CFA一级会计笔记1

CFA1财务分析记忆要点

CFA1财务分析记忆要点1.财务报表分析是一个评估公司财务状况和业绩的重要工具。

其中包括利润表、资产负债表和现金流量表。

2.利润表反映了公司在一定期间内的收入、费用和利润。

利润表中的关键指标包括营业收入、营业利润和净利润。

3.资产负债表展示了公司在特定日期上的资产、负债和所有者权益。

资产负债表中的关键指标包括总资产、总负债和净资产。

4.现金流量表反映了公司在一定期间内的现金流入和流出情况。

现金流量表中的关键指标包括经营活动、投资活动和筹资活动的净现金流量。

5.财务比率分析是一种衡量公司财务状况和业绩的方法。

常用的财务比率包括流动比率、速动比率、资产负债比率、营业利润率和净利润率。

6.流动比率是衡量公司偿付短期债务能力的指标,计算公式为流动资产除以流动负债。

速动比率是衡量公司偿付短期债务能力的更严格指标,计算公式为速动资产除以流动负债。

7.资产负债比率是衡量公司资产权益比例的指标,计算公式为总负债除以净资产。

资产负债比率越高,公司的财务风险越大。

8.营业利润率是衡量公司每单位销售收入所赚取的利润水平的指标,计算公式为营业利润除以营业收入。

净利润率则是衡量公司每单位销售收入所获利润的指标,计算公式为净利润除以营业收入。

9.财务报表的调整是为了使其更准确地反映公司的经营状况。

调整项目包括非经常性项目、会计估计和会计政策变更。

10.财务报表分析的目的是评估公司的盈利能力、偿债能力和投资价值。

其中,盈利能力包括利润水平和利润增长;偿债能力包括偿付能力和债务比例;投资价值包括股东权益回报和市场估值。

11.在进行财务报表分析时,需要考虑公司的行业特点和竞争环境,以及宏观经济环境的影响。

12.财务报表分析是一种量化和定性的方法,需要综合运用财务比率、财务指标和财务策略等多个因素进行综合研判。

13.财务报表分析的局限性包括会计制度的差异、信息不对称和不确定性等因素的影响。

14.在进行财务报表分析时,需要注意财务报表的可靠性、一致性和可比性,以及财务报表分析的时效性和客观性。

cfa会计部分总结

cfa会计部分总结篇一:cFa一级Ethics部分知识点总结全球最大的cFa(特许金融分析师)培训中心cFa一级Ethics部分知识点总结objectiveofcodesandstandard:永远是为了maintainpublictrustin1.Financialmarket2.investmentprofession(:cfa会计部分总结)6个codeofethics1.code1—ethicsandpertinentdpersons2.code2---primacyofclient’sinteresta.integritywithinvestmentprofessionb.客户利益高于自身利益3.code3---reasonableandindependenta.必须注意reasonablecareb.必须exerciseindependentprofessionaljudgment---必须独立判断!4.code4---ethicalcultureintheprofessiona.不但自己要practice,而且要鼓励别人practice—不仅仅是自己一个人去做,要所有人共同去做5.code5---ethnicalcultureinthecapitalmarket!a.促进整个capitalmarket的integrity,推广其相关法规---增强公众对资本市场的trust!b.capitalmarket是基于i.Fairlypricingofriskyassets;ii.investors‘confidence6.有关competence—能力---competence7个standardofprofessionalconduct1.Standard1---professionalism---knowledgeoflaw总部地址:上海市虹口区花园路171号a3幢高顿教育电话:400-600-8011网址:微信公众号:gaoduncfa1 全球最大的cFa(特许金融分析师)培训中心a.不需要成为法律专家,但是必须understand和complywithapplicablelaw;b.当两个law发生conflict,则要遵守更加严格的法律!c.Knowingly---knoworshouldknowd.必须attempttostoptheviolation,如果不能stop,thenmustdissociatefromtheviolation!必须从其中分离出去!i.Removenamefromthewritteeport;ii.askforadifferentassignmente.并不要求向有关部门report!(donotrequire)f.向cFa进行书面报告report--encouragedtoso2.Standard1---professionalism---integrityofcapitalmarketa.Biasfromclientorothergroups—listedcompany,controllingshareholder!b.Biasfromsellsideanalystc.Buyersideclient—d.issuerpaidreport---只能接受flatfeefortheirworke.3.Standard1---professionalism---misinterpretation—不能误导客户,不能剽窃其他人的研究成果各位考生,20XX年cFa备考已经开始,为了方便各位考生能更加系统地掌握考试大纲的重点知识,帮助大家充分备考,体验实战,网校开通了全免费的高顿题库(包括精题真题和全真模考系统),题库里附有详细的答案解析,学员可以通过多种题型加强练习,通过针对性地训练与模考,对学习过程进行全面总结。

cfa一级十科笔记

cfa一级十科笔记CFA一级考试是金融行业中非常重要的职业资格认证,涵盖了广泛的金融知识领域。

下面是关于CFA一级考试十科的笔记,以帮助你更好地准备考试。

1. 伦理与专业标准(Ethics and Professional Standards):了解职业道德和行业规范的重要性。

理解与客户、公司和市场参与者之间的关系。

掌握投资专业人士应遵循的道德准则。

2. 数量方法(Quantitative Methods):熟悉基本的数学和统计概念。

掌握概率论和假设检验的基本原理。

理解回归分析和时间序列分析的基本概念。

3. 经济学(Economics):理解宏观经济和微观经济的基本原理。

掌握货币政策、财政政策和国际贸易的影响。

理解经济指标和金融市场之间的关系。

4. 金融报表分析(Financial Reporting and Analysis):理解财务报表的结构和内容。

掌握财务比率分析和财务报表的解读。

熟悉资产负债表、利润表和现金流量表之间的关系。

5. 公司金融(Corporate Finance):理解资本预算和资本结构的基本原理。

掌握投资决策和融资决策的方法。

熟悉公司治理和股权结构的影响。

6. 证券投资(Equity Investments):理解股票市场和股票投资的基本原理。

掌握股票估值和投资组合管理的方法。

熟悉股票投资的风险管理和绩效评估。

7. 固定收益投资(Fixed Income Investments):理解债券市场和债券投资的基本原理。

掌握债券估值和债券组合管理的方法。

熟悉利率风险和信用风险的评估和管理。

8. 衍生品投资(Derivative Investments):理解衍生品市场和衍生品投资的基本原理。

掌握期权、期货和其他衍生品的估值和交易策略。

熟悉衍生品投资的风险管理和绩效评估。

9. 另类投资(Alternative Investments):理解另类投资市场和另类投资的基本原理。

掌握房地产、私募股权和大宗商品等另类投资的特点和风险。

CFA一级笔记之经济学

AVC=

X

c Cost per share ATC

AVC

Economy scale

ATC= =AVC+

MC——总成本关于 Q 的导数

TC=VC+FC

成本曲线的移动:

(1)资源 P↑,成本↑

(2)tax↑,cost↑

Diseconomy (3)regulation↑

scale

LTC cost↑

Q

Q

Q

9. 四种市场结构(profit max MR=MC)。

Elasticity

P

Inelasticity

P

高价区间弹性大,P↓,

P-E

总收入↑

1.替代品的存在

P-1

E=-1,单位弹性收入最大化

2.预算约束

低价区间弹性大,P↑, 总收入↓

D

D

需求收入弹性→1.低档品,负弹性,收入↑→D↓。2.正常商品,收入↑→D↑。 0<E<1, 必需品。E>1 奢侈品

7. law of D (边际效用 8.

(1)完全竞争(同质产品、价格接受者、无进入障(2)垄断竞争(monopolistic competition 差异化产品、负斜率 D、低障碍)

P

M

P

MC

P

ATC

MR=P=D

ATC

M

P

long

short

D

M AT

short

MR=P=D

AT

D

利润最大化

Q

long

Q

(3)垄断(monopoly 一个卖者,无替代品,进入障碍高)

经济学

1. 财政政策——凯恩斯主义(关注 AD 而非 AS,价格和工资具有向下刚性) (1) 相机决策(discretionary)→反周期政策(countercyclical)

cfa一级notes习题笔记

CFA一级Notes习题笔记EthicsCode of Ethics1.act with integrity, competence, diligence, respect, and in an ethical manner with the public, clients, prospective clients, employers, employees, colleagues in the investment profession, and other participants in the global capital markets2.place the integrity of the investment profession and the interests of clients above their own personal interestse reasonable care and exercise independent professional judgement when conducting investment analysis, making investment recommendations, taking investment actions, and engaging in other professional activities4.practice and encourage others to practice in a professional and ethical manner that will reflect credit on themselves and the profession5.promote the integrity of, and uphold the rules governing, capital markets6.maintain and improve their professional competence and strive to maintain and improve the competence of other ivestment professionals.Standards of Professional ConductI professionalismA.knowledge of the lawB.independence and objectivityC.MisrepresentationD.MisconductII.integrity of capital marketsA.material nonpublic informationB.market manipulationIII.duties to clientsA.Loyalty,Prudence and CareB.Fair DealingC.SuitabilityD.Performance presentationE.preservation of confidentialityIV.duties to employersA.loyaltyB.additional compensation arrangementsC.responsibilities of supervisorsV.investment analysis, reommendations,and actionsA.Diligence and reasonable basismunication with clients and prospective clientsC.record retentionVI.conflicts of interestA.Disclosure of conflictsB.priority of transactionsC.referral feesVII.responsibilities as a CFA institute member or CFA candidateA.conduct as menbers and candidates in the cfa programB.reference to CFA institute, the cfa designation, and the cfa program1.私人投资跟Code无关,但滥用举报违反personal conduct。

cfa1级 2023 品职三色笔记

CFA 1级2023三色笔记:打造高效学习技巧在CFA 1级考试备考过程中,一份高质量的笔记是至关重要的。

在这篇文章中,我将共享我对CFA 1级2023三色笔记的理解和个人观点,帮助你更好地理解这一学习方法并提高学习效率。

一、三色笔记的概念三色笔记是一种高效的学习方法,它通过使用不同颜色的笔记录重要知识点、关键概念和需要重点记忆的内容,帮助学生更好地理解和记忆。

在CFA 1级考试备考中,采用三色笔记可以帮助考生整理复杂的知识点,提高复习效率。

二、三色笔记的制作方法1. 黑色笔:用于记录主要内容和关键知识点,例如定义、公式和重要概念。

黑色笔记录的内容应该是整篇笔记的核心,重点突出。

2. 红色笔:用于标记重点和难点部分,帮助考生在复习时更快地找到需要重点记忆的内容。

标记的内容可以是重要公式、易错知识点等。

3. 蓝色笔:用于记录个人理解、补充说明和重要提示。

蓝色笔的内容可以是对某个知识点的个人理解、与其他知识点的联系等。

三、三色笔记的优势1. 帮助记忆:通过不同颜色的标记,可以帮助大脑更好地记忆和理解知识点,提高复习效果。

2. 突出重点:通过红色标记,可以帮助考生更快地找到重点和难点内容,有针对性地进行复习和强化记忆。

3. 个性化学习:通过蓝色笔的使用,可以帮助考生记录个人理解和补充说明,使笔记更贴近个人学习情况。

四、个人观点和理解在我个人的学习过程中,我发现三色笔记是一种非常有效的学习方法。

通过不同颜色的标记,我可以更清晰地把握重点和难点内容,也更好地理解和记忆知识点。

在CFA 1级考试备考中,三色笔记帮助我更好地整理复杂的知识,提高了复习效率,也增强了自信心。

总结回顾CFA 1级2023三色笔记是一种非常有效的学习方法,它通过不同颜色的标记帮助考生更好地理解和记忆知识点,提高复习效率。

在制作笔记时,考生可以根据自己的学习情况灵活运用三种颜色的笔,使笔记更加个性化。

通过三色笔记的使用,考生可以更有效地备考,取得更好的成绩。

CFA一级常用公式和学习笔记总结可以直接打印

CFA一级常用公式和学习笔记总结从第一次考CFA一级到今天,四年过去了,持证也已经是前年的事情了。

感谢,FRM,CFA,让我见识了更多不一样的人生。

记录自己考试前的公式总结,很怀念那些用word公式编辑器逐个编辑公式的日子,现在也在从事与CFA考试相关的工作,所以决定把它们重新发上来,希望可以帮助到更多的有志于此道的同路人。

Statistic (5)1.1 Standard error of the sample mean: (5)1.2Measure of performance (5)1.3远期利率公式: (6)1.4 Leptokurtotic: (6)1.5 Positive skewed (6)1.6 Holding period return(HPR) (7)1.7 arithmetic or mean return (7)1.8 Geometric Mean return (7)1.9 Money-weighted return or time-weighted return (8)1.10 quartiles/quintiles/deciles/percentiles (8)1.11 probability (9)1.12 ratio/ordinal/interval/nominal (9)1.13 Chebyshev’s Inequality (9)1.14 distribution (10)1.15 desirable properties of an estimator (10)1.16 Bayes’ formula (10)1.17 type I and type II error (10)1.18 hypothesis testing (11)1.19 technical analysis (13)derivatives (16)2.1 option portfolio (16)2.2 Put-call parity (16)2.3 backwardation \contango (16)Corporate finance (16)3.1 NPV (16)3.2 IRR(internal rate of return) (17)3.3 PBP(backed period) (17)3.4DPB(discounted backed period) (17)3.5 Profitable index(PI) (17)3.6 WACC (17)3.7 cost of debt (18)3.8 Cost of preferred stock (18)3.9 Cost of equity (18)3.10 Break point (20)3.11 Floatation cost (20)3.12 Degree of operating leverage (21)3.13 Degree of financial leverage(DFL) (21)3.14 Degree of total leverage(DTL) (21)3.15 Breakeven Analysis (22)3.16 working capital management (22)3.17 Liquidity ratios and turnover ratios (22)portfolio (23)4.1 nominal 与real之间的转换 (23)4.2 portfolio’s deviation (24)4.3 Many risk assets (24)4.4 MPT理论 (24)4.5 Capital allocating line(CAL) (25)4.6 beta : a measure of systematic risk (26)FINANCIAL REPORTING (27)5.1 应收应付/预收预付 (27)5.2 audit report (27)5.3 Footnotes/MD&A/proxy statement (28)5.4 美国准则和国际准则 (30)5.5 IFRS对sales of goods销售商品收入确认的方法 (31)5.6 IFRS对rendering of service?收入确认的方法 (32)5.7 Financial statement Elements (32)5.8 steps in the financial statement analysis framework (33)5.9 Revenue recognition criteria (33)5.10 Revenue recognition (34)5.11 installment sales and cost recovery method (35)5.12 accounting equation 有计算 (36)5.13 income statement其它处理 (37)5.14 income statement线下项目 (38)5.15 EPS计算 (39)5.16 comprehensive income (40)5.17 金融资产与负债的计量有计算 (40)5.18 bad debt计算坏账 (41)5.19 CFO直接法与间接法有计算 (41)5.20 CFI和CFF的计算 (42)5.21 FCFE和FCFF的计算 (43)5.22 CF中的其它知识点 (44)5.23 financial analysis techniques (44)5.24 inventory 理解 (47)5.25 depreciation 理解 (50)5.26 impairment 理解 (51)5.27 capitalized and expense 的理解 (52)5.28 investment property (new) (54)5.29 early repayment of bond (55)5.30 issuance cost of bond (56)5.31 debt security 理解 (57)5.32 defer tax 理解 (59)5.33 承租人和出租人理解 (64)5.34 off-balance sheet (66)5.35 ratio (68)5.37 cash management manipulation (68)Economics (70)6.1 Utility Theory and indifference Curves (70)6.2 Economic profit and accounting profit (70)6.3 elasticity (70)6.4 Cross elasticity of demand, (71)6.5 盈亏平衡点 (71)6.6 GDP的定义: (71)6.7 nation income (72)6.8 GDP deflator: GDP平减指数 (73)6.9 IS-LM model (74)6.10 LM曲线是指货币市场的均衡。

CFA 1 笔记

Session11、永续年金只有现值PERPETUAL ANNUITIES 或PERPETUITIES)永续年金是指无限期支付的年金2、马赛克理论 mosaic theory 一个洞察力很强的分析员,如果通过对公开信息,以及一些非重大的非公开信息的分析,得出了关于公司的行为或者事件的结论,即使这个结论是重大的非公开信息,也不构成对这条准则的违反,这就是所谓的马赛克理论,也是分析员的价值所在。

3、P44客户隐私保守,但非法的,法律要求的,客户允许的可披露,同时可给为同一客户服务的同事。

P46,工作之外的行为要报告雇主且在开始前得到雇主同意P47为了保护客户的利益,或者为了维护资本市场的诚信,而不是为了个人的得失的情况下,有时候可以违反对雇主的的忠诚责任(有限忠诚)4、记录保存,如公司没有要求,CFA要求保存7年P605、Chartered Financial Analyst 或者CFA 的标志,必须跟在一个证书持有人名字的后面(比如张三,CFA),或者作为形容词(例如张三是CFA Charterholder);但是不能够作为名词(不能够说,张三是CFA)。

这个规定适用于书面和口头的沟通。

CFA 个人titile,不能用作公司titile.CFA 三级前只有candidate(报名,且参加考试后)6、GIPS 标准是2004 年12 月7 日被投资业绩委员会(IPC)修订,并于2005 年2 月4 日被CFA 协会理事会(CFA Institute Board ofGovernors)采用的。

修订之后的标准的生效时间是2006 年1 月1 日。

包含了2005 年12 月31 日以后数据的业绩表现,都必须符合修订之后的标准的要求。

只包含2005 年12 月31 日以前数据的业绩表现,可以按照符合1999 年版本的GIPS 标准进行展示(06年以前特别国家适用CVG的公司也可以宣称符合GIPS, country version of GIPS(CVG ),are granted reciprocity to claim compliance with theGIPS standards for historical periods prior to 1 January 2006。

CFA1 财务分析记忆要点

分清题目是那个报表里的概念,则答案也该也是想要报表里的概念一、收入表(不包含和股东的交易)从股东手里得到或者发放利益给股东的部分不用于计算incomeNon-recurring items(考虑频率):Discontinued operations(不影响营业利润): measurement date, phaseout period.在measurement date公司就要对其进行估计它的Income or loss (税后)在income statement里分开,之前的income statement 要重算(它的Income of loss 要在income statement里分开),在销售没有结束前,gains不能计入。

Unusual or infrequent items(影响营业利润): 包含在Incomes from Continuing operations and reported before tax.Extraordinary items(不影响营业利润):U.S.GAAP: 它的Income or loss (税后)要在income statement里分开IFRS: 不允许在income statement里分开对原有错误会计方法的订正(Prior-period adjustment)或改变使用的财务标准要回溯计算后表示在当期的报表中。

改变对财产的估计,不要求回溯。

EPS:使用月份(从可转化证券发行开始算)加权平均后拖欠股息的股数;被公司回购后的股票无需计算;Dilutive EPS:首先判断是否是Dilutive,计算后主要和Basis EPS比较大小;期权行使的计算:相当于在总资产不便的情况下,市场上增加的股数;净收入是已经计算过利息,所以在算可转换债是要将利息加回去(税后)。

Commone-size income statement: 其中Tax和ruvenue的比率的值意义不大,意义比较大的是tax和毛利的比率(effective tax rate)Other Comprehensive income: P74二、资产负债表(包含和股东的交易):由于衡量公司的liquidity, solvency the ability to pay dividends无法估计价值的A或者L不在balance sheet里体现。

CFA一级重要笔记

Ethic1.GIPS 初始5年,而后每年+1保存至少10年记录。

2.must promote the integrity and viability of the global capital markets for theultimate benefit of society. 是原则不是standard。

3.Standard V diligence and resonable basis 可以使用第三方研报,但要定期对研报提供者进行考察。

4.Portfolio valuations must use fair market values for periods on or after 1 January2011.5.Standard III(C)–Suitability of the CFA Institute Standards of ProfessionalConduct requires that when members and candidates are in an advisory relationship with a client, they must judge the suitability of investments in the context of the client’s total portfolio.6. a personal bankruptcy does not necessarily constitute a violation of StandardI(D). If the circumstances of the bankruptcy involved fraudulent or deceitful business conduct, then failing to disclose it may constitute a violation of the Standards.7. A composite must include all actual, fee-paying, discretionary portfoliosmanaged in accordance with the same investment mandate, objective, or strategy.Quantitative methodsHypothesis testCOefficient=S/X拔The variance of the number of yearly increases over the next 10 years is σ2=np(1 −p)binomial randomThe position of the first quintile is found with the following formula:Ly= (n+ 1) × (y/100),.Free trade areas(FTA) are one of the most prevalent forms of regional integration in which all barriers to the flow of goods and services among members have been eliminated. However, each country maintains its own polices against non-members.A customs union extends the FTA by not only allowing free movement of goods and services among members but also creating a common trade policy against non-members.The common market is the next level of economic integration that incorporates all aspects of the customs union and extends it by allowing free movement of factors of production among members.Economics求谁的弹性,谁就是分母We can expand Equation 5 algebraically by noting that the percentage change in any variable x is simply the change in x (∆x) divided by the level of x. So, we can rewrite Equation 5, using a few simple steps, asE>1ELASTIC E<1 inelastic求谁的弹性,谁就是分母In summary, own-price elasticity of demand is likely to be greater (i.e., more sensitive) for items that have many close substitutes, occupy a large portion of the total budget (House), are seen to be optional instead of necessary, or have longer adjustment times. Obviously, not all these characteristics operate in the same direction for all goods, so elasticity is likely to be a complex result of these and other characteristics. In the end, the actual elasticity of demand for a particular good turns out to be an empirical fact that can be learned only from careful observation and, often, sophisticated statistical analysis.Market structureShifts in the aggregate demand curveShifts in the SR aggregate supply curve•●Easy fiscal policy/tight monetary policy: If taxes are cut or government spendingrises, the expansionary fiscal policy will lead to a rise in aggregate output. If this is accompanied by a reduction in money supply to offset the fiscal expansion, then interest rates will rise and have a negative effect on private sector demand.We have higher output and higher interest rates, and government spending will be a larger proportion of overall national income.●Tight fiscal policy/easy monetary policy: If a fiscal contraction is accompanied byexpansionary monetary policy and low interest rates, then the private sector will be stimulated and will rise as a share of GDP, while the public sector will shrink.●Easy monetary policy/easy fiscal policy: If both fiscal and monetary policy areeasy, then the joint impact will be highly expansionary—leading to a rise in aggregate demand, lower interest rates (at least if the monetary impact is larger), and growing private and public sectors.●Tight monetary policy/tight fiscal policy: Interest rates rise (at least if themonetary impact on interest rates is larger) and reduce private demand. At the same time, higher taxes and falling government spending lead to a drop in aggregate demand from both public and private sectors.Trade surplus X>MTrade dificit X <M•Empl oyed: The number of people with a job. This figure normally does not include people working in the informal sector (e.g., unlicensed cab drivers, illegal workers, etc.).Labor force: The number of people who either have a job or are actively looking for a job. This number excludes retirees, children, stay-at-home parents, full-time students, and other categories of people who are neither employed nor actively seeking employment.Unemployed: P eople who are actively seeking employment but are currently without a job. Some special subcategories include:Long-term unemployed: People who have been out of work for a long time (more than three to four months in many countries) but are still looking for a job. Frictionally unemployed: they are “between jobs,” and those new entrants or re-entrants into the labor force who have not yet found work. Frictional unemployment is short-term and transitory in natureUnemployment rate: The ratio of unemployed to labor force.Activity ratio(or participation ratio): The ratio of labor force to total population of working age (i.e., those between 16 and 64 years of age).Underemployed: A person who has a job but has the qualifications to work at a significantly higher-paying job.Discouraged worker:Discouraged workers are statistically outside the labor force (similar to children and retirees), which means they are not counted in the officialunemployment rate.•Equal weighting 1/nPrice weightingMarket-Capitalization WeightingFinancial report周转天数Money marketyield 360=FV-PV/PV*(360/days) Bond equivalent yield =FV-PV/PV*(365/days)天Discount basis yield =FV-Pv/FV*(360/days)Under US GAAP, material items that are unusual or infrequent and that are both as of reporting periods beginning after 15 December 2015 are shown as part of a company’s continuing operations but are presented separately.Fixed incomeMoneyDur = AnnModDur ×PV Full永续麦考利回流的时间ModDur =1/1+r*麦考林久期收益率变动1%,债券价格变动的% R 是期间利率。

CFA_一级知识点完全总结

CFA_⼀级知识点完全总结Chartered Financial AnalystCFA ⼀级考试知识点总结StanhopeCFA⼀级知识点总结Ethics 部分Objective of codes and standard:永远是为了maintain public trust in1.Financial market2.Investment profession6个code of ethics职业道德1.Code 1—ethics and pertinented personsa.2.Code 2---primacy of client‘s interesta.Integrity with investment professionb.客户利益⾼于⾃⾝利益3.Code 3---reasonable and independenta.必须注意reasonable careb.必须exercise independent professional judgment---必须独⽴判断!4.Code 4---ethical culture in the professiona.不但⾃⼰要practice,⽽且要⿎励别⼈practice—不仅仅是⾃⼰⼀个⼈去做,要所有⼈共同去做5.Code 5---ethnical culture in the capital market!a.促进整个capital market的integrity,推⼴其相关法规---增强公众对资本市场的trust!b.Capital market是基于i.Fairly pricing of risky assets;ii.Investors? confidence6.有关competence—能⼒---competence7个standard of professional conduct1.Standard 1---professionalism---knowledge of lawa.不需要成为法律专家,但是必须understand和comply with applicable law;b.当两个law发⽣conflict,则要遵守更加严格的法律!c.Knowingly---know or should knowd.必须attempt to stop the violation,如果不能stop, then must dissociate from the violation!必须从其中分离出去!i.Remove name from the written report;f.向CFA 进⾏书⾯报告report--encouraged to so2. Standard 1 ---professionalism---integrity of capital marketa.Bias from client or other groups—listed company,controlling shareholder!b.Bias from sell side analystc.Buyer side client—d.Issuer paid report---只能接受flat fee for their worke.3.Standard 1 ---professionalism---misinterpretation—不能误导客户,不能剽窃其他⼈的研究成果4.Standard 1 ---professionalism---misconduct---5.Standard 2---integrity of capital marketa.不能使⽤⾮公开信息!---material nonpublic information---b.mosaic theory---conclusion from analysis of public and non-material nonpublic information6.standard 3—duties to clientsa.Loyalty, prudence and care---i.如何定义客户?---考虑最终受益⼈!---雇佣我们的⼈未必就是我们的客户,要考虑最终受益⼈!ii.Soft dollar---when a manager uses client brokerage to purchase research report to benefit the investment manager---⽐如,作为基⾦公司,使⽤证券公司的席位进⾏交易,肯定会⽀付⼀定的费⽤,这些费⽤来⾃客户,所以基⾦公司只能⽤这些soft dollar为客户服务!b.Fair dealing---i.对所有客户要公平客观ii.个别的客户要求,可以征收premium的费⽤之后,是可以做的!条件是,其他的分析都已经公布给其他客户了iii.More critical when changes recommendationiv.Investment action---taking investment action based on research recommendationv.Prorated the allocationc.Suitabilityi.了解客户的经验,风险和回报⽬标ii.要有书⾯⽬标—⾄少⼀年进⾏更新!iii.是否和客户的书⾯⽬标相符合?iv.是否符合客户的整个total portfolio的投资⽬标?v.必须理解其投资组合的constraints,只能进⾏符合其书⾯⽬标的投资推荐!1.Investment policy statement—IPS---risk tolerance,return requirement,investmentd.Performance presentationi.这⾥有performance presentation的规定,同时在GIPS⾥⾯也有类似规定!其区别是1.⼀个是⾃愿的---GIPS,⼀个是必需的;2.⼀个是针对公司—firm wide,⼀个是针对个⼈member和candidate3.GIPS要求公司to use accurate input data and approved calculation method, toprevent the performance record in accordance with a prescribed formate.Preservation of confidentiality---必须保密---可以不保密的情况i.违法⾏为ii.法律要求进⾏披露iii.Client或者prospective client同意披露iv.以现⾏法律为准v.CFA进⾏investigate固定收益债券,⾦融衍⽣品和alternative investment 部分Nonrefundable bond是指不能通过发⾏新的债券还旧债Sinking fund provisions---偿债基⾦条款---为了保护投资者,规定经过⼀段时间后,每年偿还⼀定⾦额的本⾦。

cfa一级笔记

cfa一级笔记

CFA一级笔记主要包括以下内容:

1. 金融市场与资产类别:包括全球金融市场概览、资产类别和金融产品概述等内容。

2. 数量方法:包括财务数据分析和处理、统计学、概率论和回归分析等内容。

3. 经济学:包括微观经济学、宏观经济学和国际经济学等内容。

4. 公司财务:包括财务报表分析、公司估值和资本结构等内容。

5. 投资组合管理:包括投资组合理论、投资组合构建和风险管理等内容。

6. 固定收益投资:包括固定收益市场和产品、债券估值和风险管理等内容。

7. 权益投资:包括股票市场和产品、股票估值和风险管理等内容。

8. 衍生品投资:包括衍生品市场和产品、衍生品估值和风险管理等内容。

9. 另类投资:包括房地产、私募股权和对冲基金等内容。

10. 道德与职业准则:包括道德和职业准则、合规和监管等内容。

此外,CFA一级笔记中还可能包含一些重要公式和概念,例如现值公式、终值公式、有效利率、单资产和两资产等。

这些公式和概念对于理解CFA一

级考试中的金融概念和问题至关重要。

CFA一级知识点总结

CFA一级知识点总结1.伦理与专业准则:这一部分考察考生对职业道德和行为准则的理解,包括对金融市场行为规范、职业操守、诚信和责任的认识。

2.投资工具:这一部分包括了股票、债券、衍生工具、期权、期货和外汇等金融工具的特点、种类和运作方式。

3.金融市场与参与者:这一部分考察了对金融市场的了解,包括股票市场、债券市场、货币市场、商品市场和外汇市场等的运作机制和参与者。

4.估值与估计:这一部分涉及股票和债券的估值方法,包括现金流量折现法、市盈率法、市净率法和利率敏感性等。

5.数量方法:这一部分考察对统计学和数量分析的理解,包括概率、统计推断、回归分析等。

6.宏观经济学和微观经济学:这一部分涵盖了宏观经济学和微观经济学的基本概念和原理,包括经济增长、通货膨胀、失业、供求关系等。

7.金融报表分析:这一部分考察对财务报表的理解和应用,包括资产负债表、利润表和现金流量表的分析和比较。

8.风险管理:这一部分涉及对风险的识别、测量和管理方法的了解,包括市场风险、信用风险、操作风险和流动性风险等。

9.投资组合管理:这一部分考察了对投资组合理论和实践的了解,包括资产配置、证券选择和风险管理等。

10.金融市场与机构:这一部分涉及金融市场和金融机构的运作和监管机制,包括中央银行、商业银行、证券公司、投资银行和保险公司等。

以上是CFA一级考试的知识点总结。

考生在备考中要基于这些知识点进行系统的复习和理解,掌握各个知识点的关键要点和应用技巧。

此外,还需要注重真题和模拟试卷的练习,提高解题能力和应试技巧。

同时,科学合理的复习计划和时间安排也是备考的关键。

希望这份总结对考生的备考有所帮助。

(完整word版)CFA一级学习重点记录

? Quantitative methodP99、P253? Continuous compounding:EAR=eRcc—1? Continuous compounding of return (Rcc) = ln(1+EAR)P141:? Time—weighted rate of return(分期计算收益率,然后相乘再开根,与投入资金的时间无关)? Money-weighted rate of return(IRR)P143:? Bank discount yield = D/F *360/t 即把折扣率单利年化? HPY holding period yield? EAY effective annual yield = (1+HPY)365/t – 1 即把HPY按照复利年化(365)? MMY money market yield(CD equivalent yield )= HPY * 360/t 即把HPY单利年化(360)? BEY bond—equivalent yield = HPY *365 / t 即把HPY按照单利年化(365):(1 + BEY/2)2 = 1 + EAY切比雪夫不等式:在k standard deviation 以内的概率至少有1-1/k2 (k>1)夏普比率Sharpe ratio = ( portfolio return – risk-free return )/standard deviation of portfolio returns条件概率P(I|O) = P(O|I)*P(I) / P(O)置信区间:? Two-tailed : 90% ?1。

65 ,95%?1。

96 , 99% ?2。

58 。

? One-tailed :90% ? 1。

28 , 95%? 1.65 , 99%?2.33 .SFR ratio SFR比率越大,越不可能小于threshold level ? P250中央极限定理:? Standard error of the sample mean is? Reliability factor is 置信区间的上界如? 90%(a=10%)?Z=1.65 , 95%(a=5%)?Z=1.96 , 99%? 2.58 。

CFA一级会计笔记

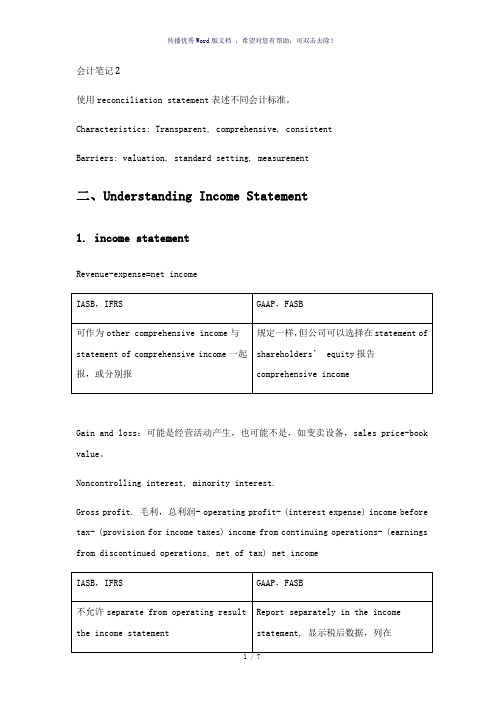

会计笔记2使用reconciliation statement表述不同会计标准。

Characteristics: Transparent, comprehensive, consistentBarriers: valuation, standard setting, measurement二、Understanding Income Statement1. income statementRevenue-expense=net incomeGain and loss:可能是经营活动产生,也可能不是,如变卖设备,sales price-book value。

Noncontrolling interest, minority interest.Gross profit. 毛利,总利润- operating profit- (interest expense) income before tax- (provision for income taxes) income from continuing operations- (earnings from discontinued operations, net of tax) net income2.收入的确认:分期销售:1)确定可收,一般方法,2)无法估计,installment method收到时才确认。

3)highly uncertainty,recovery method,收到的超过成本才确认。

Gross revenue reporting 总收入报告 net revenue reporting 净收入报告3.费用的确认Matching 原则,与产生收入的对应。

此外,period cost期间费用as administrative cost1)inventory expense recognition:FIFO和weighted average GAAP和IFRS都认可,LIFO,GAAP认可,IFSB不允许。

2020年度CFA一级NO.1_重要知识点独家整理~!!

2020年度CFA一级重要知识点总结独家整理,请勿转载~职业伦理1.1The process for the enforcement of the Code and Standards1.2Primary Principles:(1)Fairness of the process to members and candidates(2)Confidentiality of the proceedings.1.3Disciplinary Review Committee has overall responsibility for the Professional Conductprogram and enforcement of the code and standards.1.4How to detectSelf-disclosureonannualProfessionalConductStatementsofinvolvementincivil litigationoracriminalinvestigation,orthatthemember orcandidateisthesubjectofawritten complaint.Written complaints about professional conduct received by the Professional Conduct staff.Evidence of misconduct by a member or candidate that the Professional Conduct staff received through public sources,such as a media article or broadcast.A report by a CFA exam proctor of a possible violation during the examination.发现有人违反,经过CFA调查后,一般会有三种处理方法:1)不处罚;2)发警告信;3)进行处罚(由轻到重依次为:privatecensor,public censor,timed suspension)1.5Hearing panelconsists of DRC members and CFAInstitute member volunteers affiliated with the DRC 1.6AMC vs.Code and standardsThe Asset Manager Code of Professional Conduct(AMC),which is designed,in part,to help asset managers comply with the regulations mandating codes of ethics forinvestment advisers.AMC was drafted specifically for firmsCode and Standards is aimed at individual investment professionals1.7Knowledge of law必须了解与工作直接相关(directly governing their work)的法律和规则,但不需要成为expert on compliance;总是遵守最严格的,但最低限度要遵守CFA Institute准则和标准;如果有传递关系,遵循最后一个生效的law or regulations;work(applicable)live Comply withMs→Live Ls Ls<Code→CodeLs→Live Ms Ms>Code→MsGuidance of compliance●如果你感觉(feel)有人违法,你必须consult for advice,but not exempt fromrequirements to compliance;●如果你知道(know)有人在违法,还可以采取分步骤的方法:向公司里的适当人员汇报(r e po r t);如果汇报后仍没有改进,则你必须与违法行为划清界限(d i sass o ci a te),甚至辞职;同时要进一步咨询以便采取进一步的行动;还可以(m a y c on s i d e r t o p e r s u a d e t o s t op)考虑劝说违法的人终止违法行为;(注:I fyou were a supervisor,how to do?)当发现有违法行为时,CFA Institute并不要求你向政府管理机构汇报。

10A通过-CFA-level-1-知识点精简总结

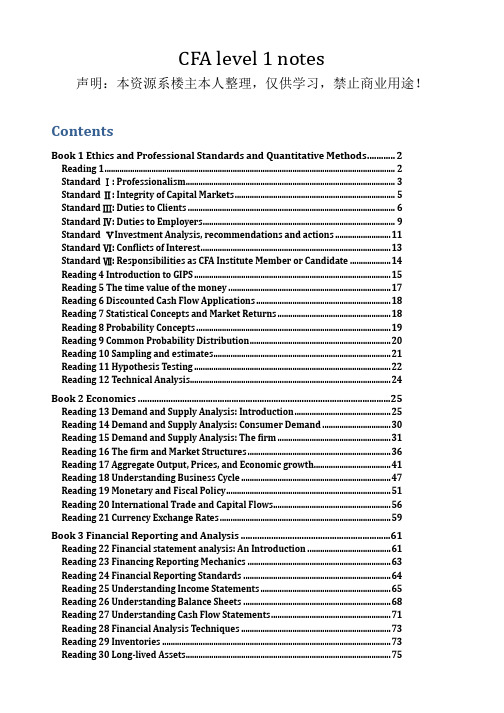

CFA level 1 notes声明:本资源系楼主本人整理,仅供学习,禁止商业用途!ContentsBook 1 Ethics and Professional Standards and Quantitative Methods (2)Reading 1 (2)Standard Ⅰ: Professionalism (3)Standard Ⅱ: Integrity of Capital Markets (5)Standard Ⅲ: Duties to Clients (6)Standard Ⅳ: Duties to Employers (9)Standard ⅤInvestment Analysis, recommendations and actions (11)Standard Ⅵ: Conflicts of Interest (13)Standard Ⅶ: Responsibilities as CFA Institute Member or Candidate (14)Reading 4 Introduction to GIPS (15)Reading 5 The time value of the money (17)Reading 6 Discounted Cash Flow Applications (18)Reading 7 Statistical Concepts and Market Returns (18)Reading 8 Probability Concepts (19)Reading 9 Common Probability Distribution (20)Reading 10 Sampling and estimates (21)Reading 11 Hypothesis Testing (22)Reading 12 Technical Analysis (24)Book 2 Economics (25)Reading 13 Demand and Supply Analysis: Introduction (25)Reading 14 Demand and Supply Analysis: Consumer Demand (30)Reading 15 Demand and Supply Analysis: The firm (31)Reading 16 The firm and Market Structures (36)Reading 17 Aggregate Output, Prices, and Economic growth (41)Reading 18 Understanding Business Cycle (47)Reading 19 Monetary and Fiscal Policy (51)Reading 20 International Trade and Capital Flows (56)Reading 21 Currency Exchange Rates (59)Book 3 Financial Reporting and Analysis (61)Reading 22 Financial statement analysis: An Introduction (61)Reading 23 Financing Reporting Mechanics (63)Reading 24 Financial Reporting Standards (64)Reading 25 Understanding Income Statements (65)Reading 26 Understanding Balance Sheets (68)Reading 27 Understanding Cash Flow Statements (71)Reading 28 Financial Analysis Techniques (73)Reading 29 Inventories (73)Reading 30 Long-lived Assets (75)Reading 31 Income Taxes (78)Reading 32 Non-Current Liabilities (80)Reading 33 Financial Reporting Quality: Red Flags and Accounting Warning Signs84 Reading 34 Accounting Shenanigans on the Cash Flow Statement (86)Reading 35 Financial Statement Analysis: Applications (87)Book 4 Corporate Finance, Portfolio Management and Equity Investment.88Reading 36 Capital Budgeting (88)Reading 37 Cost of Capital (90)Reading 38 Measure of leverage (92)Reading 39 Dividends and share repurchase basics (92)Reading 40 Working Capital Management (93)Reading 41 the Corporate Governance of Listed Companies (95)Reading 42 Portfolio Management: An Overview (97)Reading 43 Portfolio risk and return: Part 1 (98)Reading 44 Portfolio risk and return: Part 2 (99)Reading 45 Basics of portfolio planning and construction (101)Reading 46 Market organization and structure (102)Reading 47 Security Market Indices (106)Reading 48 Market Efficiency (108)Reading 49 Overview of Equity Securities (111)Reading 50 Introduction to Industry and Company analysis (113)Reading 51 Equity valuation (116)Book 5 Fixed Income, Derivatives, and alternative investments (117)Reading 52 Fixed-income securities: Defining Elements (117)Reading 53 Fixed-income Markets: Issuance, Trading, and Funding (121)Reading 54 Introduction to Fixed Income Valuation (122)Reading 55 Understanding Fixed-Income Risk and Return (124)Reading 56 Fundamentals of credit analysis (126)Reading 57 Derivative Markets and Instruments (129)Reading 58 Forward Markets and Contracts (130)Reading 59 Future Markets and Contracts (131)Reading 60 Option Markets and Contracts (132)Reading 61 Swap Markets and Contracts (134)Reading 62 Risk Management Applications of Option Strategies (135)Reading 63 Introduction to Alternative Investments (135)Book 1 Ethics and Professional Standards and Quantitative MethodsTips: 答案中违反两种规则的,倾向于选择只违反一个规则的选项。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

会计笔记

财务报表作用:使用公司财务报表的信息及其他相关信息来make economic decision.(外部用途,决定是否投资,推荐,贷款)

Statement of comprehensive income报告所有shareholder transaction的权益变动。

Income statement(损益表)报告一段时间内公司的financial performance(revenue,expense,gain,loss)在IFRS下,两者可以分开也可以将Income statement合并到Statement of comprehensive income,类似在GAAP下,公司可以选择在statement of shareholder’s equity里报告comprehensive income。

Statement of change in equity:一段时间内公司权益投资者的投资变动或来源的变化。

Statement of cash flow:公司的现金收付。

Financial statement notes(footnotes):1. Basis of presentation ,as fiscal period,inclusion of consolidated entities.2.accounting method, assumption,estimates,3.additional info as 并购,处置,法律行为,员工福利计划,以外事故,主要客户,关联方,segment of firm。

Management’s commentary(MD&A):nature of business,past performance,future outlook,有些部分是可以不被审计。

对于美国publicly held firm要求discuss 趋势,影响公司流动性,资本resource 运作结果的重大事件和不确定性。

还要包括:通胀和价格变化的影响,表外债务和contractual obligation 的影响,如购买commitment,根据政策需要管理层作出的重大调整,预测将来的费用或divestiture

审计:

Unqualified opinion :free from material omission and error

qualified opinion:make any exception to accounting principles,需要解释特例adverse opinion:不公平或实质性与accounting standard不符

disclaimer of opinion:不能发表意见

中期报告,更新数据,不一定要审计。

一、财务报告机制

1.Financial statement elements

A.资产

1)Cash and cash equivalents:90天以内的流动证券。

2)Accounts receivable通常有allowance for bad debt expense或allowance for doubtful accounts。

3)存货。

4)金融资产。

5)prepaid expense。

6)property,plant,and equipment,包括累计折旧的抵消资产科目。

7)投资in affiliates accounted for 使用股权方式。

8)递延税资产。

9)无形资产

B.负债

1)Accounts payable and trade payable,2)金融负债,如短期note payable,3)unearnedrevenue,4)income tax payable,5)长期负债eg,bond payable。

6)递延税负债

C.所有者权益

1)capital普通股par value,2)Additional paid-in capital卖出普通股超出par value 的收益。

3)retained earning累计的分配利润。

4)other comprehensive income由于外汇汇兑,minimum pension liability adjustment或unrealized 的投资损益。

D.收入

1)Sales。

2)gain日常活动交易产生的资产增加。

3)investment income利息和股息收入。

E.费用expense

1)cost of goods sold,2)selling,general and administrative expense,as广告,管理层工资,租金,公用事业。

3)折旧和摊销。

4)tax expense。

5)利息。

6)losses,日常活动交易产生的资产减少。

2. 基本等式

资产=负债+所有者权益=负债

=负债+contributed capital +beginning retained earnings+revenue-expenses-dividends Double-entry accounting一向交易必须记录2个accounts

accrual accounting权责发生制有四类:1)unearned revenue预收,2)Accrued revenue 应计收入(商品或服务以提供,还未收款),3)prepaid expense预付,4)Accrued expense (应付,已发生还未付)

Journal entries流水分录记录每笔交易,general journal日记薄,general ledger总分类账将分录归到会计科目,期末,initial trial balance初步试算平衡,需要再调整,presented in financial statement。

分析师需要从footnotes和MD&A中得到信息,管理层可能会操纵公司财务表现。

3.财务报告标准

标准制定主体:1)FASB,美国,GAAP。

2)IASB,美国以外,IFRS

监管机构:SEC(USA),FSA(UK),很多国家监管机构belong to ICSCO

影响统一的因素:1)不同国家的标准制定和监管在会计处理不同,2)来自于企业及其他受影响方的压力。

1)IASB,IFRS

fundamental qualitative characteristics:1)relevance,能影响economic decision ,对过去的估值和未来的预测,是可预测的或是确定的value,or both。

2)faithful

representation,完整、中立、无误。

为保证这两点:1)comparability,2)Verifiability,3)Timelines,4)Understandability

Measurement base:历史成本法history cost,amortized cost(历史成本通过折旧,摊销,depletion,impairment调整后),current cost,realizable value可变现价值,present value(PV),fair value(公允价值,双方认可)。

限制和假设:A.限制:cost-benefit tradeoff,user的gain from info必须高于presenting cost。

Non-quantifiable info不能直接从财务报表获得。

B.假设:权责发生制accrual accounting,持续经营going concern。

IFRS,IAS:1)要求的报表:balance sheet,statement of comprehensive income,cash flow statement,statement of change in owner’ equity,explanatory notes包括会计政策summary。

2)general feature:Fair presentation,going concern basis,accrual basis,consistency,materiality(无misstatement和omission),aggregation,no offsetting (不能将资产与负责抵消,收入与expense抵消),frequency,comparative info(之前的数据)3)报表组成:1)classified balance sheet,2)minimum info on face of报告,3)comparative info(之前的比较)

2)GAAP,FASB。