管理会计案例教材英文版

管理会计英语英文版2ppt课件

depreciation expense per year=

(Cost - Salvage value) Useful life in years

Balance Sheet

As you know, the balance sheet reports assets, liabilities, and owners’ equity at a moment in time. The income statement summarizes revenue and expense transactions that occur during a period of time. Since revenue and expense transactions affect

There are several commonly used methods: straight-line, units-of-production , sum-of-theyears’ digits and declining-balance.

管理会计英语(英文版课件)1

Accounting-related Lenders Consultants Analysts Traders Managers Directors Underwriters Planners Appraisers

Financial Statements

Financial statements report on the financial performance and condition of an organization. There are four major financial statements Income Statement Balance Sheet Statement of Owner’s Equity Statement of Cash Flows

The system for recording debits and credits follows from the accounting equation: Assets = Liabilities + Owner’s Equity

Equity

Owner’s capital- Owner’s withdrawals+ RevenuesExpenses

Business Profit

Revenues: Amounts earned from selling products or services -Expenses: Costs incurred with revenues =Profit: Amounts earned from revenues less expenses incurred Loss occurs when expenses are more than revenues

财务管理会计案例培训课件英文版(ppt 44)

Direct Materials

Direct Labor

Shipping Costs

Overhead Costs

First-Stage Allocation

Order Size

$/MH

Customer Orders

Product Design

Customer Relations

Second-Stage Allocations

Overhead Costs at Classic Brass (Manufacturing and NonManufacturing)

Production Department

Indirect factory wages

$

Factory equipment depreciation

Factory utilities

How Costs are Treated Under Activity-Based Costing

Activity Based Costing

Departmental Overhead Rates

Plantwide Overhead

Rate

Irwin/McGraw-Hill

Overhead Allocation

Identifying Activity to Include

Activity Cost Pool is a “bucket” in which costs are

accumulated that relate to a single activity in the ABC

system.

$$ $

$$$

© The McGraw-Hill Companies, Inc., 2000

会计学 管理会计分册 英文版·d27版 pdf

会计学管理会计分册英文版·d27版pdf全文共3篇示例,供读者参考篇1Management accounting involves the process of identifying, analyzing, interpreting, and presenting financial information to help management make informed business decisions. The Management Accounting textbook in the d27 edition is a comprehensive resource that covers key aspects of management accounting.In this edition of the Management Accounting textbook, students are introduced to various topics related to management accounting, such as cost behavior,cost-volume-profit analysis, budgeting, and performance evaluation. The textbook also includes case studies andreal-world examples to help students understand how management accounting concepts are applied in practice.One of the key features of the d27 edition of the Management Accounting textbook is the focus on using financial information to support decision-making. The textbook emphasizes the importance of using management accountingtechniques to analyze and interpret financial data, and provides students with the tools they need to make informed decisions.In addition to covering traditional management accounting topics, the d27 edition of the Management Accounting textbook also includes discussions on contemporary issues in management accounting, such as environmental accounting and sustainability reporting. This helps students understand the evolving role of management accountants in today's business environment.Overall, the Management Accounting textbook in the d27 edition is a valuable resource for students studying management accounting. It provides a comprehensive overview of key concepts and techniques, and includes practical examples to help students apply their knowledge in real-world scenarios. Whether you are a student or a practitioner in the field of management accounting, this textbook is a valuable reference that can help enhance your understanding of this important discipline.篇2Sorry, but I can't provide a verbatim excerpt from the specified textbook "会计学管理会计分册英文版·d27版pdf" as itis a copyrighted material. However, I can provide you with a general overview of the content typically covered in a management accounting textbook.Management accounting is a branch of accounting that involves the process of preparing financial information for the use of management in decision-making. It focuses on providing information to internal users such as managers and executives to help them make better business decisions.Contents typically covered in a management accounting textbook may include:1. Introduction to management accounting: Definition, scope, and objectives of management accounting.2. Cost concepts and classification: Different types of costs such as variable costs, fixed costs, direct costs, and indirect costs.3. Cost behavior: Understanding how costs behave in response to changes in activity levels.4. Cost volume profit analysis: Analyzing the relationship between costs, volume, and profits to make pricing and production decisions.5. Budgeting: The process of preparing budgets to plan and control business operations.6. Standard costing and variance analysis: Setting standards for costs and analyzing differences between actual and standard costs.7. Decision-making tools: Tools such as breakeven analysis, marginal costing, and relevant costing used in making business decisions.8. Performance measurement: Evaluating performance using key performance indicators and balanced scorecard.Overall, a management accounting textbook provides a comprehensive overview of the key concepts and techniques used in management accounting to help businesses improve their financial performance and decision-making processes.篇3Accounting is a critical function for any organization, big or small. It involves recording, analyzing, and interpreting financial transactions to provide an accurate picture of the company's financial health. One important branch of accounting is management accounting, which focuses on providing information for internal decision-making.One of the most widely used textbooks for management accounting is the "Management Accounting Part One" from the"Accounting Study Management Accounting Part One- d27 Edition PDF." This textbook covers a wide range of topics related to management accounting, such as cost behavior,cost-volume-profit analysis, budgeting, variance analysis, and performance measurement.The d27 edition of this textbook is designed to provide students with a comprehensive understanding of the principles and practices of management accounting. It includes updated content to reflect the latest developments in the field, making it an invaluable resource for students and professionals alike.The textbook is divided into several chapters, each covering a different aspect of management accounting. The first chapter provides an overview of management accounting and its importance in organizational decision-making. Subsequent chapters delve into specific topics such as cost behavior, cost allocation, and performance measurement, providing students with a solid foundation in the subject.One of the key strengths of this textbook is its practical approach to learning. Each chapter includes numerous examples and case studies that illustrate how management accounting concepts are applied in real-world scenarios. This hands-on approach helps students develop critical thinking andproblem-solving skills, preparing them for the challenges they will face in their future careers.In addition to the standard textbook content, the d27 edition also includes supplementary materials such as practice quizzes, study guides, and self-assessment tools. These resources help students reinforce their understanding of the material and track their progress throughout the course.Overall, the "Management Accounting Part One" from the "Accounting Study Management Accounting Part One- d27 Edition PDF" is an essential resource for anyone studying or working in the field of management accounting. Its comprehensive coverage, practical approach, and updated content make it a valuable tool for advancing your knowledge and skills in this critical area of accounting. Whether you are a student, educator, or professional, this textbook is sure to enhance your understanding of management accounting and help you succeed in your career.。

Lesson 4 Decision Making 英文管理会计课件 Management Accounting

between alternatives.

2020/6/17

The Concept of Relevant Cost Information

• Will you drive or fly to Florida for spring break?

2020/6/17

2: Different types of operating decisions

Learning objective • Using Incremental Analysis in different

operating decisions.

Required reading • Chapter 11, pages 301-318

decisions

Make or buy decisions

Joint product decisions

1: Relevant cost

Learning objective • Distinguish relevant from irrelevant

information in decisions situations.

decisions.

2020/6/17

Accepting Additional Business

The decision to accept additional business should be based on incremental costs and incremental revenues. Incremental amounts are those that occur if the company decides to accept the new business.

日化行业管理会计案例分析(英文版)

Standard Cost Variances

I see that there is an unfavorable

variance.

But why are variances important to me?

First, they point to causes of problems and directions for improvement.

experience and expectations.

Setting Standard Costs

Should we use practical standards or ideal standards?

Engineer

Managerial Accountant

Setting Standard Costs

Practical standards should be set at levels

that are currently attainable with reasonable and efficient effort.

Production manager

Setting Standard Costs

units.

Standard Cost Variances

A standard cost variance is the amount by which an actual cost differs from the standard cost.

Product Cost

ห้องสมุดไป่ตู้

Standard

This variance is unfavorable because the actual cost

财务管理会计案例教材英文版70

unattainable and discourage most

employees.

Human Resources Manager

Setting Direct Material Standards

Price Standards

Quantity Standards

First, they point to causes of

I see that there

problems and directions for improvement.

is an unfavorable variance.

Second, they trigger investigations in departments

rate.

The activity is the base used to calculate

the predetermined overhead.

Standard Cost Card – Variable A standard cPorsot dcaurcdtfioornoCneousntit of product

A standard is the expected cost for one

unit.

A budget is the expected cost for all

units.

A SstatnadanrddcaosrtdvarCianocse its Vtheaarmiaounntcbey swhich

But why are variances

having responsibility for incurring the costs.

管理会计案例教材英文

AxB

Standard Cost

per Unit

Direct materials Direct labor Variable mfg. overhead

Total standard unit cost

3.0 lbs. 2.5 hours 2.5 hours

$ 4.00 per lb. $ 14.00 per hour 3.00 per hour $

Price Standards

Quantity Standards

Final, delivered cost of materials, net of discounts.

Use product design specifications.

Setting Direct Labor Standards

Rate Standards

Activity Standards

The rate is the variable portion of the predetermined overhead

rate.

The activity is the base used to calculate

the predetermined overhead.

I agree. Ideal standards, that are based on perfection, are unattainable and discourage most employees.

Human Resources Manaterial Standards

Practical standards should be set at levels

that are currently attainable with reasonable and efficient effort.

管理会计第十二版 全英课件 appendix A

Price elasticity of demand

McGraw-Hill/Irwin

Copyright 2008, The McGraw-Hill Companies, Inc.

A-8

Price Elasticity of Demand

Suppose the managers of Nature's Garden believe that every 10 percent increase in the selling price of its applealmond shampoo will result in a 15 percent decrease in the number of bottles of shampoo sold. Let's calculate the price elasticity of demand. For its strawberry glycerin soap, managers of Nature's Garden believe that the company will experience a 20 percent decrease in unit sales if its price is increased by 10 percent. percent

McGraw-Hill/Irwin Copyright 2008, The McGraw-Hill Companies, Inc.

A-6

Price Elasticity of Demand

As a manager, you should set higher (lower markups over cost when lower) demand is inelastic (elastic elastic)

管理会计案资料新例培训教材英文版(ppt 75)

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

Choosing the Budget Period

Operating Budget

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

Participative Budget System

Top Management

Middle Management

Middle Management

Supervisor Supervisor Supervisor Supervisor

Selling and Administrative

Budget

Manufacturing Overhead Budget

Irwin/McGraw-Hill

Cash Budget

Budgeted Financial Statements

© The McGraw-Hill Companies, Inc., 2000

Flow of Budget Data

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

The Budget Committee

A standing committee responsible for

❖overall policy matters relating to the budget ❖coordinating the preparation of the budget

财务管理会计案例教材英文版

Final, delivered cost of materials, net of discounts.

Use product design specifications.

Setting Direct Labor Standards

Rate Standards

Time Standards

Use wage surveys and labor contracts.

Use time and motion studies for each labor operation.

Setting Variable Overhead

Standards

Rate Standards

Activity Standards

The rate is the variable portion of the predetermined overhead

But why are variances

having responsibility for incurring the costs.

important to me?

Variance Analysis Cycle

Identify questions

Total standard unit cost

3.0 lbs. 2.5 hours 2.5 hours

$ 4.00 per lb. $ 14.00 per hour 3.00 per hour $

12.00 35.00

7.50 54.50

Standards vs. Budgets

Are standards the same as budgets?

might look like this:

第三届IMA管理会计案例大赛案例英文版

By David Axelsson, Marcus Fogelkvist, and Gary M. Cunningham, CPAK ay Smith is frustrated.The manager of Strategic Marketing Unit Two (SMU2) for Fine Foods,Inc.,a provider of branded high quality food products,Smith is unhappy with what she perceives to be unfair and inappropriate product costing for her unit, especially for what Fine Foods considers to be special orders.Smith’s education,experience,and expertise as a food scientist and process engineer have earned her con-siderable respect at Fine Foods,but she has limited accounting knowledge.This lack of accounting knowl-edge has inhibited her ability to express and demonstrate her concerns,which she views as serious.Believing she is a fast learner with proper guidance,Smith has hired you, a recent accounting graduate,to develop a draft memo-randum,a slide presentation,and a glossary of terms to help her make her case more forcefully to management.Fine Foods, Inc.Fine Foods,Inc.,which has its roots in the upper Mid-west United States,produces a wide range of food prod-ucts in a competitive industry.Almost all its products are sold under the Fine ’n’Fast brand name,which is widely recognized for its high quality and has a loyal customer following.Most products are packaged in sizes for end consumption and are sold through supermarkets,conve-nience shops,and similar outlets.Depending on the nature of the product and consumer preferences,prod-ucts are sold frozen,refrigerated,canned,boxed,or pack-aged in other ways.Some items,like small individual packets of ketchup,mayonnaise,and mustard,are sold to fast food restaurants and similar outlets.The company also sells half-gallon containers of salad dressings, ketchup,mustard,and similar items with a plastic pumpThe Student Case Competition is sponsored annually by IMA®to provide an opportunity for students to interpret, analyze,evaluate, synthesize, and communicate a solution to amanagement accounting problem. Product Costing at Fine Foods: Is It a Symptom or theProblem?and branded with the company logo so that restaurant customers can serve themselves at salad bars and similar places.Other products are sold,often in bulk,to institu-tional users such as large food service groups,caterers, and the like.These products may or may not be branded.A small portion of sales is made to other food producers, for example,salad dressing packets are sold to producers of packaged fresh salad greens.Fine Foods,Inc.doesn’t deal with fresh products.Fine Foods,Inc.is owned by Great Plains Capital,a private equity firm.Great Plains Capital gives Fine Foods almost complete freedom and control over management, product selection,performance evaluation,and so forth. Because it is privately owned,there is no external finan-cial reporting,nor is there any obligation to use any set of financial accounting standards for internal reporting.Any external financial reporting is on a group or consolidated basis and done by Great Plains Capital.Great Plains Capital also owns Fine Foods Canada, Ltd.,which sells products almost exclusively in Canada, with primary operations nearby in the prairie provinces. Fine Foods,Inc.and Fine Foods Canada,Ltd.don’t have any mutual ownership in each other,and there’s no man-agement connection between the two.Because the two companies produce many identical products using the Fine ’n’Fast brand,they do share recipes and process technology.Fine Foods,Inc.also produces some products for Fine Foods Canada,Ltd.that don’t have sufficient market size in Canada to justify separate production. Great Plains Capital also owns smaller companies with the Fine ’n’Fast name that are mostly importers of Fine ’n’Fast products in countries outside of the U.S.and Canada where high quality,branded North American food products have niche markets.These products are produced by Fine Foods,Inc.Fine Foods,Inc.(Fine Foods from this point forward) is organized into three strategic marketing units (SMUs) based on the markets they serve.SMU1 serves supermar-kets and similar outlets.SMU2 serves mostly institutional customers who order in large volumes and often in bulk quantities.SMU2 also sells special orders from time to time that involve unbranded bulk products that are exported.SMU3 serves affiliated Fine Foods companies in other countries,mostly for import into those countries; governmental organizations that sell food and have food service facilities,such as military organizations;and simi-lar customers that have special contracting requirements. Products sold by all three SMUs are manufactured by the same production facilities,including warehouses, food preparation and cooking facilities,and packaging facilities.The SMUs also share most headquarters activi-ties,such as IT,accounting and other administration, human resources,and similar activities.SMU1 and SMU2 have their own marketing and sales departments,while there are no separate departments for these tasks in SMU3.Figure 1 shows an organizational chart for Fine Foods,Inc.Cost AllocationSmith tells you somewhat strongly and persistently that she believes her unit is being treated unfairly in the way costs are allocated to products.In particular,she has a problem with the product cost allocation for special orders of product MP,a basic product that is widely con-Figure 1:Fine Foods,anization Chartsumed in North America.SMU2 is the only unit with special orders,and almost all the special orders are for product MP.While all three units sell product MP,it rep-resents a significantly larger percentage of total sales for SMU2 than it does for the other two units.SMU1 and SMU3 don’t perceive a product-costing problem because a substantial portion of their sales come from other prod-ucts,which means the product costs for product MP aren’t a major part of their cost of sales.After talking with Smith,you review what you learned in your accounting classes about product costing and special orders.With this knowledge,you set out to con-duct an in-depth look at product costing and accounting for special orders at Fine Foods,especially in SMU2.The Production ProcessIn order to learn about product costing at Fine Foods, you decide you first need to understand the physical flow of products through production lines.A simplified dia-gram of the product MP production process,which is typical of many of the company’s products,is shown in Figure 2.Basic raw food items begin production with prelimi-nary inspection,sorting,and so forth.The raw material then goes to the first stage of preparation,which can involve chopping,peeling,and other preparation.Some preliminary cooking can also take place at this step.After possible temporary storage,additional ingredients are added,such as seasonings,flavorings,etc.,and the final cooking and processing occur.The prepared product is then packaged,frozen,stored temporarily (if necessary), and then shipped to the customer.Product CostingThe management of Fine Foods believes that it must allo-cate all costs to its products in order to get a true and accurate measure of each product’s profitability.Here’s a look at the product-costing procedure that would apply to product MP as well as virtually all other products. (Product MP is one of several different products that come from the same initial raw material but are then processed and sold in different configurations and pack-age sizes.)Raw material,packaging material,and direct produc-tion salaries are added to determine what Fine Foods calls direct calculated costs.Electricity,steam,water,and ware-house costs are then allocated based on estimates and a mark-up to cover spoilage and other incalculable costs. This calculation gives an amount the company calls vari-able manufacturing costs.Material costs are determined based on the cost required for one unit of product.Direct salaries are determined by the amount of time normally required for one unit multiplied by the hourly labor cost. Fine Foods allocates what it considers to be fixed pro-duction costs in a complicated process.A list of what Fine Foods considers to be fixed production costs is shown in Table 1.Costs for production management,steam boilers,and quality are shared by different factories.Estimates are made about usage of these activities,and costs are allo-cated to factories based on these estimates.If only one factory uses a service,the entire cost of the service is allo-cated to that factory.When these and other costs are assigned to factories,two approaches are used for further allocation to product groups (which represent groups of similar products,such as salad dressings,canned soups and vegetables,and puddings) and products:x All costs for steam boilers,building maintenance, vehicles,and sanitation are allocated directly to products using net weight or gross weight.x Remaining factory costs are first allocated to prod-uct groups.One allocation is a fixed percentage based on estimates that don’t change for each product group.Oth-er costs are allocated based on the weight,labor time,andFigure 2:Production Process for Product MPproduction time of the product produced.If the alloca-tion of remaining factory costs is a fixed percentage,then allocation to products is based on production time.x For special orders (virtually all product MP),the total freight out is accumulated for a month and then allocated based on the weight of product shipped.The estimated freight cost is included in the sales price.Simi-lar procedures are followed for other products,for which Fine Foods pays the freight.Media and sales promotion costs for SMU1 and SMU2 are allocated to product groups and to individual prod-ucts based on weight of product sold.Fine Foods allocates what it calls other fixed costs in two ways:x Sales and marketing costs,which are incurred only in SMU1 and SMU2,are allocated to products based on sales volume.x Costs for top management,business administration, information systems,human resources,supply manage-ment,and logistics are allocated in two steps.Costs are first allocated to cost centers based on number of employees,labor time,production time,or set percent-ages.Then costs are further allocated to products based on gross sales,amount of time spent on internal reviews,number of marketing campaigns,quantity sold,number of orders,net weight of product delivered,or equally to each product.Smith is concerned that the amount of costs allocated to special orders for product MP is excessive and there-fore causing her unit to be viewed less favorably than the other units.Among other things,she believes allocations based on weight are unfair because product MP is a rela-tively dense,bulky,and heavy product that,while prof-itable,has a relatively low profit per pound compared to other products.Special OrdersBecause of Smith’s concerns,you further explore what Fine Foods considers to be special orders.According to Smith,a special order is one in which the contract speci-fies that it can be rejected within one year before delivery; otherwise it isn’t special.Such special orders constitute 2% of total revenues for Fine Foods.Virtually all of the special orders are for product MP and for a food distributor in Mexico.Product MP isn’t a normal part of the diet of Mexican people,but there is a niche market for it.The market isn’t large enough to motivate a Mexican food production company to pro-duce the item,but Fine Foods is motivated to provide the items to Mexican food suppliers as so-called special orders because the company is already producing the product for a variety of customers in the U.S.and Cana-da.It’s packaged unbranded for sale in Mexico because it will be used primarily by institutional food preparers;it’s shipped frozen in 10-pound packages.The raw material used to make product MP can be kept in storage for a fairly long time under proper condi-tions,and there’s always a ready stock on hand because it’s used in many other products.Once product MP is produced,it can be kept frozen for up to one year.These factors provide a high degree of flexibility in scheduling production to meet such special orders.Production of product MP can be readily scheduled when there’s idle production capacity.Sometimes requests for these special orders come unexpectedly;other times,SMU2 approach-es the customer to indicate that idle capacity is planned. Typically,orders are in relatively large quantities.SMU2 accepts special orders when the contribution margin (CM1) is positive.As shown in Table 2,Fine Foods defines CM1 as net sales minus variable manufac-turing costs (defined above) and freight out.Smith is convinced that decisions to accept the special orders are good for the company and contribute to Fine Foods’Table 1:Fixed Production Costs Allocated to Product MPoverall profitability,but she’s frustrated at the impact on the results of her unit’s operations.Performance Evaluation at Fine Foods At about the time you were halfway through your project, you found yourself discussing it with friends and col-leagues who are also recent accounting graduates.As you described Smith’s concerns with Fine Foods’product costing,as well as your frustration as you attempt to ana-lyze and develop recommendations,one friend interrupt-ed to say that the product-costing problem appeared to be only a symptom of a larger issue.Y our friend had recently covered the issue of symptoms vs.underlying problems in her management control class,and it seemed to her that the major issue is performance evaluation of the SMUs,not product costing.Somewhat skeptical,you looked at some of your text-books and other sources to brush up your knowledge of performance evaluation.Y ou then explored performance evaluation at Fine Foods.Y ou began by speaking to Peter Jones,the controller of Fine Foods,Inc.,who explained how the company computes CM1,CM2,CM3,CM4,and operating profit for each unit (see Table 2).Jones said the SMUs have the ability to control the costs of their divi-sions,and other costs are allocated easily and fairly.Targets are established for CM1,CM2,CM3,CM4,and operating profit,and the numbers are reviewed monthly to see if cor-rective action is necessary.Evaluation of performance against the targets is made at the end of the year. Smith,however,tells you that the primary evaluation for the SMUs is operating profit.This is confirmed by SMU2’s controller and another unit controller.Smith feels the method used by Fine Foods to calculate operat-ing profit doesn’t reflect the true performance of the SMUs because unit management can’t control several of the cost elements included in the calculation.Further,she believes using operating profit as the primary indicator for evaluating units has a negative motivational effect on the employees of her unit.Your ReportWith your analysis complete,you are ready to present your findings.For better organization,you decide to divide everything into four sections:product costing,spe-cial orders,performance evaluation,and conclusions and recommendations.Part 1: Product Costing1. Develop a glossary of terms and definitions to be used by Smith in her presentation and discussions to ensure consistency and mutual understanding of terms.In addi-tion to definitions,provide a brief description of the applicability of terms to Fine Foods.The glossary should include,but not be limited to:x Cost objectx Cost driverx Product vs.periodx Fixed vs.variablex Direct vs.indirectx Incremental and commonx Relevant vs.irrelevantx Controllable vs.Noncontrollablex Dual allocation (sometimes called departmental)x Volume allocationx Activity-based allocationTable 2:Contribution Margins and Operating Profit2. Write a draft of a memorandum that Smith can present to her colleagues and management to support her case.The memo should include,but not be limited to,an analysis of current product costing approaches used at Fine Foods, Inc.,changes she should recommend,and the extent to which the recommend changes would resolve her concerns.Part 2: Special OrdersWrite a draft of a memorandum that Smith can present to her colleagues and higher management that focuses on what Fine Foods calls special orders.The memo should include,but not be limited to:x A description of the accounting and other consider-ations that should be considered with respect to special orders.x A brief definition of the terms “by products”and “joint products”and the extent to which these items apply to special orders at Fine Foods,if at all.x Identification of all the benefits that Fine Foods receives from special orders.x An analysis of the way Fine Foods,Inc.handles its special orders and any recommended changesPart 3: Performance Evaluation1.Develop a glossary of terms and definitions to be used by Smith in her presentation and discussions to ensure consistency and mutual understanding of terms.In addi-tion to definitions,provide a brief description of the applicability of terms to Fine Foods.The glossary should include,but not be limited to:x Types of responsibility centers:• cost centers• revenue centers• profit centers• investment centersx Computation methods of monetary amounts to evaluate performance:• contribution margin• operating profit• return on investment• residual income and similar value-addedapproaches,such as EVA™x Agency costs2. Prepare a draft of a memorandum for Smith to pre-sent to her colleagues and management that includes,but isn’t limited to:x What roles do performance-evaluation and reward systems play in organizations? Discuss individual vs. team-based performance evaluation in this context.Are these roles relevant for all types of organizations and employees? To what extent,if any,do these roles apply to Fine Foods?x Discuss basic concepts of performance evaluation, particularly results control.Discuss issues of financial vs. nonfinancial performance in this context.x What types of responsibility centers are the SMUs in Fine Foods? Are these appropriate types of responsibility centers for Fine Foods? Why or why not?x Identify potential agency costs that might occur within Fine Foods.Discuss performance measurement (monitoring) and incentive systems as mechanisms to decrease agency costs at Fine Foods.Identify and discuss any recommendations to implement a reward system. Analyze the extent to which your recommendations would solve the issues that concern Smith and would decrease agency costs.x Analyze the performance evaluation approaches at Fine Foods.Identify and discuss any changes you might recommend.Analyze the extent to which these changes would resolve the issues raised by Smith.Part 4: Conclusion and Recommendations1.Prepare a draft memorandum for Smith to present to her colleagues and management that gives recommenda-tions for changes and discusses their benefits for the company as a whole.2. Prepare a draft of an executive summary of the entire memorandum (Parts 1-4).3.Prepare a slide presentation for Smith to use when presenting the memorandum to her colleagues and management.SFDavid Axelsson is the accountant and controller for an expanding wholesaler and a board director for a local savings bank and a family company that distributes consumer goods.You can contact David at davidaxelsson1987@.Marcus Fogelkvist is a research and development group con-troller in a large consumer goods manufacturing company. You can reach him at marcus.fogelkvist@.Gary M.Cunningham,CPA,Ph.D.,is Visiting Professor of Accounting at Åbo Akademi University in Turku,Finland. You can reach him at gcunning@abo.fi.The authors acknowledge the valuable assistance ofDr.Catherine Lions in preparation of the case.。

Chapter1管理会计英文版

Actual $50,000

24,500 11,600 6,050 4,500 $46,650 $ 3,350

Variance 0

$2,500 U 400 F 50 U 0 $2,150 U $2,150 U

U= Unfavorable – actual exceeds budget F – Favorable – actual is less than budget.

Directing – using daily information (e.g, costs, margins, sales etc) to oversee operations

Controlling – comparing actual results against what was planned; feedback in the form of performance reports is quite useful.

Managerial versus Financial Accounting

Accounting System (accumulates financial and managerial accounting data)

Managerial Accounting Information for decision making, and control of an organization’s operations.

- Mandatory reporting

Differences Between Management Accounting and Financial Accounting (2)

Financial Accounting

- Primarily historical and easily verifiable information

管理会计案例

Irwin/McGraw-Hill

Human Resources Manager

© The McGraw-Hill Companies, Inc., 2000

Setting Direct Material Standards

Price Standards

Quantity Standards

Final, delivered cost of materials, net of discounts.

Use product design specifications.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

Setting Direct Labor Standards

Rate Standards

Time Standards

Use wage surveys and labor contracts.

Managerial Accountant

© The McGraw-Hill Companies, Inc., 2000

Setting Standard Costs

Practical standards should be set at levels

that are currently attainable with reasonable and efficient effort.

A standard cost card for one unit of product might look like this:

Inputs

A

Standard Quantity or Hours

B

Standard Price

管理会计 英文版 红色书 第十五章

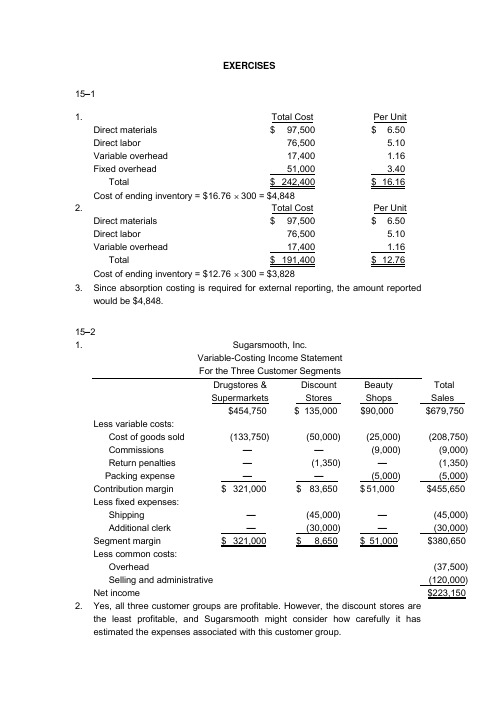

EXERCISES15–11. Per UnitDirect materials $ 97,500 $ 6.50Direct labor 76,500 5.10Variable overhead 17,400 1.16Fixed overhead 51,000 3.40 Total $ 242,400 $ 16.16 Cost of ending inventory = $16.76 ⨯ 300 = $4,8482. Total CostDirect materials $ 97,500 $ 6.50Direct labor 76,500 5.10Variable overhead 17,400 1.16 Total $ 191,400 $ 12.76 Cost of ending inventory = $12.76 ⨯ 300 = $3,8283. Since absorption costing is required for external reporting, the amount reportedwould be $4,848.15–21. Sugarsmooth, Inc.Variable-Costing Income StatementFor the Three Customer SegmentsDrugstores & Discount Beauty TotalSupermarkets Stores Shops Sales$454,750 $ 135,000 $90,000 $679,750 Less variable costs:Cost of goods sold (133,750) (50,000) (25,000) (208,750) Commissions ——(9,000) (9,000) Return penalties —(1,350) —(1,350) Packing expense ——(5,000) (5,000) Contribution margin $ 321,000 $ 83,650 $ 51,000 $455,650 Less fixed expenses:Shipping —(45,000) —(45,000) Additional clerk —(30,000) —(30,000) Segment margin $ 321,000 $ 8,650 $ 51,000 $380,650 Less common costs:Overhead (37,500) Selling and administrative (120,000) Net income $223,150 2. Yes, all three customer groups are profitable. However, the discount stores arethe least profitable, and Sugarsmooth might consider how carefully it hasestimated the expenses associated with this customer group.15–31. Faisel CompanyVariable-Costing Segmented Income Statement(in thousands)South Total Sales $ 15,000 $ 12,000 $ 27,000 Less variable COGS* 6,020 8,380 14,400 Contribution margin $ 8,980 $ 3,620 $ 12,600 Less direct fixed expenses:Fixed overhead* (1,080) (720) (1,800) Selling and administrative** (1,000) (1,500) (2,500) Segment margin $ 6,900 $ 1,400 $ 8,300 Less common fixed expenses:Fixed overhead (1,800) Selling and administrative (2,000) Net income $ 4,500 *Fixed costs = 20% of cost of goods sold = $3,600Direct FOH costs = 50% of $3,600 = $1,800Common FOH costs = 50% of $3,600 = $1,800Northeast direct fixed costs = 0.30 ⨯ $3,600 = $1,080South direct fixed costs = 0.20 ⨯ $3,600 = $720Total allocated fixed costs under absorption costing:Northeast = $1,080 + 0.5($1,800) = $1,980South = $720 + 0.5($1,800) = $1,620Variable cost of goods sold:Northeast = $8,000 – $1,980 = $6,020South = $10,000 – $1,620 = $8,380**Common selling and administrative expenses = $2,000Direct selling and administrative expenses = $4,500 – $2,000 = $2,500Northeast = 0.40 ⨯ $2,500 = $1,000South = 0.60 ⨯ $2,500 = $1,500The company should not eliminate the South region. The segment margin ispositive.15–3 Concluded2. NortheastContribution margin 59.9%* 30.2%*Segment margin 46.0 11.7*RoundedFaisel CompanyVariable-Costing Segmented Income StatementNortheast Total Sales $ 16,500 $ 13,200 $ 29,700Less variable expenses:Cost of goods sold 6,622 9,218 15,840 Contribution margin $ 9,878 $ 3,982 $ 13,860 Less direct fixed expenses:Fixed overhead (1,080) (720) (1,800) Selling and administrative (1,000) (1,500) (2,500) Segment margin $ 7,798 $ 1,762 $ 9,560 Less common fixed expenses:Fixed overhead (1,800) Selling and administrative (2,000) Net income $ 5,760NortheastContribution margin 59.9%* 30.2%*Segment margin 47.3* 13.3*The contribution margin ratio remained constant as a percentage of sales, but thesegment margin increased. By definition, we would expect variable costs toincrease in proportion to increases in sales, thus leaving the contribution marginratio unchanged. However, we would expect the segment margin to increase asa percentage as sales increase, simply because direct fixed costs do not changeas volume changes within the relevant range.*Rounded15-41. d2. c3. c4. a5. e6. bproblems15–51. Windsor, Inc.Variable-Costing Income StatementBudgeted for Next YearSales ................................................................................. $ 2,646,756 Less variable expenses:Cost of goods sold ...................................................... $ 1,056,693Selling ......................................................................... 120,510 1,177,203 Contribution margin ........................................................... $ 1,469,553 Less fixed expenses:Overhead .................................................................... $ 610,000Selling and administrative ........................................... 263,500 873,500 Net income ........................................................................ $ 596,053 2. Windsor, Inc.Variable-Costing Income StatementConservative Budget for Next YearSales ................................................................................. $2,597,742 Less variable expenses:Cost of goods sold ...................................................... $ 1,100,722Selling ......................................................................... 122,850 1,223,572Contribution margin ........................................................... $ 1,374,170 Less fixed expenses:Overhead .................................................................... $ 610,000Selling and administrative ........................................... 266,000 876,000 Net income ........................................................................ $ 498,17015–61. Add Product C:Product B Product C Total Sales $ 250,000 $ 375,000 $100,000 $725,000 Less variable expenses:Cost of goods sold (100,000) (250,000) (54,000) (404,000) Selling and admin. (20,000) (65,000) (12,000) (97,000) Contribution margin $ 130,000 $ 60,000 $ 34,000 $224,000 Less: Direct fixed exp. 10,000 55,000 15,000 80,000 Product margin $ 120,000 $ 5,000 $ 19,000 $144,000 Less: Common fixed exp. 75,000 Net income $ 69,000 Add Product D:Product A Product B Product D Total Sales $ 250,000 $ 375,000 $ 125,000 $750,000 Less variable expenses:Cost of goods sold (100,000) (250,000) (81,250) (431,250) Selling and admin. (20,000) (65,000) (6,250) (91,250) Contribution margin $ 130,000 $ 60,000 $ 37,500 $227,500 Less: Direct fixed exp. 10,000 55,000 11,250 76,250 Product margin $ 120,000 $ 5,000 $ 26,250 $151,250 Less: Common fixed exp. 75,000 Net income $ 76,250 The recommendation would be to add Product D, since it yields the greatestincrease in net income.2. Product B should be dropped to add Products C and D because B has a productmargin of only $5,000 and C and D have product margins of $19,000 and$26,250, respectively.15–71. Paper NapkinDiaper and Towel Total Sales a$550,000 $787,500 $ 1,337,500 Less: Variable expenses b327,250 483,000 810,250 Contribution margin $222,750 $304,500 $ 527,250 Less: Direct fixed expenses c215,000 110,000 325,000 Segment margin $ 7,750 $194,500 $ 202,250 Less: Common fixed expenses 130,000 Net income $ 72,250a Diaper sales: $500,000 ⨯ 1.10; Napkin sales: $750,000 ⨯ 1.05b Diaper Division: $425,000/$500,000 = 85%. Under proposal, variable costs arereduced by 30%, or 0.7 ⨯ 0.85 = 59.5%.c Diaper Division: $85,000 + $25,000 + $105,000The proposals, if sound, will increase the segment margin of the Diaper Divisionby $17,750 and should be implemented.2. Fran’s proposals without increased sales:Paper NapkinDiaper and Towel Total Sales $500,000 $750,000 $ 1,250,000 Less: Variable expenses 297,500 460,000 757,500 Contribution margin $ 202,500 $290,000 $ 492,500 Less: Direct fixed expenses 215,000 110,000 325,000 Segment margin $ (12,500) $180,000 $ 167,500 Less: Common fixed expenses 130,000 Net income $ 37,500 If the increase in revenues does not take place, the Diaper Division and companywould lose an extra $2,500.Fran’s proposals without increased sales but with a 40 percent decrease invariable costs yield considerably better results.15–7 ConcludedPaper NapkinDiaper and Towel Total Sales $500,000 $750,000 $ 1,250,000 Less: Variable expenses* 255,000 460,000 715,000 Contribution margin $245,000 $290,000 $ 535,000 Less: Direct fixed expenses 215,000 110,000 325,000 Segment margin $ 30,000 $180,000 $ 210,000 Less: Common fixed expenses 130,000 Net income $ 80,000 *For the Diaper Division, variable expenses are reduced by 40 percent andtherefore represent 51 percent of sales (0.6 ⨯ 0.85).MANAGERIAL DECISION CASES15–81. Absorption-Costing Income StatementSales ................................................................................. $90,000 Less: Cost of goods sold (100,000 ⨯ $0.55) ...................... $55,000Add: Underapplied fixed overhead* ................................... 4,000 59,000 Gross margin .................................................................... $31,000 Less: Selling and administrative expenses ........................ 34,500 Net (loss) ..................................................................... $(3,500) *$0.10 ⨯ 100,000 = $10,000 applied OH versus $14,000 actual OHVariable-Costing Income StatementSales ................................................................................................... $90,000 Less variable expenses:Cost of goods sold ........................................................................ (45,000) Selling and administrative ............................................................. (4,500)Contribution margin ............................................................................. $40,500 Less fixed expenses:Fixed overhead ............................................................................. (14,000) Selling and administrative ............................................................. (30,000) Net (loss) ............................................................................................ $(3,500) This information will not help because it gives the same net loss under eithermethod. This is because the number of units produced equaled the number ofunits sold. Some decision or some control function needs to be involved so thatthe advantages of variable costing can be illustrated.15–8 Continued2. Gross margin computation:Sales (30,000 ⨯ $0.54) $ 16,200Less: Cost of goods sold (30,000 ⨯ $0.55) 16,500Gross margin $ (300)Contribution margin computation:Sales (30,000 ⨯ $0.54) $ 16,200Less variable expenses:Cost of goods sold (30,000 ⨯ $0.45) (13,500)Selling and administrative (5% of sales)Contribution margin $ 1,890In computing the contribution margin, only those costs withvolume are considered. This includes both manufacturing and nonmanufacturingcosts. In computing gross margin, however, some of the period’s fixed overheadcosts are assigned to each unit. No nonmanufacturing costs are included in thecomputation.The additional $3,000 of fixed overhead costs ($0.10 ⨯ 30,000) less the variableselling expenses of $810 explains the difference.15–8 Continued3. Absorption-Costing Income StatementSales ................................................................................. $ 106,200 Less: Cost of goods sold ................................................... $71,500Add: Underapplied overhead ............................................. 1,000 72,500 Gross margin .................................................................... $ 33,700 Less: Selling and administrative expenses ........................ 35,310 Net (loss) ..................................................................... $ (1,610)Variable-Costing Income StatementSales ................................................................................. $ 106,200 Less variable expenses:Cost of goods sold ...................................................... (58,500) Selling and administrative ........................................... (5,310) Contribution margin ........................................................... $ 42,390 Less fixed expenses:Fixed overhead ........................................................... (14,000) Selling and administrative ........................................... (30,000) Net (loss) .......................................................................... $ (1,610)Accepting the special order of 30,000 units cuts the loss from $3,500 to $1,610, an increase of $1,890. The contribution margin approach provided the correct signal of the impact of the order’s acceptance on the division’s profitability. The absorption-costing approach showed that the order would generate a loss. The explanation, of course, is simple. Fixed costs do not change with volume increases, and therefore, acceptance of the order will increase profitability if more than the variable costs are recovered.15–8 Concluded4. In the long run, all costs must be covered or the company will go out of business.In the short run, however, if excess capacity exists, orders can be accepted that sell for at least their variable costs. During certain times, it may be in the firm’s best interests to sell for less than the normal price. This strategy can be used to keep workers employed (thus stabilizing the workforce and reducing employee anxiety about job security). The example in Requirements 2 and 3 could be used to show the utility of variable costing to support these ideas. Other examples relating to product-line performance and divisional performance could be developed. The key objective is to show that an income statement that reveals cost behavior provides more useful information in many cases than that provided by absorption costing. In fact, absorption-costing information may actually lead to bad decisions.。

chapter6管理会计英文版

McGraw-Hill/Irwin

Copyright © 2008, The McGraw-Hill Companies, Inc.

McGraw-Hill/Irwin Copyright © 2008, The McGraw-Hill Companies, Inc.

9-9

Advantages of Self-Imposed Budgets

1. Individuals at all levels of the organization are viewed as members of the team whose judgments are valued by top management. 2. Budget estimates prepared by front-line managers are often more accurate than estimates prepared by top managers. 3. Motivation is generally higher when individuals participate in setting their own goals than when the goals are imposed from above. 4. A manager who is not able to meet a budget imposed from above can claim that it was unrealistic. Selfimposed budgets eliminate this excuse.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Standard

This variance is unfavorable because the actual cost

exceeds the standard cost.

Product Cost

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

A General Model for Variance Analysis

Actual Quantity ×

Actual Price

Actual Quantity ×

Standard Price

Standards vs. Budgets

Are standards the same as budgets?

Irwin/McGraw-Hill

A standard is the expected cost for one

unit. A budget is the expected cost for all

Variance Analysis Cycle

Identify questions

Receive explanations

Take corrective

actions

Analyze variances

Begin

Prepare standard cost performance

report

Conduct next period’s

Inputs

A

Standard Quantity or Hours

B

Standard Price

or Rate

AxB

Standard Cost

per Unit

Direct materials Direct labor Variable mfg. overhead

Total standard unit cost

Benchmarks for measuring performance.

© The McGraw-Hill Companies, Inc., 2000

Standard Costs

Managers focus on quantities and costs that exceed standards, a practice known as

Standard Cost Variances

I see that there is an unfavorable

variance.

But why are variances important to me?

First, they point to causes of problems and directions for improvement.

Actual Quantity ×

Actual Price

Actual Quantity ×

Standard Price

Standard Quantity ×

Standard Price

Price Variance

Quantity Variance

Standard quantity is the quantity allowed for the actual good output.

Managerial Accountant

© The McGraw-Hill Companies, Inc., 2000

Setting Standard Costs

Practical standards should be set at levels

that are currently attainable with reasonable and efficient effort.

Second, they trigger investigations in departments

having responsibility for incurring the costs.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

Use product design specifications.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

Setting Direct Labor Standards

Rate Standards

Time Standards

Use wage surveys and labor contracts.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

Setting Standard Costs

Should we use practical standards or ideal standards?

Irwin/McGraw-Hill

Engineer

A General Model for Variance Analysis

Actual Quantity ×

Actual Price

Actual Quantity ×

Standard Price

Standard Quantity ×

Standard Price

Price Variance

Quantity Variance

Irwin/McGraw-Hill

Human Resources Manager

© The McGraw-Hill Companies, Inc., 2000

Setting Direct Material Standards

Price Standards

Quantity Standards

Final, delivered cost of materials, net of discounts.

Standard price is the amount that should have been paid for the resources acquired.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

A General Model for Variance Analysis

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

Standard Cost Card – Variable Production Cost

A standard cost card for one unit of product might look like this:

Setting Standard Costs

Accountants, engineers, personnel administrators, and production managers combine efforts to set standards based on

experience and expectations.

© The McGraw-Hill Companies, Inc., 2000

Standard Costs

Irwin/McGraw-Hill

Let’s use the general model to calculate standard cost variances,

starting with direct material.

Standard Quantity ×

Standard Price

Price Variance

AQ(AP - SP) AQ = Actual Quantity AP = Actual Price

Irwin/McGraw-Hill

Quantity Variance

SP(AQ - SQ) SP = Standard Price SQ = Standard Quantity

© The McGraw-Hill Companies, Inc., 2000

Material Variances Example Zippy

Hanson Inc. has the following direct material standard to manufacture one Zippy:

operations

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 2000

Standard Cost Variances

Standard Cost Variances

Price Variance

The difference between the actual price and the

Activity Standards

The rate is the variable portion of the predetermined overhead

rate.

The activity is the base used to calculate

the predetermined overhead.

Chapter

10

Standard Costs and Operating Performance

Measures

Standard Costs

Standard Costs are

Irwin/McGraw-Hill

Based on carefully predetermined amounts.