国际金融Lecture 10

《国际金融学》PPT课件全

输入 各国标政题策性

银行

如中国国家开发银行、中国进出口银行等,它们在国 内提供政策性金融服务的同时,也积极拓展海外业务, 支持中国企业“走出去”。

各国中央银 行

各国商业银 行

如挪威政府全球养老基金、新加坡政府投资公司等, 它们管理着庞大的外汇储备和财政盈余资金,在全球

范围内进行资产配置和投资。

各国主权财 富基金

成立于1964年,总部设在科特迪瓦经 济首都阿比让。成立目的是为非洲鼓劲 发展的动力,帮助非洲各国进行经济重 建和发展,协助成员国发展经济和减少 贫困,为成员国的经济和社会发展活动 提供资金支持。

各国的国际金融机构

如美联储、欧洲央行等,它们不仅在国内执行货币政 策和金融监管职能,同时也参与国际金融合作与协调。

国际资本流动定义

指资本在国际间转移,包括直接投资、间接投资、国际信贷等方 式。

国际资本流动类型

长期资本流动与短期资本流动。

国际资本流动规模与趋势

近年来,随着全球化进程加速,国际资本流动规模不断扩大,流动 速度也在加快。

国际资本流动的原因与影响

利润驱动

企业为追求更高利润,在全球范围内配置资源。

汇率与利率变动

成立于1966年11月,是面向亚洲和太 平洋地区的区域性政府间金融开发机构。 它不是联合国下属机构,但它是联合国 亚洲及太平洋经济社会委员会(联合国 亚太经社会)赞助建立的机构,同联合 国及其区域和专门机构有密切的联系。

是欧洲经济共同体成员国合资经营的金 融机构,根据1957年《建立欧洲投资 银行协定》的规定,于1958年1月1日 成立。该银行宗旨是利用国际资本市场 和共同体内部资金,促进共同体的平衡 和稳定发展。

《国际金融学》PPT课件 全

《国际金融讲义》课件

4 掌握国际投资策略

学习国际投资的基本理念和策略,提高投资 决策的准确性。

课程大纲

第一章 第二章 第三章 第四章 第五章

国际金融的基本概念 国际金融市场与外汇市场 金融风险管理 货币政策与贸易平衡 国际投资与跨国公司

课程内容

1

第一章

国际金融的基本概念和特点,全球金融市场的结构与机制。

2

第二章

外汇市场和汇率制度,国际收支及汇率形成的影响因素。

《国际金融讲义》PPT课 件

欢迎来到《国际金融讲义》PPT课件,本课程将带您进入精彩的金融世界,探 索全球经济的奥秘。

讲义说明

本讲义将深入介绍国际金融的关键概念和理论,帮助学员全面了解金融市场、 外汇市场和国际投资。

同时,本课程还将重点关注国际金融中的重要问题和挑战,如金融风险管理、 货币政策和贸易平衡。

小组讨论与案例分析

• 组织学员进行小组讨论 和案例分析,激发思维 和合作能力。

• 通过讨论和分析实际问 题,提高学员的问题解

• 决鼓能励力学。员提出自己的见 解和观点,培养批判性 思维和创新能力。

课堂练习和作业

• 提供课堂练习和作业, 帮助学员巩固所学知识

• 和通技过能练。习和作业,评估 学员的学习进展和理解

通过学习本讲义,学员将具备全球金融领域所需的知识和技能,为未来的职 业发展奠定坚实基础。

课程目标

1 深入了解国际金融体系

掌握国际金融市场的基本原则和操作方法。

2 分析并应对金融风险

了解金融市场中的风险因素,学会有效管理 和应对风险。

3 理解货币政策的重要性

掌握货币政策对经济的影响,了解各国央行 的政策措施。

3

第三章

金融风险的种类和评估,金融衍生品的使用与管理。

《国际金融教案》课件

《国际金融教案》课件第一章:国际金融概述1.1 教学目标了解国际金融的基本概念和定义理解国际金融市场的作用和重要性掌握国际金融的基本要素和参与者1.2 教学内容国际金融的定义和范围国际金融市场的作用和重要性国际金融的基本要素:汇率、外汇、国际资本流动国际金融的参与者:各国政府、金融机构、国际组织1.3 教学方法采用多媒体课件进行讲解结合具体案例分析,加深学生对国际金融的理解进行小组讨论,促进学生思考和交流1.4 教学评估进行课堂提问,检查学生对国际金融基本概念的理解第二章:外汇市场2.1 教学目标了解外汇市场的定义和功能掌握外汇市场的交易机制和交易工具理解外汇市场的主要参与者和影响因素2.2 教学内容外汇市场的定义和功能外汇市场的交易机制:即期交易、远期交易、期货交易外汇市场的交易工具:外汇合约、外汇期权外汇市场的主要参与者:商业银行、企业、政府、投机者2.3 教学方法通过案例分析和实际数据展示,讲解外汇市场的运作机制利用模拟交易软件,让学生进行外汇市场的交易操作进行小组讨论,分析外汇市场的主要参与者和影响因素2.4 教学评估进行课堂提问,检查学生对外汇市场的理解布置课后作业,要求学生分析具体的外汇市场案例,阐述交易机制和交易工具的使用第三章:汇率决定理论3.1 教学目标理解汇率的决定机制和影响因素掌握汇率决定的经典理论和现代理论分析汇率波动的原因和影响3.2 教学内容汇率的决定机制:市场供求关系、经济基本面、政策干预汇率决定的经典理论:金本位制度下的汇率决定、购买力平价理论汇率决定的现代理论:资产市场模型、黏性价格模型汇率波动的原因和影响:经济指标、政策变动、突发事件3.3 教学方法通过图表和数据,讲解汇率决定机制和影响因素分析具体案例,阐述汇率决定的经典理论和现代理论进行小组讨论,探讨汇率波动的原因和影响3.4 教学评估进行课堂提问,检查学生对汇率决定理论的理解布置课后作业,要求学生分析具体的汇率波动案例,阐述影响因素和影响结果第四章:国际资本流动4.1 教学目标了解国际资本流动的定义和特点掌握国际资本流动的类型和动机分析国际资本流动的影响和风险4.2 教学内容国际资本流动的定义和特点国际资本流动的类型:直接投资、证券投资、其他投资国际资本流动的动机:利润动机、风险分散动机、资产配置动机国际资本流动的影响:经济增长、汇率波动、金融稳定4.3 教学方法通过案例分析和实际数据,讲解国际资本流动的定义和特点利用模拟投资游戏,让学生体验国际资本流动的动机和过程进行小组讨论,分析国际资本流动的影响和风险4.4 教学评估进行课堂提问,检查学生对国际资本流动的理解布置课后作业,要求学生分析具体的国际资本流动案例,阐述影响和风险第五章:国际金融市场5.1 教学目标理解国际金融市场的种类和功能掌握国际金融市场的运作机制和特点分析国际金融市场的主要参与者及其策略5.2 教学内容国际金融市场的种类:货币市场、债券市场、资本市场、衍生品市场国际金融市场的功能:资金筹措、风险管理、资产配置国际金融市场的运作机制:市场准入、交易规则、监管体系国际金融市场的主要参与者:商业银行、投资银行、对冲基金、主权财富基金5.3 教学方法通过案例分析和实际数据,讲解国际金融市场的种类和功能利用模拟金融市场游戏,让学生体验国际金融市场的运作机制进行小组讨论,分析国际金融市场的主要参与者及其策略5.4 教学评估进行课堂提问,检查学生对国际金融市场的理解布置课后作业,要求学生分析具体的国际金融市场案例,阐述运作机制和特点第六章:国际金融政策6.1 教学目标理解国际金融政策的概念和目标掌握国际金融政策的工具和传导机制分析国际金融政策的实践和挑战6.2 教学内容国际金融政策的概念和目标:稳定汇率、控制通货膨胀、促进经济增长国际金融政策的工具:利率政策、汇率政策、公开市场操作国际金融政策的传导机制:货币供应、信用创造、投资和消费国际金融政策的实践和挑战:资本流动、政策协调、国际金融体系改革6.3 教学方法通过案例分析和实际数据,讲解国际金融政策的概念和目标利用模拟政策制定游戏,让学生体验国际金融政策的工具和传导机制进行小组讨论,分析国际金融政策的实践和挑战6.4 教学评估进行课堂提问,检查学生对国际金融政策的理解布置课后作业,要求学生分析具体的国重点和难点解析1. 第一章至第五章的基础概念和理论:这些章节涵盖了国际金融的基本概念、外汇市场、汇率决定理论以及国际资本流动等内容,是理解国际金融运作的基础。

《国际金融学》课件

03

外汇市场与汇率

外汇市场概述

外汇市场的定义

外汇市场是全球各国货币交换的场所,主要参与者包括中央银行 、商业银行、跨国公司以及投资银行等。

外汇市场的功能

外汇市场的主要功能是提供货币兑换服务,帮助人们进行国际支付 和跨国投资等活动。

外汇市场的参与者

外汇市场的参与者主要包括外汇交易商、进出口商、跨国公司、中 央银行等。

03

欧洲货币市场与离岸金融市场的区别

欧洲货币市场主要服务于国际商业和贸易融资,而离岸金融市场则主要

服务于投资和投机活动。

国际金融市场的全球化趋势

全球化趋势的表现

国际资本流动加速、跨国公司扩张、国际金融监管合作加强等。

全球化趋势的影响

促进全球经济的增长和发展、提高资源配置效率、增加金融市场的 竞争和风险等。

汇率制度与政策

固定汇率制度

固定汇率制度是指一国政府通过 各种措施将本国货币的汇率固定 在一个特定的水平上。

浮动汇率制度

浮动汇率制度是指一国政府不干 预外汇市场,让市场力量决定本 国货币的汇率。

汇率政策

汇率政策是指一国政府通过各种 措施影响本国货币的汇率,以达 到一定的经济目标。

04

国际资本流动与金融危机

详细描述

国际金融学涵盖了多个方面的理论,如国际收支理论主要研究各国之间的贸易和投资往来如何影响各国的经济状 况;外汇汇率理论则关注各国货币之间的交换比率及其决定因素;国际资本流动理论探讨资本跨国流动的原因和 影响;国际货币体系理论则研究全球货币体系的运作和改革。

国际金融学的研究方法

总结词

国际金融学的研究方法主要包括实证研究和 规范研究两种。

和家庭等。

国际金融市场的功能

国际金融课件internationalfinance

06

中国国际金融的实践与展望

中国国际金融业在规模和业务范围上不断扩大,成为全球金融市场的重要参与者。

中国国际金融业在推动经济增长、促进国际贸易和投资等方面发挥了重要作用。

改革开放以来,中国国际金融业经历了从无到有、从小到大的发展历程,逐步建立起较为完善的金融机构体系和金融市场体系。

中国国际金融的发展历程与现状

Global financial markets facilitate the flow of capital across borders, allowing for the efficient allocation of resources and the hedging of risks.

Regional financial markets serve specific geographical regions and are often associated with trade blocs or economic unions.

01

国际金融危机的定义

由于国际金融市场上的过度投机、金融监管缺失等原因,导致国际金融市场出现大规模动荡,影响各国经济的稳定。

02

国际金融危机的传染机制

通过贸易、金融和信息等渠道,将危机从一个国家传递到另一个国家。

国际金融危机及其传染机制

1

2

3

通过监测和分析国际金融市场的相关信息,及时发现潜在的风险点,采取应对措施。

02

03

04

05

Main International Financial Centers and Their Characteristics 主要国际金融中心及其特点

ห้องสมุดไป่ตู้

《国际金融第十章》PPT课件

Krugman’s trilemma克鲁格曼“三元asic Model

美国经济学家弗莱明(J. Flemming)和蒙代尔(R. Mundell)分别于1962年至1963年发表有关文章, 运 用 凯 恩 斯 主 义 的 IS—LM—BP 曲 线 , 继 续 研 究 斯旺曲线模型提出的政策性难题。他们的主要贡 献是分析了财政政策和货币政策对一国经济内部 和外部均衡的不同作用,并且着重探讨了国际资 本流动的影响,他们的研究成果被称为蒙代尔— —弗莱明模型(M-F )。

精选PPT

9

1、丁伯根原则(Tinbergen’s Principle)

• 丁伯根(J·Tinbergen)最早提出将政策目标和政 策工具联系在一起的正式模型,指出要实现若干 个独立的政策目标,至少需要相互独立的若干个 有效的政策工具。 但是,丁伯根原则假设各种政策工具可以供政策 当局集中控制,而且没有指出政策工具调控的侧 重点。

精选PPT

11

• 如果资本完全流动,汇率政策则无效;只 有一种支出政策工具,斯旺搭配无效;

• 没有区分支出政策工具中的财政政策与货 币政策

精选PPT

12

3、政策指派(Assignment)的 有效市场分类原则

• 罗伯特·蒙代尔(Robert Mundell)提出了关于 政策指派的有效市场分类原则。(the principle of effective market classification)

internal and external equilibrium • (三) Assignment of Policies

国际金融PPT课件课件

2、外汇价格

E=S$/US$

SUS$

1.50 1.40 1.30

0

100 200

《国际金融》PPT课件

D US$ 300 US$

2、外汇价格

a)代理商供应或需求 $:

– 商品交易者:出口商向外国人出售商品,得 到$;同时进口商从海外购买商品,并支付$。

– 投资者:外国投资者用$换购S$,去购买SIA 发行的股票。新加坡的投资者用S$兑换成$, 去购买IBM的股票。

资本流入

$供给曲线外移

– S$的预期

投机资本

《国际金融》PPT课件

$供给曲线外移

3、外汇对冲、投机与套利

1)对冲与投机

由于汇率的波动,外汇市场的参与者因为汇 率的不确定性就可能使“未平仓交易”盈利 或亏损。面对汇率风险有两种表现: a)风险回避者:进行对冲来避免汇率风险, 或者将未平仓交易平仓。 b)风险获得者:进行投机,或不平仓。

《国际金融》PPT课件

2、外汇价格

2)固定、完全浮动和管理浮动汇率

a)固定汇率: – 管理当局将汇率固定在某一特定水平,不在

市场上进行操作。所以货币受到控制,不可 自由兑换。黑市交易盛行。

– 金本位或金汇兑本位制:汇率固定与黄金价 格挂钩。如1880-1914,1947-1971

– 贬值(升值):管理当局审慎地提高(降低) 汇率水平

3、外汇对冲、投机与套利

i)对销套利:

国际资本流动是无汇率风险的。这得益于风 险回避者进行的对冲。例如: S$对US$的即期汇率是:E=US$/S$1=US$ 即,S$1=(1/E) US$ 30天的远期汇率是: E30=US$/S$1=US$ 现在投资者想要购买US T-bill(30天)

最新国际金融讲义(上海海事大学潘国陵教授)

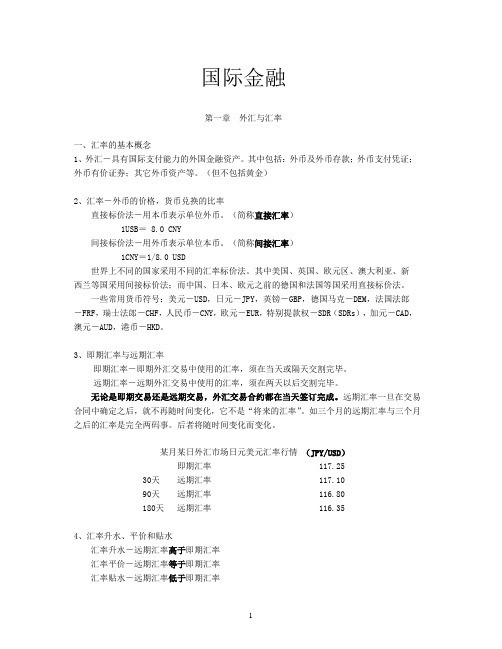

国际金融第一章外汇与汇率一、汇率的基本概念1、外汇-具有国际支付能力的外国金融资产。

其中包括:外币及外币存款;外币支付凭证;外币有价证券;其它外币资产等。

(但不包括黄金)2、汇率-外币的价格,货币兑换的比率直接标价法-用本币表示单位外币。

(简称直接汇率)1USB= 8.0 CNY间接标价法-用外币表示单位本币。

(简称间接汇率)1CNY=1/8.0 USD世界上不同的国家采用不同的汇率标价法。

其中美国、英国、欧元区、澳大利亚、新西兰等国采用间接标价法;而中国、日本、欧元之前的德国和法国等国采用直接标价法。

一些常用货币符号:美元-USD,日元-JPY,英镑-GBP,德国马克-DEM,法国法郎-FRF,瑞士法郎-CHF,人民币-CNY,欧元-EUR,特别提款权-SDR(SDRs),加元-CAD,澳元-AUD,港币-HKD。

3、即期汇率与远期汇率即期汇率-即期外汇交易中使用的汇率,须在当天或隔天交割完毕。

远期汇率-远期外汇交易中使用的汇率,须在两天以后交割完毕。

无论是即期交易还是远期交易,外汇交易合约都在当天签订完成。

远期汇率一旦在交易合同中确定之后,就不再随时间变化,它不是“将来的汇率”。

如三个月的远期汇率与三个月之后的汇率是完全两码事。

后者将随时间变化而变化。

某月某日外汇市场日元美元汇率行情(JPY/USD)即期汇率 117.2530天远期汇率 117.1090天远期汇率 116.80180天远期汇率 116.354、汇率升水、平价和贴水汇率升水-远期汇率高于即期汇率汇率平价-远期汇率等于即期汇率汇率贴水-远期汇率低于即期汇率远期汇率–即期汇率汇率升水 = ———————————×100%即期汇率这里的“高于”或“低于”全是指货币的内在价值,不是指汇率的数值。

对直接汇率来说,汇率升水为负值;对间接汇率来说,汇率升水为正值。

汇率的升水、贴水、平价是专门用来反映在一个时点上即期汇率与远期汇率之间关系的。

国际金融课件

国际金融体系的发展历程

01

早期的国际金融体系

以金本位制度为基础,通过黄金的自由流动和固定汇率制度来维持国际

货币秩序。

02

布雷顿森林体系

1944年布雷顿森林会议确立了以美元为中心的国际货币体系,通过双

挂钩制度(美元与黄金挂钩,其他货币与美元挂钩)来维持汇率稳定。

03

牙买加体系

1976年牙买加协议后,国际货币体系进入浮动汇率时代,多种货币并

04

国际金融机构

BIG DATA EMPOWERS TO CREATE A NEW

ERA

国际货币基金组织

宗旨

促进国际货币合作、稳定汇率、扩大国际货币流通等 。

职能

制定成员国间的汇率政策和经常项目的支付以及货币 兑换性方面的规则,并进行监督;对发生国际收支困 难的成员国在必要时提供紧急资金融通,避免其他国 家受其影响;为成员国提供有关国际货币合作与协商 等会议场所;促进国际间的金融与货币领域的合作; 促进国际经济一体化的步伐;维护国际间的汇率秩序 ;协助成员国之间建立经常性多边支付体系等。

存,国际金融市场得到迅速发展。

国际金融体系的核心机构

国际货币基金组织(IMF)

01

负责促进国际货币合作、稳定汇率、提供临时性财政援助等。

世界银行(WB)

02

提供长期贷款和技术援助,支持发展中国家减少贫困和促进经

济发展。

国际清算银行(BIS)

03

促进各国中央银行之间的合作,为国际金融市场提供清算和支

主要内容

国际储备多元化、汇率安排多样化、 多种渠道调节国际收支。

对世界经济的影响

多元化的国际储备结构为国际经济提 供了多种清偿货币,摆脱了布雷顿森 林体系下对美元的过分依赖;多样化 的汇率安排适应了多样化的、不同发 展水平的各国经济,为各国维持经济 发展与稳定提供了灵活性与独立性; 多种渠道调节国际收支,使国际收支 的调节更为有效与及时。

(2024年)《国际金融》ppt课件

提供短期资金支持,促进国际货币合 作;提供长期贷款和技术援助,支持 发展中国家经济发展;提供清算和支 付服务,维护国际金融稳定等。

23

国际金融合作的形式与内容

国际金融合作的形式

包括政府间合作、国际金融机构合作、商业银行合作等。

国际金融合作的内容

涉及货币政策协调、金融市场监管、国际支付体系改革、国际金融机构改革等。

2024/3/26

20

国际资本流动与跨国公司财务管理的关系

2024/3/26

相互影响

国际资本流动影响跨国公司的融资和投资决策,而跨国公 司的财务管理也影响国际资本流动的规模和方向。

相互促进

国际资本流动为跨国公司提供了更广阔的融资和投资渠道 ,而跨国公司的财务管理则通过优化资源配置和风险管理 等手段,提高了国际资本的使用效率。

响。

速度快

02

随着金融科技的发展,国际资本流动速度加快,市场反应更加

迅速。

影响因素多

03

国际资本流动受汇率、利率、政策等多种因素影响,具有不确

定性。

17

跨国公司财务管理的内容与目标

资金管理

包括资金的筹集、使用和分配等。

风险管理

识别和评估各种风险,并采取相应措施进行防范和控制。

2024/3/26

18

12

国际金融工具的种类与特点

传统金融工具

包括外汇、股票、债券等,具有 标准化、流动性强和透明度高等

特点。

2024/3/26

衍生金融工具

包括期货、期权、互换等,具有高 风险、高收益和杠杆效应等特点。

创新金融工具

包括结构化产品、资产证券化产品 等,具有定制化、灵活性和复杂性 等特点。

《导论国际金融》课件

交易更加普遍。

金融机构国际化

随着全球化的发展,金融机构的跨 国经营和跨境服务变得更为重要, 许多大型金融机构在全球范围内开 展业务。

金融监管的挑战

全球化对金融监管提出了更高的要 求,如何确保跨国金融机构的合规 性和金融稳定成为重要议题。

通过调整国内外投资政策,影响资本 流动,从而调节国际收支不平衡。

PART 03

外汇市场与汇率

外汇市场的构成与功能

总结词

外汇市场的构成与功能概述

外汇市场参与者

包括中央银行、商业银行、跨国公司、经 纪人等,各自扮演着不同的角色。

外汇市场交易品种

外汇市场功能

包括即期外汇交易、远期外汇交易、掉期 外汇交易以及外汇期货交易等。

PART 05

国际货币体系

国际货币体系的演变与类型

演变

国际货币体系经历了金本位制、布雷 顿森林体系和牙买加体系等阶段。

类型

国际货币体系主要分为固定汇率制度 和浮动汇率制度两种类型。

汇率制度与政策协调

汇率制度

指各国政府为了规范外汇市场而采取的一系列措施,包括汇率的确定、调整和维持等。

政策协调

指各国政府在国际经济合作中,通过协商和合作,共同制定和实施货币政策、财政政策 等经济政策,以实现全球经济稳定和发展的目标。

PART 04

国际金融市场与投资

国际金融市场的类型与特点

国际金融市场的分类与特性

国际金融市场可以根据不同的标准进行分类,如按照交易对象可以分为外汇市场 、股票市场、债券市场等。每种市场都有其独特的特点和功能,如外汇市场主要 进行货币兑换和外汇交易,股票市场则为企业融资和投资者提供投资机会。

国际金融讲义

国际金融目录Chapter1 国际收支Chapter2 外汇与汇率Chapter3 外汇市场与外汇交易Chapter4 外汇风险管理Chapter5 外汇管制Chapter6 国际储备Chapter7 国际金融市场Chapter8 国际资本流动与国际债务Chapter9 对外贸易融资Chapter10 国际货币体系Chapter11 国际金融组织Chapter12 国际结算进度提示1Chapter1 国际收支< R>Chapter2 外汇与汇率Chapter3 外汇市场与外汇交易Chapter4 外汇风险管理Chapter5 外汇管制Chapter6 国际储备Chapter7 国际金融市场Chapter8 国际资本流动与国际债务Chapter9 对外贸易融资Chapter10 国际货币体系Chapter11 国际金融组织Chapter12 国际结算Chapter1 国际收支教学目的掌握国际收支的概念掌握国际收支平衡表结构和编制方法明白国际收支失衡的含义,弊端懂得分析国际收支失衡的原因介绍国际收支失衡的调整措施§1 国际收支概述国际收支(balance of payment):是以统计报表的方式,对特定时期内一国的经济主体(居民)与他国经济主体(非居民)之间的各项经济交易的货币价值总和.从三个方面理解:国际收支是一个流量概念.国际收支反映的内容是以货币记录的交易,它不是以收支为基础,而是以交易为基础,有些交易可能不涉及货币支付,但这些不涉及货币收支的交易需折算成货币交易记录.交易包括:交换(含实际资源和金融资产的交换),转移(无补偿转移,如赠款),移居(伴随的资产负债转移),其他根据推论而存在的交易(如海外收益在海外再投资).国际收支记录的是一国居民与非居民之间的交易.判断一项交易是否应包括在国际收支的范围内,所依据的不是交易双方的国籍,而是依据交易双方是否有一方是该国居民.国际收支相关概念―居民与非居民居民:指一个国家的经济领土内具有一经济利益中心的经济单位.包括居民官方(坐落在该国领土上的各级政府机构以及派驻国外的政府机构,在外国的军事基地等),居民企业(在该国领土上生产货物或提供劳务的企业),个人(在该国居住期限在一年以上的个人,不论其国籍,但外交官,驻外军事人员除外),非盈利团体.一国经济领土:一般包括一个政府所管辖的地理领土,包括该国天空,水域和邻近水域下的大陆架,以及该国在世界其他地方的飞地.依照这一标准,一国大使馆等驻外机构是所在国的非居民,而国际组织是任何国家的非居民.一国经济领土内经济利益中心:是指该单位在某国的经济领土内在一年或一年以上的时间中已经大规模地从事经济活动或交易,或计划如此行事.经济体的居民单位主要组成:家庭和组成家庭的个人;法定实体和社会团体.国际收支范围界定:指居民与非居民之间的全部交易.居民之间的交易属于国内经济交易.非居民与非居民之间的经济交易不能纳入该国的国际收支统计范围.我国的居民单指大陆居民. 国际收支相关概念―涵盖范围国际收支以经济交易为基础:经济交易不仅包括涉及到外汇收支的交易,而且包括尚未实现(如预收,预付)和不涉及到外汇收支的交易(如易货贸易),因而称为广义的国际收支概念..时间界定:一般以一年为统计期,大多数国家以公历年度为一个统计期间.统计原则:权责发生制(应计制或应收应付制)作为判断标准,来确定收入和支出.一般以所有权的变更与否进行判断.注意:国际收支是流量概念,即只统计当期发生的对外经济交易金额.流量与存量:流量是指一定的时期内测算出来的价值,存量是指一定的时点上测算出来的价值.存量的变化量等于流量.国际收支相关概念―计价计价基础:市场价格.市场价格:在自愿基础上买方从卖方获取某种物品而支付的货币金额.注意:市场价格是特定交易价格(如株冶的锌价),而不等同于其他任何内容相仿的交易的总体价格,如市场报价,国际市场价格等.市场价格不等同于自由市场价格,即不能认为市场交易是在纯粹的竞争市场环境下进行的.市场交易可以在垄断与其他形式的市场结构下进行.交易双方必须是独立的,有独立自主决定价格或是否成交的权利.在某些情况下,市场价格可能不存在,如易货贸易,税收支付,企业分支机构与母公司的交易,单方面转移,优惠的政府贷款,非商业性交易等,应参照市场定价核算.国际收支相关概念―记帐单位和折算办法记帐单位:不同国家的经济交易的计价与结算币种可能不同,有的用某种国家的货币计价或结算,有的以特别提款权或欧元来表示.任何国家都必须折算成单一的记帐单位,以便汇总;国际组织需要一个标准或通用的记帐单位以便汇总地区或全球的数据,并有助于开展国际间比较. 选择记帐单位的原则:第一,该单位币值相对稳定;第二,为大多数使用国家收支统计资料的人所熟悉.实践中,各国按国内使用的记帐单位编制统计报表,国际货币基金组织将各国的报表折算为一种在现阶段认为最稳定的通用记帐单位.折算办法:将交易货币折算成国际收支平衡表记帐单位最合适的汇率是交易日的市场汇率(通常情况);如果市场汇率不存在的话,应使用最短时期内的平均汇率(如假期);在多重汇率体系下,不同种类的交易所使用的汇率有两个或者更多,此时折算可以采用单一汇率,即对外交易的所有官方汇率的加权平均值,或采用某种适用于大多数对外交易的实际汇率.§2 国际收支平衡表国际收支平衡表(Balance of Payments Statement):是一个国家在一定时期内(一年,半年,一季或一个月)所有对外外汇收支的系统记录,并应用会计原则,按照会计核算的借贷平衡方式编制,经过调整最终达到帐面上收付平衡的统计报表.国际收支平衡表结构:它包括经常项目(Current Account),资本项目(Capital Account),平衡项目三大类.经常项目是其中最重要,最基本的项目,是一个实项目,其所记录的各项交易都是以所有权的转移为特征的.资本项目反映的是以货币表示的债权,债务在国际间的变动,所记录的交易是以转换使用权而所有权不变为特征的.因此因借贷资本而衍生之利息,股利,利润等则属于经常项目项下的劳务收支.平衡项目是对自主性交易出现缺口或差额时进行的弥补性交易的记录,以及为最终正式帐面平衡所进行会计调整的记录,其作用在于最终实现国际收支平衡表中外汇收入与外汇支出相等,达成帐面上的平衡.记帐规则记帐规则:国际收支帐户运用的是复式记帐法,即每笔交易都是由两笔价值相等,方向相反的帐目表示.根据复式记帐的惯例,不论是对于实际资源还是金融资产,借方表示经济体资产(资源)持有量的增加,贷方表示资产(资源)持有量的减少.国际收支帐户可分为两大类:经常帐户,资本与金融帐户.记入借方的帐目包括:反映进口实际资源的经常项目;反映资产增加或负债减少的金融项目. 记入贷方的帐目包括:表示出口实际资源的经常项目;反映资产减少或负债增加的金融项目. 更具体来说:进口商品属于借方项目,出口商品属于贷方项目;非居民为本国居民提供服务或从本国取得收入属于借方项目,本国居民为非居民提供服务或从外国取得收入属于贷方项目;本国居民对非居民的单方转移属于借方项目,本国居民收到国外的单方转移属于贷方项目;本国居民获得外国资产属于借方项目,外国居民获得本国资产或对本国投资属于贷方项目;本国居民偿还非居民债务属于借方项目,非居民偿还本国居民债务属于贷方项目;官方储备增加属于借方项目,官方储备减少属于贷方项目.经常帐户―经常项目经常帐户是指对实际资源在国际间的流动行为进行记录的帐户,包括四个项目:(1)货物(goods):包括一般商品,用于加工的货物,货物修理,各种运输工具在港口购买的货物和非货币黄金.在处理上,货物的出口和进口应在货物的所有权从一居民转移到另一居民时记录下来.一般来说,货物按边界离岸价(free of board,简称FOB)计价.(2)服务(services):服务是经常项目的第二大项目,包括运输,旅游以及在国际贸易中越来越重要的其他项目(通讯,金融和计算机服务,专用权征用和特许以及其他商业服务).(3)收入(income):包括居民和非居民之间进行的两大交易,一是支付给非居民工人(如季节性的短期工人)的报酬,二是投资收入项下有关对外金融资产和负债的收入和支出(主要是有关直接投资,证券投资和其他投资的收入和支出以及储备资产的收入,最常见的投资收入是股本收入――红利和债务收入――利息.(4)经常转移(current transfer):当一计价实体的居民实体向另一非居民实体无偿提供了实际资源或金融产品时,按照复式记帐原理,需要在另一方进行抵消性记录以达到平衡,也就是需要建立转移帐户作为平衡项目.包括固定资产所有权的资产转移;同固定资产收买或放弃相联系的或以其为条件的资产转移;债权人不索取任何回报而取消的债务.资本与金融项目资本与金融帐户是指对资产所有权在国际间流动行为进行记录的帐户,包括资本帐户和金融帐户.(1)资本帐户:包括资本转移和非生产,非金融资产的收买或放弃.非生产,非金融资产的收买或放弃是指各种无形资产如专利,版权,商标,经销权以及租赁和其他可转让合同的交易.(2)金融帐户:包括一经济体对外资产和负债所有权变更的所有权交易.可以分为直接投资,证券投资,其他投资,储备资产四类.金融帐户的各个项目并不按借贷方总额来记录,而是按净额来记入相应的借方和贷方.直接投资(direct investment):主要特征是投资者对另一经济体的企业拥有永久权益,对企业的经营管理施加着相当大的影响.可以采取在国外直接建立分支企业的形式,也可以采用购买国外企业10%以上的股票的形式.证券投资(portfolio investment):主要对象是股票证券和债务证券.对于债券而言,可以细分为期限在一年以上的中长期债券,货币市场工具和其他派生金融工具.其他投资(other investment):这是一个剩余项目,包括所有直接投资,证券投资或储备资产未包括的金融交易.储备资产(reserve assets):包括货币当局可随时动用并控制在手的外部资产,可以分为货币黄金,特别提款权,在基金组织的储备头寸,外汇资产(包括货币,存款和有价证券)和其他债权.净误差与遗漏由于不同帐户的统计资料来源不一,记录时间不同以及一些人为因素(如虚报出口)等原因,会造成结帐时出现净的借方或贷方余额,这是就需要人为设立一个抵消帐户,数目与上述余额相等而方向相反. 如果借方总额大于贷方总额,其差额记入项目的贷方;反之,记入项目的借方. 其他概念国民收入:是反映一国一定时期(通常为一年)投入的生产资源所产出的最终产品和服务的市场价值或由此形成的收入的一个数量指标.国民收入是一个流量概念.国内生产总值(gross domestic products,GDP):是以一国领土为标准,指的是在一定时期内一国境内生产的产品与服务总值.国民生产总值(gross national products,GNP):是以一国居民为标准,指的是在一定时期内一国居民生产的产品与服务总值.一般主要采用GNP概念.封闭条件下的国民收入帐户在封闭条件下,全部产品或服务都是由本国居民在本国领土上生产出来的.从产品的最终支出角度看,可以分为:私人消费(C),私人投资(I),政府支出(G);从收入来源角度看,可以分为私人消费(C),私人储蓄(SP),政府税收(T).C+I+G=Y=C+ SP+T→I= SP +(T-G)T-G=Sg(政府储蓄)总支出中未被用于私人消费和政府购买的部分――国民储蓄(S),它是由私人储蓄和政府储蓄两部分构成的.在封闭条件下,I=S.开放条件下的国民收入帐户在开放条件下,X代表进口,M代表出口,开放经济的国民收入等式为:Y=C+I+G+X-M产品和服务的出口与进口之间的差额称为贸易帐户余额(或净出口),记为TB,TB=X-M在很多国家,贸易帐户余额在国民收入中所占比重相当大,并且,在经济增长过程中,贸易帐户余额对国民收入增长率的贡献非常突出.进出口贸易是体现经济开放性的重要指标,出口占国民收入或者进出口总额占国民收入的比重是衡量一国经济开放程度的重要指标.GNP=GDP+NFP,NFP指本国从外国取得的净要素收入,包括付给工人的净报酬,净投资收入(直接投资与间接投资).CA=TB+NFP,CA称为经常帐户余额(current account balance)经常帐户的宏观经济分析当NFP=0时,CA=X-MC,I,G构成国内居民的总支出,称为国内吸收(domestic absorption),用A表示,即:A=C+I+G经常帐户是国民收入与国内吸收的差额,即:CA=Y-A.在开放条件下,一国的国民收入与国内支出可以不必相等.当CA>0时,称为贸易顺差;当CA<0时,称为贸易逆差,此时必须进口外国产品与服务来满足国内支出需求.CA反映国民收入与国内吸收之间的关系.国际投资头寸(international investment position,简称IIP),是指一国某一时点上对世界其它地方的资产与负债的概念.净国际投资头寸(net international investment position,简称NIIP),一国对外资产与负债相抵后的净值.一国某一时期内的经常帐户余额,会形成新的净国外资产或负债,造成本期的净国际投资头寸相对于上期发生的变化,即:CA=NIP-NIP-1.国际投资头寸综合反映了一国在海外的资产负债情况,经常帐户顺差造成一国国际投资头寸增加,逆差则导致国际投资头寸减少.CA=S-I,表明在开放条件下,一国投资与储蓄不必相等,当SI时,可以通过净出口带来的资本流出而形成海外资产.资本往往从经常帐户赢余国家流向赤字国家.§3 国际收支的失衡与调节国际收支失衡的原因经济发展的不平衡造成周期性失衡:在各国的经济增长过程中,由于经济制度,经济政策等原因会引发周期性经济波动,导致国际收支恶化.国际分工格局变化造成结构性失衡:一国的产业结构与国际分工结构失调,无法适应国际市场的需求,会引起该国的国际收支的失衡.货币价值的变动造成货币性失衡:当一国出现通货膨胀,物价上涨,短期内出口商品的价格没有竞争力,导致国际收支恶化,当一国出现通货紧缩,物价下降,短期内出口商品具有价格优势,国际收支顺差.国民收入的变动造成收入性失衡:当一国的国内和国外的政治和经济发生重大变化,引起国民收入的变动,也成为影响国际收支不平衡的重要因素.季节性和偶然性失衡:季节性变化对进出口产生影响;偶然性的短期灾害也影响进出口,但往往是暂时的.投机性失衡:在短期资本流动中,不稳定的投机和资本外逃也是造成国际收支失衡的重要原因.投机性资本流动是指利用利率差别与预期的汇率变动牟利的资本流动,取决于利率或汇率变动空间.国际收支失衡的调节方法商品调节.采取对出口商品给予补贴用优惠利率刺激出口等奖出限入的措施来改善国际收支逆差.实施金融政策.以调节利率或汇率的办法来平衡国际收支.当国际收支出现逆差,就利用提高再贴现率或使货币贬值来刺激出口,当国际收支出现顺差,则降低再贴现率或使货币升值以增加进口.实施财政政策.即以扩大和缩小财政开支或调节税率的办法来进行国际收支调节的政策措施.一般是采取增税减支来扭转国际收支逆差,采取减税增支来调节国际收支顺差.利用国际贷款.利用国际贷款来及时灵活地融通资金是最普遍使用的措施.直接管制.国家以行政命令的方式直接干预国际收支,包括外汇管制和外贸管制.进度提示2Chapter1 国际收支Chapter2 外汇与汇率Chapter3 外汇市场与外汇交易Chapter4 外汇风险管理Chapter5 外汇管制Chapter6 国际储备Chapter7 国际金融市场Chapter8 国际资本流动与国际债务Chapter9 对外贸易融资Chapter10 国际货币体系Chapter11 国际金融组织Chapter12 国际结算Chapter2 外汇与汇率教学目的掌握外汇和汇率的概念掌握汇率的分类,标价方法掌握影响汇率变动的因素掌握外汇风险的防范方法了解汇率的决定因素和汇率制度了解汇率变动对经济的影响§1 外汇与汇率外汇(foreign exchange):指以外国货币表示的并可用于国际结算的信用票据,支付凭证,有价证券以及外汇现钞.动态的外汇:是国际汇兑的简称,就是把一个国家的货币兑换成另外一个国家的货币,借以清偿国际间债权,债务关系的一种专门性的经营活动.静态的外汇:是一种以外币表示的支付手段,用于国际间的结算.是常用概念.《中华人民共和国外汇管理条例》规定的外汇内容1,外国货币:包括钞票,铸币等;2,外币有价证券:包括政府公债,国库券,公司债权,股票,息票等;3,外汇支付凭证:包括票据,银行存款凭证,邮政储蓄凭证;4,其他货币资金.外币支付凭证,信用凭证构成外汇的条件外币支付凭证或信用凭证构成外汇.必须具备三个要素1.外汇必须是外币表示的国外资产,而用本国货币表示的信用工具和有价证券是不能视为外汇的;2.外汇必须是在国外能得到补偿的债权,而空头支票和拒付的汇票不能视为外汇;3.外汇必须是能兑换成其他支付手段的外币资产,亦即可兑换货币表示的支付手段,而不可兑换货币表示的支付手段是不能视为外汇的.由以上的分析可知,外汇与外币不是同一概念,外汇包含可兑换的外币,同时还包括外币表示的支付凭证和信用凭证.而且并不是所有的外币都是外汇,只有可兑换的外币才能构成外汇. 国外货币代码THB泰珠KRW韩国元新加坡元SUR俄罗斯卢布PHP菲律宾比索NZD新西兰元MYR马来西亚林吉特IDR印尼盾ESP西班牙比塞塔PIE葡萄牙埃斯库多NLG荷兰盾LUF卢森堡法郎ITL意大利里拉IEP爱尔兰磅BEF比利时法郎FIM芬兰马克A TS奥地利先令HKD港币AUD澳大利亚元CAD加拿大元CHF瑞士法郎GBP英镑EUR欧元JPY日元美元RMB人民币货币符号货币名称货币符号货币名称外汇汇率外汇汇率(foreign exchange rate)----又称汇价,或称外汇行市,是两国货币折算的比率,或者说是一国货币以另一国货币表示的价格.外汇是一种特殊的商品,汇率就是这种特殊商品的价格.汇率具有双向表示的特点.◎一国货币对各种货币都有汇率.◎汇率有直接和间接两种标价方法.◎汇率制度大体有固定汇率制和浮动汇率制.外汇汇率的标价方法1直接标价法(direct quotation):又称应付标价法.它是指以一定单位的(1或100等)外国货币作为标准,折成若干单位的本国货币的标价方法.如某日国家外汇管理局公布的外汇牌价:HKD100=RMB106.06USD100=RMB827.75◎直接标价法表示买入一定单位的外币要支付多少本币,或卖出一定单位的外币应该收多少本币.◎使用直接标价法,汇率变动的数字大小与本币币值高低反方向,与外币币值高低同正向.若本币数额增加,则表明外币升值,本币贬值.◎目前除英国,美国,欧盟以外,世界上大多数国家都采取直接标价法.外汇汇率的标价方法2间接标价法(indirect quotation):又称应收标价法,它是以一定单位的(1或100等)本国货币为标准,折成若干外国货币的标价方法.◎使用间接标价法,汇率变动的数字大小与本币币值高低同方向,与外币币值高低反方向.若外币数增加,则表示本币升值,外币贬值.◎能够采取间接标价法的国家,都正在或曾经在国际政治及经济舞台上占有统治地位,其货币都曾经是最主要的国际货币.英国一直采用此法,美国除对英镑,欧元采用直接标价法外,均采用间接标价法.美元标价法(U.S.dollar quotation):指以美元为标准来表示各国货币的方法,美元是基准货币,其他货币是报价货币.◎美元标价法已成为现实.◎非美元之间的汇率通常通过各自对美元的汇率进行套算.外汇汇率种类官方汇率;市场汇率按外汇决定方式开盘汇率;收盘汇率按市场或银行营业时间即期汇率;远期汇率按外汇交割期限电汇汇率;信汇汇率;票汇汇率按外汇交易支付通知方式买入汇率;卖出汇率按银行买卖外汇固定汇率;浮动汇率按汇率制度基本汇率;套算汇率按汇率制定方法外汇汇率种类――按确定汇率的方法划分基本汇率(basic rate):指本国货币与关键货币对比制定出来的汇率.一国的基本汇率一般不对外公布,只是作为一种内部掌握起主导作用的汇率.一般以本币与美元的汇率作为基本汇率. 关键货币(key currency):指在国际贸易或国际收支中使用最多,在各国外汇储备中所占比重最大,自由兑换性最强,汇率行情最为稳定,事实上普遍为各国所接受的货币.一般以美元作为关键货币.套算汇率(cross rate):也称交叉汇率,指根据基本汇率套算出来的本币与其他国家货币的汇率.或者说,两国间的汇率是通过各自与第三方货币的汇率间接计算出来的.使用的参照货币由本国决定,不对外公布.我国外汇市场上公布对美元,欧元,日元和港币的基准汇率,对其他货币的汇率都是套算出来的.外汇汇率种类――按银行买入外汇的价格划分买入汇率(buying rate):又称买入价,指银行向同业或客户买入外汇时所使用的汇率.在直接标价法下,较低的汇率是买入价;在间接标价法下,较高的价格是买入价.卖出汇率(selling rate):又称卖出价,指银行向同业或客户卖出外汇时所使用的汇率.在直接标价法下,较高的价格是卖出价;在间接标价法下,较低的价格是卖出价.买入,卖出都是从银行的角度来看的,二者之间的差价是银行买卖外汇的收益.直接标价法下,前买后买,买低卖高;在间接标价法下,前卖后买,卖低买高.中间汇率(middle rate):指银行买入价和卖出价的平均数.中间汇率一般不挂牌公布.套算汇率一般用中间汇率计算.现钞汇率(bank notes rate):指银行收兑外汇现钞时所使用的汇率.国家一般不允许外币在本国流通,存在换汇的问题,银行也存在对外币现钞的保管,运送,保险等费用,这部分费用银行要在购买价格中予以扣除.所以,银行买入外汇现钞的汇率要低于外汇买入汇率.但是,现钞卖出汇率与现汇卖出汇率相同.我国使用的是直接标价法,某日外汇牌价示例:基准价卖出价现钞买入价现汇买入价汇买,汇卖中间价币种827.66828.9821.45826.42。

国际金融讲义

2019/11/10

17

(六)国际货币体系的改革

1.改革建议。

1)本位币:恢复金本位;

改进金汇兑本位制;

美元本位制;

国际通货本位。

(2)汇率问题:浮动汇率制;

爬行钉住汇率制;

复合汇率制;

汇率目标区方案。

2019/11/10

18

2.改革过程。

1972年9月,成立“20国委员会”。

本位货币:金币。

金币等同于黄金:

自由铸造,自由熔化,自由输入,自由输出。

关键货币:金币或黄金。

货币之间的比价由含金量确定。

2019/11/10

5

评价:

增长。

1具有刚性。 2货币的增长受制于黄金产量的

3黄金集中于发达国家。

2019/11/10

6

(二)国际金汇兑本位

资金

2019/11/10

35

1922年,日内瓦会议。针对国际支付手段不足

进行协调

构成新的体系:双挂钩制度

1.黄金依然是国际货币制度的基础,但金币不流通, 流通的纸币中规定了含金量。

2.本国货币通过与实行金本位制国家的货币挂钩,而 间接的与黄金挂钩。

3.本国货币需通过购买实行金本位制国家的货币之后 才可兑换黄金。

2019/11/10

29

(二). 缴 纳 基 金

份额:按份额各国须交一定的美圆价值的货币 黄金缴纳:25% 本国货币:75%

2019/11/10

30

(三). 份 额 分 布

发达国家

61%

不发达国家 39%

2024年度国际金融课件完整版

国家风险及管理

国家风险类型

包括政治风险、经济风险、法律风险 等。

国家风险管理策略

包括加强国别风险评估、建立国家风 险管理制度、使用国际政治和经济组

织提供的保险和担保工具等。

国际合作与监管

各国政府通过加强国际合作、完善国 际监管体系等措施来降低国家风险。

2024/2/2

36

金融衍生工具风险管理

2024/2/2

31

06

国际金融风险与管理

2024/2/2

32

国际金融风险概述

定义与分类

国际金融风险指因国际金融市场 变动、汇率波动、政策调整等因 素导致的金融机构或投资者遭受 损失的可能性,可分为市场风险 、信用风险、流动性风险等。

风险来源

包括全球经济环境的不稳定性、 金融市场波动、政治风险、法律 风险等。

功能

国际货币体系的主要功能包括确定国际清算和支付手段、确定国际储备资产、确定国际货 币关系、提供国际信贷或协调国际信贷关系等。

演变

国际货币体系经历了从金本位制、金汇兑本位制、布雷顿森林体系到牙买加体系的演变过 程。

21

金本位制度

特点

金本位制是以黄金作为本位货币的货币制度,具有自由铸造、自由兑换、自由输出入等 三大特点。

非洲开发银行

非洲开发银行是非洲大陆最重要的多边金融机构之一,致力于为非 洲国家的经济和社会发展提供资金支持和技术援助。

18

国际清算银行

01

成立背景与宗旨

国际清算银行(BIS)成立于1930年,旨在促进各国中央银行之间的合

作,为国际金融业务提供清算和结算服务。

02

组织机构与运作

BIS由全球主要国家的中央银行组成,通过提供清算、结算、外汇交易

国际金融讲义课件(ppt 85页)

四、汇率和国际交易 ➢汇率在国际贸易中具有核心的作用,这是因为汇率使我们 能够比较不同国家的商品和服务的价格。 ➢汇率与相对价格。当其他条件相同时,一国货币的升值, 使出口商品的相对价格上升,并使进口商品的相对价格下 降。反之,贬值则相反。

8

(七)国际金融学课程分类

➢西方讲授国际金融学一般有两种方式:一是作为一门独立的 课程,直接称为《国际金融》或《国际金融管理》;二是将国 际金融的主要内容包含在其他课程中讲授,如《国际经济学》 。

➢直接称为《国际金融》的教材又分为两类:一类是从宏观角 度来阐述国际金融,具有较强的理论性,适合于专业基础知识 学习使用;另一类是从微观角度来透视国际金融,偏重于实务 ,适合于应用研究。

3

二、国际金融学内容的不断丰富和发展

(一)国际收支调节理论的出现:价格——铸币流动机制 ➢十八世纪,英国古典政治经济学家对重商主义的保护政策展开了猛 烈的抨击,主张自由贸易政策。

➢大卫·休谟提出了有名的“价格——铸币流动机制”学说,这是国际 金融学关于国际收支调节理论的早期学说。

➢实践中,第一次世界大战以前的金本位制度时期,西方各国政府在 国际收支调节方面都奉行这一基本理论学说。

。

6

(五)国际金融市场和国际资本流动理论出现 ➢国际资本流动规模增加、国际外汇市场交易量扩大,成 为现代国际金融学有关国际金融市场和国际资本流动理论 研究的重要内容。 ➢20世纪70年代,金融创新方兴未艾和金融管制的放松为 跨国公司和跨国金融机构的发展提供了重要的金融制度环 境,使得它们逐渐成为世界经济和国际金融活动中的主导 力量。 ➢由此,金融自由化、投资机构化和金融交易电子化使得 国际金融资本的流动速度大大加快、流动规模更加庞大。 ➢国际金融市场上庞大的金融资本流动势必对国际货币体 系和汇率产生巨大的冲击,一方面使得汇率的决定和变动 变得更加难以确定,另一方面也经常引发货币危机和金融 危机,暴露出国际货币体系的内在缺陷。

2024年度《国际金融》课件

2024Байду номын сангаас3/23

特点

交易主体多样化、交易客体复杂化、交易方式电子化、市场 监管国际化。

12

国际金融市场的交易工具与方式

交易工具

股票、债券、期货、期权、外汇等。

交易方式

现货交易、期货交易、期权交易、信用交易等。

2024/3/23

13

国际金融市场的监管与合作

2024/3/23

监管

国际金融市场监管机构如国际货币基金组织(IMF)、世界银行(WB)等对国 际金融市场的运行进行监管,各国政府也通过制定相关法规和政策来规范本国金 融市场。

合作

各国政府和监管机构通过签订国际协议、建立国际合作机制等方式加强国际合作 ,共同维护国际金融市场的稳定和繁荣。例如,G20峰会就是各国政府加强国际 金融合作的重要平台之一。

14

04

国际金融机构与国际 金融法

2024/3/23

15

国际金融机构的构成与职能

2024/3/23

国际金融机构的构成

包括全球性国际金融机构(如国际货 币基金组织、世界银行等)和区域性 国际金融机构(如亚洲开发银行、欧 洲投资银行等)。

国际金融机构的职能

提供贷款和援助,促进成员国经济发 展和贸易;维护国际货币体系稳定, 推动国际货币合作;提供技术援助和 培训,帮助成员国提高经济管理水平 。

16

国际金融法的渊源与内容

国际金融法的渊源

主要包括国际条约、国际惯例和国内 立法。其中,国际条约是国际金融法 的主要渊源,如《国际货币基金组织 协定》、《世界银行协定》等。

金融科技带来的风险与挑战

金融科技的发展也带来了新的风险和挑战,如网络安全、 数据隐私保护、市场操纵等问题,需要国际社会共同应对 和监管。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Irwin/McGraw-Hill

Copyright © 2001 by The McGraw-Hill Companies, Inc. All rights

The current spot rate is $1.5530, and the forward rate is $1.5450 for six months.

If change at spot rate: 1.5530x50,000=77,650

The firm will sell £50,000 for a maturity window of June 10th through July 9th: 50,000x1.5450=$77,250

(2): The importer can buy £335,570 forward for 90 days: 335,570x1.4867=$498,892

In 90 days’s time, the importer has to deliver $498,892

(3)Suppose the pound appreciates to $1.60 during the 90 days, the cars would cost the company the following amount: 1.60x335,570=537,000

Irwin/McGraw-Hill

Copyright © 2001 by The McGraw-Hill Companies, Inc. All rights

Forward Contract

A forward contract is an agreement between a corporation and a commercial bank to exchange a specified amount of a currency at a specified exchange rate (called the forward rate) on a specified date in the future.

Irwin/McGraw-Hill

Copyright © 2001 by The McGraw-Hill Companies, Inc. All rights

Forward Market

Forward contracts are used to reduce the risk that foreign exchange rate change will adversely affect transactions that will be settled in the future.

Irwin/McGraw-Hill

Copyright © 2001 by The McGraw-Hill Companies, Inc. All rights

Currency Derivative

Currency Forward Currency Future Currency Options

The company has saved more than $1,000 on the original contract to avoide a loss of $37,000.

Irwin/McGraw-Hill

Copyright © 2001 by The McGraw-Hill Companies, Inc. All rights

Eg. Assume an American car dealer expects to import ten Jaguar motor cars in 90 days from now. The Jaguar Motor car company quotes a price for ten cars at £335,570.The current spot rate is $1.49/ £.And the forward rate quoted for 90 days is $1.4867/ £. How will the company hedge the risk?

Irwin/McGraw-Hill

Copyright © 2001 by The McGraw-Hill Companies, Inc. All rights

Forward Contract

When a firm anticipate future need or future receipt of a foreign currency, they can set up forward contracts to lock in the exchange rate, hedge the risk.

10

The Currency Derivatives Market (Chapter 7)

Irwin/McGraw by The McGraw-Hill Companies, Inc. All rights

Essential Reading

P172-181

Irwin/McGraw-Hill

Copyright © 2001 by The McGraw-Hill Companies, Inc. All rights

Forward Contract

(1) If change GBP into USD at spot rate, the company has to pay: 335,570x1.49=$500,000

Forward Contract

Example:

XYZ company, a US manufacturer receives a purchase order from a customer in England on Jan.10th. The invoice is £50,000 and payment is due on June 10th.