国内贸易信用保险条款

安联财产保险(中国)有限公司安联国内贸易信用保险(全球融资保单)条款-中文版

4.01 营业额的申报 4.02 保险费的计算 4.03 保险费的缴付 4.04 抵销权

5. 其它规定

5.01 您的投保单以及告知义务 5.02 保单货币 5.03 查验您的文件 5.04 保密 5.05 保险期间 5.06 违约 5.07 通讯

5/16

5.08 法律、仲裁和语言 6/16

- 您或供应商与买方之间,与原合同项 下的义务相关,并导致买方拒绝支付 您任何欠款;

- 您和供应商之间; - 您和进口保理商或出口保理商之间。

自负额 是指任何适用于保单的免赔额或起赔额。

保理协议 假如您是一家保理公司,经授权根据您本 国的法律从事保理业务,保理协议是指以 下任何一份协议: - 任何由您和供应商签订的具有法律效

营业额 营业额是指,在特别条款规定的保险期间 内,您根据保理协议从供应商或出口保理

商处购买的,或者是您卖给进口保理商的 应收账款的全部发票价值。

等待期 是指特别条款规定的相关期限,该期限自 我们收到完整的逾期欠款通知以及我们所 要求的其他文件或信息之日起开始计算。

4/16

1. 承保范围

1.01 您所获得的保障 1.02 除外责任

承保损失 是指逾期欠款通知书内所列的承保欠款的 金额或其经扣减第 3.01 款 (承保损失的 计算) 所列金额后的余额。

承保比例 是指特别条款中列明的比例,在计算赔偿 款项时,承保损失将乘以该比例。

最长延长期限 是指特别条款列明的最长期限,您可以用 该最长期限延长承保欠款的最初付款到期 日。

最长付款期限 是指您与买方合同中约定其支付承保欠款 的最长付款期限。

除非另行明确约定,本保单承保您全部的无追索权的营业额。

保险事故

在保单项下,当买方未能向您支付承保欠款并且发生下列任何一种情况,即构成保险事 故:

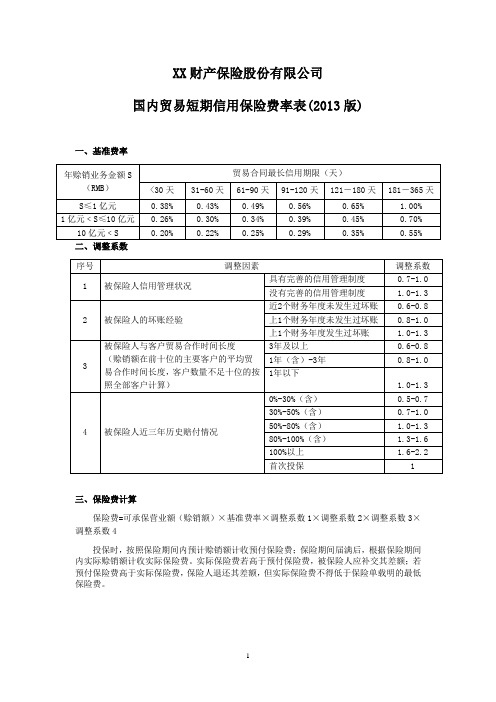

国内贸易短期信用保险条款的费率(2013版) 保险基础知识学习资料 条款产品开发

XX财产保险股份有限公司

国内贸易短期信用保险费率表(2013版)

一、基准费率

二、调整系数

三、保险费计算

保险费=可承保营业额(赊销额)×基准费率×调整系数1×调整系数2×调整系数3×调整系数4

投保时,按照保险期间内预计赊销额计收预付保险费;保险期间届满后,根据保险期间内实际赊销额计收实际保险费。

实际保险费若高于预付保险费,被保险人应补交其差额;若预付保险费高于实际保险费,保险人退还其差额,但实际保险费不得低于保险单载明的最低保险费。

1。

国内短期贸易信用保险的业务流程

国内短期贸易信用保险的业务流程下载温馨提示:该文档是我店铺精心编制而成,希望大家下载以后,能够帮助大家解决实际的问题。

文档下载后可定制随意修改,请根据实际需要进行相应的调整和使用,谢谢!并且,本店铺为大家提供各种各样类型的实用资料,如教育随笔、日记赏析、句子摘抄、古诗大全、经典美文、话题作文、工作总结、词语解析、文案摘录、其他资料等等,如想了解不同资料格式和写法,敬请关注!Download tips: This document is carefully compiled by theeditor.I hope that after you download them,they can help yousolve practical problems. The document can be customized andmodified after downloading,please adjust and use it according toactual needs, thank you!In addition, our shop provides you with various types ofpractical materials,such as educational essays, diaryappreciation,sentence excerpts,ancient poems,classic articles,topic composition,work summary,word parsing,copy excerpts,other materials and so on,want to know different data formats andwriting methods,please pay attention!中国国内短期贸易信用保险的业务流程详解在国际贸易中,短期贸易信用保险是一种重要的风险管理工具,它可以帮助企业在面对买家信用风险时提供保障。

中银保险国内贸易信用保险产品推介

02

CATALOGUE

中银保险国内贸易信用保险产品保障范围

保障货物范围

保障货物范围广泛

中银保险国内贸易信用保险产品保障 的货物范围涵盖了各类商品,包括但 不限于原材料、半成品、制成品等, 满足不同企业的多样化需求。

高价值货物保障

对于价值较高的货物,如贵金属、珠 宝玉石等,中银保险提供专门的保障 方案,确保企业在贸易过程中得到充 分的保障。

风险调整费率

根据被保险人的信用状况 、历史表现和其他风险因 素,对费率进行适当调整 。

附加服务费率

对于一些额外的附加服务 ,如催收、追偿等,会额 外收取一定的服务费用。

报价流程

提交申请

被保险人向中银保险提 交投保申请,包括企业 基本信息、贸易背景和

风险状况等。

风险评估

中银保险对申请进行风 险评估,确定被保险人 的风险等级和费率水平

VS

详细描述

中银保险为某进口企业提供了全面的国内 贸易信用保险方案。根据企业的实际需求 和情况,中银保险量身定制了保障方案, 有效提升了企业的抗风险能力,为企业的 发展提供了坚实的保障。

06

CATALOGUE

中银保险国内贸易信用保险产品的合作渠 道与联系方式

合作渠道介绍

银行渠道

直接销售渠道

中银保险与多家银行合作,通过银行 渠道向企业提供国内贸易信用保险产 品,满足企业在贸易过程中的风险保 障需求。

产品目标客户

国内贸易中的各类企 业,尤其是涉及大宗 商品交易、长期合作 的企业。

对国内贸易信用风险 有较高关注,希望通 过保险手段降低风险 的客户。

需要规避买方或卖方 违约风险,提高贸易 安全性的客户。

产品优势与卖点

专业性强

平安国内贸易信用险保单补充条款-中文-General

B1504–信用额度信用额度可以通过以下方式获得:1. 如被保险人注册使用保险人指定的在线系统,被保险人须向保险人咨询以获得买家的@rating 信用评级。

当被保险人获得买家@rating 信用评级后,该买家的信用额度将按照保险单中相对应的@rating 评级水平以及承保比例决定(但@rating 信用评级为X的除外)。

2. 如被保险人未注册使用保险人指定的在线系统,或被保险人需要申请更高的信用额度,或被保险人买家未被授予@rating信用评级,被保险人必须向保险人申请信用额度。

该信用额度设定保险人承保的金额上限以及任何可能适用的特定条件。

如果保险人授予信用额度的前提是被保险人必须获得担保,被保险人有责任确保此担保有效并能得以执行。

如果被保险人未注册使用保险人指定的在线系统申请信用额度,则须填写《信用额度申请表》申请信用额度。

保险人授予的信用额度属保密信息,被保险人承诺不得将信用额度内容泄漏给任何本合同未提及的第三方。

对本合同提及的人员,被保险人承诺这些人员将为信用额度保密。

3.被保险人首次申请或调整买家@rating信用评级或信用额度时,被保险人必须告知保险人有关买家的任何负面信息以及截止申请日已发生的超过保险单中规定的最长信用期的逾期未付账款。

4. 对于已获得@rating信用评级或信用额度的买家,保险人将提供买家追踪服务。

在作出授信决定后,被保险人被授予的@rating信用评级和信用额度均从保险人收到被保险人申请之日起生效,且其效力和金额在保险人未发出减少或取消信用额度通知的情况下始终有效,但是就信用额度而言,在信用额度通知中另有规定的除外。

保险人拥有拒绝授予、随时降低或取消买家@rating信用评级或信用额度的权利。

如果保险人做出上述决定,这些决定将适用于被保险人收到保险人通知之日起发生的交货或服务。

C 1.02 –全面追偿服务1 –保险人为本合同承保的债款提供追偿服务。

2 –为保险人提供上述服务之目的,被保险人需要在保险单规定的时限内,通知保险人发生逾期欠款,并要求保险人介入。

国内贸易信用保险介绍资料

货物发送信用期限被保险人提供索赔材料齐全后,保险

人在30天内付款

最高延长期

到期日

账款逾期提交索赔申请(最后期限)

逾期/可能损失通知最初到期日

开具发票损失确定日提交索赔申请保单签署最长**天保险责任开始

货物被发送信用保险重要时间节点示意

保险公司将协助被保险人进行及时有效的账款追收并承担相应费用,但不包括被保险人内部管理费用启动企业内部

信控机制,进行账款追收* 最高延长期–按照客户实际情况设定,一般最长不超过60天。

** 损失确定日期:

-无清偿能力–立刻

-延期付款–原始到期日后6个月

Proposal Form

Policy Wording

Credit Limit

Declaration

Claim Form。

国内贸易短期信用保险条款(2013版) (英文) 保险基础知识学习资料 条款产品开发

Short-Term Domestic Trade Credit Insurance Terms & ConditionsEnglishVersion 2013CatalogueContents Page Article 1 Notice 3 Article 2 The Policy 3 Article 3 Losses Covered 3 Article 4 Exclusions 4 Article 5 Contracts Covered 5 Article 6 Commencement of Cover 6 Article 7 Despatch 6 Article 8 Credit Limits 6 Article 9 Compliance with Credit Limit 6 Article 10 Withdrawal by Us 6 Article 11 Declarations 7 Article 12 Risk Premium 7 Article 13 Credit Limit Charges 7 Article 14 Credit beyond the Due Date 7 Article 15 Maximum Extension Period 7 Article 16 No Liability beyond Maximum Extension Period 8 Article 17 Bills of Exchange etc. 8 Article 18 The Proposal and Disclosure of Facts 8 Article 19 Minimising Loss and Obtaining Recoveries 9Contents Page Article 20 Period for Submission and Payment 10 Article 21 Calculation of Loss 10 Article 22 Date of Ascertainment of Loss 10 Article 23 Insurer’s Maximum Liability 10 Article 24 Allocation of Moneys Received and Recoveries 11 Article 25 Assignment of Policy Rights 11 Article 26 Assignment of Contract Rights 11 Article 27 Observance of Stipulations and Confidentiality 12 Article 28 Joint and Several Obligations 12 Article 29 Retained Risk 12 Article 30 Trade Disputes and Third Party Guarantees of Payment 13 Article 31 Misrepresentations or Fraudulent Acts 13 Article 32 Set Off 13 Article 33 Currencies 13 Article 34 Variations of Terms of Cover 14 Article 35 Your Insolvency 14 Article 36 Law, Arbitration and Language 14Chapter 1 General RulesArticle 1 NoticeThe following Notice is incorporated in and made part of this Policy.This is a Short-Term Domestic Trade Credit Insurance Policy. The insurance period under this policy is no more than one year subject to the date of the commencement and date of termination indicated in the Schedule. This Policy has certain provisions and requirements unique to it and may be different from other policies you may have purchased.Please read this Policy carefully.The descriptions in the headings and titles of this Policy are solely for reference and convenience and do not lend any meaning to this agreement.Article 2 The PolicyWe, the Insurer named in the Schedule, have issued this Policy of insurance to you, the Insured named in the Schedule. This Policy includes, without limitation, these General Terms, the Proposal, the Schedule and any endorsements or other documents expressly incorporated thereby and all Credit Limits. This Policy supersedes any previous statement, promise or representation by the parties relating to the agreement or its subject matter. Chapter 2 Insurance CoverageArticle 3 Losses CoveredThe purpose of this insurance is to indemnify you, in accordance with the terms of this Policy, up to the Covered Percentage of any loss you may sustain because of the occurrence of any of the following causes of loss, provided in each case that there is an amount owing from the buyer which shall constitute such loss:A. InsolvencyThe Insolvency of any of your buyers. For the purposes of this Policy "Insolvency"shall occur if:a. a bankruptcy, winding-up or administration order is made against the buyer; orb. the buyer is declared bankrupt by the People’s Court; orc. in the course of execution of a judgment the levy of execution fails to satisfy the debt in full; ord. a valid assignment, composition or other arrangement is made for the benefit of the buyer’s creditors generally according to a decision of the People’s Court; ore. an effective resolution is passed for the winding-up of the buyer; orf. a liquidation committee, an administrative or other receiver or manager of any of thebuyer ’s property is appointed; org. you sh ow, to our satisfaction, that the buyer ’s financial state is such that even partial payment is unlikely and that to enforce judgment or to apply for a bankruptcy or winding-up order would have no foreseeable result other than one disproportionate to the likely cost of the proceedings.h. such situations or events which, in our sole opinion, in substance or effect are equivalent to the situations and events described above.B. DefaultThe failure of a buyer to pay you the amount owing under the contract within 6months of original due date of payment.Chapter 3 ExclusionsArticle 4 The insurer shall not be liable for any loss arising in connection with any of the following:A. Failure by YouWe shall not be liable for any loss you may sustain where there has been any failureby you or by any person acting on your behalf to fulfill any of the terms andconditions of the contract or to comply with the provisions of any law (including any order, decree or regulation having the force of law).B. Radioactive ContaminationWe shall not be liable for any loss directly or indirectly caused by, contributed toby or arising from the ionising, radioactive, toxic, explosive or otherhazardous or contaminating properties or effects of any explosive nuclear assembly or component thereto, nuclear fuel, combustion or waste.C. WarWe shall not be liable for any loss arising directly or indirectly from war (whether before or after the outbreak of hostilities) between any country.D. Interest/penalties/damages/costsWe shall not be liable for any loss you may sustain in respect ofa. any interest accruing after the original due date of payment, orb. any penalties or damages, whether contractual or otherwise, which you may be entitled to be paid by the buyer in addition to the amount owing, orc. any costs, legal or otherwise, which you incur in pursuing payment of any amount owing where the buyer claims for any reason whatsoever to be justified in withholding payment of all or part thereof or in defending any proceedings brought against you, ord. any costs, legal or otherwise, which you incur in establishing the validity and enforceability of a guarantee of payment or surety, obtaining a final enforceablejudgement and enforcing the guarantee or surety in a court, where we have made this a condition of cover, ore.. any banking costs, unless contractually agreed to be part of the amount owing from the buyer.E. Other InsuranceWe shall not be liable for any loss you may sustain where such loss is (or would bebut for the existence of this Policy) capable of being covered by any other insurance held by you.or from which you may be entitled to benefit or receive paymentF. Non-acceptance of goodsWe shall not be liable for any loss you may sustain where the buyer has failed or refused to accept good despatched. However, if such failure or refusal is in breach ofthe contract, this exclusion shall not apply.G. State or Government actionWe shall not be liable for any loss arising from any decision taken by a State or government department, local authority or any entity which cannot be declared insolvent that either hinders execution of the contract or prevents payment.H. Natural DisasterWe shall not be liable for any loss directly or indirectly caused by, contributed to by or arising from cyclone, flood, earthquake, volcanic eruption or tidal wave or otherforms of natural disaster or force majeure.Chapter 4 Contracts covered and Commencement of CoverArticle 5Contracts CoveredThe Policy applies to all contracts you make with buyers in your country inconnection with your Trade as specified in the Schedule. Contracts must be true,legally effective, binding and in writing. They must also specify the nature andquantity of the goods to be sold (or the services to be performed), as well as the termsof payment, which must not exceed the Maximum Credit Terms specified in the Schedule. Unless we agree otherwise in writing, the Policy does not apply to:a. any contracts you make with buyers over whom you have direct or indirect controlor in whom you have a direct or indirect interest or who have such control over or interest in you or where there is any family relationship or there exists any loans or guarantees between you and the buyer, either directly or indirectly;b. any contracts you make with private individuals, sole proprietorships or partnerships;c. any contracts you make with state or governmental departments, local authorities, institutions or organisations or any entity which cannot be declared insolvent;d. trial/approval contracts or to sales from consignment stock.Article 6 Commencement of CoverRisk shall attach in respect of those contracts for which cover commences during the Policy Period specified in the Schedule. Cover commences when the goods are despatched or, in the case of services, when each invoice for services performed is submitted to the buyer. Invoices for goods despatched or services performed must be submitted to the buyer within the Invoicing Period specified in the Schedule. This Invoicing Period commences on the day of despatch of such goods or, in the case of services, on the date when the contract is made.Article 7 DespatchDespatch is deemed to be made when you, or anyone acting on your behalf, parts with possession of the goods for the purpose of transmitting them to the buyer in accordance with the terms and conditions of the contract.Chapter 5 The Credit Limit and Withdrawal of CoverYou must have a Credit Limit for every buyer. In the event of a claim, we will not be liable to pay more than the Covered Percentage, specified in the Schedule, of the Credit Limit.Article 8 Credit LimitsYou may obtain a Credit Limit from us. The amount shall be determined from us at our discretion and shall be approved on the terms and conditions we think appropriate. Those terms and conditions may vary any provision of the Policy. Credit Limits from us remain valid until expiry of the Policy Period unless we cancel them or renew the Policy.Article 9 Compliance with Credit LimitWe shall not be liable for any loss where you have not complied with the terms and conditions of the Credit Limit.Article 10 Withdrawal by UsWe may at any time and for any reason by written notice to you cancel any CreditLimit and withdraw cover in respect of any contract or buyer. The policy will notapply in relation to goods despatched or, in the case of services, to invoices submitted,on or after the date specified in the notice. We may also at any time and for any reasonby written notice to you reduce any Credit Limit and such reduction shall apply inrelation to any goods despatched or, in the case of services, to invoices submitted, on or after the date specified in the notice.Chapter 6 Declarations, Premium and ChargesArticle 11 DeclarationsYou must declare to us the sale price (net of Value Added Tax or other similar tax) in respect of all goods despatched or services invoiced under contracts to which the policy applies. Where appropriate, a nil declaration must be submitted. Declarations must be returned to us by the time specified in the Schedule.Article 12 Risk PremiumPremium is payable, together with any applicable Insurance Premium Tax or other similar tax, in relation to each contract to which the policy applies. Premium is calculated at the percentage rate specified in the Schedule in respect of the amount of business declared. Payment of premium must be made at the times we specify.Article 13 Credit Limit ChargesWe shall also charge you (at the rates specified in the Schedule, which we may vary from time to time) for each response, decision and yearly review we give in respect of Credit Limits from us. Payment of all charges must be made at the times we specify.Chapter 7 Credit Beyond Due DateArticle 14 Credit beyond the Due DateYou may, if the need arises, allow credit to run for a period beyond the due date of payment specified in the contract with the buyer, or agree in writing to an extension of due date, provided that the period or extension you allow or agree is not longer thanthe Maximum Extension Period specified in the Schedule. If the buyer fails to pay infull by the expiry of the first such period or extension that you allow or agree, youmust not allow or agree to any further period or extension unless we agree otherwisein writing. You must not agree in the contract itself to any term which provides for the due date to be extendedArticle 15 Maximum Extension PeriodThe Maximum Extension Period commences on the day after the original due date of payment and ends on the expiry of either:(a) the number of calendar days specified as the Maximum Extension Period in the Schedule or(b) if shorter, the period or extension you allow or agree. We may vary the Maximum Extension Period by written notice at any time.Article 16 No liability beyond Maximum Extension PeriodIf payment of any amount is overdue from a buyer at the expiry of the Maximum Extension Period, we shall not be liable for any loss you may sustain in relation to goods despatched or in the case of services, to invoices submitted, to that buyer after that date, unless we agree otherwise in writing.Article 17 Bills of Exchange etc.Unless you obtain our prior written agreement, the granting of credit beyond due date is not permitted in the case of bills of exchange, promissory notes, cash against documents, documentary sight draft, documents against payment transactions or wherever payment is to be made out of a letter of credit.Chapter 8 Obligations of the InsuredArticle 18 The Proposal and Disclosure of FactsA. The Proposal for this insurance is incorporated into this Policy as its basis. You must have disclosed, and continue at all times to disclose promptly, all facts which might affect the risks insured. If you intentionally conceal any relevant facts which might affect our risk assessment, or otherwise grossly negligently fail to fulfill your obligation to make a full and accurate disclosure in answer to any questions contained in the Proposal and such concealment or failure adversely affects our underwriting decisions or premium rate assessment, we shall be entitled to avoid the policy and we shall not be liable for any loss you may sustain.B. As soon as it comes to your notice, you must immediately inform us of any substantial or material change in the information given in the proposal form, particularly in the nature or scope of your activities or in your own legal status.C. You undertake to allow us to exercise the right of discovery for checking and verifying that you have fulfilled all your obligations under this Policy. Where we so require, you must also cooperate with a certified auditor or other independent party that we may employ to certify the accuracy of the information and documents you have provided.D. You must disclose promptly and will at all times continue to disclose promptly all information and documents which might affect the risks insured under this Policy ormight influence our acceptance or assessment of the risks and Buyers insured under this Policy.Article 19 Minimising Loss and Obtaining RecoveriesA. NotificationYou must notify us immediately of the occurrence of any event likely to cause a loss. Such an event shall include, without limitation:a. the failure of a buyer to pay any amount still overdue 20 calendar days after the expiry of the Maximum Extension Period; orb. a buyer requesting an amendment of payment terms which is unfavourable to you or an extension of due date beyond the expiry of the Maximum Extension Period; orc. a buyer failing to take up the goods or the documents on first presentation where the payment terms are cash against documents or documents against acceptance; ord. the imminent or actual Insolvency of a buyer; ore. your having reason to believe that a buyer is unable or is likely to be unable to perform or comply with the terms of the contract; orf. the failure of a buyer to honour a bill of exchange or a cheque; org. the institution of any proceedings against a buyer for non-payment of an amount owing.B. Due Care & DiligenceYou must use due care and diligence and take all practicable measures to prevent and minimize loss. This includes, without limitation, ensuring that all rights against the contract goods, buyers and third parties are properly preserved and exercised.C. Taking All StepsYou must take all steps that we may require in connection with a potential or actual loss, including, without limitation, the institution of legal proceedings and such steps,if any, as may be specified in the Schedule. If we require it you must assign to us all rights against the contract goods, buyers or third parties or appoint us as your agent or attorney with power in your name to take legal proceedings or to appoint any personfor the purposes of collection of amounts owing. If you recover the contract goods and, with our prior written approval, resell them, any shortfall between the amount realised on resale and the amount owing from the buyer will be taken into accountwhen calculating your loss.D. InformationYou must provide us with all information and documents that we may require.E. Contributions to your Costs and ExpensesWe will contribute towards costs and expenses that you properly and reasonably incurin fulfilling the above obligations. Our contribution will be proportionate to ourliability for your total loss, including any uninsured portion, or for what such losswould have been but for your action in fulfilling the above obligations. However, wewill not contribute towards your administrative costs and expenses. We will also not contribute (without prejudice to any other rights we may have) to the costs and expenses of collecting any amount owing if you have chosen not to place thecollection of the amount as we may propose or as may be required in the Schedule.F. Failure to complyIf you fail to comply with any of the provisions of this Article after we have made a payment, then you will be liable to refund the payment to us on first written demand. Chapter 9 ClaimsArticle 20 Period for Submission and PaymentClaims (including all available information) must be made within 6 months of the expiry of the Maximum Extension Period, using the form we will provide. Provided that we are satisfied that we are liable to make payment, we will pay you the Covered Percentage either of the amount of your loss or of the Credit Limit for the buyer, whichever is less. We will make such payment no more than 30 days from either the date of receipt of all the information and documents we require or, if later, the date of ascertainment of loss.Article 21 Calculation of LossWe will calculate the amount of your loss as being the amount owing to you from the buyer less (i)any amount which, at the date of ascertainment of loss, you or the buyerare entitled to credit to the buyer ’s account whether by way of payment, set-off, counterclaim, deduction or otherwise and (ii)any expenses which you have saved. Article 22 Date of Ascertainment of LossThe amount of your loss shall be ascertained on the date of ascertainment of loss which shall be as follows:a. for Insolvency, on the day when Insolvency occurs;b. for Default, 6 months after original due date of payment.Article 23 Insurer ’s Maximum LiabilityThe maximum amount which we shall be liable to pay in respect of all contracts taken together for which our liability commences during the Policy Period shall be the amount of the Insurer ’s Maximum Liability shown in the Schedule for that period,notwithstanding that such amount may be less than the Covered Percentage of any individual Credit Limit or aggregate of Credit Limits.Article 24 Allocation of Moneys Received and RecoveriesA. Allocations by Chronological OrderAll amounts whenever received, in connection with any contracts (including contracts not covered by this Policy) shall, for the purposes of this Policy, be applied toamounts owing under all your contracts with the same buyer in chronological order of due dates. If such amounts fall to be applied to amounts owing under a contract on which we have paid a claim, they must be remitted to us and until this remittance is made you receive and hold such amounts in trust for us.B. RecoveriesAll sums whatsoever received, recovered or realised whether by you, by any person acting on your behalf, or by us in relation to a contract after the date of ascertainmentof loss shall be Recoveries. All Recoveries shall immediately be remitted to us. Untilthis remittance is made you receive and hold Recoveries in trust for us. After receiptby us Recoveries will be divided in the proportion in which the loss is borne by eachof us.C. Failure to complyIf you fail to comply with any of the provisions of this Article after we have made a payment, then you will be liable to refund the payment to us on first written demand. Chapter 10 MiscellaneousArticle 25 Assignment of Policy RightsLoss PayeeYou cannot assign or transfer this policy or any of its benefits without our priorwritten consent. You may, however, require claims payments to be made to a namedloss payee, using the form we will provide, your obligations under the policy remaining unaffected.Article 26 Assignment of Contract RightsYou may assign or charge your rights under the contract provided this does not contravene the contract terms and you give us details when making a claim. However, we shall not be liable to pay you for any loss unless: (a) you can show that you, not the person in whose favour the assignment or charge has been made, have sustained such loss and (b) that person has given us a written undertaking in a form acceptable to us that hewill not make any claim to our portion of any Recoveries.Article 27 Observance of Stipulations and ConfidentialityA. Due payment of all premiums and other charges and the due performance and observance of every stipulation in the policy or the proposal shall be your obligation. In the event of any breach of any condition we, according to the relevant stipulations of Insurance Law of the People’s Republic of China,also have the right to retain any premium paid and terminate the Policy from the date of our written notice to you. No variation or waiver relating to any stipulation of the policy shall be binding unless we have specifically agreed the same in writing.B. No failure by you to comply with any of the stipulations of this Policy shall be deemed to have been accepted or excused by us unless the same is expressly so excused or accepted by us in writing. The waiver by us of any breach or default by you in respect of any of the stipulations of this Policy shall not be construed as a waiver of any succeeding breach or default in respect of the same or any other stipulation.C. You must treat any information provided to you in strict confidence and you must not disclose such information to any third party. We shall not be liable for any loss which might arise from third parties gaining access to confidential information. All information, including but not limited to Credit Limit Decisions, is non-binding. We shall not be liable for any loss you may sustain where you use this information, especially for your own commercial decisions.D. If you fail to observe your obligations or stipulations of this insurance contract, and this would have had essential influence on the occurrence of loss or the amount of our liability, your right of indemnification will be forfeited. In such cases we also have the right to terminate the policy with immediate effect, unless otherwise stipulated by laws of the People’s Republic of China.E. You must not disclose the existence of this Policy to any buyer, whether insured or not. Article 28 Joint and Several ObligationsThe obligations of the persons named as the Insured in the Schedule shall be joint and several.Article 29 Retained RiskYou must retain exclusively for your own account as an uninsured risk any amount which exceeds the amount we are liable to pay you under the policy.Article 30 Trade Disputes and Third Party Guarantees of PaymentA. Trade DisputesWe shall not ascertain loss so long as a buyer claims for any reason whatsoever thathe is justified in withholding payment of all or part of an amount owing or in not performing any of his obligations under the contract.B. Third Party Guarantees of PaymentWhere we have made it a condition of cover that there be a guarantee or surety, weshall not ascertain loss until a final judgement for the amount owing has beenobtained against that guarantor or surety in a court in the country specified in such condition.Article 31 Misrepresentations or Fraudulent ActsAny misrepresentation with gross negligence which is material to the risk, or non-disclosure of information, or fraudulent conduct on your part (or on the part of any other person who has a legal or beneficial interest in the policy or its proceeds), in relation to this Policy (including the proposal), to any claim under it, or to any contract to which the Policy applies, will render the Policy void but we may retain any earned premium paid and you will be liable to refund to us any payment we may have made under the Policy unless otherwise stipulated by laws of the People’s Republic of China.Article 32 Set OffWe have the right to apply any amount payable under this policy in or towards payment of any amount owing from you to us (paying interest before principal) whether under this policy or otherwise. You have no right to apply any amount payable by you to us, whether under this policy or otherwise, in or towards payment of any amount owing from us to you.Article 33 CurrenciesA. The policy shall be denominated in the currency specified in the Schedule, which currency shall be used for the purpose of making declarations, paying premium and calculating the amount of any loss. Where you contract in a currency other than the denominated currency, a conversion to the equivalent amount in the denominated currency shall be made using the exchange rate on the last working day of the month during which cover commenced.B. Recoveries, if received in another currency, shall be converted to the denominatedcurrency at the exchange rate on the date of receipt by you or by any person acting onyour behalf.C. The exchange rate on a given date shall be the closing mid-point rate quoted on that date by the People’s Bank of China or, if the rate has not been quoted, such rate on the next succeeding date when the rate is quoted.Article 34 Variations of Terms of CoverWe have the right at any time to vary by written notice any of the provisions of the Policy in respect of contracts made with buyers insured under this Policy. The variation will apply to goods despatched or (in the case of services), to invoices submitted, after the date which will be specified in the notice (not being earlier than the date of the notice).Article 35 Your InsolvencyThe Policy shall terminate automatically with immediate effect if:a. a bankruptcy, winding-up or administration order is made against you; orb. an effective resolution is passed for your winding-up; orc. a liquidation committee, an administrative or other receiver or manager of any of your property is appointed; ord. a valid assignment, composition or other arrangement is made for the benefit of your creditors generally.Article 36 Law, Arbitration and LanguageA. The Policy shall be governed by and construed in accordance with the Law of the People’s Republic of China and subject to the jurisdiction of the arbitral tribunal established in accordance with sub-clause B below.B. All disputes arising under, out of or in connection with this Policy, including without limitation disputes as to its formation and validity, and whether arising during or after the Policy Period, which have not been settled amicably by negotiation between the Parties shall be submitted to China International Economic and Trade Arbitration Commission (CIETAC) for arbitration. The arbitration shall take place at the Place of Arbitration specified in the Schedule. The arbitration shall be conducted in accordance with the CIETAC’s arbitration rules in effect at the date of applic ation for arbitration. The arbitration award shall be final and binding on both parties.C. The Language of Policy shall be that specified in the Schedule. Where we provide translations of the Policy the version in the Language of Policy shall prevail in the event of any conflict or difference in meaning or effect.。

大地保险国内贸易信用险条款

大地保险国内贸易信用险条款鉴于投保人愿意根据本保险单的规定,向保险人支付保险费,保险人同意按本保险单的规定,承担赔偿责任,特此订立保险合同如下:第一条保险合同的构成1. 保险单或其他保险凭证、条款、费率表和其他有关文件。

2. 保险费的缴纳及保险期限的确定,应按照本合同及其他有关保险条款的有关规定。

第二条被保险人被保险人应是具有中华人民共和国国籍,且与投保人签订了国内贸易合同并已支付货款的单位或个人。

第三条保险标的保险标的是指国内贸易合同中约定的货物。

第四条保险责任保险人承担下列损失赔偿责任:1. 因债务人不能或不愿履行贸易合同义务而造成被保险人的直接损失;2. 被保险人因贸易合同违约或欺诈而遭受的全部损失和费用;3. 被保险人因追讨欠款而发生的费用,包括律师费、诉讼费等。

第五条除外责任对于下列损失和费用,保险人不承担赔偿责任:1. 战争、暴乱、恐怖袭击等不可抗力因素导致的损失;2. 被保险人或其代表的故意行为或重大过失导致的损失;3. 核辐射、核爆炸、核污染及其他放射性污染导致的损失;4. 其他不属于保险责任范围内的损失和费用。

第六条赔偿处理1. 当发生本保险责任范围内的损失时,被保险人应及时向保险人报告,并提供必要的索赔文件。

如果被保险人未能及时报告或提供必要的索赔文件,保险人有权拒绝赔偿。

2. 在赔偿过程中,被保险人应积极配合保险人的调查和核实工作。

如果被保险人未能配合调查核实工作,保险人有权拒绝赔偿。

3. 赔偿金额应根据贸易合同约定的金额、实际损失金额、追讨欠款费用等因素确定。

如果实际损失金额高于贸易合同约定的金额,保险人只负责赔偿贸易合同约定的金额。

4. 如果被保险人在一个保单年度内多次发生本保险责任范围内的损失,保险人的赔偿责任以本保险单中列明的每次事故赔偿限额为限。

5. 赔偿时,被保险人应提供必要的索赔文件和资料,如贸易合同、商业发票、货运单据、付款凭证、仲裁裁决书或法院判决书等。

如果被保险人未能提供必要的索赔文件和资料,保险人有权拒绝赔偿。

国内贸易短期信用险

应收帐款管理

中期

后期

• 案例1 – – – • 案例2 – –

保单周期末的年赊销总额:人民币8000万 增付保费: (8000万 x 0.42% - 168,000) = 人民币168,000

保单期末年赊销总额: 人民币3000万 保险公司保留最低保费, 不予退回.

国内贸易短期信用保险的主要内容

• 赔款支付

根据以下条件支付赔款:

• •

• • • •

☆保单管理简便:被保险人只需每季度末申报营业总额,无需申报买家明细营业额。 ☆待交付订单条款:如果保险人决定降低或取消买方的额度,在满足以下条件时,保险人对 自通知之日起三个月内被保险人必须对该买方履行的发货或服务义务继续提供保障:

1. 规定发货或提供服务的销售合同是在保险人通知之日前6个月之内签订。 2. 被保险人在保险人通知后的8天内书面要求保险人核准所有上述的发货或提供的服务。 3. 如果被保险人已经或应该向保险人发出买家的逾期欠款通知,则该买家丌在本保障范围内。 如果保险人要求被保险人停止对相关买家发货或提供服务,保险人将承担被保险人因重新出 售而导致的损失,在无特别说明的情冴下,对该损失的最高赔偿金额为在原核定信用额度内, 以发票金额的50%为限。

国内贸易短期信用保险的主要内容

• 信用额度 • 投保人为每个买家申请信用额度,信用额度的数额为在 任一时点投保人给予买方的最高帐面放帐总额

• 保险人为每一赊销买家批复一个信用额度:此额度为本保单 针对此买家的承保限额。 • 所有批复的信用额度均可循环使用,被保险人在保险期间可 根据实际情冴提出的其买家信用额度的变更

保单一年一签

国内贸易短期信用保险的优势____产品优势

• • • ☆ 最长信用期限条款:被保险人可根据自己对买家的判断,自主决定在此期限 内延长信用期限或提出索赔申报。该架构能在保障被保险人索赔时效的基础上,又给予被保 险人维护好客户关系的自由度 ☆ 全面追偿服务:一旦发生索赔,只要在等待期内,保险人协劣收回的任何款项都是先还给 被保险人,冲减损失金额,然后按照债款余额(即净损失)理赔,即使被保险人超出信用额 度交易也是如此。 这样能最大程度地利用保险的催收工作,降低损失。

《国内贸易信用保险投保单》

国内贸易信用保险投保单请您仔细阅读保险条款,尤其是黑体字标注部分的条款内容,并听取保险公司业务人员的说明,如对保险公司业务人员的说明不明白或有异议的,请在填写本投保单之前向保险公司业务人员进行询问,如未询问,视同已经对条款的内容完全理解并无异议。

中国出口信用保险公司:遵照贵公司《国内贸易信用保险》条款规定,并在出具以下申报、要求和保证的基础上,我公司特向贵公司提出投保国内贸易信用保险的申请。

请贵公司审核承保, 并及时通知我公司承保条件及费率。

填写说明:1.对于多项选择的,请投保人在适合的“□”内打“√”。

2.如表中预留空间不够填写,可另附页具体说明,该附页同样需要投保人法人代表签字并加盖投保人公章。

3.除特别说明外,本调查表采用的货币为人民币、单位为元。

一、投保人基本情况公司名称(中文):公司名称(英文):注册地址:营业地址:组织机构代码:工商注册号:邮政编码:企业类型:经营性质:行业信息:是否上市公司:成立时间:注册资本:股份结构:股东名称:占比:股东名称:占比:股东名称:占比:主营产品或服务:是否从事出口:如是,开始出口年份:电话:传真:电子信箱:公司网址:法人代表姓名:职务:电话:委托代理人姓名:职务:电话:电子信箱:主要联系人姓名:职务:电话:电子信箱:姓名:职务:电话:电子信箱:关联公司:二、投保人内部管理情况(一)信用风险管理体系1、是否设有信用管理部门?[]是[]否2、信用管理部门是否独立于销售部门、财务部门?[]是[]否3、谁有权利批准与买方采用信用销售及信用销售条件?4、批准与买方采用信用销售模式的主要依据?(请在适合的[ ]内打“√”)[]与买方以往的合作关系[]买方的财务信息[]银行信息[]资信报告[]其他说明其他说明描述:5、在销售合同中是否约定物权保留条款?[]全部约定[]部分约定[]否6、对于买方拖欠到期应付款的处理是否有成文的规定?[]是 []否无论是否成文规定,对拖欠是否有以下安排:1、停止供货:拖欠天后停止供货2、追讨:[]自行追讨 []委托第三方追讨追讨的频率、负责人员,以及追讨过程要求文件如下描述:3、拖欠天后诉诸法律(二)通过有关质量体系认证(三)信用保险投保情况三、投保人业务情况(以含税金额填列)(一)投保人业务总体情况(二)投保人最近完整年度主要产品或服务情况(三)收帐款余额(非关联公司国内买方)1、应收帐款余额范围分析(截止至年月底)2.前12个月按月末账龄分析(365天以内应收账款)(截止至年月底)(四)非关联公司国内买方逾期应收账款分析 填制要求:拖欠原因请选择下述代码填写:A=破产,B=技术性拖欠,C=习惯性拖欠,D=恶意拖欠,E=贸易纠纷,F=其他,请具体填写。

安联财产保险(中国)有限公司国内贸易信用保险(短期B款)条款

被保险人可以同意一次或多次延长承保欠款的最初付款到期日。然而,额外给予的信用期限的总和不 得超过特别条款规定的最长延长期限。除非保险人同意,保单不承保任何被保险人已经同意延期至最 长延长期限以后的欠款。 除非被保险人获得保险人事先的书面同意,在下列情况下,被保险人不得延长到期日: (a) 如果初始的付款方式是凭单付现、本票、汇票或者不可撤销信用证;或

到期日后的应收款项 2.05 被保险人的信用管理义务 在任何时候,被保险人都必须如同没有被保险一样行事。所以被保险人必须采取一切合理的措施 来预防和/或减少损失,包括但不限于:

7 / 25

本

-

启动法律诉讼, 执行任何判决, 启动针对买方的破产程序;以及 将欠款交由特别条款列明的商账管理服务方(如有)处理,被保险人同意其费用由被保险人支付。

安联财产保险(中国)有限公司 国内贸易信用保险(短期 B 款)条款

样

1 / 25

本

保险条款的内容 1. 承保范围 1.01 被保险人所获得的保障 1.02 除外责任 风险管理 设定和修改信用限额 2.01 注意和谨慎义务 2.02 限额申请 2.03 自定信用限额项下的承保责任 2.04 承保责任的修改和撤销 到期日后的应收款项 2.05 被保险人的信用管理义务 2.06 到期日的延长 2.07 逾期欠款及保险事故通知 赔偿款项 3.01 承保损失的计算 3.02 赔偿款项的计算 3.03 赔偿款项的支付 3.04 追偿款 3.05 最高责任限额 3.06 赔偿款项的转让 3.07 风险分担 3.08 诉讼时效 保单管理 4.01 营业额的申报 4.02 保险费的计算 4.03 保险费的缴付 4.04 抵销权 其他规定 5.01 被保险人的投保单及告知义务 5.02 保单货币 5.03 查验被保险人的文件 5.04 保密 5.05 保险期间 5.06 违约 5.07 通讯 5.08 法律、仲裁和语言 核准的信用限额 买方 凭单付现 逾期欠款确定日 发送 自定信用限额 争议 自负额 4 4 4 6 6 6 6 7 7 7 7 8 8 9 9 9 9 10 11 11 11 11 12 12 12 12 12 13 13 13 13 13 14 14 14 14 16 16 16 16 16 16 16 16 17

贸易信用险基础知识(资料一)_396

Payment Debt Payment Amount

付款

债务 付款

债务总额

650

650

1,000

1,650

1,650

300 1,650 300

1,350

600

2,250 300

1,950*

650 2,250 950

1,300

1,000 2,250 1,950

300

650

2,900 1,950

赔款金额:1,000,000 x 90% =人民币 900,000

平安国内贸易短期信用保险的主要内容

赔款支付(全面追偿服务优势举例)

我司是根据追不回来的应收账款余额在批复的信用额 度范围内赔付的,举例说明如下:

如在一信用期限内,投保人向A买家发了3次货,第一次赊销额 是50万,第二次赊销额是100万,第三次赊销额是100万,应收账款 此时余额是250万,此时第一次发货的发票50万到期了,但是买家不 付款,投保人要停止再向客户发货,并向我司报案。假设A买家我司 批复的信用额度是100万, 情形一:我司在5个月全面追偿期内部分追回了100万,会把这100万 还给客户,并按此时应收账款余额150万,在我司批复的信用额度内 理赔,即赔付100*90%=90万; 情形二:我司在5个月全面追偿期内部分追回了200万,则会把这200 万还给客户,并按此时应收账款余额50万,在我司批复的信用额度内 理赔,即赔付50*90%=45万;

供货后2个月

6,000,000 = 1,000,000 6

申请信用额度=预计年赊销营业额/年周转次数

年周转次数=360/信用期限

信用额度计算方法– 实例二 (最高值法)

(Credit: 2 m. x 放帐期:2个月

平安国内贸易信用险基础知识(资料一)

年周转次数=360/信用期限

信用额度计算方法– 实例二 (最高值法)

(单位:人民币千元)

(Credit: 2 m. x 放帐期:2个月 Accumulated 累计 Outstanding 债务余额

Date 日期 9/01 22/01 7/02 4/03 9/04 18/04 9/05

最低保费: 人民币5000万 x 0.5% x 80% = 200,000 付款时间表:(不需要融资的情况) 第一季度初: 50,000 第二季度初: 50,000 第三季度初: 50,000 第四季度初: 50,000 保险期末

情况1

– – 情况2 保单周期末的年赊销总额:人民币6000万 增付保费: (6000万 x 0.5% - 200,000) = 人民币100,000

平安国内贸易短期信用保险的主要内容 赔款支付时限的图例

• 所有批复的信用额度在保单期限内(一年)可循环使用,被保险人在保险期间可根据实 际情况提出的其买家信用额度的变更 保单签定前对投保前十个买家财务状况和资信情况的调查、评估,并对每一买家批复的 信用额度,是不收取任何费用 保单签定后,会对买家的财务状况和资信情况进行实时监控,如买家情况有变,会及时 做出预警通知,避免应收账款损失;故收取每一买家828元一年的信用额度管理费用。

Transaction 交易 Invoice 8/01 发票 Invoice 21/01 发票 Payment 6/02 付款 Invoice 3/03 发票 Payment 8/04 付款 Payment 17/04 付款 Invoice 8/05 发票

Debt 债务 650 1,000

Payment 付款

平安国内贸易期信用保险介绍 1、承保范围 投保人? 凡在中国境内(不包括香港、澳门和台湾地区)注册的公司 投保的贸易额? 对国内客户(不包括香港、澳门和台湾地区)的赊销额,且 信用期限在4个月内(货出30天内要开出发票或对账单,开出 发票或对账单之日起120天内买家要还款) 承保损失? 投保企业的客户(买家)未付款造成的损失(包括恶意拖欠 及丧失清偿能力) 保险比例:90%

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

中国出口信用保险公司国内贸易信用保险条款本保险单指本《国内贸易信用保险单》,其中包括《投保单》、《保险单明细表》、《批单》、《国内贸易信用保险条款》、《信用限额申请表》及其附表、《信用限额审批单》、《索赔单证明细表》、《委托代理协议书》、《申报单》及其它相关单证。

第一章 适保范围第一条 本保险单适用于在中华人民共和国境内注册的企业进行的符合下列条件的贸易,但寄售除外:(一)贸易合同以书面形式订立,且真实、合法、有效;(二)信用期限不超过本保险单约定的最长信用期限。

第二章 保险责任第二条 在本保险单有效期内,被保险人按贸易合同交付货物或提供服务后,且在《保险单明细表》列明的发票开票期限内开具发票,因下列风险引起的直接损失,在被保险人履行本保险单各项约定的条件下,保险人按本保险单的规定承担保险责任:(一)买方破产或无力偿付债务;(二)买方拖欠。

第三章 除外责任第三条 除非本保险单另有规定,保险人对下列损失不承担赔偿责任:(一)通常可由其它财产保险承保的损失;(二)除买方外,包括被保险人在内的任何其他方的破产或无力偿付债务、违约、欺诈或其它违法行为引起的损失;(三)被保险人知道或应当知道买方负面信息以及本条款第二条项下约定的风险已经发生,或交付货物或提供服务前被保险人依照贸易合同或相关法律的规定有权拒绝履行或中止履行交付货物或提供服务义务,仍继续向买方交付货物或提供服务所遭受的损失;(四)因被保险人或买方未能及时获得各种所需许可证或批准书,致使贸易合同无法继续履行而造成的损失;(五)因国家及地方各级国家机关所颁布的法律、法规、规章、其它规范性文件以及发布的命令、决定等导致贸易合同无法继续履行而造成的损失;(六)因不可抗力导致的损失;(七)被保险人与具有关联关系的主体之间贸易项下发生的损失;(八)被保险人依据法律规定或贸易合同约定应向买方收取的利息、罚息和违约金;(九)本保险单保险责任以外的其它损失。

第四章 责任限额第四条 本保险单责任限额包括最高赔偿限额和信用限额。

第五条 最高赔偿限额是指保险人对本保险单年度有效期内产生的保险责任可能承担赔偿责任的累计最高金额。

该最高赔偿限额在《保险单明细表》中列明。

第六条 信用限额是指保险人对被保险人与适保范围内特定买方的贸易可能承担赔偿责任的最高限额,具体赔偿额应按本保险单约定的赔偿比例计算。

(一)被保险人应向保险人书面申请买方信用限额。

(二)对被保险人提出的买方信用限额申请,保险人将批复结果以《信用限额审批单》形式通知。

(三)批复的信用限额对其生效日后的相应货物交付或服务提供有效。

该限额在本保险单有效期内除特别注明外均可循环使用。

(四)当风险发生重大变化时,保险人有权调整或撤销信用限额,并书面通知被保险人。

(五)信用限额如有调整,则同一买方的原信用限额自动失效,保险责任余额自动归于调整后的信用限额内。

(六)自被保险人提交《可能损失通知书》之日起,该买方的信用限额自动被撤销。

(七)保险人对信用限额的调整或撤销适用于调整或撤销生效日之后的货物交付或服务提供,不影响此前保险人已承担的保险责任。

第五章 申 报第七条 被保险人应按照《保险单明细表》列明的申报方法,以保险人规定的格式申报适保范围内的全部贸易。

第八条 保险人对被保险人未按本保险单规定申报的贸易不承担赔偿责任。

第六章 保险费第九条 保险人按《保险单明细表》列明的方式计算并收取保险费。

被保险人未在规定期限内足额交纳保险费,保险人对被保险人申报的相关贸易有权拒绝承担赔偿责任。

如果保险人书面催交保险费通知送达之日起30日内被保险人仍未足额交纳保险费的,保险人有权解除本保险单,并书面通知被保险人,本保险单自该通知送达被保险人之日起解除。

本保险单项下被保险人已交纳的所有保险费不予退还。

该解除不影响解除日前保险人按照本保险单规定应承担的保险责任。

第七章 索 赔第十条 被保险人知道或应当知道本保险单条款第二条项下风险发生时,应按以下时限向保险人提交《可能损失通知书》:(一)买方破产或无力偿付债务风险发生之日起10日内;(二)买方拖欠情况下最迟应不超过最长信用期限截止日后的10日内。

被保险人提交《可能损失通知书》是索赔的前提条件。

被保险人未能在本保险单规定期限内提交《可能损失通知书》,导致案情无法查明、损失扩大或其它影响保险人利益的情形,保险人有权降低赔偿比例直至拒绝承担赔偿责任。

第十一条 被保险人提交《可能损失通知书》后收回的任何欠款和其它权益,应在收到欠款和其它权益后10日内书面通知保险人。

第十二条 被保险人应在提交《可能损失通知书》后90日内向保险人索赔,并提交《索赔申请书》及《索赔单证明细表》列明的相关文件和单证等能够证明损失发生的文件。

超过上述期限,保险人有权降低赔偿比例直至拒绝承担赔偿责任,但事先经保险人书面同意的除外。

被保险人提交的索赔单证不全而又未能按保险人要求提交补充文件的,保险人有权拒绝受理索赔申请。

被保险人向保险人请求赔偿的诉讼时效期间为二年,自其知道或者应当知道本保险单承保范围内的损失发生之日起计算。

第十三条 在受理被保险人的索赔申请后,对拖欠案件,保险人应在120日内核实损失原因,并将核赔结果书面通知被保险人。

对买方破产或无力偿付债务案件,在保险人收到法院确认被保险人破产债权书面文件及证明破产债权成立的所有文件或事先经保险人书面同意的情况下,保险人应在30日内核实损失原因,并将核赔结果书面通知被保险人。

在符合保险单最高赔偿限额约定的前提下,保险人对保险责任范围内的损失,按照核定损失金额与信用限额从低原则确定赔付基数。

该赔付基数在任何情况下不超过发票金额。

保险人赔付金额为赔付基数与本保险单约定赔偿比例的乘积。

保险人应在做出赔付决定后30日内支付赔款,但支付赔款的前提是保险人收到被保险人签署的《赔款收据及权益转让书》及《委托代理协议书》。

第十四条 对有付款担保或存在纠纷的情况,保险人定损核赔的原则是:(一)对有付款担保的贸易合同,除非保险人书面认可,在担保人按担保协议付款以前,或在被保险人申请仲裁或向法院提起诉讼,并获得已生效的仲裁裁决或法院可执行判决并申请执行之前,保险人不予定损核赔;(二)若存在纠纷,除非保险人书面认可,被保险人应先进行仲裁或诉讼,在获得已生效的仲裁裁决或法院可执行判决并申请执行之前,保险人不予定损核赔;(三)上述发生的诉讼费、仲裁费和律师费由被保险人先行支付,在被保险人胜诉且损失属本保险单项下责任时,该费用由保险人与被保险人按权益比例分摊,否则,由被保险人自行承担。

第十五条 保险人在本保险单第十三条规定的时间内,对保险责任已确定,但赔付金额不能确定的案件,应当根据已有证明和资料对可以确定的数额先予支付赔款;保险人最终确定赔付金额后,支付相应的差额。

第十六条 保险人定损核赔时,应扣除下列款项:(一)买方已支付、已抵销,及被保险人未经保险人书面同意擅自降价、放弃债权的部分或接受买方反索赔的款项;(二)被保险人已通过其它途径收回的相关款项和其它权益,包括但不限于转卖货物或变卖抵押物所得的款项及担保人支付的款项;(三)被保险人已从买方获得的其它款项和其它权益;(四)其它不合理的款项或费用。

第八章 追 偿第十七条 被保险人提交《可能损失通知书》后,应委托保险人进行追偿或按照保险人的指示自行追偿,否则保险人有权降低赔偿比例直至拒绝承担赔偿责任。

第十八条 在被保险人委托保险人追偿或按照保险人的指示自行追偿的情况下,如查明被保险人所受损失属于赔偿责任,保险人与被保险人按照各自权益比例分摊追偿费用;如查明被保险人的损失不属于保险人的赔偿责任,追偿费用由被保险人承担。

第十九条 保险单约定的风险发生后,无论被保险人与买方是否有特别约定,除非保险人书面同意,买方或担保方对被保险人的任何付款和付出的权益均被视为按时间顺序偿还保险项下被保险人对该买方的应收账款。

第二十条 在保险人赔付后,被保险人应将赔款所涉及的贸易合同项下的权益转让给保险人。

对赔款金额外的欠款,除非保险人书面同意,被保险人应授权保险人代为追偿,并提供相应的授权文件。

在保险人赔付后,从买方或担保方收回的任何款项和其它权益,保险人按照本保险单项下各自的权益比例与被保险人分摊追偿费用和追回款。

如果被保险人及其代理人从买方或担保方追回或收到任何款项或其它权益,在与保险人分摊之前,视为代保险人保管。

被保险人应在收到上述款项后15个工作日内将保险人应得部分退还保险人。

第二十一条 保险人赔付后出现下列情况时,被保险人应在收到保险人退款要求后10日内退还保险人已支付的赔款及相关利息:(一)保险人发现被保险人与买方存在付款担保或贸易纠纷,或被保险人未遵守最大诚信原则,存在欺诈行为或与买方有恶意串通行为;(二)被保险人收到赔款后,未经保险人书面同意又接受退货、同意折扣,或未经保险人书面同意与买方达成还款或和解协议;(三)由于被保险人原因致使保险人不能完全或部分行使代位求偿权;(四)保险人查明致损原因不属于本保险单保险责任范围。

第九章 被保险人义务第二十二条 被保险人应认真审查贸易合同,经常检查贸易合同的执行情况,切实做好应收账款催收工作。

在知道或应当知道买方负面信息以及本保险单条款第二条项下任一风险发生时,应立即以书面形式通知保险人,同时被保险人应及时采取一切必要措施,包括但不限于及时在相关法院或机构登记债权,以避免或减少损失。

第二十三条 被保险人不得就本保险单项下适保范围内的贸易向其他机构投保信用保险。

第二十四条 在本保险单有效期内,如被保险人的公司名称、股权结构、经营范围等,与被保险人告知保险人的内容发生变化,被保险人应于变化发生日起10日内书面通知保险人。

第二十五条 被保险人有义务协助保险人行使调查权利。

被保险人应提供任何与贸易合同有关的文件和经核实的副本,并允许保险人进行相关调查,包括核实被保险人是否履行合同义务,是否向保险人全面、准确、真实地进行申报。

第二十六条 保险人赔付后,被保险人仍有义务协助保险人向买方追偿。

第二十七条 被保险人可展延信用期限,但经累计的信用期限不得超过本保险单约定的最长信用期限。

有下列情况之一的,除非经保险人事先书面同意,被保险人不得展延该买方项下信用期限:(一)如果展延后的信用期限超过本保险单约定的最长信用期限;(二)保险人已经撤销该买方信用限额;(三)被保险人知道或应当知道买方负面信息;(四)被保险人已经或应该向保险人提交《可能损失通知书》。

第二十八条 被保险人应按本保险单规定履行其义务。

被保险人未履行应尽的义务而影响保险人利益时,保险人有权降低赔偿比例、拒绝承担赔偿责任或解除本保险单,并不退还已收保险费。

被保险人在本保险单订立及履行过程中,未就与本保险相关事项进行如实告知的,保险人有权解除本保险单,但应在得知解除事由之日起三十日内行使解除权。