国际税收(讲义苏州大学 罗正英)

《国际税收一》演示文稿1

(三)国际税收的两个基本要素

1、国际税收涉及的所得税纳税人 2、国际税收涉及的直接税的征税对象

1、国际税收涉及的所得税纳税人

(1)作为国际税收涉及的纳税人,必须是跨国的自 然人和法人 ;

(2)作为国际税收涉及的纳税人,必须在两个或两 个以上国家负有双重交叉纳税义务。

凡有来源于两个或两个以上国家的收入,或 有存在于两个或两个以上国家的财产,或者虽然 只有来源于一个国家的收入,但是却在两个或两 个以上国家同时负有双重交叉纳税义务的跨国自 然人或法人,都是国际税收涉及的纳税人。

⑴国际税收涉及的所得税的征税对象 ①跨国一般经常性所得 ②跨国超额所得 ③跨国资本利得 ④跨国其他所得

⑴跨国一般经常性所得 跨国一般经常性所得,是指跨国纳税人在通常情况下可

以经常获得的跨国所得。 ①经营所得,即营业利润; ②劳务所得; ③投资所得; ④租赁所得; ⑤其他所得。

⑵跨国超额所得 跨国超额所得,是指跨国纳税人所取得的超过一般经常性所得 标准的那部分跨国所得。 ⑶跨国资本利得 跨国资本利得,是指跨国纳税人通过出售或交换房屋、机器设 备、股票、债券、商誉、商标和专利权等一些资本项目所得到 的毛收入,从中减去购入价格后的那一部分差额。 ⑷跨国其他所得 跨国其他所得,是指除上述三类跨国所得以外的某些非经常性 的跨国所得。

合同的第一段明确规定CBS唱片公司聘用原告提供排他性 的服务。

合同第三段要求原告每年为该公司录制一定数量的唱片。 最重要的是合同第四段表明CBS认为原告的服务是该合同 的核心内容:原告承诺性合同有效期内不为他人录制类似的唱 片。 合同第五段规定:唱片一经灌制,由CBS拥有全部所有权, 原告和其他当事人不得提出任何权利要求。 最后,依合同第13段规定,CBS唱片公司有权中止或终结 支付费用,“如果由于疾病,伤痛或罢工原因,你不能依协议 条款为我方履行义务。”

苏大导师

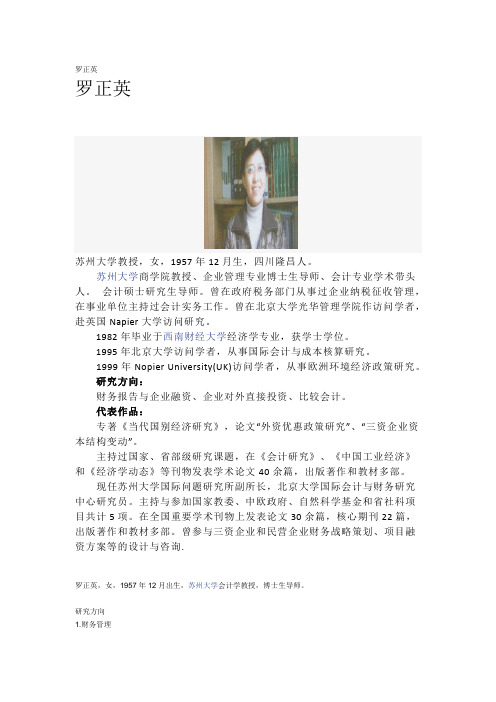

罗正英罗正英苏州大学教授,女,1957年12月生,四川隆昌人。

苏州大学商学院教授、企业管理专业博士生导师、会计专业学术带头人。

会计硕士研究生导师。

曾在政府税务部门从事过企业纳税征收管理,在事业单位主持过会计实务工作。

曾在北京大学光华管理学院作访问学者,赴英国Napier大学访问研究。

1982年毕业于西南财经大学经济学专业,获学士学位。

1995年北京大学访问学者,从事国际会计与成本核算研究。

1999年Nopier University(UK)访问学者,从事欧洲环境经济政策研究。

研究方向:财务报告与企业融资、企业对外直接投资、比较会计。

代表作品:专著《当代国别经济研究》,论文“外资优惠政策研究”、“三资企业资本结构变动”。

主持过国家、省部级研究课题,在《会计研究》、《中国工业经济》和《经济学动态》等刊物发表学术论文40余篇,出版著作和教材多部。

现任苏州大学国际问题研究所副所长,北京大学国际会计与财务研究中心研究员。

主持与参加国家教委、中欧政府、自然科学基金和省社科项目共计5项。

在全国重要学术刊物上发表论文30余篇,核心期刊22篇,出版著作和教材多部。

曾参与三资企业和民营企业财务战略策划、项目融资方案等的设计与咨询.罗正英,女,1957年12月出生,苏州大学会计学教授,博士生导师。

研究方向1.财务管理著作(1)《中小企业融资问题研究》(专著),经济科学出版社2004年出版(2)《国别经济研究》(专著),中国建材工业出版社1999年出版(3)《区域经济:双圈联动发展战略分析——兼论江苏省区域经济发展》(第一作者),上海交通大学出版社2007年出版(4)《会计学原理——建立企业会计信息平台》(第二作者),北京大学出版社2007出版(5)《成本会计》(主编),高等教育出版社2007年出版论文(1)“中小企业信贷融资战略重点提升”《中国工业经济》2004年第4期(2)“中小企业融资结构选择的内生性约束模型研究”《会计研究》2006年第8期(3)“信誉链:中小企业融资的关联策略”《会计研究》2003年第7期(4)“中小企业融资战略的国际比较与经验启示”《经济学动态》2003年第11期(5)“中小企业会计信息披露制度特征、结构与实现机制” 《会计研究》2004年第8期(6)“县域政府在农业产业结构调整中的作用”《中国农村经济》2004年第12期(7)“股权结构的形成及其有效性分析” 《经济科学》2002年第3期(8)“我国中小企业信贷融资可获性特征研究——基于苏州地区中小企业财务负责人的观点”《上海经济研究》2005年第3期(9)“中小企业的企业家风险厌恶、财富集中度与融资结构研究”《上海经济研究》2006年第9期(被人大复印资料“乡镇企业、民营经济”2006年第12期所收录)(10)“东西部区域经济联动发展研究”《西部发展》2003年第5期(11)“信誉链假说:中小企业融资能力放大” 《上海经济研究2003年第5期(12)增长极与区域经济增长的外向带动”《江南大学学报(人文社会科学版)》2003年第2期(13)“上市公司信息披露诚信机制的建立与完善”《会计研究》2002年第8期(14)“我国环境会计的现状与趋势” 《当代经济科学》2002年增刊(15)“以差异缩小差距:论地区经济的协调发展”《经济问题探索》2002年第12期(16)“需求导向型会计信息披露制度特征与条件”《四川会计》2002年第12期(17)“中国环境会计发展趋势”《财会月刊》2001年11期(18)“国际直接投资自由化过程中的外资政策选择”《江汉论坛》2001年8期(19)“试论盘活城市土地的意义与途径” 《河南师范大学学报·哲学社会科学版》2000年第1期(20)“改善外商投资环境要有新思路” 《世界经济文汇》2000年第6期课题1、主持国家自然科学基金项目“信贷配给条件下中小企业筹资战略:国际比较与对策研究”(2002——2003)(已结题)。

国际税收学(PPT 269页)

税收管辖权与税种的关系

n 商品税的税收管辖权

n 地域税收管辖权

n 所得税的税收管辖权

n 综合所得税制下:居民(公民)管辖权和(或)地 域管辖权

n 分类所得税制下:单一的地域管辖权

n 财产税的税收管辖权

n 一般财产税 :居民(公民)管辖权和/或地域管辖 权

n 特别财产税 :单一的地域管辖权

PPT文档演模板

n 在常设机构不能提供准确凭证据以计算扣除营 业费用时,可以采取这种方法确定常设机构利 润。

PPT文档演模板

国际税收学(PPT 269页)

开放经济条件下的国际税收问题

n 跨国纳税人和跨国课税对象 n 国际税收协调和国际税收分配

PPT文档演模板

国际税收学(PPT 269页)

跨国纳税人和跨国课税对象

n 跨国纳税人指在两个或两个以上国家同 时负有纳税义务的个人或经济组织。

n 跨国课税对象,则是指两个或两个以上 国家都享有征税权的课税对象。跨国课 税对象主要包括跨国所得、跨国商品流 转额和跨国一般财产价值。

石场等; n 建筑工地,建筑、装配或安装工程,或者与其

有关的监督管理活动,但应连续超过一定期限, 一般为六个月或一年; n 有雇员或其他非独立代理人(包括本企业的子 公司)经常代表本企业从事营业活动。

PPT文档演模板

国际税收学(PPT 269页)

构成常设机构的场所的基本条件

n 是场所。 如房屋、场地或机器设备等设施;没有规模上 的限制;也不论是自有的还是租用的。

国际税收学(PPT 269页)

公民/居民税收管辖权的确立

n 公民纳税人的确定标准 n 居民纳税人的确定标准

PPT文档演模板

国际税收学(PPT 269页)

西财《国际税收》教学资料 教学课件 第一章

目录

30

第一章 导论

3.对所得的征税 对所得的征税包括对一般经常性所得、超额所得、其他所得

和财产收益等方面的征税。 对跨国纳税人来说,其所得往往来源于几个国家。出于维护

各自税收权益的目的,有关国家都要对所涉及的跨国纳税人的所 得行使税收管辖权,由此发生了国际重复征税。

2021年12月5日星期日

目录

2021年12月5日星期日

目录

21

(三)国际税收与涉外税收

1.国际税收与涉外税收的联系

二者均体现本 国政府与外国 纳税人和本国 政府与具有国 际收入的本国 纳税人之间的 税收分配关系。

第一章 导论

各国涉外税收制度的 理论与实务是国际税 收这门学科形成的基 础,而国际税收既是 各国涉外税收在国际 关系上的反映,又是 各国涉外税收的延伸 和扩展。

首先,纳税人 的所得不象古 老直接税的征 税对象那样要 受土地固定在 一个国家疆域 范围以内的限 制。

其次,纳税人的所得 也不象间接税的征税 对象商品流转额那样, 有着明确的交易行为 起点和终点所在国的 概念,不会发生

有关国家政府对跨国 的商品流转额重叠交 叉征税问题。

2021年12月5日星期日

目录

2021年12月5日星期日

目录

17

第一章 导论

国际税收的概念:国际税收是指两个或两个以上的国家政府

凭借其各自的政治权力,在对跨国纳税人的跨国所得或财产进行

重叠交叉课税而形成的征纳关系中,所发生的国家之间的税收分

配关系。

甲国

税收分配关系

乙国

跨国纳税人

国际税收分配关系示意图

2021年12月5日星期日

目录

国际税收

第一章 导论

国际税收学.1ppt

PPT文档演模板

2020/11/10

国际税收学.1ppt

目录

导言 国家税收管辖权 国际重复课税及其免

除

国际避税与反避税 商品课税的国际协调 涉外税收制度 国际税收协定

PPT文档演模板

国际税收学.1ppt

导言

n 开放经济条件下的国际税收问题 n 国际税收的概念 n 国际税收学的研究对象 n 本书体系与内容安排

n 如果A公司在乙国设有分公司B公司(B公司应 认定为A公司在乙国设立的常设机构),A公司 通过B公司销售电视机,取得营业所得10,000 美元,另外还通过乙国的C公司(C公司与A公 司没有任何附属或控制关系,因此是一家独立 代理人)销售收录机,取得营业所得8,000美 元。

n 按照归属原则,乙国将对归属于B公司的电视 机营业所得10,000美元行使地域管辖权征税; 而按照引力原则,乙国不但可以对归属于B公 司的电视机营业所得10,000美元征税,还可以 对并未通过B公司但与B公司经营同类商品所获 取的收录机营业所得8,000美元一并行使地域 管辖权征税。

n 税收管辖权的原则和类型 n 公民/居民税收管辖权的确立 n 地域税收管辖权的确立

PPT文档演模板

国际税收学.1ppt

税收管辖权的原则和类型

n 税收管辖权的原则 n 税收管辖权的类型 n 税收管辖权的具体实施情况 n 税收管辖权与税种的关系

PPT文档演模板

国际税收学.1ppt

税收管辖权的原则

n 属人原则

PPT文档演模板

国际税收学.1ppt

跨国商品、所得和财产课税中 的重复征税

n 跨国所得课税中的重复征税 对同一纳税人的同一课税对象(例)

n 跨国财产课税中的重复征税 对同一纳税人的同一课税对象(例)

国际税收英文讲义

Chapter 1 Overview of international taxation1.1 the meaning of international taxation1.2 the nomination of international taxation1.3 the development trend of international taxation1.1 the meaning of international taxation1.1.1 What’s international taxation?1.1.2 the attribute of international taxation1.1.3 the connection and difference between international taxation and national taxation1.1.1 what’s international taxation?In generally speaking, international taxation refers to some tax problems and tax environments under the condition of opening economy because of two reasons. First, the taxpayers’ economic activities have expanded to the outside of the boundaries. Second, there exist difference and conflict between the tax laws and regulations in different countries.1.1.2 the attribute of international taxationAs to so much tax environments under the condition of opening economy, the problems of international taxation is in fact referred to the tax relationship between different countries. The tax relationship between countries is just the attribute of international taxation.The tax relationship between countries can be revealed mainly in the next two respects.1. The tax distribution relationship between different countries.2. The tax coordination relationship between different countries.(1) Cooperative coordination(2) non-cooperative coordination1.1.3 the connection and difference between international taxation and national taxationthe difference between international taxation and national taxation is as follows.1.National taxation is a forced collection form based on the state political power, but international taxation is the tax environments and tax relation derived from national tax, which is not a forced collection form meanwhile.2.National tax involves the equity distribution relationship between country and taxpayers, but international taxation involves the tax equity distribution and coordinative relationship between different countries because of the interaction of different countries’ tax systems.3. National tax can be classified as different categories of taxes according to its objects of taxation. As international taxation is not a actual tax form, it has no single categories of taxes.We should pay special attention to the relationship between national tax and international taxation.•We can’t confuse international taxation with foreign tax.•We can’t view the taxes levied on the income within boundary from foreign residents and income outside boundary from domestic residents as international taxation.1.2 the nomination of international taxation1.2.1 the classifications of international taxation1.2.2 the impact of tax to international economic activities1.2.3 the development of international economy and the nomination of international taxation1.2.1 the classifications of international taxation•The classifications of commodity tax2. The classifications of income tax3. The classifications of property taxThe classifications of commodity tax1.Customs duty (the duty levied on the commodities inside and outside boundary or customs frontier of a country)(1) Import duty (the duty levied on the commodities imported)(2) Export duty (the duty levied on the commodities exported)(3) Transit duty (the duty levied on the commodities transited)The classifications of commodity tax2.Internal commodity tax (the tax levied on the commodities or service circulate within country)(1)Sales tax (its concentration is on the business activities of selling commodities and rendering service.)(2)Consumption tax (its concentration is on the consumption activities )The classifications of income tax•Individual income tax(1) The classified income tax system(2) The comprehensive income tax system(3) The mixed income tax system2.Enterprise income tax3.Withholding income taxThe classifications of property tax1.Tax assessed to property owned by taxpayers(1)Specific property tax(2)General property tax (also called wealthy tax)2.Tax assessed to property transferred by taxpayers(1) Gift tax(2) Death tax (①settlement tax; ②inheritance tax)1.2.2 the impact of tax to international economic activities1.The impact of commodity tax to international taxation(1) Customs duty and international trade(2) Internal commodity tax and international trade2. The impact of income tax to international investment(1) The influence to international direct investment(2)The influence to international indirect investment3. The impact of property tax to international investment1.2..3 the development of international economy and nomination of international taxation1.The nomination of international coordination to commodity tax.2. The nomination of international income tax.3. The nomination of international property tax.1.3 the development trend of international taxation1.In the area of commodity tax, the coordination of V AT and consumption tax will gradually substitute for the coordination of customs duty and will become the core of it.2.In the area of income tax, the tax competition between countries will be more violent. In order to prevent fiscal degradation from happening, it is necessary for United Nations to coordinate different countries’ capital income tax system.3.With development of regional international economy integrations, the regional international tax coordination will have more broader future.4.Countries will strengthen their collection and administrative corporation to deal with together transnational taxpayers’ activities for international tax avoidance and tax evasion.5.With the development of electronic commerce, there will be more subjects in area of international taxation which will be settled by countries and international society.New emerging issuance in the area of international taxation with the rapid development of electronic commerce1.Wether the income source country should levy on the operation income of foreign sellers in the electronic transactions?2.There is sometimes, it is difficult to define the characteristics and categories of income in the electronic commerce which bring some difficulties to classify their tax powers between different countries.3.The transnational taxpayers’ activities for international tax avoidance and tax evasion will become more hidden. So it is urgent for international society to make the effective methods of preventing it.Problems of thinking1.What’s the definition of international taxation? What’s its characteristics?2.What’s the relationship between international taxation and national taxation?3.What’s the scope of researching on international taxation?4.What are the impacts of tax to economic activity?5.What’s the developing trend of international taxation in the future?Chapter 2 Jurisdictions of income tax2.1 the types of jurisdictions of income tax2.2 the judgments norms on inhabitant taxpayer2.3 the judgments norms on source places of income2.4 the obligation to pay tax between resident and non-resident taxpayer2.1 the types of jurisdictions of income tax2.1.1 what’s tax jurisdiction?2.1.2 the present conditions of tax jurisdictions in different countries.2.1.1 what’s tax jurisdiction?Tax jurisdiction is the sovereignty of a country in tax, which means the government can decide on whom to levy, what taxes and how much taxes can levied.The principles of personality and dependency⏹The principle of personality means the government can exercise its political power over all of its domestic citizen and residents.⏹The principle of dependency means the government can exercise its political power in its own air space and territory.⏹As to the levy of income tax, according to the principle of dependency, the government has the power to levy on all of income earned within the boundary without considering the person who gets the income is the resident or foreigner. According to the principles of personality and dependency, tax jurisdiction s can be classified into three categories.1.Geographical tax jurisdiction, which is also called source places tax jurisdiction, means the government will exercise its taxing power over all of income earned within its boundary.2.Resident tax jurisdiction means the government can exercise its taxing power over all of income earned by the residents who are specified in its tax law, including natural persons and legal entity.3.Citizen tax jurisdiction means the government will exercise its taxing power over the income earned by the citizen who has its nationality.2.1.2 the present conditions of tax jurisdiction in different countriesSince tax jurisdict ions belong to the state’s sovereignty, every country which owns sovereignty has the power to select the type of tax jurisdiction which is suitable for it based on its own country’s condition.2.2 the judgment norms on inhabitant taxpayer2.2.1 the judgment norms on resident identity of natural persons2.2.2 the judgment norms on resident identity of legal entity2.2.1 the judgment norms on resident identity of natural personsFor natural persons, resident is a counter concept with respect to visitor and travelers. If a man is a resident of a country, he has lived in the country for a long time. He is not a transit traveler who visits or is going to live in the country for a short time.The judgment norms on resident identity of natural person include:1.Domicile norms: it is a concept in civil law which means one’s fixed or permanent living place.2.Residence norms: In practice, residence means generally one’s living place where he has lived for so long time but he is not going to live there permanently.3. Stay time norms: As regulated in so many countries, if a person stays actually in the a country for a long time in excess of the stated time in a fiscal year although he has no domicile or residence in this country, he is viewed also as this countr y’sresident.The difference between domicile and residence1.Domicile is the permanent living place for a person, but residence is only the living place for a person temporally because of some reasons.2.Domicile involves generally some intention which means a person plans to make some place as his permanent living place. Residence refers to a fact which means someone has lived in someplace for la long time or he has the conditions to live long.The stay time norms in ChinaAs specified in Chinese tax law, a person who has lived in China in fiscal year is our country’s resident taxpayer. Chinese fiscal year is the calendar year. So a person without domicile in China is viewed as Chinese taxpayer only if he has lived in China from Jan 1, to Dec 31 in a fiscal year. He will not be looked as Chinese taxpayer if he has lived for 365 days straddling over year.2.2.2 the judgment norms on resident identity of legal entity1.Registration place norms (also called legal norms)2.Management and control place norms3.Head office place norms4.V oting power controlled place normsThe judgment norms on resident identity of legal entity is implemented in some countries which is as follow In the four norms, registration place and management or control place norms are most often used. There are some countries which only adopt registration place norms such as Denmark, Egypt, France, Niger, Sweden, Thailand and USA. There are some countries which only adopt management and control place norms such as Ireland, Malaysia, Mexico and Singapore. But also are there some countries which adopt both the above two norms such as Canada, Germany, Greece, India, Kenya, Luxemburg, Malta, Mauritius, Netherlands, Sir lanka, Switzerland and England.Any company which meets one of the norms , it will be the resident taxpayer in these countries. Additionally, some countries adopt only the registration and management or control place norms but also adopt the head office place norms. In Belgium and Japan, registration and head office place norms are adopted together. In Portugal and Norway, both management or control and registration place norms are implemented. The three norms are adopted all in New Zealand and Spain. In the above four mentioned norms, voting power controlled place norms is seldom adopted. In the main countries, only Australia adopts it beside registration and management or control place norms. The rule of judging resident identity of legal entity in China is as followed.We can define the norms of judging resident identity of legal entity in the laws of income tax to enterprise with foreign investment and foreign enterprise which specifies the enterprise with foreign investment set up within China include three types, namely, Chinese-foreign joint venture, Chinese-foreign cooperative enterprise and foreign enterprise. If its head office is in China, it should pay tax on its income earned from both within and outside Chinese boundary. It means China adopts head office place norms as the judgment norms on resident identity of legal entity, neither of them could be missed.2.3 the judgments norms on source places of income2.3.1 business income2.3.2 service income2.3.3 investment income2.3.4 property income2.3.1 business incomeBusiness income is the operation profit which is the net income of individual or legal entity which is engaged in productive or non-productive activities. Whether the income is the taxpayer’s taxable income depends on mainly whether the operation activities is the taxpayer’s main econom ic activities or not.The norms for judging source place of income include:1.Permanent establishment normsMany countries which have the continent system of law adopt the permanent establishment norms to judge whether or not taxpayer’s business income comes from this country.2.Trading floor normsEnglish and American countries often adopt the trading floor norms to judge the source place of business income.2.3.2 service income1.Place of rendering service normsIt means where the multicountry taxpayer render his service or in which country he works, the income he earned is viewed as the income originated from this country.2.Place of paying income normsIt means the country where the taxpayer who pay for the service lives in or the fixed base or permanent establishment is the source place of income.2.3.3 investment incomeInvestment income refers to the income earned because of having the property including mainly dividend, interest and royalties. Dividend is the investor’s income earned because he owns a company’s share or other equity similar. Interest is the investor’s income earned on basis of his creditor’s rights. Royalties is the investor’s income because he offered his patent, trademark right, good-will, copyright, marketing right, craft-manship or other intangible property to others for use. Investment income include mainly:1.DividendThe rule for judging the source place of dividend in every country is the resident place where the company which pays the dividend locates.2.InterestThe rule for judging the source place of interest in every country is the resident place where the company which pays the interest locates.3.Royalties(1)The place where the franchise is used is the source place of royalties(2)The place where the franchise owner lives is the source place of royalties(3)The place where the royalties’ payer lives is the source place of royalties4.RentalsThe rule for judging the source place of rentals is similar to the rule for royalties.2.3.4 property incomeProperty income is the income earned by the taxpayer because he owns, uses, transfers his property (also called capital gains). As for real estate, all countries take it for granted that the place where the real estate locates is the source place of property income. But as for chattel, the rules for judging the source place of property income are not the same.2.4 the obligation to pay tax between resident and non-resident taxpayer2.4.1 The obligation to pay tax for resident taxpayers2.4.2 The obligation to pay tax for non-resident taxpayers2.4.1 The obligation to pay tax for resident taxpayersA country which implements resident tax jurisdiction will levy on its residents all income within or outside its boundary. From the view of taxpayer, he will pay tax not only on his income within this country, but also pay tax on his income from the entire world. The obligation to pay tax on income from the whole world for a taxpayer is called unlimited obligation of paying tax. In a country which implements resident tax jurisdiction, the taxpayer, no matter he is a natural person or a legal entity, must fulfill the unlimited obligation of paying tax to the government of residence country.2.4.2 The obligation to pay tax for non-resident taxpayersIn a country which implements resident tax jurisdiction and geographical tax jurisdiction, non-resident taxpayer only has to pay tax on the income he earned from this country to the government. The obligation to pay tax on income within a country’s boundary for a taxpayer is called limited obligation of paying tax. The taxpayer, no matter he is a natural person or a legal entity, must fulfill the limited obligation of paying tax to the government of non-residence country.Problems of thinking1.Wh at’s the tax jurisdiction? How many types are there?2.What’s the judgment norm on inhabitant taxpayer?3.What’s the judgment norm on source place of income?4.What’s the unlimited obligation of taxpayer? Who has the unlimited obligation?Chapter 3 International double taxation and ways of resolving it3.1the nomination of international double taxation3.2the avoidance ways to international double taxation because of overlap of the same tax jurisdictions3.3the exemption ways to international double taxation because of overlap of different tax jurisdictions3.4the economic analysis on the exemption ways to international double taxation3.1the nomination of international double taxation3.1.1 What’s international double taxation?3.1.2 The reasons of international double taxation3.1.1 What’s international double taxation?1.Legal double taxation: When two or more levy entities which have tax jurisdictions levy the same object of taxation of the same taxpayer, legal international double taxation appears.2.Economic double taxation: When two or more levy entities levy on the same object of taxation of different taxpayers, economic international double taxation appears.In a word, international double taxation means two or more countries levy the same or similar tax on the same object of taxation of the same or different taxpayer at the same period.3.1.2 The reasons of international double taxation1.The overlap of the same kind of tax jurisdictions of two countries2.The overlap of the different kinds of tax jurisdictions of two countries(1)Overlap of resident tax jurisdiction and geographical tax jurisdiction(2)Overlap of citizen tax jurisdiction and geographical tax jurisdiction(3)Overlap of citizen tax jurisdiction and resident tax jurisdiction3.2the avoidance ways to international double taxation because of overlap of the same tax jurisdictions3.2.1 The international norms of binding resident tax jurisdictions3.2.2 The international norms of binding geographical tax jurisdictions3.2.1 The international norms of binding resident tax jurisdictions1.The international norms of binding implementing resident tax jurisdictions to natural persons(1)Permanent home(2)Center of vital interest(3)Habitual abode(4)Nationality2. The international norms of binding implementing resident tax jurisdictions to legal entity3.2.2 The international norms of binding geographical tax jurisdictions1.Business income2.Service income3.Investment income4.Property income3.3the exemption ways to international double taxation because of overlap of different tax jurisdictions3.3.1 tax deduction method3.3.2 tax allowance method3.3.3 tax exemption method3.3.4 tax credit method3.3.1 tax deduction methodWhen a government levies on the income outside the country of its resident, it allows the taxpayer to deduct his tax payment to the foreign country from his taxable income. The way of levying only on the deducted balance is called tax deduction method.3.3.2 tax allowance methodTax allowance method is also called low tax method which means the government gives the resident taxpayer some tax cut on his income outside the country based on the normal tax rate and levies on the income in lower tax rate, meanwhile,levies on his income within the country i n the general tax rate. This method can just relieves the taxpayer’s burden but can’t avoid international double taxation.3.3.3 tax exemption methodTax exemption method means the government will not levy on all or some of the income outside the country of the resident taxpayer.◆General tax exemption method: It means the government will not levy on all the income outside the country of the resident taxpayer and will not take the outside taxable income into account when the government levies on the taxpayer’ s income within the country.◆Progressive tax exemption method: It means the government will not levy on all the income outside the country of the taxpayer, but when the government levies on the taxpayer’s income within the country, it will gather the inside and outside income together to determine its tax rate.3.3.4 tax credit methodIt means the government allows the taxpayer to use his tax payment paid to the foreign country to credit his tax payment in this country when the government levies on the income outside th e country. So the taxpayer’s tax payment is only the difference between tax payable in this country and the tax payment already paid to the foreign country. This method can effectively avoid international double taxation.1.Creditable quota2.Direct and indirect credit method3.The exchange rate of foreign tax credit4.Charge distribution5.Tax sparing credit1.Creditable quotaIn practice, every country credits tax under its creditable quota to protect its interest which means the taxpayer’s domesti c tax creditable amount per country can’t exceed the creditable quota which is computed by the foreign income times the domestic tax rate.Creditable quota is the highest amount which is allowed to credit the taxpayer’s domestic tax payment , but it mig ht not equal its actual creditable amount.▲the formula for computing creditable quota is as follows:▪Creditable quota per country=sum of tax payable computed by all of the taxpayer’s income from all of the world in accordance with the tax law in residence country×income from some foreign country/income from all of the world▲the formula for computing creditable quota is as follows:▪Comprehensive creditable quota=sum of tax payable computed by all of the taxpayer’s income from all of the world in accordance with the tax law in the residence country ×all income from outside of the country /income from all of the world▲the formula for computing creditable quota is as follows:▪Creditable quota per country or comprehensive creditable quota=all income from outside of the country or income from some foreign country ×tax rate of the residence country2.Direct and indirect credit method▪Direct credit method means the taxpayer could use the tax payment paid to the foreign countries to credit directly the tax payable in the residence country.▪The formula for computing the tax payable to the residence country in direct credit method is as follows.The tax amount payable to the residence country=(income derived from the residence country + income derived from source country) ×tax rate of the residence country-the actual creditable amount=all of the income of the taxpayer’s ×tax rate of the residence country-the actual creditable amount●indirect credit methodIt means the taxpayer could use the tax payment paid to the foreign countries to credit indirectly the tax payable in the residence country. This method is applicable only for legal entity, not for natural person and for income tax only.3.The exchange rate of foreign tax creditFrom the situation of tax credit between parent and its subsidiary, every country uses the current tax rate to compute the taxable dividend payable in domestic currency. It is the tax rate that the subsidiary uses to distribute dividend to the parentcompany. But there is not common tax rate to compute indirect credit. Some countries use the tax rate when the foreign subsidiary pays the tax payment in foreign countries (so called the historical tax rate), but some countries still use the current tax rate when the foreign subsidiary distributes profit to the parent company.4.Charge distributionThere are two ways of distributing charge. One is the actual distribution method which means the taxpayer can distribute charge according to the actual connection between the charge and the foreign income; Another way is the formula distribution method which means the taxpayer has to distribute charge according to : assets in foreign countries /sum of all assets or gross income from foreign countries/sum of all gross income5.Tax sparing creditIn short, tax sparing credit can be called tax sparing which means the government deems the taxpayer’s exemption of income tax in foreign countries as tax payment paid and allows this part of exemption to credit the tax payable in the residence country. For the residence country, it is not a way of avoidance of international double taxation, but a preferential tax measure to the taxpayer who is engaged in international economic activities.Problems of thinking1. What’s the international double taxation? What causes the international double taxation?2. What’s the impact of international double taxation? How to relief it?3. Which income is suitable for the exemption method?4. What’s the exemption quota? How to compute it?5. What’s the tax sparing? What’s its usefulness?Chapter 4 Overviews of international tax evasion4.1 What’s international tax evasion?4.2 International tax heaven4.3 Transfer pricing4.1 What’s international tax evasion?4.1.1 The meaning of tax evasion4.1.2 Wha t’s international tax evasion?4.1.3 The causes of international tax evasion4.1.1 The meaning of tax evasionIn general, tax evasion refers to the taxpayer uses the loophole or points which aren’t definite in tax law to evade, relief or defer his liability to pay tax.Actually, in foreign countries, tax avoidance, tax planning and legal tax saving are almost the same meaning which refers to the taxpayer uses some legal ways to relief or evade his tax liability.The common between tax avoidance and tax evasionThe two are both the actions mention ally taken by the taxpayers to relief their tax burden, but they are different concepts after all.The difference between tax avoidance and tax evasion1. Tax evasion refers to the taxpayer can’t pay his tax payment after his tax liability has already happened; But tax evasion refers to the taxpayer plans to evade or relief his tax liability in advance.2. Tax evasion goes against tax law directly which is illegal. But tax avoidance refers to using loophole in tax law which doesn’t infringe tax law directly. So its form is legal.3. Tax evasion not only goes against the tax law, but also utilizes some illegal ways such as making false account or vouchers. So, it should be punished by law; but tax avoid ance is legal which doesn’t commit crime. So it won’t by punished by law.The government can take some measures to prevent tax avoidance1.Perfect the tax law and block the loophole in tax law to make the taxpayer have no chance to use.2.Introduce the con cept of “power shopping” and “low power shopping”. It means in one aspect, it allows the taxpayer to have the right to use the ways of minimizing his tax liability to run business, in another aspect, it doesn’t approve the taxpayer’s transaction activities to evade tax and deem the taxpayer abusing his power given by the government.。