Chapter9公司理财

公司理财第九版中文答案

第一章1.在所有权形式的公司中,股东是公司的所有者。

股东选举公司的董事会,董事会任命该公司的管理层。

企业的所有权和控制权分离的组织形式是导致的代理关系存在的主要原因。

管理者可能追求自身或别人的利益最大化,而不是股东的利益最大化。

在这种环境下,他们可能因为目标不一致而存在代理问题。

2.非营利公司经常追求社会或政治任务等各种目标。

非营利公司财务管理的目标是获取并有效使用资金以最大限度地实现组织的社会使命。

3.这句话是不正确的。

管理者实施财务管理的目标就是最大化现有股票的每股价值,当前的股票价值反映了短期和长期的风险、时间以及未来现金流量。

4.有两种结论。

一种极端,在市场经济中所有的东西都被定价。

因此所有目标都有一个最优水平,包括避免不道德或非法的行为,股票价值最大化。

另一种极端,我们可以认为这是非经济现象,最好的处理方式是通过政治手段。

一个经典的思考问题给出了这种争论的答案:公司估计提高某种产品安全性的成本是30美元万。

然而,该公司认为提高产品的安全性只会节省20美元万。

请问公司应该怎么做呢?”5.财务管理的目标都是相同的,但实现目标的最好方式可能是不同的,因为不同的国家有不同的社会、政治环境和经济制度。

6.管理层的目标是最大化股东现有股票的每股价值。

如果管理层认为能提高公司利润,使股价超过35美元,那么他们应该展开对恶意收购的斗争。

如果管理层认为该投标人或其它未知的投标人将支付超过每股35美元的价格收购公司,那么他们也应该展开斗争。

然而,如果管理层不能增加企业的价值,并且没有其他更高的投标价格,那么管理层不是在为股东的最大化权益行事。

现在的管理层经常在公司面临这些恶意收购的情况时迷失自己的方向。

7.其他国家的代理问题并不严重,主要取决于其他国家的私人投资者占比重较小。

较少的私人投资者能减少不同的企业目标。

高比重的机构所有权导致高学历的股东和管理层讨论决策风险项目。

此外,机构投资者比私人投资者可以根据自己的资源和经验更好地对管理层实施有效的监督机制。

公司理财第九版罗斯课后案例答案 Case Solutions Corporate Finance

公司理财第九版罗斯课后案例答案 Case Solutions CorporateFinance1. 案例一:公司资金需求分析问题:一家公司需要资金支持其新项目。

通过分析现金流量,推断该公司是否需要向外部借款或筹集其他资金。

解答:为了确定公司是否需要外部资金,我们需要分析公司的现金流量状况。

首先,我们需要计算公司的净现金流量(净收入加上非现金项目)。

然后,我们需要将净现金流量与项目的投资现金流量进行对比。

假设公司预计在项目开始时投资100万美元,并在项目运营期为5年。

预计该项目每年将产生50万美元的净现金流量。

现在,我们需要进行以下计算:净现金流量 = 年度现金流量 - 年度投资现金流量年度投资现金流量 = 100万美元年度现金流量 = 50万美元净现金流量 = 50万美元 - 100万美元 = -50万美元根据计算结果,公司的净现金流量为负数(即净现金流出),意味着公司每年都会亏损50万美元。

因此,公司需要从外部筹集资金以支持项目的运营。

2. 案例二:公司股权融资问题:一家公司正在考虑通过股权融资来筹集资金。

根据公司的财务数据和资本结构分析,我们需要确定公司最佳的股权融资方案。

解答:为了确定最佳的股权融资方案,我们需要参考公司的财务数据和资本结构分析。

首先,我们需要计算公司的资本结构比例,即股本占总资本的比例。

然后,我们将不同的股权融资方案与资本结构比例进行对比,选择最佳的方案。

假设公司当前的资本结构比例为60%的股本和40%的债务,在当前的资本结构下,公司的加权平均资本成本(WACC)为10%。

现在,我们需要进行以下计算:•方案一:以新股发行筹集1000万美元,并将其用于项目投资。

在这种方案下,公司的资本结构比例将发生变化。

假设公司的股本增加至80%,债务比例减少至20%。

根据资本结构比例的变化,WACC也将发生变化。

新的WACC可以通过以下公式计算得出:新的WACC = (股本比例 * 股本成本) + (债务比例 * 债务成本)假设公司的股本成本为12%,债务成本为8%:新的WACC = (0.8 * 12%) + (0.2 * 8%) = 9.6%•方案二:以新股发行筹集5000万美元,并将其用于项目投资。

公司理财 斯蒂芬A罗斯 第九版精要

Invests in assets (B)

Current assets Fixed assets Firm issues securities (A) Retained cash flows (F)

Financial markets

Short-term debt

Cash flow from firm (C) Dividends and debt payments (E) Taxes (D) Long-term debt Equity shares

1-1

Chapter Outline

1.1 What is Corporate Finance?

1.2 The Corporate Firm

1.3 The Importance of Cash Flows

1.4 The Goal of Financial Management 1.5 The Agency Problem and Control of the Corporation 1.6 Regulation

1-10

Forms of Business Organization

The Sole Proprietorship The Partnership

General Partnership Limited Partnership

The Corporation

1-11

A Comparison

Know

the basic types of financial management decisions and the role of the Financial Manager Know the financial implications of the various forms of business organization Know the goal of financial management Understand the conflicts of interest that can arise between owners and managers Understand the various regulations that firms face

罗斯《公司理财》第9版英文原书课后部分章节答案

罗斯《公司理财》第9版精要版英文原书课后部分章节答案详细»1 / 17 CH5 11,13,18,19,20 11. To find the PV of a lump sum, we use: PV = FV / (1 + r) t PV = $1,000,000 / (1.10) 80 = $488.19 13. To answer this question, we can use either the FV or the PV formula. Both will give the same answer since they are the inverse of each other. We will use the FV formula, that is: FV = PV(1 + r) t Solving for r, we get: r = (FV / PV) 1 / t –1 r = ($1,260,000 / $150) 1/112 – 1 = .0840 or 8.40% To find the FV of the first prize, we use: FV = PV(1 + r) t FV = $1,260,000(1.0840) 33 = $18,056,409.94 18. To find the FV of a lump sum, we use: FV = PV(1 + r) t FV = $4,000(1.11) 45 = $438,120.97 FV = $4,000(1.11) 35 = $154,299.40 Better start early! 19. We need to find the FV of a lump sum. However, the money will only be invested for six years, so the number of periods is six. FV = PV(1 + r) t FV = $20,000(1.084)6 = $32,449.33 20. To answer this question, we can use either the FV or the PV formula. Both will give the same answer since they are the inverse of each other. We will use the FV formula, that is: FV = PV(1 + r) t Solving for t, we get: t = ln(FV / PV) / ln(1 + r) t = ln($75,000 / $10,000) / ln(1.11) = 19.31 So, the money must be invested for 19.31 years. However, you will not receive the money for another two years. From now, you’ll wait: 2 years + 19.31 years = 21.31 years CH6 16,24,27,42,58 16. For this problem, we simply need to find the FV of a lump sum using the equation: FV = PV(1 + r) t 2 / 17 It is important to note that compounding occurs semiannually. To account for this, we will divide the interest rate by two (the number of compounding periods in a year), and multiply the number of periods by two. Doing so, we get: FV = $2,100[1 + (.084/2)] 34 = $8,505.93 24. This problem requires us to find the FV A. The equation to find the FV A is: FV A = C{[(1 + r) t – 1] / r} FV A = $300[{[1 + (.10/12) ] 360 – 1} / (.10/12)] = $678,146.38 27. The cash flows are annual and the compounding period is quarterly, so we need to calculate the EAR to make the interest rate comparable with the timing of the cash flows. Using the equation for the EAR, we get: EAR = [1 + (APR / m)] m – 1 EAR = [1 + (.11/4)] 4 – 1 = .1146 or 11.46% And now we use the EAR to find the PV of each cash flow as a lump sum and add them together: PV = $725 / 1.1146 + $980 / 1.1146 2 + $1,360 / 1.1146 4 = $2,320.36 42. The amount of principal paid on the loan is the PV of the monthly payments you make. So, the present value of the $1,150 monthly payments is: PV A = $1,150[(1 – {1 / [1 + (.0635/12)]} 360 ) / (.0635/12)] = $184,817.42 The monthly payments of $1,150 will amount to a principal payment of $184,817.42. The amount of principal you will still owe is: $240,000 – 184,817.42 = $55,182.58 This remaining principal amount will increase at the interest rate on the loan until the end of the loan period. So the balloon payment in 30 years, which is the FV of the remaining principal will be: Balloon payment = $55,182.58[1 + (.0635/12)] 360 = $368,936.54 58. To answer this question, we should find the PV of both options, and compare them. Since we are purchasing the car, the lowest PV is the best option. The PV of the leasing is simply the PV of the lease payments, plus the $99. The interest rate we would use for the leasing option is the same as the interest rate of the loan. The PV of leasing is: PV = $99 + $450{1 –[1 / (1 + .07/12) 12(3) ]} / (.07/12) = $14,672.91 The PV of purchasing the car is the current price of the car minus the PV of the resale price. The PV of the resale price is: PV = $23,000 / [1 + (.07/12)] 12(3) = $18,654.82 The PV of the decision to purchase is: $32,000 – 18,654.82 = $13,345.18 3 / 17 In this case, it is cheaper to buy the car than leasing it since the PV of the purchase cash flows is lower. To find the breakeven resale price, we need to find the resale price that makes the PV of the two options the same. In other words, the PV of the decision to buy should be: $32,000 – PV of resale price = $14,672.91 PV of resale price = $17,327.09 The resale price that would make the PV of the lease versus buy decision is the FV ofthis value, so: Breakeven resale price = $17,327.09[1 + (.07/12)] 12(3) = $21,363.01 CH7 3,18,21,22,31 3. The price of any bond is the PV of the interest payment, plus the PV of the par value. Notice this problem assumes an annual coupon. The price of the bond will be: P = $75({1 – [1/(1 + .0875)] 10 } / .0875) + $1,000[1 / (1 + .0875) 10 ] = $918.89 We would like to introduce shorthand notation here. Rather than write (or type, as the case may be) the entire equation for the PV of a lump sum, or the PV A equation, it is common to abbreviate the equations as: PVIF R,t = 1 / (1 + r) t which stands for Present V alue Interest Factor PVIFA R,t = ({1 – [1/(1 + r)] t } / r ) which stands for Present V alue Interest Factor of an Annuity These abbreviations are short hand notation for the equations in which the interest rate and the number of periods are substituted into the equation and solved. We will use this shorthand notation in remainder of the solutions key. 18. The bond price equation for this bond is: P 0 = $1,068 = $46(PVIFA R%,18 ) + $1,000(PVIF R%,18 ) Using a spreadsheet, financial calculator, or trial and error we find: R = 4.06% This is thesemiannual interest rate, so the YTM is: YTM = 2 4.06% = 8.12% The current yield is:Current yield = Annual coupon payment / Price = $92 / $1,068 = .0861 or 8.61% The effective annual yield is the same as the EAR, so using the EAR equation from the previous chapter: Effective annual yield = (1 + 0.0406) 2 – 1 = .0829 or 8.29% 20. Accrued interest is the coupon payment for the period times the fraction of the period that has passed since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six months is one-half of the annual coupon payment. There are four months until the next coupon payment, so two months have passed since the last coupon payment. The accrued interest for the bond is: Accrued interest = $74/2 × 2/6 = $12.33 And we calculate the clean price as: 4 / 17 Clean price = Dirty price –Accrued interest = $968 –12.33 = $955.67 21. Accrued interest is the coupon payment for the period times the fraction of the period that has passed since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six months is one-half of the annual coupon payment. There are two months until the next coupon payment, so four months have passed since the last coupon payment. The accrued interest for the bond is: Accrued interest = $68/2 × 4/6 = $22.67 And we calculate the dirty price as: Dirty price = Clean price + Accrued interest = $1,073 + 22.67 = $1,095.67 22. To find the number of years to maturity for the bond, we need to find the price of the bond. Since we already have the coupon rate, we can use the bond price equation, and solve for the number of years to maturity. We are given the current yield of the bond, so we can calculate the price as: Current yield = .0755 = $80/P 0 P 0 = $80/.0755 = $1,059.60 Now that we have the price of the bond, the bond price equation is: P = $1,059.60 = $80[(1 – (1/1.072) t ) / .072 ] + $1,000/1.072 t We can solve this equation for t as follows: $1,059.60(1.072) t = $1,111.11(1.072) t –1,111.11 + 1,000 111.11 = 51.51(1.072) t2.1570 = 1.072 t t = log 2.1570 / log 1.072 = 11.06 11 years The bond has 11 years to maturity.31. The price of any bond (or financial instrument) is the PV of the future cash flows. Even though Bond M makes different coupons payments, to find the price of the bond, we just find the PV of the cash flows. The PV of the cash flows for Bond M is: P M = $1,100(PVIFA 3.5%,16 )(PVIF 3.5%,12 ) + $1,400(PVIFA3.5%,12 )(PVIF 3.5%,28 ) + $20,000(PVIF 3.5%,40 ) P M = $19,018.78 Notice that for the coupon payments of $1,400, we found the PV A for the coupon payments, and then discounted the lump sum back to today. Bond N is a zero coupon bond with a $20,000 par value, therefore, the price of the bond is the PV of the par, or: P N = $20,000(PVIF3.5%,40 ) = $5,051.45 CH8 4,18,20,22,244. Using the constant growth model, we find the price of the stock today is: P 0 = D 1 / (R – g) = $3.04 / (.11 – .038) = $42.22 5 / 17 18. The price of a share of preferred stock is the dividend payment divided by the required return. We know the dividend payment in Year 20, so we can find the price of the stock in Y ear 19, one year before the first dividend payment. Doing so, we get: P 19 = $20.00 / .064 P 19 = $312.50 The price of the stock today is the PV of the stock price in the future, so the price today will be: P 0 = $312.50 / (1.064) 19 P 0 = $96.15 20. We can use the two-stage dividend growth model for this problem, which is: P 0 = [D 0 (1 + g 1 )/(R – g 1 )]{1 – [(1 + g 1 )/(1 + R)] T }+ [(1 + g 1 )/(1 + R)] T [D 0 (1 + g 2 )/(R –g 2 )] P0 = [$1.25(1.28)/(.13 –.28)][1 –(1.28/1.13) 8 ] + [(1.28)/(1.13)] 8 [$1.25(1.06)/(.13 – .06)] P 0 = $69.55 22. We are asked to find the dividend yield and capital gains yield for each of the stocks. All of the stocks have a 15 percent required return, which is the sum of the dividend yield and the capital gains yield. To find the components of the total return, we need to find the stock price for each stock. Using this stock price and the dividend, we can calculate the dividend yield. The capital gains yield for the stock will be the total return (required return) minus the dividend yield. W: P 0 = D 0 (1 + g) / (R – g) = $4.50(1.10)/(.19 – .10) = $55.00 Dividend yield = D 1 /P 0 = $4.50(1.10)/$55.00 = .09 or 9% Capital gains yield = .19 – .09 = .10 or 10% X: P 0 = D 0 (1 + g) / (R – g) = $4.50/(.19 – 0) = $23.68 Dividend yield = D 1 /P 0 = $4.50/$23.68 = .19 or 19% Capital gains yield = .19 – .19 = 0% Y: P 0 = D 0 (1 + g) / (R – g) = $4.50(1 – .05)/(.19 + .05) = $17.81 Dividend yield = D 1 /P 0 = $4.50(0.95)/$17.81 = .24 or 24% Capital gains yield = .19 – .24 = –.05 or –5% Z: P 2 = D 2 (1 + g) / (R – g) = D 0 (1 + g 1 ) 2 (1 +g 2 )/(R – g 2 ) = $4.50(1.20) 2 (1.12)/(.19 – .12) = $103.68 P 0 = $4.50 (1.20) / (1.19) + $4.50(1.20) 2 / (1.19) 2 + $103.68 / (1.19) 2 = $82.33 Dividend yield = D 1 /P 0 = $4.50(1.20)/$82.33 = .066 or 6.6% Capital gains yield = .19 – .066 = .124 or 12.4% In all cases, the required return is 19%, but the return is distributed differently between current income and capital gains. High growth stocks have an appreciable capital gains component but a relatively small current income yield; conversely, mature, negative-growth stocks provide a high current income but also price depreciation over time. 24. Here we have a stock with supernormal growth, but the dividend growth changes every year for the first four years. We can find the price of the stock in Y ear 3 since the dividend growth rate is constant after the third dividend. The price of the stock in Y ear 3 will be the dividend in Y ear 4, divided by the required return minus the constant dividend growth rate. So, the price in Y ear 3 will be: 6 / 17 P3 = $2.45(1.20)(1.15)(1.10)(1.05) / (.11 – .05) = $65.08 The price of the stock today will be the PV of the first three dividends, plus the PV of the stock price in Y ear 3, so: P 0 = $2.45(1.20)/(1.11) + $2.45(1.20)(1.15)/1.11 2 + $2.45(1.20)(1.15)(1.10)/1.11 3 + $65.08/1.11 3 P 0 = $55.70 CH9 3,4,6,9,15 3. Project A has cash flows of $19,000 in Y ear 1, so the cash flows are short by $21,000 of recapturing the initial investment, so the payback for Project A is: Payback = 1 + ($21,000 / $25,000) = 1.84 years Project B has cash flows of: Cash flows = $14,000 + 17,000 + 24,000 = $55,000 during this first three years. The cash flows are still short by $5,000 of recapturing the initial investment, so the payback for Project B is: B: Payback = 3 + ($5,000 / $270,000) = 3.019 years Using the payback criterion and a cutoff of 3 years, accept project A and reject project B. 4. When we use discounted payback, we need to find the value of all cash flows today. The value today of the project cash flows for the first four years is: V alue today of Y ear 1 cash flow = $4,200/1.14 = $3,684.21 V alue today of Y ear 2 cash flow = $5,300/1.14 2 = $4,078.18 V alue today of Y ear 3 cash flow = $6,100/1.14 3 = $4,117.33 V alue today of Y ear 4 cash flow = $7,400/1.14 4 = $4,381.39 To findthe discounted payback, we use these values to find the payback period. The discounted first year cash flow is $3,684.21, so the discounted payback for a $7,000 initial cost is: Discounted payback = 1 + ($7,000 – 3,684.21)/$4,078.18 = 1.81 years For an initial cost of $10,000, the discounted payback is: Discounted payback = 2 + ($10,000 –3,684.21 –4,078.18)/$4,117.33 = 2.54 years Notice the calculation of discounted payback. We know the payback period is between two and three years, so we subtract the discounted values of the Y ear 1 and Y ear 2 cash flows from the initial cost. This is the numerator, which is the discounted amount we still need to make to recover our initial investment. We divide this amount by the discounted amount we will earn in Y ear 3 to get the fractional portion of the discounted payback. If the initial cost is $13,000, the discounted payback is: Discounted payback = 3 + ($13,000 – 3,684.21 – 4,078.18 – 4,117.33) / $4,381.39 = 3.26 years 7 / 17 6. Our definition of AAR is the average net income divided by the average book value. The average net income for this project is: A verage net income = ($1,938,200 + 2,201,600 + 1,876,000 + 1,329,500) / 4 = $1,836,325 And the average book value is: A verage book value = ($15,000,000 + 0) / 2 = $7,500,000 So, the AAR for this project is: AAR = A verage net income / A verage book value = $1,836,325 / $7,500,000 = .2448 or 24.48% 9. The NPV of a project is the PV of the outflows minus the PV of the inflows. Since the cash inflows are an annuity, the equation for the NPV of this project at an 8 percent required return is: NPV = –$138,000 + $28,500(PVIFA 8%, 9 ) = $40,036.31 At an 8 percent required return, the NPV is positive, so we would accept the project. The equation for the NPV of the project at a 20 percent required return is: NPV = –$138,000 + $28,500(PVIFA 20%, 9 ) = –$23,117.45 At a 20 percent required return, the NPV is negative, so we would reject the project. We would be indifferent to the project if the required return was equal to the IRR of the project, since at that required return the NPV is zero. The IRR of the project is: 0 = –$138,000 + $28,500(PVIFA IRR, 9 ) IRR = 14.59% 15. The profitability index is defined as the PV of the cash inflows divided by the PV of the cash outflows. The equation for the profitability index at a required return of 10 percent is: PI = [$7,300/1.1 + $6,900/1.1 2 + $5,700/1.1 3 ] / $14,000 = 1.187 The equation for the profitability index at a required return of 15 percent is: PI = [$7,300/1.15 + $6,900/1.15 2 + $5,700/1.15 3 ] / $14,000 = 1.094 The equation for the profitability index at a required return of 22 percent is: PI = [$7,300/1.22 + $6,900/1.22 2 + $5,700/1.22 3 ] / $14,000 = 0.983 8 / 17 We would accept the project if the required return were 10 percent or 15 percent since the PI is greater than one. We would reject the project if the required return were 22 percent since the PI。

公司理财Corporate_Finance_第九版_CASE答案(完整资料).doc

【最新整理,下载后即可编辑】Case SolutionsFundamentals of Corporate FinanceRoss, Westerfield, and Jordan9th editionCHAPTER 1THE McGEE CAKE COMPANY1.The advantages to a LLC are: 1) Reduction of personal liability. A soleproprietor has unlimited liability, which can include the potential loss of all personal assets. 2) Taxes. Forming an LLC may mean that more expenses can be considered business expenses and be deducted from the company’s income. 3) Improved credibility. The business may have increased credibility in the business world compared to a sole proprietorship. 4) Ability to attract investment. Corporations, even LLCs, can raise capital through the sale of equity. 5) Continuous life. Sole proprietorships have a limited life, while corporations have a potentially perpetual life. 6) Transfer of ownership. It is easier to transfer ownership in a corporation through the sale of stock.The biggest disadvantage is the potential cost, although the cost of forminga LLC can be relatively small. There are also other potential costs, includingmore expansive record-keeping.2.Forming a corporation has the same advantages as forming a LLC, but thecosts are likely to be higher.3.As a small company, changing to a LLC is probably the most advantageousdecision at the current time. If the company grows, and Doc and Lyn are willing to sell more equity ownership, the company can reorganize as a corporation at a later date. Additionally, forming a LLC is likely to be less expensive than forming a corporation.CHAPTER 2CASH FLOWS AND FINANCIAL STATEMENTS AT SUNSET BOARDS Below are the financial statements that you are asked to prepare.1.The income statement for each year will look like this:Income statement2008 2009Sales $247,259 $301,392Cost of goods sold 126,038 159,143Selling & administrative 24,787 32,352Depreciation 35,581 40,217EBIT $60,853 $69,680Interest 7,735 8,866EBT $53,118 $60,814Taxes 10,624 12,163Net income $42,494 $48,651Dividends $21,247 $24,326Addition to retainedearnings 21,247 24,3262.The balance sheet for each year will be:Balance sheet as of Dec. 31, 2008C-26 CASE SOLUTIONSCash $18,187 Accounts payable $32,143 Accountsreceivable 12,887 Notes payable 14,651 Inventory 27,119 Current liabilities $46,794 Current assets $58,193Long-term debt $79,235 Net fixed assets $156,975 Owners' equity 89,139Total assets $215,168 Total liab. &equity $215,168In the first year, equity is not given. Therefore, we must calculate equity as a plug variable. Since total liabilities & equity is equal to total assets, equity can be calculated as:Equity = $215,168 – 46,794 – 79,235Equity = $89,139CHAPTER 2 C-5Balance sheet as of Dec. 31, 2009Cash $27,478 Accounts payable $36,404 Accountsreceivable 16,717 Notes payable 15,997 Inventory 37,216 Current liabilities $52,401 Current assets $81,411Long-term debt $91,195 Net fixed assets $191,250 Owners' equity 129,065Total assets $272,661 Total liab. &equity $272,661The owner’s equity for 2009 is the beginning of year owner’s equity, plus the addition to retained earnings, plus the new equity, so:Equity = $89,139 + 24,326 + 15,600Equity = $129,065ing the OCF equation:OCF = EBIT + Depreciation – TaxesThe OCF for each year is:OCF2008 = $60,853 + 35,581 – 10,624OCF2008 = $85,180OCF2009 = $69,680 + 40,217 – 12,163OCF2009 = $97,734C-26 CASE SOLUTIONS4.To calculate the cash flow from assets, we need to find the capital spendingand change in net working capital. The capital spending for the year was: Capital spendingEnding net fixed assets $191,250– Beginning net fixedassets 156,975+ Depreciation 40,217Net capital spending $74,492And the change in net working capital was:Change in net working capitalEnding NWC $29,010– Beginning NWC 11,399Change in NWC $17,611CHAPTER 2 C-5 So, the cash flow from assets was:Cash flow from assetsOperating cash flow $97,734– Net capital spending 74,492– Change in NWC 17,611Cash flow from assets $ 5,6315.The cash flow to creditors was:Cash flow to creditorsInterest paid $8,866– Net new borrowing 11,960Cash flow to creditors –$3,0946.The cash flow to stockholders was:Cash flow tostockholdersDividends paid $24,326– Net new equityraised 15,600Cash flow tostockholders $8,726Answers to questions1.The firm had positive earnings in an accounting sense (NI > 0) and hadpositive cash flow from operations. The firm invested $17,611 in new netC-26 CASE SOLUTIONSworking capital and $74,492 in new fixed assets. The firm gave $5,631 to its stakeholders. It raised $3,094 from bondholders, and paid $8,726 to stockholders.2.The expansion plans may be a little risky. The company does have a positivecash flow, but a large portion of the operating cash flow is already going to capital spending. The company has had to raise capital from creditors and stockholders for its current operations. So, the expansion plans may be too aggressive at this time. On the other hand, companies do need capital to grow. Before investing or loaning the company money, you would want to know where the current capital spending is going, and why the company is spending so much in this area already.CHAPTER 3RATIOS ANALYSIS AT S&S AIR1.The calculations for the ratios listed are:Current ratio = $2,186,520 / $2,919,000Current ratio = 0.75 timesQuick ratio = ($2,186,250 – 1,037,120) / $2,919,000Quick ratio = 0.39 timesCash ratio = $441,000 / $2,919,000Cash ratio = 0.15 timesTotal asset turnover = $30,499,420 / $18,308,920Total asset turnover = 1.67 timesInventory turnover = $22,224,580 / $1,037,120Inventory turnover = 21.43 timesReceivables turnover = $30,499,420 / $708,400Receivables turnover = 43.05 timesTotal debt ratio = ($18,308,920 – 10,069,920) / $18,308,920 Total debt ratio = 0.45 timesDebt-equity ratio = ($2,919,000 + 5,320,000) / $10,069,920C-26 CASE SOLUTIONSDebt-equity ratio = 0.82 timesEquity multiplier = $18,308,920 / $10,069,920Equity multiplier = 1.82 timesTimes interest earned = $3,040,660 / $478,240Times interest earned = 6.36 timesCash coverage = ($3,040,660 + 1,366,680) / $478,420 Cash coverage = 9.22 timesProfit margin = $1,537,452 / $30,499,420Profit margin = 5.04%Return on assets = $1,537,452 / $18,308,920Return on assets = 8.40%Return on equity = $1,537,452 / $10,069,920Return on equity = 15.27%CHAPTER 3 C-11 2. Boeing is probably not a good aspirant company. Even though bothcompanies manufacture airplanes, S&S Air manufactures small airplanes, while Boeing manufactures large, commercial aircraft. These are two different markets. Additionally, Boeing is heavily involved in the defense industry, as well as Boeing Capital, which finances airplanes.Bombardier is a Canadian company that builds business jets, short-range airliners and fire-fighting amphibious aircraft and also provides defense-related services. It is the third largest commercial aircraft manufacturer in the world. Embraer is a Brazilian manufacturer than manufactures commercial, military, and corporate airplanes. Additionally, the Brazilian government is a part owner of the company. Bombardier and Embraer are probably not good aspirant companies because of the diverse range of products and manufacture of larger aircraft.Cirrus is the world's second largest manufacturer of single-engine, piston-powered aircraft. Its SR22 is the world's best selling plane in its class. The company is noted for its innovative small aircraft and is a good aspirant company.Cessna is a well known manufacturer of small airplanes. The company produces business jets, freight- and passenger-hauling utility Caravans, personal and small-business single engine pistons. It may be a good aspirant company, however, its products could be considered too broad and diversified since S&S Air produces only small personal airplanes.3. S&S is below the median industry ratios for the current and cash ratios.This implies the company has less liquidity than the industry in general.However, both ratios are above the lower quartile, so there are companiesC-26 CASE SOLUTIONSin the industry with lower liquidity ratios than S&S Air. The company may have more predictable cash flows, or more access to short-term borrowing.If you created an Inventory to Current liabilities ratio, S&S Air would havea ratio that is lower than the industry median. The current ratio is below theindustry median, while the quick ratio is above the industry median. This implies that S&S Air has less inventory to current liabilities than the industry median. S&S Air has less inventory than the industry median, but more accounts receivable than the industry since the cash ratio is lower than the industry median.The turnover ratios are all higher than the industry median; in fact, all three turnover ratios are above the upper quartile. This may mean that S&S Air is more efficient than the industry.The financial leverage ratios are all below the industry median, but above the lower quartile. S&S Air generally has less debt than comparable companies, but still within the normal range.The profit margin, ROA, and ROE are all slightly below the industry median, however, not dramatically lower. The company may want to examine its costs structure to determine if costs can be reduced, or price can be increased.Overall, S&S Air’s performance seems good, although the liquidity ratios indicate that a closer look may be needed in this area.CHAPTER 3 C-11 Below is a list of possible reasons it may be good or bad that each ratio is higher or lower than the industry. Note that the list is not exhaustive, but merely one possible explanation for each ratio.Ratio Good BadCurrent ratio Better at managingcurrent accounts. May be having liquidity problems.Quick ratio Better at managingcurrent accounts. May be having liquidity problems.Cash ratio Better at managingcurrent accounts. May be having liquidity problems.Total asset turnover Better at utilizing assets. Assets may be older anddepreciated, requiringextensive investmentsoon.Inventory turnover Better at inventorymanagement, possibly dueto better procedures.Could be experiencinginventory shortages.Receivables turnover Better at collectingreceivables.May have credit termsthat are too strict.Decreasing receivablesturnover may increasesales.Total debt ratio Less debt than industrymedian means thecompany is less likely toexperience creditproblems. Increasing the amount of debt can increase shareholder returns. Especially notice that it will increase ROE.Debt-equity Less debt than industry Increasing the amount ofC-26 CASE SOLUTIONSratio median means thecompany is less likely toexperience creditproblems. debt can increase shareholder returns. Especially notice that it will increase ROE.Equity multiplier Less debt than industrymedian means thecompany is less likely toexperience creditproblems.Increasing the amount ofdebt can increaseshareholder returns.Especially notice that itwill increase ROE.TIE Higher quality materialscould be increasing costs. The company may have more difficulty meeting interest payments in a downturn.Cash coverage Less debt than industrymedian means thecompany is less likely toexperience creditproblems. Increasing the amount of debt can increase shareholder returns. Especially notice that it will increase ROE.Profit margin The PM is slightly belowthe industry median. Itcould be a result of higherquality materials or bettermanufacturing. Company may be having trouble controlling costs.ROA Company may have newerassets than the industry. Company may have newer assets than the industry.ROE Lower profit margin maybe a result of higherquality. Profit margin and EM are lower than industry, which results in the lower ROE.CHAPTER 4PLANNING FOR GROWTH AT S&S AIR1.To calculate the internal growth rate, we first need to find the ROA and theretention ratio, so:ROA = NI / TAROA = $1,537,452 / $18,309,920ROA = .0840 or 8.40%b = Addition to RE / NIb = $977,452 / $1,537,452b = 0.64Now we can use the internal growth rate equation to get:Internal growth rate = (ROA × b) / [1 – (ROA × b)]Internal growth rate = [0.0840(.64)] / [1 – 0.0840(.64)]Internal growth rate = .0564 or 5.64%To find the sustainable growth rate, we need the ROE, which is:ROE = NI / TEROE = $1,537,452 / $10,069,920ROE = .1527 or 15.27%C-26 CASE SOLUTIONSUsing the retention ratio we previously calculated, the sustainable growth rate is:Sustainable growth rate = (ROE × b) / [1 – (ROE × b)]Sustainable growth rate = [0.1527(.64)] / [1 – 0.1527(.64)]Sustainable growth rate = .1075 or 10.75%The internal growth rate is the growth rate the company can achieve with no outside financing of any sort. The sustainable growth rate is the growth rate the company can achieve by raising outside debt based on its retained earnings and current capital structure.CHAPTER 4 C-21 2.Pro forma financial statements for next year at a 12 percent growth rate are:Income statementSales $ 34,159,35COGS 24,891,530 Other expenses 4,331,600 Depreciation 1,366,680EBIT $ 3,569,541Interest 478,240Taxable income $ 3,091,301Taxes (40%) 1,236,520Net income $ 1,854,78Dividends $ 675,583C-26 CASE SOLUTIONSAdd to RE 1,179,197Balance sheetAssets Liabilities & EquityCurrent Assets Current LiabilitiesCash $ 493,92AccountsPayable $ 995,680Accounts rec. 793,408 Notes Payable 2,030,000 Inventory 1,161,574 Total CL $ 3,025,680 Total CA $ 2,448,902Long-term debt $ 5,320,000ShareholderEquityCommon stock $ 350,000Fixed assets Retainedearnings 10,899,117Net PP&E $ 18,057,088 Total Equity $ 11,249,117Total Assets $ 20,505,990 Total L&E $ 19,594,787CHAPTER 4 C-21 So, the EFN is:EFN = Total assets – Total liabilities and equityEFN = $20,505,990 – 19,594,797EFN = $911,193The company can grow at this rate by changing the way it operates. For example, if profit margin increases, say by reducing costs, the ROE increases, it will increase the sustainable growth rate. In general, as long as the company increases the profit margin, total asset turnover, or equity multiplier, the higher growth rate is possible. Note however, that changing any one of these will have the effect of changing the pro forma financial statements.C-26 CASE SOLUTIONS3.Now we are assuming the company can only build in amounts of $5 million.We will assume that the company will go ahead with the fixed asset acquisition. To estimate the new depreciation charge, we will find the current depreciation as a percentage of fixed assets, then, apply this percentage to the new fixed assets. The depreciation as a percentage of assets this year was:Depreciation percentage = $1,366,680 / $16,122,400Depreciation percentage = .0848 or 8.48%The new level of fixed assets with the $5 million purchase will be:New fixed assets = $16,122,400 + 5,000,000 = $21,122,400So, the pro forma depreciation will be:Pro forma depreciation = .0848($21,122,400)Pro forma depreciation = $1,790,525We will use this amount in the pro forma income statement. So, the pro forma income statement will be:Income statementSales $ 34,159,35COGS 24,891,530 Other expensesCHAPTER 4 C-214,331,600Depreciation 1,790,525EBIT $ 3,145,696Interest 478,240Taxable income $ 2,667,456Taxes (40%) 1,066,982Net income $ 1,600,473Dividends $ 582,955Add to RE 1,017,519C-26 CASE SOLUTIONSThe pro forma balance sheet will remain the same except for the fixed asset and equity accounts. The fixed asset account will increase by $5 million, rather than the growth rate of sales.Balance sheetAssets Liabilities & EquityCurrent Assets Current LiabilitiesCash $ 493,92AccountsPayable $ 995,680Accounts rec. 793,408 Notes Payable 2,030,000 Inventory 1,161,574 Total CL $ 3,025,680 Total CA $ 2,448,902Long-term debt $ 5,320,000ShareholderEquityCommon stock $ 350,000Fixed assets Retainedearnings 10,737,439Net PP&E $ 21,122,400 Total Equity $ 11,087,439Total Assets $ 23,571,302 Total L&E $ 19,433,119CHAPTER 4 C-21 So, the EFN is:EFN = Total assets – Total liabilities and equityEFN = $23,581,302 – 19,433,119EFN = $4,138,184Since the fixed assets have increased at a faster percentage than sales, the capacity utilization for next year will decrease.CHAPTER 6THE MBA DECISION1. Age is obviously an important factor. The younger an individual is, the moretime there is for the (hopefully) increased salary to offset the cost of the decision to return to school for an MBA. The cost includes both the explicit costs such as tuition, as well as the opportunity cost of the lost salary.2. Perhaps the most important nonquantifiable factors would be whether ornot he is married and if he has any children. With a spouse and/or children, he may be less inclined to return for an MBA since his family may be less amenable to the time and money constraints imposed by classes. Other factors would include his willingness and desire to pursue an MBA, job satisfaction, and how important the prestige of a job is to him, regardless of the salary.3.He has three choices: remain at his current job, pursue a Wilton MBA, orpursue a Mt. Perry MBA. In this analysis, room and board costs are irrelevant since presumably they will be the same whether he attends college or keeps his current job. We need to find the aftertax value of each, so:Remain at current job:Aftertax salary = $55,000(1 – .26) = $40,700CHAPTER 6 C-27 His salary will grow at 3 percent per year, so the present value of his aftertax salary is:PV = C {1 – [(1 + g)/(1 + r)]t} / (r–g)]PV = $40,700{[1 – [(1 +.065)/(1 + .03)]38} / (.065 – .03)PV = $836,227.34Wilton MBA:Costs:Total direct costs = $63,000 + 2,500 + 3,000 = $68,500PV of direct costs = $68,500 + 68,500 / (1.065) = $132,819.25PV of indirect costs (lost salary) = $40,700 / (1.065) + $40,700(1 + .03) / (1 + .065)2 = $75,176.00Salary:PV of aftertax bonus paid in 2 years = $15,000(1 –.31) / 1.0652= $9,125.17Aftertax salary = $98,000(1 – .31) = $67,620C-26 CASE SOLUTIONSHis salary will grow at 4 percent per year. We must also remember that he will now only work for 36 years, so the present value of his aftertax salary is: PV = C {1 – [(1 + g)/(1 + r)]t} / (r–g)]PV = $67,620{[1 – [(1 +.065)/(1 + .04)]36} / (.065 – .04)PV = $1,554,663.22Since the first salary payment will be received three years from today, so we need to discount this for two years to find the value today, which will be: PV = $1,544,663.22 / 1.0652PV = $1,370,683.26So, the total value of a Wilton MBA is:Value = –$75,160 – 132,819.25 + 9,125.17 + 1,370,683.26 =$1,171,813.18Mount Perry MBA:Costs:Total direct costs = $78,000 + 3,500 + 3,000 = $86,500. Note, this is also the PV of the direct costs since they are all paid today.PV of indirect costs (lost salary) = $40,700 / (1.065) = $38,215.96Salary:CHAPTER 6 C-27 PV of aftertax bonus paid in 1 year = $10,000(1 – .29) / 1.065 = $6,666.67 Aftertax salary = $81,000(1 – .29) = $57,510His salary will grow at 3.5 percent per year. We must also remember that he will now only work for 37 years, so the present value of his aftertax salary is: PV = C {1 – [(1 + g)/(1 + r)]t} / (r–g)]PV = $57,510{[1 – [(1 +.065)/(1 + .035)]37} / (.065 – .035)PV = $1,250,991.81Since the first salary payment will be received two years from today, so we need to discount this for one year to find the value today, which will be:PV = $1,250,991.81 / 1.065PV = $1,174,640.20So, the total value of a Mount Perry MBA is:Value = –$86,500 – 38,215.96 + 6,666.67 + 1,174,640.20 = $1,056,590.90C-26 CASE SOLUTIONS4.He is somewhat correct. Calculating the future value of each decision willresult in the option with the highest present value having the highest future value. Thus, a future value analysis will result in the same decision. However, his statement that a future value analysis is the correct method is wrong since a present value analysis will give the correct answer as well.5. To find the salary offer he would need to make the Wilton MBA asfinancially attractive as the as the current job, we need to take the PV of his current job, add the costs of attending Wilton, and the PV of the bonus on an aftertax basis. So, the necessary PV to make the Wilton MBA the same as his current job will be:PV = $836,227.34 + 132,819.25 + 75,176.00 – 9,125.17 = $1,035,097.42This PV will make his current job exactly equal to the Wilton MBA on a financial basis. Since his salary will still be a growing annuity, the aftertax salary needed is:PV = C {1 – [(1 + g)/(1 + r)]t} / (r–g)]$1,035,097.42 = C {[1 – [(1 +.065)/(1 + .04)]36} / (.065 – .04)C = $45,021.51This is the aftertax salary. So, the pretax salary must be:Pretax salary = $45,021.51 / (1 – .31) = $65,248.576.The cost (interest rate) of the decision depends on the riskiness of the use offunds, not the source of the funds. Therefore, whether he can pay cash orCHAPTER 6 C-27 must borrow is irrelevant. This is an important concept which will be discussed further in capital budgeting and the cost of capital in later chapters.CHAPTER 7FINANCING S&S AIR’S EXPANSION PLANS WITH A BOND ISSUEA rule of thumb with bond provisions is to determine who benefits by theprovision. If the company benefits, the bond will have a higher coupon rate.If the bondholders benefit, the bond will have a lower coupon rate.1. A bond with collateral will have a lower coupon rate. Bondholders have theclaim on the collateral, even in bankruptcy. Collateral provides an asset that bondholders can claim, which lowers their risk in default. The downside of collateral is that the company generally cannot sell the asset used as collateral, and they will generally have to keep the asset in good working order.2.The more senior the bond is, the lower the coupon rate. Senior bonds getfull payment in bankruptcy proceedings before subordinated bonds receive any payment. A potential problem may arise in that the bond covenant may restrict the company from issuing any future bonds senior to the current bonds.3. A sinking fund will reduce the coupon rate because it is a partial guaranteeto bondholders. The problem with a sinking fund is that the company must make the interim payments into a sinking fund or face default. This means the company must be able to generate these cash flows.4. A provision with a specific call date and prices would increase the couponrate. The call provision would only be used when it is to the company’s advantage, thus the bondholder’s disadvantage. The downside is theCHAPTER 7 C-29 higher coupon rate. The company benefits by being able to refinance at a lower rate if interest rates fall significantly, that is, enough to offset the call provision cost.5. A deferred call would reduce the coupon rate relative to a call provision witha deferred call. The bond will still have a higher rate relative to a plain vanillabond. The deferred call means that the company cannot call the bond for a specified period. This offers the bondholders protection for this period. The disadvantage of a deferred call is that the company cannot call the bond during the call protection period. Interest rates could potentially fall to the point where it would be beneficial for the company to call the bond, yet the company is unable to do so.6. A make-whole call provision should lower the coupon rate in comparison toa call provision with specific dates since the make-whole call repays thebondholder the present value of the future cash flows. However, a make-whole call provision should not affect the coupon rate in comparison to a plain vanilla bond. Since the bondholders are made whole, they should be indifferent between a plain vanilla bond and a make-whole bond. If a bond with a make-whole provision is called, bondholders receive the market value of the bond, which they can reinvest in another bond with similar characteristics. If we compare this to a bond with a specific call price, investors rarely receive the full market value of the future cash flows.CASE 3 C-30 7. A positive covenant would reduce the coupon rate. The presence of positivecovenants protects bondholders by forcing the company to undertake actions that benefit bondholders. Examples of positive covenants would be: the company must maintain audited financial statements; the company must maintain a minimum specified level of working capital or a minimum specified current ratio; the company must maintain any collateral in good working order. The negative side of positive covenants is that the company is restricted in its actions. The positive covenant may force the company into actions in the future that it would rather not undertake.8. A negative covenant would reduce the coupon rate. The presence ofnegative covenants protects bondholders from actions by the company that would harm the bondholders. Remember, the goal of a corporation is to maximize shareholder wealth. This says nothing about bondholders.Examples of negative covenants would be: the company cannot increase dividends, or at least increase beyond a specified level; the company cannot issue new bonds senior to the current bond issue; the company cannot sell any collateral. The downside of negative covenants is the restriction of the company’s actions.9.Even though the company is not public, a conversion feature would likelylower the coupon rate. The conversion feature would permit bondholders to benefit if the company does well and also goes public. The downside is that the company may be selling equity at a discounted price.10. The downside of a floating-rate coupon is that if interest rates rise, thecompany has to pay a higher interest rate. However, if interest rates fall, the company pays a lower interest rate.CHAPTER 8STOCK VALUATION AT RAGAN, INC.1.The total dividends paid by the company were $126,000. Since there are100,000 shares outstanding, the total earnings for the company were: Total earnings = 100,000($4.54) = $454,000This means the payout ratio was:Payout ratio = $126,000/$454,000 = 0.28So, the retention ratio was:Retention ratio = 1 – .28 = 0.72Using the retention ratio, the company’s growth rate is:g = ROE × b = 0.25*(.72) = .1806 or 18.06%The dividend per share paid this year was:= $63,000 / 50,000D= $1.26DNow we can find the stock price, which is:C-84 CASE SOLUTIONSP 0 = D 1 / (R – g )P 0 = $1.26(1.1806) / (.20 – .1806)P 0 = $76.752.Since Expert HVAC had a write off which affected its earnings per share, we need to recalculate the industry EPS. So, the industry EPS is:Industry EPS = ($0.79 + 1.38 + 1.06) / 3 = $1.08Using this industry EPS, the industry payout ratio is:Industry payout ratio = $0.40/$1.08 = .3715 or 37.15%So, the industry retention ratio isIndustry retention ratio = 1 – .3715 = .6285 or 62.85%。

公司理财精要版第10版Chap09

$ 200

$ 182

2

400

331

3

700

526

4

300

205现CF $ 182

价值?

9-6

9.1 为什么要使用净现值

净现值(NPV)法则是决定是否实施投资的一个有效判 断标准。

投资的净现值等于: 投资产生的未来全部现金流量的现值 – 初始投资

一项投资的净现值是这项投资的未来现金流量(收益)的 现值减去初始投资成本。

未来现金流量的现值是考虑过适当的市场利率进行贴现后 的现金流量的价值。

项目A、B、C的预期现金流量

年份

A

0

-100

1

20

2

30

3

50

4

60

回收期(年)

3

B

C

-100

-100

50

50

30

30

20

20

60

60000

3

3

回收期法

管理视角

回收期法决策过程简便(容易理解)。 回收期法便于决策评估。 回收期法有利于加快资金回笼。

由于上述原因,回收期法常常被用来筛选大量的小 型投资项目。

固定资产 1 有形 2 无形

公司应该投

资于什么样

的长期资产 ?

流动 负债 长期 负债

所有者 权益

Good Decision Criteria

一个好的资本预算评估准则要考虑以下问题:

▪ 该评估准则考虑了货币的时间价值? ▪ 该评估准则是否考虑了投资蕴含的风险? ▪ 该评估准则能否判断某项投资是否为企业创造了

什么是公司理财?

公司资产负债表模型

公司理财研究以下三个问题:

公司理财9

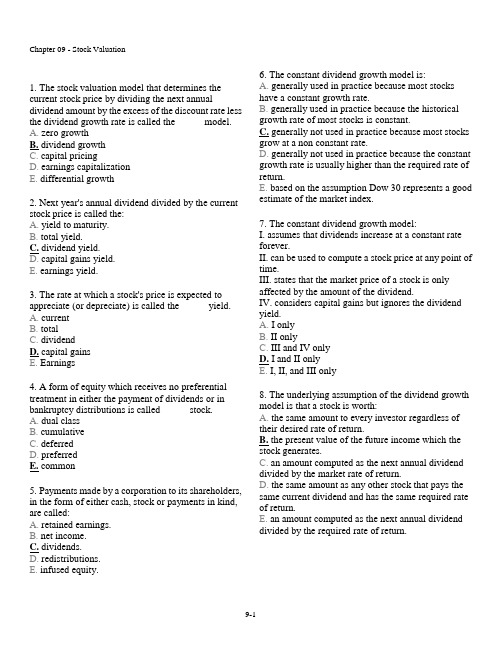

1. The stock valuation model that determines the current stock price by dividing the next annual dividend amount by the excess of the discount rate less the dividend growth rate is called the _____ model.A. zero growthB. dividend growthC. capital pricingD. earnings capitalizationE. differential growth2. Next year's annual dividend divided by the current stock price is called the:A. yield to maturity.B. total yield.C. dividend yield.D. capital gains yield.E. earnings yield.3. The rate at which a stock's price is expected to appreciate (or depreciate) is called the _____ yield.A. currentB. totalC. dividendD. capital gainsE. Earnings4. A form of equity which receives no preferential treatment in either the payment of dividends or in bankruptcy distributions is called _____ stock.A. dual classB. cumulativeC. deferredD. preferredE. common5. Payments made by a corporation to its shareholders, in the form of either cash, stock or payments in kind, are called:A. retained earnings.B. net income.C. dividends.D. redistributions.E. infused equity. 6. The constant dividend growth model is:A. generally used in practice because most stocks have a constant growth rate.B. generally used in practice because the historical growth rate of most stocks is constant.C. generally not used in practice because most stocks grow at a non constant rate.D. generally not used in practice because the constant growth rate is usually higher than the required rate of return.E. based on the assumption Dow 30 represents a good estimate of the market index.7. The constant dividend growth model:I. assumes that dividends increase at a constant rate forever.II. can be used to compute a stock price at any point of time.III. states that the market price of a stock is only affected by the amount of the dividend.IV. considers capital gains but ignores the dividend yield.A. I onlyB. II onlyC. III and IV onlyD. I and II onlyE. I, II, and III only8. The underlying assumption of the dividend growth model is that a stock is worth:A. the same amount to every investor regardless of their desired rate of return.B. the present value of the future income which the stock generates.C. an amount computed as the next annual dividend divided by the market rate of return.D. the same amount as any other stock that pays the same current dividend and has the same required rate of return.E. an amount computed as the next annual dividend divided by the required rate of return.9. Assume that you are using the dividend growth model to value stocks. If you expect the market rate of return to increase across the board on all equity securities, then you should also expect the:A. market values of all stocks to increase, all else constant.B. market values of all stocks to remain constant as the dividend growth will offset the increase in the market rate.C. market values of all stocks to decrease, all else constant.D. stocks that do not pay dividends to decrease in price while the dividend-paying stocks maintain a constant price.E. dividend growth rates to increase to offset this change.10. Latcher's Inc. is a relatively new firm that is still ina period of rapid development. The company plans on retaining all of its earnings for the next six years. Seven years from now, the company projects paying an annual dividend of $.25 a share and then increasing that amount by 3% annually thereafter. To value this stock as of today, you would most likely determine the value of the stock _____ years from today before determining today's value.A. 4B. 5C. 6D. 7E. 811. The Robert Phillips Co. currently pays no dividend. The company is anticipating dividends of $0, $0, $0, $.10, $.20, and $.30 over the next 6 years, respectively. After that, the company anticipates increasing the dividend by 4% annually. The first step in computing the value of this stock today, is to compute the value of the stock when it reaches constant growth in year:A. 3B. 4C. 5D. 6E. 7 12. Differential growth refers to a firm that increases its dividend by:A. three or more percent per year.B. a rate which is most likely not sustainable over an extended period of time.C. a constant rate of two or more percent per year.D. $.10 or more per year.E. an amount in excess of $.10 a year.13. The total rate of return earned on a stock is comprised of which two of the following?I. current yieldII. yield to maturityIII. dividend yieldIV. capital gains yieldA. I and II onlyB. I and IV onlyC. II and III onlyD. II and IV onlyE. III and IV only14. Fred Flintlock wants to earn a total of 10% on his investments. He recently purchased shares of ABC stock at a price of $20 a share. The stock pays a $1 a year dividend. The price of ABC stock needs to _____ if Fred is to achieve his 10% rate of return.A. remain constantB. decrease by 5%C. increase by 5%D. increase by 10%E. increase by 15%15. The Scott Co. has a general dividend policy whereby it pays a constant annual dividend of $1 per share of common stock. The firm has 1,000 shares of stock outstanding. The company:A. must always show a current liability of $1,000 for dividends payable.B. is obligated to continue paying $1 per share per year.C. will be declared in default and can face bankruptcy if it does not pay $1 per year to each shareholder on a timely basis.D. has a liability which must be paid at a later date should the company miss paying an annual dividend payment.E. must still declare each dividend before it becomes an actual company liability.16. The value of common stock today depends on:A. the expected future holding period and the discount rate.B. the expected future dividends and the capital gains.C. the expected future dividends, capital gains and the discount rate.D. the expected future holding period and capital gains.E. None of the above.17. The closing price of a stock is quoted at 22.87, with a P/E of 26 and a net change of 1.42. Based on this information, which one of the following statements is correct?A. The closing price on the previous day was $1.42 higher than today's closing price.B. A dealer will buy the stock at $22.87 and sell it at $26 a share.C. The stock increased in value between yesterday's close and today's close by $.0142.D. The earnings per share are equal to 1/26th of $22.87.E. The earnings per share have increased by $1.42 this year.18. A stock listing contains the following information: P/E 17.5, closing price 33.10, dividend .80, YTD% chg 3.4, and net chg - .50. Which of the following statements are correct given this information?I. The stock price has increased by 3.4% during the current year.II. The closing price on the previous trading day was $32.60.III. The earnings per share are approximately $1.89. IV. The current yield is 17.5%.A. I and II onlyB. I and III onlyC. II and III onlyD. III and IV onlyE. I, III, and IV only19. The discount rate in equity valuation is composed entirely of:A. the dividends paid and the capital gains yield.B. the dividend yield and the growth rate.C. the dividends paid and the growth rate.D. the capital gains earned and the growth rate.E. the capital gains earned and the dividends paid. 20. The net present value of a growth opportunity, NPVGO, can be defined as:A. the initial investment necessary for a new project.B. the net present value per share of an investment in a new project.C. a continual reinvestment of earnings when r < g.D. a single period investment when r > g.E. None of the above.21. Angelina's made two announcements concerning its common stock today. First, the company announced that its next annual dividend has been set at $2.16 a share. Secondly, the company announced that all future dividends will increase by 4% annually. What is the maximum amount you should pay to purchase a share of Angelina's stock if your goal is to earn a 10% rate of return?A. $21.60B. $22.46C. $27.44D. $34.62E.$36.0022. How much are you willing to pay for one share of stock if the company just paid an $.80 annual dividend, the dividends increase by 4% annually and you require an 8% rate of return?A. $19.23B. $20.00C. $20.40D. $20.80E.$21.6323. Lee Hong Imports paid a $1.00 per share annual dividend last week. Dividends are expected to increase by 5% annually. What is one share of this stock worth to you today if the appropriate discount rate is 14%? A. $7.14 B. $7.50 C. $11.11 D. $11.67 E.$12.2524. Majestic Homes' stock traditionally provides an 8% rate of return. The company just paid a $2 a year dividend which is expected to increase by 5% per year. If you are planning on buying 1,000 shares of this stock next year, how much should you expect to pay per share if the market rate of return for this type of security is 9% at the time of your purchase? A. $48.60 B. $52.50 C. $55.13 D. $57.89 E.$70.0025. Leslie's Unique Clothing Stores offers a common stock that pays an annual dividend of $2.00 a share. The company has promised to maintain a constant dividend. How much are you willing to pay for one share of this stock if you want to earn a 12% return on your equity investments? A. $10.00 B. $13.33 C. $16.67 D. $18.88 E.$20.0026. Martin's Yachts has paid annual dividends of $1.40, $1.75, and $2.00 a share over the past three years, respectively. The company now predicts that it will maintain a constant dividend since its business has leveled off and sales are expected to remain relatively constant. Given the lack of future growth, you will only buy this stock if you can earn at least a 15% rate of return. What is the maximum amount you are willing to pay to buy one share today? A. $10.00 B. $13.33 C. $16.67 D. $18.88 E.$20.0027. The common stock of Eddie's Engines, Inc. sells for $25.71 a share. The stock is expected to pay $1.80 per share next month when the annual dividend is distributed. Eddie's has established a pattern ofincreasing its dividends by 4% annually and expects to continue doing so. What is the market rate of return on this stock? A. 7% B. 9% C. 11% D. 13% E.15%28. The current yield on Alpha's common stock is 4.8%. The company just paid a $2.10 dividend. The rumor is that the dividend will be $2.205 next year. The dividend growth rate is expected to remainconstant at the current level. What is the required rate of return on Alpha's stock? A. 10.04% B. 16.07% C. 21.88% D. 43.75% E. 45.94%29. Martha's Vineyard recently paid a $3.60 annual dividend on its common stock. This dividend increases at an average rate of 3.5% per year. The stock is currently selling for $62.10 a share. What is the market rate of return? A. 2.5% B. 3.5% C. 5.5% D. 6.0% E.9.5%30. Bet'R Bilt Bikes just announced that its annual dividend for this coming year will be $2.42 a share and that all future dividends are expected to increase by 2.5% annually. What is the market rate of return if this stock is currently selling for $22 a share? A. 9.5% B. 11.0% C. 12.5% D. 13.5% E.15.0%31. Shares of common stock of the Samson Co. offer an expected total return of 12%. The dividend is increasing at a constant 8% per year. The dividend yield must be: A. -4%. B. 4%. C. 8%. D. 12%. E.20%.32. The common stock of Grady Co. had an 11.25% rate of return last year. The dividend amount was $.70 a share which equated to a dividend yield of 1.5%. What was the rate of price appreciation on the stock? A. 1.50% B. 8.00% C. 9.75% D. 11.25% E. 12.75%g = .1125 - .015 = .0975 = 9.75%33. Weisbro and Sons' common stock sells for $21 a share and pays an annual dividend that increases by 5% annually. The market rate of return on this stock is 9%. What is the amount of the last dividend paid by Weisbro and Sons? A. $.77 B. $.80 C. $.84 D. $.87 E.$.8834. The common stock of Energizer's pays an annual dividend that is expected to increase by 10% annually. The stock commands a market rate of return of 12% and sells for $60.50 a share. What is the expected amount of the next dividend to be paid on Energizer's common stock? A. $.90 B. $1.00 C. $1.10 D. $1.21 E.$1.3335. The Reading Co. has adopted a policy ofincreasing the annual dividend on its common stock at a constant rate of 3% annually. The last dividend it paid was $0.90 a share. What will the company's dividend be in six years? A. $0.90 B. $0.93 C. $1.04 D. $1.07 E.$1.1136. A stock pays a constant annual dividend and sells for $31.11 a share. If the dividend yield of this stock is 9%, what is the dividend amount? A. $1.40 B. $1.80 C. $2.20 D. $2.40 E.$2.8037. You have decided that you would like to own some shares of GH Corp. but need an expected 12% rate of return to compensate for the perceived risk of such ownership. What is the maximum you are willing to spend per share to buy GH stock if the company pays a constant $3.50 annual dividend per share? A. $26.04 B. $29.17 C. $32.67 D. $34.29 E.$36.5938. Turnips and Parsley common stock sells for$39.86 a share at a market rate of return of 9.5%. The company just paid its annual dividend of $1.20. What is the rate of growth of its dividend? A. 5.2% B. 5.5% C. 5.9% D. 6.0% E.6.3%39. B&K Enterprises will pay an annual dividend of $2.08 a share on its common stock next year. Last week, the company paid a dividend of $2.00 a share. The company adheres to a constant rate of growth dividend policy. What will one share of B&K common stock be worth ten years from now if the applicable discount rate is 8%? A. $71.16 B. $74.01 C. $76.97 D. $80.05 E.$83.2540. Wilbert's Clothing Stores just paid a $1.20 annualdividend. The company has a policy whereby the dividend increases by 2.5% annually. You would like to purchase 100 shares of stock in this firm but realize that you will not have the funds to do so for another three years. If you desire a 10% rate of return, how much should you expect to pay for 100 shares when you can afford to buy this stock? Ignore trading costs. A. $1,640 B. $1,681 C. $1,723 D. $1,766 E. $1,810P 3 = $17.66; Purchase cost =100 $17.66 = $1,76641. The Merriweather Co. just announced that it will pay a dividend next year of $1.60 and is establishing a policy whereby the dividend will increase by 3.5% annually thereafter. How much will one share beworth five years from now if the required rate of return is 12%? A. $21.60 B. $22.36 C. $23.14 D. $23.95 E.$24.79P 5 = $22.3642. The Bell Weather Co. is a new firm in a rapidlygrowing industry. The company is planning onincreasing its annual dividend by 20% a year for the next four years and then decreasing the growth rate to 5% per year. The company just paid its annualdividend in the amount of $1.00 per share. What is the current value of one share if the required rate of return is 9.25%? A. $35.63 B. $38.19 C. $41.05 D. $43.19 E. $45.81Dividends for the first 4 years are: $1.20, $1.44, $1.728, and $2.0736.43. The Extreme Reaches Corp. last paid a $1.50 per share annual dividend. The company is planning on paying $3.00, $5.00, $7.50, and $10.00 a share over the next four years, respectively. After that thedividend will be a constant $2.50 per share per year. What is the market price of this stock if the market rate of return is 15%? A. $17.04 B. $22.39 C. $26.57 D. $29.08 E.$33.7144. Can't Hold Me Back, Inc. is preparing to pay its first dividends. It is going to pay $1.00, $2.50, and $5.00 a share over the next three years, respectively. After that, the company has stated that the annual dividend will be $1.25 per share indefinitely. What is this stock worth to you per share if you demand a 7% rate of return? A. $7.20 B. $14.48 C. $18.88 D. $21.78 E.$25.0645. NU YU announced today that it will begin paying annual dividends. The first dividend will be paid next year in the amount of $.25 a share. The following dividends will be $.40, $.60, and $.75 a share annually for the following three years, respectively. After that, dividends are projected to increase by 3.5% per year. How much are you willing to pay to buy one share of this stock if your desired rate of return is 12%? A. $1.45 B. $5.80 C. $7.25 D. $9.06 E.$10.5846. Now or Later, Inc. recently paid $1.10 as an annual dividend. Future dividends are projected at $1.14, $1.18, $1.22, and $1.25 over the next four years, respectively. After that, the dividend is expected to increase by 2% annually. What is one share of this stock worth to you if you require an 8% rate of return on similar investments? A. $15.62 B. $19.57 C. $21.21 D. $23.33 E.$25.9847. The Red Bud Co. just paid a dividend of $1.20 a share. The company announced today that it will continue to pay this constant dividend for the next 3 years after which time it will discontinue payingdividends permanently. What is one share of this stock worth today if the required rate of return is 7%? A. $2.94 B. $3.15 C. $3.23 D. $3.44 E.$3.6048. Bill Bailey and Sons pays no dividend at the present time. The company plans to start paying an annual dividend in the amount of $.30 a share for two years commencing two years from today. After that time, the company plans on paying a constant $1 a share dividend indefinitely. Given a required return of 14%, what is the value of this stock? A. $4.82 B. $5.25 C. $5.39 D. $5.46 E.$5.5849. The Lighthouse Co. is in a downsizing mode. The company paid a $2.50 annual dividend last year. The company has announced plans to lower the dividend by $.50 a year. Once the dividend amount becomes zero, the company will cease all dividendspermanently. The required rate of return is 16%. What is one share of this stock worth? A. $3.76 B. $4.08 C. $4.87 D. $5.13 E.$5.3950. Mother and Daughter Enterprises is a relatively new firm that appears to be on the road to great success. The company paid its first annual dividend yesterday in the amount of $.28 a share. The company plans to double each annual dividend payment for the next three years. After that time, it is planning on paying a constant $1.50 per share indefinitely. What is one share of this stock worth today if the market rate of return on similar securities is 11.5%? A. $9.41 B. $11.40 C. $11.46 D. $11.93 E. $12.43Dividends for the next three years are $.56, $1.12, and$2.24.51. BC ‘n D just paid its annual dividend of $.60 a share. The projected dividends for the next five years are $.30, $.50, $.75, $1.00, and $1.20, respectively. After that time, the dividends will be held constant at $1.40. What is this stock worth today at a 6% discount rate? A. $20.48 B. $20.60 C. $21.02 D. $21.28 E.$21.4352. Beaksley, Inc. is a very cyclical type of business which is reflected in its dividend policy. The firm pays a $2.00 a share dividend every other year. The last dividend was paid last year. Five years from now, the company is repurchasing all of the outstanding shares at a price of $50 a share. At an 8% rate of return, what is this stock worth today? A. $34.03 B. $37.21 C. $43.78 D. $48.09 E.$53.1853. Last week, Railway Cabooses paid its annual dividend of $1.20 per share. The company has been reducing the dividends by 10% each year. How much are you willing to pay to purchase stock in this company if your required rate of return is 14%? A. $4.50 B. $7.71 C. $10.80D. $15.60E.$27.0054. Nu-Tek, Inc. is expecting a period of intense growth and has decided to retain more of its earnings to help finance that growth. As a result it is going to reduce its annual dividend by 10% a year for the next three years. After that, it will maintain a constant dividend of $.70 a share. Last month, the company paid $1.80 per share. What is the value of this stock if the required rate of return is 13%? A. $6.79 B. $7.22 C. $8.22 D. $8.87 E.$9.0155. The Double Dip Co. is expecting its ice cream sales to decline due to the increased interest in healthy eating. Thus, the company has announced that it will be reducing its annual dividend by 5% a year for the next two years. After that, it will maintain a constant dividend of $1 a share. Two weeks ago, the company paid a dividend of $1.40 per share. What is this stock worth if you require a 9% rate of return? A. $10.86 B. $11.11 C. $11.64 D. $12.98 E.$14.2356. Which of the following amounts is closest to what should be paid for Overland common stock? Overland has just paid a dividend of $2.25. These dividends are expected to grow at a rate of 5% in the foreseeable future. The required rate of return is 11%. A. $20.45 B. $21.48 C. $37.50 D. $39.38 E. $47.70Value of stock = D 0(1 + g)/(r - g) = $2.25(1 + 0.05)/(0.11 - 0.05) = $39.37557. What would be the maximum an investor should pay for the common stock of a firm that has no growth opportunities but pays a dividend of $1.36 per year? The next dividend will be paid in exactly 1 year. The required rate of return is 12.5%. A. $9.52 B. $10.88 C. $12.24 D. $17.00E. None of the above $1.36/.125 = $10.8858. Mortgage Instruments Inc. is expected to paydividends of $1.03 next year. The company just paid a dividend of $1. This growth rate is expected to continue. How much should be paid for Mortgage Instruments stock just after the dividend if the appropriate discount rate is 5%. A. $20.00 B. $21.50 C. $34.75 D. $50.00 E. $51.50g = (D 1 - D 0)/D 0 = ($1.03 - $1.00)/$1.00 = 0.03 (g = 3%)Value of stock = D 1/(r - g) = $1.03/(0.05 - 0.03) = $51.5059. The Felix Corp. projects to pay a dividend of $.75 next year and then have it grow at 12% for thefollowing 3 years before growing at 8% indefinitely thereafter. The equity has a required return of 10% in the market. The price of the stock should be ____. A. $9.38 B. $17.05 C. $41.67 D. $59.80 E. $62.38Value of stock = [($.75/1.1) + ($.84/(1.1)2) +($.94/(1.1)3) + ($1.05/(1.1)4) + (($1.13/.02)/(1.1)4) = $41.67Chapter 09 - Stock Valuation9-1160. If a company paid a dividend of $0.40 last month and it is expected to grow at 7% for the next 6 years and then grow at 4% thereafter, the dividend expected in year 8 is ___. A. $0.63 B. $0.65 C. $0.68 D. $0.69 E. $0.74Div 8 = $.4*(1 + .07)6 (1.04)2 = $.6561. The Lory Company had net earnings of $127,000 this past year. Dividends of $38,100 were paid. The company's equity was $1,587,500. If Lory has 100,000 shares outstanding with a current marketprice of $11.625 per share, and the growth rate is 5.6%, what is the required rate of return? A. 4.2% B. 6% C. 9% D. 14%E. None of the aboveR = Div/P 0 + g = (.381(1.056))/11.625) + .056 = (.40/11.625) + .056 = .0346 + .056 = .0906 = 9% 62. Doctors-On-Call, a newly formed medical group, just paid a dividend of $.50. The company's dividend is expected to grow at a 20% rate for the next 5 years and at a 3% rate thereafter. What is the value of the stock if the appropriate discount rate is 12%? A. $8.08 B. $11.17 C. $14.22 D. $17.32 E. $30.90Years 1-5: ($.50(1.2)t /(1.12)t + (1.28/.09)/(1.12)5 = $11.1763. A stock you are interested in paid a dividend of $1 last week. The anticipated growth rate in dividends and earnings is 20% for the next year and 10% the year after that before settling down to a constant 5% growth rate. The discount rate is 12%. Calculate the expected price of the stock. A. $17.20 B. $17.90 C. $18.20 D. $19.40 E. $19.75Price = $1.00(1.20)/1.12 + $1.20(1.100)/1.2544 + [$1.32(1.05)/(.12 - .05)]/1.2544 = $17.9064. A stock you are interested in paid a dividend of $1 last month. The anticipated growth rate in dividends and earnings is 25% for the next 2 years before settling down to a constant 5% growth rate. The discount rate is 12%. Calculate the expected price of the stock. A. $15.38 B. $20.50 C. $21.04 D. $22.27 E. $26.14Price = $1.00(1.25)/1.12 + $1.25(1.25)/1.2544 + [$1.5625(1.05)/(.12 - .05)]/1.2544 = $21.0465. Which of the following values is closest to the amount that should be paid for a stock that will pay a dividend of $10 in one year and $11 in two years? The stock will be sold in 2 years for an estimated price of $120. The appropriate discount rate is 9%. A. $114.60 B. $119.43 C. $124.20 D. $129.50 E. $138.75Value of stock = D 1/(1 + r) + (D 2 + P 2)/(1 + r)2 = $10/(1 + 0.09) + ($11 + $120)/(1 + 0.09) 2 = $119.43。

《公司理财》斯蒂芬A.罗斯

• There are two dimensions:

1. A Time Frame

• Short run is probably anything less than a year. • Long run is anything over that; usually taken to be a

two-year to five-year period.

2. A Level of Aggregation

• •

McGraw-Hill/Irwin

Each division and operational unit should have a plan.

As the capital-budgeting analyses of each of the firm’s divisions are added up, the firm aggregates these small projects as a big project.

McGraw-Hill/Irwin

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved.

3-6

Sales Forecast

• All financial plans require a sales forecast. • Perfect foreknowledge is impossible since

3-0

Chapter Three

Long-Term FCinoarpnocriaatel Finance

Planning and Growth Ross • Westerfield • Jaffe

公司理财第九章

McGraw-

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights

Key Concepts and Skills

• Decision Rule – Accept if the payback period is less than some preset limit

9-11

Computing Payback for the Project

• Assume we will accept the project if it pays back within two years.

9-15

Computing Discounted Payback for the Project

• Assume we will accept the project if it pays back on a discounted basis in 2 years. • Compute the PV for each cash flow and determine the payback period using discounted cash flows

9-10

Payback Period

• How long does it take to get the initial cost back in a nominal sense? • Computation

– Estimate the cash flows – Subtract the future cash flows from the initial cost until the initial investment has been recovered

英文版罗斯公司理财习题答案chap009.doc