interbank market refers to loans for more than one year.C.No,because the interbank market does not include reserves at the central bank.4.In a repurchase agreement,the percentage difference between the repurchase price and the amount borrowed ismost accurately described as:A.the haircut.B.the repo rate.C.the repo margin.MODULE QUIZ52.1To best evaluate your performance,enter your quiz answers online.1.A20-year,10%annual-pay bond has a par value of $1,000.What is the price of the bond if it has a yield-to-maturity of15%?A.$685.14.B.$687.03.C.$828.39.2.An analyst observes a5-year,10%semiannual-pay bond. The face amount is£1,000.The analyst believes that the yield-to-maturity on a semiannual bond basis should be15%. Based on this yield estimate,the price of this bond would be:A.£828.40.B.£1,189.53.C.£1,193.04.3.An analyst observes a20-year,8%option-free bond withsemiannual coupons.The required yield-to-maturity on a semiannual bond basis was8%,but suddenly it decreased to7.25%.As a result,the price of this bond:A.increased.B.decreased.C.stayed the same.4.A$1,000,5%,20-year annual-pay bond has a YTM of 6.5%. If the YTM remains unchanged,how much will the bond value increase over the next three years?A.$13.62.B.$13.78.C.$13.96.MODULE QUIZ52.2To best evaluate your performance,enter your quiz answers online.1.If spot rates are 3.2%for one year, 3.4%for two years, and 3.5%for three years,the price of a$100,000face value,3-year,annual-pay bond with a coupon rate of4%is closest to:A.$101,420.B.$101,790.C.$108,230.2.An investor paid a full price of$1,059.04each for100 bonds.The purchase was between coupon dates,and accrued interest was$23.54per bond.What is each bond’s flat price?A.$1,000.00.B.$1,035.50.C.$1,082.58.3.Cathy Moran,CFA,is estimating a value for an infrequently traded bond with six years to maturity,an annual coupon of7%,and a single-B credit rating.Moran obtains yields-to-maturity for more liquid bonds with the same credit rating:5%coupon,eight years to maturity,yielding7.20%.6.5%coupon,five years to maturity,yielding6.40%.The infrequently traded bond is most likely trading at:A.par value.B.a discount to par value.C.a premium to par value.MODULE QUIZ52.3To best evaluate your performance,enter your quiz answers online.1.A market rate of discount for a single payment to bemade in the future is:A.a spot rate.B.a simple yield.C.a forward rate.2.Based on semiannual compounding,what would the YTM be on a15-year,zero-coupon,$1,000par value bond that’s currently trading at$331.40?A. 3.750%.B. 5.151%.C.7.500%.3.An analyst observes a Widget&Co.7.125%,4-year, semiannual-pay bond trading at102.347%of par(where par is$1,000).The bond is callable at101in two years.What is the bond’s yield-to-call?A. 3.167%.B. 5.664%.C. 6.334%.4.A floating-rate note has a quoted margin of+50basis points and a required margin of+75basis points.On its next reset date,the price of the note will be:A.equal to par value.B.less than par value.C.greater than par value.5.Which of the following money market yields is a bond-equivalent yield?A.Add-on yield based on a365-day year.B.Discount yield based on a360-day year.C.Discount yield based on a365-day year.MODULE QUIZ52.4,52.5To best evaluate your performance,enter your quiz answers online.1.Which of the following yield curves is least likely to consist of observed yields in the market?A.Forward yield curve.B.Par bond yield curve.C.Coupon bond yield curve.2.The4-year spot rate is9.45%,and the3-year spot rate is9.85%.What is the1-year forward rate three years from today?A.8.258%.B.9.850%.C.11.059%.3.Given the following spot and forward rates:Current1-year spot rate is 5.5%.One-year forward rate one year from today is7.63%.One-year forward rate two years from today is12.18%.One-year forward rate three years from today is15.5%.The value of a4-year,10%annual-pay,$1,000par value bond is closest to:A.$996.B.$1,009.C.$1,086.4.A corporate bond is quoted at a spread of+235basis points over an interpolated12-year U.S.Treasury bond yield.This spread is:A.a G-spread.B.an I-spread.C.a Z-spread.MODULE QUIZ53.1To best evaluate your performance,enter your quiz answers online.1.Economic benefits of securitization least likely include:A.reducing excessive lending by banks.B.reducing funding costs for firms that securitize assets.C.increasing the liquidity of the underlying financialassets.2.In a securitization,the issuer of asset-backed securities is best described as:A.the SPE.B.the seller.C.the servicer.3.A mortgage-backed security with a senior/subordinated structure is said to feature:A.time tranching.B.credit tranching.C.a pass-through structure.4.A mortgage that has a balloon payment equal to the original loan principal is:A.a convertible mortgage.B.a fully amortizing mortgage.C.an interest-only lifetime mortgage.5.Residential mortgages that may be included in agency RMBS are least likely required to have:A.a minimum loan-to-value ratio.B.insurance on the mortgaged property.C.a minimum percentage down payment.6.The primary motivation for issuing collateralizedmortgage obligations(CMOs)is to reduce:A.extension risk.B.funding costs.C.contraction risk.MODULE QUIZ53.2To best evaluate your performance,enter your quiz answers online.1.The risk that mortgage prepayments will occur more slowly than expected is best characterized as:A.default risk.B.extension risk.C.contraction risk.2.For investors in commercial mortgage-backed securities, balloon risk in commercial mortgages results in:A.call risk.B.extension risk.C.contraction risk.3.During the lockout period of a credit card ABS:A.no new receivables are added to the pool.B.investors do not receive interest payments.C.investors do not receive principal payments.4.A debt security that is collateralized by a pool of thesovereign debt of several developing countries is most likely:A.a CMBS.B.a CDO.C.a CMO.MODULE QUIZ54.1To best evaluate your performance,enter your quiz answers online.1.The largest component of returns for a7-year zero-coupon bond yielding8%and held to maturity is:A.capital gains.B.interest income.C.reinvestment income.2.An investor buys a10-year bond with a 6.5%annual coupon and a YTM of6%.Before the first coupon payment is made,the YTM for the bond decreases to5.5%.Assuming coupon payments are reinvested at the YTM, the investor’s return when the bond is held to maturity is:A.less than6.0%.B.equal to 6.0%.C.greater than 6.0%.3.Assuming coupon interest is reinvested at a bond’s YTM, what is the interest portion of an18-year,$1,000par,5% annual coupon bond’s return if it is purchased at par and held to maturity?A.$576.95B.$1,406.62.C.$1,476.95.4.An investor buys a15-year,£800,000,zero-coupon bond with an annual YTM of7.3%.If she sells the bond after three years for£346,333 she will have:A.a capital gain.B.a capital loss.C.neither a capital gain nor a capital loss.5.A14%annual-pay coupon bond has six years to maturity. The bond is currently trading at ing a25basis point change in yield,the approximate modified duration of the bond is closest to:A.0.392.B. 3.888.C. 3.970.6.Which of the following measures is lowest for acallable bond?A.Macaulay duration.B.Effective duration.C.Modified duration.7.Effective duration is more appropriate than modified duration for estimating interest rate risk for bonds with embedded options because these bonds:A.tend to have greater credit risk than option-free bonds.B.exhibit high convexity that makes modified duration less accurate.C.have uncertain cash flows that depend on the path of interest ratechanges.MODULE QUIZ54.2To best evaluate your performance,enter your quiz answers online.1.A bond portfolio manager who wants to estimate the sensitivity of the portfolio’s value to changes in the5-year spot rate should use:A.a key rate duration.B.a Macaulay duration.C.an effective duration.2.Which of the following three bonds(similar except for yield and maturity)has the least Macaulay duration?A bond with:A.5%yield and10-year maturity.B.5%yield and20-year maturity.C.6%yield and10-year maturity.3.Portfolio duration has limited usefulness as a measure of interest rate risk for a portfolio because it:A.assumes yield changes uniformly across all maturities.B.cannot be applied if the portfolio includes bonds with embedded options.C.is accurate only if the portfolio’s internal rate of return is equal to its cashflow yield.4.The current price of a$1,000,7-year,5.5%semiannual coupon bond is$1,029.23.The bond’s price value of a basis point is closest to:A.$0.05.B.$0.60.C.$5.74.MODULE QUIZ54.3To best evaluate your performance,enter your quiz answersonline.1.A bond has a convexity of114.6.The convexity effect, if the yield decreases by110basis points,is closest to:A.–1.673%.B.+0.693%.C.+1.673%.2.The modified duration of a bond is7.87.The approximate percentage change in price using duration only for a yield decrease of110basis points is closest to:A.–8.657%.B.+7.155%.C.+8.657%.3.Assume a bond has an effective duration of10.5and a convexity ing both of these measures,the estimated percentage change in price for this bond,in response to a decline in yield of200basis points,is closest to:A.19.05%.B.22.95%.C.24.89%.4.Two bonds are similar in all respects except maturity. Can the shorter-maturity bond have greater interest raterisk than the longer-term bond?A.No,because the shorter-maturity bond will have a lower duration.B.Yes,because the shorter-maturity bond may have a higher duration.C.Yes,because short-term yields can be more volatile than long-term yields.5.An investor with an investment horizon of six years buys a bond with a modified duration of6.0.This investment has:A.no duration gap.B.a positive duration gap.C.a negative duration gap.6.Which of the following most accurately describes the relationship between liquidity and yield spreads relative to benchmark government bond rates?All else being equal, bonds with:A.less liquidity have lower yield spreads.B.greater liquidity have higher yield spreads.C.less liquidity have higher yield spreads.MODULE QUIZ55.1To best evaluate your performance,enter your quiz answersonline.1.The two components of credit risk are:A.default risk and yield spread.B.default risk and loss severity.C.loss severity and yield spread.2.Expected loss can decrease with an increase in a bond’s:A.default risk.B.loss severity.C.recovery rate.3.Absolute priority of claims in a bankruptcy might be violated because:A.of the pari passu principle.B.creditors negotiate a different outcome.C.available funds must be distributed equally among creditors.4.“Notching”is best described as a difference between:A.an issuer credit rating and an issue credit rating.B.a company credit rating and an industry average credit rating.C.an investment grade credit rating and a noninvestment grade credit rating.5.Which of the following statements is least likely a limitation of relying on ratings from credit rating agencies?A.Credit ratings are dynamic.B.Firm-specific risks are difficult to rate.C.Credit ratings adjust quickly to changes in bond prices.6.Ratio analysis is most likely used to assess a borrower’s:A.capacity.B.character.C.collateral.MODULE QUIZ55.2To best evaluate your performance,enter your quiz answers online.1.Higher credit risk is indicated by a higher:A.FFO/debt ratio.B.debt/EBITDA ratio.C.EBITDA/interest expense ratio.pared to other firms in the same industry,an issuer with a credit rating of AAA should have a lower:A.FFO/debt ratio.B.operating margin.C.debt/capital ratio.3.Credit spreads tend to widen as:A.the credit cycle improves.B.economic conditions worsen.C.broker-dealers become more willing to provide capital.pared to shorter duration bonds,longer duration bonds:A.have smaller bid-ask spreads.B.are less sensitive to credit spreads.C.have less certainty regarding future creditworthiness.5.One key difference between sovereign bonds and municipal bonds is that sovereign issuers:A.can print money.B.have governmental taxing power.C.are affected by economic conditions.。

2019年CFA一级notes整理固定收益习题

固定收益习题MODULE QUIZ50.1To best evaluate your performance,enter your quiz answers online.1.A dual-currency bond pays coupon interest in a currency:A.of the bondholder’s choice.B.other than the home currency of the issuer.C.other than the currency in which it repays principal.2.A bond’s indenture:A.contains its covenants.B.is the same as a debenture.C.relates only to its interest and principal payments.3.A clause in a bond indenture that requires the borrower to perform a certain action is most accurately described as:A.a trust deed.B.a negative covenant.C.an affirmative covenant.4.An investor buys a pure-discount bond,holds it to maturity,and receives its par value.For tax purposes, the increase in the bond’s value is most likely to be treated as:A.a capital gain.B.interest income.C.tax-exempt income.MODULE QUIZ50.2To best evaluate your performance,enter your quiz answers online.1.A10-year bond pays no interest for three years,then pays$229.25,followed by payments of$35semiannually for seven years,and an additional$1,000at maturity.This bond is:A.a step-up bond.B.a zero-coupon bond.C.a deferred-coupon bond.2.Which of the following statements is most accurate with regard to floating-rate issues that have caps and floors?A.A cap is an advantage to the bondholder,while a floor is an advantage tothe issuer.B.A floor is an advantage to the bondholder,while a cap is an advantage tothe issuer.C.A floor is an advantage to both the issuer and thebondholder,while a capis a disadvantage to both the issuer and the bondholder. 3.Which of the following most accurately describes the maximum price for a currently callable bond?A.Its par value.B.The call price.C.The present value of its par value.MODULE QUIZ51.1To best evaluate your performance,enter your quiz answers online.1.An analyst who describes a fixed-income security as being a structured finance instrument is classifying the security by:A.credit quality.B.type of issuer.C.taxable status.2.LIBOR rates are determined:A.by countries’central banks.B.by money market regulators.C.in the interbank lending market.3.In which type of primary market transaction does an investment bank sell bonds on a commission basis?A.Single-price auction.B.Best-efforts offering.C.Underwritten offering.4.Secondary market bond transactions most likely take place:A.in dealer markets.B.in brokered markets.C.on organized exchanges.5.Sovereign bonds are described as on-the-run when they:A.are the most recent issue in a specific maturity.B.have increased substantially in price since they were issued.C.receive greater-than-expected demand from auction bidders.6.Bonds issued by the World Bank would most likely be:A.quasi-government bonds.B.global bonds.C.supranational bonds.MODULE QUIZ51.2To best evaluate your performance,enter your quiz answers online.1.With which of the following features of a corporatebond issue does an investor most likely face the risk of redemption prior to maturity?A.Serial bonds.B.Sinking fund.C.Term maturity structure.2.A financial instrument is structured such that cash flows to the security holder increase if a specified reference rate increases.This structured financial instrument is best described as:A.a participation instrument.B.a capital protected instrument.C.a yield enhancement instrument.3.Smith Bank lends Johnson Bank excess reserves on deposit with the central bank for a period of three months. Is this transaction said to occur in the interbank market?A.Yes.B.No,because the interbank market refers to loans for more than one year.C.No,because the interbank market does not include reserves at the central bank.4.In a repurchase agreement,the percentage difference between the repurchase price and the amount borrowed ismost accurately described as:A.the haircut.B.the repo rate.C.the repo margin.MODULE QUIZ52.1To best evaluate your performance,enter your quiz answers online.1.A20-year,10%annual-pay bond has a par value of $1,000.What is the price of the bond if it has a yield-to-maturity of15%?A.$685.14.B.$687.03.C.$828.39.2.An analyst observes a5-year,10%semiannual-pay bond. The face amount is£1,000.The analyst believes that the yield-to-maturity on a semiannual bond basis should be15%. Based on this yield estimate,the price of this bond would be:A.£828.40.B.£1,189.53.C.£1,193.04.3.An analyst observes a20-year,8%option-free bond withsemiannual coupons.The required yield-to-maturity on a semiannual bond basis was8%,but suddenly it decreased to7.25%.As a result,the price of this bond:A.increased.B.decreased.C.stayed the same.4.A$1,000,5%,20-year annual-pay bond has a YTM of 6.5%. If the YTM remains unchanged,how much will the bond value increase over the next three years?A.$13.62.B.$13.78.C.$13.96.MODULE QUIZ52.2To best evaluate your performance,enter your quiz answers online.1.If spot rates are 3.2%for one year, 3.4%for two years, and 3.5%for three years,the price of a$100,000face value,3-year,annual-pay bond with a coupon rate of4%is closest to:A.$101,420.B.$101,790.C.$108,230.2.An investor paid a full price of$1,059.04each for100 bonds.The purchase was between coupon dates,and accrued interest was$23.54per bond.What is each bond’s flat price?A.$1,000.00.B.$1,035.50.C.$1,082.58.3.Cathy Moran,CFA,is estimating a value for an infrequently traded bond with six years to maturity,an annual coupon of7%,and a single-B credit rating.Moran obtains yields-to-maturity for more liquid bonds with the same credit rating:5%coupon,eight years to maturity,yielding7.20%.6.5%coupon,five years to maturity,yielding6.40%.The infrequently traded bond is most likely trading at:A.par value.B.a discount to par value.C.a premium to par value.MODULE QUIZ52.3To best evaluate your performance,enter your quiz answers online.1.A market rate of discount for a single payment to bemade in the future is:A.a spot rate.B.a simple yield.C.a forward rate.2.Based on semiannual compounding,what would the YTM be on a15-year,zero-coupon,$1,000par value bond that’s currently trading at$331.40?A. 3.750%.B. 5.151%.C.7.500%.3.An analyst observes a Widget&Co.7.125%,4-year, semiannual-pay bond trading at102.347%of par(where par is$1,000).The bond is callable at101in two years.What is the bond’s yield-to-call?A. 3.167%.B. 5.664%.C. 6.334%.4.A floating-rate note has a quoted margin of+50basis points and a required margin of+75basis points.On its next reset date,the price of the note will be:A.equal to par value.B.less than par value.C.greater than par value.5.Which of the following money market yields is a bond-equivalent yield?A.Add-on yield based on a365-day year.B.Discount yield based on a360-day year.C.Discount yield based on a365-day year.MODULE QUIZ52.4,52.5To best evaluate your performance,enter your quiz answers online.1.Which of the following yield curves is least likely to consist of observed yields in the market?A.Forward yield curve.B.Par bond yield curve.C.Coupon bond yield curve.2.The4-year spot rate is9.45%,and the3-year spot rate is9.85%.What is the1-year forward rate three years from today?A.8.258%.B.9.850%.C.11.059%.3.Given the following spot and forward rates:Current1-year spot rate is 5.5%.One-year forward rate one year from today is7.63%.One-year forward rate two years from today is12.18%.One-year forward rate three years from today is15.5%.The value of a4-year,10%annual-pay,$1,000par value bond is closest to:A.$996.B.$1,009.C.$1,086.4.A corporate bond is quoted at a spread of+235basis points over an interpolated12-year U.S.Treasury bond yield.This spread is:A.a G-spread.B.an I-spread.C.a Z-spread.MODULE QUIZ53.1To best evaluate your performance,enter your quiz answers online.1.Economic benefits of securitization least likely include:A.reducing excessive lending by banks.B.reducing funding costs for firms that securitize assets.C.increasing the liquidity of the underlying financialassets.2.In a securitization,the issuer of asset-backed securities is best described as:A.the SPE.B.the seller.C.the servicer.3.A mortgage-backed security with a senior/subordinated structure is said to feature:A.time tranching.B.credit tranching.C.a pass-through structure.4.A mortgage that has a balloon payment equal to the original loan principal is:A.a convertible mortgage.B.a fully amortizing mortgage.C.an interest-only lifetime mortgage.5.Residential mortgages that may be included in agency RMBS are least likely required to have:A.a minimum loan-to-value ratio.B.insurance on the mortgaged property.C.a minimum percentage down payment.6.The primary motivation for issuing collateralizedmortgage obligations(CMOs)is to reduce:A.extension risk.B.funding costs.C.contraction risk.MODULE QUIZ53.2To best evaluate your performance,enter your quiz answers online.1.The risk that mortgage prepayments will occur more slowly than expected is best characterized as:A.default risk.B.extension risk.C.contraction risk.2.For investors in commercial mortgage-backed securities, balloon risk in commercial mortgages results in:A.call risk.B.extension risk.C.contraction risk.3.During the lockout period of a credit card ABS:A.no new receivables are added to the pool.B.investors do not receive interest payments.C.investors do not receive principal payments.4.A debt security that is collateralized by a pool of thesovereign debt of several developing countries is most likely:A.a CMBS.B.a CDO.C.a CMO.MODULE QUIZ54.1To best evaluate your performance,enter your quiz answers online.1.The largest component of returns for a7-year zero-coupon bond yielding8%and held to maturity is:A.capital gains.B.interest income.C.reinvestment income.2.An investor buys a10-year bond with a 6.5%annual coupon and a YTM of6%.Before the first coupon payment is made,the YTM for the bond decreases to5.5%.Assuming coupon payments are reinvested at the YTM, the investor’s return when the bond is held to maturity is:A.less than6.0%.B.equal to 6.0%.C.greater than 6.0%.3.Assuming coupon interest is reinvested at a bond’s YTM, what is the interest portion of an18-year,$1,000par,5% annual coupon bond’s return if it is purchased at par and held to maturity?A.$576.95B.$1,406.62.C.$1,476.95.4.An investor buys a15-year,£800,000,zero-coupon bond with an annual YTM of7.3%.If she sells the bond after three years for£346,333 she will have:A.a capital gain.B.a capital loss.C.neither a capital gain nor a capital loss.5.A14%annual-pay coupon bond has six years to maturity. The bond is currently trading at ing a25basis point change in yield,the approximate modified duration of the bond is closest to:A.0.392.B. 3.888.C. 3.970.6.Which of the following measures is lowest for acallable bond?A.Macaulay duration.B.Effective duration.C.Modified duration.7.Effective duration is more appropriate than modified duration for estimating interest rate risk for bonds with embedded options because these bonds:A.tend to have greater credit risk than option-free bonds.B.exhibit high convexity that makes modified duration less accurate.C.have uncertain cash flows that depend on the path of interest ratechanges.MODULE QUIZ54.2To best evaluate your performance,enter your quiz answers online.1.A bond portfolio manager who wants to estimate the sensitivity of the portfolio’s value to changes in the5-year spot rate should use:A.a key rate duration.B.a Macaulay duration.C.an effective duration.2.Which of the following three bonds(similar except for yield and maturity)has the least Macaulay duration?A bond with:A.5%yield and10-year maturity.B.5%yield and20-year maturity.C.6%yield and10-year maturity.3.Portfolio duration has limited usefulness as a measure of interest rate risk for a portfolio because it:A.assumes yield changes uniformly across all maturities.B.cannot be applied if the portfolio includes bonds with embedded options.C.is accurate only if the portfolio’s internal rate of return is equal to its cashflow yield.4.The current price of a$1,000,7-year,5.5%semiannual coupon bond is$1,029.23.The bond’s price value of a basis point is closest to:A.$0.05.B.$0.60.C.$5.74.MODULE QUIZ54.3To best evaluate your performance,enter your quiz answersonline.1.A bond has a convexity of114.6.The convexity effect, if the yield decreases by110basis points,is closest to:A.–1.673%.B.+0.693%.C.+1.673%.2.The modified duration of a bond is7.87.The approximate percentage change in price using duration only for a yield decrease of110basis points is closest to:A.–8.657%.B.+7.155%.C.+8.657%.3.Assume a bond has an effective duration of10.5and a convexity ing both of these measures,the estimated percentage change in price for this bond,in response to a decline in yield of200basis points,is closest to:A.19.05%.B.22.95%.C.24.89%.4.Two bonds are similar in all respects except maturity. Can the shorter-maturity bond have greater interest raterisk than the longer-term bond?A.No,because the shorter-maturity bond will have a lower duration.B.Yes,because the shorter-maturity bond may have a higher duration.C.Yes,because short-term yields can be more volatile than long-term yields.5.An investor with an investment horizon of six years buys a bond with a modified duration of6.0.This investment has:A.no duration gap.B.a positive duration gap.C.a negative duration gap.6.Which of the following most accurately describes the relationship between liquidity and yield spreads relative to benchmark government bond rates?All else being equal, bonds with:A.less liquidity have lower yield spreads.B.greater liquidity have higher yield spreads.C.less liquidity have higher yield spreads.MODULE QUIZ55.1To best evaluate your performance,enter your quiz answersonline.1.The two components of credit risk are:A.default risk and yield spread.B.default risk and loss severity.C.loss severity and yield spread.2.Expected loss can decrease with an increase in a bond’s:A.default risk.B.loss severity.C.recovery rate.3.Absolute priority of claims in a bankruptcy might be violated because:A.of the pari passu principle.B.creditors negotiate a different outcome.C.available funds must be distributed equally among creditors.4.“Notching”is best described as a difference between:A.an issuer credit rating and an issue credit rating.B.a company credit rating and an industry average credit rating.C.an investment grade credit rating and a noninvestment grade credit rating.5.Which of the following statements is least likely a limitation of relying on ratings from credit rating agencies?A.Credit ratings are dynamic.B.Firm-specific risks are difficult to rate.C.Credit ratings adjust quickly to changes in bond prices.6.Ratio analysis is most likely used to assess a borrower’s:A.capacity.B.character.C.collateral.MODULE QUIZ55.2To best evaluate your performance,enter your quiz answers online.1.Higher credit risk is indicated by a higher:A.FFO/debt ratio.B.debt/EBITDA ratio.C.EBITDA/interest expense ratio.pared to other firms in the same industry,an issuer with a credit rating of AAA should have a lower:A.FFO/debt ratio.B.operating margin.C.debt/capital ratio.3.Credit spreads tend to widen as:A.the credit cycle improves.B.economic conditions worsen.C.broker-dealers become more willing to provide capital.pared to shorter duration bonds,longer duration bonds:A.have smaller bid-ask spreads.B.are less sensitive to credit spreads.C.have less certainty regarding future creditworthiness.5.One key difference between sovereign bonds and municipal bonds is that sovereign issuers:A.can print money.B.have governmental taxing power.C.are affected by economic conditions.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

CFA一级考试知识点第八部分固定收益证券债券五类主要发行人超国家组织supranational organizations,收回贷款和成员国股金还款主权(国家)政府sovereign/national governments,税收、印钞还款非主权(地方)政府non-sovereign/local governments(美国各州),地方税收、融资、收费。

准政府机构quasi-governments entities(房利美、房地美)公司(金融机构、非金融机构)经营现金流还款Maturity到期时间、tenor剩余到期时间小于一年是货币市场证券、大于一年是资本市场证券、没有明确到期时间是永续债券。

计算票息需要考虑付息频率,未明确的默认半年一次付息。

双币种债券dual-currency bonds支付票息时用A货币,支付本金时用B货币。

外汇期权债券currency option bongds给予投资人选择权,可以选择本金或利息币种。

本金偿还形式子弹型债券bullet bond,本金在最后支付。

也称为plain vanilla bond(香草计划债券)摊销性债券amortizing bond,分为完全摊销和部分摊销。

偿债基金条款sinking found provision,也是提前收回本金的方式,债券发行方在存续期间定期提前偿还部分本金,例如每年偿还本金初始发行额的6%。

票息支付形式固定票息债券fixed-rate coupon bonds,零息债券会折价发行,面值与发行价之差就是利息,零息债券也称为纯贴现债券pure discount bond。

梯升债券step – up coupon bonds票息上升递延债券deferred coupon bonds/split coupon bonds,期初几年不支付,后期才开始支付票息。

(前期资金紧张或研发型项目)实物支持债券payment-in-kind/PIK coupon bonds票息不是现金,而是实物。

常见的是同等的债券或股票来代替,这类风险更高,收益率更高。

浮动票息债券folating-rate notes/FRN,通常与LIBOR绑定,通过利差quoted margin和基点basis point来体现。

切记计算时需要使用上一期的LIBOR。

最常见的LIBOR是美元3月期。

指数挂钩债券index-linked bonds,消费者价格指数/通货膨胀保障指数信用挂钩债券credit linked coupon bonds与信用评级挂钩股权挂钩债券equity linked notes与股权权益挂钩。

或有条款可赎回债券callable bond权利属于债券发行人,价格等于同等条件不可赎回债券价格减去期权的价格。

随时可赎回叫美式期权、一个赎回日叫欧式期权、多个赎回日称为百慕大期权。

可回收债券putable bond权利属于债券投资人,利率上升时投资人会行使此权利。

价格等于同等条件不可赎回债券价格加上期权的价格。

可转换债券convertible bond,持有人可将持有债券转换为公司股票的权利。

价格等于同等条件不可转债券价格加上股票看涨期权的价格。

有抵押品的债券称为担保债券cecured bonds;没有抵押品的债券称为无担保债券unsecured bonds资产担保债券比资产支持证券信用风险更低。

原因1.资产支持证券会成立SPV公司,担保债券可要求清算的资产基数更大。

2.资产无法提供足够现金时,担保债券可以要求替换资产。

内部信用增强:结构化subordination、超额抵押overcollateralization、储备账户reserve accounts(现金储备、利差储备)。

外部信用增信:银行保函、信用证、现金担保账户。

正面条款affirmative要求发行人必须做的事情、负面条款negative禁止发行人做的事情。

本币债券national bond 包含了所有机构或本人在本国以本币发行的债券。

欧元债券eurobond指在欧洲债券市场发行和交易的债券,本质而言是指离岸发行和交易的债券,和“欧洲”并无关联。

欧洲美元债eurodollar bond指美国境外发行以美元计价的债券、欧洲日元债券euroyen bond指在日本境外发行的日元计价债券。

因为没有使用主权国本币,欧元债券受到监管最弱。

如果在欧洲债券市场和至少一个本国债券市场同时发行债券,则被称为全球债券global bond。

大部分欧洲债券是不记名债券bearer bonds,本币债券是记名债券registered bonds。

根据信用质量债券市场分为投资级investment grade和投机级speculative grade债券。

一级分为私募发行private placement和债券市场公开发行public offerings公开发行分为:包销underwritten offering,多家包销称为辛迪加或银团发行syndicated offering代销best effort offering拍卖auctions上架注册shelf registration,主体提交一份注册资料,但可以多次发行,好的主体才有资格。

市场新发行的国债称为新发行国债on the run,新发行国债是二级市场交易最为活跃的。

期限小于1年的为短期国库券treasury bills/T-bills1年和10年之间的称为treasury notes/T-notes大于10年的称为treasury bonds/T-bonds公司债务分为银行贷款:双边贷款bilateral loan(一家银行一个公司)、辛迪加贷款syndicated loan商业票据commercial paper期限1天到1年的融资票据公司债券大于1年的债券。

结构化金融工具structured financial instruments,又称为结构化产品structured products,根据需求设计,通常是一个传统固定收益证券加上至少一个衍生工具构成。

核心是对资产现金流结构重塑,以便重新分配风险。

分为以下几类:资本保护性工具capital protected instruments,分为全额资本保护型工具和部分资本保护型工具。

最常见的是保护凭证guarantee certificate,由零息债券和看涨期权的多头组成。

核心是保护本金安全,使用利润冒险。

收益增强型工具yield enhancement,通过增加风险敞口以增加期望收益,最常见的是信用联结债券credit linked notes。

归还本金取决于信用事件是否发生,将风险转移给了投资人,通常深度折价发行,如果发生违约,归还本金部分应减去对应损失额。

参与性工具participation instruments让投资者参与特定资产收益。

常见的是“付固定、收浮动”的互换头寸,可以间接获得市场利率上升的收益。

杠杆工具leveraged instruments银行短期融资方式零售存款retail deposits,分为活期存款账户demand deposits/checking accounts、定期存款账户savings account、货币市场账户money market accounts(介于活期和定期,支付市场利率,可在较短时间取出存款)短期批发融资short term wholesale funds。

准备金reserve funds(向超额准备金银行借)、银行间资金interbank funds、大额可转让定期存单certificate of deposit/CD。

回购repurchase /reop与逆回购reverse repurchase协议,指出售证券时同时签订一份协议,约定特定价格购回证券,可看成是抵押贷款,出售的证券就是抵押品。

1天的回购叫隔夜回购,大于1天的称为期限回购。

买入证券、借出资金的一方称为逆回购reverse repo 方。

单一折现率的债券定价- 市场折现率当票息率小于市场折现率,债券价格小于面值,称为折价债券当票息率等于市场折现率,债券价格等于面值,称为平价债券当票息率大于市场折现率,债券价格大于面值,称为溢价债券单一折现率的债券定价–到期收益率yield to maturity ,YTM本质是债券现金流的内部收益率IRR单一折现率的债券定价–赎回收益率yield to call赎回收益率与到期收益率本质是一样的,只不过持有期限不同,到期收益率持有至到期,赎回持有至赎回。

第一个赎回日收益率yield to first call、第二个赎回日收益率yield to second call单一折现率的债券定价–矩阵定价matrix pricing利用交易活跃的可比债券对不活跃债券进行定价单一折现率的债券定价–浮动利率债券收益率市场参考利率加上报价利差quoted margin,除报价利差还有一种叫要求利差requited margin即期利率spot rates,用即期利率给债券定价时,每一个时间点对应现金流所使用的折现率(即期利率)彼此不同。

例题:一年期即期利率3%、两年期4%、三年期5%,求三年期、每年付息一次、票息率6%、面值100的债券价格。

P=+ + =102.939远期利率forward rates,未来某一时间点看“更未来”某段时间的利率,是远期市场上所使用利率。

3y2y代表3年后的2年期利率。

例题:计算隐含远期利率2y1y,1年期零票息债券YTM3%,2年期零票息债券YTM4%,3年期零票息债券YTM5%。

2年后利率乘以1年后利率,应该与3年后利率相等(1+)^4 * (1+)^2= (1+)^6例题:计算远期利率的定价0y1y=3%,1y1y=4%,2y1y=5%,求三年期每年付息一次,票息率4%,面值100的债券价格。

P=()+()()= 100.082债券报价和交割家不一样,因为需要加上上一个付息日到交割日之前的应计利息accrued interest /AIAI = * PMT,其中PMT表示两个付息日之间的票息。

价格价格称为全价full price/dirty price,报价称为净价flat price/clean price。

计算净价时,先求现价、再求全价、再将全价减去应计利息,得出净价。

计算债券收益率,按照合同约定付息时间计算天数,不避开周末或假期称为管理收益率street convention yield,如果遇到假期付息推迟到下一交易日称为真实收益率true yield,真实收益率永远不可能大于管理收益率。

通常使用华尔街street的管理收益率当前收益率current yield,是一种一年期票息除以债券净价不考虑付息和应计利息的简单估计方法简单收益率simple yield,将利得和损失考虑在内,除以债券净价。