账目附注 Notes to the Financial Statements

The Balance Sheet and Notes to the Financial Statements

3-11

This term includes legal commitments as well as moral, social, and implied obligations.

3-12

Most liabilities involve an obligation to transfer assets in the future. However, an obligation to provide a service is also a liability.

3-18

3-19

Current Assets

The normal operating cycle involves the use of cash to purchase inventories, the sale of inventories resulting in receivables, and ultimately the cash collection of those receivables.

3-22

Noncurrent Assets

• Investments • Property, plant, and equipment • Intangible assets • Deferred income taxes

3-23

Investments

Investments held for such longterm purposes as regular income, appreciation, or ownership control are reported under the heading Investments.

Stice | Stice | Skousen

Notes to the Financial Statements财务报表附注

1.GeneralHyComm Wireless Limited (“the Company”) was incorporated in Bermuda on 30 July 1997 as an exempted company with limited liability under the Companies Act 1981 of Bermuda (as amended). The shares of the Company are listed on The Stock Exchange of Hong Kong Limited (the “Stock Exchange”).The Company is an investment holding company. The activities of its principal subsidiaries are set out in note 36.2.Basis of Preparation of Financial StatementsIn preparing the financial statements, the directors have given careful consideration to the future liquidity of the Group. The Group incurred a loss of approximately HK$80 million for the year ended 31 March 2004 and had net current liabilities of approximately HK$27 million at that date.The directors consider that the Group will be able to meet in full its financial obligations as they fall due for the foreseeable future because the Group is currently in the process of disposing certain properties and arranging additional banking facilities in order to provide additional working capital for the Group.Accordingly, the financial statements have been prepared on a going concern basis.1.362.80,000,00027,000,0003.Adoption of Revised Statement of StandardAccounting PracticeIn the current year, the Group has adopted the following revised Statement of Standard Accounting Practice (“SSAP”) issued by the Hong Kong Society of Accountants:SSAP 2.112 (Revised)Income TaxesIn accordance with the SSAP 2.112 (Revised), deferred tax liabilities are provided in full, using the liability method, on all temporary differences between the carrying amount of assets and liabilities in the balance sheet and their tax bases used in the computation of taxable profits, while deferred tax assets are recognized to the extent that it is probable that the future taxable profits will be available against which the deductible temporary differences and unused tax losses can be utilized.The adoption of the revised SSAP 2.112 represents a change in accounting policy, which has been applied retrospectively, and the comparative figures have been restated accordingly. In adjusting prior year figures, the opening accumulated losses as at 1 April 2003 have been increased by HK$588,000 (2002: HK$160,000) which represents the unprovided net deferred tax liabilities of the Group in prior years. In addition, this change in accounting policy has resulted in an increase of HK$560,000 (2003: HK$428,000) in the Group’s net loss for the year.3.:2.1122.1122.112588,000160,000560,000428,0004.Significant Accounting PoliciesThe financial statements have been prepared under the historical cost convention as modified for the revaluation of investment properties, leasehold land and buildings and investments in securities. The financial statements have been prepared in accordance with accounting principles generally accepted in Hong Kong. The significant accounting policies adopted by the Group are set out below:(a)Basis of consolidationThe consolidated financial statements of the Group includethe financial statements of the Company and its subsidiariesmade up to 31 March each year.A subsidiary is a company whose financial and operatingpolicies are under the Company’s control, directly orindirectly, so as to obtain benefits from its activities.The results of subsidiaries acquired or disposed of duringthe year are consolidated from the effective dates ofacquisition or up to their effective dates of disposal.All significant inter-company transactions and balanceshave been eliminated on consolidation.In the Company’s financial statements, investments insubsidiaries are carried at cost less any accumulatedimpairment losses. The results of the subsidiaries areincluded in the income statement to the extent of dividendsreceived and receivable.4.(a)4.Significant Accounting Policies (Continued)(b)AssociatesAn associate is a company, not being a subsidiary nor ajoint venture, in which an equity interest is held, or thelong-term and significant influence is exercised in itsmanagement.The consolidated income statement includes the Group’sshare of the current year’s results of the associates, and theconsolidated balance sheet includes the Group’s share ofthe net assets or liabilities of the associates and goodwill/negative goodwill (net of accumulated amortisation andaccumulated impairment losses) arising on acquisition.In the Company’s balance sheet, the investments inassociates are stated at cost less provision for impairmentlosses. The results of associates are accounted for by theCompany on the basis of dividends received andreceivable.(c)Revenue recognitionSales of goods are recognised when goods are deliveredand title has passed.Rental income, including rentals invoiced in advance fromproperties let under operating leases, is recognised on astraight line basis over the term of the relevant lease.Interest income is accrued on a time basis by reference tothe principal outstanding and at the interest rate applicable.Property management and other fees are recognised whenservices are rendered.Service fee income is recognised as revenue when the inter-operator short message services are rendered.4.(b)(c)4.Significant Accounting Policies (Continued)(d)Investment propertiesInvestment properties are completed properties which areheld for their investment potential, any rental income beingnegotiated at arm’s length.Investment properties are stated at their open market valuebased on independent professional valuations at thebalance sheet date. Any surplus or deficit arising onrevaluation of investment properties is credited or chargedto the investment property revaluation reserve unless thebalance of the reserve is insufficient to cover a deficit, inwhich case the excess of the deficit over the balance ofthe investment property revaluation reserve is charged tothe income statement. Where a deficit has previously beencharged to the income statement and a revaluation surplussubsequently arises, this surplus is credited to the incomestatement to the extent of the deficit previously charged.On subsequent disposal of an investment property, thebalance on the investment property revaluation reserveattributable to that property is included in the determinationof the profit and loss on disposal.No depreciation and amortisation is provided in respectof investment properties which are held under leases withunexpired terms, including the renewable period, of morethan twenty years.4.(d)4.Significant Accounting Policies (Continued)(e)Property, plant and equipmentProperty, plant and equipment, other than leasehold landand buildings, are stated at cost less depreciation,amortisation and accumulated impairment losses.The gain or loss arising from the disposal or retirement ofan asset is determined as the difference between the saleproceeds and the carrying amount of the asset and isrecognised in the income statement.Leasehold land and buildings are stated in the balancesheet at their revalued amount, being the fair value on thebasis of their existing use at the date of revaluation lessany subsequent accumulated depreciation andamortisation. Revaluations are performed with sufficientregularity such that the carrying amount does not differmaterially from that which would be determined using fairvalues at the balance sheet date.Any surplus arising on revaluation of leasehold land andbuildings is credited to the revaluation reserve, except tothe extent that it reverses a revaluation deficit of the sameasset previously recognised as an expense, in which casethis surplus is credited to the income statement to the extentof the deficit previously charged. A decrease in net carryingamount arising on revaluation of an asset is charged to theincome statement to the extent that it exceeds the balance,if any, on the revaluation reserve relating to a previousrevaluation of that asset. On the subsequent sale orretirement of a revalued asset, the attributable revaluationsurplus is transferred to retained profits.4.(e)4.Significant Accounting Policies (Continued)(e)Property, plant and equipment (Continued)Depreciation and amortisation is provided to write off thecost or valuation of property, plant and equipment overtheir estimated useful lives, using the straight line method,at the following rates per annum:Leasehold land Over the lease termsBuildings2%Furniture, fixtures and equipment20-30%Motor vehicles20-30%(f)Properties under developmentLand and buildings in the course of development for sale,rental or administrative purposes or for purposes not yetdetermined are carried at cost less any provision forimpairment loss considered necessary by the directors. Costincludes land cost, development cost, borrowing costscapitalized and other direct costs attributable to suchproperties. Depreciation and amortisation of these assets,on the same basis as other property assets, commenceswhen the assets are ready for their intended use.Properties under development which are due forcompletion more than one year from the balance sheetdate are shown as non-current assets.Properties under development which are due forcompletion within one year from the balance sheet dateand are intended to be held for long term for theirinvestment potential are shown as non-current assets.4.(e)2%20-30%20-30%(f)4.Significant Accounting Policies (Continued)(f)Properties under development (Continued)Properties under development which are due forcompletion within one year from the balance sheet dateand are intended to be held for sale will be treated asproperties under development for sale and are shown ascurrent assets.(g)Cash and cash equivalentsCash and cash equivalents comprise cash at bank and onhand, demand deposits with banks and other financialinstitutions, and short-term, highly liquid investments thatare readily convertible into known amounts of cash andwhich are subject to an insignificant risk of changes invalue, having been within three months of maturity atacquisition. Bank overdrafts that are repayable on demandand form an integral part of the group’s cash managementare also included as a component of cash and cashequivalents for the purpose of the cash flow statement.(h)Capitalisation of borrowing costsBorrowing costs directly attributable to the acquisition,construction or production of qualifying assets, which areassets that necessarily take a substantial period of time toget ready for their intended use or sale, are capitalized aspart of the costs of those assets. Capitalisation of suchborrowing costs ceases when the assets are substantiallyready for their intended use or sale. Investment incomeearned on the temporary investment of specific borrowingspending their expenditure on qualifying assets is deductedfrom the borrowing costs capitalized.All other borrowing costs are recognised as an expense inthe period in which they are incurred.4.(f)(g)(h)4.Significant Accounting Policies (Continued)(i)Investments in securitiesInvestments in securities are recognised on a trade-datebasis and are initially measured at cost.Investments other than held-to-maturity debt securities areclassified as investment securities and other investments.Investment securities, which are securities held for anidentified long-term strategic purpose, are measured atsubsequent reporting dates at cost, as reduced by anyimpairment loss that is other than temporary.Other investments are measured at fair value, withunrealised gains and losses included in net profit or lossfor the period.(j)GoodwillGoodwill arising on consolidation represents the excessof the cost of acquisition over the Group’s interest in thefair value of the identifiable assets and liabilities of asubsidiary, associate or jointly controlled entity at the dateof acquisition.Goodwill arising on acquisitions prior to 1 April 2001continues to be held in reserves, and will be charged tothe income statement at the time of disposal of the relevantsubsidiary, associate or jointly controlled entity, or at suchtime as the goodwill is determined to be impaired.4.(i)(j)4.Significant Accounting Policies (Continued)(j)Goodwill (Continued)Goodwill arising on acquisitions after 1 April 2001 iscapitalised and amortised on a straight line basis over itsuseful economic life. Goodwill arising on the acquisitionof an associate or a jointly controlled entity is includedwithin the carrying amount of the associate or jointlycontrolled entity. Goodwill arising on the acquisition ofsubsidiaries is presented separately in the balance sheet.On disposal of a subsidiary, an associate or jointlycontrolled entity, the attributable amount of unamortisedgoodwill/goodwill previously eliminated against reservesis included in the determination of the profit or loss ondisposal.(k)Negative goodwillNegative goodwill represents the excess of the Group’sinterest in the fair value of the identifiable assets andliabilities of a subsidiary, associate or jointly controlledentity at the date of acquisition over the cost of acquisition.Negative goodwill arising on acquisitions prior to 1 April2001 continues to be held in reserves and will be creditedto income at the time of disposal of the relevant subsidiary,associate or jointly controlled entity.Negative goodwill arising on acquisitions after 1 April 2001is presented as a deduction from assets and will be releasedto income based on an analysis of the circumstances fromwhich the balance resulted.4.(j)(k)4.Significant Accounting Policies (Continued)(k)Negative goodwill (Continued)To the extent that the negative goodwill is attributable tolosses or expenses anticipated at the date of acquisition, itis released to income in the period in which those lossesor expenses arise. The remaining negative goodwill isrecognised as income on a straight line basis over theremaining average useful life of the identifiable acquireddepreciable assets. To the extent that such negativegoodwill exceeds the aggregate fair value of the acquiredidentifiable non-monetary assets, it is recognised in incomeimmediately.Negative goodwill arising on acquisitions of an associateor a jointly controlled entity is deducted from the carryingvalue of that associate or jointly controlled entity. Negativegoodwill arising on the acquisition of subsidiaries ispresented separately in the balance sheet as a deductionfrom assets.(l)InventoriesInventories represent trading merchandise and are statedat the lower of cost and net realisable value. Cost iscalculated using the first-in, first-out method. Net realisablevalue represents the estimated selling price in the ordinarycourse of business less the estimated costs necessary tomake the sale.4.(k)(l)4.Significant Accounting Policies (Continued)(m)ImpairmentAt each balance sheet date, the Group reviews the carryingamounts of its tangible and intangible assets to determinewhether there is any indication that these assets havesuffered an impairment loss. If the recoverable amount ofan asset is estimated to be less than its carrying amount,the carrying amount of the asset is reduced to itsrecoverable amount. Impairment losses are recognised asan expense immediately, unless the relevant asset is carriedat a revalued amount under another SSAP, in which casethe impairment loss is treated as revaluation decrease underthat SSAP.Where an impairment loss subsequently reverses, thecarrying amount of the asset is increased to the revisedestimate of its recoverable amount, but so that the increasedcarrying amount does not exceed the carrying amount thatwould have been determined had no impairment loss beenrecognised for the asset in prior years. A reversal of animpairment loss is recognised as income immediately,unless the relevant asset is carried at a revalued amountunder another SSAP, in which case the reversal of theimpairment loss is treated as a revaluation increase.(n)TaxationThe charge for taxation is based on the results for the yearafter adjusting for items which are non-assessable ordisallowed. Certain items of income and expense arerecognised for tax purposes in a different accounting periodfrom that in which they are recognised in the financialstatements. The tax effect of the resulting timing differences,computed under the liability method, is recognised asdeferred taxation in the financial statements to the extentthat it is probable that a liability or asset will crystallise inthe foreseeable future.4.(m)(n)4.Significant Accounting Policies (Continued)(o)Foreign currenciesTransactions in currencies other than Hong Kong dollarsare translated into Hong Kong dollars at the rates rulingon the dates of the transactions. Monetary assets andliabilities denominated in currencies other than Hong Kongdollars are translated into Hong Kong dollars at the ratesruling on the balance sheet date. Gains and losses arisingon exchange are dealt with in the income statement.(p)Operating leasesLeases where substantially all the rewards and risks ofownership of assets remain with the lessor are accountedfor as operating leases. Where the Group is the lessor, assetsleased by the Group under operating leases are includedin non-current assets and rental receivable under theoperating leases are credited to the income statement onthe straight line basis over the lease terms. Where the Groupis the lessee, rentals payable under the operating leasesare charged to the income statement on the straight linebasis over the lease terms.4.(o)(p)17.Investments in Securities (Continued)The trading of the shares in Codebank Limited (“Codebank”), a company with its shares listed on the Growth Enterprise Market (“GEM”) of the Stock Exchange on 21 December 2001, have been suspended since 14 May 2002. On 28 May 2002, the previous directors of Codebank informed its shareholders that certain recent events took place in Codebank were being investigated by them and since then trading of the shares remains suspended. Accordingly, the directors of the Company determined that the investments in Codebank were fully impaired as at 31 March 2002.The amount stated in the investments in securities represents the carrying value of the Group’s investment in Inno-Tech Holdings Limited (“Inno-Tech”). The shares of Inno-Tech was listed on GEM on 12 August 2002 and it is the Group’s plan to hold this investment on a long term basis.17.24.Share OptionsThe Company’s share option scheme (the “old scheme”) was adopted on 15 September 1997 for the primary purpose of providing incentives to the employees of the Group. Pursuant to a resolution passed at a special general meeting of the shareholders held on 15 July 2002, the Company terminated the old scheme and adopted the new share option scheme.There were no outstanding options granted under the old and the new schemes at the beginning and at the end of the year. In addition, there were no options granted to, or exercised by, any eligible employees during the year.24.25.Share Premium and Reserves (Continued)Under the Companies Act 1981 of Bermuda (as amended), contributed surplus is also available for distribution to shareholders. However, a company cannot declare or pay a dividend, or make a distribution out of contributed surplus, if:(a)the company is, or would after the payment be, unable topay its liabilities as they become due; or(b)the realisable value of the company’s assets would therebybe less than the aggregate of its liabilities and its issuedshare capital and share premium accounts.In the opinion of the directors, as at 31 March 2003 and 31 March 2004, the Company did not have any reserve available for distribution to shareholders.25.(a)(b)30.Retirement Benefit SchemeWith effect from 1 December 2000, the Group joined a Mandatory Provident Fund Scheme (“MPF Scheme”) for all employees in Hong Kong. The MPF Scheme is registered with the Mandatory Provident Fund Scheme Authority under the Mandatory Provident Fund Schemes Ordinance. The assets of the MPF Scheme are held separately from those of the Group in funds under the control of independent trustees.Under the rules of the MPF Scheme, the employer and its employees are each required to make contributions to the scheme at rates specified in the rules. The only obligation of the Group with respect of MPF scheme is to make the required contributions under the scheme. No forfeited contribution is available to reduce the contribution payable in the future years.The retirement benefit scheme contribution arising from the MPF Scheme charged to the consolidated income statement represent contributions payable to the funds by the Group at rates specified in the rules of the MPF Scheme.During the year, the retirement benefit schemes contribution, net of forfeited contributions utilised of approximately HK$Nil (2003: HK$Nil), amounted to approximately HK$586,450 (2003: HK$124,450).At the balance sheet date, the Group had no significant 30.586,450124,450At 31 March 2004, the Company had outstanding unlimited guarantees and a corporate guarantee given in favour of banks amounting to approximately HK$120,000, 000 (2003: HK$126,000,000) to secure general banking facilities granted to a subsidiary. The total amount of facilities utilised by the subsidiary as at 31 March 2004 amounted to approximately HK$113,881,000 (2003: HK$107,750,000).33.Pledge of AssetsTHE GROUP(a)At 31 March 2004, the Group’s borrowings were secured by the following:(i)first legal charges over the investment properties ofHK$126,500,000 (2003: HK$111,700,000);(ii)the interest in share capital of a subsidiary;(iii)assignment of rental income generated from certain investment properties;(iv)floating charges on all the existing and future assets undertakings of a subsidiary;(v)assignments of the right, title, interest and benefits in and under all the existing and future building contracts in respect of properties under development;(vi)the benefit under all insurance policies of properties under development;(vii)assignment of sales proceeds from sales of investment properties; and(viii)subordination of shareholders’ loans of a subsidiary 33.(a)(i)126,500,000111,700,000(ii)(iii)(iv)(v)(vi)(vii)(viii)(b)11,000,00014,397,0008,000,00010,000,000。

2008年度英文附注新准则09.4.3

PPD Pharmaceutical Development (Beijing) Co., Ltd.Notes to the Financial StatementsFor the year ended December 31, 2008(Expressed in Renminbi Yuan, except as indicated)1. General Information1.1 Company BackgroundPPD Pharmaceutical Development (Beijing) Co., Ltd. (hereinafter referred to as “the Company”) was established in Beijing city on 23 April, 2007 by PPD Development (S) Pte Ltd. as a wholly foreign-owned enterprise after approved by Beijing authority (No. Shang Wai Zi Jing Du Zi [2007]0001). The company obtained business license (No.110000450007377) issued by the Administration Bureau for Industry and Commerce in Beijing, and the registered capital is is USD$ 175,000. The legal representative is Mr. K C Lau. The place of registration is Beijing.The parent company is PPD Development (S) Pte Ltd.1.2 Operating IndustryThe Company is in the industry of consulting.1.3 Scope of BusinessThe Company is mainly engaged in consulting in the pharmaceutical industry. (Excluding diagnosis and treat activities)1.4 Major Service RenderedThe Company may provide the services of managing clinical research programs as requested by the parent company.2. Basis of PresentationThe Company adopts the Accounting Standards for Business Enterprises 2006 issued by the Ministry of Finance for annual periods beginning on or after January 1, 2008. The financial statements for the year ended December 31, 2007 were formerly prepared in conformity with the Accounting Regulations for Business Enterprises and Accounting Standards for Business Enterprises and relative supplementary rules. According to the requirements of two documentations issued by China Securities Regulatory Commission, which are “Notice of Disclosure of Relevant financial information under the New CAS” (Zheng Jian Fa [2006] No.136) and “No. 7 Guideline on Contentsand Format for Information Disclosure of Companies that Make Public Offering of Securities ----Compilation and Disclosure of Comparative Financial Accounting Information during the Transitional Period of Old and New Accounting Standards” (Kuai Ji Zi [2007] No.10), the Company determined the opening balances as at January 1, 2008 and critically analyzed the key impacts on the profit statement of the comparative period and the balance sheet as of the beginning of comparative period based on the understanding of “Accounting Standards for Enterprises No.38 – Initial Implementation of Accounting Standards for Enterprises: article 5 – article 19”, therefore in accordance with the principle of retrospective application, the financial statements for the year 2007 were prepared on the basis of the adjusted profit statement and balance sheet of comparative period .Based on the estimation of the Company’s capability of sustainable operation, the management believes that there are no events or circumstances may cause substantive doubt about the Company’s sustainable operation, and the financial statements are prepared on a basis of going concern assumption.3. Statement of ComplianceThe financial statements are in conformity with the requirements of Accounting Standards for Business Enterprises and present fairly, in all material respects, the financial position of the Company as of December 31, 2008, and the results of its operations and its cash flows for the year then ended.4. Summary of Significant Accounting Policies, Accounting Estimatesand Principles of Consolidation1) Fiscal YearThe fiscal year of the Company is coincided with the calendar year, i.e. from January 1 to December 31.2) Functional CurrencyThe financial statements of the Company are stated in Renminbi (“RMB”), which is also the Company’s functional currency.3) Accounting measurement bases and items in financialstatements with changes in measurement bases in financialreporting periodThe Company generally adopts historical cost as the measurement basis for accounting elements. If the accounting elements are measured at replacement cost, net realizable value, present value or fair value, the Company shall ensure such amounts can be obtained and reliably measured.(1) Accounting measurement bases adopted in the current financial reporting periodUnder the historical cost basis, assets are recorded at the amount of cash or cash equivalents paid or the fair value of the consideration given to acquire them at the time of their acquisition. Liabilities are recorded at the amount of proceeds or assets received in exchange for the present obligation, or the amount payable under contract for assuming the present obligation, or at the amount of cash or cash equivalents expected to be paid to satisfy the liability in the normal course of business.(2) Items in financial statements with changes in measurement bases in financial reporting periodAccounting measurement bases did not change in financial reporting period.4) Cash EquivalentsIn preparing the cash flow statement, cash equivalents refers to short-term (usually with maturity of three months or less) and highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of change in value. Equity investments are not considered to be cash equivalents.5) Accounting Treatment for Foreign Currency TransactionsAt the time of initial recognition of a foreign currency transaction, the amount in the foreign currency is translated into the amount in RMB at the spot exchange rate of the transaction date.At the balance sheet date, the foreign currency monetary items are translated at the spot exchange rate at the balance sheet date. Exchange differences arising on the settlement of monetary items or on translating monetary items at rates different from those at which they were translated on initial recognition during the period or in previous financial statements are recognized in profit or loss in the period in which they arise.Foreign currency non-monetary items that are measured at the historical cost are translated at the spot exchange rate on the transaction date, of which the amount of functional currency is not changed.Foreign currency non-monetary items that are measured at fair value are translated at the spot exchange rate at the date when fair value was determined. Exchange differences arising on the translation of non-monetary items carried at fair value are treated as changes in fair value, and suchexchange differences (including the effect of changes in foreign currency rates) are included in profit or loss for the period.6) Accounting Treatment for Financial Assets and FinancialLiabilities(1) Classification of Financial Assets and Financial LiabilitiesIn accordance with the intentions of financial assets acquired and financial liabilities assumed, designations based on documented risk management or investment strategies of the Company, features of financial assets/liabilities, the management classified financial assets/liabilities as follows, the financial assets/liabilities at fair value through profit or loss, including transactional financial assets/liabilities and the financial assets/liabilities designated by the Company as at fair value through profit or loss; held-to-maturity investments, loans and receivables, available-for-sale financial assets and other financial liabilities. Discretionary reclassification is not permitted once the aforementioned classification was determined.(2) Measurement of Financial Assets and Financial Liabilities Accounts ReceivableAccounts receivable resulting from the sale/delivery of goods or rendering of services to third parties are to be initially recognized and recorded at the amounts stipulated in the contract or agreement signed between the Company and the buyer.At receipt of payment or disposal, the differences between payment received or proceeds from the disposal and carrying amount are reported in current earnings.(3) Impairment of Financial AssetsThe Company assesses the carrying amount of financial assets, other than financial assets at fair value through profit or loss, at each balance sheet date to determine whether there is any objective evidence that a financial asset is impaired as a result of one or more events. Loss event refers to the event that occurred after the initial recognition of the asset and has an impact on the estimated future cash flows of the financial asset that can be reliably estimated. If any such evidence exists, the Company will make an impairment provision.Account ReceivableIf there is objective evidence that an impairment loss on receivables has been incurred, the amount of the loss is measured as the difference between theasset’s carrying amount and the present value of estimated future cash flows. At each balance sheet date, the Company assesses whether objective evidence of impairment exists individually for receivables that are individually significant. If any such evidence exists, the Company will recognize the impairment loss and make a bad debt provision based on the difference between the asset’s carrying amount and the present value of estimated future cash flows.For receivables that are not individually significant, if there is no evidence of impairment on an individual basis, a collective impairment review is undertaken whereby the assets are grouped together, on the basis of similar credit risk characteristics, in order to calculate a collective impairment loss. The bad debt provision will be made based on the collective impairment loss of each asset group, which is determined by the proportion of the collective carrying amount of the group to the carrying amount of total receivables as of the balance sheet date. Such proportion is a reflection of actual impairment loss of each group, which is the difference between the collective carrying amounts and the collective present values of estimated future cash flows.7) Measurement and Depreciation Method of Fixed Assets(1) Recognition of Fixed assetsFixed assets are tangible items that are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes and are expected to be used during more than one period. The cost of an item of fixed asset is recognized as an asset if, and only if:(a) it is probable that future economic benefits associated with the item willflow to the entity; and(b) the cost of the item can be measured reliably.(2)Classification of Fixed AssetsThe fixed assets are classified as follows: buildings, machineries, motor vehicles, office equipments and others.(3) Measurement of Fixed AssetsA fixed asset is initially measured at its cost.The Company recognizes in the carrying amount of a fixed asset the subsequent expenditures incurred if the probable future economic benefits associated with the fixed asset is greater than previous estimation. The new carrying amount of the fixed asset shall not exceed its recoverable amount.(4) The depreciation method of fixed assets: the Company begins to depreciate a fixed asset, one month after it is available for use, under straight-line method. The residual values (percentage), useful lives and annual rate of depreciation of different classifications of fixed assets are as follow:Classifications of Fixed Assets Useful Lives(in years)ResidualValue(%)Annual Rate ofDepreciation(%)Machineries50%20% Transportationequipment50%20% Medical equipment50%20% Medical reagent50%20%IT equipment30%33.33%After the recognition of an impairment loss, the depreciation charge for the fixed asset will be adjusted in future periods to allocate the asset’s revised carrying amount, less its residual value (if any), on a systematic basis over its remaining useful life;After a reversal of an impairment loss is recognized, the depreciation charge for the asset will be adjusted in future periods to allocate the asset’s revised carrying amount, less its residual value (if any), on a systematic basis over its remaining useful life.If the carrying amount of a fixed asset is reduced to zero after an impairment loss is recognized, no depreciation amount is recognized for it in future periods.8) Revenue RecognitionRendering of servicesRevenue associated with the transaction should be recognised when: (a) Cost plus revenue: The service has been rendered and revenue is recognised based on the amount of costs and expenses occurred and fixed cost plus ratio.(b) Pass through revenue: The service has been rendered and revenue is recognised equalling to the amount of prepaid costs and expenses.9) Accounting Treatment for Income TaxThe income tax is accounted for using balance sheet liability method.(1) Recognition of Deferred Tax Assets(a) A deferred tax asset will be recognized for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilized, unless the deferred tax asset arises from the initial recognition of an asset or liability in a transaction that:(i) is not a business combination; and(ii) at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).(b) The Company will recognize a deferred tax asset for all deductible temporary differences arising from investments in subsidiaries, branches and associates, and interests in joint ventures, to the extent that, and only to the extent that, it is probable that:(i) the temporary difference will reverse in the foreseeable future; and(ii) taxable profit will be available against which the temporary difference can be utilized.(c) A deferred tax asset will be recognized for the carry forward of unused tax losses and unused tax credits to the extent that it is probable that future taxable profit will be available against which the unused tax losses and unused tax credits can be utilized.(2) Recognition of Deferred Tax LiabilitiesA deferred tax liability will be recognized for all taxable temporary differences, except to the extent that the deferred tax liability arises from:(a) the initial recognition of goodwill; or(b) the initial recognition of an asset or liability in a transaction which:(i) is not a business combination; and(ii) at the time of the transaction, affects neither accounting profit nor taxableprofit (tax loss).(c) all taxable temporary differences associated with investments in subsidiaries, branches and associates, and interests in joint ventures, except to the extent that both of the following conditions are satisfied:(i) the parent, investor or venture is able to control the timing of the reversalof the temporary difference; and(ii) it is probable that the temporary difference will not reverse in the foreseeable future.(3) Measurement of Tax ExpenseCurrent and deferred tax will be recognized as income or an expense and included in profit or loss for the period, except to the extent that the tax arises from:(a) a business combination; or(b) a transaction or event which is recognized, in the same or a differentperiod, directly in equity.5. Changes in accounting policiesThe Company adopts the Accounting Standards for Business Enterprises 2006 issued by the Ministry of Finance for annual periods beginning on or after January 1, 2008. This accounting policy is applied retrospectively, and it does not affect the opening balance of retained earnings, and we have reclassified the opening balance of some other items in the balance sheet.6. TaxationTax items and tax rates applicable to the Company are as follows:Tax Items Levied on Tax Rates Business Tax Taxable gross turnover5% Enterprise Income Tax Taxable income20% The Company is classified into small-scale and little-profit company which adopts income tax rate of 20%.7. Notes to the Major Line Items of Financial Statements1) Cash and Cash EquivalentsItems2008.12.312007.12.31OriginalCurrencyExchangeRateFunctionalCurrencyOriginalCurrencyExchangeRateFunctionalCurrencyCash inhandRMB6,219.60 1.00006,219.60717.27 1.0000717.27 Sub-total6,219.60717.27BankRMB264,964.40 1.0000264,964.40246,729.49 1.0000246,729.49 USDollar36,179.48 6.8230246,852.7586,557.917.3041632,229.51 Sub-total511,817.15878,959.00 Total518,036.75879,676.272) Accounts Receivable(1) The composition of accounts receivableItems2008.12.31AmountProportionof total(%)Bad debtsprovisionaspercentageofaccountsreceivableProvisionfor baddebtAmountProportionof total(%)PPDDevelopment(S) Pte Ltd.750,275.35100.00%--263,094.00100.00% Total750,275.35-263,094.00(2) Aging analysisAge2008.12.312007.12.31 Amount PercentageProvisionfor baddebtsNet value Amount PercentageProvisionfor baddebtsUnder1 year750,275.35100.00%-750,275.35263,094.00100.00% Total750,275.35-750,275.35263,094.00According to the Company’s accounting policy, bad debt provision will be recognized by case-by-case analysis method. All of the ending balance is within one year and need not accrue any provision.(3) As of December 31, 2008, the outstanding amount due from shareholders with ownership of more than 5 %( inc.5%) of voting shares of the company is as follows:Name Amount Time%ReasonPPD Development (S) Pte Ltd.750,275.35Oct toDec, 2008100.00%TransactionTotal750,275.35100.00%3) Other accounts receivable(1) The Composition of Other Accounts ReceivableItems2008.12.312007.12.31 AmountProportionof total (%)Bad debtsprovisionaspercentageof accountreceivableProvisionfor baddebtAmountProportionof total (%)percentageOtheraccountsreceivable50,000.00100.00%--120,906.93100.00% Total50,000.00--120,906.93(2) Aging AnalysisAge2008.12.312007.12.31 Amount PercentageProvisionfor baddebtsNet value Amount PercentageProvisionfor baddebtsUnder1 year50,000.00100.00%-50,000.00120,906.93100.00% Total50,000.00100.00%-50,000.00120,906.93100.00%According to the Company’s accounting policy, bad debt provision will be recognized by case-by-case analysis method. All of the ending balance is within one year and need not accrue any provision.(3) As of December 31, 2008, there are no balances with shareholder with shareholdings above 5% (Including 5%).4) PrepaymentsItems2008.12.312007.12.31Under 1 year75,283.3854,243.38 Total75,283.3854,243.385) Fixed assets and accumulated depreciation(1) Classification of fixed assetsItem2007.12.31Increased incurrent periodDecreaseincurrentperiod2008.12.311.Total costof fixedassets292,718.0047,162.08-339,880.08 Machineries10,800.00--10,800.00 Medicalequipment227,500.00--227,500.00 Medicalreagent54,418.00--54,418.00IT-47,162.08-47,162.08 equipment2. Totalaccumulated9,397.2864,806.34-74,203.62 depreciationMachineries-2,160.00-2,160.00Medical7,583.3445,500.04-53,083.38 equipmentMedical1,813.9410,883.64-12,697.58 reagentIT-6,262.66-6,262.66 equipment3.Provisionforimpairmentloss of fixedassetsMachineries----Medical----equipmentMedical----reagentIT----equipment4.Totalcarryingamounts offixed assets283,320.72--265,676.46Machineries10,800.00--8,640.00 Medicalequipment219,916.66--174,416.62 Medicalreagent52,604.06--41,720.42 ITequipment---40,899.426) Deferred income tax assets(1) The recognized deferred income tax assets and deferred income tax liabilitiesItems2008.12.312007.12.31 Deferred income tax assetsOffice dilapidation accruals –deferred tax assets19,714.00-Total19,714.00-The basis for recognition of deferred income tax assets is that the office dilapidation accruals could not be deducted before income tax.7) Payroll AccrualItems2007.12.31Increased incurrentperiod Paid incurrentperiod2008.12.311. Wages,bonuses,allowances andsubsidies101,533.271,538,843.051,550,433.6689,942.662. Welfareexpenses foremployees;8,165.858,165.853. Socialinsurances300,913.86296,607.364,306.50Include:(1)Medicalinsurance92,246.6690,896.661,350.00(2)Endowmentinsurance(3)Pension186,905.64184,205.642,700.00(4)Unemploymentinsurance13,992.4213,789.92202.50 (5)Work injuryinsurance3,697.403,643.4054.00 (6)Maternityinsurance4,071.744,071.744. Housing fund101,314.0099,694.001,620.00 Total101,533.271,949,236.761,954,900.8795,869.168) Taxes PayableTax Items2008.12.312007.12.31 Business Tax37,481.2330,499.85 Enterprise incomeTax23,768.816,793.54 Total61,250.0437,293.399) Other payables(1) Aging AnalysisAge2008.12.312007.12.31 Under 1 year77,800.00122,294.34 Total77,800.00122,294.34 (2) As at 2008.12.31, there are no balances with shareholder with shareholdings above 5% (Including 5%) and with related parties.(3) Detail of other payablesName of company OutstandingamountAge ofoutstandingPercentage tototal otherpayablesThe natureor contentReanda CPAs59,600.00Within 1year76.61%Service feeOthers18,200.00Within 1year23.39%Total77,800.00100.00%10) Accrued liabilitiesItem2008.12.312007.12.31 Office dilapidationaccruals98,570.00-Total98,570.00-The office dilapidation accruals were booked as accrued liability per PRC GAAP.11) Paid-in CapitalItem Beginningbalance Increase DecreaseEndingbalancePPD Development(S) Pte Ltd.1,316,093.10--1,316,093.10Total1,316,093.10--1,316,093.1012) Surplus ReservesClassification2007.12.31Increased incurrentperiodDecreased incurrentperiod2008.12.31Statutory SurplusReserveOther surplusreservesReserve funds1,285.321,621.92-2,907.24 Enterprisedevelopment fundProfits reinvestedTotal1,285.321,621.92-2,907.2413) Retained EarningsItem Year2008Year2007 Retained earnings, beginning11,567.90-of periodAdd: Transferred from current16,219.2212,853.22 earningsOther transferred inLess: Withdraw for surplusreserveWithdraw for staff bonusand welfare fundWithdraw for reserve fund1,621.921,285.32 Withdraw for enterprisedevelopment fundProfits reinvestedLess: Preferred share dividendspayableWithdraw for othersurplus reservesOrdinary share dividendspayableDividends on ordinaryshares transferred into sharecapitalRetained earnings, end of26,165.2011,567.90 period14) Operating Revenue(1) Items listedItems Year 2008Year 2007Major operating revenue3,976,625.821,320,503.00 Total3,976,625.821,320,503.00(2) Listed by production or business categoriesProduct/CategoryYear 2008Year 2007 OperatingrevenueOperatingcostsOperatingprofitOperatingrevenueOperatingcostsCost plusrevenue3,546,714.381,306,362.042,240,352.341,128,260.00357,684.49Pass throughrevenue429,911.44429,911.44-192,243.00192,243.00 Total3,976,625.821,736,273.482,240,352.341,320,503.00549,927.4915) Tax and surchargeItems Tax Rate Year 2008Year 2007 Business tax5%198,831.2866,025.15 Total198,831.2866,025.1516) Finance chargesItem Year 2008Year 2007Interests expense--less:interest income5,779.253,364.75 Foreign exchange gainsor losses19,785.9126,479.78Bank charges4,335.73536.00Total18,342.3923,651.0317) Income tax expensesItem Year 2008Year 2007Current income taxexpenses4,054.816,793.54Deferred income tax19,714.00-assetsTotal23,768.816,793.5418) Other cash provided by operating activitiesItems Year2008Year2007Other receivables120,906.93-Interest income5,779.253,364.75 Total126,686.183,364.7519) Other cash used in operating activitiesItems Year2008Year2007General and392,372.84167,019.02 administrative expensesOther receivables50,000.00-Prepayments21,040.0054,243.38 Other payables59,751.61-Total523,164.45221,262.4020) Other cash used in investing activitiesItems Year2008Year2007 Purchase of fixed assets47,162.08292,718.00 Total47,162.08292,718.0021) Adjustments to reconcile net income to net cash provided by(used in) operating activitiesSupplement Information Year 2008Year 2007 1. Adjustments to reconcile net incometo net cash provided by (used in)operating activities:Net profit16,219.2212,853.22 Add:Impairment loss of assetsDepreciation of fixed assets, oil and gas64,806.349,397.28 assets and productive biological assetsAmortization of intangible assetsAmortization of long-term deferredexpensesLoss on disposal of fixed assets,intangible assets, other long terminvestment( “-”used for gain)Loss resulting from scraped asset(“-”used for gain)Loss from changes in fair value(“-”used for gain)Finance charges( “-”used for19,785.9126,479.78 Receipts)Investment losses( “-”used forgain)Decrease of deferred tax assets(-19,714.00“-”used for increase)Increase of deferred tax liabilities(“-”used for decrease)Decrease of inventory( “-”used forincrease)Decrease of operating receivables(-437,314.42-438,244.31“-”used for increase)Increase of operating payables(61,525.41272,294.98“-”used for decrease)Net cash flows from operating activities-294,691.53-117,219.05 2 Cash flows from investing andfinancing activities:Debt converted into capitalConvertible bonds due within one yearFixed assets held under a finance lease3.Changes in cash and cashequivalents:Net cash at the end of the period518,036.75879,676.27 Less: cash at the beginning of the period879,676.27-Add: cash equivalents at the end of theperiodLess: cash equivalent at the beginningof the periodNet Increase(Decrease) in Cash and-361,639.52879,676.27 Cash Equivalents22) Cash and Cash EquivalentsItems Year 2008Year 2007 (1)Cash518,036.75879,676.27 Include:Cash in hand6,219.60717.27Bank accounts with no restrictions on511,817.15878,959.00 withdrawOther monetary funds with no restrictionson withdrawDeposits and required reserve in centralbank with no restrictions on withdrawInter-bank DepositsInter-bank Loans(2)Cash EquivalentsInclude:Bonds investment with maturitydate less than three months(3)Cash equivalents at the end of the period518,036.75879,676.27 Include:Restricted cash and cashequivalents in Parent and other subsidiarycompanies8. Related Party Relationships and Transactions1) The identification of related partiesWhen a party controls, jointly controls or exercises significant influence over another party, or when a party is controlled or exercised significant influence by another party, or when two or more parties are under the common control, joint control or significant influence of the same party, the related party relationships are constituted.2) Related Party Relationships(1) Related parties where a control relationship existsName of the EnterprisePlace ofRegistrationMajoroperatingbusinessTherelationshipwith thecompanyOwnershipformsLegalRepresentativePPD Development (S) Pte Ltd.10 SciencePark Road,#02-04 TheAlpha,SciencePark IISingaporeManagingclinicalresearchprogramsParentcompanyLimitedCompanyBrainard JuddHartman(2) The amount of and the change in registered capital of related parties where a control relationship existsName of theEnterprise2007.12.31Increase Decrease2008.12.31PPD Development (S)SGD8,298,666.95--SGD8,298,666.95。

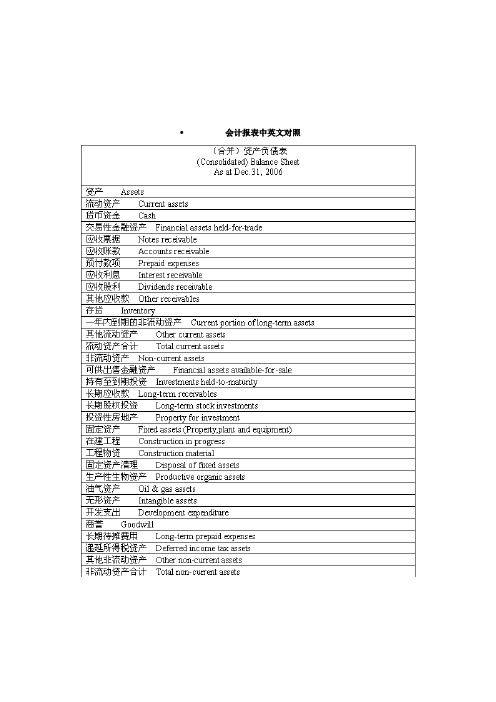

公司年报术语中英对照

公司年报术语中英对照english chineseAnnual Report 年報CONTENTS 目錄Corporate Information 公司資料Financial Highlights 財務摘要Chairman’s Statement主席報告書Directors and Senior Management Profile 董事及高級管理人員簡介Corporate Governance Report 企業管治報告Directors’ Report董事會報告Independent Auditor’s Report獨立核數師報告Consolidated Income Statement 綜合收益表Consolidated Statement of Comprehensive Income 綜合全面收益表Consolidated Statement of Financial Position 綜合財務狀況表Statement of Financial Position 財務狀況表Consolidated Statement of Changes in Equity 綜合權益變動表Consolidated Statement of Cash Flows 綜合現金流量表Notes to the Financial Statements 財務報表附註Financial Summary 財務概要DIRECTORS 董事Executive Directors 執行董事Deputy Chairman 副主席Chairman 主席Independent Non-executive Directors 獨立非執行董事AUDIT COMMITTEE 審核委員會REMUNERATION COMMITTEE 薪酬委員會COMPANY SECRETARY 公司秘書REGISTERED OFFICE 註冊辦事處HEAD OFFICE AND PRINCIPAL PLACE OF BUSINESS 總辦事處及主要營業地點PLACE OF BUSINESS 营业地点LEGAL ADVISERS 法律顾问PRINCIPAL BANKERS 主要往来银行Bank of China Limited 中國銀行股份有限公司Industrial & Commercial Bank of China Limited 中國工商銀行股份有限公司China Construction Bank Corporation 中國建設銀行股份有限公司China Merchants Bank Company Limited 招商銀行股份有限公司Standard Chartered Bank (Hong Kong) Limited 渣打銀行(香港)有限公司BNP Paribas 法國巴黎銀行CITIC Bank International Limited 中信銀行國際有限公司Bank of China (Hong Kong) Limited 中國銀行(香港)有限公司Nanyang Commercial Bank, Limited 南洋商業銀行有限公司PRINCIPAL SHARE REGISTRAR AND TRANSFER OFFICE 主要股份過戶登記處INTERNET WEBSITE 互聯網址STOCK CODE ON THE STOCK EXCHANGE OF HONG KONG LIMITED 香港聯合交易所有限公司股份代號PUBLIC RELATIONS CONSULTANT 公關顧問Strategic Financial Relations Limited 縱橫財經公關顧問有限公司TURNOVER 营业额For the year ended 31 December 截至十二月三十一日止年度NET PROFIT/(LOSS) ATTRIBUTABLE TO OWNERS OF THE COMPANY 本公司擁有人應佔溢利╱(虧損)淨HK$’M百萬港元The PRC 中国On behalf of 本人谨代表Board of Directors 董事会the “Company”本公司subsidiaries 附属公司together the “Group”合称“本集团”financial tsunami 金融海啸gradually subsided 慢慢减退the Chinese Government 中国政府launched new policies 推出新政策sales volume 销售配额upstream business 上游业务acquisition 收购specialising in 从事income stream 收入来源market demand 市场需求upstream products 上游产品refractory materials 耐火材料economic stimulus measures 刺激经济的措施integrate its operation 整合营运enhance cost effectiveness 优化成本效益gross profit margin 毛利率PROSPECTS 展望PLACING OF SHARES 股份配售fund raising 资金筹集REMUNERATION 薪酬APPRECIATION 致谢(Continued) (续)Note: 附注HK$’000千港元Turnover 营业额Cost of sales 销售成本Gross profit 毛利Profit/(loss) before taxation Income tax 除税前溢利(亏损)所得税Profit/(loss) for the year 本年度溢利(亏损)Attributable to: 应占Owners of the company 本公司拥有人Non-controlling interests 非控股权益Current assets 流动资产Non-current assets 非流动资产Total assets 资产总值Current liabilities 流动负债Non-current liabilities 非流动负债Total liabilities 总负债值Net assets 资产净值Share capital 股本Reserves 储蓄Non-controlling interests 非控股权益Total equity 权益总值FINANCIAL SUMMARY 财务概要NOTES TO THE FINANCIAL STATEMENTS 财务报表附注GENERAL 一般资料immediate parent 直接母公司ultimate controlling party 最终控股人士is incorporated in 于注册成立subsidiaries 附属公司SIGNIFICANT ACCOUNTING POLICIES 主要会计政策Statement of compliance 遵守声明Basis of preparation of the financial statements 财务报表编制基准historical cost basis 历史成本法the year under review 回顾年Profit after taxation 除税后净溢利LIQUIDITY 流动资金FINANCIAL RESOURCES 财务资源prudent capital arrangements 审慎财务安排unsecured bank loans 无抵押银行贷款short term bank loans 短期银行贷款cash and bank deposits 现金及银行存款pledged deposits 抵押存款trade receivable 应收账款trade facilities 贸易融资balance of net current assets 流动资产净额total liabilities to total assets ratio 总负债对应资产的比率material contingent liability 重大或然负债financial derivative products 金融衍生工具产品interest rate differential 息差stated bank loans 银行存款material risk from interest rate fluctuations 重大息率风险are denominated in Renminbi 以人民币结算appreciation of the Renminbi 人民币升值university graduates 大学毕业生staff remuneration and welfare system 薪酬及福利制度share option scheme 股权计划staff costs 雇员成本directors’ emoluments董事酬金business partners 业务伙伴senior economist 高级经济师marketing 市场推广Chinese Career Manager 中国职业经理人SENIOR MANAGEMENT 高级管理层CORPORATE GOVERNANCE REPORT 企业管治报告CORPORATE GOVERNANCE PRACTICES 企业管制常规DIRECTORS’ SECURITIES TRANSACTIONS 董事进行证券交易businesses, strategic decision and performance 业务、决策及表现TRAINING FOR DIRECTORS 董事培训PRACTICES AND CONDUCT OF MEETINGS 董事常规及操守Board papers 董事会文件appropriate, complete and reliable information 合适、完整及可靠之资料Board meeting 董事会会议committee meeting 委员会会议financial position 财务状况make informed decisions 做出知情决定PRACTICES AND CONDUCT OF MEETINGS 会议常规及操守conflict of interests for a substantial shareholder 设计主要股东利益冲突CHAIRMAN AND CHIEF EXECUTIVE OFFICER 主席及行政总裁ROTATION OF DIRECTORS 董事轮值退任forthcoming annual general meeting 应届股东周年大会interim review 中期查阅non-audit service 非审核服务DIRECTORS’ RESPONSIBILITIES ON THE FINANCIAL STATEMENTS董事对财务报表所负之责任a going concern basis 持续经营基准INTERNAL CONTROLS 内部控制system of internal controls 内部控制系统external advisor 外聘顾问SHAREHOLDER RIGHTS AND INVESTOR RELATIONS 股东福利及投资者关系voting procedures 投票程序by poll 以点票形式independent scrutineer 独立监票员DIRECTORS’ REPORT董事会报告PRINCIPAL ACTIVITIES 主要业务SEGMENTAL INFORMATION 分类资料RESULTS AND APPROPRIATIONS 业绩及分派DISTRIBUTABLE RESERVES OF THE COMPANY 本公司可供分派之储蓄FINANCIAL SUMMARY 财务概要PROPERTY, PLANT AND EQUIPMENT AND CONSTRUCTION-IN-PROGRESS 物业、房产、设施及在建工程SHARE CAPITAL 股本BORROWINGS 借贷RETIREMENT SCHEMES 退休金计划Nature of interest 權益性質Capacity 身份Number of Shares 股份数目% to the issued share capital of the Company 占本公司已发行股本的百分比Founder of a trust 信托之成立人Interest of spouse 配偶之权益Interests in shares, underlying shares or equity与相关公司股份、相关股份或股本权 interests in associated corporationsBeneficial owner 权益拥有人non-voting deferred shares 无投票权过延股份Interest of controlled corporation 受控公司之权益1 ordinary share 普通股份1股SHARE OPTION SCHEME 购股权计划nominal value of a share 股份面值SHORT POSITIONS 淡仓DIRECTORS’ INTERESTS IN CONTRACTS董事于合约的权益MANAGEMENT CONTRACTS 管理合约PURCHASE, SALE OR REDEMPTION OF THE COMPANY’S LISTED购买、出售或购回本公司的上市证券SECURITIESMAJOR CUSTOMERS AND SUPPLIERS 主要客户及供应商PRE-EMPTIVE RIGHTS 有限购股权SUFFICIENCY OF PUBLIC FLOAT 足够公众持股量statements of financial position 财务状况表consolidated income statement 综合收益表consolidated statement of comprehensive income 综合全面收益表consolidated statement of changes in equity 综合权益变动表consolidated statement of cash flows 综合现金流量表summary of significant accounting policies 主要会计政策概要DIRECTORS’ RESPONSIBILITY FOR THE CONSOLIDATED FINANCIAL董事就财务报表须承担的责任STATEMENTSdisclosure requirements 披露规定material misstatement 重大错误陈述due to fraud or error 由于欺诈或错误In our opinion 我们认为a true and fair 公平、真实Profit for the year 本年度溢利Earnings per share 每股盈利Basic 基本Diluted 摊薄form part of 构成其中一部分Other comprehensive income for the year (net of tax) 本年度其他全面收益(扣除税项)Exchange differences on translation of financial statements换算海外业务财务报表之汇兑差额of foreign operationsSurplus on revaluation of buildings held for own use 持作自用之楼宇重估盈余Deferred tax on revaluation of buildings held for own use 持作自用之楼宇延期税项Deferred tax arising on change in tax rate 税率变动之延期税项Fair value loss on available-for-sale equity securities 可供出售权益证券公平值亏损Total comprehensive income for the year 本年度全面收益总值Non-current assets 非流动资产Goodwill 商誉Property, plant and equipment 物业、房产及设备Prepaid lease payments on land under operating leases 经营租约下预付土地租金Intangible assets 无形资产Available-for-sale equity securities 可供出售权益证券Pledged bank deposits 已抵押银行存款Restricted bank balance 受限制银行结余Deferred tax assets 延期税项资产Current assets 流动资产Inventories 存货Trade and other receivables 应收账款及其他应收款Prepayments and deposits 预付款项及按金Tax recoverable 可收回税项Cash and cash equivalents 现金及现金等值项目Current liabilities 流动负债Trade payables 应付账款Accruals and other payables 预提费用及其他应付款Amounts due to directors 应付董事款项Bank borrowings due within one year 于一年内到期的银行贷款Tax payable 应付税项Net current assets 流动资产净值Total assets less current liabilities 资产总值减流动负债Deferred tax liabilities 延期税项负债NET ASSETS 资产净值CAPITAL AND RESERVES 资本及储蓄TOTAL EQUITY 权益总值Investments in subsidiaries 与附属公司之投资Amounts due from subsidiaries 应收附属公司款项Operating activities 经营活动Adjustments for 调整项目Depreciation 拆旧Amortisation of prepaid lease payments on land under经营租约下预付土地租金之摊销operating leasesAmortisation of intangible assets 无形资产摊销Impairment loss 减值亏损Write back of impairment loss 减值亏损拨回Net gains on disposal of property, plant and equipment 出售物业、厂房、设备之收益净值Reversal of write down of inventories 存货撇除拨回Bad debt written off 坏账撇销Operating cash flows before changes in working capital 营运资金变动前的经营现金流量(Increase)/decrease in inventories 存货(增加)/减少Decrease/(increase) in trade and other receivables 应收账款及其他应收款(增加)/减少(Increase)/decrease in prepayments and deposits 预存款项及按金(增加)/减少Increase/(decrease) in trade payables 应付账款(增加)/减少Decrease in accruals and other payables 预提费用及其他应付款减少(Decrease)/increase in amounts due to directors 应付董事款项(减少)/增加Cash (used in)/generated from operations 经营(使用)/所得的现金PRC Enterprise Income Tax paid 已付中国企业所得税Tax paid 已付税款Net cash (used in)/generated from operating activities 经营活动(使用)/所得的现金净值Investing activities 投资活动Purchase of property, plant and equipment 购置物业、房产及设备Proceeds from disposal of property,plant and equipment 出售物业、厂房、设备所得款项Payment for purchase of availablefor-sale equity securities 购买可供出售权益证券付款Interest received 已收利息Deferred consideration paid for acquisition of subsidiaries 已付收购公司之递延代价Financing activities 融资活动Net proceeds from placement of new shares 配售新股份之所得款项净值Repayment of bank borrowings 偿还银行贷款Proceeds from new bank borrowings 新造银行贷款所得款项Interest paid on bank borrowings 已付银行贷款利息Proceeds from shares issued under share option scheme 根据购股权计划发行股份是所得款项Net cash from financing activities 融资活动所得现金净值Net increase in cash and cash equivalents 现金及现金等值项目增加净值Cash and cash equivalents at beginning of the year 年初现金及现金等值项目Effect of changes in exchange rate 外币汇率变动之影响Cash and cash equivalents at end of the year 年末现金及现金等值项目principal place of business 主要营业地点Subsidiaries and non-controlling interests 附属公司及非控股权益contractual obligations 合约责任Jointly controlled entity 共同控制实体Other investments in equity securities 其他权益证券投资transaction price 交易价格Office equipment and fixtures 办公室设备及装置Motor vehicles 汽车Lease assets 租赁资产Classification of assets leased to the Group 出租于本集团之资产分类Operating lease charges 经营租赁费用Recognition of impairment losses 减值亏损确认Termination benefits 终止福利Provisions and contingent liabilities 拨备及或然负债Revenue recognition 收入确认prepared 编制Hong Kong Financial Reporting Standards 香港财务报表准则Hong Kong Institute of Certified Public Accountants 香港会计师公会Companies Ordinance 公司条例certain amendments 修订本interpretations 诠释are or have become effective 现时及已经生效accounting period 会计期间historical experience 过往经验Actual results may differ from these estimates. 实际数字或会有别于估计数字accounting estimates 会计估计Intra-group balances and transactions 集团内公司间之结余及交易unrealised profits 未变现溢利previously known as 前称minority interests 少数股东权益represent 指held for sale 持作出售。

财务报表附注翻译