A course in financial calculus chapter 4's Solutions

金融工程经典书籍

金融工程经典书籍1.Futures, Options and other derivatives--John Hull这本书被称为“华尔街圣经”,不管是找工作还是senior quant都会用到。

John Hull 非常厉害,各个方面都有开创性的成果。

2.Arbitrage theory in continuous time--Tomas Bjork这本书非常适合数学/物理背景的人读,注重数学理论的培养。

3.Financial Calculus--Martin Baxter& Rennie非常薄但是elegant的一本书,1996年,算是比较早了,但是和Hull的书齐名。

4.Financial calculus for finance I II--ShreveShreve的书,非常elegant,非常仔细,适合有数学背景的人读。

I是讲离散模型,II是讲连续模型。

5.Martingale methods in Financial modelling--Musiela & Rutkovski6. Brownian motion and stochastic calculus--Shreve& Karasatz7.Stochastic differential equations--Oksendal8.Stochastic integration and differential equations--Protter9.Numerical analysisJunior quant:10.Concepts and practice of Mathematical Finance--Mark Joshi非常适合刚入行的quant,对于学生不推荐。

非常实用,作者非常聪明。

11. C++ design patterns and derivatives pricing--Mark Joshi对于懂得C++基础的人来说很重要,更重要的是教你学会Monte Carlo。

金融工程硕士书单Master reading list for Quants, MFE students范文

以下推荐书目,由华尔街的Quant们和美国各名牌大学毕业生推荐。

FREE QUANT CAREER GUIDES•What do quant do ? A guide by Mark Joshi. Download•Paul & Dominic's Guide to Quant Careers (see attachment)•Career in Financial Markets 2011- a guide by efinancialcareers. Download•Interview Preparation Guide by Michael Page: Quantitative Analysis. Download•Interview Preparation Guide by Michael Page: Quantitative Structuring. Download•Paul & Dominic's Job Hunting in Interesting Times Second Edition (see attachment)•Peter Carr's A Practitioner's Guide to Mathematical Finance (see attachment)GENERAL READING ON WALL STREET•Reminiscences of a Stock Operator (Wiley Investment Classics)•Working the Street: What You Need to Know About Life on Wall Street•Liar’s Poker: Rising Through the Wreckage on Wall Street•Monkey Business: Swinging Through the Wall Street Jungle•Fiasco: The Inside Story of a Wall Street Trader•Den of Thieves•When Genius Failed: The Rise and Fall of Long-Term Capital Management•Traders, Guns & Money: Knowns and unknowns in the dazzling world of derivatives•The Greatest Trade Ever: The Behind-the-Scenes Story of How John Paulson Defied Wall Street and Made Financial History•Goldman Sachs : The Culture of Success•The House of Morgan: An American Banking Dynasty and the Rise of Modern Finance•Wall Street: A History: From Its Beginnings to the Fall of Enron•The Murder of Lehman Brothers: An Insider’s Look at the Global Meltdown•On the Brink: Inside the Race to Stop the Collapse of the Global Financial System•House of Cards: A Tale of Hubris and Wretched Excess on Wall Street•Too Big to Fail: The Inside Story of How Wall Street and Washington Fought to Save the Financial System-and Themselves•Liquidated: An Ethnography of Wall Street•Fortune’s Formula: The Untold Story of the Scientific Betting System That Beat the Casinos and Wall StreetCAREER AS A QUANT•My Life as a Quant: Reflections on Physics and Finance•How I Became a Quant: Insights from 25 of Wall Street’s Elite•The Big Short: Inside the Doomsday Machine•The Quants: How a New Breed of Math Whizzes Conquered Wall Street and Nearly Destroyed It •Nerds on Wall Street: Math, Machines and Wired Markets•Physicists on Wall Street and Other Essays on Science and Society•The Complete Guide to Capital Markets for Quantitative Professionals•Starting Your Career as a Wall Street Quant: A Practical, No-BS Guide to Getting a Job in Quantitative Finance and Launching a Lucrative CareerBOOKS FOR QUANT INTERVIEWS•Heard on The Street: Quantitative Questions from Wall Street Job Interviews by Timothy Crack •Quant Job Interview Questions And Answers by Mark Joshi•Frequently Asked Questions in Quantitative Finance by Paul Wilmott•A Practical Guide To Quantitative Finance Interviews by Xinfeng Zhou•Basic Black-Scholes: Option Pricing and Trading by Timothy Crack•Fifty Challenging Problems in Probability with Solutions by Frederick Mosteller•Vault Guide to Advanced Finance & Quantitative InterviewsGOOD BOOKS TO READ BEFORE STARTING MFE PROGRAM•A Primer for the Mathematics of Financial Engineering (+ Solutions Manual) by Dan Stefanica •An Introduction to the Mathematics of Financial Derivatives, Second Edition by Salih Neftci •Options, Futures, and Other Derivatives with Derivagem CD (7th Edition) by John Hull•Paul Wilmott on Quantitative Finance 3 Volume Set (2nd Edition) by Paul Wilmott•Principles of Financial Engineering, Second Edition by Salih Neftci•Elementary Stochastic Calculus With Finance in View by Thomas Mikosch•The Concepts and Practice of Mathematical Finance by Mark Joshi•Financial Options: From Theory to Practice by Stephen Figlewski•Financial Calculus : An Introduction to Derivative Pricing by Martin Baxter•A Course in Financial Calculus by Etheridge Alison•The Mathematics of Financial Derivatives: A Student Introduction by Paul Wilmott •Frequently Asked Questions in Quantitative Finance by Paul Wilmott•Derivatives Markets by Robert L. McDonald•An Undergraduate Introduction to Financial Mathematics by Robert Buchanan PROGRAMMINGC++ (ordered by level of difficulty)•Problem Solving with C++, 7th Edition by Walter Savitch•C++ How to Program (7th Edition) by Harvey Deitel•Absolute C++ (4th Edition) by Walter Savitch•Thinking in C++: Introduction to Standard C++, Volume One by Bruce Eckel•Thinking in C++: Practical Programming, Volume Two by Bruce Eckel•The C++ Programming Language: Special Edition by Bjarne Stroustrup (C++ inventor) •Effective C++: 55 Specific Ways to Improve Your Programs and Designs by Scot Myers•C++ Primer (4th Edition) by Stanley Lippman•C++ Design Patterns and Derivatives Pricing (2nd edition) by Mark Joshi•Financial Instrument Pricing Using C++ by Daniel DuffyC# (ordered by level of difficulty)•C# 2010 for Programmers (4th Edition)•Computational Finance Using C and C# by George Levy•C# in Depth, Second Edition by Jon SkeetF# (ordered by level of difficulty)•Programming F#: An introduction to functional language by Chris Smith•F# for Scientists by Jon Harrops (Microsoft Researcher)•Real World Functional Programming: With Examples in F# and C#•Expert F# 2.0 by Don Syme•Beginning F# by Robert PickeringMatlab (ordered by level of difficulty)•Matlab: A Practical Introduction to Programming and Problem Solving•Numerical Methods in Finance and Economics: A MATLAB-Based Introduction (Statistics in Practice)Excel•Excel 2007 Power Programming with VBA by John Walkenbach•Excel 2007 VBA Programmer’s Reference•Financial Modeling by Simon Benninga•Excel Hacks: Tips & Tools for Streamlining Your Spreadsheets•Excel 2007 Formulas by John WalkenbachVBA•Advanced modelling in finance using Excel and VBA by Mike Staunton•Implementing Models of Financial Derivatives: Object Oriented Applications with VBAPython•Learning Python: Powerful Object-Oriented Programming•Python CookbookFINITE DIFFERENCES•Option Pricing: Mathematical Models and Computation, by P. Wilmott, J.N. Dewynne, S.D. Howison•Pricing Financial Instruments: The Finite Difference Method, by Domingo Tavella, Curt Randall •Finite Difference Methods in Financial Engineering: A Partial Differential Equation Approach by Daniel DuffyMONTE CARLO•Monte Carlo Methods in Finance, by Peter Jäcke (errata available at )•Monte Carlo Methodologies and Applications for Pricing and Risk Management , by Bruno Dupire (Editor)•Monte Carlo Methods in Financial Engineering, by Paul Glasserman•Monte Carlo Frameworks in C++: Building Customisable and High-performance Applications byDaniel J. Duffy and Joerg KienitzSTOCHASTIC CALCULUS•Stochastic Calculus and Finance by Steven Shreve•Stochastic Differential Equations: An Introduction with Applications by Bernt Oksendal VOLATILITY•Volatility and Correlation, by Riccardo Rebonato•Volatility, by Robert Jarrow (Editor)•Volatility Trading by Euan SinclairINTEREST RATE•Interest Rate Models - Theory and Practice, by D. Brigo, F. Mercurio updates available on-line Professional Area of Damiano Brigo's web site•Modern Pricing of Interest Rate Derivatives, by Riccardo Rebonato•Interest-Rate Option Models, by Riccardo Rebonato•Efficient Methods for Valuing Interest Rate Derivatives, by Antoon Pelsser•Interest Rate Modelling, by Nick Webber, Jessica JamesFX•Foreign Exchange Risk, by Jurgen Hakala, Uwe Wystup•Mathematical Methods For Foreign Exchange, by Alexander LiptonSTRUCTURED FINANCE•The Analysis of Structured Securities: Precise Risk Measurement and Capital Allocation (Hardcover) by Sylvain Raynes and Ann Rutledge•Salomon Smith Barney Guide to MBS & ABS, Lakhbir Hayre, Editor•Securitization Markets Handbook, Structures and Dynamics of Mortgage- and Asset-backed securities by Stone & Zissu•Securitization, by Vinod Kothari•Modeling Structured Finance Cash Flows with Microsoft Excel: A Step-by-Step Guide (good for understanding the basics)•Structured Finance Modeling with Object-Oriented VBA (a bit more detailed and advanced than the step by step book)STRUCTURED CREDIT•Collateralized Debt Obligations, by Arturo Cifuentes•An Introduction to Credit Risk Modeling by Bluhm, Overbeck and Wagner (really good read, especially on how to model correlated default events & times)•Credit Derivatives Pricing Models: Model, Pricing and Implementation by Philipp J. Schönbucher •Credit Derivatives: A Guide to Instruments and Applications by Janet M. Tavakoli•Structured Credit Portfolio Analysis, Baskets and CDOs by Christian Bluhm and Ludger Overbeck RISK MANAGEMENT/VAR•VAR, by various authors•Value at Risk, by Philippe Jorion•RiskMetrics Technical Document RiskMetrics Group•Risk and Asset Allocation by Attilio MeucciSAS/S/S-PLUS•The Little SAS Book: A Primer, Third Edition by Lora D. Delwiche and Susan J. Slaughter •Modeling Financial Time Series with S-PLUS•Statistical Analysis of Financial Data in S-PLUS•Modern Applied Statistics with SHANDS ON•Implementing Derivative Models, by Les Clewlow, Chris Strickland•The Complete Guide to Option Pricing Formulas, by Espen Gaarder HaugNOT ENOUGH YET?•Energy Derivatives, by Les Clewlow, Chris Strickland,•Hull-White on Derivatives, by John Hull, Alan White•Exotic Options: The State of the Art, by Les Clewlow (Editor), Chris Strickland (Editor)•Market Models, by C.O. Alexander•Pricing, Hedging, and Trading Exotic Options, by Israel Nelken•Modelling Fixed Income Securities and Interest Rate Options, by Robert A. Jarrow•Black-Scholes and Beyond, by Neil A. Chriss•Risk Management and Analysis: Measuring and Modelling Financial Risk, by Carol Alexander •Mastering Risk: Volume 2 - Applications: Your Single-Source Guide to Becoming a Master of Risk, by Carol Alexander。

新编金融英语教程 Chapter6 Financial Markets

Overview of the Financial Markets

CONTENTS

6.1 L e a d - i n 6.2 K e y Po i n t s 6.3 L a n g u a g e N o t e s 6.4 F o l l o w - u p Ta s k s 6.5 E x t e n d e d Ta s k s

6.3 Language Notes

III. Sentences

1. Financial markets are typically defined by having transparent pricing, basic regulations on trading, costs and fees, and market forces determining the prices of securities that trade.

2. Financial markets can be classified as debt or equity markets, as primary or secondary markets, as exchanges and Over-the-Counter markets, as money or capital markets, or as spot or futures and forward markets.

discuss the various functions of the financial market.

6.2 Key Points

6.2.1 Definition of Financial Markets

¥$

Financial Markets

Calculus I

Calculus ICalculus, also known as mathematical analysis, is a branch of mathematics that deals with the study of rates of change and how things change over time. It is a fundamental mathematical tool that has become essential in many fields such as physics, engineering, economics, and biology. In this essay, we will explore Calculus I, which is the introductory course for Calculus.The study of Calculus is divided into two main branches: differential calculus and integral calculus. Differential calculus is concerned with the study of rates of change, while integral calculus is concerned with the study of accumulation. Calculus I focuses on the fundamental concepts of differential calculus.One of the key ideas in Calculus I is the concept of limit. A limit is the value that a function approaches as the independent variable approaches a certain value. Limits are an essential tool for studying the behavior of functions, especially at points where the function may not be defined.Another important concept in Calculus I is the derivative. The derivative of a function is the rate of change of the function at a particular point. It is defined as the limit of the difference quotient as the change in the independent variable approaches zero. The derivative is a fundamental concept in Calculus and is used extensively in many fields, including physics, engineering, and economics.The derivative has many important properties, including the power rule, product rule, quotient rule, and chain rule. These rules allowus to find the derivative of complicated functions quickly and efficiently.The derivative also has many applications, including optimization problems and finding the location of maximum and minimum values of a function. For example, in economics, the derivative is used to find the marginal cost and marginal revenue of a company. In physics, the derivative is used to find the instantaneous velocity and acceleration of an object.Another important concept in Calculus I is the notion of differentiation. Differentiation is the process of finding the derivative of a function. It is an integral part of Calculus and is used extensively in many fields.One of the most important applications of differentiation is in the study of optimization problems. Optimization problems involve finding the maximum or minimum value of a function subject to certain constraints. For example, in economics, firms try to maximize their profits subject to certain constraints, such as the cost of production.Integration is the second branch of Calculus, and it deals with finding the area under a curve. Integration is the inverse of differentiation, and it is used extensively in many fields, including physics and engineering.One of the most important applications of integration is in the study of volumes and areas. For example, in physics, the volume of a solid can be found by integrating the area under the curve of itscross-section. In engineering, the area of an irregular shape can be found by integrating the area under the curve of its boundary.Calculus I also covers important topics such as limits, continuity, and trigonometric functions. Limits are used extensively in Calculus to study the behavior of functions. Continuity is a fundamental concept in Calculus that ensures that a function is well-behaved and has no abrupt changes.Trigonometric functions are essential in Calculus because they are used extensively in the study of differential equations, which are equations that involve derivatives. Differential equations are used to model many real-world phenomena, such as the growth of a population and the spread of diseases.In conclusion, Calculus I is an essential course for any student studying mathematics, physics, engineering, or economics. It provides a solid foundation for more advanced courses in Calculus and other fields. The concepts of differential calculus, such as limits, derivatives, and differentiation, are fundamental in the study of many real-world problems. The concepts covered in Calculus I, such as optimization and integration, have many applications in numerous fields and are essential for solving problems in many areas of science and engineering.In addition to the topics mentioned above, Calculus I also covers related rates, which are useful in real-world scenarios where things are changing at different rates. For example, if you are filling a pool with water and you want to know how fast the water level is rising, you would use related rates. This involves finding the relationship between the rates of change of different variables and using this relationship todetermine one rate when the other rate is known.Another important concept in Calculus I is the Mean Value Theorem. This theorem states that if a function is continuous on a closed interval and differentiable on the open interval, then there exists a point in the interval where the derivative is equal to the average rate of change of the function over the interval. This theorem has applications in many areas, including economics, where it is used to prove the existence of equilibrium prices.Calculus I also covers curve sketching, which involves studying the behavior of a function as it approaches zero and infinity, finding its intercepts, and determining where it is increasing or decreasing. This is important in many fields as it allows us to understand the behavior of functions and predict their future values.One of the most important applications of Calculus I is in physics, where it is used extensively in studying motion. The concepts of calculus are used to determine the velocity, acceleration, and position of an object at any given point in time. Understanding these concepts is essential in fields such as aerospace engineering, where the motion of objects in space is critical to the success of missions.Calculus I is also used extensively in engineering, especially in the design and analysis of systems. For example, in electrical engineering, calculus is used to determine the power consumed by a circuit, while in civil engineering, it is used to calculate the stress on structures such as bridges and buildings. Calculus is also essential in chemical engineering, where it is used to determine therate of chemical reactions.In economics, calculus is used to model and analyze various economic phenomena, such as supply and demand, consumer behavior, and production optimization. The concepts of calculus are essential in understanding the dynamics of markets and the behavior of firms in different situations.Calculus I has numerous real-life applications, from modeling the growth of populations to understanding the spread of diseases. It is used in biostatistics to determine the probability of an individual developing a certain disease and in epidemiology to model the spread of infectious diseases. In ecology, calculus is used to study predator-prey relationships and competition between species.In the field of finance, calculus is used to determine the value of financial securities such as stocks and bonds. Understanding the concepts of calculus is essential in the field of quantitative finance, which involves using mathematical models to predict the behavior of financial markets.Overall, Calculus I is a fundamental course in mathematics that teaches students the basic concepts of differential calculus, including limits and derivatives, and their applications in various fields. It provides a solid foundation for more advanced courses in Calculus and other related fields. The concepts covered in Calculus I have numerous applications in many fields, including physics, engineering, economics, and biology, making it an essential tool for solving real-world problems.。

安徽省宿州市省、市示范高中2022-2023 学年高一下学期期中考试英语试题

安徽省宿州市省、市示范高中2022-2023 学年高一下学期期中考试英语试题1. Where is Amy now?A.In Seoul. B.In Beijing. C.In London.2. What does the man mean?A.His mother likes apple pie.B.The apple pie tastes very good.C.He’ll make apple pies for his mother.3. Why does the woman talk to David?A.To make an apology. B.To ask for a favor. C.To invite him over.4. What are the speakers talking about?A.A strong team. B.A wonderful game. C.A great sportsman.5. What will the woman do for the man?A.Teach him cleaning skills.B.Find him a new apartment.C.Help him clean his apartment.6. 听下面一段较长对话,回答以下小题。

1. Who is the woman speaking to?A.Her son. B.Her husband. C.A salesman.2. Where is the washroom?A.On the 5th floor. B.On the 4th floor. C.On the 3rd floor.7. 听下面一段较长对话,回答以下小题。

1. What does the man plan to do this afternoon?A.Go swimming. B.Go to class. C.Go to the library.2. What does Mr. Smith probably teach?A.History. B.Chemistry. C.Math.3. What does the woman offer to do for the man?A.Collect information for his paper.B.Help him with his chemistry.C.Teach him to study math.8. 听下面一段较长对话,回答以下小题。

公司理财(罗斯)第1章(英文

03 Valuation Basis

The concept and significance of valuation

要点一

Definition

Valuation is the process of estimating the worth of an asset or a company, typically through the use of financial metrics and analysis.

The Time Value of Money

金融数学简介

Kushner and Dupuis, Numerical Methods for Stochastic Control Problems in Continuous Time, 1992. Kushner's Markov chain approximation method是控制论里最有用的算法

金融数学里面用的主要是随机控制,和粘性解(因为operator is often degenerate)

经典的随机控制书是

1.FLEMING and RISHEL, (1975) Deterministic and Stochastic Optimal Control.

ROGERS and TALAY, Numerical Methods in Financial Mathematics. 1997.论文集

Kloeden and Platen, Numerical Solution of Stochastic Differential Equations, 1997. 偏理论,实用性差一点

主要的研究内容和拟重点解决的问题包括:

(1)有价证券和证券组合的定价理论

发展有价证券(尤其是期货、期权等衍生工具)的定价理论。所用的数学方法主要是提出合适的随机微分方程或随机差分方程模型,形成相应的倒向方程。建立相应的非线性Feynman一Kac公式,由此导出非常一般的推广的Black一Scho1es定价公式。所得到的倒向方程将是高维非线性带约束的奇异方程。

粘性解的标准文献是

1. Crandall, Ishii and Lions, User's guide to viscosity solutions of second order partial differential equations, Bull. Amer. Math. Soc. 27 (1992),

Chap022公司理财罗斯英文原书第九版底2章

Option Premium

=

Intrinsic Value

+ Speculative Value

22-14

Call Option Payoffs

60

Option payoffs ($)

40

20

20 –20

40

50

60

80

100

120 Stock price ($)

–40

Exercise price = $50

22-9

Put Option Pricing at Expiry

At expiry, an American put option is worth the same as a European option with the same characteristics. If the put is in-the-money, it is worth E – ST. If the put is out-of-the-money, it is worthless. P = Max[E – ST, 0]

Option Quotes

In-the-Money

At-the-Money

Exercising the option would result in a zero payoff (i.e., exercise price equal to spot price). Exercising the option would result in a negative payoff.

22-18

Option Quotes

This option has a strike price of $135;

《微积分英文》课件 (2)

Types of Limits

One-sided limits

Limits approached

from one direction

Limits at infinity

Behavior of functions at

infinity

● 02

第2章 Limits and Continuity

01 Definition of a limit

Explanation of what a limit is

02 Properties of limits

Key characteristics of limits

03 Calculating limits algebraically

Graphing functions by analyzing their derivatives and key points

Higher Order Derivatives

Second derivative

Rate of change of the rate of

change

nth derivative

● 03

第3章 Differentiation

Derivatives and Rates of

Change

A derivative is defined as the rate of change of a function at a given point. Notation for derivatives includes symbols such as f'(x) or dy/dx. Derivatives can be interpreted as rates of change in various realworld applications.

AP Calculus Chapter 01 Function函数

Chapter 1 Function函数【Vocabulary 词汇梳理】sum and difference formula [s ʌm ənd ˈdɪfr əns ˈfɔːrmjəl ə] (角)和差公式sin(x ± y )= sin x cos y ± cos x sin y polar equation[ˈpo ʊl ər ɪˈkwe ɪʒn]极坐标方程[引] vertex 顶点polar coordinate [ˈpoʊl ər ko ʊˈɔːrdɪne ɪt] 极坐标【导图】A. DEFINITIONS 定义A1. DefinitionsA function f is a correspondence that associates with each element a of a set called the domain(定义域) one and only one element b of a set called the range (值域). We write f(a)=bto indicate that b is the value of f at a . The elements in the domain are called inputs, and those in the range are called outputs.A function is often represented by an equation, a graph, or a table . A vertical line cuts the graph of a function in at most one point . Example 1The domain of f (x )=x 2−2 is the set of all real numbers, its range is the set of all reals greater than or equal to −2.Example 2Find the domains of (a)f (x )=4x−1; (b) g (x )=xx 2−9; (c) ℎ(x )=√4−xxSolution:(a) The domain of f (x )=4x−1 is the set of all reals except x =1 (which we shorten to “x ≠−1”).(b) The domain of g(x)=xx2−9is x≠3,−3.(c) The domain of ℎ(x)=√4−xxis x≤4,x≠0(which is a short way of writing {x|x is real,x<0 or 0<x≤4}).A2. Operatin of Function函数的运算Two functions f and g with the same domain may be combined to yield their sum and difference: f(x)+g(x)and f(x)−g(x) , also written as (f+g)(x)and (f−g)(x) , respectively; or their product and quotient: f(x)g(x)and f(x) /g(x), also written as (fg)(x) and (f/g)(x), respectively. The quotient is defined for all x in the shared domain except those values for which g(x), the denominator, equals zero.Example 3If f(x)=x2−4x and g(x)=x+1, then find f(x)g(x)and g(x)f(x).Solution:f(x) g(x)=x2−4xx+1and has domain x≠−1;g(x) f(x)=x+1x2−4x=x+1x(x−4)and has domain x≠0,4.A3. Composite Functions复合函数The composition (or composite) of f with g, written as f(g(x))and read as “f of g of x,” is the function obtained by replacing x wherever it occurs in f(x)by g(x). We also write (f∘g)(x)for f(g(x). The domain of (f∘g)(x)is the set of all x in the domain of g for which g(x)is in the domain of f. In general,f(g(x))≠g(f(x)).Example 4AIf f(x)=2x−1and g(x)=x2, then does f(g(x))=g(f(x))?Solution:f(g(x)=2(x2)−1=2x2−1g(f(x))=(2x−1)2=4x2−4x+1.In general, f(g(x))≠g(f(x)).Example 4BIf f(x)=4x2−1and g(x)=√x, find f(g(x))and g(f(x)).Solution:f(g(x))=4x−1 (x≥0);g(f(x))=√4x2−1 (|x|≥12).A4. The parity of functions函数的奇偶性A function f is oddeven if, for all x in the domain of f,f(−x)=−f(x)f(−x)=f(x).The graph of an odd function is symmetric about the origin; the graph of an even function is symmetric about the y-axis.Example 5x3and g(x)=3x2−1are shown in Figure 1-1; f(x)is odd, The graphs of f(x)=12g(x)even.Figure 1-1A5. One-to-one一一映射If a function yields a single output for each input and also yields a single input for every output, then f is said to be one-to-one. Geometrically this means that any horizontal line cuts the graph off in at most one point. The function sketched at the left in Figure N1-1 is one-to-one; the function sketched at the right is not. A function that is increasing (or decreasing) on an interval I is one-to-one on that interval.A6. Inverse Functions反函数If f is one-to-one with domain X and range Y, then there is a function f−1, with domain Y and range X, such thatf−1(y0)=x0if and only if f(x0)=y0.The function f−1is the inverse of f. It can be shown that f−1is also one-to-one and that its inverse is f. The graphs of a function and its inverse are symmetric with respect to the line y= x.Example 6Find the inverse of the one-to-one function f(x)=x3−1.Solution:Interchange x and y: x=y3−13=f−1(x)Solve for y: y=√x+1Figure 1-2Note that the graphs of f and f−1in Figure N1-2 are mirror images, with the line y=x as the mirror.A7. Intercepte of axis函数的截距The zeros of a function f are the values of x for which f(x)=0; they are the x-intercepts of the graph of y=f(x).Example 7Find zeros of f(x)=x4−2x2.Solution:The zeros are the x′s for which x4−2x2=0. The function has three zeros, sincex x4−2x2=x2(x2−2)equals zero if x=0,±√2.B. SPECIAL FUNCTIONS 特殊函数The absolute-value function f(x)=|x|and the greatest-integer function g(x)=[x]are sketched in Figure N1-3.Figure 1-3Example 8Let f(x)=x3−3x2+2. Graph the following functions on your calculator in the window [−3,3]×[−3,3]: (a) y=f(x); (b) y=|f(x)|; (c) y=f(|x|).Solution:(a) f=f(x)(b) y=|f(x)|(c) y=f(|x|)Note how the graph for (b) and (c) compare with the graph for (a).C. POLYNOMIAL AND OTHER RATIONAL FUNCTIONS 多项式函数和其他有理函数C1. Power Function幂函数y=xμ(μ is a constant)(1) When μ=n(where n is a positive integer)When n is even, the function is also an even function (偶函数);When n is odd, the function is also an odd function (奇函数);(where n is a positive integer)(2) When μ=1nWhen n is even, the function is also an even function and the domain is [ 0,+∞);When n is odd, the domain of the function is (−∞,+∞);The following figure are the graphs of the functions when μ=−1,12,1,2.C2. Polynomial Functlons 多项式函数A polynomial function is of the formf(x)=a0x n+a1x n−1+a2x n−2+⋯+a n−1x+a nwhere n is a positive integer or zero, and the a k’s, the coefficients, are constants. If a0≠0,the degree of the polynomial is n.A linear function(一次函数,线性函数), f(x)=mx+b, is of the first degree; its graph is a straight line with slope m, the constant rate of change of f(x)(or y) with respect to x, and b is the line's y-intercept.A quadratic function(二次函数), f(x)=ax2+bx+c, has degree 2; its graph is a parabolathat opens up if a > 0, down if a < 0, and whose axis is the line x=−b2a.A cubic(三次函数), f(x)=a0x3+a1x2+a2x+a3, has degree 3; calculus enables us tosketch its graph easily; and so on. The domain of every polynomial is the set of all reals.C3. Rational Functions 有理函数A rational function is of the formf(x)=P(x) Q(x)where P(x)and Q(x)are polynomials. The domain of f is the set of all reals for which Q(x)≠0.D. TRIGONOMETRIC FUNCTIONS 三角函数D2. Formulas for operation以上公式能够全部掌握最好,因为西方国家(特别是美国)很重视三角函数的学习,对三角函数的要求比在国内高考还高,例如在国内,我们基本上只需掌握sin,cos,tan三个函数就可以了,但是在国外六个三角函数都要求熟练掌握。

[平衡计分卡]金融数学专业

![[平衡计分卡]金融数学专业](https://img.taocdn.com/s3/m/3695735c0c22590103029d30.png)

(平衡计分卡)金融数学专业金融数学BSc(Hons)FinancialMathematics内容包含:(中文)•课程介绍•课程结构(每年具体的学习内容)•职业方向•哪些大学于这些专业有优势金融数学现状:金融数学以及金融工程专业是英国近俩年才新兴的热门专业:主要包括股票市场分析、投资组合分析、期货和期权、金融风险管理等课程。

持有金融数学学位的人才于市场上炙手可热,基本上全部被各大投资银行、基金管理公司、保险公司、风险投资公司所聘用。

北京大学金融数学系王铎教授于2003年底指出:“金融数学这门新兴的交叉学科已经成为国际金融界的壹枝奇葩。

”“但遗憾的是,我国关联人才的培养,才刚刚起步。

当下,既懂金融又懂数学的复合型人才相当稀缺。

目前国内不少高校均陆续开展了和金融数学关联的教学,但毕业的学生远远满足不了整个市场的需求。

”享有金融数学专业盛名的大学:由于是新兴专业,所以没有具体的专业排名,可是大家能够综合金融和数学俩个专业的排名作为参考。

Mathematics数学排名1Oxford 5*C 528 87% 88% 96 StAndrews 5A 472 84% 76% 89.20 Birmingham 4B 428 82% 78% 85.41 Bristol 5*A 469 69% 79% 84.9 5 Sheffield 5C 395 81% 69% 81.3 1 Manchester 4B 448 54% 79.7 3 Aston 326 78% 79.1 5 Leeds 5B 412 72% 69% 78.9 7 Liverpool 4A 379 77% 61% 78.2 9 Kent 5*D 286 73% 84% 77.53 SheffieldHallam 247 89% 76% 72.8Accounting&Finance会计金融排名21来源于泰晤士报网:/tol_gug/gooduniversityguide.php?subject=MATHEMATICS2来源于泰晤士报网:/tol_gug/gooduniversityguide.php?sort=TOTAL&subject=ACCOUNTINGLondonSchoolofEconomics 5*A 464 72% 87% 99. Exeter 5D 370 91% 80% 99. Manchester 5*A 396 80% 70% 97. Birmingham 4D 380 86% 73% 93. Bristol 5B 408 68% 81% 89. Leeds 5C 396 72% 79% 89. Sheffield 4B 358 75% 71% 87. Kent 3aC 327 75% 77% 85. Bradford 4C 223 82% 62% 83. Liverpool 3aA 374 75% 49% 83 Salford 3aB 295 79% 54% 79. LiverpoolJohnMoores 3bE 231 78% 64% 77.SheffieldHallam 3aF 260 79% 50% 75. Kingston 249 78% 53% 73. ManchesterMetropolitan 246 75% 57% 72. Huddersfield 3bE 232 73% 52% 71.LeedsMetropolitan 257 64% 49% 64.英国享有知名金融数学专业的大学有:课程介绍及结构1:以谢菲尔德大学为例,此专业是为了给学生创造壹个数学知识和金融背景相结合的课程,课程包含了纯数学,应用数学,概率和统计,且把它们运用到企业,商务和经济学中。

罗斯《公司理财》第9版精要版英文原书课后部分章节答案

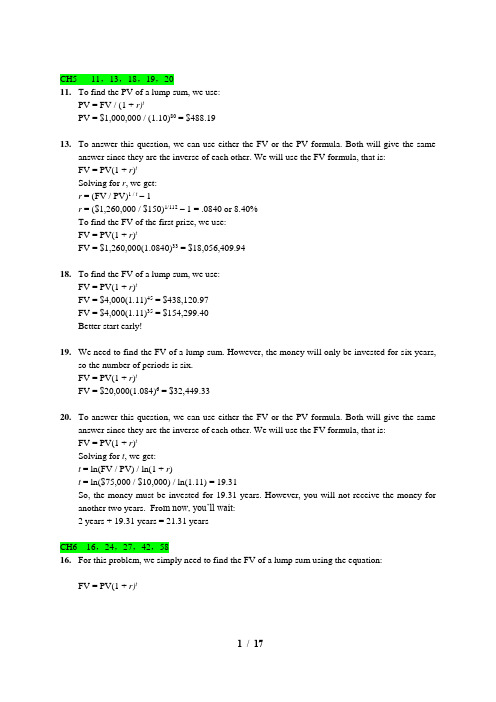

CH5 11,13,18,19,2011.To find the PV of a lump sum, we use:PV = FV / (1 + r)tPV = $1,000,000 / (1.10)80 = $488.1913.To answer this question, we can use either the FV or the PV formula. Both will give the sameanswer since they are the inverse of each other. We will use the FV formula, that is:FV = PV(1 + r)tSolving for r, we get:r = (FV / PV)1 / t– 1r = ($1,260,000 / $150)1/112– 1 = .0840 or 8.40%To find the FV of the first prize, we use:FV = PV(1 + r)tFV = $1,260,000(1.0840)33 = $18,056,409.9418.To find the FV of a lump sum, we use:FV = PV(1 + r)tFV = $4,000(1.11)45 = $438,120.97FV = $4,000(1.11)35 = $154,299.40Better start early!19. We need to find the FV of a lump sum. However, the money will only be invested for six years,so the number of periods is six.FV = PV(1 + r)tFV = $20,000(1.084)6 = $32,449.3320.To answer this question, we can use either the FV or the PV formula. Both will give the sameanswer since they are the inverse of each other. We will use the FV formula, that is:FV = PV(1 + r)tSolving for t, we get:t = ln(FV / PV) / ln(1 + r)t = ln($75,000 / $10,000) / ln(1.11) = 19.31So, the money must be invested for 19.31 years. However, you will not receive the money for another two years. Fro m now, you’ll wait:2 years + 19.31 years = 21.31 yearsCH6 16,24,27,42,5816.For this problem, we simply need to find the FV of a lump sum using the equation:FV = PV(1 + r)tIt is important to note that compounding occurs semiannually. To account for this, we will divide the interest rate by two (the number of compounding periods in a year), and multiply the number of periods by two. Doing so, we get:FV = $2,100[1 + (.084/2)]34 = $8,505.9324.This problem requires us to find the FVA. The equation to find the FVA is:FVA = C{[(1 + r)t– 1] / r}FVA = $300[{[1 + (.10/12) ]360 – 1} / (.10/12)] = $678,146.3827.The cash flows are annual and the compounding period is quarterly, so we need to calculate theEAR to make the interest rate comparable with the timing of the cash flows. Using the equation for the EAR, we get:EAR = [1 + (APR / m)]m– 1EAR = [1 + (.11/4)]4– 1 = .1146 or 11.46%And now we use the EAR to find the PV of each cash flow as a lump sum and add them together: PV = $725 / 1.1146 + $980 / 1.11462 + $1,360 / 1.11464 = $2,320.3642.The amount of principal paid on the loan is the PV of the monthly payments you make. So, thepresent value of the $1,150 monthly payments is:PVA = $1,150[(1 – {1 / [1 + (.0635/12)]}360) / (.0635/12)] = $184,817.42The monthly payments of $1,150 will amount to a principal payment of $184,817.42. The amount of principal you will still owe is:$240,000 – 184,817.42 = $55,182.58This remaining principal amount will increase at the interest rate on the loan until the end of the loan period. So the balloon payment in 30 years, which is the FV of the remaining principal will be:Balloon payment = $55,182.58[1 + (.0635/12)]360 = $368,936.5458.To answer this question, we should find the PV of both options, and compare them. Since we arepurchasing the car, the lowest PV is the best option. The PV of the leasing is simply the PV of the lease payments, plus the $99. The interest rate we would use for the leasing option is thesame as the interest rate of the loan. The PV of leasing is:PV = $99 + $450{1 – [1 / (1 + .07/12)12(3)]} / (.07/12) = $14,672.91The PV of purchasing the car is the current price of the car minus the PV of the resale price. The PV of the resale price is:PV = $23,000 / [1 + (.07/12)]12(3) = $18,654.82The PV of the decision to purchase is:$32,000 – 18,654.82 = $13,345.18In this case, it is cheaper to buy the car than leasing it since the PV of the purchase cash flows is lower. To find the breakeven resale price, we need to find the resale price that makes the PV of the two options the same. In other words, the PV of the decision to buy should be:$32,000 – PV of resale price = $14,672.91PV of resale price = $17,327.09The resale price that would make the PV of the lease versus buy decision is the FV of this value, so:Breakeven resale price = $17,327.09[1 + (.07/12)]12(3) = $21,363.01CH7 3,18,21,22,313.The price of any bond is the PV of the interest payment, plus the PV of the par value. Notice thisproblem assumes an annual coupon. The price of the bond will be:P = $75({1 – [1/(1 + .0875)]10 } / .0875) + $1,000[1 / (1 + .0875)10] = $918.89We would like to introduce shorthand notation here. Rather than write (or type, as the case may be) the entire equation for the PV of a lump sum, or the PVA equation, it is common to abbreviate the equations as:PVIF R,t = 1 / (1 + r)twhich stands for Present Value Interest FactorPVIFA R,t= ({1 – [1/(1 + r)]t } / r )which stands for Present Value Interest Factor of an AnnuityThese abbreviations are short hand notation for the equations in which the interest rate and the number of periods are substituted into the equation and solved. We will use this shorthand notation in remainder of the solutions key.18.The bond price equation for this bond is:P0 = $1,068 = $46(PVIFA R%,18) + $1,000(PVIF R%,18)Using a spreadsheet, financial calculator, or trial and error we find:R = 4.06%This is the semiannual interest rate, so the YTM is:YTM = 2 4.06% = 8.12%The current yield is:Current yield = Annual coupon payment / Price = $92 / $1,068 = .0861 or 8.61%The effective annual yield is the same as the EAR, so using the EAR equation from the previous chapter:Effective annual yield = (1 + 0.0406)2– 1 = .0829 or 8.29%20. Accrued interest is the coupon payment for the period times the fraction of the period that haspassed since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six months is one-half of the annual coupon payment. There are four months until the next coupon payment, so two months have passed since the last coupon payment. The accrued interest for the bond is:Accrued interest = $74/2 × 2/6 = $12.33And we calculate the clean price as:Clean price = Dirty price – Accrued interest = $968 – 12.33 = $955.6721. Accrued interest is the coupon payment for the period times the fraction of the period that haspassed since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six months is one-half of the annual coupon payment. There are two months until the next coupon payment, so four months have passed since the last coupon payment. The accrued interest for the bond is:Accrued interest = $68/2 × 4/6 = $22.67And we calculate the dirty price as:Dirty price = Clean price + Accrued interest = $1,073 + 22.67 = $1,095.6722.To find the number of years to maturity for the bond, we need to find the price of the bond. Sincewe already have the coupon rate, we can use the bond price equation, and solve for the number of years to maturity. We are given the current yield of the bond, so we can calculate the price as: Current yield = .0755 = $80/P0P0 = $80/.0755 = $1,059.60Now that we have the price of the bond, the bond price equation is:P = $1,059.60 = $80[(1 – (1/1.072)t ) / .072 ] + $1,000/1.072tWe can solve this equation for t as follows:$1,059.60(1.072)t = $1,111.11(1.072)t– 1,111.11 + 1,000111.11 = 51.51(1.072)t2.1570 = 1.072tt = log 2.1570 / log 1.072 = 11.06 11 yearsThe bond has 11 years to maturity.31.The price of any bond (or financial instrument) is the PV of the future cash flows. Even thoughBond M makes different coupons payments, to find the price of the bond, we just find the PV of the cash flows. The PV of the cash flows for Bond M is:P M= $1,100(PVIFA3.5%,16)(PVIF3.5%,12) + $1,400(PVIFA3.5%,12)(PVIF3.5%,28) + $20,000(PVIF3.5%,40)P M= $19,018.78Notice that for the coupon payments of $1,400, we found the PVA for the coupon payments, and then discounted the lump sum back to today.Bond N is a zero coupon bond with a $20,000 par value, therefore, the price of the bond is the PV of the par, or:P N= $20,000(PVIF3.5%,40) = $5,051.45CH8 4,18,20,22,24ing the constant growth model, we find the price of the stock today is:P0 = D1 / (R– g) = $3.04 / (.11 – .038) = $42.2218.The price of a share of preferred stock is the dividend payment divided by the required return.We know the dividend payment in Year 20, so we can find the price of the stock in Year 19, one year before the first dividend payment. Doing so, we get:P19 = $20.00 / .064P19 = $312.50The price of the stock today is the PV of the stock price in the future, so the price today will be: P0 = $312.50 / (1.064)19P0 = $96.1520.We can use the two-stage dividend growth model for this problem, which is:P0 = [D0(1 + g1)/(R –g1)]{1 – [(1 + g1)/(1 + R)]T}+ [(1 + g1)/(1 + R)]T[D0(1 + g2)/(R –g2)]P0= [$1.25(1.28)/(.13 – .28)][1 – (1.28/1.13)8] + [(1.28)/(1.13)]8[$1.25(1.06)/(.13 – .06)]P0= $69.5522.We are asked to find the dividend yield and capital gains yield for each of the stocks. All of thestocks have a 15 percent required return, which is the sum of the dividend yield and the capital gains yield. To find the components of the total return, we need to find the stock price for each stock. Using this stock price and the dividend, we can calculate the dividend yield. The capital gains yield for the stock will be the total return (required return) minus the dividend yield.W: P0 = D0(1 + g) / (R–g) = $4.50(1.10)/(.19 – .10) = $55.00Dividend yield = D1/P0 = $4.50(1.10)/$55.00 = .09 or 9%Capital gains yield = .19 – .09 = .10 or 10%X: P0 = D0(1 + g) / (R–g) = $4.50/(.19 – 0) = $23.68Dividend yield = D1/P0 = $4.50/$23.68 = .19 or 19%Capital gains yield = .19 – .19 = 0%Y: P0 = D0(1 + g) / (R–g) = $4.50(1 – .05)/(.19 + .05) = $17.81Dividend yield = D1/P0 = $4.50(0.95)/$17.81 = .24 or 24%Capital gains yield = .19 – .24 = –.05 or –5%Z: P2 = D2(1 + g) / (R–g) = D0(1 + g1)2(1 + g2)/(R–g2) = $4.50(1.20)2(1.12)/(.19 – .12) = $103.68P0 = $4.50 (1.20) / (1.19) + $4.50 (1.20)2/ (1.19)2 + $103.68 / (1.19)2 = $82.33Dividend yield = D1/P0 = $4.50(1.20)/$82.33 = .066 or 6.6%Capital gains yield = .19 – .066 = .124 or 12.4%In all cases, the required return is 19%, but the return is distributed differently between current income and capital gains. High growth stocks have an appreciable capital gains component but a relatively small current income yield; conversely, mature, negative-growth stocks provide a high current income but also price depreciation over time.24.Here we have a stock with supernormal growth, but the dividend growth changes every year forthe first four years. We can find the price of the stock in Year 3 since the dividend growth rate is constant after the third dividend. The price of the stock in Year 3 will be the dividend in Year 4, divided by the required return minus the constant dividend growth rate. So, the price in Year 3 will be:P3 = $2.45(1.20)(1.15)(1.10)(1.05) / (.11 – .05) = $65.08The price of the stock today will be the PV of the first three dividends, plus the PV of the stock price in Year 3, so:P0 = $2.45(1.20)/(1.11) + $2.45(1.20)(1.15)/1.112 + $2.45(1.20)(1.15)(1.10)/1.113 + $65.08/1.113 P0 = $55.70CH9 3,4,6,9,153.Project A has cash flows of $19,000 in Year 1, so the cash flows are short by $21,000 ofrecapturing the initial investment, so the payback for Project A is:Payback = 1 + ($21,000 / $25,000) = 1.84 yearsProject B has cash flows of:Cash flows = $14,000 + 17,000 + 24,000 = $55,000during this first three years. The cash flows are still short by $5,000 of recapturing the initial investment, so the payback for Project B is:B: Payback = 3 + ($5,000 / $270,000) = 3.019 yearsUsing the payback criterion and a cutoff of 3 years, accept project A and reject project B.4.When we use discounted payback, we need to find the value of all cash flows today. The valuetoday of the project cash flows for the first four years is:Value today of Year 1 cash flow = $4,200/1.14 = $3,684.21Value today of Year 2 cash flow = $5,300/1.142 = $4,078.18Value today of Year 3 cash flow = $6,100/1.143 = $4,117.33Value today of Year 4 cash flow = $7,400/1.144 = $4,381.39To find the discounted payback, we use these values to find the payback period. The discounted first year cash flow is $3,684.21, so the discounted payback for a $7,000 initial cost is:Discounted payback = 1 + ($7,000 – 3,684.21)/$4,078.18 = 1.81 yearsFor an initial cost of $10,000, the discounted payback is:Discounted payback = 2 + ($10,000 – 3,684.21 – 4,078.18)/$4,117.33 = 2.54 yearsNotice the calculation of discounted payback. We know the payback period is between two and three years, so we subtract the discounted values of the Year 1 and Year 2 cash flows from the initial cost. This is the numerator, which is the discounted amount we still need to make to recover our initial investment. We divide this amount by the discounted amount we will earn in Year 3 to get the fractional portion of the discounted payback.If the initial cost is $13,000, the discounted payback is:Discounted payback = 3 + ($13,000 – 3,684.21 – 4,078.18 – 4,117.33) / $4,381.39 = 3.26 years6.Our definition of AAR is the average net income divided by the average book value. The averagenet income for this project is:Average net income = ($1,938,200 + 2,201,600 + 1,876,000 + 1,329,500) / 4 = $1,836,325And the average book value is:Average book value = ($15,000,000 + 0) / 2 = $7,500,000So, the AAR for this project is:AAR = Average net income / Average book value = $1,836,325 / $7,500,000 = .2448 or 24.48%9.The NPV of a project is the PV of the outflows minus the PV of the inflows. Since the cashinflows are an annuity, the equation for the NPV of this project at an 8 percent required return is: NPV = –$138,000 + $28,500(PVIFA8%, 9) = $40,036.31At an 8 percent required return, the NPV is positive, so we would accept the project.The equation for the NPV of the project at a 20 percent required return is:NPV = –$138,000 + $28,500(PVIFA20%, 9) = –$23,117.45At a 20 percent required return, the NPV is negative, so we would reject the project.We would be indifferent to the project if the required return was equal to the IRR of the project, since at that required return the NPV is zero. The IRR of the project is:0 = –$138,000 + $28,500(PVIFA IRR, 9)IRR = 14.59%15.The profitability index is defined as the PV of the cash inflows divided by the PV of the cashoutflows. The equation for the profitability index at a required return of 10 percent is:PI = [$7,300/1.1 + $6,900/1.12 + $5,700/1.13] / $14,000 = 1.187The equation for the profitability index at a required return of 15 percent is:PI = [$7,300/1.15 + $6,900/1.152 + $5,700/1.153] / $14,000 = 1.094The equation for the profitability index at a required return of 22 percent is:PI = [$7,300/1.22 + $6,900/1.222 + $5,700/1.223] / $14,000 = 0.983We would accept the project if the required return were 10 percent or 15 percent since the PI is greater than one. We would reject the project if the required return were 22 percent since the PI is less than one.CH10 9,13,14,17,18ing the tax shield approach to calculating OCF (Remember the approach is irrelevant; the finalanswer will be the same no matter which of the four methods you use.), we get:OCF = (Sales – Costs)(1 – t C) + t C DepreciationOCF = ($2,650,000 – 840,000)(1 – 0.35) + 0.35($3,900,000/3)OCF = $1,631,50013.First we will calculate the annual depreciation of the new equipment. It will be:Annual depreciation = $560,000/5Annual depreciation = $112,000Now, we calculate the aftertax salvage value. The aftertax salvage value is the market price minus (or plus) the taxes on the sale of the equipment, so:Aftertax salvage value = MV + (BV – MV)t cVery often the book value of the equipment is zero as it is in this case. If the book value is zero, the equation for the aftertax salvage value becomes:Aftertax salvage value = MV + (0 – MV)t cAftertax salvage value = MV(1 – t c)We will use this equation to find the aftertax salvage value since we know the book value is zero.So, the aftertax salvage value is:Aftertax salvage value = $85,000(1 – 0.34)Aftertax salvage value = $56,100Using the tax shield approach, we find the OCF for the project is:OCF = $165,000(1 – 0.34) + 0.34($112,000)OCF = $146,980Now we can find the project NPV. Notice we include the NWC in the initial cash outlay. The recovery of the NWC occurs in Year 5, along with the aftertax salvage value.NPV = –$560,000 – 29,000 + $146,980(PVIFA10%,5) + [($56,100 + 29,000) / 1.105]NPV = $21,010.2414.First we will calculate the annual depreciation of the new equipment. It will be:Annual depreciation charge = $720,000/5Annual depreciation charge = $144,000The aftertax salvage value of the equipment is:Aftertax salvage value = $75,000(1 – 0.35)Aftertax salvage value = $48,750Using the tax shield approach, the OCF is:OCF = $260,000(1 – 0.35) + 0.35($144,000)OCF = $219,400Now we can find the project IRR. There is an unusual feature that is a part of this project.Accepting this project means that we will reduce NWC. This reduction in NWC is a cash inflow at Year 0. This reduction in NWC implies that when the project ends, we will have to increase NWC. So, at the end of the project, we will have a cash outflow to restore the NWC to its level before the project. We also must include the aftertax salvage value at the end of the project. The IRR of the project is:NPV = 0 = –$720,000 + 110,000 + $219,400(PVIFA IRR%,5) + [($48,750 – 110,000) / (1+IRR)5]IRR = 21.65%17.We will need the aftertax salvage value of the equipment to compute the EAC. Even though theequipment for each product has a different initial cost, both have the same salvage value. The aftertax salvage value for both is:Both cases: aftertax salvage value = $40,000(1 – 0.35) = $26,000To calculate the EAC, we first need the OCF and NPV of each option. The OCF and NPV for Techron I is:OCF = –$67,000(1 – 0.35) + 0.35($290,000/3) = –9,716.67NPV = –$290,000 – $9,716.67(PVIFA10%,3) + ($26,000/1.103) = –$294,629.73EAC = –$294,629.73 / (PVIFA10%,3) = –$118,474.97And the OCF and NPV for Techron II is:OCF = –$35,000(1 – 0.35) + 0.35($510,000/5) = $12,950NPV = –$510,000 + $12,950(PVIFA10%,5) + ($26,000/1.105) = –$444,765.36EAC = –$444,765.36 / (PVIFA10%,5) = –$117,327.98The two milling machines have unequal lives, so they can only be compared by expressing both on an equivalent annual basis, which is what the EAC method does. Thus, you prefer the Techron II because it has the lower (less negative) annual cost.18.To find the bid price, we need to calculate all other cash flows for the project, and then solve forthe bid price. The aftertax salvage value of the equipment is:Aftertax salvage value = $70,000(1 – 0.35) = $45,500Now we can solve for the necessary OCF that will give the project a zero NPV. The equation for the NPV of the project is:NPV = 0 = –$940,000 – 75,000 + OCF(PVIFA12%,5) + [($75,000 + 45,500) / 1.125]Solving for the OCF, we find the OCF that makes the project NPV equal to zero is:OCF = $946,625.06 / PVIFA12%,5 = $262,603.01The easiest way to calculate the bid price is the tax shield approach, so:OCF = $262,603.01 = [(P – v)Q – FC ](1 – t c) + t c D$262,603.01 = [(P – $9.25)(185,000) – $305,000 ](1 – 0.35) + 0.35($940,000/5)P = $12.54CH14 6、9、20、23、246. The pretax cost of debt is the YTM of the company’s bonds, so:P0 = $1,070 = $35(PVIFA R%,30) + $1,000(PVIF R%,30)R = 3.137%YTM = 2 × 3.137% = 6.27%And the aftertax cost of debt is:R D = .0627(1 – .35) = .0408 or 4.08%9. ing the equation to calculate the WACC, we find:WACC = .60(.14) + .05(.06) + .35(.08)(1 – .35) = .1052 or 10.52%b.Since interest is tax deductible and dividends are not, we must look at the after-tax cost ofdebt, which is:.08(1 – .35) = .0520 or 5.20%Hence, on an after-tax basis, debt is cheaper than the preferred stock.ing the debt-equity ratio to calculate the WACC, we find:WACC = (.90/1.90)(.048) + (1/1.90)(.13) = .0912 or 9.12%Since the project is riskier than the company, we need to adjust the project discount rate for the additional risk. Using the subjective risk factor given, we find:Project discount rate = 9.12% + 2.00% = 11.12%We would accept the project if the NPV is positive. The NPV is the PV of the cash outflows plus the PV of the cash inflows. Since we have the costs, we just need to find the PV of inflows. The cash inflows are a growing perpetuity. If you remember, the equation for the PV of a growing perpetuity is the same as the dividend growth equation, so:PV of future CF = $2,700,000/(.1112 – .04) = $37,943,787The project should only be undertaken if its cost is less than $37,943,787 since costs less than this amount will result in a positive NPV.23. ing the dividend discount model, the cost of equity is:R E = [(0.80)(1.05)/$61] + .05R E = .0638 or 6.38%ing the CAPM, the cost of equity is:R E = .055 + 1.50(.1200 – .0550)R E = .1525 or 15.25%c.When using the dividend growth model or the CAPM, you must remember that both areestimates for the cost of equity. Additionally, and perhaps more importantly, each methodof estimating the cost of equity depends upon different assumptions.Challenge24.We can use the debt-equity ratio to calculate the weights of equity and debt. The debt of thecompany has a weight for long-term debt and a weight for accounts payable. We can use the weight given for accounts payable to calculate the weight of accounts payable and the weight of long-term debt. The weight of each will be:Accounts payable weight = .20/1.20 = .17Long-term debt weight = 1/1.20 = .83Since the accounts payable has the same cost as the overall WACC, we can write the equation for the WACC as:WACC = (1/1.7)(.14) + (0.7/1.7)[(.20/1.2)WACC + (1/1.2)(.08)(1 – .35)]Solving for WACC, we find:WACC = .0824 + .4118[(.20/1.2)WACC + .0433]WACC = .0824 + (.0686)WACC + .0178(.9314)WACC = .1002WACC = .1076 or 10.76%We will use basically the same equation to calculate the weighted average flotation cost, except we will use the flotation cost for each form of financing. Doing so, we get:Flotation costs = (1/1.7)(.08) + (0.7/1.7)[(.20/1.2)(0) + (1/1.2)(.04)] = .0608 or 6.08%The total amount we need to raise to fund the new equipment will be:Amount raised cost = $45,000,000/(1 – .0608)Amount raised = $47,912,317Since the cash flows go to perpetuity, we can calculate the present value using the equation for the PV of a perpetuity. The NPV is:NPV = –$47,912,317 + ($6,200,000/.1076)NPV = $9,719,777CH16 1,4,12,14,171. a. A table outlining the income statement for the three possible states of the economy isshown below. The EPS is the net income divided by the 5,000 shares outstanding. The lastrow shows the percentage change in EPS the company will experience in a recession or anexpansion economy.Recession Normal ExpansionEBIT $14,000 $28,000 $36,400Interest 0 0 0NI $14,000 $28,000 $36,400EPS $ 2.80 $ 5.60 $ 7.28%∆EPS –50 –––+30b.If the company undergoes the proposed recapitalization, it will repurchase:Share price = Equity / Shares outstandingShare price = $250,000/5,000Share price = $50Shares repurchased = Debt issued / Share priceShares repurchased =$90,000/$50Shares repurchased = 1,800The interest payment each year under all three scenarios will be:Interest payment = $90,000(.07) = $6,300The last row shows the percentage change in EPS the company will experience in arecession or an expansion economy under the proposed recapitalization.Recession Normal ExpansionEBIT $14,000 $28,000 $36,400Interest 6,300 6,300 6,300NI $7,700 $21,700 $30,100EPS $2.41 $ 6.78 $9.41%∆EPS –64.52 –––+38.714. a.Under Plan I, the unlevered company, net income is the same as EBIT with no corporate tax.The EPS under this capitalization will be:EPS = $350,000/160,000 sharesEPS = $2.19Under Plan II, the levered company, EBIT will be reduced by the interest payment. The interest payment is the amount of debt times the interest rate, so:NI = $500,000 – .08($2,800,000)NI = $126,000And the EPS will be:EPS = $126,000/80,000 sharesEPS = $1.58Plan I has the higher EPS when EBIT is $350,000.b.Under Plan I, the net income is $500,000 and the EPS is:EPS = $500,000/160,000 sharesEPS = $3.13Under Plan II, the net income is:NI = $500,000 – .08($2,800,000)NI = $276,000And the EPS is:EPS = $276,000/80,000 sharesEPS = $3.45Plan II has the higher EPS when EBIT is $500,000.c.To find the breakeven EBIT for two different capital structures, we simply set the equationsfor EPS equal to each other and solve for EBIT. The breakeven EBIT is:EBIT/160,000 = [EBIT – .08($2,800,000)]/80,000EBIT = $448,00012. a.With the information provided, we can use the equation for calculating WACC to find thecost of equity. The equation for WACC is:WACC = (E/V)R E + (D/V)R D(1 – t C)The company has a debt-equity ratio of 1.5, which implies the weight of debt is 1.5/2.5, and the weight of equity is 1/2.5, soWACC = .10 = (1/2.5)R E + (1.5/2.5)(.07)(1 – .35)R E = .1818 or 18.18%b.To find the unlevered cost of equity we need to use M&M Proposition II with taxes, so:R E = R U + (R U– R D)(D/E)(1 – t C).1818 = R U + (R U– .07)(1.5)(1 – .35)R U = .1266 or 12.66%c.To find the cost of equity under different capital structures, we can again use M&MProposition II with taxes. With a debt-equity ratio of 2, the cost of equity is:R E = R U + (R U– R D)(D/E)(1 – t C)R E = .1266 + (.1266 – .07)(2)(1 – .35)R E = .2001 or 20.01%With a debt-equity ratio of 1.0, the cost of equity is:R E = .1266 + (.1266 – .07)(1)(1 – .35)R E = .1634 or 16.34%And with a debt-equity ratio of 0, the cost of equity is:R E = .1266 + (.1266 – .07)(0)(1 – .35)R E = R U = .1266 or 12.66%14. a.The value of the unlevered firm is:V U = EBIT(1 – t C)/R UV U = $92,000(1 – .35)/.15V U = $398,666.67b.The value of the levered firm is:V U = V U + t C DV U = $398,666.67 + .35($60,000)V U = $419,666.6717.With no debt, we are finding the value of an unlevered firm, so:V U = EBIT(1 – t C)/R UV U = $14,000(1 – .35)/.16V U = $56,875With debt, we simply need to use the equation for the value of a levered firm. With 50 percent debt, one-half of the firm value is debt, so the value of the levered firm is:V L = V U + t C(D/V)V UV L = $56,875 + .35(.50)($56,875)V L = $66,828.13And with 100 percent debt, the value of the firm is:V L = V U + t C(D/V)V UV L = $56,875 + .35(1.0)($56,875)V L = $76,781.25c.The net cash flows is the present value of the average daily collections times the daily interest rate, minus the transaction cost per day, so:Net cash flow per day = $1,276,275(.0002) – $0.50(385)Net cash flow per day = $62.76The net cash flow per check is the net cash flow per day divided by the number of checksreceived per day, or:Net cash flow per check = $62.76/385Net cash flow per check = $0.16Alternatively, we could find the net cash flow per check as the number of days the system reduces collection time times the average check amount times the daily interest rate, minusthe transaction cost per check. Doing so, we confirm our previous answer as:Net cash flow per check = 3($1,105)(.0002) – $0.50Net cash flow per check = $0.16 per checkThis makes the total costs:Total costs = $18,900,000 + 56,320,000 = $75,220,000The flotation costs as a percentage of the amount raised is the total cost divided by the amount raised, so:Flotation cost percentage = $75,220,000/$180,780,000 = .4161 or 41.61%8.The number of rights needed per new share is:Number of rights needed = 120,000 old shares/25,000 new shares = 4.8 rights per new share.Using P RO as the rights-on price, and P S as the subscription price, we can express the price per share of the stock ex-rights as:P X = [NP RO + P S]/(N + 1)a.P X = [4.8($94) + $94]/(4.80 + 1) = $94.00; No change.b. P X = [4.8($94) + $90]/(4.80 + 1) = $93.31; Price drops by $0.69 per share.。

Mathematics_for_Finance

Mathematics for Finance: An Introduction to Financial EngineeringAmerican Mathematical Monthly, The, Dec 2004 by Protter, PhilipMathematical finance (or financial engineering, as it is often known) is a young subject for mathematics, but is highly popular with students. No doubt the allure of being connected to vast sums of money is a part of the attraction. Yet it is a difficult subject, requiring a broad array of knowledge of subjects that are traditionally considered hard to learn.Forty years ago, options and what are now called "financial derivatives" were little known. Options were traded on the Chicago Board Options Exchange (CBOE), primarily for commodities such as pork bellies, orange juice, coffee, and precious metals. Let us take a minute to describe a situation where an option is useful. Imagine a small Indiana farmer raising pigs. The price is high now, but his pigs are only 80% grown. He can market them now and make a handsome profit, or he can wait until they are fully grown and make a larger profit if the price stays up, but end up making significantly less money if the price falls. He could solve the problem by buying a forward contract, locking in a prearranged price and thus a sure profit, but what if the price rises further? Then he will kick himself for having locked in the price. An option, on the other hand, gives him the right, but not the obligation, to sell his pigs at the prearranged price, thus guaranteeing him the nice profit but not excluding a potentially bigger one.The prices of options such as the one just described were set by the market: supply and demand. In the United States there is a fervent belief that the market knows best and, if left alone, will arrive at a fair and just price. There are many unspoken hypotheses involved with this belief, and in the case of commodities, several were violated. It will suffice to point out that small farmers were buying options sold by large banks and companies. In the early 1970s, Black, Scholes, and Merton showed that by using the ItO stochastic calculus and a simple model describing the dynamics of the price of a risky asset, one could arrive at a fair price for an option. They did this using a key idea: if one sells the option for $x, there is a hedging strategy by which one can use that $x to trade in the commodity over time until the option is due and end up with exactly what is owed to the option purchaser at the settlement time. There is no risk at all, except the implicit risk that the model for the dynamic price of the commodity is wrong. Therefore, if the market price is larger than $x, one can charge the market price and match the option and have money left over. If the market price is less than $x, one can buy the options and make money in reverse. It turned out that the market is often wrong, but the breakthrough of Black and Scholes went largely ignored by the financial players. This gradually changed, largely through the efforts of a few visionary people at Wells Fargo Bank, who worked not so much with commodities as with the (then) new concepts of portfolio insurance and index funds (see [2]).The option I described has the result of removing the risk for the pig farmer. For a (usually rather small) fee, he can buy what amounts to an insurance policy on the price of pork bellies. This is known as a transfer of risk: the option seller assumes the risk the farmer is not willing to assume, just as an insurance company assumes (for a fee) the financial risk of one's house burning down. This example also shows the utility of such insurance, since now the farmer will not slaughter the pigs before they are fully grown, and society as a whole will benefit (assuming that people eat pork). Once the methodology for pricing this transfer of risk became widely known, the concept spread widely. It has transformed modern business and arguably helped to create the financial boom years of the 1990s. One can now insure against currency fluctuations, dangerous drops in stock prices in one's portfolio, and all manner of (often fairly esoteric) business operations by this form of risk transfer. Options are also widely used for less virtuous goals, such as helping companies and executives avoid paying taxes, and of course for what amounts, simply, to gambling。

Letter of interest

Motivation LetterDear Sir or Madam,During my undergraduate studies, I have accumulated knowledge and skills to start my journey as international financial analyst. Since I love reading about current events, The Economist and Bloomberg became my favorite economics magazines outside of class. The most interesting research I have done was studying and modeling How Dynamic Economic Factors can Influence the Value of A Currency. I collected 6 currency indicators from years 2008-2015 and created a model to calculate the mathematical relation between British pound and US dollar and the other 5 indicators. After an in-depth analysis I found that: When central bank interest rate increases by 1 unit, the exchange rate increases by 9.086406; When GDP increases by 1 unit, rate rises by 2.531843; when the inverse rate of unemployment rise 1 unit, pound against dollar ascend 0.009526 and so on. My model lacked the influence of international political events, such as the risk of Grexit, which taught me to take a more global view at financial markets. Nevertheless, the professor still praised my performance as outstanding and even showed my report as an example to my classmates. Financial research and analysis bring me a lot of satisfaction and I am convinced that I will improve my analytic skills by attending your Master program in Finance.I strongly believe myself to be a competitive candidate for your program. During my college years, my curiosity in the financial industry and my striving for excellence secured me a solid academic foundations in finance, economics, statistics, mathematics, accounting and computer science. Major courses include Calculus, Linear Algebra, Probability and Statistics, Econometrics, Bank Accounting and International Finance. Within two and a half years I finished most of a 4 year program, with above average score and graduated as a top student in my class. Then I attended the exchange program of University of Warsaw in Poland for one year. Several courses I took in Warsaw were for master level students. I also demonstrated outstanding academic performance in those courses. At the graduation ceremony I’ll received Cum Laude Student of Anhui University of Finance and Economics.To became an analyst, the ability of mathematical modeling, anti-pressure and other valuable characters are essential. Be aware of that, I have honed my practical and analytical skills through contests. Usually 3 students take the contest as a group to solve a problem in unknown fields within 3 days, using WORD, EXCEL, EVIEWS, SPSS, and MATLAB, etc, and write an essay usually about 20 pages as our researchresults. The most interesting model I have built was for CUMCM in 2016, a question required to use geographic coordinate data of the shadow edge of a fixed stick on ground, to analyze possible location of the fixed stick. We got stuck on calculating latitude, finally I was inspired by an article on a foreign math organization website: The assumption of fixed stick is a horizontal sundial. Combing the shadow data of the stick with the movement regulation of erect stylus, I built a model and solved the problem. Although high pressure and overnight working keep burning my energy in contests, I always feel exciting and confident because of the encouragement of the other members and my ambition to become an analyst in near future. Up to now, I have took several elective courses and training related to mathematical modeling. What is more, I have participated in at least 5 national or international contest as team leader or member, acquiring 4 prizes. Thanks to the contests, I have built my systematic thinking habits and have acquired the ability to quickly identify and solve problems in diverse fields.My long term goal is to become an outstanding fund manager. The responsibilities of a fund manager not only involve creating fund's investing strategy, but also managing its portfolio trading activities. Although I have obtained fund qualification certificate, I feel that it is insufficient to achieve my goals. An overseas graduate program will be one of the steps towards accumulating theoretical knowledge and practical experience. First, I wish to participate in your program and earn CFA level one and level two. After my graduation, I hope to work in a western company as an analyst to obtain valuable professional experience and international insight. It could pave a way for my future career as a fund manager in China. Nowadays, China plays an increasingly important role globally. I believe my international experience and strong educational background will enable me to help Chinese companies be highly competitive in the global market.As one of the most renowned in Portugal , Master Program in Finance of University of Lisbon is an ideal choice for me. Firstly, University of Lisbon is among the best universities in Portugal. I will feel glad and honored to study at a university which has great reputation and profound history.Secondly, when I was traveling in Lisbon, it has left a deep impression with its international atmosphere, developed infrastructure, amazing culture and rich opportunities. Thirdly, offering a wide range of courses in a variety of fields including business analysis and project management, your program perfectly fits me since the curriculum provides an excellent opportunityto enhance my analytic skills while further honing my technical skills. I sincerely believe that participating in your program will be a unique adventure and a milestone on the route to my ultimate career goal. I am confident that all the training and preparation that I have acquired so far, make me a qualified candidate for your graduate program. I certainly appreciate your consideration of my application for admission and hope for a favorable reply.Your faithfully,Qingyu ZHAO。

罗森第九版英文《财政学》课件cha

05

Fiscal Policy and Economy

The goals and tools of Fiscal policy

Goal

Stabilize the economy, reduce unemployment, control inflation, and promote economic growth

and use funds

It encompasses the processes of investing, borrowing, saving, and insurance

Finance aims to maximize the value of assets while

minimizing financial risks

Scientific research …

funding for universities, research institutions, and enterprises

Public facilities

schools, hospitals, libraries, cultural centers, etc

A

B

Value added tax (VAT)

A consumption tax proposed on goods and services at each stage of production and distributionCDCorprate income tax

Charged on profits earned by companies

The course covers a wide range of topics, including the basic concepts of finance, financial markets and institutions, investment theory, corporate finance, and international finance It also explores the latest developments and trends in the financial industry

高一英语大学专业选择因素单选题50题

高一英语大学专业选择因素单选题50题1. If your interest is in music, which major is the most suitable for you?A. Computer ScienceB. Music EducationC. EngineeringD. Business Administration答案:B。

本题考查对不同专业与兴趣的匹配。

选项A“Computer Science”主要涉及计算机领域,与音乐兴趣无关。

选项C“Engineering”侧重于工程方面,也与音乐兴趣不直接相关。

选项D“Business Administration”是商业管理,和音乐兴趣联系不大。

而选项B“Music Education”与音乐兴趣直接相关,是针对对音乐有兴趣的人的合适专业。

2. When your passion lies in art, which of the following majors should you consider?A. MedicineB. LawC. Fine ArtsD. Physics答案:C。

本题考查专业与兴趣的对应。

选项A“Medicine”是医学专业,与艺术兴趣不相符。

选项B“Law”是法律专业,和艺术兴趣没有直接关联。

选项D“Physics”是物理学专业,不属于艺术范畴。

而选项C“Fine Arts”是美术专业,与对艺术的兴趣高度契合。

3. If you are interested in sports, which major might be a good choice for you?A. LiteratureB. Physical EducationC. ChemistryD. History答案:B。

本题考查兴趣与专业的适配性。

选项A“Literature”是文学专业,与体育兴趣关系不大。

选项C“Chemistry”是化学专业,和体育兴趣没有直接联系。

IFSYLLAB