财务报表分析-(台湾中兴大学)chap008

分析中兴通讯的财务报告(3篇)

第1篇一、前言中兴通讯(ZTE Corporation)是中国领先的通信设备和网络解决方案提供商,成立于1985年,总部位于深圳。

中兴通讯致力于为全球运营商、政企客户和消费者提供创新的产品、解决方案和服务。

本文将对中兴通讯的财务报告进行深入分析,旨在了解其财务状况、经营成果和发展趋势。

二、中兴通讯财务报告概述1. 财务报表中兴通讯的财务报表包括资产负债表、利润表和现金流量表。

以下是2019年度财务报表的主要数据:(1)资产负债表资产总计:人民币2,563.19亿元负债总计:人民币1,979.28亿元所有者权益:人民币583.91亿元(2)利润表营业收入:人民币1,020.7亿元营业利润:人民币-35.5亿元利润总额:人民币-7.6亿元净利润:人民币-2.7亿元(3)现金流量表经营活动产生的现金流量净额:人民币76.7亿元投资活动产生的现金流量净额:人民币-56.1亿元筹资活动产生的现金流量净额:人民币-21.3亿元2. 财务指标(1)资产负债率资产负债率=负债总额/资产总额×100%2019年资产负债率为:1,979.28/2,563.19×100%=77.18%(2)毛利率毛利率=(营业收入-营业成本)/营业收入×100%2019年毛利率为:(1,020.7-820.5)/1,020.7×100%=18.85%(3)净资产收益率净资产收益率=净利润/所有者权益×100%2019年净资产收益率为:-2.7/583.91×100%=-0.46%三、财务报告分析1. 资产负债状况(1)资产结构从资产负债表可以看出,中兴通讯的资产主要由流动资产和非流动资产构成。

流动资产占比最高,说明公司在日常运营中拥有充足的流动资金。

非流动资产主要包括固定资产、无形资产和长期投资等,表明公司在长期发展方面具备一定的实力。

(2)负债结构中兴通讯的负债主要由流动负债和非流动负债构成。

中兴财务报表分析

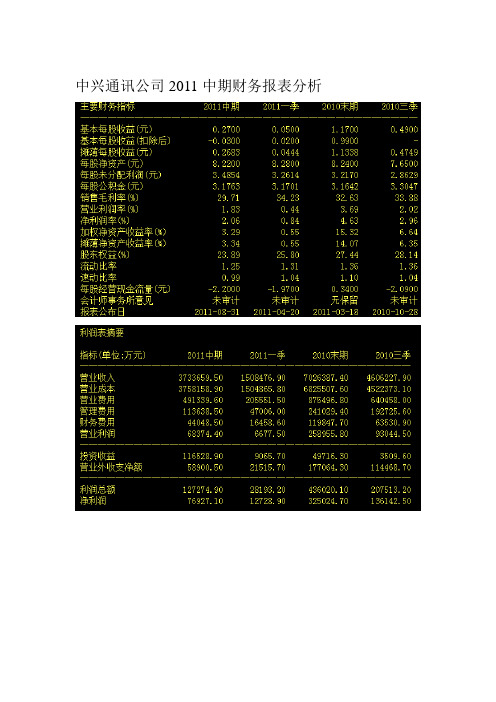

中兴通讯公司2011中期财务报表分析偿债能力分析1.流动比率:从表面看,2011年中期流动比率为1.25,也就是说每有一元的流动资产,就有1.25元的流动资产多为安全保障,这个数字相比来说偏低,而且经过和前几段时间的比较甚至还有下降趋势,因此中兴短期偿债能力需要提高。

2.速动比率:2011年中期,中兴的速动比率为0.99,在正常范围内,说明企业应收账款很容易收回,偿债能力很好,比较流动比率,两者判断方式不一,但考虑到速动比率撇开了存活问题,综合看来,中兴偿债能力中等。

3.现金流量比率:现金流量比率=经营活动产生的现金流量净额/流动负债=94191/4821414=1.95% 实在很低,11年偿还能力不高4.资产负债率:资产负债率=负债总额/资产总额=7170709/9648482=0.745.权益乘数:权益乘数=资产总额/股东权益总额=9648482/2305185=4.18 说明股东投入的资本在资产中所占比重小,财务杠杆大综上,中兴通讯的偿债能力很优秀,值得信赖。

营运能力分析1.存货周转率:存货周转率=销售成本/存货平均余额=3758158/((1514622+1405258)/2)=2.57次存货周转率说明2011年初到中期内企业存货周转的次数,反应变现速度。

可见销售能力处中等。

2.流动资产周转率=销售收入/流动资产平均余额=3733659/((7713569+7065317)/2)=0.5 资金效率太低综上,中兴通讯的营运能力偏差,需要提高管理层的素质和能力,以及提高资产的利用率。

..盈利能力分析1.资产利润率:资产利润率=利润总额/资产平均总额=68347/((9648482+9000173)/2)=0.73%和以往相比没什么提高..2.总资产周转率:总资产周转率=销售收入/资产平均总额=0.22 应该采取措施提高销售收入或处置资产3.销售净利率:销售净利率=净利润/营业收入净额=2.06% 该比率相对来说偏低,需要扩大销售获取利益。

andAnalysis(财务报表分析,台湾中兴大学).pptx

• M• aNnoagtecriualrdreisncrtelytioanciscenpecteesdsairny Uin.S.

accounting

• M• aSjoEr Clobubnyidset ornpGreAsAsPure to accept IAS

Environmental Factors

Other SEC Filings

Earnings Announcements

• Key summary measures (pre-audit) • Often one to six week lag • Informative to market • Lacks supporting financial details

Environmental Factors

Managers of Companies

• M• aSinertebspyonInstibeirlintyaftoirofnaiar l&Aacccuorautne trienpgorts • ApSpltiaesndacacrodusntiBngoatordreflect business

Analysts

SEC

Corporate Governance Litigation Auditors

Enforcement and Monitoring Mechanisms

Other Users

Investors and

Creditors

Users

Form 10-K

(Annual Report)

Level II

FASB Technical Bulletins

AICPA Industry Audit & Accounting Guidelines

chap009Profitability Analysis(财务报表分析,台湾中兴大学)

Analyzing Profitability

Measuring Income

Income is defined as revenues less expenses over a reporting period

This definition does not yield a unique amount becauseபைடு நூலகம்of: Estimation Issues Accounting Methods

Analyzing Profitability

Measuring Income--Incentives for Disclosure

Reality: Each of us possess opinions--we see the world from different perspectives Managers bring strong views to the table Managers feel pressures of competition and society Directors expect results Shareholders concentrate on the bottom line Creditors want safeguards Financial analysts dislike surprises Accounting preparers and auditors demand acceptable practices

These estimates require:

• Use of judgment and probabilities • Allocations of revenues and expenses across periods • Prediction of the future usefulness of many assets • Forecasts of future obligations

chap011CreditAnalysis(财务报表分析,台湾中兴大学)

3. Managerial policies are directed primarily at efficient and profitable asset utilization and secondly at liquidity

prepaid expenses

Liquidity and Working Capital

Current Ratio

Three important qualifications 1. Liquidity depends to a large extent on prospective cash

flows

Liquidity and Working Capital

Working Capital

Working capital more relevant when related to other key variables such as Sales Total assets Working capital is of limited value as an absolute amount

Liquidity and Working Capital

Current Assets

Classification as current asset depends on:

1. Manament’s intent 2. Industry practice

Balance Sheet

Analysis must assess this classification

chap007CashFlowAnalysis(财务报表分析,台湾中兴大学)

Statement of Cash Flows

Cash Flow Relations

Illustration: Consider two consecutive years’ balance sheets divided into (1) cash, and (2) all other balance sheet accounts:

Cash Flow Analysis

McGraw-Hill/Irwin

7

CHAPTER

© 2004 The McGraw-Hill Companies, Inc., All Rights Reserved.

Statement of Cash Flows

Relevance of Cash Flows

Liquidity is the nearness to cash of assets and liabilities. Solvency is the ability to pay liabilities when they mature. Financial flexibility is the ability to react to opportunities and adversities.

Cash repays loans, replaces equipment, expands facilities, and pays dividends.

Analyzing cash inflows and outflows helps assess liquidity, solvency, and financial flexibility.

Accounts

Cash and cash equivalents

Analysis(财务报表分析,台湾中兴大学)-PPT文档资料

Analyzing Revenues

Revenue Sources

• Evaluation, projection, and valuation of income is aided by segment analysis

• Segments share characteristics of variability, growth, and risk • Income forecasting benefits from forecasts by segments • Must separate and interpret the impact of individual segments

Analyzing Profitability

Measuring Income--Estimation Issues

Management discretion is part of income measurement

Estimates of skilled and experienced professionals Some consensus (less variability)

❖ Estimation Issues ❖ Accounting Methods ❖ Incentives for Disclosure ❖ Diversity across Users

Analyzing Profitability

Measuring Income--Estimation Issues

chap005 Analyzing Investing Activities Special Topics(财务报表分析-台湾中兴大学)

generally through ownership of equity securities, the activities of another separate legal entity known as a subsidiary

Parent-subsidiary relation —when one corporation

(to record proportionate share of investee company earnings)

Cash 5,000 Investment

5,000

(to record receipt of dividends)

Investment balance = % Share of Investee Equity

Business Combinations

Companies Reporting Business Combinations

Combinations 60%

No Combinations 40%

Source:Accounting Trends & Techniques

Business Combinations

2,080,000 End.

Equity Investments

Important Points in Equity Method Accounting

The investment account represents the proportionate share of the stockholders’ equity of the investee company. Substantial assets and liabilities may, therefore, not be recorded on balance sheet unless the investee is consolidated. This can have important implications for the analysis of the investor company.

onInvestedCapital(财务报表分析,台湾中兴大学)

• Focus is on individual shareholder, not the company

• Uses the purchase price of securities as invested capital

construction, surplus plant, surplus inventories, surplus cash, and deferred charges from invested capital

Adjustment is not valid as it fails to: ➢ recognize that management has discretion

Return on Invested Capital

McGraw-Hill/Irwin

8

CHAPTER

© 2004 The McGraw-Hill Companies, Inc., All Rights Reserved.

Return on Invested Capital

Importance of Joint Analysis

• Joint analysis is where one measure is assessed relative to another

• Return on invested capital (ROI) is an important joint analysis

Return on Invested Capital

Income Invested capital

Components of ROI

Invested Capital Defined

chap011CreditAnalysis(财务报表分析,台湾中兴大学)

Liquidity and Working Capital

Current Assets

Current assets are cash and other assets reasonably expected to be (1) realized in cash, or (2) sold or consumed, during the longer of oneyear or the company’s operating cycle

Liquidity and Working Capital

Working Capital

Working capital is defined as the excess of current assets over current liabilities Widely used measure of short-term liquidity Deficient when current liabilities exceed current assets In surplus when current assets exceed current liabilities A margin of safety for creditors A liquid reserve to meet contingencies and uncertainties A constraint for technical default in many debt agreements

Credit Analysis

McGraw-Hill/Irwin

11

CHAPTER

© 2004 The McGraw-Hill Companies, Inc., All Rights Reserved.

chap007CashFlowAnalysis财务报表分析-台湾中兴大学

? In period of collection no income is recorded.

Net Income

0

Depreciation and amortization expense

0

Gains (losses) on sale of assets

0

Change in accounts receivable

Statement of Cash Flows

Income vs. Cash Flows Example

Consider a $100 sale on account (1) In period of sale, net income is increased by $100 but no

cash has been generated.

Indirect Method

Net Cash Flows from Operations

Net Income + Depreciation +/- Gains (losses) on sales of assets +/- Cash generated (used) by current assets & liabilities

Operating activities are the earning-related activities of a company.

Investing activities are means of acquiring and disposing of noncash assets.

Financing activities are means of contributing, withdrawing, and servicing funds to support business activities.

AnalysisandValuation(财务报表分析,台湾中兴大学

195.4

220.4

212.9

219.1

203.5

181.4

Repairs and maintenance (see Note 1 below)

173.9

180.6

173.9

155.6

148.8

144.0

Administrative expen

232.6

213.9

Earnings Persistence

Recasting and Adjusting

General Recasting Procedures

Income statements of several years (typically at least five) are recast

Recast earnings components to yield meaningful classifications and a relevant format for analysis

$ 672.2 $ 510.7 $ 444.4 $ 421.9 $ 387.7 $ 384.2

Equity in earnings of affiliates

2.4

13.5

10.4

6.3

15.1

4.3

Minority interests

(7.2)

(5.7)

(5.3)

(6.3)

(4.7)

(3.9)

Income before taxes

195.9

Research and development expenses

56.3

53.7

47.7

46.9

44.8

42.2

chap007CashFlowAnalysis(财务报表分析,台湾中兴大学)

Statement of Cash Flows

Cash Flow Relations

Interrelations between cash and noncash balance sheet accounts can be generalized:

❖ Net changes in cash are explained by net changes in noncash balance sheet accounts.

Cash repays loans, replaces equipment, expands facilities, and pays dividends.

Analyzing cash inflows and outflows helps assess liquidity, solvency, and financial flexibility.

Accounts

Cash and cash equivalents

Noncash accounts: Noncash current assets Noncurrent assets Current liabilities Long-term liabilities Equity accounts Net noncash balance

Statement of Cash Flows

Relevance of Cash Flows

Cash is the beginning and the end of a company’s operating cycle.

Net cash flow is the end measure of profitability.

Liquidity is the nearness to cash of assets and liabilities. Solvency is the ability to pay liabilities when they mature. Financial flexibility is the ability to react to opportunities and adversities.

andAnalysis(财务报表分析,台湾中兴大学)

Environmental Factors

Economic, Industry & Company News

Impacts current & future financial condition and performance

Voluntary Disclosure

Many factors encourage voluntary disclosure by managers

Level IV (Least authoritative)

FASB Implementation

Guides

AICPA Interpretations

Recognized and Widely Used Industry

Practices

Environmental Factors

Securities and Exchange

Information Intermediaries

Industry devoted to collecting, processing, interpreting & disseminating company information

Includes analysts, advisers, debt raters, buy- and sell-side analysts, and forecasters

- oversee accounting process

-oNveortseceuinrrteernnatllycoanctrcoel pted in U.S. I-notSevreEnraCsleAauuinnddtietoernrrapl/erxetsersnualreautdoit accept

chap002 Financial Reporting and Analysis(财务报表分析-台湾中兴大学)

Environmental Factors

International Accounting Standards (IAS)

Set by International Accounting Standards Board Not currently accepted in U.S. SEC under pressure to accept IAS

Politicians

Others

Accountants

Provide input to

Financial Accounting Standards Board

Help set

Generally Accepted Accounting Principles

Environmental Factors

IAS

Environmental Factors

Corporate Governance

Board of directors oversightAccounting Set by International Audit committeeBoard Standards of the board - oversee accounting process Not currently accepted in U.S. - oversee internal control - oversea internal/external audit SEC Auditor pressure to accept under Internal

Environmental Factors

Economic, Industry & Company News

Impacts current & future financial condition and performance

Analysis(财务报表分析,台湾中兴大学)

Analyzing Revenues

Revenue Sources

Full disclosure by segments is rare because of: • Difficulties in separating segments • Management’s reluctance to release information

• Different segments usually experience varying rates of profitability, risk, and growth

• Asset composition and financing requirements of segments often vary

Purpose: To apply analysis tools to aid achieve the analysis objectives—such as income forecasting and estimating earning power

Analyzing Revenues

Revenue Sources

Graphical analysis is a useful tool to interpret the sources of revenues

Analyzing Revenues

Revenue Sources

Diversified Companies present special challenges

Shareholders concentrate on the bottom line Creditors want safeguards Financial analysts dislike surprises Accounting preparers and auditors demand acceptable

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

• Excludes current liability financing

Components of ROI

Equity Capital

• Perspective is that of equity holders

Return on Invested Capital

Application of ROI

ROI is applicable to:

(1) evaluating managerial effective-

ness

(2) assessing profitability

(3) earnings forecasting

• ROI relates key summary measures: profits with financing

• ROI conveys return on invested capital from different financing perspectives

Return on Invested Cቤተ መጻሕፍቲ ባይዱpital

• Assumes certain assets not recognized in financial statements

• Uses the market value of invested capital (debt and equity)

Components of ROI

Investor Invested Capital

age

Components of ROI

Long-Term Debt Plus Equity Capital

• Perspective is that of the two main suppliers of long-term financing — long-term creditors and equity shareholders

Components of ROI

Computing Invested Capital

• Usually computed using average capital available for the period

• Typically add beginning and ending invested capital amounts and divide by 2

Components of ROI

Total Assets

• Perspective is that of its total financing base

• Called return on assets (ROA)

ROA: measures operating efficiency/ performance reflects return from all financing does not distinguish return by

Assists in Forecasting Earnings

• ROI links past, current, and forecasted earnings with

invested capital

• ROI adds discipline

to forecasting

• ROI helps identify

• Excludes intangible assets from invested capital

Adjustment is not valid as: Lack of information or increased

uncertainty does not justify exclusion

Components of ROI

Total Assets

Unproductive Asset Adjustment • Assumes management not responsible for

earning a return on capital not in operations • Excludes idle plant, facilities under

(4) planning and

control

Return on Invested Capital

Evaluating Managerial Effectiveness

• Management is responsible for all company activities

• ROI is a measure of managerial effectiveness in business activities

depreciation expense Acquisitions of new depreciable assets offset a declining

capital base It fails to recognize increased maintenance costs as assets

• More accurate computation is to average interim amounts — quarterly or monthly

Components of ROI

Return on Invested Capital

McGraw-Hill/Irwin

8

CHAPTER

© 2004 The McGraw-Hill Companies, Inc., All Rights Reserved.

Return on Invested Capital

Importance of Joint Analysis

Components of ROI

Total Assets

Accumulated Depreciation Adjustment • Assumes plant assets maintained in prime condition • Assumes inappropriate to assess return relative to net assets • Concern with a decreasing invested capital base • Includes an addback for accumulated depreciation on

Components of ROI

Alternative Measures of Invested Capital

Five Common Measures:

• Total Assets • Long-Term Debt Plus Equity • Equity • Market Value of Invested Capital • Investor Invested Capital

ROI Relation

•ROI relates income, or other performance measure, to a company’s level and source of financing

•ROI allows comparisons with alternative investment opportunities

• Perspective is that of the individual investor

• Focus is on individual shareholder, not the company

• Uses the purchase price of securities as invested capital

Income Investedcapital

Components of ROI

Invested Capital Defined

• No universal measure of invested capital exists

• Different measures of invested capital reflect different financiers’ perspectives

over all investment assess overall management effectiveness

Components of ROI

Total Assets

Intangible Asset Adjustment

• Assumes skepticism of intangible asset values

• Joint analysis is where one measure is assessed relative to another

• Return on invested capital (ROI) is an important joint analysis

Return on Invested Capital

•Riskier investments are expected to yield a higher ROI

•ROI impacts a company’s ability to succeed, attract financing, repay creditors,and reward owners

construction, surplus plant, surplus inventories, surplus cash, and deferred charges from invested capital

Adjustment is not valid as it fails to: recognize that management has discretion

financing sources