5公司理财

公司理财罗斯第五章

钱变两倍。投资报酬率? 100=200/(1+r)8 __(1+r)8=2 (1)计算器:x^y ---1+r=2^0.125

(2) Rule of 72 (3) 财务函数RATE(8,0,-100,200)=9%

已知r, 本金翻倍所需期数

n

72

r 100

已知期数n, 本金翻倍所需报酬率

r

72

式两期后就可创造出1.1881元的投资收益。

若我们希望在两期后能有1元的收入,市场均衡利 率为9%情形下,请问本期应投资多少? PV×(1,09)2=1 PV=1÷(1.09)2=0.84168

如何验证0.84168的确是两年后1元的现值?

0.84168 ×(1.09)= 0.91743

1=0.91743 ×1.09 =(0.84168×1.09)×1.09=0.84168×(1.09)2

近日又闻湖南娄底一新入市投资者因屡买屡亏, 一年间入市资金从20万缩水成6千元,其间多次 买了就套、割了就涨,每次买在牛角割在熊掌, 又恰是屡战成名。经典案例是投资黄金股一役, 恰在启动前斩仓,斩仓后大涨,因而被亲友视 作反向选股风向标而获封“股神”称号。对照 娄底“股神”的交易对账单,频繁交易是落败 关键 (2008-3-26上海证券报姜韧) 。

第二节、基本现值等式及应用

张三购买彩票中了头奖,奖金100万元。张三 想将它存入银行,计划五年后将本金及利息用 于购房,而张三看上的房子其房价 为161万500 元。假设五年内房价不变,若张三将这笔奖金 存入银行,请问市场均衡利率水平应是多少才 让他五年后有足够钱支付房款。

现金支出 -100万元

公司理财(罗斯 第五版)

Corporate Finance

财务分析三

Fifth Edition

三、财务杠杆(长期偿债能力) 债务增大具有双重性:风险和收益 负债比率 = 总 负 债 总资产 负债权益比 = 总 债 务 总权益 权益乘数 = 总 资 产 总权益 利息保障倍数 = 息前税前利润 利息费用

Fifth Edition

公司理财

第五版

斯蒂芬 A.罗斯 (Stephen A.Ross)

Corporate Finance

Ross Westerfield Jaffe

罗德尔福 W.菲斯特费尔德

(Randolph W.Westerfield) 杰弗利 F.杰富 (Jeffrey F.Jaffe) 吴世农 沈艺峰 等译

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

. .

公司理财研究的问题

1-7 Fifth Edition

投资:资本预算、资本性支出、流动资产投资 筹资:资本成本、资本结构(V=B+S) 经营中现金流量管理:短期资本(流动资本)、 短

Corporate Finance

Ross Westerfield Jaffe

期负债(流动负债)、净营运资本(短期资本-短期 负债)

股利分配:股利政策 净营

运资本 流动资产

流动负债 长期负债

. .

固定资产 1、有形固定资产 2、无形固定资产

Irwin/McGraw-Hill

所有者权益

© The McGraw-Hill Companies, Inc., 1999

公司理财(第5版)第13章 公司股利政策

(三)固定支付比率的股利政策

• 固定支付比率的股利政策是指公司事先确定一个股利占税 后利润的百分比,以后每年均按这一比率向股东发放股利 。在固定支付比率的股利政策下,各年股利随公司经营好 坏而上下波动,盈余多的年份股利额高,盈余少的年份股利 额低。

• 从税收角度看,机构股东在股利和资本利得两者之间更偏 好高股利。

三、股利政策与交易成本

• 一般而言,经纪人佣金和发行费用与交易规模是呈反方向 变化的。由于存在规模经济,公司出售大批股票与个人出 售少量股票相比,相对显得便宜。

• 稳定地支付股利,可使股东免除因经常少量出售股票而带 来的麻烦和经纪人佣金。

• 一、公司利润的分配顺序

– 1.弥补以前年度亏损,计算可供分配的利润 – 2.计提法定盈余公积金 – 3.支付优先股利 – 4.计提任意盈余公积金 – 5.向普通股股东支付股利

二、股利的支付

• (一)股利的支付程序

– 一是股利宣告日,在这一天公司董事会将股利支付情况予以公告,宣 布每股股利、股权登记期限、除去股息的日期和股利支付日期。

第13章 公司股利政策

• 第1节 公司股利分配概述 • 第2节 公司股利政策 • 第3节 股利政策对公司发展的作用

本章要点

• ■ 公司利润的分配顺序; • ■ 股利支付的各种形式; • ■ 公司经常采用的股利政策; • ■ 影响公司股利政策的因素; • ■ 股利政策对公司发展的作用。

第1节 公司股利概述

• 总体来看,当宣布提高股利时,股价会上升;当宣布降低股利 时,股价会随之下降。

复习

• □ 重点概念

– 股利政策 现金股利 财产股利

负债股利

– 股票股利 剩余股利政策 固定或持续增长的股利政策

公司理财(第5版)第8章 资本预算中现金流量的估算

所得税

34

153

153

加:折旧

200

200

200

经营现金流量

266

497

497

4

5

240

0

81.6

0

200

200

358.4 200

ห้องสมุดไป่ตู้

• 2.测算净营运资本的变化

– 净营运资本(net working capital)指流动资产与流动负债之差。 – 把净利润调整为经营活动产生的现金流量时,需要做一个重要的调

• (一)现金流量转移

– 评价一个项目时,要考虑投资方案对公司其他项目的影响。 – 在测算增量现金流量时,我们应该把公司作为一个整体来考虑,而不

是仅仅着眼于某一独立的项目。

• (二)沉没成本

– 沉没成本是过去已经发生而且与现在决策无关的成本。 – 计算增量现金流量时应该对沉没成本忽略不计

• (三)机会成本

• 案例8-1 红光公司的资本预算项目 (详情见书P166) • 在该案例中,涉及了红光日用化工公司投资新项目的各项

收支。在进行资本预算时,关键的问题是判断和识别哪些 现金流量属于增量现金流量。

– 1.市场测试费用的处理 • 该案例中5万元的市场测试费用属于沉没成本,因为不管该项目 是否上马,市场测试环节中的现金流出已经发生,与该新产品决 策没有关系,故不应包括在洁净液项目的现金流量中。

– 经营现金流量=销售收入-经营成本-所得税

– (3)期末现金流量。指投资项目完结时所发生的现金流量,主要包括 • 固定资产的残值收入或变价收入 • 原有垫支在各种流动资产上的资金的收回 • 停止使用土地的变价收入等。

• 2.按现金的流入、流出来表述。

公司理财第四章筹资成本分析-精品

32

EBIT/ EBIT DOL= x/ x

= EBIT/ EBIT (px)/ px

式中: DOL为经营杠杆系 数; EBIT为变动前的息 税前利润; ΔEBIT为息税前利 润的变动额; px为变动前的销售 收入; Δ(px)为销售收入 的变动额; x为变动前的产销量; Δx为产销量的变动 数。

2020/5/29

西南政法大学

24

(1)固定成本

固定成本,是指其总额在一定时期和一 定业务量范围内不随业务量发生任何变 动的那部分成本。

属于固定成本的主要有按直线法计提 的折旧费、保险费、管理人员工资、办 公费等,这些费用每年支出水平基本相 同,即使产销业务量在一定范围内变动, 它们也保持固定不变。

p为销售单价; b为单位变动成本; x为产销量; m为单位边际贡献。

2020/5/29

西南政法大学

29

(三)息税前利润及其计算

息税前利润是指企业支付利息和交纳所得税 之前的利润。成本按习性分类后,息税前利润可 用下列公式计算:

EBIT=px-bx-a=(p-b)x-a=M-a

式中:EBIT为息税前利润;a为固定成本。

2020/5/29

西南政法大学

25

(2)变动成本

变动成本是指其总额随着业务量成 正比例变动的那部分成本。

直接材料、直接人工等都属于变动 成本。

但从产品的单位成本来看,则恰好 相反,产品单位成本中的直接材料、直 接人工将保持不变。

2020/5/29

西南政法大学

26

(3)混合成本

有些成本虽然也随业务量的变动而变 动,但不成同比例变动,不能简单地归 人变动成本或固定成本,这类成本称为 混合成本。

无风险利率Rf一般用同期国库券收益率表示, 这是证券市场最基础的数据。

公司理财第五版课件

School of International Trade & Economics

Professor Shao Xueyan

课程宗旨

创造财富 谋之有道 取之有术 管之有方

学习方法

学而不思则罔

思而不学则殆

选自《论语》

哈佛学生学习不是与未来就业相匹配的,他们 学的东西可能与他们将来所要做的工作完全不一样。 广泛的知识面、有专业技能、有一定的远见、有能 力在职业生涯中继续学习是哈佛对学生的培养目标。

◆ Making an outlay immediately vs. Yielding benefits in the distant future. ◆ A single large amount of outlay vs. A stream of smaller amount of cash inflows. ◆ It is difficult to withdraw from an investment. ◆ Time is vital to investment decision–making

Capital Structure

The mix of long term debt and equity financing.

Investment and Financing Decisions

The Investment Decision

Real Assets

The Financing Decision

Agency Problems

• Managers are agents for stockholders, but the managers may act in their own interests rather than maximizing value

公司理财英文版题库5

CHAPTER 5Interest Rate and Bond Valuation Multiple Choice QuestionsI. DEFINITIONSCOUPONa 1. The stated interest payment, in dollars, made on a bond each period is called the bond’s:a. coupon.b. face value.c. maturity.d. yield to maturity.e. coupon rate.Difficulty level: EasyFACE VALUEb 2. The principal amount of a bond that is repaid at the end of the loan term is called the bond’s:a. coupon.b. face value.c. maturity.d. yield to maturity.e. coupon rate.Difficulty level: EasyMATURITYc 3. The specified date on which the principal amount of a bond is repaid is called the bond’s:a. coupon.b. face value.c. maturity.d. yield to maturity.e. coupon rate.Difficulty level: EasyYIELD TO MATURITYd 4. The rate of return required by investors in the market for owning a bond is called the:a. coupon.b. face value.c. maturity.d. yield to maturity.e. coupon rate.Difficulty level: EasyCOUPON RATEe 5. The annual coupon of a bond divided by its face value is called t he bond’s:a. coupon.b. face value.c. maturity.d. yield to maturity.e. coupon rate.Difficulty level: EasyPAR BONDSa 6. A bond with a face value of $1,000 that sells for $1,000 in the market is called a _____ bond.a. par valueb. discountc. premiumd. zero coupone. floating rateDifficulty level: EasyDISCOUNT BONDSb 7. A bond with a face value of $1,000 that sells for less than $1,000 in the market is called a_____ bond.a. parb. discountc. premiumd. zero coupone. floating rateDifficulty level: EasyPREMIUM BONDSc 8. A bond with a face value of $1,000 that sells for more than $1,000 in the market is called a_____ bond.a. parb. discountc. premiumd. zero coupone. floating rateDifficulty level: EasyUNFUNDED DEBTd 9. The unfunded debt of a firm is generally understood to mean the firm’s:a. preferred stock.b. debts that mature in more than one year.c. debentures.d. debts that mature in less than one year.e. secured debt.Difficulty level: EasyINDENTUREa 10. The written, legally binding agreement between the corporate borrower and the lender detailingthe terms of a bond issue is called the:a. indenture.b. covenant.c. terms of trade.d. form 5140.e. call provision.Difficulty level: EasyREGISTERED BONDSb 11. The form of bond issue in which the registrar of the company records ownership of each bond,with relevant payments made directly to the owner of record, is called the _____ form.a. new-issueb. registeredc. bearerd. debenturee. collateralDifficulty level: MediumBEARER BONDSc 12. The form of bond issue in which the bond is issued without record of the owner’s name, withrelevant payments made directly to whoever physically holds the bond, is called the _____form.a. new-issueb. registeredc. bearerd. debenturee. collateralDifficulty level: EasyDEBENTURESe 13. The unsecured debts of a firm with maturities greater than 10 years are most literally called:a. unfunded liabilities.b. sinking funds.c. bonds.d. notes.e. debentures.Difficulty level: EasyNOTESd 14. The unsecured debts of a firm with maturities less than 10 years are most literally called:a. unfunded liabilities.b. sinking funds.c. bonds.d. notes.e. debentures.Difficulty level: EasySINKING FUNDa 15. An account managed by the bond trustee for early bond redemption payments is called a:a. sinking fund.b. collateral payment account.c. deed in trust account.d. call provision.e. par value fund.Difficulty level: EasyCALL PROVISIONb 16. An agreement giving the bond issuer the option to repurchase the bond at a specified price priorto maturity is the _____ provision.a. sinking fundb. callc. seniorityd. collaterale. trusteeDifficulty level: EasyCALL PREMIUMc 17. The amount by which the call price exceeds the bond’s par value is the:a. coupon rate.b. redemption value.c. call premium.d. original-issue discount.e. call rate.Difficulty level: EasySENIORITYe 18. In the event of default, _____ debt holders must give preference to more _____ debt holders inthe priority of repayment distributions.a. short-term; long-termb. long-term; short-termc. senior; juniord. senior; subordinatede. subordinated; seniorDifficulty level: MediumDEFERRED CALL PROVISIONd 19. A deferred call provision refers to the:a. open market price of a callable bond on a certain date.b. seniority of callable bonds to noncallable bonds in the event of corporate default.c. prohibition of a company from ever redeeming callable bonds.d. prohibition of a company from redeeming callable bonds prior to a certain date.e. amount by which the call price for a callable bond exceeds its par value.Difficulty level: EasyTREASURY BONDSa 20. The long-term bonds issued by the United States government are called _____ bonds.a. Treasuryb. municipalc. floating-rated. junke. zero couponDifficulty level: EasyMUNICIPAL BONDSb 21. The long-term bonds issued by state and local governments in the United States are called_____ bonds.a. Treasuryb. municipalc. floating-rated. junke. zero couponDifficulty level: EasyZERO COUPON BONDSe 22. A bond that makes no coupon payments and is initially priced at a deep discount is called a_____ bond.a. Treasuryb. municipalc. floating-rated. junke. zero couponDifficulty level: EasyFLOATING-RATE BONDSc 23. A bond that pays a variable amount of coupon interest over time is called a _____ bond.a. Treasuryb. municipalc. floating-rated. junke. zero couponDifficulty level: EasyPROTECTIVE COVENANTe 24. Parts of the indenture limiting certain actions that might be taken during the term of the loan toprotect the interests of the lender are called:a. trustee relationships.b. sinking funds provisions.c. bond ratings.d. deferred call provisions.e. protective covenants.Difficulty level: EasyCONVERTIBLE BONDSd 25. A bond which, at the election of the holder, can be swapped for a fixed number of shares ofcommon stock at any time prio r to the bond’s maturity is called a _____ bond.a. zero couponb. callablec. putabled. convertiblee. warrantDifficulty level: MediumPRICE TRANSPARENCYa 26. A financial market is _____ if it is possible to easily observe its prices and trading volume.a. transparentb. openc. orderedd. in equilibriume. chaoticDifficulty level: MediumCURRENT YIELDb 27. The annual coupon payment of a bond divided by its market price is called the:a. coupon rate.b. current yield.c. yield to maturity.d. bid-ask spread.e. capital gains yield.Difficulty level: EasyTIP BONDSb 28. A TIP bond’s interest rate is linked to:a. income.b. inflation.c. liquidity.d. maturity of the 30 year government bond.e. corporate tax rates.Difficulty level: MediumPUT BONDa 29. A bond that allows the holder to force the issuer to buy back bonds at a stated rate is called a:a. put bond.b. call bond.c. guaranteed bond.d. TIP bond.e. none of the above.Difficulty level: MediumNOMINAL RATESe 30. Interest rates or rates of return on investments that have not been adjusted for the effects ofinflation are called _____ rates.a. couponb. strippedc. effectived. reale. nominalDifficulty level: MediumREAL RATESa 31. Interest rates or rates of return on investments that have been adjusted for the effects ofinflation are called _____ rates.a. realb. nominalc. effectived. strippede. couponDifficulty level: MediumFISHER EFFECTb 32. The relationship between nominal rates, real rates, and inflation is known as the:a. Miller and Modigliani theorem.b. Fisher effect.c. Gordon growth model.d. term structure of interest rates.e. interest rate risk premium.Difficulty level: MediumTERM STRUCTURE OF INTEREST RATESc 33. The relationship between nominal interest rates on default-free, pure discount securities and thetime to maturity is called the:a. liquidity effect.b. Fisher effect.c. term structure of interest rates.d. inflation premium.e. interest rate risk premium.Difficulty level: MediumINFLATION PREMIUMd 34. The _____ premium is that portion of a nominal interest rate or bond yield that representscompensation for expected future overall price appreciation.a. default riskb. taxabilityc. liquidityd. inflatione. interest rate riskDifficulty level: EasyDEFAULT RISK PREMIUMa 35. The _____ premium is that portion of a nominal interest rate or bond yield that representscompensation for the possibility of nonpayment by the bond issuer.a. default riskb. taxabilityc. liquidityd. inflatione. interest rate riskDifficulty level: EasyII. CONCEPTSBOND FEATURESd 36. A bond with a 7 % coupon that pays interest semi-annually and is priced at par will have amarket price of _____ and interest payments in the amount of _____ each.a. $1,007; $70b. $1,070; $35c. $1,070; $70d. $1,000; $35e. $1,000; $70Difficulty level: MediumBOND PRICES AND YIELDSe 37. All else constant, a bond will sell at _____ when the yield to maturity is _____ the coupon rate.a. a premium; higher thanb. a premium; equal toc. at par; higher thand. at par; less thane. a discount; higher thanDifficulty level: MediumBOND PRICES AND YIELDSd 38. All else constant, a coupon bond that is selling at a premium, must have:a. a coupon rate that is equal to the yield to maturity.b. a market price that is less than par value.c. semi-annual interest payments.d. a yield to maturity that is less than the coupon rate.e. a coupon rate that is less than the yield to maturity.Difficulty level: EasyBOND PRICESc 39. The market price of a bond is equal to the present value of the:a. face value minus the present value of the annuity payments.b. annuity payments plus the future value of the face amount.c. face value plus the present value of the annuity payments.d. face value plus the future value of the annuity payments.e. annuity payments minus the face value of the bond.Difficulty level: EasyBOND PRICESa 40. As the yield to maturity increases, the:a. amount the investor is willing to pay to buy a bond decreases.b. longer the time to maturity.c. lower the coupon rate desired by that investor.d. higher the price the investor offers to buy a bond.e. lower the rate of return desired by the investor.Difficulty level: EasySEMIANNNUAL BONDSe 41. American Fortunes is preparing a bond offering with an 8 % coupon rate. Thebonds will be repaid in 10 years. The company plans to issue the bonds at par value and payinterest semiannually. Given this, which of the following statements are correct?I. The initial selling price of each bond will be $1,000.II. A fter the bonds have been outstanding for 1 year, you should use 9 as the number of compounding periods when calculating the market value of the bond.III. Each interest payment per bond will be $40.IV. The yield to maturity when the bonds are first issued is 8 %.a. I and II onlyb. II and III onlyc. II, III, and IV onlyd. I, II, and III onlye. I, III, and IV onlyDifficulty level: MediumSEMIANNUAL BONDS AND EFFECTIVE ANNUAL RATEd 42. The newly issued bonds of the Wynslow Corp. offer a 6 % coupon with semiannual interestpayments. The bonds are currently priced at par value. The effective annual rate provided bythese bonds must be:a. equal to 3 %.b. greater than 3 % but less than 4 %.c. equal to 6 %.d. greater than 6 % but less than 7 %.e. equal to 12 %.Difficulty level: MediumINTEREST RATE RISKd 43. Which one of the following statements is correct concerning interest rate risk as it relates tobonds, all else equal?a. The shorter the time to maturity, the greater the interest rate risk.b. The higher the coupon rate, the greater the interest rate risk.c. For a bond selling at par value, there is no interest rate risk.d. The greater the number of semiannual interest payments, the greater the interest rate risk.e. The lower the amount of each interest payment, the lower the interest rate risk.Difficulty level: MediumINTEREST RATE RISKe 44. Which one of the following bonds has the greatest interest rate risk?a. 5-year; 9 % couponb. 5-year; 7 % couponc. 7-year; 7 % coupond. 9-year; 9 % coupone. 9-year; 7 % couponDifficulty level: MediumINTEREST RATE RISKb 45. Interest rate risk _____ as the time to maturity increases.a. increases at an increasing rateb. increases at a decreasing ratec. increases at a constant rated. decreases at an increasing ratee. decreases at a decreasing rateDifficulty level: MediumINTEREST RATE RISKc 46. You own a bond that has a 7 % coupon and matures in 12 years. You purchasedthis bond at par value when it was originally issued. If the current market rate for thistype and quality of bond is 7.5 %, then you would expect:a. the bond issuer to increase the amount of each interest payment on these bonds.b. the yield to maturity to remain constant due to the fixed coupon rate.c. to realize a capital loss if you sold the bond at the market price today.d. today’s market price to exceed the face value of the bond.e. the current yield today to be less than 7 %.Difficulty level: MediumINTEREST RATE RISKb 47. A brand with semi-annual interest payments, all else equal, would be priced _________ thanone with annual interest payments.a. higherb. lowerc. the samed. it is impossible to telle. either higher or the sameDifficulty level: MediumYIELD TO MATURITY AND CURRENT YIELDe 48. All else constant, as the market price of a bond increases the current yield _____ andthe yield to maturity _____a. increases; increases.b. increases; decreases.c. remains constant; increases.d. decreases; increases.e. decreases; decreases.Difficulty level: MediumBOND FEATURESd 49. Which of the following statements concerning bond features is (are) correct?I. Bondholders generally have voting power in a corporation.II. Bond interest is tax-deductible as a business expense.III. The repayment of the bond principle is tax-deductible.IV. Failure to pay either the interest payments or the bond principle as agreed can cause a firm to go into bankruptcy.a. II onlyb. I and II onlyc. III and IV onlyd. II and IV onlye. II, III, and IV onlyDifficulty level: MediumBOND INDENTUREd 50. Which of the following items are generally included in a bond indenture?I. call provisionsII. security descriptionIII. current yieldIV. protective covenantsa. I and II onlyb. II and IV onlyc. II, III, and IV onlyd. I, II, and IV onlye. I, II, III, and IVDifficulty level: MediumBOND CLASSIFICATIONSe 51. Which one of the following statements is correct concerning bond classifications?a. A debenture is a long-term bond secured by the fixed assets of a firm.b. A mortgage security is a bond issued solely by a home builder.c. A note is a bond which has an original maturity date longer than 10 years.d. A subordinated bond receives preferential treatment over all other bonds in abankruptcy.e. A callable bond can be repurchased by the issuer prior to the initial maturity date.Difficulty level: MediumCALLABLE BONDSb 52. Callable bonds generally:a. allow the bondholder to decide when the bond is to be called.b. are associated with sinking funds.c. permit the issuer to repurchase the bonds at a discount.d. are called within the first couple of years after issuance.e. are required to have a deferred call provision if they have a “make-whole” callprovision.Difficulty level: MediumPROTECTIVE COVENANTSc 53. Which of the following is a (are) positive covenant(s) that might be found in a bondindenture?I. The company shall maintain a current ratio of 1.5 or better.II. The company must limit the amount of dividends it pays according to the stated formula.III. The company cannot lease any major assets without approval by the lender.IV. The company must maintain the loan collateral in good working order.a. I onlyb. I and II onlyc. I and IV onlyd. II and IV onlye. I, II, and IV onlyDifficulty level: ChallengePROTECTIVE COVENANTSe 54. Protective covenants:a. are primarily designed to protect the issuing corporation from unreasonable demandsof bondholders.b. are consistent for all bonds issued by a corporation within the United States.c. are limited to stating actions which a firm must take.d. only apply to bonds that have a deferred call provision.e. are primarily designed to protect bondholders from future actions of the bond issuer.Difficulty level: MediumBOND RATINGSb 55. Which one of the following statements concerning bond ratings is correct?a. Standard and Poor’s and Value Line are the primary bond rating agencies.b. Bond ratings are solely an assessment of the creditworthiness of the bond issuer.c. Investment grade bonds include only those bonds receiving one of the highest threebond ratings.d. Bond ratings evaluate the expected price volatility of a bond issue.e. All bonds receive the same rating classification from all rating agencies.Difficulty level: MediumBOND RATINGSd 56. A “fallen angel” is a bond that:a. lowered its annual interest payment.b. has moved from being a long-term obligation to being a short-term obligation.c. has moved from having a yield to maturity in excess of the coupon rate to having ayield to maturity that is less than the coupon rate.d. has moved from being an investment-grade bond to being a junk bond.e. is rated as Ba by one rating agency and rated as BB by another rating agency.Difficulty level: MediumTREASURY BONDSa 57.Bonds issued by the U.S. government:I. are considered to be free of default risk.II. are considered to be free of interest rate risk.III. provide totally tax-free income.IV. pay interest that is exempt from federal income taxes.a. I onlyb. I and III onlyc. I and IV onlyd. II and III onlye. II and IV onlyDifficulty level: MediumTREASURY BONDSd 58. Treasury bonds are:a. those bonds issued by any governmental agency in the U.S.b. issued only on the first day of each fiscal year by the U.S. Department of Treasury.c. preferred by high-income individuals because they offer the best tax benefits.d. generally issued as coupon bonds.e. totally risk-free.Difficulty level: MediumMUNICIPAL BONDSa 59. Municipal bonds:a. offer income tax advantages to individuals.b. generally pay a higher rate of return than corporate bonds.c. are those bonds issued only by local municipalities, such as a city or a borough.d. are rarely callable.e. pay interest that is always exempt from both federal and state income taxes.Difficulty level: EasyTAXABLE VERSUS MUNICIPAL BONDSd 60. The break-even tax rate between a taxable corporate bond yielding 7 % and acomparable nontaxable municipal bond yielding 5 % can be expressed as:a. .07 ÷ (1 - t*) = .05.b. .05 ÷ (1 - t*) = .07.c. .07 + (1 - t*) = .05.d. .07 ⨯ (1 - t*) = .05.e. .05 ⨯ (1 - t*) = .07.Difficulty level: MediumZERO COUPON BONDSe 61. A zero coupon bond:a. is sold at a large premium.b. has a price equal to the future value of the face amount given a specified rate ofreturn.c. can only be issued by the U.S. Treasury.d. has less interest rate risk than a comparable coupon bond.e. has implicit interest which is calculated by amortizing the loan.Difficulty level: MediumZERO COUPON BONDSb 62. The total interest paid on a zero-coupon bond is equal to:a. zero.b. the face value minus the issue price.c. the face value minus the market price on the maturity date.d. $1,000 minus the face value.e. $1,000 minus the par value.Difficulty level: MediumFLOATING-RATE BONDSd 63. The collar of a floating-rate bond refers to the minimum and maximum:a. call periods.b. maturity dates.c. market prices.d. coupon rates.e. yields to maturity.Difficulty level: MediumFLOATING-RATE BONDSd 64. Which of the following are common characteristics of floating-rate bonds?I. adjustable coupon ratesII. adjustable maturity datesIII. put provisionIV. coupon capa. I and II onlyb. II and III onlyc. I, II, and IV onlyd. I, III, and IV onlye. I, II, III, and IVDifficulty level: MediumFLOATING RATE BONDSc 65. A corporation is more prone to issue floating-rate bonds when they expect futureinterest rates to _____ over the life of the bond.a. remain constantb. increase briefly and then decline slightlyc. continually declined. decline briefly and then increase significantlye. continually increaseDifficulty level: EasyYIELD TO MATURITYe 66. The yield to maturity isa. the rate that equates the price of the bond with the discounted cash flows.b. the expected rate to be earned if held to maturity.c. the rate that is used to determine the market price of the bond.d. equal to the current yield for bonds priced at par.e. All of the above.Difficulty level: MediumTYPES OF BONDS AND INVESTOR PREFERENCESc 67. Investors generally tend to buy:a. Treasury bonds for their high yields.b. municipal bonds for their high yields.c. convertible bonds for their potential price appreciation.d. corporate bonds for their liquidity.e. Treasury bonds for their preferential tax treatment.Difficulty level: MediumTYPES OF BONDSb 68. A convertible bond is a bond that can be:a. exchanged for cash at prescribed points in time.b. exchanged for a stated number of shares of common stock of the bond issuer.c. modified from a fixed coupon bond into a floating coupon bond at prescribed points intime.d. submitted to the issuer for redemption at the discretion of the bondholder.e. submitted for payment any time the economy converts into a recessionary period.Difficulty level: EasyPUT PROVISIONc 69. A put provision in a bond indenture allows:a. a bond issuer to recall the bond after a specified period of time at a price that exceedsthe face amount.b. a bondholder to force the issuer to increase the coupon rate if inflation increases by more than aspecified amount.c. the bondholder to force the issuer to buy back the bond at a specified price prior tomaturity.d. the issuer to convert a coupon bond into a zero coupon bond at their discretion.e. t he issuer to suspend interest payments for any year in which the interest expense exceeds thenet income of the firm.Difficulty level: EasyFACE VALUEe 70. Face value isa. always higher than current price.b. always lower than current price.c. the same as the current price.d. the coupon amount.e. None of the above.Difficulty level: EasyBASIS POINTa 71. One basis point is equal to:a. .01 %.b. .10 %.c. 1.0 %.d. 10 %.e. 100 %.Difficulty level: EasyCORPORATE BOND QUOTEc 72. The “EST SPREAD” shown in The Wall Street Journal listing of corporate bondsrepresents the estimated:a. yield to maturity.b. difference between the current yield and the yield to maturity.c. difference between the bond’s yield and the yield of a particular Treasury issue.d. range of yields to maturity provided by the bond over its life to date.e. difference between the yield to call and the yield to maturity.Difficulty level: MediumCOUPON PAYMENTb 73. A bond is listed in The Wall Street Journal as a 12 3/4s of July 2009. This bonds paysa. $127.50 in July and January.b. $63.75 in July and January.c. $127.50 in July.d. $63.75 in July.e. None of the above.Difficulty level: EasyYIELD TO MATURITYc 74. If its yield to maturity is less than its coupon rate, a bond will sell at a _____, and increases inmarket interest rates will _____.a. discount; decrease this discount.b. discount; increase this discount.c. premium; decrease this premium.d. premium; increase this premium.e. None of the above.Difficulty level: MediumCLEAN VERSUS DIRTY PRICESc 75. Today, August 13, you want to buy a bond with a quoted price of 101.5. The bondpays interest on February 1 and August 1. The price you will pay to purchase thisbond is equal to the:a. clean price.b. muddy price.c. dirty price.d. par value price.e. bid price.Difficulty level: MediumREAL RATE OF RETURNd 76. The increase you realize in buying power as a result of owning a bond is referred to asthe _____ rate of return.a. inflatedb. realizedc. nominald. reale. risk-freeDifficulty level: EasyFISHER EFFECTe 77. The Fisher formula is expressed as:a. 1 + r = (1 + R) ÷ (1 + h).b. 1 + r = (1 + R) ⨯ (1 + h).c. 1 + h = (1 + r) ÷ (1 + R).d. 1 + R = (1 + r) ÷ (1 + h).e. 1 + R = (1 + r) ⨯ (1 + h).Difficulty level: MediumFISHER EFFECTd 78. The Fisher Effect primarily emphasizes the effects of _____ risk on an inv estor’s rateof return.a. defaultb. marketc. interest rated. inflatione. maturityDifficulty level: EasyTERM STRUCTURE OF INTEREST RATESa 79. The term structure of interest rates reflects the:a. pure time value of money for various lengths of time.b. actual risk premium being paid for corporate bonds of varying maturities.c. pure inflation adjustment applied to bonds of various maturities.d. interest rate risk premium applicable to bonds of varying maturities.e. nominal interest rates applicable to coupon bonds of varying maturities.Difficulty level: EasyBOND VALUESa 80. The market price of _____ maturity bonds fluctuates _____ compared with _____ maturitybonds as interest rates change.a. shorter; less; longerb. longer; less; shorterc. shorter; more; longerd. Both B and c.e. None of the above.Difficulty level: MediumCORPORATE VERSUS TREASURY BONDSc 81. Two of the primary differences between a corporate bond and a Treasury bond withidentical maturity dates are related to:a. interest rate risk and time value of money.b. time value of money and inflation.c. taxes and potential default.d. taxes and inflation.e. inflation and interest rate risk.Difficulty level: MediumIII. PROBLEMSBOND VALUATIONc 82. Consider a bond which pays 7% semiannually and has 8 years to maturity. The market requiresan interest rate of 8% on bonds of this risk. What is this bond's price?a. $ 942.50b. $ 911.52c. $ 941.74d. $1,064.81e. None of the above.Difficulty level: EasyZERO COUPON BONDa 83. The value of a 20 year zero-coupon bond when the market required rate of return of 9%(semiannual) is ____ .a. $171.93b. $178.43c. $318.38d. $414.64e. None of the above.Difficulty level: EasyYIELD TO MATURITYc 84. The bonds issued by Jensen & Son bear a 6 % coupon, payable semiannually. The bondmatures in 8 years and has a $1,000 face value. Currently, the bond sells at par. What is theyield to maturity?a. 5.87 %b. 5.97 %c. 6.00 %d. 6.09 %e. 6.17 %Difficulty level: MediumYIELD TO MATURITYa 85. A General Co. bond has an 8 % coupon and pays interest annually. The face value is $1,000and the current market price is $1,020.50. The bond matures in 20 years. What is the yield tomaturity?a. 7.79 %。

公司理财名词解释整理

Chapter2资产负债表是反映企业在某一特定日期财务状况的报表利润表用来衡量企业在一个特定时期(如一年)内的业绩。

折旧是将过去的固定资产支出(成本)在将来的期限内分摊,进行收入与费用的配比,以合理地反映报告期的收益。

直线法——每年都提取等额的折旧。

加速折旧法——在固定资产使用的早期多提折旧,相应地在后期少提折旧。

它并没有在总量上多折旧,只是改变了确认的时间。

递延税款是由会计利润(向股东报告)和实际应纳税利润(向税务部门报告)之间的差异引起的。

3一项投资在期末的本息合计金额被称为终值(Future Value, FV),或复利值。

现值(Present Value,PV)是未来现金流折算到今天的价值。

某个项目的净现值(Net Present Value,NPV)等于该项目的预期现金流量的现值与项目投资成本之差。

永续年金(Perpetuity)是一系列没有止境的固定的现金流量永续增长年金(Growing Perpetuity)是一系列没有止境的且具有永续增长趋势的现金流量年金(Annuity)是一系列固定、有规律、持续一段时期的现金流量。

用来计算T期内等额支付1元现金流价值通常称为年金(现值)系数AA A。

增长年金(Growing Annuity)是一种在有限时期内增长的现金流量。

费雪分离定理一个人的投资决策与消费决策是可以分开进行的,最优的投资决策与人们的消费偏好无关.4回收期 (payback) = 收回项目初始投资的年数折现回收期:在考虑货币的时间价值后,项目收回它的初始投资需要的时间内部收益率(Internal Rate of Return, IRR):使得项目的净现值(NPV)等于0的贴现率盈利指数(profitability index,PI)是初始投资以后所有预期未来现金流的现值和初始投资的比,也叫现值指数平均会计收益率(Average accounting return,AAR)是会计平均净利润与项目期内平均账面净投资额之比平均报酬率(Average rate of return,ARR)是投资项目寿命周期内的年平均现金流入量与初始投资额的比值5增量现金流量:公司接受项目和不接受项目引起的现金流量的差别,即与项目有关的现金流量。

江苏自考07524公司理财重点知识点汇总速记宝典

公司理财(32-07524适用江苏)速记宝典一、简答题命题来源:围绕学科的基本概念、原理、特点、内容。

答题攻略:(1)不能像名词解释那样简单,也不能像论述题那样长篇大论,但需要加以简要扩展。

(2)答案内容要简明、概括、准确,即得分的关键内容一定要写清楚。

(3)答案表述要有层次性,列出要点,分点分条作答,不要写成一段;(4)如果对于考题内容完全不知道,利用选择题找灵感,找到相近的内容,联系起来进行作答。

如果没有,随意发挥,不放弃。

考点1:简述确立公司理财目标的优点。

答:公司在确定财务管理目标时,应从股东的利益出发,选择股东财富最大化。

(1)考虑了获取收益的时间因素和风险因素;(2)克服公司在追求利润上的短期行为,保证了公司的长期发展;(3)充分体现公司所有者对资本保值与增值的要求。

考点2:简述如何解决代理问题。

答:(1)股东与经营者——资本的所有者与经营权分离,会导致产生“机会主义倾向”,“道德风险”等问题,最好方法就是建立激励和约束经营者的长期契约或合约,外加监督机制。

(2)股东与债权人——股东与债权人之间是一种“不平等”的契约关系,解决方法降低债券投资的支付价格或者提高利率,还会在债务契约中增加各种限制性条款。

考点3:请简述金融市场的作用。

答:(1)资本的筹措与投放:一方面吸收不同期限的资本,另一方面投资金融工具获取额外收益。

(2)分散风险:每个风险投资者所承担的风险量减少;通过期货、期权交易对冲风险。

(3)转售市场:二级市场股票转让,公司筹集巨额资本。

(4)降低交易成本:减少了信息成本和搜集成本,降低了公司的交易成本。

(5)确定金融资产价格:金融市场交易中形成的各种参数是进行财务决策的前提和基础。

考点4:简述三种不同程度的市场效率。

答:(1)弱式效率性:所有包含在过去证券价格变动的资料和信息(价格、交易量等历史资料)都已完全反映在证券的现行市价中。

因此,任何投资者不能通过任何方式分析历史信息获取超额收益。

公司理财英文版第五章第六章-表格

• Formula:

1 1 (1.01) 48 PV 632 23,999.54 .01

6F-18

Buying a House

• You are ready to buy a house, and you have $20,000 for a down payment and closing costs. Closing costs are estimated to be 4% of the loan value. You have an annual salary of $36,000, and the bank is willing to allow your monthly mortgage payment to be equal to 28% of your monthly income. The interest rate on the loan is 6% per year with monthly compounding (.5% per month) r a 30-year fixed rate loan. How much money will the bank loan you? How much can you offer for the house?

• Future value interest factor = (1 + r)t

5F-6

Effects of Compounding

• Simple interest • Compound interest • Consider the previous example

– FV with simple interest = 1,000 + 50 + 50 = 1,100 – FV with compound interest = 1,102.50 – The extra 2.50 comes from the interest of .05(50) = 2.50 earned on the first interest payment

《公司理财》习题及答案

《公司理财》习题及答案-CAL-FENGHAI-(2020YEAR-YICAI)」INGBIAN《公司理财》习题答案第一章公司理财概论案例:华旗股份公司基本财务状况华旗股份有限公司,其前身是华旗饮料厂,创办于20世纪80年代,当时是当地最大的饮料企业,生产的“华旗汽水”是当地的名牌产品,市场占有率较高。

2003年改组为华旗股份有限公司,总股本2 500万股。

公司章程中规定,公司净利润按以下顺序分配:(2)弥补上一年度亏损;(2)提取10%的法定公积金;(3)提取15%任意公积金;(4)支付股东股利。

公司实行同股同权的分配政策。

公司董事会在每年会计年度结束后提出分配预案,报股东大会批准实施。

除股东大会另有决议外,股利每年派发一次,在每个会计年度结束后六个月内,按股东持股比例进行分配。

当董事会认为必要时,在提请股东大会讨论通过后,可增派年度中期股利。

随着市场经济的不断深化,我国饮品市场发展越来越迅猛,全球市场一体化趋势在饮品市场尤为突出,一些国内外知名饮品,如可口可乐、百事可乐、汇源等,不断涌入本地市场,饮品行业竞争日益激烈。

华旗公司的市场占有率不断降低,经营业绩也随之不断下降,公司管理层对此忧心忡忡,认为应该对华旗公司各个方面进行重新定位,其中包括股利政策。

华旗公司于2015年1月15日召开莆事会会议,要求公司的总会计师对公司LI前财务状况做出分析,同时提出新的财务政策方案,以供董事会讨论。

总会计师为此召集有关人员进行了深入细致的调查,获得了以下有关资料:(一)我国饮品行业状况近儿年我国饮品行业发展迅速,在国民经济各行业中走在了前列,目前市场竞争非常激烈,但市场并没有饱和。

从资料看,欧洲每年人均各类饮品消费量为200公斤,我国每年人均消费各种饮料还不到10公斤。

可见,我国饮品仍有着巨大的市场潜力。

果味饮料、碳酸饮料市场日趋畏缩,绿色无污染保健饮品、纯果汁饮品、植物蛋白饮品,以及茶饮品,正在成为饮品家族的新生力量,在市场上崭露头角,市场潜力巨大。

公司理财(罗斯)第5章(英文)

McGraw-Hill/Irwin Corporate Finance, 7/e

5-2

Valuation of Bonds and Stock

First Principles:

Value of financial securities = PV of expected future cash flows

5-10

Example of pure discount bonds:

What is the price of a 25-year, pure discount bond that pays $50 at maturity if the current yield-to maturity is 8 percent? 0 1 2… 25 |----------|---------|-------------------| $50 PV0 = 50 ÷ (1.08)25 = $7.30

Time to maturity (T) = Maturity date - today’s date Face value (F) Discount rate (r)

$0

0

$0

$0

$F

T

1

2

T 1

Present value of a pure discount bond at time 0:

F PV = T (1+ r)

批注本地保存成功开通会员云端永久保存去开通

5-0

CHAPTER

5

2005 The McGraw-Hill Companies, Inc. All Rights Reserved.

公司理财(第5版)第7章 资本预算与公司投资决策

– “独立”是指是否选择该项目不取决于其他项目。若进行一项投 资就不能进行另一项投资,或者正相反,那么这两项投资就是互斥的 。

– “常规”是指一个项目有初始现金流出量后,在未来各期都有现金 流入量,即投资后预期未来各年的现金流量都为正值。

• 在遇到非常规项目时,使用内部收益率法就很难做出决策 了。

• 显然,净现值越大的项目,为公司创造的价值越大;净现值为 负的项目,不仅不能创造价值,反而会消耗公司的财富;净现 值为零的项目,既没有为公司创造财富,也没有消耗公司财 富。

• 净现值法的运用程序可分为以下步骤:

– (1)估算出投资方案的预期现金流量;

– (2)估计项目的风险,确定资本成本;

– (3)计算出项目的净现值,净现值大于零则可接受该方案,净现值小 于零则拒绝该方案。

–

3+(100/200)=3.5(年)

• 该生产线的回收期大于3年,因此应该放弃。

[例7—2]

• 东兴公司现有两个备选方案。方案一:投资购建一条新的生产线;方案 二:投资改造现有的生产线。假设两个方案的初始投资都是1 000万元, 两个方案投产后预计产生的现金流量如表7-2所示。如果东兴公司希 望在3年内收回初始投资,那么应该选择哪一个方案?

五、会计收益率法

• 会计收益率(accounting rate of return,ARR)是指投资项目 年平均净收益与该项目年平均投资额的比率。

• 其计算公式为:

会计收益率

年平均净收益 年平均投资额

100 %

• 式中,年平均净收益可按项目投产后各年净收益总和简单 平均计算;年平均投资总额是指固定资产投资账面价值的 平均数。

第5章-资本成本 (《公司理财》PPT课件)

2020年5月

第6页

第一节 资本的构成

2. 加权平均资本成本的计算

例1:假设某公司债务成本为8%,所得税率为25%,权益资 本成本为14%,则公司按照30%债务融资,70%股权融资的方 式进行筹资,求资本成本。

WACC=14%*70%+8%*30%*(1-25%)=11.60%

2020年5月

第7页

2020年5月

第15页

第二节 权益成本

• 权益成本计算的两种思路: • 1、公司的角度:预计未来支付给股东的股利和现

在的筹资费用,计算出权益成本;

• 计算方法:股利法 • 2、资本市场角度:遵循风险与收益对等原则,按

照股东承担风险的大小,计算其应得到的回报, 股东回报即为资本成本;

• 计算方法:资本资产定价模型和套利定价模型

K

(1

5% )4 4

1(1

25%)

3.82%

2020年5月

第10页

第一节 资本的构成

5. 债券成本

①债务资本成本K=I*(1-T)/ B0(1-f)=i*B*(1-T)/ B0(1-f)

I:债券每年支付的年利息;B:债券面值;i:债券的票面利息率;

B0:债券筹资额,按照发行价格确定;f:债券筹资费率;

债券:股利在税前支付,且有固定到期期限;

优先股:股利在税后支付,没有固定的到期期限;

Kp

D P0 (1

f

)

K p : 优先股成本; D : 优先股每年股利; P0:发行优先股总额; f : 优先股筹资费率;

2020年5月

第20页

第二节 权益成本

①公司破产时,优先股求偿权位于债券持有人之后,优先股股东的风 险大于债券持有人的风险,因此优先股的股利率一般要求高于债券的 利息率;

公司理财第五版课后习题答案

公司理财第五版课后习题答案考试题型:一、单项选择题:15分二、多项选择题:10分三、填空题15分四、名词解释:15分后五、简答题:15分后六、计算题:30分后一、单项选择题1、在筹资投资理财阶段,公司投资理财的重点内容就是()。

BA有效运用资金 B如何设法筹集到所需资金 C研究投资组合 D国际融资2、以往被西方经济学家和企业家做为公司的经营目标和投资理财目标的就是()。

AA利润最大化 B资本利润率最大化 C每股利润最大化 D股东财富最大化3、现代公司投资理财的目标就是()。

CA获利能力最大化 B偿债能力最大化 C股东财富最大化 D追求利润最大化4、由于生产经营不断地展开而引发资金不断地循环叫做()。

CA资金运动 B财务活动 C资金周转 D资金耗费二、多项选择题1、以利润最大化作为公司理财目标存在的缺陷有()。

ABCDEA无法精确充分反映所荣获利润额同资金投入资本额的关系 B没考量利润出现的时间C会导致公司理财决策者的短期行为 D没有考虑货币的时间价值E没考虑到经营风险问题2、股东财富最大化作为公司理财目标的优点有()。

ABCDEA考量了货币的时间价值 B考量了风险价值C体现了对公司资产保值增值的要求 D克服公司经营上的短期行为E使得公司投资理财当局从长远战略角度展开财务决策3、公司的财务活动包括()。

ABCDEA资金的筹措 B资金的运用 C资金的花费 D资金的归还 E资金的分配4、公司理财的内容主要有()。

ABEA筹资决策 B投资决策 C成本决策 D价格决策 E股利分配决策三、填空题1、直观地谈,公司投资理财就是公司如何(万晓塘、多管齐下、以有)。

2、公司理财产生至今经历了筹资、(内部控制)、投资和国际理财阶段。

3、在内部掌控投资理财阶段,公司投资理财的重点内容就是如何有效地(运用资金)。

4、投资理财阶段重视两项理财内容:一是研究公司(最佳资本结构)的构成;一是研究(投资组再分理论)及其对公司财务决策的影响。

金融研究生必读书目i

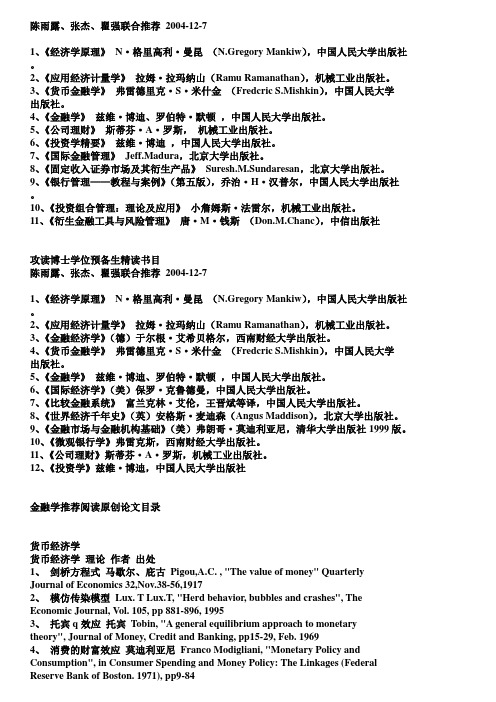

陈雨露、张杰、瞿强联合推荐2004-12-71、《经济学原理》N·格里高利·曼昆(N.Gregory Mankiw),中国人民大学出版社。

2、《应用经济计量学》拉姆·拉玛纳山(Ramu Ramanathan),机械工业出版社。

3、《货币金融学》弗雷德里克·S·米什金(Fredcric S.Mishkin),中国人民大学出版社。

4、《金融学》兹维·博迪、罗伯特·默顿,中国人民大学出版社。

5、《公司理财》斯蒂芬·A·罗斯,机械工业出版社。

6、《投资学精要》兹维·博迪,中国人民大学出版社。

7、《国际金融管理》Jeff.Madura,北京大学出版社。

8、《固定收入证券市场及其衍生产品》Suresh.M.Sundaresan,北京大学出版社。

9、《银行管理——教程与案例》(第五版),乔治·H·汉普尔,中国人民大学出版社。

10、《投资组合管理:理论及应用》小詹姆斯·法雷尔,机械工业出版社。

11、《衍生金融工具与风险管理》唐·M·钱斯(Don.M.Chanc),中信出版社攻读博士学位预备生精读书目陈雨露、张杰、瞿强联合推荐2004-12-71、《经济学原理》N·格里高利·曼昆(N.Gregory Mankiw),中国人民大学出版社。

2、《应用经济计量学》拉姆·拉玛纳山(Ramu Ramanathan),机械工业出版社。

3、《金融经济学》(德)于尔根·艾希贝格尔,西南财经大学出版社。

4、《货币金融学》弗雷德里克·S·米什金(Fredcric S.Mishkin),中国人民大学出版社。

5、《金融学》兹维·博迪、罗伯特·默顿,中国人民大学出版社。

6、《国际经济学》(美)保罗·克鲁德曼,中国人民大学出版社。

【公司管理】公司理财

【公司管理】公司理财第一章公司理财概述一、名词解释1、公司理财2、财务活动二、单项选择1、公司理财在筹资理财阶段的重点内容是()。

A、有效运用资金B、如何设法筹集到所需资金C、研究投资组合D、国际融资2、内部控制理财阶段公司理财的重点内容是()。

A、有效运用资金B、如何设法筹集到所需资金C、研究投资组合D、国际融资3、现代公司理财的目标是()。

A、获利能力最大化B、偿债能力最大化C、追求财富最大化D、追求利润最大化4、当()达到最高时,意味着股东财富达到最大化。

A、每股溢价B、每股股利C、每股收益D、股票价格5、资金运动的起点和终点都是()。

A、货币资金B、商品资金C、生产资金D、结算资金6、由于生产经营活动地进行而引起资金不断地循环叫做()。

A、资金运动B、财务活动C、资金周转D、资金耗费7、资金的运用、耗费和收回又称为()。

A、分配B、投资C、支出D、决策8、股东财富由其所拥有的股票数量和()两个因素所决定的。

A、持股比例B、股权结构C、股票市场价格D、股票市场规范程度三、多项选择1、以利润最大化作为公司理财目标存在的缺陷有()。

A、不能准确反映所获利润额与投入资本额的关系B、没有考虑利润发生的时间C、没有考虑货币的时间价值D、没有考虑到经营风险问题,会导致公司管理当局不顾风险大小盲目追求利润最大化E、会导致公司理财决策者的短期行为2、公司资产价值增加,生产经营能力提高,意味着公司具有持久的、强大的()。

A、发展能力B、增值能力C、获利能力D、偿债能力E、支付能力3、股东财富最大化理财目标具有的优点有()。

A、考虑了货币的时间价值B、考虑了风险价值 C 、体现了对公司资产保值增值的要求 D、克服公司经营上的短期行为 E、促使公司理财当局从长远战略进行财务决策4、公司理财的内容包括()。

A、筹资决策B、投资决策C、股利分配决策D、价格决策E、成本决策5、公司财务活动的内容包括()。

A、资金的筹集B、资金的运用C、资金的耗费D、资金的收回E、资金的分配6、公司从投资者那里筹集到的资金可以是()。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

14

(net) Working capital management

Think:

How to manage net working capital?

… …

15

(net) Working capital management

The guiding principal of net working capital:

5

the Balance Sheet (资产负债表)

Assets (资产) ====

Liabilities + Equity(负债+权益) Current liabilities(流动负债) Account Payable(应付帐款) Salary Payable(应付工资) Income Tax Payable(应交税金) Long-term debts with maturity date within one year(一年内 到期长期负债) Long-term Debts(长期负债) Note Payable(应付票据) Bond Payable(应付债券) ---------------------------------------------Shareholders’ equity(股东权益) Common Stock(普通股) Paid-In-Capital In Excess of Par (相当于资本公积金——溢价发行) Retained Earnings(保留盈余,相 当于盈余公积和未分配利润) Current Assets (流动资产) Cash and cash equivalents (现金 和银行存款) Account Receivable(应收账款) Inventory(存货) Long-term Assets(长期资产) Assets Investment(长期投资) Building, Property, plants and equipments (PPE) Intangible assets(无形资产)

10

(net) Working capital management

Liabilities: Risk –return tradeoff

The firm’s use of current versus long-term debt also involves a risk- return trade off .

17

(net) Working capital management

The use of hedging principal

1.total assets are divided into two groups: Permanent assets

An investment in an asset that the company expects to hold for the foreseeable future. Permanent investment can be made in fixed assets and the minimum level of current assets.

16

(net) Working capital management

The guiding principal of net working capital:

Principal of self-liquidating debt (Hedging principal)

This principal provides a guide to the maintenance of a level of liquidity sufficient for the company to meet its maturing obligations on time.

4

Introduction

Think:

1.What is the working capital? 2.Producing the same sales, the company need invest less working capital than other companies. What’s that mean? 3.How to manage the working capital?

3

Introduction

Case:

In 1990, American Standard Company invested over $735 million in working capital. Later, American Standard performed a strategic plan and the inventory decreased by half. By 1993, American Standard had revenues totaling $4.2 billion, and the company’s sales of $1 need invest only 5 cents working capital compared to the norm of 15 cents.

8

(net) Working capital management

Assets: Risk –return tradeoff

Generally speaking, the greater the company’s investment in current assets, the greater its liquidity. But if the investing more in cash or marketable securities, the company’s current assets earn little or no return.

6

(net) Working capital management

Working capital

The company’s total investment in current assets or assets which it expects to be converted into cash within a year or less.

Chapter 5 working capital management

1

Section 5.1 working capital and shortterm financing

2

Main content

Net working capital Risk-return trade off principal Hedging principal Short-term financing

12

(net) Working capital management

Liabilities: Risk –return tradeoff

Disadvantages of current liabilities: the risk

The use of current liabilities subject the company to a greater risk of illiquidity: Short-term debt must be repaid or rolled over often, so it maybe increase the possibility the needed funds might not be available; The other disadvantage of short-term debt is the uncertainty of interest costs from year to year.

9

(net) Working capital management

Assets: Risk –return tradeoff

Managing the company’s working capital involves a trade off between the company’s liquidity and its profitability

13

(net) Working capital management

Liabilities: Risk –return tradeoff

Remember:

Other things remaining the same, the greater the company’s reliance on short-term debt or current liabilities in financing its asset investments, the greater the risk of illiquidity.

7

(net) Working capital management

Net working capital

The difference between the company’s current assets and its current liabilities.

Notice: Frequently when the term working capital is used actually intended to mean net working capital.

20

(net) Working capital management

The use of hedging principal

In general, liquidate debt is used as temporary financing, equity and long-term debt used as Permanent financing. Spontaneous financing includes:

Principal of self-liquidating debt (Hedging principal)