外文翻译-- 欧盟成员国的增值税

vat欧洲也要交吗

vat欧洲也要交吗

如果欧盟外的公司将欧盟外的商品运送储存在某一欧盟国家,则卖家必须在该国进行VAT增值税的注册、申报和缴纳。

如果卖家将货物从欧盟某国运送到欧盟别国(消费国)的商品销售额超出了该消费国的远程销售起征点,则卖家必须在消费国进行VAT增值税的注册、申报和缴纳。

VAT (Value Added Tax)简单来说是欧盟国家普遍采用的对纳税人生产经营活动的增值额征收的税。

跨境卖家只要在欧盟范围内进行销售,不管是使用亚马逊FBA服务,还是欧盟本地仓储进行发货,都属于欧盟VAT增值税应交范畴,需要注册VAT税号并申报和缴纳税款,以免影响产品的正常销售。

如果您没有按时申报和缴纳应付税款,欧洲相关国家税局会采取惩罚措施,例如征收应缴税额之外的罚金、滞纳金、利息等。

如果卖家不遵守增值税法规相关要求,该国税局还会将该问题反映给您交易所在的平台,并要求该平台采取限制措施。

平台会在法律允许的范围内配合政府相关部门对于可能存在增值税不合规的卖家和账号进行调查;并且会在收到税局的通知后,对被认定为不合规的卖家和账号采取限制措施,包括下架货物、限制刊登和禁止销售等。

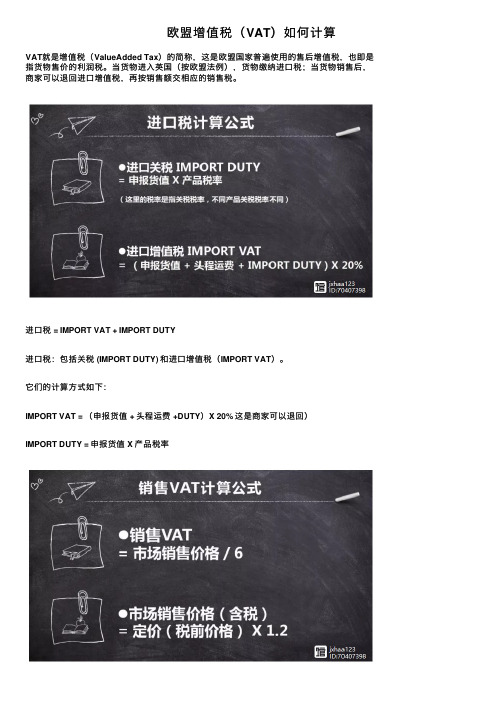

欧盟增值税(VAT)如何计算

欧盟增值税(VAT)如何计算

这是欧盟国家普遍使⽤的售后增值税,也即是

)的简称,这是欧盟国家普遍使⽤的售后增值税,也即是VAT就是增值税(ValueAdded Tax)的简称,

指货物售价的利润税。

当货物进⼊英国(按欧盟法例),货物缴纳进⼝税;当货物销售后,商家可以退回进⼝增值税,再按销售额交相应的销售税。

进⼝税 = IMPORT VAT + IMPORT DUTY

进⼝税:包括关税 (IMPORT DUTY) 和进⼝增值税(IMPORT VAT)。

它们的计算⽅式如下:

IMPORT VAT = (申报货值 + 头程运费 +DUTY)X 20% 这是商家可以退回)

IMPORT DUTY = 申报货值 X 产品税率

销售税VAT= 市场销售价格 / 6 (上缴的VAT,实为市场售价的1/6)

假如设产品申报的货值为:4000欧元

头程运费为:500欧元

关税假定为:400欧元

进⼝增值税=(申报货值+头程运费+关税)*20%=(4,000+500+400)*20%=980欧元若全部销售额为20,000欧元

销售增值税为20,000/6=3,333.3欧元

当期应缴的VAT为3,333.3-980=2,353.3欧元

注意进⼝关税不可抵扣

(⽂中部分素材来源于⽹络,如有侵权联系客服)。

VAT

简介

VAT即 Value Added Tax/ AD VALOREM tax,附加税,欧盟的一种税制,即购物时要另加税,是根据商品 的价格而征收的。如定价是 inc vat,即已含税, excl vat是未包税,Zero vat是税率为0。各国税率不相同, 如意大利是 22%税率(2013年10月开始实行),(英国是17.5%,2011年1月4日调高至20%),即要多给20%款项, 阿根廷为21%(部分商品实行50%减免,即为10.5%)。

主要税率

欧盟大部分国家主要税率有:标准税率、减免税率、零税率三种。以下为欧盟部分国家常见VAT税率分类: 英国:20%,5%、0%; 德国:19%、7%、0%; 法国:20%、 5.5%、10%、0%; 意大利:22%、5%、10%、0%; 西班牙:21%、 10%、4%

例子

举个例子,如果商家A给一个东西定价2元,增值税是17%,那他就得卖2.34元,这0.34元就是给政府的,商 家还是只收2元,但这个产品的原材料需要1元,原料供应商同样要上缴17%的增值税0.17元并提供买家增值税发 票,商家A可以用发票抵扣联去抵扣这0.17元的应缴增值税,也就是说商家A实际缴纳的增值税为其商品的增值部 分(2元-1元=1元)缴纳17%的增值税0.17元。

谢谢观看

VAT

欧盟的一种税制

01 简介

03 主要税率

目录

02 征收范围 04 例子

vat:单词vat, [væ t],n. (酿造或染色用的)大桶、大缸,vt.把……装入大桶。

VAT:单词缩写,Value-added Tax,最早起源于法国,是在欧盟应用的一种税制。等同于中国地区的增值 税。而在部分地区如澳大利亚地区又称为GST(Goods and Services Tax)。

欧盟的税收政策与税收合作

欧盟的税收政策与税收合作税收是国家经济发展的重要支柱之一,在全球范围内,各国都在积极探索和制定相应的税收政策。

欧盟作为一个经济和政治联盟,也有着自己独特的税收政策和税收合作机制。

本文将重点探讨欧盟的税收政策及其与成员国之间的税收合作方式。

一、欧盟的税收政策欧盟的税收政策主要由欧洲委员会负责制定和执行。

欧洲委员会根据欧洲联盟的宗旨和目标,致力于促进成员国之间的税收合作,协调税收政策,提升税收制度的透明度和效率,以及打击跨国税收逃避行为。

以下是欧盟的一些主要税收政策措施:1.增值税(VAT)欧盟统一增值税制度是欧盟税收政策的核心之一。

增值税是一种消费税,按照货物和服务的增值额计征,逐级追加。

欧洲委员会主导了欧盟内增值税制度的统一与协调,包括税率、纳税义务、税收申报等方面的规定。

这有助于促进欧洲内部市场的一体化和公平竞争。

2.企业所得税(CIT)欧盟的企业所得税政策旨在减少欧洲范围内的税收竞争和负面影响。

欧洲委员会提出了公平合理的企业所得税政策,通过合理的税基设定、防止利润转移和避税等手段,减少成员国之间的税收不平等,并推动成员国之间的税收合作。

3.金融交易税(FTT)金融交易税是欧盟致力于减少金融部门风险和增加稳定性的一项措施。

欧洲委员会计划推行欧洲范围内的金融交易税,以征收金融交易的一定比例。

这将有助于增加金融行业的稳定性,并为欧洲产业和公共财政提供更多的资金来源。

二、欧盟成员国间的税收合作为了加强成员国之间的税收合作,欧盟采取了一系列措施,以确保税收政策的协调和税收制度的高效运作。

以下是欧盟在税收合作方面的主要机制和举措:1.共同税收基础(CCCTB)共同税收基础是欧盟推动税收协调的一项重要举措。

该制度旨在为跨境企业提供简化的纳税义务,通过采用统一的税基计算方法,减少企业在不同国家纳税制度之间的差异,降低企业成本,促进欧洲内部市场的发展。

2.信息交换与透明度欧盟各成员国之间通过信息交换和合作促进税收透明度。

欧盟征税流程的流程和注意事项

欧盟征税流程的流程和注意事项一、欧盟征税流程。

1. 确定应税交易。

- 首先要明确交易是否属于欧盟增值税(VAT)的应税范围。

这包括商品的销售、服务的提供等。

例如,在欧盟境内销售货物,如果货物的供应地在欧盟境内,通常是应税交易。

对于服务,根据服务的类型和接受服务的对象所在地等因素来确定是否应税。

- 企业需要对自身的业务活动进行详细梳理,判断每一项交易是否涉及应税行为。

2. 注册增值税号(VAT号)- 如果企业在欧盟境内有应税交易,且达到了注册门槛(不同成员国门槛可能不同),就需要在相关成员国注册增值税号。

- 注册过程中,企业要提供准确的公司信息,包括公司名称、地址、联系方式、业务范围等。

通常需要通过当地的税务机关网站在线注册,有些情况下可能需要提交纸质文件。

- 例如,在英国(仍在一定程度上遵循欧盟增值税相关规定的过渡期内情况),企业可以通过英国税务海关总署(HMRC)的在线平台进行VAT注册。

3. 计算应纳税额。

- 对于商品销售,增值税应纳税额=应税销售额×增值税税率。

不同类型的商品可能适用不同的税率,欧盟有标准税率、低税率和零税率等多种税率结构。

- 以销售电子产品为例,如果适用标准税率20%(假设某成员国的标准税率),销售额为1000欧元,那么应纳税额 = 1000×20% = 200欧元。

- 对于服务,计算方式类似,但要根据服务的性质确定应税基数。

例如,对于咨询服务,应税基数可能是服务收费金额。

4. 开具增值税发票。

- 当发生应税交易时,企业需要按照欧盟的规定开具增值税发票。

发票上应包含必要信息,如供应商和客户的名称和地址、增值税号、发票日期、商品或服务描述、数量、单价、增值税税率和税额等。

- 发票必须清晰、准确,并且要按照规定的格式开具。

在一些成员国,电子发票也是被认可的,但同样要满足相关的电子签名、存储和可访问性等要求。

5. 申报增值税。

- 企业需要按照规定的申报周期向当地税务机关申报增值税。

欧盟财务状况分析报告(3篇)

第1篇一、引言欧盟(European Union,简称EU)是世界上最大的经济体之一,由28个成员国组成,其经济总量和影响力在全球范围内具有重要地位。

随着全球经济的不断发展,欧盟的财务状况备受关注。

本报告将对欧盟的财务状况进行详细分析,包括财政收入、支出、债务等方面,以期为我国相关决策提供参考。

二、欧盟财政收支概况1. 财政收入欧盟的财政收入主要来源于以下几个方面:(1)成员国缴纳的会费:欧盟会费是欧盟财政的主要收入来源,占欧盟财政收入的约80%。

会费缴纳标准根据各成员国的国内生产总值(GDP)和人口等因素确定。

(2)关税和进口税:欧盟对进口商品征收关税和进口税,这部分收入占欧盟财政收入的约10%。

(3)增值税:欧盟内部增值税是欧盟财政的重要收入来源,占欧盟财政收入的约10%。

(4)其他收入:包括罚款、利息收入等,占欧盟财政收入的约10%。

2. 财政支出欧盟的财政支出主要包括以下几个方面:(1)农业补贴:农业补贴是欧盟财政支出的重要组成部分,主要用于支持欧盟农业发展和农民利益。

(2)区域发展基金:区域发展基金用于支持欧盟内部欠发达地区的经济发展,缩小地区发展差距。

(3)社会保障:社会保障支出包括养老保险、失业保险、医疗保险等,占欧盟财政支出的约30%。

(4)其他支出:包括教育、科研、环境保护、外交、安全等领域支出。

三、欧盟债务状况1. 债务规模截至2020年底,欧盟债务总额达到约7.5万亿美元,占欧盟GDP的约80%。

其中,欧元区债务总额约为6.6万亿美元,占欧元区GDP的约88%。

2. 债务结构欧盟债务主要分为以下几类:(1)公共债务:包括政府债务和地方政府债务,占欧盟债务总额的约70%。

(2)私营部门债务:包括银行、企业等私营部门债务,占欧盟债务总额的约30%。

(3)家庭债务:家庭债务占欧盟债务总额的约10%。

3. 债务风险欧盟债务风险主要体现在以下几个方面:(1)债务水平较高:欧盟债务水平较高,容易引发债务危机。

european vat number格式

european vat number格式全文共四篇示例,供读者参考第一篇示例:欧洲增值税号码(European VAT number)是指欧盟成员国企业的增值税登记号码,用于在跨境贸易中进行增值税规范征收。

欧盟成员国之间的贸易是征收增值税的,而只有具有增值税号码的企业才能参与增值税交易,并享受相关的退税或减免政策。

欧洲增值税号码的格式是由各个欧盟成员国自行制定的,并且格式可能会有所不同。

一般来说,欧洲增值税号码由国家代码加上企业注册号码组成,中间可能会有一些分隔符号,具体格式如下:- 国家代码:欧盟成员国有不同的国家代码,如德国是“DE”、法国是“FR”、意大利是“IT”等等。

- 企业注册号码:根据各个国家的注册制度不同,企业注册号码可能由数字、字母或者组合而成。

举个例子,德国的欧洲增值税号码格式为“DE123456789”,其中“DE”表示德国的国家代码,而“123456789”则是企业的注册号码。

而法国的欧洲增值税号码格式可能是“FR12345678”,具体格式可能有所不同。

在申请欧洲增值税号码时,企业需要根据所在国家的规定向当地税务机关进行注册。

一般来说,欧盟成员国的税务机关会对企业进行严格审核和核实,确保企业具有合法经营资格和真实的营业信息。

一旦注册成功,企业就会获得一个独一无二的欧洲增值税号码,并可以在跨境贸易中合法开展业务。

欧洲增值税号码是欧盟成员国企业在跨境贸易中不可或缺的重要证明,具有合法性和信誉性。

企业需要按照各国的规定合法申请并使用欧洲增值税号码,避免不必要的法律风险和经济损失。

希望以上内容能为您对欧洲增值税号码有更深入的了解。

第二篇示例:欧洲增值税号(VAT number)是指欧洲国家对企业征收增值税(VAT)的一种税号,也称为欧洲税号。

不同国家有不同的VAT号格式和命名规则,但基本上都是由不同国家的地区代码、企业代码和校验码组成。

欧洲VAT号的格式通常是由数字和字母组合而成的,不同国家之间也会有所不同。

增值税暂行条例中英文对照

中华人民共和国增值税暂行条例The Provisional Regulations of the People‘s Republic of China on Value-Added Tax第一条在中华人民共和国境内销售货物或者提供加工、修理修配劳务以及进口货物的单位和个人,为增值税的纳税义务人(以下简称纳税人),应当依照本条例缴纳增值税。

Article 1 All units and individuals engaged in the sales of goods, provision of processing,repairs and replac ement services, and the importation of goods within the territory of the People“s Republic of China are taxpayers of Value-Added Tax (heteinafter referred to as "taxpayers“),and shall pay VAT in acco rdance with these Regulations.第二条增值税税率:Article 2 VAT rates:(一)纳税人销售或者进口货物,除本条第(二)项、第(三)项规定外,税率为17%。

(1)For taxpayers selling or importing goods,other than those stipulated in items (2)and (3)of this Article,the tax rate shall be 17%.(二)纳税人销售或者进口下列货物,税率为13%:(2)For taxpayers selling or importing the following goods,the tax rate shall be 13%:1.粮食、食用植物油;i。

德国vat系列问题汇总---欧洲税务

什么情况下我们需要申请德国VAT。

1:远程销售,如果货物从欧盟境内的非德国仓库发到德国终端消费者,如果销售额在一个自然年内(1.1-12.31)低于10万欧,那么不需要申请德国VAT。

(如果你卖的是含消费税的产品,比如香烟,酒之类的产品,那么不管你销售多少金额,都需要注册德国VAT)。

【如果说你等到销售额达到10万欧元再去注册的话,我认为注册成功的概率很小(已经有人被拒,税务局也没给原因),如果你要在德国做大做强,建议提早注册,防止账号做起来了再去申请VAT被拒】。

2:如果是德国FBA仓库或者是德国第三方海外仓库发货,换句话说,如果你的货物是从德国本土发给终端消费者,那么不管你的销售额是多少,都需要注册德国VAT并交税。

(很多人说,德国FBA发货,德国税务局也看不出后台我到底是把货放在德国还是英国FBA仓库。

这个是可以知晓的,从前台listing页面,如果放在德国fba,那么第二天就可以收到,如果放在英国FBA仓库,可能需要2-3天的运输时间)。

在申请德国VAT的时候,还有一个叫欧盟通用税号VAT ID【德语是Umsatzsteuer Identifikationsnummer (USt-IdNr)】,如果你卖货给法国,西班牙这样国家的终端消费者,限额达到当地规定(法国和西班牙是3.5W EUR)就不能再卖了。

但如果你是批发给当地过的经销商(B类客户),那么就需要这个USt-IdNr了,有了他,代表你这批货物是不含税的。

而目的国的B类经销商需要自己开发票给当地终端消费者。

有人说注册德国VAT后有了欧盟通用税号后可以通用欧盟的说法是错误的。

3:如果你的欧洲站一不小心被封,那么申诉的时候是需要提供VAT号码的(虽然是可选,但是如果你能提供,必然会增加成功的几率)。

4:如果你已经在运营德国站,相信绝大多数德国客人都会要求开具VAT Invocie(增值税专用发票),如果没有VAT账号,你怎么开给客人?OK,了解了以上知识,我们就知道自己是否需要申请VAT。

欧盟地区主要国家的税制简介

各类税收收入占全国税收收入总额的比重依次为:社会保障税占38.8%,所得、利润、资本收益税占31%,国内货物与劳务税占28.1%,财产税占2.1%。

德国是以直接税为主的国家,在德国1991年税收收入中,直接税占71.9%,间接税占28.1%。

1995年,公司承担无限纳税义务的,其正常税率为45%,对分配利润的税率降为30%。

从1995年开始就德国公司收到股息所发生的归集税收抵免作扣除后的核定公司税额征收7.5%的附加税。

德国在州一级不征收所得税。

但地方当局要基于所使用的财产和营业所得征收营业税,各地确定本地适用的税率。

营业税可以从应纳税所得额中扣除。

个人所得税是对单身1.2095万马克或已婚夫妇2.419马克以上的所得征收的,采用10级累进税率,最高边际税率达53%。

此外还要就核定的税额缴纳7.5%的附加税。

德国增值税的标准税率为15%,对适用于食品、书籍等的低税率为7%。

财产税适用于个人的税率通常为1%,适用于公司营业资产和股权的税率为0.5%,适用于公司的税率为0.6%。

对土地的财产税按单价的140%征收。

联邦政府和所有16个州政府都提供各种财政鼓励以促进私人投资。

鼓励措施包括给予直接补贴和作为折旧备抵的税收抵免。

这些优惠既限定行业,也限定地区。

德国对国外所得的有关税收实行免税、扣除或抵免等优惠。

三、意大利意大利属于高收入国家,1992年意大利国内生产总值(CDP)为1641.1万亿里拉,全国税收收入总额为630.952万亿里拉,中央税收收入占GDP的38.4%,省级税收收入占GDP的1.3%。

意大利现行的主要税种有:公司所得税、个人所得税、增值税、遗产与赠与税、土地财产税、登记税、不动产税、社会保障税、营业资产税、财产收益税、公司特权税、印花税等税种。

据国际货币基金组织的分类综合统计,意大利地方级税收在GDP中的比重很小,1989年仅占GDP的1.3%,中央和地方的非税收入也很小,只占GDP的1%左右。

增值税外文翻译

中文3837字Value added taxFrom Wikipedia,the free encyclopediAbstractA value added tax(V AT)is a form of consumption tax.It is a tax on the”value added”to a product or material,from an accounting view, at each stage of its manufacture or distribution.The”value added”to a product by a business is the sale price charged to its customer,minus the cost of materials and other taxable inputs.A V AT is like a sales tax in that ultimately only the end consumer is taxed.It differs from the sales tax in that,with the latter,the tax is collected and remitted to the government only once.at the point of purchase by the end consumer.With the V AT, collections,remittances to the government,and credits for taxes already paid occur each time a business in the supply chain purchases products from another business. The reason businesses end up paying no tax is that at the time they sell the product,they receive a credit for all the tax they have paid to suppliers.Personal end-consumers of products and services cannot recover V AT on purchases,but businesses are able to recover V AT(input tax)on the products and services that they buy in order to produce further goods or services that will be sold to yet another business in the supply chain or directly to a final consumer.In this way, the total tax levied at each stage in the economic chain of supply is a constant fraction of the value added by a business to its products,and most of the cost of collecting the tax is borne by business,rather than by the state.Value Added Taxes were introduced in part because they create stronger incentives to collect than a sales tax does.Both types of consumption tax create an incentive by end consumers to avoid or evade the tax.But the sales tax offers the buyer a mechanism to avoid or evade the tax--persuade the seller that he is not really an end consumer,and therefore the seller is not legally required to collect it.The burden of determining whether the buyer’S motivation is to consume or re-sell is on the seller.but the seller has no direct economic incentive to the seller to collect it.The V AT approach gives sellers a direct financial stake in collecting the tax,and eliminates the problematic decision by the seller about whether the buyer is or is not an end consumer.Chapter I Comparison with a sales taxValue added tax(V AT)avoids the cascade effect of sales tax by taxing only the value added at each stage of production.For this reason,throughout the world,V AT has been gaining favor over traditional sales taxes.In principle,V AT applies to all provisions of goods and services.V AT is assessed and collected on the value of goods or services that have been provided every time there is a transaction (sale/purchase). The seller charges V AT to the buyer, and the seller pays this V AT to the government.If however, the purchaser is not an end user,but the goods or services purchased are costs to its business, the tax it has paid for such purchases can be deducted from the tax it charges to its customers.The government only receives the difference;in other words,it is paid tax on the gross margin of each transaction,by each participant in the sales chain.Sales tax is normally charged on end users(consumers).The V AT mechanism means that the end—user tax is the same as it would be with a sales tax.The main difference is the extra accounting required by those in the middle of the supply chain;this disadvantage of V AT is balanced by application of the same tax to each member of the production chain regardless of its position in it and the position of its customers, reducing the effort required to check and certify their status.When the V AT system has few, if any, exemptions such as with GST in New Zealand,payment of V AT is even simpler.A general economic idea is that if sales taxes exceed 1 0%,people start engaging in widespread tax evading activity(1ike buying over the Internet,pretending to be a business,buying at wholesale,buying products through an employer etc. On the other hand.total V AT rates can rise above 1 0%without widespread evasion because of the novel collection mechanism.However,because of its particular mechanism of collection,V AT becomes quite easily the target of specific frauds like carousel fraud, which can be very expensive in terms of loss of tax incomes for states.1.1 Principle of V ATThe standard way to implement a V AT involves assuming a business owes some percentage on the price of the product minus all taxes previously paid on the good. If V AT rates were 10%,an orange juice maker would pay 10%of the£5 per litre price (£0.50)minus taxes previously paid by the orange farmer(maybe£0.20).In this example,the orange juice maker would have a £0.30 tax liability. Each business has a strong incentive for its suppliers to pay their taxes,allowing V AT rates to be higherwith less tax evasion than a retail sales tax.Behind this simple principle are the variations in its implementations,as discussed in the next section.1.2 Basis for V ATsBy the method of collection. V AT can be accounts-based or invoice-based. Under the invoice method of collection, each seller charges V AT rate on his output and passes the buyer a special invoice that indicates the amount of tax charged. Buyers who are subject to V AT on their own sales(output tax),consider the tax on the purchase invoices as input tax and can deduct the sum from their own V AT liability. The difference between output tax and input tax is paid to the government (or a refund is claimed,in the case of negative liability). Under the accounts based method,no such specific invoices are used.Instead,the tax is calculated on the value added, measured as a difference between revenues and allowable purchases. Most countries today use the invoice method, the only exception being Japan, which uses the accounts method.Chapter II CriticismsThe “value-added tax” has been criticized as the burden of it relies on personal end-consumers of products. Some critics consider it to be a regressive tax, meaning the poor pay more, as a percentage of their income, than the rich. Defenders argue that excising taxation through income is an arbitrary standard,and that the value-added tax is in fact a proportional tax in that people with higher income pay more at the same rate that they consume more. The effective progressiveness or regressiveness of a V AT system can also be affected when different classes of goods are taxed at different rates. To maintain the progressive nature of total taxes on individuals, countries implementing V AT have reduced income tax on lower income-earners, as well as instituted direct transfer payments to lower-income groups, resulting in lower tax burdens on the poor.Revenues from a value added tax are frequently lower than expected because they are difficult and costly to administer and collect.In many countries, however, where collection of personal income taxes and corporate profit taxes has been historically weak, V AT collection has been more successful than other types of taxes. V AT has become more important in many jurisdictions as tariff levels have fallen worldwide due to trade liberalization. as V AT has essentially replaced lost tariff revenues. Whether the costs and distortions of value added taxes are lower than the economic inefficiencies and enforcement issues (e.g. smuggling) from high import tariffs is debated, but theory suggests value added taxes are far more efficient.Certain industries(small.scale services,for example)tend to have more V AT avoidance, particularly where cash transactions predominate,and V AT may be criticized for encouraging this. From the perspective of government, however, V AT may be preferable because it captures at least some of the value-added, For example, a carpenter may offer to provide services for cash (i.e. without a receipt, and without V AT)to a homeowner, who usually cannot claim input V AT back. The homeowner will hence bear lower costs and the carpenter may be able to avoid other taxes (profit or payroll taxes). The government, however, may still receive V AT for various other inputs(1umber, paint, gasoline, tools, etc.) sold to the carpenter,who would be unable to reclaim the V AT on these inputs (unless of course the carpenter also has at 1east some jobs done with receipt, and claims all purchased inputs to go to those jobs). While the total tax receipts may be lower compared to full compliance, it may not be lower than under other feasible taxation systems.Chapter III V AT systems3.1 European UnionThe European Union Value Added Tax(EU V AT)is a value added tax encompassing member states in the European Union Value Added Tax Area. Joining in this is compulsory for member states of the European Union. As a consumption tax, the EU V AT taxes the consumption of goods and services in the EU V AT area. The EU V AT’s key issue asks where the supply and consumption occurs thereby determining which member state will collect the V AT and which V AT rate will be charged.Each Member State’s national V AT legislation must comply with the provisions 0f EU V AT law as set out in Directive 2006/112/EC. This Directive sets out the basic framework for EU V AT, but does allow Member States some degree of flexibility in implementation of V AT legislation. For example different rates of V AT are allowed in different EU member states. However Directive 2006/112requires Member states to have a minimum standard rate of V AT of 15%and one or two reduced rates not to be below 5%. Some Member States have a 0%V AT rate on certain supplies-these Member States would have agreed this as part of their EU Accession Treaty(for example, newspapers and certain magazines in Belgium). The current maximum rate in operation in the EU is 25%, though member states are free to set higher rates.V AT that is charged by a business and paid by its customers is known as ”output V AT” (that is,V AT on its output supplies). V AT that is paid by a business to other businesses on the supplies that it receives is known as ”input V AT”(that is, V AT on its input supplies). A business is generally able to recover input V AT to the extent that the input V AT is attributable to(that is, used to make)its taxable outputs. Input V AT is recovered by setting it against the output V AT for which the business is required to account to the government, or, if there is an excess, by claiming a repayment from the government.The V AT Directive (prior to 1 January 2007 referred to as the Sixth V AT Directive) requires certain goods and services to be exempt from V AT (for example, postal services, medical care, lending, insurance, betting), and certain other goods and services to be exempt from V AT but subject to the ability of an EU member state to opt to charge V AT on those supplies (such as land and certain financial services). Input V AT that is attributable to exempt supplies is not recoverable,although a business Can increase its prices SO the customer effectively bears the cost of the ’sticking’ V AT (the effective rate will be lower than the headline rate and dependon the balance between previously taxed input and labor at the exempt stage).3.2 The Nordic countriesIn Denmark,V AT is generally applied at one rate, and with few exceptions is not split into two or more rates as in other countries (e.g. Germany), where reduced rates apply to essential goods such as foodstuffs.The current standard rate of V AT in Denmark is 25%. That makes Denmark one of the countries with the highest value added tax, alongside Norway and Sweden. A number of services has reduced V AT, for instance public transportation of private persons, health care services, publishing newspapers, rent of premises (the lessor can, though, voluntarily register as V AT payer, except for residential premises), and travel agency operations.In Finland,the standard rate of V AT is 23%, along with all other V AT rates, excluding the zero rate. In addition,two reduced rates are in use:12%(reduced in October 2009 from 17% for non-restaurant food, from July 2010 will encompass restaurant food also), which is applied on food and animal feed, and 8%, which is applied on passenger transportation services, cinema performances, physical exercise services, books, pharmaceuticals, entrance fees to commercial cultural and entertainment events and facilities. Supplies of some goods and services are exempt under the conditions defined in the Finnish V AT Act: hospital and medical care; social welfare services; educational. financial and insurance services; lotteries and money games; transactions concerning bank notes and coins used as legal tender; real property including building land; certain transactions carried out by blind persons and interpretation services for deaf persons. The seller of these tax-exempt services or goods is not subject to V AT and does not pay tax on sales. Such sellers therefore may not deduct V AT included in the purchase prices of his inputs.In Sweden, V AT is split into three levels; 25% for most goods and services including restaurants bills, 12% for foods (incl. bring home from restaurants) and hotel stays (but breakfast at 25%) and 6% for printed matter, cultural services, and transport of private persons. Some services are not taxable for example education of children and adults if public utility, and health and dental care, but education is taxable at 25% in case of courses for adults at a private school. Dance events (for the guests) have 25%, concerts and stage shows have 6%, and some types of cultural events have 0%.-References:∙(Icelandic)"Lög nr. 50/1988 um virðisaukaskatt". 1988. Archived from the original on 2007-10-09./web/20071009093025/http://rsk.is/skattalagasafn/virdisaukaskattur/log/log_0501988.htm. Retrieved 2007-09-05.∙ Ahmed. Ehtisham and Nicholas Stern. 1991. The Theory and Practice of Tax Reform in Developing Countries (Cambridge University Press).∙ Bird, Richard M. and P.-P. Gendron .1998. “Dual VATs and Cross-border Trade: Two Problems, One Solution?” International Tax and Public Finance, 5: 429-42.∙ Bird, Richard M. and P.-P. Gendron .2000. “CVAT, VIVAT and Dual VAT; Vertical ‘Sharing’ and Interstate Trade,” International Tax and Pu blic Finance, 7: 753-61.∙Keen, Michael and S. Smith .2000. “Viva VIVAT!” International Tax and Public Finance, 7: 741-51.∙ Keen, Michael and S. Smith .1996. "The Future of Value-added Tax in the European Union," Economic Policy, 23: 375-411.∙ McLure, Charles E. (1993) "The Brazilian Tax Assignment Problem: Ends, Means, and Constraints," in A Reforma Fiscal no Brasil (São Paulo: Fundaçäo Instituto de Pesquisas Econômicas).∙McLure, Charles E. 2000. “Implementing Subnational VATs on Internal Trad e: The Compensating VAT (CVAT),” International Tax and Public Finance, 7: 723-40.∙ Muller, Nichole. 2007. Indisches Recht mit Schwerpunkt auf gewerblichem Rechtsschutz im Rahmen eines Projektgeschäfts in Indien, IBL Review, VOL. 12, Institute of International Business and law, Germany. Law-and-business.de∙ Muller, Nichole. 2007. Indian law with emphasis on commercial legal insurance within the scope of a project business in India. IBL Review, VOL. 12, Institute of International Business and law, Germany.∙ MOMS, Politikens Nudansk Leksikon 2002, ISBN 87-604-1578-9∙ Andhra Pradesh Value Added Tax Act, 2005, Andhra Pradesh Gazette Extraordinary, 25 March 2005, retrieved on 16 March 2007.∙ OECD. 2008. Consumption Tax Trends 2008: VAT/GST and Excise Rates, Trends and Administration Issues. Paris:OECD.∙Serra, J. and J. Afonso. 1999. “Fiscal Federalism Brazilian Style: Some Reflections,” Paper present ed to Forum of Federations, Mont Tremblant, Canada, October 1999.增值税From Wikipedia,the free encyclopedi摘要增值税(V AT)是消费税的一种形式。

营业税改征增值税中英文对照外文翻译文献

营业税改征增值税中英文对照外文翻译文献(文档含英文原文和中文翻译)营业税改征增值税试点方案的进一步扩围2012年7月25日国务院总理温家宝主持召开国务院常务会议正式决定,自2012年8月1日起至年底,将自2012年1月1日起已在上海进行的交通运输业和部分现代服务业营业税改征增值税试点方案("试点方案")范围,分批扩大至其他10个省市:北京、天津、江苏、浙江、安徽、福建、湖北、广东、厦门和深圳("10个新试点地区")。

不仅如此,会议还决定,明年继续扩大试点地区,并选择部分行业作全国试点。

在本期《中国税务/商务新知》中,我们将分析试点方案进一步扩围至10个新试点地区后带来的潜在影响,并分享我们的观察。

普华永道观察根据公开统计信息,2012年上半年10个新试点地区的生产地区的生产总值超过50%。

地理上,这10个新试点地区各广布在中国北部、中部、东部和南部地区。

因此,试点方案的进一步扩围无疑会对中国下半年的宏观经济发展产生很大影响。

总体而言,10个新试点地区的试点方案应与上海的试点方案一直。

自2012年1月1日上海开展试点方案以来,财政部和国家税务总局出台了一系列关于试点方案的政策和实施细则。

理论上来说,除非将来有专门针对10个新地区的不同政策出台,这些已出台的政策文件应该适用于所有试点地区。

在10个新试点地区开展试点方案可能要面临更为复杂的问题。

与上海国税合一的情形不同,这些地区的国税局和地税局各自管理,分别负责增值税和营业税的征管。

这样可能出现各方对试点服务范围有不同的理解,尤其是对那些未在现有规定中有清楚定义的试点服务。

这可能对这些新试点地区的纳税人带来更大的挑战,特别是在营业税改增值税的过渡时期。

同时,我们也期待上海试点中遇到的实际问题能够进一步予以明确。

例如,进一步明确某些在现行办法和法规中没有明确定义的试点服务的范围,特别是认定某项咨询服务是否属于试点服务的范围,从而向境外方提供上述咨询服务时能够享受免增值税的处理;如何具体实施对符合条件的试点企业出口实行免抵退税方法等问题以及如何将这10个新试点地区的基础实际操作与上海保持一致。

欧盟保险业增值税处理及对我国的启示

欧盟保险业增值税处理及对我国的启示作者:殷佳楠来源:《大陆桥视野·经济瞭望》 2021年第3期文 / 殷佳楠摘要:是否对保险业征税以及如何征税,是增值税法律设计中最经典也最困难的问题之一。

世界上大部分国家、地区对保险业实行免征增值税政策,其中以欧盟为典型。

由于欧盟《增值税指令》中对保险业的豁免条款过于笼统,一项服务是否属于保险交易经常存在各种争议。

欧洲法院通过判例法对该条款进行补充解释,逐步阐明保险交易的定义,很大程度上明确了保险业的免征增值税范围。

借鉴欧盟保险业增值税的处理经验,可以为我国金融业增值税改革提供参考。

关键词:保险业;增值税;欧盟一、欧盟对保险业增值税的处理在欧洲增值税中,对保险业实行免税政策。

根据欧盟2006年《增值税指令》(Directive 2006/112/EC)第135条第1款a项规定,成员国的以下交易免税:保险和再保险交易,包括由保险经纪人和保险代理人提供的相关服务。

但该豁免条款在解释上存在一定问题,导致一项交易是否应被视为“保险或再保险交易”或“由保险经纪人和保险代理人提供的相关服务”成为欧盟法院审理的众多法律纠纷的理由。

在这种情况下,欧洲法院通过判例法对该豁免条款进行补充解释,很大程度上阐明了保险和再保险交易的免征增值税范围,包括保险经纪人和保险代理人提供的相关服务,有利于欧盟保险业增值税的发展。

(一)保险和再保险交易1.未经授权从事保险交易的保险人提供的服务。

CPP案是法院对保险交易进行定义的第一个案例,并为《增值税指令》第135条第1款a项所确立概念的未来发展制定了框架。

法院认为,一般来说,保险交易为保险人承诺,在承保的风险实现时,向被保险人提供订立合同时约定的服务,作为事先支付保险费的回报。

英国上议院在CPP案中提出的问题是基于一家向消费者提供“信用卡保护计划”的有限合伙企业与英国税务机关之间的纠纷。

该计划包括合伙企业向信用卡持有人提供的一系列服务。

BS-标准-与-BS-EN-标准-区别

BS 标准与BS EN 标准区别EN的欧盟标准,这是对的。

BS是英国标准组织BSI制定的标准。

但因为英国是欧盟成员国,故经常直接拿欧盟的标准转化(等同采用)为自己的标准。

采标大致有三种情况,通俗的说:1. 等同,一模一样,完全一致;2. 等效,各自表述,殊途同归;3. 非等效,指标相同或类似,但要求不同。

BS EN 或DIN EN 都完全=EN。

都不是自己制定的,直接拿来的。

拿EN的,就叫BS EN,拿ISO的,就叫BSISO。

拿IEC的,就叫BS IEC。

如果隔了一层,也不是EN自己制定的,是EN拿ISO或IEC的(EN ISO 和ENIEC),就叫BS EN ISO和BS EN IEC。

这时,BS EN ISO完全=ISO。

早期的BS EN属于内容完全一致,但形式上会转化为自己的风格。

但近年来可能是知识产权意识提高了,只是加个封皮和说明,后面的内容就都遵照EN的风格了(DIN比较牛,还是将人家的东西转化为自己的格式,不过不会花功夫翻译成德文的)。

BS ENISO也一样,翻过前几页,后面就都是EN或ISO 的内容了。

由于通常见到的EN标准都是英文的(注1),因此BSEN和EN不存在误读。

不像部分GB,虽然等同采标EN、ISO、IEC,但中文翻译是仁者见仁智者见智,会有分歧的。

因此使用他人翻译的东西,不妨存点疑问,如果能溯源原版外文标准最佳。

由于欧盟成员众多,一般EN都可能有多语种版本。

就像IEC的标准,通常都是英/法文对照的。

这些版本中,法文是最严谨的。

但受限于国人的能力,我们通常见到的都是英文版。

由于EN数据库难度大,现在各论坛流通的都是BSEN版本。

法国增值税号码SIREN还是SIRET

法国增值税号码:SIREN还是SIRET?

法国税务机关向注册企业发放不同的税号。

每一个数字都有不同的含义和格式:

SIREN 数量

SIREN 编号由统计机构(INSEE)发布。

它由9个数字组成。

前8个数字没有任何意义,第9位仅用于对前8个数字的对数进行双重检查。

SIRET数量

SIRET 编号由14 个号码组成。

前9 位数字是SIREN 号码,接下来的5 位数字是NIC 号码( Numéro Interne de Classement )。

SIRET 编号提供有关企业在法国的位置信息(适用于已建立的公司)。

在欧盟增值税号码必须用于所有共同体内部的运动。

它由法国“ FR ”的首字母缩写词组成,后跟两位数字以仔细检查对数和您的SIREN 号码的9 位数字

将您的SIRET号码转换为您的增值税号码

该工具将自动将您的SIRET id转换为增值税号码。

输入您的SIRET并点击转换。

14339952_国外增值税与国内增值税的比较

L i a o n i n gE c o n o my国外增值税与国内增值税的比较〔内容提要〕本文通过对部分欧洲国家、亚洲国家增值税的简要介绍,比较分析我国的增值税制度,从中借鉴经验,以期完善我国的增值税制度。

〔关键词〕增值税流转税税率!姜昕刘彦廷增值税是指以商品生产、流通和提供劳务的各个环节的增值额作为课税对象的一种流转税。

自"#$%年提出这个概念以来,现已有"&&多个国家和地区陆续开始征收这项税款。

“道道征税,税不重征”是增值税最显著的特征,这体现了税收公平的特质,因而能够提升纳税人的纳税积极性,促进社会经济的发展。

一、欧洲国家的增值税制度"'法国的增值税制度。

增值税最早于"#$%年产生于法国。

起初,法国征收增值税的范围只包括工业生产与商品批发这两个部分,到(&世纪)&年代中期,法国将农业、商品零售业纳入到收取增值税的范畴,在("世纪的今天,法国境内的有偿活动都要缴纳增值税。

法国对于增值税采取多档税率的纳税方案:标准税率"#')*,低税率$'$*和('"*以及零税率。

低税率$'$*主要针对日常生活中所需要的食物、饮品、客运、书籍等;低税率('"*主要针对报刊、药物、音乐演出等。

法国对外出口的货物或进口后用于出口的货物以及对外的劳务输出不需要缴纳税款。

这类商品所需进行的各个环节都免除增值税,同时本环节不需要缴纳增值税。

可免除税款的项目有:部分农产品、某些特定商品的交易、有价证券的交易、报纸杂志类、保险类的交易等。

('英国的增值税制度。

(&世纪+&年代初,英国就制定了增值税征收的制度法案,随后开始征收增值税。

"#,-年英国制定了《增值税法》,确保了增值税的合法征收。

增值税纳税人是涉及货品交易和劳务交易的企业负责人。

欧盟经济的税收政策与税收竞争

欧盟经济的税收政策与税收竞争在全球化的背景下,税收政策对一个地区的经济发展起着至关重要的作用。

欧洲联盟(European Union,简称EU)作为一个经济合作和政治一体化的组织,其税收政策也备受关注。

本文将会探讨欧盟经济的税收政策以及因税收竞争而带来的影响。

1. 欧盟税收政策的概述欧盟的税收政策由各成员国根据欧盟范围内的政策框架来制定。

由于欧盟成员国之间的税收制度和税率存在差异,因此存在着潜在的税收竞争现象。

欧盟通过一系列的税收法规来协调成员国之间的税收政策,以保障公平和竞争的原则。

2. 欧盟税收政策的目标欧盟税收政策的主要目标之一是促进内部市场的发展和经济增长。

为了实现这一目标,欧盟采取了一系列措施,如降低跨境交易的税收障碍,减少成本和增加效率。

同时,欧盟税收政策也致力于支持可持续发展、促进社会公正和保护环境。

3. 欧盟税收竞争的现状及影响由于欧盟成员国之间的税收制度差异较大,存在着潜在的税收竞争。

一些欧盟成员国借助税收政策来吸引外国投资和人才流动,以增加自己的竞争力。

然而,这种税收竞争也可能导致一些问题,比如税基侵蚀和利润转移,以及财政收入的减少。

4. 欧盟税收合作的措施与挑战为了减少税收竞争的负面影响,欧盟推出了一系列税收合作措施。

其中最重要的是欧盟利润转移和税基侵蚀行动计划(Anti-Tax Avoidance Directive,简称ATAD)。

这一计划旨在限制利润转移到低税率国家,并加强对税基侵蚀行为的打击。

然而,由于各成员国之间的利益冲突和政策差异,税收合作也面临着一些挑战。

5. 欧盟税收政策对全球经济的影响欧盟作为世界上最大的经济体之一,其税收政策的变化对全球经济产生重大影响。

欧盟税收政策的调整和改革可能会吸引更多的投资和贸易活动,也可能对全球供应链和金融市场造成波动。

因此,全球其他国家和地区应密切关注欧盟的税收政策动向,以及其对全球经济的影响。

总结:欧盟经济的税收政策与税收竞争是一个复杂而多样的议题。

国外关于软件产品增值税政策

国外关于软件产品增值税政策1. 介绍软件产品增值税政策是指国外针对软件产品销售和服务提供的增值税相关规定。

随着信息技术的发展,软件产业在全球范围内得到了迅猛发展,各国纷纷制定相关政策来规范和管理软件产品的销售和服务。

本文将重点介绍一些主要国家(美国、欧洲、日本)在软件产品增值税方面的政策,并对其进行比较分析。

2. 美国的软件产品增值税政策美国目前没有统一的联邦级别的增值税制度,但各州可以自行决定是否征收销售和使用税。

对于软件产品,根据美国国内收入法典第26章第61节中所定义的“智力财产权”(Intellectual Property),以及“数字商品”(Digital Goods)和“数字服务”(Digital Services)等概念,可以确定其应纳税种类和税率。

具体来说,如果软件产品被视为实体商品,则根据当地州的销售和使用税法规征收相应税款。

例如,在纽约州购买实体媒体上的软件盒子时,可能需要支付8.875%的销售税。

而如果软件产品被视为数字商品或数字服务,则根据各州的数字商品和服务税法规征收相应税款。

例如,在佛罗里达州购买在线订阅的软件服务时,可能需要支付6%的数字服务税。

需要注意的是,美国各州对软件产品增值税政策的具体规定可能有所不同,因此在销售和购买软件产品时,需要了解当地州的相关法规。

3. 欧洲的软件产品增值税政策欧洲国家在软件产品增值税方面采取了统一的政策,即根据欧盟增值税指令(VAT Directive)来征收增值税。

根据该指令,欧洲国家将软件产品分为两类:有形媒体上提供的软件和通过下载或流媒体方式提供的软件。

对于有形媒体上提供的软件,例如光盘或DVD上的安装程序,征收标准增值税率。

不同欧洲国家的标准增值税率略有差异,例如德国为19%,英国为20%。

对于通过下载或流媒体方式提供的软件,根据购买者所在地区(消费者所属国)来确定适用的增值税率。

这种方式被称为“电子增值税(eVAT)”或“远程销售增值税(RST)”。

外文翻译--显示性比较优势与竞争力:以土耳其对欧盟为例

本科毕业论文外文翻译外文题目:Revealed Comparative Advantage and Competitiveness: A Case Study for Turkey towards the EU出处:Journal of Economic & Social Research作者:Vildan Serin & Abdulkadir Civan译文:显示性比较优势与竞争力:以土耳其对欧盟为例Vildan Serin & Abdulkadir Civan摘要本文旨在量化土耳其有比较优势的番茄,橄榄油和果汁行业,在1995年-2005年期间在欧盟市场上的竞争力变化。

为了研究土耳其的竞争力和进度,使用两个被广泛使用的指标:显示性比较优势(RCA)和相对出口(CEP)。

此外,估计在欧盟竞争对手国家的进口需求函数。

利用回归分析,我们假设,如果土耳其是这些国家的竞争对手,那么其产品价格将会在出口需求函数上有显著的影响效果。

这两个指数和回归结果表明,土耳其的果汁和橄榄油已经在欧盟市场有非常惊人的高竞争优势,但是番茄则不是。

1.引言1995年,土耳其与欧盟签署的关税同盟协议是关于工业和农产加工品方面的,已经在1996年1月实施。

然而,关税同盟不涉及许多关键领域,如在双边贸易中优惠适用的传统农业。

关于农产加工品,双方已经商定在欧洲共同体建立一个适用于土耳其区分农业和工业部件之间类似方法的体系(Yörük,2005年),这样,土耳其的关税和从欧盟进口工业产品所征收的各种税费被取消。

土耳其也开始应用从第三方国家进口欧盟的共同对外关税。

土耳其的平均保护水平已经从10.9%降低至5%。

(Bekmez和Genç,2002年)另一种将被列入CU的商品标准是产品的原产地。

该协会协议规定“协会也应扩大到农业和农产品贸易,按照规则,特别应考虑欧盟共同体共同农业政策”。

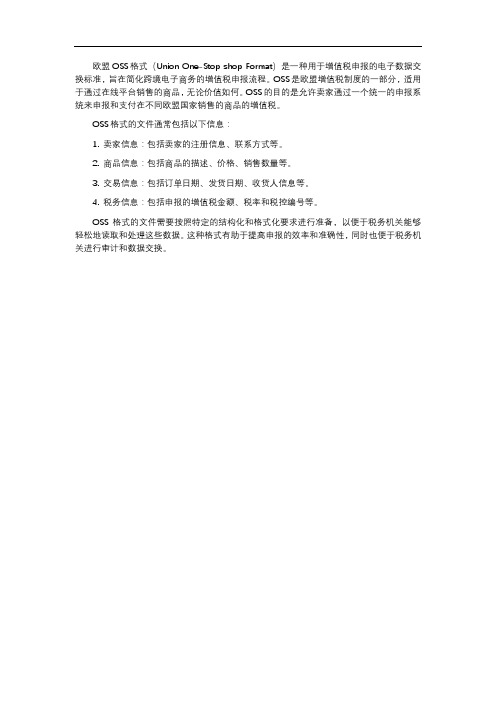

欧盟oss格式

欧盟OSS格式(Union One-Stop shop Format)是一种用于增值税申报的电子数据交换标准,旨在简化跨境电子商务的增值税申报流程。

OSS是欧盟增值税制度的一部分,适用于通过在线平台销售的商品,无论价值如何。

OSS的目的是允许卖家通过一个统一的申报系统来申报和支付在不同欧盟国家销售的商品的增值税。

OSS格式的文件通常包括以下信息:

1. 卖家信息:包括卖家的注册信息、联系方式等。

2. 商品信息:包括商品的描述、价格、销售数量等。

3. 交易信息:包括订单日期、发货日期、收货人信息等。

4. 税务信息:包括申报的增值税金额、税率和税控编号等。

OSS格式的文件需要按照特定的结构化和格式化要求进行准备,以便于税务机关能够轻松地读取和处理这些数据。

这种格式有助于提高申报的效率和准确性,同时也便于税务机关进行审计和数据交换。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

毕业设计/论文外文文献翻译院系经济管理学院专业班级会计1202班姓名原文出处Bruce. V AT Between EU Member States[J].Int-ernational Tax and Public Finance.2013,(6).评分指导教师2016年3 月1 日欧盟成员国的增值税布鲁斯.欧盟成员国的增值税[J].国际税收与公共财政.2013,(6).本文结合了法律、经济等方面的知识对增值税(V AT)的征收过程中存在的问题进行了分析。

其主要目的是提供全面的教学工具、法律、案例和分析演习,并通过对世界各国的税务专家和学者的研究分析得出的启发,为未来应对的增值税问题提供借鉴意义。

通过本文的比较介绍,提供了一个分析有关税收结构和税收基础的政策问题,以及深入了解为何产生增值税纠纷,从而使增值税纠纷得到解决。

作者扩大了覆盖范围,包括在欧洲,亚洲,非洲和澳大利亚,介绍了这些国家新增值税的相关发展。

最后用一章对生活服务业进行了补充和案例分析。

增值税作为政府收入的主要来源正在被130 多个国家所使用。

增值税是一个具有普遍性和基础性的消费税,它增加了商品和服务的价值评估。

增值税是在生产的每一个阶段普遍征收的附加值,它也是一个让卖方为买方支付己购买的商品和服务的税款(进项税额)的一中税收信贷机制(销项税额)。

一般而言,增值税有以下几层含义:一个普通税适用于所有涉及生产和销售商品以及提供服务的商业活动;消费税最终由消费者承担;是间接征收消费的商品或服务价格的一部分;在每个阶段的生产和分配阶段间接税可见多级税收征收消费的商品或服务价格;一个小幅收税款,已被控在其所有的采购系统,它采用的是由卖方收取了相应的信贷索赔其所有销售的增值税或增值税的部分付款。

增值税纳税义务的计算方法有三种:信贷发票的计算方法是—加减法,还有另外的两种方法,但是仅仅只有信用发票的计算方法是相对使用广泛的。

信贷发票的方法突出了增值税的定义功能:使用销项税(销售缴纳的税款)和进项税(采购缴纳的税款)一般纳税人收取的增值税应税销售额和采购所支付的应税进项税额之间的差额作为计算其增值税纳税义务。

因此这种方法需要使用发票,分别列出所有应税销售额的增值税部分。

从而销售货物的一方为买方提供购货发票。

销售发票显示的是收取的销项税额,则购货发票显示的就是支付的进项税额。

最后,纳税人通过使用增值税发票抵免的计算方法来计算需汇到税务机关的增值税额。

方法如下:销售发票中的增值税(销项税额)减去购货发票所示的增值税(进项税额),减去进项税额后的余额汇给税务机关;如果进项税大于了销项税一般需退款。

美国是唯一一个作为经济合作与发展组织的成员不征收增值税的国家,然而,增值税已经成为联邦税收改革辩论争议的重要对象。

间接税如增值税产生的税收收入是许多国家的重要税收部分。

在实践中,增值税制度产生全球四分之一的税收收入。

近130个国家现在有一个增值税制度(包括过去10年中已经采用该系统的70个国家)(肯尼和明茨2004年)。

更多专注于国际流动性税基,备受外界关注更多的是税负、间接税、消费税或增值税制度,少缴纳企业所得税,特别是资本所得(戈登和尼尔森1997年)。

在欧盟统一增值税期间,间接税和增值税制度的协调受到重视(费尔等人,1995年)。

一项涵盖所有私人物品和服务的增值税法律都是现行欧盟制度的特点,但仍有许多豁免,这一普遍的指令,在2001年挪威的增值税改革也同样存在。

改革引入了服务增值税一般法,但许多豁免仍然特别存在着。

相比于不完善的、不均匀的系统更多的支持一般的、统一的增值税系统。

这样的系统可以提高经济效率,降低行政成本,寻租和欺诈活动的行业,低利率和零评级大堂(肯尼和史密斯2006)。

一般的、统一的增值税系统相当于一个统一的消费税的所有商品和服务。

这样的系统也意味着,生产者的物质投入净增值税税率为零,不论速度结构。

根据生产效率定理(德蒙和米尔利斯)。

一个增值税制度与豁免是不遵守生产效率定理,因为中间的税收将产业之间的差异,这是最佳的。

在另一方面,它覆盖了增值税制度,但有较低的利率,对他们的销售零的评级行业的青睐,它们可以在全速率撤销支出增值税中间体,只减少销售率或为销售率零。

一个一般的和统一的增值税制度也可能正面影响家庭福利的分配。

如果初始情况的特点是在大部分商品和少数服务征收增值税的税率不同,福利分配就相对较小,因此实行对所有商品和服务的统一税率可能会提高福利,因为服务消费随收入的分配提高福利分配。

热衷缺乏价值利益点(肯尼2007年)从理论的角度出发讨论了这一观点,尽管在实际的税收政策以及增值税的普及增加了税收。

正如上面所提到的,增值税系统一般不统一。

理论分析要求相对简单的模型和简单的税制结构分析的实际政策,经济和税收制度的结构是非常复杂的,需要有一个详细的数值模型,以分析不同增值税的影响系统。

本文主要分析了不完善和不均匀增值税系统的福利效应,通过分析和比较不同的不完善,不均匀增值税系统,做出了一个统一的以增值税体系为基础的动态和可计算的一般小型开放型经济均衡模型(CGE)。

该模型反映了实体经济在许多方面有所不同,从更简单的理论模型,满足规范税收理论的假设,并建议统一商品税,以便减少税务。

在我们的分析中,我们提出了下面的问题。

不完善的增值税制度可以导致经济发展更加糟糕,纳税对象是服务行为的增值税体系还不如纳税对象仅仅只包括商品的增值税体系,这是为什么呢?2001年进行增值税改革的挪威和从1990年底开始增值税改革的欧盟都出现过这种情况。

将一个不完善的增值税体系扩展成一个统一的和一般的增值税体系,会带来很多福利,那么它的先决条件又是什么呢?美国对其进行了解释,不能纯粹依据理论来建立增值税制度系统,因为这样会存在税收楔子和扭曲市场经济。

基线增值税系统是一个非均匀增值税系统,它的增税对象主要包括商品。

这个基线增值税系统与2001年挪威增值税改革相比较,它的特点是统一了所有商品和服务,包括公共产品和服务的增值税税率。

2001年挪威的增值税改革迈出了一步,它的一般增值税系统包括许多服务,但仍有许多免税、零税率和较低的税率。

特别是增值税税率对食品和不含酒精的饮料的征税,其征税率是一般增值税率的一半。

本文对公开收入的中性政策改革、一次性转移的变化以及系统中特定的增值税率都进行了研究,从中得出系统特定的增值税率对收入没有影响变化,但对其家庭福利有所影响。

综上所述,研究增值税对企业税收影响的影响是一项非常系统的工程。

首先,要对该项工程的必要性与重要性有一个清晰认识;其次,要对该项工程的研究现状有一个全面分析;最后,要对该项工程的加强路径有一个科学把握。

只有这样,才能真正夯实该项工程的基础,增强该项工程的有效性与实效性。

V AT Between EU Member StatesBruce.V AT Between EU Member States[J].International Tax and PublicFinance.2013,(6).This paper integrates legal, economic, and administrative materials about value added tax. Its principal purpose is to provide comprehensive teaching tools-laws, cases, analytical exercises, and questions drawn from the experience of countries and organizations from all areas of the world. It also serves as a resource for tax practitioners and government officials that must grapple with issues under their V AT or their prospective V AT. The comparative presentation of this volume offers an analysis of policy issues relating to tax structure and tax base as well as insights into how cases arising out of V AT disputes have been resolved. The authors have expanded the coverage to include new V AT related developments in Europe, Asia, Africa and Australia. A chapter on life service industry has been added as well as an analysis of significant new cases.More than 130 countries use V AT as a key source of government revenue. V AT is a general, broad-based consumption tax assessed on the value added to goods and services. V AT is generally levied on value added at every stage of production, with a mechanism allowing the sellers a credit for the tax they have paid on their own purchases of goods and services (input tax) against the taxes collected on their sales of goods and service (output tax). Generally, V AT is: A general tax that applies to all commercial activities involving the production and distribution of goods and the provision of services; A consumption tax ultimately borne by the consumer; An indirect tax levied on the consumer as part of the price of goods or services; A multistage tax visibleateach stage of the production and distribution chain; and A fractionally collected tax that uses a system of partial payments whereby a seller charges V AT on all of its sales with a corresponding claim of credit for V AT that it has been charged on all of its purchases.There are three methods of calculating V AT liability: the credit-invoice method, the subtraction method, and the addition method. This column deals with only the credit-invoice method, which is the most widely used. The credit-invoice method highlights the V AT defining feature: the use of output tax (tax collected on sales) and input tax (tax paid on purchases). A taxpayer generally computes its V AT liability as the difference between the V ATcharged on taxable sales and the V AT paid on taxable purchases. This method requires the use of an invoice that separately lists the V AT component of all taxable sales. The sales invoice for the seller becomes the purchase invoice of the buyer. The sales invoice shows the output tax collected and the purchase invoice shows the input tax paid. To summarize, taxpayers use the credit-invoice method to calculate the amount of V AT to be remitted to the taxing authorities in the following manner: Aggregate the V AT shown in the sales invoices (output tax); Aggregate the V AT shown in the purchase invoices (input tax); Subtract the input tax from the output tax and remit any balance to the government; and In the event the input tax is greater than the output tax. The United States is the only member of the Organization of Economic Cooperation and Development that does not levy a V AT on a national level; however, V AT has become widely recognized as an important option in federal tax reform debates.Indirect taxes such as value added taxes generate a substantial part of tax revenue in many countries. In fact, V AT systems generate a quarter of the world’s tax revenue. Nearly 130 countries now have a V AT system (with over 70 countries having adopted the system during the last 10 years) (Keen and Mintz 2004). More focus on internationally mobile tax bases has drawn attention to directing more of the tax burden to indirect taxes such as consumption taxes or V AT systems, and less to income taxes, especially capital income (Gordon and Nielsen 1997). During the harmonization of EU taxes, indirect taxes, and V AT systems received much attention (Fehr etal. 1995). A general V AT law covering all private goods and services characterizes the current EU system, but there are still many exemptions from this general instruction.Such a V AT system also exists in Norway as a consequence of the Norwegian V AT reform in 2001. The reform introduced a general V AT law on services, but many exemptions are still specified.There are several arguments in favor of a general and uniform V AT system, compared with imperfect, nonuniform (and nongeneral) systems.Such a system may improve economic efficiency and reduce administration costs, rent-seeking and fraud activities by industries that lobby for lower rates and zero ratings (Keen and Smith 2006). A general and uniform V AT system equals a uniform consumer tax on all goods and services.Such a system also implies that the producers’ net V AT rate on material inputs equals zero, irrespective of the ratestructure. This is optimal according to the production efficiency theorem (Diamond and Mirrlees ).A V AT system with exemptions violates the production efficiency theorem because taxation of intermediates will differ between industries. On the other hand, industries that are covered by the V AT system but have lower rates or zero ratings on their sales are favored because they can withdraw expenditures to V AT on intermediates at full rates and only levy reduced or zero rates on their sales.A general and uniform V AT system may also have positive effects on the distribution of welfare among households. If the initial situation is characterized by a V AT on most goods but only on a few services, the introduction of a uniform rate on all goods and services may improve the distribution of welfare because services shareof consumption increases with income.Keen (2007) points to the lack of interest in value added taxation from the theoretical second-best literature in spite of the V AT’s popularity in practical tax policy. As mentioned above, V AT systems are in general not uniform. Theoretical analyses demand relatively simple models and simple tax structures to be analytically tractable.In practical policies, the structures of the economy and the tax systems are quite complex, and there is a need for detailed numerical models in order to analyze the effects of different V AT systems. This paper contributes to the literature by analyzing the welfare effects of an imperfect extension of a nonuniform V AT system, and comparing different imperfect, nonuniform V AT systems with a uniform and general V AT system within an empirically based dynamic computable general equilibrium (CGE) model for a small open economy. This model mirrors a real economy, Norway, and differs in many respects from the more simple theoretical models that fulfill the assumptions of normative tax theory and recommend uniform commodity taxes, combined with no input taxation.In our analyses, we ask the following questions. Can the introduction of a nonuniform V AT system including only some services make the economy worse off than having a V AT system only covering goods and in that case, why? Such reforms characterize both the Norwegian V AT reform of 2001 and the EU V AT reform from the late 1990-ties. Will an additional extension to a uniform and general V AT system be welfare superior to the nonuniform (and nongeneral) V AT systems and what are important preconditions? As will beexplained below, one cannot on purely theoretical grounds establish the welfare rankings of such V AT systems when there are preexisting distortions as tax wedges and market power in the economy. The baseline V AT system is a nonuniform V AT system mainly covering goods. This baseline V AT system is then compared with the extended nonuniform Norwegian V AT reform of 2001, and a general V AT system characterized by a uniform V AT rate on all goods and services, including public goods and services. The Norwegian V AT reform of 2001 was a step in the direction of a general V AT system by including many services, but there are still many exemptions, zero ratings and lower rates. In particular, the V AT rate on food and nonalcoholic beverages is half the general V AT rate. The policy reforms are made public revenue neutral, and changes in lump sum transfers as well as in the system specific V AT rate are studied. With a revenue-neutral change in the system-specific V AT rate, the V AT systems can be ranked with respect to welfare effects.When comparing the two different nonuniform V AT systems, our analysis shows that an imperfect extension of the V AT system to cover more services is welfare inferior to the baseline nonuniform V AT system only covering goods.In summary, influence of V AT tax on enterprises is a system engineering. First of all, it is necessary to have a clear understanding of the necessity and importance of the project; secondly, it is necessary to have a comprehensive analysis on the present situation of the project. Only in this way can we truly strengthen the foundation of the project, and enhance the effectiveness and effectiveness of the project.。