Deferred taxes

会计英语分录中英对照

2 负债 liabilities21~ 22 流动负债 current liabilities211 短期借款 short-term borrowings(debt)2111 银行透支 bank overdraft2112 银行借款 bank loan2114 短期借款 -业主 short-term borrowings - owners 2115 短期借款 -员工 short-term borrowings - employees 2117 短期借款-关系人 short-term borrowings- related parties2118 短期借款 -其它 short-term borrowings - other 212 应付短期票券 short-term notes and bills payable 2121 应付商业本票 commercial paper payable2122 银行承兑汇票 bank acceptance2128 其它应付短期票券other short-term notes and bills payable2129 应付短期票券折价 discount on short-term notes and bills payable213 应付票据 notes payable2131 应付票据 notes payable2137 应付票据-关系人 notes payable - related parties 2138 其它应付票据 other notes payable214 应付帐款 accounts pay able2141 应付帐款 accounts payable2147 应付帐款-关系人 accounts payable - related parties 216 应付所得税 income taxes payable2161 应付所得税 income tax payable217 应付费用 accrued expenses2171 应付薪工 accrued payroll2172 应付租金 accrued rent payable2173 应付利息 accrued interest payable2174 应付营业税 accrued VAT payable2175 应付税捐 -其它 accrued taxes payable- other2178 其它应付费用 other accrued expenses payable218~219 其它应付款 other payables2181 应付购入远汇款 forward exchange contract payable 2182 应付远汇款-外币forward exchange contract payable - foreign currencies2183 买卖远汇溢价 premium on forward exchange contract 2184 应付土地房屋款payables on land and building purchased2185 应付设备款 Payables on equipment2187 其它应付款-关系人 other payables - related parties 2191 应付股利 dividend payable2192 应付红利 bonus payable2193 应付董监事酬劳 compensation payable to directors and supervisors2198 其它应付款 -其它 other payables - other226 预收款项advance receipts2261 预收货款 sales revenue received in advance2262 预收收入 revenue received in advance2268 其它预收款 other advance receipts227 一年或一营业周期内到期长期负债long-term liabilities -current portion2271 一年或一营业周期内到期公司债 corporate bonds payable - current portion2272 一年或一营业周期内到期长期借款 long-term loans payable - current portion2273 一年或一营业周期内到期长期应付票据及款项long-term notes and accounts payable due within one year or one operating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人long-term notes and accounts payables to related parties - current portion2278 其它一年或一营业周期内到期长期负债other long-term lia- bilities - current portion228~229 其它流动负债 other current liabilities2281 销项税额 VAT received(or output tax) 2283 暂收款 temporary receipts2284 代收款 receipts under custody2285 估计售后服务/保固负债estimated warranty liabilities2291 递延所得税负债 deferred income tax liabilities 2292 递延兑换利益 deferred foreign exchange gain 2293 业主(股东)往来 owners' current account2294 同业往来 current account with others2298 其它流动负债-其它 other current liabilities - others23 长期负债 long-term liabilities231 应付公司债 corporate bonds payable2311 应付公司债 corporate bonds payable2319 应付公司债溢(折)价premium(discount) on corporate bonds payable232 长期借款 long-term loans payable2321 长期银行借款 long-term loans payable - bank 2324 长期借款 -业主 long-term loans payable - owners 2325 长期借款 -员工 long-term loans payable - employees 2327 长期借款-关系人 long-term loans payable - related parties2328 长期借款 -其它 long-term loans payable - other 233 长期应付票据及款项 long-term notes and accounts payable2331 长期应付票据 long-term notes payable2332 长期应付帐款 long-term accounts pay-able2333 长期应付租赁负债long-term capital lease liabilities2337 长期应付票据及款项-关系人 Long-term notes and accounts payable - related parties2338 其它长期应付款项 other long-term payables234 估计应付土地增值税 accrued liabilities for land value increment tax2341 估计应付土地增值税 estimated accrued land value incremental tax pay-able235 应计退休金负债 accrued pension liabilities2351 应计退休金负债 accrued pension liabilities238 其它长期负债 other long-term liabilities2388 其它长期负债-其它 other long-term liabilities - other28 其它负债 other liabilities281 递延负债 deferred liabilities2811 递延收入 deferred revenue2814 递延所得税负债 deferred income tax liabilities 2818 其它递延负债 other deferred liabilities286 存入保证金 deposits received2861 存入保证金 guarantee deposit received288 杂项负债 miscellaneous liabilities2888 杂项负债-其它 miscellaneous liabilities – other3 业主权益 owners' equity31 资本 capital311 资本(或股本) capital3111 普通股股本 capital - common stock3112 特别股股本 capital - preferred stock3113 预收股本 capital collected in advance3114 待分配股票股利 stock dividends to be distributed 3115 资本 capital32 资本公积 additional paid-in capital321 股票溢价 paid-in capital in excess of par3211 普通股股票溢价 paid-in capital in excess of par- common stock3212 特别股股票溢价 paid-in capital in excess of par- preferred stock323 资产重估增值准备capital surplus from assets revaluation3231 资产重估增值准备capital surplus from assets revaluation324 处分资产溢价公积 capital surplus from gain ondisposal of assets3241 处分资产溢价公积 capital surplus from gain on disposal of assets325 合并公积 capital surplus from business combination 3251 合并公积capital surplus from business combination326 受赠公积 donated surplus3261 受赠公积 donated surplus328 其它资本公积 other additional paid-in capital 3281 权益法长期股权投资资本公积 additional paid-in capital from investee under equity method3282 资本公积- 库藏股票交易additional paid-in capital - treasury stock trans-actions33 保留盈余(或累积亏损) retained earnings (accumulated deficit)331 法定盈余公积 legal reserve3311 法定盈余公积 legal reserve332 特别盈余公积 special reserve3321 意外损失准备 contingency reserve3322 改良扩充准备 improvement and expansion reserve3323 偿债准备special reserve for redemption of liabilities3328 其它特别盈余公积 other special reserve335 未分配盈余(或累积亏损)retained earnings-unappropriated (or accumulated deficit)3351 累积盈亏 accumulated profit or loss3352 前期损益调整 prior period adjustments3353 本期损益 net income or loss for current period 34 权益调整 equity adjustments341 长期股权投资未实现跌价损失unrealized loss on market value decline of long-term equity investments 3411长期股权投资未实现跌价损失unrealized loss on market value decline of long-term equity investments 342累积换算调整数cumulative translation adjustment 3421 累积换算调整数cumulative translation adjustments343 未认列为退休金成本之净损失net loss not recognized as pension cost3431 未认列为退休金成本之净损失net loss not recognized as pension costs35 库藏股 treasury stock351 库藏股 treasury stock3511 库藏股 treasury stock36 少数股权 minority interest361 少数股权 minority interest3611 少数股权 minority interest4 营业收入 operating revenue41 销货收入 sales revenue411 销货收入 sales revenue4111 销货收入 sales revenue4112 分期付款销货收入 installment sales revenue 417 销货退回 sales return4171 销货退回 sales return419 销货折让 sales allowances4191 销货折让 sales discounts and allowances46 劳务收入 service revenue461 劳务收入 service revenue4611 劳务收入 service revenue47 业务收入 agency revenue471 业务收入 agency revenue4711 业务收入 agency revenue48 其它营业收入 other operating revenue488 其它营业收入-其它 other operating revenue 4888 其它营业收入-其它 other operating revenue - other 5 营业成本 operating costs51 销货成本 cost of goods sold511 销货成本 cost of goods sold5111 销货成本 cost of goods sold5112 分期付款销货成本 installment cost of goods sold 512 进货 purchases5121 进货 purchases5122 进货费用 purchase expenses5123 进货退出 purchase returns5124 进货折让 charges on purchased merchandise513 进料 materials purchased5131 进料 material purchased5132 进料费用 charges on purchased material5133 进料退出 material purchase returns5134 进料折让 material purchase allowances514 直接人工 direct labor5141 直接人工 direct labor515~518 制造费用 manufacturing overhead5151 间接人工 indirect labor5152 租金支出 rent expense, rent5153 文具用品 office supplies (expense)5154 旅费 travelling expense, travel5155 运费 shipping expenses, freight5156 邮电费 postage (expenses)5157 修缮费 repair(s) and maintenance (expense )5158 包装费 packing expenses5161 水电瓦斯费 utilities (expense)5162 保险费 insurance (expense)5163 加工费 manufacturing overhead - outsourced5166 税捐 taxes5168 折旧 depreciation expense5169 各项耗竭及摊提 various amortization5172 伙食费 meal (expenses)5173 职工福利 employee benefits/welfare5176 训练费 training (expense)5177 间接材料 indirect materials5188 其它制造费用 other manufacturing expenses56 劳务成本制 ervice costs561 劳务成本 service costs5611 劳务成本 service costs57 业务成本 gency costs571 业务成本 agency costs5711 业务成本 agency costs58 其它营业成本 other operating costs588 其它营业成本-其它 other operating costs-other 5888 其它营业成本-其它 other operating costs - other 6 营业费用 operating expenses61 推销费用 selling expenses615~618 推销费用 selling expenses6151 薪资支出 payroll expense6152 租金支出 rent expense, rent6153 文具用品 office supplies (expense)6154 旅费 travelling expense, travel6155 运费 shipping expenses, freight6156 邮电费 postage (expenses)6157 修缮费 repair(s) and maintenance (expense)6159 广告费 advertisement expense, advertisement 6161 水电瓦斯费 utilities (expense)6162 保险费 insurance (expense)6164 交际费 entertainment (expense)6165 捐赠 donation (expense)6166 税捐 taxes6167 呆帐损失 loss on uncollectible accounts6168 折旧 depreciation expense6169 各项耗竭及摊提 various amortization6172 伙食费 meal (expenses)6173 职工福利 employee benefits/welfare6175 佣金支出 commission (expense)6176 训练费 training (expense)6188 其它推销费用 other selling expenses62 管理及总务费用 general & administrative expenses 625~628 管理及总务费用general & administrative expenses6251 薪资支出 payroll expense6252 租金支出 rent expense, rent6253 文具用品 office supplies6254 旅费 travelling expense, travel6255 运费 shipping expenses,freight6256 邮电费 postage (expenses)6257 修缮费 repair(s) and maintenance (expense)6259 广告费 advertisement expense, advertisement 6261 水电瓦斯费 utilities (expense)6262 保险费 insurance (expense)6264 交际费 entertainment (expense)6265 捐赠 donation (expense)6266 税捐 taxes6267 呆帐损失 loss on uncollectible accounts6268 折旧 depreciation expense6269 各项耗竭及摊提 various amortization6271 外销损失 loss on export sales6272 伙食费 meal (expenses)6273 职工福利 employee benefits/welfare6274 研究发展费用 research and development expense 6275 佣金支出 commission (expense)6276 训练费 training (expense)6278 劳务费 professional service fees6288 其它管理及总务费用other general and administrative expenses63 研究发展费用 research and development expenses 635~638 研究发展费用research and development expenses6351 薪资支出 payroll expense6352 租金支出 rent expense, rent6353 文具用品 office supplies6354 旅费 travelling expense, travel6355 运费 shipping expenses, freight6356 邮电费 postage (expenses)6357 修缮费 repair(s) and maintenance (expense)6361 水电瓦斯费 utilities (expense)6362 保险费 insurance (expense)6364 交际费 entertainment (expense)6366 税捐 taxes6368 折旧 depreciation expense6369 各项耗竭及摊提 various amortization6372 伙食费 meal (expenses)6373 职工福利 employee benefits/welfare6376 训练费 training (expense)6378 其它研究发展费用 other research and development expenses7 营业外收入及费用 non-operating revenue and expenses, other income(expense)71~74 营业外收入 non-operating revenue711 利息收入 interest revenue7111 利息收入 interest revenue/income712 投资收益 investment income7121 权益法认列之投资收益investment income recognized under equity method7122 股利收入 dividends income7123 短期投资市价回升利益gain on market price recovery of short-term investment713 兑换利益 foreign exchange gain7131 兑换利益 foreign exchange gain714 处分投资收益 gain on disposal of investments 7141 处分投资收益 gain on disposal of investments 715 处分资产溢价收入 gain on disposal of assets7151 处分资产溢价收入 gain on disposal of assets748 其它营业外收入 other non-operating revenue7481 捐赠收入 donation income7482 租金收入 rent revenue/income7483 佣金收入 commission revenue/income7484 出售下脚及废料收入 revenue from sale of scraps 7485 存货盘盈 gain on physical inventory7486 存货跌价回升利益 gain from price recovery of inventory7487 坏帐转回利益 gain on reversal of bad debts7488 其它营业外收入-其它 other non-operating revenue- other items75~ 78 营业外费用 non-operating expenses751 利息费用 interest expense7511 利息费用 interest expense752 投资损失 investment loss7521 权益法认列之投资损失investment loss recog- nized under equity method7523 短期投资未实现跌价损失unrealized loss on reduction of short-term investments to market753 兑换损失 foreign exchange loss7531 兑换损失 foreign exchange loss754 处分投资损失 loss on disposal of investments7541 处分投资损失 loss on disposal of investments755 处分资产损失 loss on disposal of assets7551 处分资产损失 loss on disposal of assets788 其它营业外费用 other non-operating expenses7881 停工损失 loss on work stoppages7882 灾害损失 casualty loss7885 存货盘损 loss on physical inventory7886 存货跌价及呆滞损失 loss for market price decline and obsolete and slow-moving inventories7888 其它营业外费用-其它 other non-operating expenses- other8 所得税费用(或利益) income tax expense (or benefit)81 所得税费用(或利益) income tax expense (or benefit) 811 所得税费用(或利益) income tax expense (or benefit) 8111 所得税费用(或利益) income tax expense ( or benefit) 9 非经常营业损益 nonrecurring gain or loss91 停业部门损益gain(loss) from discontinued operations911 停业部门损益-停业前营业损益 income(loss) from operations of discontinued segments9111 停业部门损益-停业前营业损益 income(loss) from operations of discontinued segment912 停业部门损益-处分损益 gain(loss) from disposal of discontinued segments9121 停业部门损益-处分损益 gain(loss) from disposalof discontinued segment92 非常损益 extraordinary gain or loss921 非常损益 extraordinary gain or loss9211 非常损益 extraordinary gain or loss93 会计原则变动累积影响数 cumulative effect of changesin accounting principles931 会计原则变动累积影响数cumulative effect of changes in accounting principles9311 会计原则变动累积影响数 cumulative effect of changes in accounting principles94 少数股权净利 minority interest income941 少数股权净利 minority interest income9411 少数股权净利 minority interest income中英文资产负债表资产 ASSETS流动资产: CURRENT ASSETS:现金 Cash on hand银行存款 Cash in bank有价证券 Marketable securities 应收票据 Notes receivable 应收账款 Accounts receivable 减:坏账准备 Less:Provision for bad debts 预付帐款 Advances to suppliers 其他应收款 Other receivables待摊费用 Deferred and prepaid expenses 存货 Inventories减:存货变现损失准备Less:Provision for loss on realization of inventories一年内到期的长期投资 Long-term investments maturing within one year其他流动资产 Other current assets流动资产合计 Total current assets长期投资: LONG TERM INVESTMENTS 长期投资 Long-term investments一年以上的应收款项 Receivables collectable after one year固定资产: FIXED ASSETS:固定资产原价 Fixed assets-cost减:累计折旧 Less:Accumulated depreciationcost固定资产净值 Fixed assets-net value 固定资产清理 Disposal of fixed assets 在建工程: CONSTRUCTION IN PROGRESS 在建工程 Construction in progress 无形资产: INTANGIBLE ASSETS:场地使用权 Land occupancy righ工业产权及专有技术 Industary property rights and proprietary technology其它无形资产 Other intangible assets无形资产合计 Total intangibles assets:其它资产: OTHER ASSETS:开办费 Organization expenses筹建期间汇兑损失 Exchange loss during start-up period递延投资损失 Deferred loss on investm递延税款借项 Deferred taxes debi其它递延支出 Other deferred expense待转销汇兑损失 Unamortized cxehangs loss负债及所有者权益 LIABILITIES AND OWNER'S EQUITY 流动负债: CURRENT LIABILITIES:短期借款 Short-term loans应付票据 Notes payable应付账款 Accounts payable应付工资 Accrued payroll应交税金 Taxes payable应付股利 Dividends payable预收货款 Advances from customers其它应付款 Other payables预提费用 Accrued expense职工奖励及福利基金 Staff and worker's bonus and welfare fund一年内到期的长期负债 Long-term liabilities due within one year其他流动负债 Other current liabilities 流动负债合计 Total current liabilities 长期负债: LONG-TERM LIABILITIES:长期借款 Long-term loans应付公司债 Dividends payable应付公司债溢价(折价) Premium(discount)on debentures payable一年以上的应付款项 Payables due after one year长期负债合计Total long-term liabilities其他负债: OTHER LIABILITIES筹建期间汇兑收益 Exchange gain during start-up period递延投资收益Deferred gain on investments递延税款贷项 Deferred tax credits 其他递延贷项 Other deferred credits 待转销汇兑收益 Unamortized exchange gain 其他负债合计Total other liabilities负债合计 Total liabilities所有者权益: OWNER'S EQUITY资本总额 Registered capital (货币名称及金额currency and amount___)实收资本 Paid-in capital (非人民币资本期末金额amount of non-RMB currency at end of period___)其中:中方投资 Chinese investments(非人民币资本期末金额amount of non-RMB currency at end of period___)外方投资 Foreign investments(非人民币资本期末金额amount of non-RMB currency at end of period___)减:已归还投资 Less:Investments returned资本公积 Capital surplus储备基金 Reserve fund企业发展基金 Enterprise expansion fund利润归还投资Profit capitalised on return of investments本年利润 Current year net income未分配利润 Undistributed profit所有者权益总计 Total owner's equity负债及所有者权益总计 TOTAL LIABILITIES AND OWNER'S EQUITY。

CFA1 财务分析记忆要点

分清题目是那个报表里的概念,则答案也该也是想要报表里的概念一、收入表(不包含和股东的交易)从股东手里得到或者发放利益给股东的部分不用于计算incomeNon-recurring items(考虑频率):Discontinued operations(不影响营业利润): measurement date, phaseout period.在measurement date公司就要对其进行估计它的Income or loss (税后)在income statement里分开,之前的income statement 要重算(它的Income of loss 要在income statement里分开),在销售没有结束前,gains不能计入。

Unusual or infrequent items(影响营业利润): 包含在Incomes from Continuing operations and reported before tax.Extraordinary items(不影响营业利润):U.S.GAAP: 它的Income or loss (税后)要在income statement里分开IFRS: 不允许在income statement里分开对原有错误会计方法的订正(Prior-period adjustment)或改变使用的财务标准要回溯计算后表示在当期的报表中。

改变对财产的估计,不要求回溯。

EPS:使用月份(从可转化证券发行开始算)加权平均后拖欠股息的股数;被公司回购后的股票无需计算;Dilutive EPS:首先判断是否是Dilutive,计算后主要和Basis EPS比较大小;期权行使的计算:相当于在总资产不便的情况下,市场上增加的股数;净收入是已经计算过利息,所以在算可转换债是要将利息加回去(税后)。

Commone-size income statement: 其中Tax和ruvenue的比率的值意义不大,意义比较大的是tax和毛利的比率(effective tax rate)Other Comprehensive income: P74二、资产负债表(包含和股东的交易):由于衡量公司的liquidity, solvency the ability to pay dividends无法估计价值的A或者L不在balance sheet里体现。

Deferred Tax_201605

5

June 16

3. Deferred Tax Assets/Liabilities

DTL Conversely, a deferred tax liability occurs when assets are carried at a higher amount in the BKA balance sheet than for tax purposes (= tax base)

Taxable temporary differences, which are temporary differences that will result in taxable amounts in determining taxable profit (tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled; or

arising on first-time consolidation for which amortization is not deductible for tax purpose

the initial recognition of an asset or liability

in a transaction which is not a business combination, and at the time of the original transaction, affects neither accounting profit nor taxable profit or loss (as, e.g., in the case of non-taxable government grants related to capital expenditures);

财务报表英文翻译大全

Total liabilities

固定资产清理

Disposal of fixed assets

固定资产ห้องสมุดไป่ตู้计

Sub-total of fixed assets

所有者权益(或股东权益)

Owner’s (Stockholders’) equity

无形资产及其他资产

Intangible and other assets

三、筹资活动产生的现金流量:

III. Cash flows from financing activities:

吸收投资所收到的现金

Cash received from investment by others

借款所收到的现金

Cash received from borrowings

其他流动负债

Other current liabilities

长期投资:

Long-term investments:

长期股权投资

Long-term equity investment

流动负债合计

Sub-total of current liabilities

长期债权投资

Long-term debt investment

项目

Item

行次

Line No.

本月数

Current month

本年累计数

Current yearaccumulative

一、主营业务收入

I. Revenue from main operations

减:主营业务成本

Less: Cost of main operations

主营业务税金及附加

Taxes and surcharges for main operations

如何通俗易懂地理解递延税项(DeferredTax)?

如何通俗易懂地理解递延税项(DeferredTax)?【MrToyy的回答(28票)】:递延税项指企业所得税。

递延税项是会计当中“配比原则”的经典体现。

配比原则要求,当期的收入要与成本、费用配比。

不能只确认收入,不确认相关的成本、费用;也不能只确认成本或费用而不确认相关的收入。

此举是为了尽量减少会计操纵,稳定公司的毛利率、净利率。

那么,递延税项的存在,就是为了将应当当期负担的所得税与当期的收入、成本费用进行配比。

这里有一个疑问,为什么需要配比呢?难道企业不就应该按其利润缴纳企业所得税吗?这是源于税法与会计准则的差异。

税法因为是规范纳税,所以企业自主空间很小;会计准则更多的满足各种不同行业的需求,企业自主空间比税法更大。

在到税务局缴税的时候,企业会根据税法规定计算应缴纳的税款;在财务报表上,企业会根据实际的经营利润计算应缴纳的税款。

由于企业在会计核算上与税法规定上有差异,导致利润表上应计的税款与实际缴纳的税款有差异。

这个差异,就是递延税项。

其中,实际缴纳的多与利润表上的,就是递延所得税资产,表是以后可以少交所得税;反之就是递延所得税负债,表示以后会多交所得税。

【JerryZhang的回答(32票)】:这是个好长的问题,喝口水先!!以天朝为例,会计的记账方式和税务局认可的利润表科目记录方式之间是存在差异的,而这个差异就会导致:1. 有些费用公司账面记录了,但是税务局并不承认,导致公司无法税前抵扣,这种情况叫做永久性差异(permanent differences)2. 有些费用公司账面记录了,但是税务局认为这个事实当期并没发生,所以当期没办法抵扣,等到你实际发生这件事情的时候才让你抵扣,这种情况叫做暂时性差异(temporary differences)在上述两种情况下面,第一种是不会产生递延税项的(因为税务局到死都不会让你抵扣这部分费用的),第二种由于费用确认在不同的会计年度而产生的暂时性差异才会产生递延税项。

资产负债表中英文对照

资产负债表2007年12月31日单位名称:AAA 单位:元AAABalance Sheet (Consolidated Balance Sheets)(Amounts in yean)资产/ASSETSDECEMBER年初数/2006 年末数/2007 流动资产/Current assets货币资金/ Cash and equivalents短期投资/ Short term investments应收票据/ Notes receivable应收账款/ Accounts receivable减:/ less:坏账准备/ Allowance for bad debts/ Allowance for uncollectibles/ Allowance for doubtful accounts应收账款净额/ Accounts receivable, net预付账款/ Prepaid expenses其他应收款/ Other receivables存货/ Inventory待摊费用/ Amortization expense待处理流动资产损益/一年内到期的长期债券投资其他流动资产/ Other current assets流动资产合计:Total current assets长期投资:Long-term investments长期投资/ Long-term investments固定资产:Property, Plant and Equipment固定资产原值/ Property, Plant and Equipment减:累计折旧/ Less: Accumulated depreciation 固定资产净值/ Property, Plant and Equipment, net 固定资产清理/在建工程/待处理固定资产损益/固定资产合计:无形资产及递延资产:无形资产/递延资产/无形资产及递延资产合计:其他长期资产:Other long-lived Assets其他长期资产/ Other long-lived Assets递延税项:Deferred income taxes递延税项借项/ Deferred Tax Asset资产合计:/ Total assets负债及所有者权益Liabilities and stockholders’ equity 流动负债:Current liabilities短期借款/ Short-term borrowings应付票据/ Notes payable应付账款/ Accounts payable预收账款/ Unearned revenues其他应付款/ Other accrued expenses and liabilities应付工资/ Accrued personnel costs应付福利费/ Accrued compensation and benefits未交税金/ Taxes payable未付利润/ Dividends payable其他未交款/ Other payables预提费用/一年内到期的长期负债/ Current portion of long-term debt/ Current maturities of long-term debt 其他流动负债/ Other current liabilities流动负债合计/ Total current liabilities长期负债:Long-term liabilities长期借款/ Long-term borrowings应付债券/ Bonds payable长期应付款/递延出租收入/ Deferred rent revenues其他长期负债/ Other long-term obligations 其中:住房周转金长期负债合计/ Total long-term liabilities递延税项:Deferred income taxes递延税款贷项/ Deferred income liabilities负债合计/ Total liabilities所有者权益:Stockholders’ equity实收资本/ Common stock(普通股)资本公积/ Additional paid-in-capital盈余公积/其中:/ 公益金/未分配利润/ Retained earnings 累计亏损/ Accumulated deficit所有者权益合计/ Total Shareholders’ equity负债及所有者权益合计/ Total liabilities and Total Shareholders’ equity注:以上为部分资产负债表项目的英文翻译,其他的未被翻译的项目部分是由于会计准则、会计惯例的不同形成的,部分是由于本人专业知识及英语技能有限,希望大家多指教,有任何疑问欢迎一同探讨,谢谢!。

Deferred tax assets

举例帮你深刻理解递延所得税资产、递延所得税负债先说递延所得税资产、可抵扣暂时性差异:案例:2010年初生产设备账面价值10万元,企业预计设备寿命1年,税法规定预计寿命2年,收入20万元,税率25%。

那么2010年企业真实利润是收入-成本 20-10=10万,(设备1年就报废了嘛,所以成本是10万)2010年按税法当期的应纳税利润是收入-成本20-5=15万(设备能用2年,所以年成本就是5万了),那么税务局就暂时多收了你(15-10)*25%=1.25万的税,2010年末设备账面价值-资产的计税基础=0-5=-5,也就是可抵扣暂时性差异是5万元,递延所得税资产就是 5*25%=1.25万,正好和税务局多收了你的1.25万吻合嘛。

多收了你的税,税务局按理说应该以后退还给你啊。

但是他很坏,还开出了条件才能确认,也就是递延所得税资产的确认。

分三种情况:一,打个比方,你2011年就破产了,自然没钱再纳税了,税务局就不确认你这资产,也就是说多收了你的1.25万税不退给你。

二,你2011年生产形势良好,当年应该纳税10万,税局就还有点良心,这1.25万多收了你的税就可以抵扣了,你只需要交8.75万就放过你了。

三,2011年生产一般,利润少,只需要纳税1万元,税局就说了“应以未来期间很可能取得的应纳税所得额为限”,就是说,这1万的税就抵消啦,但不能退0.25万给你哦。

再用同样案例解释递延所得税负债、应纳税暂时性差异:案例:2010年初生产设备账面价值10万元,企业预计设备寿命2年,税法规定预计寿命1年,收入20万元。

税率25%。

2010年企业真实利润是收入-成本 20-5=15万,(设备能用2年,所以年成本就是5万了)2010年按税法当期的应纳税利润是收入-成本20-10=10万(设备1年就报废了嘛,所以成本是10万),那么税务局就暂时少收了你(15-10)*25%=1.25万的税。

2010年末设备账面价值-资产的计税基础=5-0=5,也就是应纳税暂时性差异是5万元,递延所得税负债就是 5*25%=1.25万,正好和税务局少收了你的1.25万吻合嘛。

财务报表英文翻译大全(含资产负债表、现金流量表、利润表等等)

Sub—total of long—term liabilities

固定资产净额

Fixed assets—net

递延税项

Deferred taxes

工程物资

Constructionmaterials

递延税款贷项

Deferred tax credit

在建工程

Construction in progress

长期负债:

Long-termliabilities

长期投资合计

Sub-total of long term investment

长期借款

Long—term borrowings

固定资产:

Fixed assets:

应付债券

Bonds payable

固定资产原价

Fixed assets-cost

长期应付款

二、主营业务利润(亏损以“—”填列)

II. Profit/Loss from main operations

加:其他业务利润(亏损以“—”填列)

Add:Profit/Loss fromother operations

减:营业费用

Less: Operating expenses

管理费用

General and administrative expenses

实收资本(或股本)

Paid-in capital (or stock)

无形资产

Intangible assets

减:已归还投资

Less: Investment returned

长期待摊资产

Long—term prepayment

实收资本(或股本)净额

Paid—in capital (or stock) - net

Accounting_Clinic_VI

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2010 All rights reserved.

Clinic 6-5

Examples of Permanent Differences

Interest received on municipal obligations premiums paid on officers' life insurance. Fines and other expenses that result from a violation of law. Deduction for dividend received from U.S. corporations. Percentage depletion of natural resources in excess of their cost.

Smoothing of earnings Better relationship between earnings and income tax expense effective tax rate reflects statutory rate

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2010 All rights reserved. Clinic 6-4

© The McGraw-Hill Companies, Inc., 2010 All rights reservl/Irwin

Deferred Tax Liability

A deferred tax liability is recognized for temporary differences that will result in taxable amounts in future years. For example, a temporary difference is created between the reported amount and the tax basis of an installment sale receivable if, for tax purposes, some or all of the gain on the installment sale will be included in the determination of taxable income in future years. Because amounts received upon recovery of that receivable will be taxable, a deferred tax liability is recognized in the current year for the related taxes payable in future years.

(财务报表管理)中英文对照财务报表常用单词

中英文对照财务报表(有何谬误,欢迎指正)资产负债表Balance Sheet项目ITEM货币资金Cash短期投资Short term investments应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收帐款Accounts receivable其他应收款Other receivables预付帐款Accounts prepaid期货保证金Future guarantee应收补贴款Allowance receivable应收出口退税Export drawback receivable存货Inventories其中:原材料Including:Raw materials 产成品(库存商品) Finished goods待摊费用Prepaid and deferred expenses待处理流动资产净损失Unsettled G/L on current assets一年内到期的长期债权投资Long-term debenture investment falling due in a yaear其他流动资产Other current assets流动资产合计Total current assets长期投资:Long-term investment:其中:长期股权投资Including long term equity investment长期债权投资Long term securities investment*合并价差Incorporating price difference长期投资合计Total long-term investment固定资产原价Fixed assets-cost减:累计折旧Less:Accumulated Dpreciation固定资产净值Fixed assets-net value 减:固定资产减值准备Less:Impairment of fixed assets固定资产净额Net value of fixed assets固定资产清理Disposal of fixed assets工程物资Project material在建工程Construction in Progress 待处理固定资产净损失Unsettled G/L on fixed assets固定资产合计Total tangible assets无形资产Intangible assets其中:土地使用权Including and use rights递延资产(长期待摊费用)Deferred assets 其中:固定资产修理Including:Fixed assets repair固定资产改良支出Improvement expenditure of fixed assets其他长期资产Other long term assets 其中:特准储备物资Amongit:Specially approved reserving materials无形及其他资产合计Total intangible assets and other assets递延税款借项Deferred assets debits 资产总计Total Assets资产负债表(续表) Balance Sheet项目ITEM短期借款Short-term loans应付票款Notes payable应付帐款Accounts payab1e预收帐款Advances from customers应付工资Accrued payro1l应付福利费Welfare payable应付利润(股利) Profits payab1e应交税金Taxes payable其他应交款Other payable to government其他应付款Other creditors预提费用Provision for expenses预计负债Accrued liabilities一年内到期的长期负债Long term liabilities due within one year其他流动负债Other current liabilities 流动负债合计Total current liabilities 长期借款Long-term loans payable 应付债券Bonds payable长期应付款long-term accounts payable专项应付款Special accounts payable 其他长期负债Other long-term liabilities其中:特准储备资金Including:Special reserve fund长期负债合计Total long term liabilities递延税款贷项Deferred taxation credit负债合计Total liabilities* 少数股东权益Minority interests实收资本(股本) Subscribed Capital国家资本National capital集体资本Collective capital法人资本Legal person"s capital其中:国有法人资本Including:State-owned legal person"s capital集体法人资本Collective legal person"s capital个人资本Personal capital外商资本Foreign businessmen"s capital资本公积Capital surplus盈余公积surplus reserve其中:法定盈余公积Including:statutory surplus reserve 公益金public welfare fund补充流动资本Supplermentary current capital* 未确认的投资损失(以“-”号填列)Unaffirmed investment loss未分配利润Retained earnings外币报表折算差额Converted difference in Foreign Currency Statements所有者权益合计Total shareholder"s equity负债及所有者权益总计Total Liabilities & Equity利润表INCOME STATEMENT项目ITEMS产品销售收入Sales of products其中:出口产品销售收入Including:Export sales 减:销售折扣与折让Less:Sales discount and allowances产品销售净额Net sales of products 减:产品销售税金Less:Sales tax产品销售成本Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利Gross profit on sales 减:销售费用Less:Selling expenses 管理费用General and administrativeexpenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome)汇兑损失(减汇兑收益)Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain for previous years利润总额Total profit减:所得税Less:Income tax净利润Net profit本文来自: 人大经济论坛会计与财务管理版,详细出处参考:/bbs/viewthr ead.php?tid=335564&page=1会计要素的计量属性basis of measurement历史成本historical cost重置成本replacement cost可实现净值net-realizable value现值present value公允价值fair value财务报告financial statement资产负债表Balance Sheet利润表Income Statement现金流量表Cash Flow Statement所有者权益变动表Statement of Changes in Equity附注notesDisclosure notesChap. 2货币资金monetary assets现金cash银行账户bank account现金等价物cash equivalentChap. 3金融资产financial instruments以公允价值计量且变动计入当期损益的金融资产Measure at fair value through profit or loss交易性金融资产held for trading指定为以公允价值计量且变动计入当期损益的金融资产Identified as at fair value through profit or loss持有到期投资Held-to –maturity investment贷款和应收账款Loans and receivables 可供出售金融资产available-for-sale financial assets减值impairment减值损失impairment lossChap. 4存货inventory存货的种类:Classification of inventory 原材料raw materials inventory在产品work-in-progress inventory半成品component parts产成品finished goods inventory商品merchandise inventory周转材料supplies inventory发出存货的计量cost flow assumption先进先出法first-in-first-out (FIFO)后进先出法last-in-first-out (LIFO)移动加权平均法moving-average unit cost全月一次加权平均法weighted-average system个别计价法(具体辨认法)specific identification期末存货的计量ending balance of inventory成本与可变现净值孰低lower-of –cost-or-market valueNet-realizable value存货跌价准备Allowance to reduce inventory to LCM资产减值损失—存货减值损失loss of impairment on assets ---- loss of impairment on inventoryChap. 5长期股权投资long-term investment –shareInvestment in subsidiary ***成本法cost method权益法equity method投资收益investment income可转换convertibleChap. 6固定资产capital assets在建工程wok-in-progress construction折旧amortization平均年限法straight-line-method工作量法unit-of- production双倍余额递减法declining-balance method年数总和法sum-of-the-years-digits method后续支出subsequent expenditure资本化capitalized cost费用化expensed cost处置retirement and disposal持有待售的固定资产capital assets held for sale固定资产清理disposal of capital assets 固定资产减值准备allowance ofimpairments on capital assets Chap. 7无形资产intangible assets专利权patents非专利技术industrial design registration商标权trademarks and trade name 著作权copyright特许权franchise rights土地使用权rights of using land Chap. 8投资性房地产investment property / profitable estateChap. 9非货币性资产交换non-monetaryassets exchange商业实质commercial substance Chap. 10资产减值assets impairment估计evaluation资产组assets group cash generate unit商誉goodwillChap. 11负债liabilities流动负债current liabilities非流动负债non-current liabilities初始计量initial measurement辞退福利fire fringe进口import出口export可转换公司债券convertible bond Chap. 12所有者权益equity实收资本issued capital资本公积capital reserve股本溢价share premium留存收益retained earnings未分配利润distributed profit Chap. 13完工百分比法percentage of completion method建造合同construction contract直接法direct method间接法indirect method分部报告segment report关联方related party租赁lease担保guaranteeChap. 15或有事项contingencies或有资产contingent assets或有负债contingent liabilities亏损合同onerous contractChap.16重组reorganization /resutruction Chap. 18借款费用borrowing costs borrowing expenditure溢价premium折价discount资本化capitalize costsChap. 20所得税income tax计税基础tax base永久性差别permanent difference暂时性差别temporary difference应纳税暂时性差异taxable temporary differences可抵扣暂时性差异deductible temporary difference递延所得税资产deferred tax assets递延所得税负债deferred tax liabilities Chap. 21外币折算translation of foreigncurrency外币交易foreign currency transactions外币财务报表折算translation of foreign currency financial statement 即期汇率current exchange rate远期汇率future exchange rate通货膨胀inflationChap. 22出租人lessor承租人lessee经营租赁operating lease融资租赁finance lease / capital lease 售后租回sale and leasebackChap. 23会计政策、会计估计变更和差错更正Changes in accounting policies, changes in accounting estimates and corrections of errors会计估计Accounting estimatesChap. 24资产负债表日后事项Events after the balance sheet date 调整事项Adjusting event非调整事项Unadjusting event利润分配profit allocation以前年度损益调整retained earnings--prior year adjustment Undistributed profit—prior yearadjustmentChap. 25企业合并corporate combination长期股权投资long-term investment--shareInvestment in subsidiary *** Chap. 26合并财务报表consolidated financial statementConsolidated Balance Sheet Consolidated Income Statement Consolidated Cash Flow Statement Consolidated Statement of Changes in Equity。

中英文对照财务报表常用单词

中英文对照财务报表(有何谬误,欢迎指正)资产负债表Balance Sheet项目ITEM货币资金Cash短期投资Short term investments 应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收帐款Accounts receivable其他应收款Other receivables预付帐款Accounts prepaid期货保证金Future guarantee应收补贴款Allowance receivable应收出口退税Export drawback receivable 存货Inventories其中:原材料Including:Raw materials产成品(库存商品) Finished goods待摊费用Prepaid and deferred expenses待处理流动资产净损失Unsettled G/L on current assets一年内到期的长期债权投资Long-term debenture investment falling due in ayaear其他流动资产Other current assets流动资产合计Total current assets长期投资:Long-term investment:其中:长期股权投资Including long term equity investment长期债权投资Long term securities investment*合并价差Incorporating price difference 长期投资合计Total long-term investment 固定资产原价Fixed assets-cost减:累计折旧Less:Accumulated Dpreciation固定资产净值Fixed assets-net value减:固定资产减值准备Less:Impairmentof fixed assets固定资产净额Net value of fixed assets 固定资产清理Disposal of fixed assets工程物资Project material在建工程Construction in Progress待处理固定资产净损失Unsettled G/L on fixed assets固定资产合计Total tangible assets无形资产Intangible assets其中:土地使用权Including and use rights 递延资产(长期待摊费用)Deferred assets 其中:固定资产修理Including:Fixed assets repair固定资产改良支出Improvement expenditure of fixed assets其他长期资产Other long term assets其中:特准储备物资Among it:Specially approved reserving materials 无形及其他资产合计Total intangible assets and other assets递延税款借项Deferred assets debits资产总计Total Assets资产负债表(续表) Balance Sheet项目ITEM短期借款Short-term loans应付票款Notes payable应付帐款Accounts payab1e预收帐款Advances from customers应付工资Accrued payro1l应付福利费Welfare payable应付利润(股利) Profits payab1e应交税金Taxes payable其他应交款Other payable to government 其他应付款Other creditors预提费用Provision for expenses预计负债Accrued liabilities一年内到期的长期负债Long term liabilities due within one year其他流动负债Other current liabilities流动负债合计Total current liabilities长期借款Long-term loans payable应付债券Bonds payable长期应付款long-term accounts payable 专项应付款Special accounts payable其他长期负债Other long-term liabilities 其中:特准储备资金Including:Special reserve fund长期负债合计Total long term liabilities 递延税款贷项Deferred taxation credit负债合计Total liabilities* 少数股东权益Minority interests实收资本(股本) Subscribed Capital国家资本National capital集体资本Collective capital法人资本Legal person"s capital其中:国有法人资本Including:State-owned legal person"scapital集体法人资本Collective legal person"s capital个人资本Personal capital外商资本Foreign businessmen"s capital 资本公积Capital surplus盈余公积surplus reserve其中:法定盈余公积Including:statutory surplus reserve公益金public welfare fund补充流动资本Supplermentary current capital* 未确认的投资损失(以“-”号填列)Unaffirmed investment loss未分配利润Retained earnings外币报表折算差额Converted difference in Foreign Currency Statements所有者权益合计Total shareholder"s equity负债及所有者权益总计Total Liabilities & Equity利润表INCOME STATEMENT项目ITEMS产品销售收入Sales of products其中:出口产品销售收入Including:Export sales减:销售折扣与折让Less:Salesdiscount and allowances产品销售净额Net sales of products减:产品销售税金Less:Sales tax产品销售成本Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利Gross profit on sales 减:销售费用Less:Selling expenses 管理费用General and administrative expenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome) 汇兑损失(减汇兑收益)Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment 加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain for previous years利润总额Total profit减:所得税Less:Income tax净利润Net profit本文来自: 人大经济论坛会计与财务管理版,详细出处参考:/bbs/viewthread.php ?tid=335564&page=1会计要素的计量属性basis of measurement历史成本historical cost重置成本replacement cost可实现净值net-realizable value现值present value公允价值fair value财务报告financial statement资产负债表Balance Sheet利润表Income Statement现金流量表Cash Flow Statement所有者权益变动表Statement of Changes in Equity附注notesDisclosure notesChap. 2货币资金monetary assets现金cash银行账户bank account现金等价物cash equivalentChap. 3金融资产financial instruments以公允价值计量且变动计入当期损益的金融资产Measure at fair value through profit or loss 交易性金融资产held for trading指定为以公允价值计量且变动计入当期损益的金融资产Identified as at fair value through profit or loss持有到期投资Held-to –maturity investment贷款和应收账款Loans and receivables可供出售金融资产available-for-sale financial assets减值impairment减值损失impairment lossChap. 4存货inventory存货的种类:Classification of inventory原材料raw materials inventory在产品work-in-progress inventory半成品component parts产成品finished goods inventory商品merchandise inventory周转材料supplies inventory发出存货的计量cost flow assumption先进先出法first-in-first-out (FIFO)后进先出法last-in-first-out (LIFO)移动加权平均法moving-average unit cost 全月一次加权平均法weighted-average system个别计价法(具体辨认法)specific identification期末存货的计量ending balance of inventory成本与可变现净值孰低lower-of –cost-or-market valueNet-realizable value存货跌价准备Allowance to reduce inventory to LCM资产减值损失—存货减值损失loss of impairment on assets ---- loss of impairment on inventoryChap. 5长期股权投资long-term investment –shareInvestment in subsidiary ***成本法cost method权益法equity method投资收益investment income可转换convertibleChap. 6固定资产capital assets在建工程wok-in-progress construction折旧amortization平均年限法straight-line-method工作量法unit-of- production双倍余额递减法declining-balance method年数总和法sum-of-the-years-digits method后续支出subsequent expenditure资本化capitalized cost费用化expensed cost处置retirement and disposal持有待售的固定资产capital assets held for sale固定资产清理disposal of capital assets固定资产减值准备allowance of impairments on capital assetsChap. 7无形资产intangible assets专利权patents非专利技术industrial design registration 商标权trademarks and trade name著作权copyright特许权franchise rights土地使用权rights of using landChap. 8投资性房地产investment property /profitable estateChap. 9非货币性资产交换non-monetary assets exchange商业实质commercial substanceChap. 10资产减值assets impairment估计evaluation资产组assets group cash generate unit 商誉goodwillChap. 11负债liabilities流动负债current liabilities非流动负债non-current liabilities初始计量initial measurement辞退福利fire fringe进口import出口export可转换公司债券convertible bondChap. 12所有者权益equity实收资本issued capital资本公积capital reserve股本溢价share premium留存收益retained earnings未分配利润distributed profitChap. 13完工百分比法percentage of completion method建造合同construction contract直接法direct method间接法indirect method分部报告segment report关联方related party租赁lease担保guaranteeChap. 15或有事项contingencies或有资产contingent assets或有负债contingent liabilities亏损合同onerous contractChap.16重组reorganization /resutructionChap. 18借款费用borrowing costs borrowingexpenditure溢价premium折价discount资本化capitalize costsChap. 20所得税income tax计税基础tax base永久性差别permanent difference暂时性差别temporary difference应纳税暂时性差异taxable temporary differences可抵扣暂时性差异deductible temporary difference递延所得税资产deferred tax assets递延所得税负债deferred tax liabilitiesChap. 21外币折算translation of foreign currency 外币交易foreign currency transactions外币财务报表折算translation of foreign currency financial statement即期汇率current exchange rate远期汇率future exchange rate通货膨胀inflationChap. 22出租人lessor承租人lessee经营租赁operating lease融资租赁finance lease / capital lease售后租回sale and leasebackChap. 23会计政策、会计估计变更和差错更正Changes in accounting policies, changes in accounting estimates and corrections of errors会计估计Accounting estimatesChap. 24资产负债表日后事项Events after the balance sheet date调整事项Adjusting event非调整事项Unadjusting event利润分配profit allocation以前年度损益调整retained earnings--prior year adjustment Undistributed profit—prior year adjustmentChap. 25企业合并corporate combination长期股权投资long-term investment--shareInvestment in subsidiary ***Chap. 26合并财务报表consolidated financial statementConsolidated Balance Sheet Consolidated Income Statement Consolidated Cash Flow Statement Consolidated Statement of Changes in Equity。

财务报表英文翻译大全

《财务报表英文翻译大全》摘要:编制单位: ______年______月________日单位: 元 Prepared by: Month:_______Date:_______Year Monetary unit:_______ 资产 Assets 行次Line No. 年初数 Beg. balance 期末数 End. balance 负债和所有者权益(或股东权益) Liabilities Owners’ (Stockholders’) equity 行次 Line No. 年初数 Beg. balance 期末数 End. balance 流动资产: Current assets 流动负债Current liabilities 货币资金 Monetary funds 1 .38 .45 短期借款 Short-term loans 短期投资 Short-term investment 2 应付票据 Notes payable 应收票据 Notes receivable 3 .68 .00 应付账款 Accounts payable 应收股利 Dividend receivable 4 预收账款 Advances from customers 应收利息 Interest receivable 5 应付工资 Accrued payroll 应收账款 Accounts receivable 6 .57 .05 应付福利费 Welfare expenses payable 其他应收款 Other receivable 7 .88 .07 应付股利 Dividend payable 预付账款 Advances to suppliers 8 .42 .29 应交税金 Taxes payable 应收补贴款 Subsidies receivable 9 其他应交款 Other payables 存货 Inventories 10 .93 .50 其他应付款 Other amounts payable 待摊费用 Prepaid expenses 11 .06 49722.24 预提费用 Accrued expenses 一年内到期的长期债权投资 Long-term debt investment due within a year 21 预计负债 Estimated liabilities 其他流动资产 Other current assets 24 一年内到期的长期负债 Long-term liabilities due within a year 流动资产合计 Sub-total of current assets 31 .92 .60 其他流动负债 Other current liabilities 长期投资: Long-term investments: 长期股权投资 Long-term equity investment 32 流动负债合计 Sub-total of current liabilities 长期债权投资 Long-term debt investment 34 长期负债: Long-term liabilities 长期投资合计 Sub-total of long term investment 38 长期借款Long-term borrowings 固定资产: Fixed assets: 应付债券 Bonds payable 固定资产原价 Fixed assets-cost39 .08 .52 长期应付款 Long-term payables 减: 累计折旧 Less: Accumulated depreciation 40 .35 .71 专项应付款Special payables 固定资产净值 Fixed assets-NBV 41 .73 .81 其他长期负债 Other long-term liabilities 减: 固定资产减值准备 Less: Provision for impairment of fixed assets 42 .73 .81 长期负债合计 Sub-total of long-term liabilities 固定资产净额 Fixed assets-net 43 .73 .81 递延税项 Deferred taxes 工程物资 Construction materials 44 递延税款贷项 Deferred tax credit 在建工程 Construction in progress 45 负债合计 Total liabilities 固定资产清理 Disposal of fixed assets 46 固定资产合计 Sub-total of fixed assets 50 所有者权益(或股东权益)Owner’s (Stockholders’) equity 无形资产及其他资产 Intangible and other assets 实收资本(或股本) Paid-in capital (or stock) 无形资产 Intangible assets 51 减:已归还投资 Less: Investment returned 长期待摊资产 Long-term prepayment 52 实收资本(或股本)净额 Paid-in capital (or stock) - net 其他长期资产 Other long-term assets 53 资本公积 Capital surplus 无形资产及其他资产合计 Sub-total of intangible and other assets 60 赢余公积 Surplus reserve 其中:法定公益金 Including: Statutory public welfare fund 递延税项: Deferred taxes: 未分配利润Undistributed profit 递延税款借项 Deferred tax debit 61 所有者权益(或股东权益)合计Total owner’s (stockholders’) equity 资产总计 Total assets 67 负债和所有者权益(或股东权益)合计Total liabilities owner’s (stockholders’) equity 利润表 Income Statement 编制单位: ______年______月________日单位: 元Prepared by: Month: _______Date:_______Year Monetary unit: RMB Yuan 项目 Item 行次 Line No. 本月数Current month 本年累计数 Current year accumulative 一、主营业务收入 I. Revenue from main operations 减:主营业务成本 Less: Cost of main operations 主营业务税金及附加 Taxes and surcharges for main operations 二、主营业务利润(亏损以“-”填列) II. Profit/Loss from main operations 加:其他业务利润(亏损以“-”填列) Add: Profit/Loss from other operations 减:营业费用 Less: Operating expenses 管理费用 General and administrative expenses 财务费用 Financial expenses 三、营业利润(亏损以“-”填列) III. Operating profit/loss 加:投资收益(亏损以“-”填列) Add: Investment income/losses 补贴收入 Revenue from subsidies 营业外收入Non-operating revenue 减:营业外支出 Less: Non-operating expenditures 四、利润总额(亏损以“-”填列) IV. Income/Loss before tax 减:所得税 Less: Income tax 五、净利润(亏损以“-”填列) V. Net income/loss 补充资料Supplementary information: 项目 Item 本年累计数 Current year cumulative 上年实际数 Prior year actual 1. 出售、处理部门或被投资单位所得收益 Gain on sale and disposal of a department or an invested enterprise 2. 自然灾害发生的损失 Losses arising from natural disasters 3. 会计政策变更增加(或减少)利润总额 Increase/decrease in income before tax due to a change in accounting policy 4. 会计估计变更增加(或减少)利润总额Increase/decrease in income before tax due to a change in accounting estimate 5. 债务重组损失 Losses arising from debt restructurings 6. 其他 Others 现金流量表 Cash Flow Statement 编制单位:年度单位: 元 Prepared by: Period:_________ Monetary unit: RMB Yuan 项目 Item 行次 Line No. 金额Amount 一、经营活动产生的现金流量 I. Cash flows from operating activities 销售产品、提供劳务收到的现金 Cash received from the sale of goods or rendering of services 收到的税费返还 Refunds of taxes 收到的其他与经营活动有关的现金 Other cash receipts relating to operating activities 现金流入小计 Sub-total of cash inflows 购买商品、接受劳务支付的现金 Cash paid for goods and services 支付给职工及为职工支付的现金 Cash paid to and on behalfof employees 支付的各项税费 Payments of all types of taxes 支付的其他与经营活动有关的现金 Other cash payments relating to operating activities 现金流出小计 Sub-total of cash outflows 经营活动产生的现金流量净额Net cash flows from operating activities 二、投资活动产生的现金流量 II. Cash flows from investing activities 收回投资所收到的现金 Cash received from return of investments 取得投资收益所收到的现金 Cash received from return on investment 处置固定资产、无形资产和其他长期资产所收回的现金净额 Net cash received from the sale of fixed assets, intangible assets and other long-term assets 收到的其他与投资活动有关的现金 Other cash receipts relating to investing activities 现金流入小计 Sub-total of cash inflows 购建固定资产、无形资产和其他长期资产所支付的现金 Cash paid to acquire fixed assets, intangible assets and other long-term assets 投资所支付的现金 Cash paid to acquire investments 支付的其他与投资活动有关的现金 Other cash payment relating to investing activities 现金流出小计 Sub-total of cash outflows 投资活动产生的现金流量净额 Net cash flows from investing activities 三、筹资活动产生的现金流量: III. Cash flows from financing activities: 吸收投资所收到的现金 Cash received from investment by others 借款所收到的现金 Cash received from borrowings 收到的其他与筹资活动有关的现金 Other cash receipts relating to financing activities 现金流入小计 Sub-total of cash inflows 偿还债务所支付的现金 Cash payment of amounts borrowed 分配股利、利润或偿付利息所支付的现金 Cash paid for distribution of dividends or profits and for interest expense 支付的其他与筹资活动有关的现金 Other cash payments relating to financing activities 现金流出小计 Sub-total of cash outflows 筹资活动产生的现金流量净额 Net cash flow financing activities 四、汇率变动对现金的影响 IV. Effect of changes in foreign exchange rate on cash 五、现金及现金等价物净增加额 V. Net increase in cash and cash equivalents 补充资料 Supplementary Information 行次 Line No. 金额 Amount 1. 将净利润调节为经营活动现金流量: Reconciliation of net income to cash flows from operating activities 净利润Net income 加:计提的资产减值准备 Add: Provision for impairment of assets 固定资产折旧 Depreciation of fixed assets 无形资产摊销 Amortization of intangible assets 长期待摊费用摊销 Amortization of long-term prepayment 待摊费用减少(减:增加) Decrease in prepaid expense (or deduct: increase) 预提费用增加(减:减少) Increaseof accrued expenses (or deduct: decrease) 处置固定资产、无形资产和其他长期资产的损失(减:收益) Losses on disposal of fixed assets, intangible assets and other long-term assets (or deduct: gains) 固定资产报废损失 Losses on scrapping of fixed assets 财务费用 Financial expenses 投资损失(减:收益) Investments losses (or deduct: gains) 递延税款贷项(减:借项) Deferred tax credit (or deduct: debit) 存货的减少(减:增加) Decrease in inventories (or deduct: increase) 经营性应收项目的减少(减:增加) Decrease in operating payables (or deduct: increase) 经营性应收项目的增加(减:减少) Increase in operating payables (or deduct: decrease) 其他 Other经营活动产生的现金流量净额 Net cash flows from operating activities 2. 不涉及现金收支的投资和筹资活动 Investing and financing activities that do not involve cash receipts and payments 债务转化为资本 Conversion of debt into capital 一年内到期的可转换公司债券 Convertible bonds to be expired within one year 融资租入固定资产 Fixed assets under finance lease 3. 现金及现金等价物净增加情况: Net increase in cash and can equivalents 现金的期末余额 Cash at end of period 减:现金的期初余额 Less: Cash at the beginning of the period 加:现金等价物的期末余额 Plus: Cash equivalents at the end of the period 减:现金等价物的期初余额 Less: Cash equivalents at the beginning of the period 现金及现金等价物净增加额 Net increase in cash and cash equivalents 资产减值准备明细表 Statement of Provision for Impairment of Assets 编制单位:年度单位: 元Prepared by: Period:_________ Monetary unit: RMB Yuan 项目 Item 年初余额 Beginning balance 本年增加数 Increase for current year 本年转回数 Reversal for current year 年末余额 Ending balance 一、坏账准备合计 I. Total amounts of bad debts provided 其中:应收账款 Including: Accounts receivable 其他应收款 Other receivables 二、短期投资跌价准备合计 II. Total amounts of short-term investments write-down provided 其中:股票投资 Including: Stock investment 债券投资 Bond investment 三、存货跌价准备合计Ⅲ. Total amounts of inventory written-down provided 其中:库存商品 Including: Goods on hand 原材料 Raw materials 四、长期投资减值准备合计Ⅳ. Total amounts provided for impairment of long-term investments 其中:长期股权投资Including: Long-term equity investment 长期债权投资 Long-term debt investment 五、固定资产减值准备合计Ⅴ. Total amounts provided for impairment of fix ed assets 其中:房屋、建筑物 Including: Buildings and structures 机器设备 Equipment and machinery 六、无形资产减值准备Ⅵ. Provision for impairment of intangible assets 其中:专利权 Including: Patent 商标权 Trade marks 七、在建工程减值准备Ⅶ. Provision for impairment of construction in progress 八、委托贷款减值准备Ⅷ. Provision for impairment of designated loan receivable 注:根据财会[2003]10号文件规定,此表已变动,请参见第404-407页资产负债表 Balance Sheet 编制单位: ______年______月________日单位: 元 Prepared by:Month:_______Date:_______Year Monetary unit:_______ 资产 Assets 行次Line No. 年初数 Beg. balance 期末数 End. balance 负债和所有者权益(或股东权益) Liabilities Owners’ (Stockholders’) equity 行次 Line No. 年初数 Beg. balance 期末数End. balance 流动资产: Current assets 流动负债 Current liabilities 货币资金Monetary funds 1 .38 .45 短期借款 Short-term loans 短期投资 Short-term investment 2 应付票据 Notes payable 应收票据 Notes receivable 3 .68 .00 应付账款 Accounts payable 应收股利 Dividend receivable 4 预收账款 Advances from customers 应收利息 Interest receivable 5 应付工资 Accrued payroll 应收账款 Accounts receivable6 .57 .05 应付福利费 Welfare expenses payable 其他应收款 Other receivable 7 .88 .07 应付股利 Dividend payable 预付账款 Advances to suppliers 8 .42 .29 应交税金 Taxes payable 应收补贴款 Subsidies receivable 9 其他应交款 Other payables 存货Inventories 10 .93 .50 其他应付款 Other amounts payable 待摊费用 Prepaid expenses11 .06 49722.24 预提费用 Accrued expenses 一年内到期的长期债权投资 Long-termdebt investment due within a year 21 预计负债 Estimated liabilities 其他流动资产Other current assets 24 一年内到期的长期负债 Long-term liabilities due within a year 流动资产合计 Sub-total of current assets 31 .92 .60 其他流动负债 Other current liabilities 长期投资: Long-term investments: 长期股权投资 Long-term equity investment 32 流动负债合计 Sub-total of current liabilities 长期债权投资 Long-term debt investment 34 长期负债: Long-term liabilities 长期投资合计 Sub-total of long term investment 38 长期借款 Long-term borrowings 固定资产: Fixed assets: 应付债券 Bonds payable 固定资产原价 Fixed assets-cost 39 .08 .52 长期应付款 Long-term payables 减: 累计折旧 Less: Accumulated depreciation 40 .35 .71 专项应付款 Special payables 固定资产净值 Fixed assets-NBV 41 .73 .81 其他长期负债 Other long-term liabilities 减: 固定资产减值准备 Less: Provision for impairment of fixed assets42 .73 .81 长期负债合计 Sub-total of long-term liabilities 固定资产净额 Fixed assets-net 43 .73 .81 递延税项 Deferred taxes 工程物资 Construction materials 44 递延税款贷项 Deferred tax credit 在建工程 Construction in progress 45 负债合计 Total liabilities 固定资产清理 Disposal of fixed assets 46 固定资产合计 Sub-total offixed assets 50 所有者权益(或股东权益)Owner’s (Stockholders’) equity 无形资产及其他资产 Intangible and other assets 实收资本(或股本) Paid-in capital (or stock) 无形资产 Intangible assets 51 减:已归还投资 Less: Investment returned 长期待摊资产 Long-term prepayment 52 实收资本(或股本)净额 Paid-in capital (or stock) - net 其他长期资产 Other long-term assets 53 资本公积 Capital surplus 无形资产及其他资产合计 Sub-total of intangible and other assets 60 赢余公积 Surplus reserve 其中:法定公益金 Including: Statutory public welfare fund 递延税项: Deferred taxes: 未分配利润 Undistributed profit 递延税款借项 Deferred tax debit 61 所有者权益(或股东权益)合计Total owner’s (stockholders’) equity 资产总计 Total assets 67 负债和所有者权益(或股东权益)合计Total liabilities owner’s (stockholders’) equity 利润表 Income Statement 编制单位: ______年______月________日单位: 元Prepared by: Month: _______Date:_______Year Monetary unit: RMB Yuan 项目Item 行次 Line No. 本月数 Current month 本年累计数 Current year accumulative 一、主营业务收入 I. Revenue from main operations 减:主营业务成本 Less: Cost of main operations 主营业务税金及附加 Taxes and surcharges for main operations 二、主营业务利润(亏损以“-”填列) II. Profit/Loss from main operations 加:其他业务利润(亏损以“-”填列) Add: Profit/Loss from other operations 减:营业费用 Less: Operating expenses 管理费用 General and administrative expenses 财务费用Financial expenses 三、营业利润(亏损以“-”填列) III. Operating profit/loss 加:投资收益(亏损以“-”填列) Add: Investment income/losses 补贴收入Revenue from subsidies 营业外收入 Non-operating revenue 减:营业外支出Less: Non-operating expenditures 四、利润总额(亏损以“-”填列) IV. Income/Loss before tax 减:所得税 Less: Income tax 五、净利润(亏损以“-”填列) V. Net income/loss 补充资料Supplementary information: 项目 Item 本年累计数 Current year cumulative 上年实际数 Prior year actual 1. 出售、处理部门或被投资单位所得收益 Gain on sale and disposal of a department or an invested enterprise 2. 自然灾害发生的损失Losses arising from natural disasters 3. 会计政策变更增加(或减少)利润总额Increase/decrease in income before tax due to a change in accounting policy 4. 会计估计变更增加(或减少)利润总额 Increase/decrease in income before tax due to a change in accounting estimate 5. 债务重组损失 Losses arising from debt restructurings 6. 其他 Others 现金流量表 Cash Flow Statement 编制单位:年度单位: 元 Prepared by: Period:_________ Monetary unit: RMB Yuan 项目 Item 行次 Line No. 金额 Amount 一、经营活动产生的现金流量 I. Cash flows from operating activities 销售产品、提供劳务收到的现金 Cash received from the sale of goods or rendering of services 收到的税费返还 Refunds of taxes 收到的其他与经营活动有关的现金 Other cash receipts relating to operating activities 现金流入小计Sub-total of cash inflows 购买商品、接受劳务支付的现金 Cash paid for goods and services 支付给职工及为职工支付的现金 Cash paid to and on behalf of employees 支付的各项税费 Payments of all types of taxes 支付的其他与经营活动有关的现金 Other cash payments relating to operating activities 现金流出小计 Sub-total of cash outflows 经营活动产生的现金流量净额 Net cash flows from operating activities 二、投资活动产生的现金流量 II. Cash flows from investing activities 收回投资所收到的现金Cash received from return of investments 取得投资收益所收到的现金 Cash received from return on investment 处置固定资产、无形资产和其他长期资产所收回的现金净额Net cash received from the sale of fixed assets, intangible assets and other long-term assets 收到的其他与投资活动有关的现金 Other cash receipts relating to investingactivities 现金流入小计 Sub-total of cash inflows 购建固定资产、无形资产和其他长期资产所支付的现金 Cash paid to acquire fixed assets, intangible assets and other long-term assets 投资所支付的现金 Cash paid to acquire investments 支付的其他与投资活动有关的现金 Other cash payment relating to investing activities 现金流出小计 Sub-total of cash outflows 投资活动产生的现金流量净额 Net cash flows from investing activities 三、筹资活动产生的现金流量: III. Cash flows from financing activities: 吸收投资所收到的现金 Cash received from investment by others 借款所收到的现金 Cash received from borrowings 收到的其他与筹资活动有关的现金 Other cash receipts relating to financing activities 现金流入小计 Sub-total of cash inflows 偿还债务所支付的现金 Cash payment of amounts borrowed 分配股利、利润或偿付利息所支付的现金Cash paid for distribution of dividends or profits and for interest expense 支付的其他与筹资活动有关的现金 Other cash payments relating to financing activities 现金流出小计 Sub-total of cash outflows 筹资活动产生的现金流量净额 Net cash flow financing activities 四、汇率变动对现金的影响 IV. Effect of changes in foreign exchange rate on cash 五、现金及现金等价物净增加额 V. Net increase in cash and cash equivalents 补充资料 Supplementary Information 行次 Line No. 金额 Amount 1. 将净利润调节为经营活动现金流量: Reconciliation of net income to cash flows from operating activities 净利润 Net income 加:计提的资产减值准备 Add: Provision for impairment of assets 固定资产折旧 Depreciation of fixed assets 无形资产摊销 Amortization of intangible assets 长期待摊费用摊销 Amortization of long-term prepayment 待摊费用减少(减:增加) Decrease in prepaid expense (or deduct: increase) 预提费用增加(减:减少)Increase of accrued expenses (or deduct: decrease) 处置固定资产、无形资产和其他长期资产的损失(减:收益) Losses on disposal of fixed assets, intangible assets and other long-term assets (or deduct: gains) 固定资产报废损失 Losses on scrapping of fixed assets 财务费用 Financial expenses 投资损失(减:收益) Investments losses (or deduct: gains) 递延税款贷项(减:借项) Deferred tax credit (or deduct: debit) 存货的减少(减:增加) Decrease in inventories (or deduct: increase) 经营性应收项目的减少(减:增加) Decrease in operating payables (or deduct: increase) 经营性应收项目的增加(减:减少) Increase in operating payables (or deduct: decrease) 其他Other 经营活动产生的现金流量净额 Net cash flows from operating activities 2. 不涉及现金收支的投资和筹资活动 Investing and financing activities that do not involve cashreceipts and payments 债务转化为资本 Conversion of debt into capital 一年内到期的可转换公司债券 Convertible bonds to be expired within one year 融资租入固定资产Fixed assets under finance lease 3. 现金及现金等价物净增加情况: Net increase in cash and can equivalents 现金的期末余额 Cash at end of period 减:现金的期初余额Less: Cash at the beginning of the period 加:现金等价物的期末余额 Plus: Cash equivalents at the end of the period 减:现金等价物的期初余额 Less: Cash equivalents at the beginning of the period 现金及现金等价物净增加额 Net increase in cash and cash equivalents 资产减值准备明细表 Statement of Provision for Impairment of Assets 编制单位:年度单位: 元 Prepared by: Period:_________ Monetary unit: RMB Yuan 项目 Item 年初余额 Beginning balance本年增加数 Increase for current year 本年转回数 Reversal for current year 年末余额Ending balance 一、坏账准备合计 I. Total amounts of bad debts provided 其中:应收账款 Including: Accounts receivable 其他应收款 Other receivables 二、短期投资跌价准备合计 II. Total amounts of short-term investments write-down provided 其中:股票投资 Including: Stock investment 债券投资 Bond investment 三、存货跌价准备合计Ⅲ. Total amounts of inventory written-down provided 其中:库存商品Including: Goods on hand 原材料 Raw materials 四、长期投资减值准备合计Ⅳ. Total amounts provided for impairment of long-term investments 其中:长期股权投资 Including: Long-term equity investment 长期债权投资 Long-term debt investment 五、固定资产减值准备合计Ⅴ. Total amounts provided for impairmentof fixed assets 其中:房屋、建筑物 Including: Buildings and structures 机器设备Equipment and machinery 六、无形资产减值准备Ⅵ. Pro vision for impairment of intangible assets 其中:专利权 Including: Patent 商标权 Trade marks 七、在建工程减值准备Ⅶ. Provision for impairment of construction in progress 八、委托贷款减值准备Ⅷ. Provision for impairment of designated loan receivable 注:根据财会[2003]10号文件规定,此表已变动,请参见第404-407页。

财务术语中英文翻译

财务术语中英文翻译流动资产CURRENT ASSETS:现金Cash on hand银行存款Cash in bank有价证券Marketable securitiea应收票据Notes receivable应收帐款Accounts receivable坏帐准备Provision for bad debts预付帐款Advances to suppliers其他应收款Other receivables待摊费用Deferred and prepaid expenses存货Inventories存货变现损失准备Provision for loss on realization of inventory一年内到期的长期债券投资Long-term investments maturing within one year其他流动资产Other current assets长期投资Long-term in vestments一年以上的应收款项Receivables collectable after one year固定资产:FIXED ASSETS:固定资产原价Fixed assets-cost累计折旧Accumulated depreciation固定资产净值Fixed assets-net value固定资产清理Disposal of fixed assets在建工程Construction in progress无形资产INTANGIBLE ASSETS:场地使用权Land occupancy right工业产权及专有技术Proprietary technology and patents 其他无形资产Other intangibles assets其他资产:OTHER ASSETS开办费Organization expenses筹建期间汇兑损失Exchange loss during start-up peried 递延投资损失Deferred loss on investments递延税款借项Deferred taxes debit其他递延支出Other deferred expenses待转销汇兑损失Unamortized cxehange loss流动负债CURRENT LIABILITIES:短期借款Short term loans应付票据Notes payable应付帐款Accounts payable应付工资Accrued payroll应交税金T axes payable应付利润Dividends payable预收货款Advances from customers其他应付款Other payables预提费用Accrued expenses应付福利费Staff and workers bonus and welfare fund一年内到期的长期负债Long-term liabitities due within one year其他流动负债Other current liabilities长期负债LING-TERMLIABILITIES长期借款Ling-term loans应付公司债Debentures payable应付公司债溢价(折价)Premium(discount)on debentures payable一年以上的应付款项Payables due after one year其他负债OTHER LIABILITES筹建期间汇兑收益Exchange gain during start-up period 递延投资收益Deferred gain on investments递延税款贷项Deferred taxes credit其他递延贷项Other deferred credit待转销汇兑收益Unamortized exchange gain所有者权益:OWNERS' EQUITY实收资本Paid in capital其中:中方投资Including:Chinese investment其中:外方投资Including:Foreign investment已归还投资Investment returned资本公积Capital surplus储备基金Reserve fund企业发展基金Enterprise expansion fund利润归还投资Profits capitalised on return of investment 本年利润current year profit未分配利润Undistributed profits主营业务收入Revenue from main operation主营业务成本Cost of main operation主营业务税金及附加T ax and additional duty of main operation主营业务利润Income from main operation其他业务利润Incom from other operation营业费用Operating expense管理费用General and administrative expense 财务费用Financial expense利息支出Interest expense汇兑损失Exchange loss营业利润Operating Income投资收益Investment income营业外收入Non-operating income营业外支出Non operating expense利润总额Income before tax所得税income tax净利润Net income你这太长了,有些自己都不大记得了,尽力帮你。

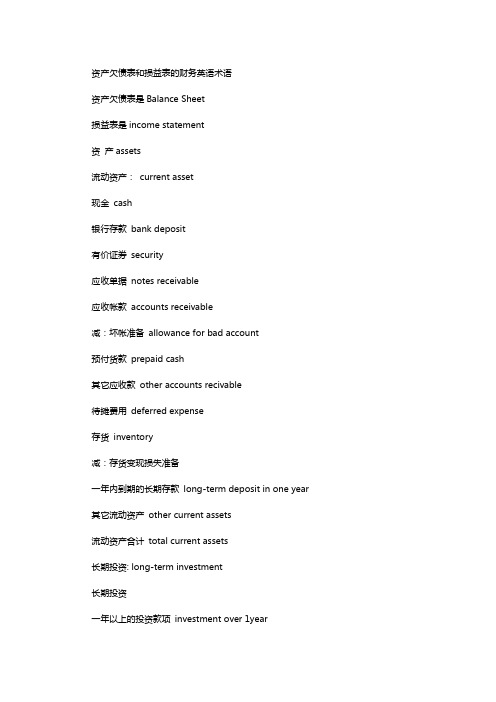

资产欠债表和损益表的财务英语术语

资产欠债表和损益表的财务英语术语资产欠债表是Balance Sheet损益表是income statement资产assets流动资产:current asset现金cash银行存款bank deposit有价证券security应收单据notes receivable应收帐款accounts receivable减:坏帐准备allowance for bad account预付货款prepaid cash其它应收款other accounts recivable待摊费用deferred expense存货inventory减:存货变现损失准备一年内到期的长期存款long-term deposit in one year 其它流动资产other current assets流动资产合计total current assets长期投资: long-term investment长期投资一年以上的投资款项investment over 1year固定资产:fixed assets固定资产原价original price减:累计折旧accumulated depreciation固定资产净值net book value融资租入固定资产原值减:累计折旧accumulated depreciation融资租入固定资产净值固定资产清理disposal of fixed assets在建工程:在建工程construction-in-progress无形资产:intangible assets场地利用权leasehold工业产权及专有技术franchises and patents其它无形资产other intangible assets无形资产合计total intangible assets其它资产:other assets开办费setting-up筹建期间汇兑损失exchange loss递延投资损失deferred investment loss递延税款借项debit of deferred tax其它递延支出other deferred expense待转销汇兑损失available-for-sale exchange loss其它资产合计total other assets资产共计total assets欠债及所得者权益liabilities and owners' equity流动欠债:current liabilities短时间借款short-term liability应付单据notes payable应付帐款accounts payable应付工资salaries payable预收货款accrued accounts应交税金taxes payable应付股利dividends payable应付福利费allowance payable其他应付款other accounts payable职工奖励及福利基金bonus and allowance bond一年内到期的长期借款short term accounts payable其它流动欠债other current liabilities流动欠债合计total current liabilities长期欠债:long-term liabilities长期借款应付公司溢价(折价)premium/discount coporate liability 中间的省略产品销售收入sales revenue其中:出口产品销售收入export goods sales revenue减:销售折扣与折让less:sales allowance and discounts产品销售净额net sales减:产品销售本钱less: cost of goods sold其中:出口产品销售本钱cost of exported goods sold产品销售税金sales tax产品销售毛利gross profit减:销售费用sales expense管理费用operating expense财务费用finance expence其中:汇兑损失(减汇兑收益)exchange loss(less exchange gain) 利息支出(减利息收入)interest expense(less interest revenue) 产品销售利润net sales加:其它业务利润add: other income补助收入bonus income营业利润加:投资收益add: investment gains营业外收入extra-operating revenue减:营业外支出^^^^^^^^^^expense加:以前年度损益调整利润总额total income减:所得税less: income tax净利润net income流动资产CURRENT ASSETS:现金Cash on hand银行存款Cash in bank有价证券Marketable securitiea应收单据Notes receivable应收帐款Accounts receivable坏帐准备Provision for bad debts预付帐款Advances to suppliers其他应收款Other receivables待摊费用Deferred and prepaid expenses存货Inventories存货变现损失准备Provision for loss on realization of inventory一年内到期的长期债券投资Long-term investments maturing within one year 其他流动资产Other current assets长期投资Long-term in vestments一年以上的应收款项Receivables collectable after one year固定资产:FIXED ASSETS:固定资产原价Fixed assets-cost累计折旧Accumulated depreciation固定资产净值Fixed assets-net value固定资产清理Disposal of fixed assets在建工程Construction in progress无形资产INTANGIBLE ASSETS:场地利用权Land occupancy right工业产权及专有技术Proprietary technology and patents 其他无形资产Other intangibles assets其他资产:OTHER ASSETS开办费Organization expenses筹建期间汇兑损失Exchange loss during start-up peried 递延投资损失Deferred loss on investments递延税款借项Deferred taxes debit其他递延支出Other deferred expenses待转销汇兑损失Unamortized cxehange loss流动欠债CURRENT LIABILITIES:短时间借款Short term loans应付单据Notes payable应付帐款Accounts payable应付工资Accrued payroll应交税金T axes payable应付利润Dividends payable预收货款Advances from customers其他应付款Other payables预提费用Accrued expenses应付福利费Staff and workers bonus and welfare fund一年内到期的长期欠债Long-term liabitities due within one year其他流动欠债Other current liabilities长期欠债LING-TERMLIABILITIES长期借款Ling-term loans应付公司债Debentures payable应付公司债溢价(折价)Premium(discount)on debentures payable 一年以上的应付款项Payables due after one year其他欠债OTHER LIABILITES筹建期间汇兑收益Exchange gain during start-up period递延投资收益Deferred gain on investments递延税款贷项Deferred taxes credit其他递延贷项Other deferred credit待转销汇兑收益Unamortized exchange gain所有者权益:OWNERS' EQUITY实收资本Paid in capital其中:中方投资Including:Chinese investment其中:外方投资Including:Foreign investment已归还投资Investment returned资本公积Capital surplus储蓄基金Reserve fund企业发展基金Enterprise expansion fund利润归还投资Profits capitalised on return of investment今年利润current year profit未分派利润Undistributed profits主营业务收入Revenue from main operation主营业务本钱Cost of main operation主营业务税金及附加Tax and additional duty of main operation主营业务利润Income from main operation其他业务利润Incom from other operation营业费用Operating expense管理费用General and administrative expense 财务费用Financial expense 利息支出Interest expense汇兑损失Exchange loss营业利润Operating Income投资收益Investment income营业外收入Non-operating income营业外支出Non operating expense利润总额Income before tax所得税income tax净利润Net incomeCertificate in Internal Auditing 内部审计证书Certificate in Management Accounting 管理会计证书Certificate Public Accountant注册会计师Cost accounting 本钱会计External users 外部利用者Financial accounting 财务会计Financial Accounting Standards Board 财务会计准则委员会Financial forecast 财务预测Generally accepted accounting principles 公认会计原则General-purpose information 通用目的信息Government Accounting Office 政府会计办公室Income statement 损益表Institute of Internal Auditors 内部审计师协会Institute of Management Accountants 管理会计师协会Integrity 整合性Internal auditing 内部审计Internal control structure 内部控制结构Internal Revenue Service 国内收入署Internal users 内部利用者Management accounting 管理会计Return of investment 投资回报Return on investment 投资报酬Securities and Exchange Commission 证券交易委员会Statement of cash flow 现金流量表Statement of financial position 财务状况表T ax accounting 税务会计Accounting equation 会计等式Articulation 勾稽关系Assets 资产Business entity 企业个体Capital stock 股本Corporation 公司Cost principle 本钱原则Creditor 债权人Deflation 通货紧缩Disclosure 批露Expenses 费用Financial statement 财务报表Financial activities 筹资活动Going-concern assumption 持续经营假设Inflation 通货膨涨Investing activities 投资活动Liabilities 欠债Negative cash flow 负现金流量Operating activities 经营活动Owner's equity 所有者权益Partnership 合股企业Positive cash flow 正现金流量Retained earning 留存利润Revenue 收入Sole proprietorship 独资企业Solvency 清偿能力Stable-dollar assumption 稳定货币假设Stockholders 股东Stockholders' equity 股东权益Window dressing 门面粉饰Account 帐户Accounting system 会计系统American Accounting Association 美国会计协会American Institute of CPAs 美国注册会计师协会Audit 审计Balance sheet 资产欠债表Bookkeepking 簿记Cash flow prospects 现金流量预测今天收到一条会计专业的术语,感觉蛮成心思的,发上来与大家分享分享^^缘分是-营业外收入;本人是-固定资产;生活是-持续经营;反思是-内部清点;爱情是-无形资产;爱人是-实收资本;孩子是-应付帐款;思念是-日记帐;吵架是-坏帐准备;成婚是-归并报表;暗恋是-收不回的呆帐;错爱是-高估净利润;疾病是-营业损失;年龄是-累计折旧;眼泪是-所有者权益;人情是-其他应付款;误解是-错误分录;解释是-更正分录;回忆是-财务分析;分手是-破产清算;复合是-回转分录;再婚是-资产重组;念书是-长期投资;买衣服是-包装费;旧情难忘是-递延资产;找情人是-营业外支出;上医院是-维修费。

course 8 Source of Capital 资本来源

Source of Capital – Debt1.Source of Funds - Capital2.Long-Term Capital3.Long-TermDebt Capital4.Bonds Proceeds at Issuance5.Bond Amortization&InterestExpense6.Capital Leases7.Deferred TaxesI.Source of Funds - CapitalA. Framework⏹Suppliers供应商- Liabilities - short-term capital⏹Creditors债权人- Debt - long-term capital⏹Investors 投资者– Equity - long-term capitalII.Long-term CapitalA. Debt Capital借入资本- Borrower⏹Borrower must comply to遵守all the terms and conditions (T&C) includedin the financing agreement⏹Borrower incurs an interest expense for its use of funds⏹Lower cost of debt; interest on debt is tax deductible⏹Borrowers must achieve the agreed financial performance targets (ratios) –covenantsMost common ratios to evaluate financing risk●Current ratio流动比率●Debt / Equity ratio●Interest (expense) coverageCovenants条款are outlined in the loan or bond indenture 债券契约(document)If the covenants are not met, debtor债务人is in default 违约A. Debt Capital - Creditor债权人⏹From a creditors standpoint debt capital is less risky than equity capitalCan impose financial requirementsCan request collateralCan take legal action⏹Creditors are willing to have a lower returnB. Equity capital – Investor⏹Investor (shareholder’s) standpointRealizes share appreciationReceives dividend⏹More risky from a shareholder’s standpointNo claims on assetsReceives dividends at the discretion of management; no share appreciation guarantee⏹Investor expects higher return than creditors⏹ 3. Long-Term Debt CapitalA. Type of Debt Instruments⏹Term loans & notesLoan reimbursed according a specified re-payment schedule⏹BondsCertificate promising to pay the holder:● A specified amount at a stated date – maturity date●Interest at a stated rate until the maturity dateIII.Long-Term Debt CapitalA. Type of Bonds 债券⏹Serial bonds分期偿还债券–redeemed赎回in instalments at specifieddates⏹Sinking fund bonds - redeemed in instalments at the discretion of the debtor ⏹Mortgage bond抵押债券–secured担保by pledged assets质押资产(buildings, equipments)⏹Convertible bonds可转换债券- equityIV.Bonds Proceeds at IssuanceA. Present Value 现值of Cash Payments现金支付⏹Bonds proceeds at issuance will be based on the sum of the present value offuture cash paymentsThe face value of the bonds (principal, par value, stated value) at maturityThe periodic interest paymentsB. Present Value Concept⏹Compound interest复利–amount invested earns interest that iscompounded annually; interest is retained and re-invested⏹Present value concept - an amount to be received in the future is discounted/ concerted to its (present) value (today) based on a given expected rate of returnC. Present Value IllustrationD. Market Rate of interest市场利率⏹The market rateof interest is the rate expected by purchasers of the bondsbased on the risks associated with future cash payments obligations⏹The market rate at the time of issuance is the effective (borrowing) interestrate⏹The interest expense is based on the effective interest rate⏹The market rate may differ from the stated rate because of fluctuationsbetweenThe time the issuer establishes the rateThe day the bonds are actually available to investorsCreditors risk assessment⏹As a result, a bond may be issued at a price that is higher or lower than itsface valueE. Issued at Par, Premium, Discount⏹ A bond is issued at pa平价发行r when a bond is issued at a price equal toits face value⏹ A bond is issued at a premium溢价发行when a bond is issued at a pricegreater than its face value⏹ A bond is issued at a discount折价发行when a bond is issued at a price lessthan its face valueF. Financial Reporting⏹On the balance sheet, bonds are reported at net book valueFace value●Minus unamortized discount●Plus unamortized premiumG. Application⏹Determine the net proceeds of a 3 year bond with a face value of $1,000. at10% interest (coupon rate) when the effective interest rate is 12%?⏹Record the net proceeds of a 3 year bond with a face value of $1,000. at 10%interest (coupon rate) when the effective interest rate is 12%?DB: Cash 952DB: Bond discount 48CR: Bond payable 1,000V.Bond Amortization&InterestExpenseA. Framework⏹Two methods for amortizing the book value账面价值of bonds that wereissued at a price other than face value票面价值The effective interest rate method–Required under IFRS, preferred under U.S. GAAPThe straight-line method: evenly amortizes the premium or discount over the life of the bondB. Effective Interest Rate Method⏹The effective interest rate method applies the market rate when the bondsare issued to the current amortized cost (book value) to determine the interest expense for the period⏹The bond amortization is the difference between the interest expense andthe interest paymentD. Application⏹Based on the net proceeds of $952 of a 3 year bond with a face value of$1,000. issued at 10% interest (coupon rate) when the effective interest rate is 12%⏹Record the interest expense, interest payment and discount amortization foryear 1, 2 and 3 using the effective interest rate method?VI. Capital Lease A. Framework⏹ Capital lease – covers a period of time that is most of the estimated useful (economic) life of the asset⏹ Assets leased are recorded as if they had been purchased - long-term assets ⏹ The lease obligation is a liability recorded as long-term debt ⏹ FASB criteriaOwnership is transferred at the end of the lease Lessee has an option to buyLease term is 75% or more of the economic life of the assetPresent value of the lease payments are 90% or more of the fair value of the assetB. Application⏹ Record the lease of an equipment with a fair value of $10,000 for 10 years with annual payments of $1,558 & interest of 9%⏹ Record the interest expense and capital lease amortization for year 1 ⏹ Record the annual asset amortizationfor 10 years with annual payments of $1,558 - interest of 9%DR: Equipement 10,000CR: Lease obligation 10,0002 - To record interest expense and amortization of capital lease for year 1DR: Interest expense 900DR: Capital lease obligation 658CR: Cash 1,5583 - To record annual depreciation of the assetDR: Depreciation expense1,000CR: Accumulated depreciation1,000VI.Deferred Taxes 递延税收A. Framework⏹Deferred taxes occur when accounting methods to prepare financialstatements (GAAP) are different than the accounting methods for tax returns⏹Deferred taxes are caused by the differences between the depreciationamounts based on GAAP rules and tax rules⏹The differences between GAAP and tax depreciation amounts are temporaryand referred as “timing differences”B. Application⏹Deferred tax liabilities are determined by using the balance sheet method: Asset – capitalized cost: $1,000NBV - GAAP: $800NBV - Tax: $500Timing difference: $300Tax rate: 40%Deferred tax liability: $120VII.Financial RatiosA. Current Ratio 流动比率= Current assets / Current liabilities⏹Determines the company’s liquidity and capacity to assume short-termliabilitiesB. Debt / Equity ratio= Long-term liabilities / Shareholders’ equity⏹Determines the level of leverage of the company - the level of long-termcapital financed through debt compared to equityC. Times Interest Earned (Interest Coverage)= Pre-tax income before interest / interest expense⏹Determines the company ability (profitability) to meet its financing (interest)obligations。

金融英语_刘文国第二版课后练习Exercises 08

Answers for Chapter eightⅠ Answer the following questions in English:1.In what section of the balance sheet would one find patents andtrademarks?Patents and trademarks can be found in section intangible section.2.Which depreciation method bases depreciation expense for a givenperiod on actual use?The Straight-line depreciation method bases depreciation expense fora given period on actual use.3.Which financial statement is prepared as of a particular date ratherthan for a period ending on a particular date?The balance sheet is prepared as a particular date.4.Who has the primary responsibility for the financial statements?Manager has the primary responsibility for the financial statements. 5.At what value is land used in a business shown on the balance sheet?Land is shown on the balance sheet at historical value.6.Which of the following results from using the LIFO method ofinventory cost flows during a period of inflation?The result is higher costs of goods sold by using the LIFO method of inventory during a period of inflation.7.What reflects the net tax effects of the temporary differencesbetween the carrying values of assets and liabilities for financial reporting purposes and amounts used for income tax purposes?The deferred income taxes result from temporary differences intaxable and financial statement income.8.What is the cost of a fixed asset less its accumulated depreciation?It is the net value of the fixed assets.9.How are held-to-maturity securities reported on the balance sheet?It is reported as current assets on the balance sheet.10.How many types of inventories does a manufacturing firm list on itsbalance sheet?There are three types of inventories that the manufacturing firmlist on its balance sheet. Such as raw material, working-in-process and finished products.11.What does the FIFO inventory method assume about the first unitspurchased?The FIFO inventory method assumes that the first units purchasedshould be first in use in order to reflect the historical cost ofgoods sold.12.What does a company record when it receives a cash payment forservices before it performs the services?The company should record it as a liability (unearned revenue) increased and meanwhile cash increased.Dr. CashCr. Liability (Unearned revenue)Ⅱ Fill in the each blank with an appropriate word or expression:1.Basic earnings per share are computed by dividing net income bynumber of outstanding shares.2.Financial statements must be prepared in accordance with generallyaccepted accounting principles.3.The annual depreciation expense using the double-declining-balancemethod is equal to multiply the twice of straight-line rate by the book value at the beginning of the year.4.Financial instruments that derive their value from an underlyingasset or index are called Derivatives.5.Accounts receivable are reported on the balance sheet at their netrealizable value.6.The book value of property, plant, and equipment is the purchaseprice minus accounting depreciation expense.7.The reporting of inventory values at the lower of cost or marketreflects the accounting principle or convention of historical.Ⅲ Translate the following sentences and passage into English:1.公司财务报表既反映了公司的财务状况,同时也是公司经营状况的综合反映。

deferred tax计算题

deferred tax计算题Deferred Tax Calculation ExerciseDeferred tax refers to the taxes that a company may owe in the future due to temporary differences between the accounting treatment of certain items and their tax treatment. In this article, we will dive into a deferred tax calculation exercise to help you better understand and apply the concept.Scenario:ABC Company, a hypothetical entity, is preparing financial statements for the year ending on December 31, 20XX. The tax rate is 25%. The following information is relevant for the deferred tax calculation:1. Depreciation- For accounting purposes, ABC Company uses straight-line depreciation over 5 years for certain assets.- For tax purposes, the same assets are depreciated using an accelerated method over 3 years.- The carrying amount of the assets at the beginning of the year is $100,000.2. Revenue Recognition- ABC Company recognizes revenue for accounting purposes when it is earned.- For tax purposes, revenue is recognized when cash is received.3. Expenses- ABC Company accrued $10,000 of expenses at year-end for accounting purposes.- For tax purposes, these expenses are tax-deductible when paid in the following year.Deferred Tax Calculation:1. Depreciation:To calculate the deferred tax liability or asset related to depreciation, we need to determine the temporary difference, which is the difference between the carrying amount of the assets for accounting purposes and their tax base.Carrying amount for accounting purposes: $100,000Tax base (accelerated depreciation): $100,000 - ($100,000 / 5 * 2) = $60,000Temporary difference: $100,000 - $60,000 = $40,000Deferred tax liability or asset: $40,000 * 25% = $10,000 (deferred tax liability)2. Revenue Recognition:Similarly, we need to compare the carrying amount of the revenue for accounting purposes with its tax base.Temporary difference: Not applicable as there is no difference between the carrying amount and the tax base for revenue recognition.Therefore, no deferred tax liability or asset is recognized for revenue recognition.3. Expenses:Here, we need to consider the temporary difference between the accrued expenses for accounting purposes and their tax-deductible amount in the following year.Temporary difference: $10,000Deferred tax liability or asset: $10,000 * 25% = $2,500 (deferred tax liability)Overall Deferred Tax Calculation:Deferred Tax Liability (Depreciation) = $10,000Deferred Tax Liability (Expenses) = $2,500Total Deferred Tax Liability (Net amount) = $12,500Conclusion:In this deferred tax calculation exercise, we examined three scenarios - depreciation, revenue recognition, and expenses - to determine the deferred tax liability or asset for ABC Company. Based on the calculations, we found that the total deferred tax liability for the year amounts to $12,500.It is important for companies to understand and calculate deferred tax liabilities or assets accurately, as they directly affect the financial statements and can impact a company's overall tax position. By properly accounting for deferred taxes, companies can present a more accurate picture of their financial performance and better manage their tax obligations.Remember that deferred tax calculations can be more complex in practice, involving various accounting methods and tax regulations. Professional advice or consulting may be necessary to ensure accurate calculations and compliance with accounting and tax standards.。

财务报表与财务分析中英文

n The cash flow received from the firm’s assets (CF(A)) must equal the cash flows to the firm’s creditors (CF(B)) and stockholders (CF(S)).

• Thus, income is reported when it is earned, even though no cash flow may have occurred.

2. Non-Cash Items 3. Time and Costs

财务报表与财务分析中英文

Non-Cash Items

the “bottom line.”

•Taxes

• 84

•(3) • Current: $71

• Deferred: $13

•Net income

•$86

• Retained earnings:

$43

• Dividends:

$43

财务报表与财务分析中英文

Income Statement Analysis

财务报表与财务分析中 英文

2020/12/22

财务报表与财务分析中英文

The Stockholders’ Report

n The guidelines used to prepare and maintain financial records and reports are generally accepted accounting principles (GAAP)(用於準備

Sylvia的学习笔记_2