Ch04 efficient securities market

Chap011有效市场假说

11-3

Efficient Market Hypothesis (EMH) 有效市场假说

• New information is unpredictable; if it could be predicted, then the prediction would be part of today’s information. 新的信息是不可预测的,如果是可预测的信息马上就会带 来股价变动从而成为了今天的信息

et = rt - (a + brMt)超额(异常)收益的 估计值是否不为零的检测很重要

INVESTMENTS | BODIE, KANE, MARCUS

11-15

Are Markets Efficient? 市场是有效的吗?

• Magnitude Issue规模问题

– Only managers of large portfolios can earn enough trading profits to make the exploitation of minor mispricing worth the effort.只有大型投资组 合的经理才能从微小的定价错误中获利

INVESTMENTS | BODIE, KANE, MARCUS

11-7

Versions of the EMH 有效市场假说的不同版本

• Weak弱式假说认为市场的股票历史价格、 成交量等市场公开信息已经无用,都已反映 在目前的股票价格里;

• Semi-strong半强式假说任何公司财务信息、 预期、以及一切公开可得的信息都已无用, 反映在当前股票价格里;

– Information-gathering is motivated by desire for higher investment returns.信息收集是由追求更高投 资收益所驱动的

2024年全球金融市场最热门的五种投资工具

03

以太坊

以太坊的起源与发展

以太坊的起源:Vitalik Buterin 于2013年提出以太坊的概念,旨 在为智能合约提供一个安全、可 靠、去中心化的平台。

以太坊的生态建设:以太坊拥有 庞大的开发者和社区支持,不断 推出新的项目和应用,推动了区 块链技术的发展和应用。

添加标题

添加标题

添加标题

添加标题

流动性风险:DeFi协议的流动性可能受到 市场波动的影响 单击此处输入你的正文,请阐述观点

流动性:DeFi协议提供流动性,降低交易 成本

单击此处输入你的正文,请阐述观点

透明度:DeFi协议提供透明度,降低信息 不对称 DeFi的风险 DeFi的风险

监管风险:DeFi协议可能受到监管机构的 限制和打击

单击此处添加副标题

2024年全球金融市场最热

门的五种投资工具

汇报人:

目录

01 02 03 04 05 06

添加目录项标题 比特币 以太坊 Libra

NFT(非同质化代币) DeFi(去中心化金融)

01

添加目录项标题

02

比特币

比特币的起源与发展

比特币的起源:中本聪提出比特币概念,旨在创造一种去中心化的数字货币

比特币的发展历程:从初始阶段到逐渐被认可,再到价格波动和监管政策的变化

比特币的特点:去中心化、匿名性、有限性和全球性

比特币的应用场景:数字支付、跨境支付、数字资产交易等

比特币的未来展望:随着区块链技术的不断发展,比特币有望成为全球金融市场的 重要投资工具之一

区块链技术及其应用

比特币的底层技 术:区块链技术

数字艺术及其应用

NFT的概念与特点 NFT在数字艺术领域的应用 NFT在金融市场的影响与前景 NFT的未来发展趋势与挑战

期货期权及其衍生品配套课件Ch04

Options, Futures, and Other Derivatives 7th International

Options, Futures, and Other Derivatives 7th International

Edition, Copyright © John C. Hull 2019

$100 grows to $100eRT when invested at a continuously compounded rate R for time T $100 received at time T discounts to $100e-RT at time zero when the continuously compounded discount rate is R

Interest Rates

Chapter 4

Options, Futures, and Other Derivatives 7th International Edition,

Copyright © John C. Hull 2019

1Hale Waihona Puke Types of Rates

Treasury rates LIBOR rates Repo rates

5

Zero Rates

A zero rate (or spot rate), for maturity T is the rate of interest earned on an investment that provides a payoff only at time T

fomc货币政策会议声明全文(中英文对照)

fomc货币政策会议声明全文(中英文对照)美联储货币政策会议声明全文(中英文对照)中文版:美联储联邦公开市场委员会于XXX年XX月XX日召开货币政策会议。

会议讨论了当前经济状况和未来货币政策调整的问题。

根据对经济数据的评估和展望,委员会决定采取以下措施:1. 将联邦基金利率目标范围维持在XX%至XX%不变。

这一利率水平有助于支持经济增长和就业市场的稳定。

2. 将继续购买国债和抵押贷款支持证券,以维持适当的货币流动性。

购买规模和节奏将根据市场情况进行调整。

3. 继续监控经济增长、通胀和就业市场的变化,并根据数据来调整货币政策。

委员会将密切关注通胀预期和金融市场的波动。

4. 将通过透明的沟通方式向公众传达货币政策决策的思路和依据。

委员会鼓励公众对货币政策进行积极的参与和理解。

委员会认为,当前美国经济正在逐步复苏,但仍面临不确定性和风险。

委员会将继续采取适当的措施来支持和促进经济增长,同时保持通胀和金融市场稳定。

英文版:The Federal Open Market Committee (FOMC) of the Federal Reserve met on XX Month XX, XXXX to discuss the current economic conditions and future adjustments to monetary policy. Based on the assessment of economic data and outlook, the Committee decided to take the following measures:1. Maintain the target range for the federal funds rate at XX% to XX%. This level of interest rates is expected to support economic growth and stabilize the job market.2. Continue to purchase Treasury securities and mortgage-backed securities to maintain appropriate monetary liquidity. The scale and pace of purchases will be adjusted based on market conditions.3. Monitor changes in economic growth, inflation, and the job market, and adjust monetary policy accordingly. The Committee will closely watch inflation expectations and financial market volatility.4. Communicate the rationale and basis for monetary policy decisions in a transparent manner to the public. The Committee encourages active public participation and understanding of monetary policy.The Committee believes that the current U.S. economy is gradually recovering but still faces uncertainty and risks. The Committee will continue to take appropriate measures to support and promote economic growth while maintaining inflation and financial market stability.。

iiqe paper 3 模拟题

《论文编号:IIQE Paper 3 模拟题》Ⅰ. 绪论IIQE(国际资格考试)是香港证券及期货事务监察委员会设立的考试,旨在评估从业人员在金融领域的专业知识和技能。

本文将就IIQE Paper 3 模拟题展开详细讨论,解答相关问题,为考生提供学习参考。

Ⅱ. 考题分析IIQE Paper 3 模拟题包含了多个部分,涉及不同的金融领域知识,具体考点如下:1. 金融市场2. 证券市场3. 投资组合理论4. 公司理财5. 衍生产品6. 风险管理7. 伦理标准Ⅲ. 解题思路1. 仔细阅读题目,理清考点。

2. 关注题目中的关键词,确定答题思路。

3. 强化对各考点相关知识的学习和理解,做到知识•技能•应用三者结合。

4. 注意审题,在答题过程中要全面回答问题,展示知识面。

Ⅳ. 答题示范1. 关于金融市场题目:金融市场包括哪些主要类型?请简要描述各类型市场的特点。

答:金融市场包括货币市场、资本市场和金融衍生品市场。

货币市场是指短期资金融通的市场,主要特点是流通的货币资金相对较短,市场参与者多为金融机构。

资本市场是指长期资金融通的市场,主要特点是筹资方式多样,市场参与者包括公司、政府和个人投资者。

金融衍生品市场是指各种金融衍生品交易的市场,主要特点是交易对象为金融衍生品合约,具有强大的杠杆效应。

2. 关于证券市场题目:证券市场的基本功能有哪些?请分别阐述。

答:证券市场的基本功能包括融资功能、投资功能和风险管理功能。

融资功能是指证券市场为企业和政府提供融资渠道,帮助其筹集资金。

投资功能是指证券市场为投资者提供投资机会,帮助其获取收益。

风险管理功能是指证券市场通过交易证券等方式进行风险的转移和分散,帮助市场参与者规避风险。

3. 关于投资组合理论题目:什么是有效边界?有效前沿与有效边界有何异同?答:有效边界是指在给定风险水平下,可实现的资产组合收益率的最高线。

有效前沿是指在给定风险水平下,可实现的资产组合中风险最小的线。

美国公司法证券法历年经典论文列表

美国是世界上公司法、证券法研究最为发达的国家之一,在美国法学期刊(Law Review & Journals)上每年发表400多篇以公司法和证券法为主题的论文。

自1994年开始,美国的公司法学者每年会投票从中遴选出10篇左右重要的论文,重印于Corporate Practice Commentator,至2008年,已经评选了15年,计177篇论文入选。

以下是每年入选的论文列表:2008年(以第一作者姓名音序为序):1.Anabtawi, Iman and Lynn Stout. Fiduciary duties for activist shareholders. 60 Stan. L. Rev. 1255-1308 (2008).2.Brummer, Chris. Corporate law preemption in an age of global capital markets. 81 S. Cal. L. Rev. 1067-1114 (2008).3.Choi, Stephen and Marcel Kahan. The market penalty for mutual fund scandals. 87 B.U. L. Rev. 1021-1057 (2007).4.Choi, Stephen J. and Jill E. Fisch. On beyond CalPERS: Survey evidence on the developing role of public pension funds in corporate governance. 61 V and. L. Rev. 315-354 (2008).5.Cox, James D., Randall S. Thoma s and Lynn Bai. There are plaintiffs and…there are plaintiffs: An empirical analysis of securities class action settlements. 61 V and. L. Rev. 355-386 (2008).6.Henderson, M. Todd. Paying CEOs in bankruptcy: Executive compensation when agency costs are low. 101 Nw. U. L. Rev. 1543-1618 (2007).7.Hu, Henry T.C. and Bernard Black. Equity and debt decoupling and empty voting II: Importance and extensions. 156 U. Pa. L. Rev. 625-739 (2008).8.Kahan, Marcel and Edward Rock. The hanging chads of corporate voting. 96 Geo. L.J. 1227-1281 (2008).9.Strine, Leo E., Jr. Toward common sense and common ground? Reflections on the shared interests of managers and labor in a more rational system of corporate governance. 33 J. Corp. L. 1-20 (2007).10.Subramanian, Guhan. Go-shops vs. no-shops in private equity deals: Evidence and implications.63 Bus. Law. 729-760 (2008).2007年:1.Baker, Tom and Sean J. Griffith. The Missing Monitor in Corporate Governance: The Directors’ & Officers’ Liability Insurer. 95 Geo. L.J. 1795-1842 (2007).2.Bebchuk, Lucian A. The Myth of the Shareholder Franchise. 93 V a. L. Rev. 675-732 (2007).3.Choi, Stephen J. and Robert B. Thompson. Securities Litigation and Its Lawyers: Changes During the First Decade After the PSLRA. 106 Colum. L. Rev. 1489-1533 (2006).4.Coffee, John C., Jr. Reforming the Securities Class Action: An Essay on Deterrence and Its Implementation. 106 Colum. L. Rev. 1534-1586 (2006).5.Cox, James D. and Randall S. Thomas. Does the Plaintiff Matter? An Empirical Analysis of Lead Plaintiffs in Securities Class Actions. 106 Colum. L. Rev. 1587-1640 (2006).6.Eisenberg, Theodore and Geoffrey Miller. Ex Ante Choice of Law and Forum: An Empirical Analysis of Corporate Merger Agreements. 59 V and. L. Rev. 1975-2013 (2006).7.Gordon, Jeffrey N. The Rise of Independent Directors in the United States, 1950-2005: Of Shareholder V alue and Stock Market Prices. 59 Stan. L. Rev. 1465-1568 (2007).8.Kahan, Marcel and Edward B. Rock. Hedge Funds in Corporate Governance and Corporate Control. 155 U. Pa. L. Rev. 1021-1093 (2007).ngevoort, Donald C. The Social Construction of Sarbanes-Oxley. 105 Mich. L. Rev. 1817-1855 (2007).10.Roe, Mark J. Legal Origins, Politics, and Modern Stock Markets. 120 Harv. L. Rev. 460-527 (2006).11.Subramanian, Guhan. Post-Siliconix Freeze-outs: Theory and Evidence. 36 J. Legal Stud. 1-26 (2007). (NOTE: This is an earlier working draft. The published article is not freely available, and at SLW we generally respect the intellectual property rights of others.)2006年:1.Bainbridge, Stephen M. Director Primacy and Shareholder Disempowerment. 119 Harv. L. Rev. 1735-1758 (2006).2.Bebchuk, Lucian A. Letting Shareholders Set the Rules. 119 Harv. L. Rev. 1784-1813 (2006).3.Black, Bernard, Brian Cheffins and Michael Klausner. Outside Director Liability. 58 Stan. L. Rev. 1055-1159 (2006).4.Choi, Stephen J., Jill E. Fisch and A.C. Pritchard. Do Institutions Matter? The Impact of the Lead Plaintiff Provision of the Private Securities Litigation Reform Act. 835.Cox, James D. and Randall S. Thomas. Letting Billions Slip Through Y our Fingers: Empirical Evidence and Legal Implications of the Failure of Financial Institutions to Participate in Securities Class Action Settlements. 58 Stan. L. Rev. 411-454 (2005).6.Gilson, Ronald J. Controlling Shareholders and Corporate Governance: Complicating the Comparative Taxonomy. 119 Harv. L. Rev. 1641-1679 (2006).7.Goshen , Zohar and Gideon Parchomovsky. The Essential Role of Securities Regulation. 55 Duke L.J. 711-782 (2006).8.Hansmann, Henry, Reinier Kraakman and Richard Squire. Law and the Rise of the Firm. 119 Harv. L. Rev. 1333-1403 (2006).9.Hu, Henry T. C. and Bernard Black. Empty V oting and Hidden (Morphable) Ownership: Taxonomy, Implications, and Reforms. 61 Bus. Law. 1011-1070 (2006).10.Kahan, Marcel. The Demand for Corporate Law: Statutory Flexibility, Judicial Quality, or Takeover Protection? 22 J. L. Econ. & Org. 340-365 (2006).11.Kahan, Marcel and Edward Rock. Symbiotic Federalism and the Structure of Corporate Law.58 V and. L. Rev. 1573-1622 (2005).12.Smith, D. Gordon. The Exit Structure of V enture Capital. 53 UCLA L. Rev. 315-356 (2005).2005年:1.Bebchuk, Lucian Arye. The case for increasing shareholder power. 118 Harv. L. Rev. 833-914 (2005).2.Bratton, William W. The new dividend puzzle. 93 Geo. L.J. 845-895 (2005).3.Elhauge, Einer. Sacrificing corporate profits in the public interest. 80 N.Y.U. L. Rev. 733-869 (2005).4.Johnson, . Corporate officers and the business judgment rule. 60 Bus. Law. 439-469 (2005).haupt, Curtis J. In the shadow of Delaware? The rise of hostile takeovers in Japan. 105 Colum. L. Rev. 2171-2216 (2005).6.Ribstein, Larry E. Are partners fiduciaries? 2005 U. Ill. L. Rev. 209-251.7.Roe, Mark J. Delaware?s politics. 118 Harv. L. Rev. 2491-2543 (2005).8.Romano, Roberta. The Sarbanes-Oxley Act and the making of quack corporate governance. 114 Y ale L.J. 1521-1611 (2005).9.Subramanian, Guhan. Fixing freezeouts. 115 Y ale L.J. 2-70 (2005).10.Thompson, Robert B. and Randall S. Thomas. The public and private faces of derivative lawsuits. 57 V and. L. Rev. 1747-1793 (2004).11.Weiss, Elliott J. and J. White. File early, then free ride: How Delaware law (mis)shapes shareholder class actions. 57 V and. L. Rev. 1797-1881 (2004).2004年:1Arlen, Jennifer and Eric Talley. Unregulable defenses and the perils of shareholder choice. 152 U. Pa. L. Rev. 577-666 (2003).2.Bainbridge, Stephen M. The business judgment rule as abstention doctrine. 57 V and. L. Rev. 83-130 (2004).3.Bebchuk, Lucian Arye and Alma Cohen. Firms' decisions where to incorporate. 46 J.L. & Econ. 383-425 (2003).4.Blair, Margaret M. Locking in capital: what corporate law achieved for business organizers in the nineteenth century. 51 UCLA L. Rev. 387-455 (2003).5.Gilson, Ronald J. and Jeffrey N. Gordon. Controlling shareholders. 152 U. Pa. L. Rev. 785-843 (2003).6.Roe, Mark J. Delaware 's competition. 117 Harv. L. Rev. 588-646 (2003).7.Sale, Hillary A. Delaware 's good faith. 89 Cornell L. Rev. 456-495 (2004).8.Stout, Lynn A. The mechanisms of market inefficiency: an introduction to the new finance. 28 J. Corp. L. 635-669 (2003).9.Subramanian, Guhan. Bargaining in the shadow of takeover defenses. 113 Y ale L.J. 621-686 (2003).10.Subramanian, Guhan. The disappearing Delaware effect. 20 J.L. Econ. & Org. 32-59 (2004)11.Thompson, Robert B. and Randall S. Thomas. The new look of shareholder litigation: acquisition-oriented class actions. 57 V and. L. Rev. 133-209 (2004).2003年:1.A yres, Ian and Stephen Choi. Internalizing outsider trading. 101 Mich. L. Rev. 313-408 (2002).2.Bainbridge, Stephen M. Director primacy: The means and ends of corporate governance. 97 Nw. U. L. Rev. 547-606 (2003).3.Bebchuk, Lucian, Alma Cohen and Allen Ferrell. Does the evidence favor state competition in corporate law? 90 Cal. L. Rev. 1775-1821 (2002).4.Bebchuk, Lucian Arye, John C. Coates IV and Guhan Subramanian. The Powerful Antitakeover Force of Staggered Boards: Further findings and a reply to symposium participants. 55 Stan. L. Rev. 885-917 (2002).5.Choi, Stephen J. and Jill E. Fisch. How to fix Wall Street: A voucher financing proposal for securities intermediaries. 113 Y ale L.J. 269-346 (2003).6.Daines, Robert. The incorporation choices of IPO firms. 77 N.Y.U. L. Rev.1559-1611 (2002).7.Gilson, Ronald J. and David M. Schizer. Understanding venture capital structure: A taxexplanation for convertible preferred stock. 116 Harv. L. Rev. 874-916 (2003).8.Kahan, Marcel and Ehud Kamar. The myth of state competition in corporate law. 55 Stan. L. Rev. 679-749 (2002).ngevoort, Donald C. Taming the animal spirits of the stock markets: A behavioral approach to securities regulation. 97 Nw. U. L. Rev. 135-188 (2002).10.Pritchard, A.C. Justice Lewis F. Powell, Jr., and the counterrevolution in the federal securities laws. 52 Duke L.J. 841-949 (2003).11.Thompson, Robert B. and Hillary A. Sale. Securities fraud as corporate governance: Reflections upon federalism. 56 V and. L. Rev. 859-910 (2003).2002年:1.Allen, William T., Jack B. Jacobs and Leo E. Strine, Jr. Function over Form: A Reassessment of Standards of Review in Delaware Corporation Law. 26 Del. J. Corp. L. 859-895 (2001) and 56 Bus. Law. 1287 (2001).2.A yres, Ian and Joe Bankman. Substitutes for Insider Trading. 54 Stan. L. Rev. 235-254 (2001).3.Bebchuk, Lucian Arye, Jesse M. Fried and David I. Walker. Managerial Power and Rent Extraction in the Design of Executive Compensation. 69 U. Chi. L. Rev. 751-846 (2002).4.Bebchuk, Lucian Arye, John C. Coates IV and Guhan Subramanian. The Powerful Antitakeover Force of Staggered Boards: Theory, Evidence, and Policy. 54 Stan. L. Rev. 887-951 (2002).5.Black, Bernard and Reinier Kraakman. Delaware’s Takeover Law: The Uncertain Search for Hidden V alue. 96 Nw. U. L. Rev. 521-566 (2002).6.Bratton, William M. Enron and the Dark Side of Shareholder V alue. 76 Tul. L. Rev. 1275-1361 (2002).7.Coates, John C. IV. Explaining V ariation in Takeover Defenses: Blame the Lawyers. 89 Cal. L. Rev. 1301-1421 (2001).8.Kahan, Marcel and Edward B. Rock. How I Learned to Stop Worrying and Love the Pill: Adaptive Responses to Takeover Law. 69 U. Chi. L. Rev. 871-915 (2002).9.Kahan, Marcel. Rethinking Corporate Bonds: The Trade-off Between Individual and Collective Rights. 77 N.Y.U. L. Rev. 1040-1089 (2002).10.Roe, Mark J. Corporate Law’s Limits. 31 J. Legal Stud. 233-271 (2002).11.Thompson, Robert B. and D. Gordon Smith. Toward a New Theory of the Shareholder Role: "Sacred Space" in Corporate Takeovers. 80 Tex. L. Rev. 261-326 (2001).2001年:1.Black, Bernard S. The legal and institutional preconditions for strong securities markets. 48 UCLA L. Rev. 781-855 (2001).2.Coates, John C. IV. Takeover defenses in the shadow of the pill: a critique of the scientific evidence. 79 Tex. L. Rev. 271-382 (2000).3.Coates, John C. IV and Guhan Subramanian. A buy-side model of M&A lockups: theory and evidence. 53 Stan. L. Rev. 307-396 (2000).4.Coffee, John C., Jr. The rise of dispersed ownership: the roles of law and the state in the separation of ownership and control. 111 Y ale L.J. 1-82 (2001).5.Choi, Stephen J. The unfounded fear of Regulation S: empirical evidence on offshore securities offerings. 50 Duke L.J. 663-751 (2000).6.Daines, Robert and Michael Klausner. Do IPO charters maximize firm value? Antitakeover protection in IPOs. 17 J.L. Econ. & Org. 83-120 (2001).7.Hansmann, Henry and Reinier Kraakman. The essential role of organizational law. 110 Y ale L.J. 387-440 (2000).ngevoort, Donald C. The human nature of corporate boards: law, norms, and the unintended consequences of independence and accountability. 89 Geo. L.J. 797-832 (2001).9.Mahoney, Paul G. The political economy of the Securities Act of 1933. 30 J. Legal Stud. 1-31 (2001).10.Roe, Mark J. Political preconditions to separating ownership from corporate control. 53 Stan. L. Rev. 539-606 (2000).11.Romano, Roberta. Less is more: making institutional investor activism a valuable mechanism of corporate governance. 18 Y ale J. on Reg. 174-251 (2001).2000年:1.Bratton, William W. and Joseph A. McCahery. Comparative Corporate Governance and the Theory of the Firm: The Case Against Global Cross Reference. 38 Colum. J. Transnat’l L. 213-297 (1999).2.Coates, John C. IV. Empirical Evidence on Structural Takeover Defenses: Where Do We Stand?54 U. Miami L. Rev. 783-797 (2000).3.Coffee, John C., Jr. Privatization and Corporate Governance: The Lessons from Securities Market Failure. 25 J. Corp. L. 1-39 (1999).4.Fisch, Jill E. The Peculiar Role of the Delaware Courts in the Competition for Corporate Charters. 68 U. Cin. L. Rev. 1061-1100 (2000).5.Fox, Merritt B. Retained Mandatory Securities Disclosure: Why Issuer Choice Is Not Investor Empowerment. 85 V a. L. Rev. 1335-1419 (1999).6.Fried, Jesse M. Insider Signaling and Insider Trading with Repurchase Tender Offers. 67 U. Chi. L. Rev. 421-477 (2000).7.Gulati, G. Mitu, William A. Klein and Eric M. Zolt. Connected Contracts. 47 UCLA L. Rev. 887-948 (2000).8.Hu, Henry T.C. Faith and Magic: Investor Beliefs and Government Neutrality. 78 Tex. L. Rev. 777-884 (2000).9.Moll, Douglas K. Shareholder Oppression in Close Corporations: The Unanswered Question of Perspective. 53 V and. L. Rev. 749-827 (2000).10.Schizer, David M. Executives and Hedging: The Fragile Legal Foundation of Incentive Compatibility. 100 Colum. L. Rev. 440-504 (2000).11.Smith, Thomas A. The Efficient Norm for Corporate Law: A Neotraditional Interpretation of Fiduciary Duty. 98 Mich. L. Rev. 214-268 (1999).12.Thomas, Randall S. and Kenneth J. Martin. The Determinants of Shareholder V oting on Stock Option Plans. 35 Wake Forest L. Rev. 31-81 (2000).13.Thompson, Robert B. Preemption and Federalism in Corporate Governance: Protecting Shareholder Rights to V ote, Sell, and Sue. 62 Law & Contemp. Probs. 215-242 (1999).1999年(以第一作者姓名音序为序):1.Bankman, Joseph and Ronald J. Gilson. Why Start-ups? 51 Stan. L. Rev. 289-308 (1999).2.Bhagat, Sanjai and Bernard Black. The Uncertain Relationship Between Board Composition and Firm Performance. 54 Bus. Law. 921-963 (1999).3.Blair, Margaret M. and Lynn A. Stout. A Team Production Theory of Corporate Law. 85 V a. L. Rev. 247-328 (1999).4.Coates, John C., IV. “Fair V alue” As an A voidable Rule of Corporate Law: Minority Discounts in Conflict Transactions. 147 U. Pa. L. Rev. 1251-1359 (1999).5.Coffee, John C., Jr. The Future as History: The Prospects for Global Convergence in Corporate Governance and Its Implications. 93 Nw. U. L. Rev. 641-707 (1999).6.Eisenberg, Melvin A. Corporate Law and Social Norms. 99 Colum. L. Rev. 1253-1292 (1999).7.Hamermesh, Lawrence A. Corporate Democracy and Stockholder-Adopted By-laws: Taking Back the Street? 73 Tul. L. Rev. 409-495 (1998).8.Krawiec, Kimberly D. Derivatives, Corporate Hedging, and Shareholder Wealth: Modigliani-Miller Forty Y ears Later. 1998 U. Ill. L. Rev. 1039-1104.ngevoort, Donald C. Rereading Cady, Roberts: The Ideology and Practice of Insider Trading Regulation. 99 Colum. L. Rev. 1319-1343 (1999).ngevoort, Donald C. Half-Truths: Protecting Mistaken Inferences By Investors and Others.52 Stan. L. Rev. 87-125 (1999).11.Talley, Eric. Turning Servile Opportunities to Gold: A Strategic Analysis of the Corporate Opportunities Doctrine. 108 Y ale L.J. 277-375 (1998).12.Williams, Cynthia A. The Securities and Exchange Commission and Corporate Social Transparency. 112 Harv. L. Rev. 1197-1311 (1999).1998年:1.Carney, William J., The Production of Corporate Law, 71 S. Cal. L. Rev. 715-780 (1998).2.Choi, Stephen, Market Lessons for Gatekeepers, 92 Nw. U. L. Rev. 916-966 (1998).3.Coffee, John C., Jr., Brave New World?: The Impact(s) of the Internet on Modern Securities Regulation. 52 Bus. Law. 1195-1233 (1997).ngevoort, Donald C., Organized Illusions: A Behavioral Theory of Why Corporations Mislead Stock Market Investors (and Cause Other Social Harms). 146 U. Pa. L. Rev. 101-172 (1997).ngevoort, Donald C., The Epistemology of Corporate-Securities Lawyering: Beliefs, Biases and Organizational Behavior. 63 Brook. L. Rev. 629-676 (1997).6.Mann, Ronald J. The Role of Secured Credit in Small-Business Lending. 86 Geo. L.J. 1-44 (1997).haupt, Curtis J., Property Rights in Firms. 84 V a. L. Rev. 1145-1194 (1998).8.Rock, Edward B., Saints and Sinners: How Does Delaware Corporate Law Work? 44 UCLA L. Rev. 1009-1107 (1997).9.Romano, Roberta, Empowering Investors: A Market Approach to Securities Regulation. 107 Y ale L.J. 2359-2430 (1998).10.Schwab, Stewart J. and Randall S. Thomas, Realigning Corporate Governance: Shareholder Activism by Labor Unions. 96 Mich. L. Rev. 1018-1094 (1998).11.Skeel, David A., Jr., An Evolutionary Theory of Corporate Law and Corporate Bankruptcy. 51 V and. L. Rev. 1325-1398 (1998).12.Thomas, Randall S. and Martin, Kenneth J., Should Labor Be Allowed to Make Shareholder Proposals? 73 Wash. L. Rev. 41-80 (1998).1997年:1.Alexander, Janet Cooper, Rethinking Damages in Securities Class Actions, 48 Stan. L. Rev. 1487-1537 (1996).2.Arlen, Jennifer and Kraakman, Reinier, Controlling Corporate Misconduct: An Analysis of Corporate Liability Regimes, 72 N.Y.U. L. Rev. 687-779 (1997).3.Brudney, Victor, Contract and Fiduciary Duty in Corporate Law, 38 B.C. L. Rev. 595-665 (1997).4.Carney, William J., The Political Economy of Competition for Corporate Charters, 26 J. Legal Stud. 303-329 (1997).5.Choi, Stephen J., Company Registration: Toward a Status-Based Antifraud Regime, 64 U. Chi. L. Rev. 567-651 (1997).6.Fox, Merritt B., Securities Disclosure in a Globalizing Market: Who Should Regulate Whom. 95 Mich. L. Rev. 2498-2632 (1997).7.Kahan, Marcel and Klausner, Michael, Lockups and the Market for Corporate Control, 48 Stan. L. Rev. 1539-1571 (1996).8.Mahoney, Paul G., The Exchange as Regulator, 83 V a. L. Rev. 1453-1500 (1997).haupt, Curtis J., The Market for Innovation in the United States and Japan: V enture Capital and the Comparative Corporate Governance Debate, 91 Nw. U.L. Rev. 865-898 (1997).10.Skeel, David A., Jr., The Unanimity Norm in Delaware Corporate Law, 83 V a. L. Rev. 127-175 (1997).1996年:1.Black, Bernard and Reinier Kraakman A Self-Enforcing Model of Corporate Law, 109 Harv. L. Rev. 1911 (1996)2.Gilson, Ronald J. Corporate Governance and Economic Efficiency: When Do Institutions Matter?, 74 Wash. U. L.Q. 327 (1996)3. Hu, Henry T.C. Hedging Expectations: "Derivative Reality" and the Law and Finance of the Corporate Objective, 21 J. Corp. L. 3 (1995)4.Kahan, Marcel & Michael Klausner Path Dependence in Corporate Contracting: Increasing Returns, Herd Behavior and Cognitive Biases, 74 Wash. U. L.Q. 347 (1996)5.Kitch, Edmund W. The Theory and Practice of Securities Disclosure, 61 Brooklyn L. Rev. 763 (1995)ngevoort, Donald C. Selling Hope, Selling Risk: Some Lessons for Law From Behavioral Economics About Stockbrokers and Sophisticated Customers, 84 Cal. L. Rev. 627 (1996)7.Lin, Laura The Effectiveness of Outside Directors as a Corporate Governance Mechanism: Theories and Evidence, 90 Nw. U.L. Rev. 898 (1996)lstein, Ira M. The Professional Board, 50 Bus. Law 1427 (1995)9.Thompson, Robert B. Exit, Liquidity, and Majority Rule: Appraisal's Role in Corporate Law, 84 Geo. L.J. 1 (1995)10.Triantis, George G. and Daniels, Ronald J. The Role of Debt in Interactive Corporate Governance. 83 Cal. L. Rev. 1073 (1995)1995年:公司法:1.Arlen, Jennifer and Deborah M. Weiss A Political Theory of Corporate Taxation,. 105 Y ale L.J. 325-391 (1995).2.Elson, Charles M. The Duty of Care, Compensation, and Stock Ownership, 63 U. Cin. L. Rev. 649 (1995).3.Hu, Henry T.C. Heeding Expectations: "Derivative Reality" and the Law and Finance of the Corporate Objective, 73 Tex. L. Rev. 985-1040 (1995).4.Kahan, Marcel The Qualified Case Against Mandatory Terms in Bonds, 89 Nw. U.L. Rev. 565-622 (1995).5.Klausner, Michael Corporations, Corporate Law, and Networks of Contracts, 81 V a. L. Rev. 757-852 (1995).6.Mitchell, Lawrence E. Cooperation and Constraint in the Modern Corporation: An Inquiry Into the Causes of Corporate Immorality, 73 Tex. L. Rev. 477-537 (1995).7.Siegel, Mary Back to the Future: Appraisal Rights in the Twenty-First Century, 32 Harv. J. on Legis. 79-143 (1995).证券法:1.Grundfest, Joseph A. Why Disimply? 108 Harv. L. Rev. 727-747 (1995).2.Lev, Baruch and Meiring de V illiers Stock Price Crashes and 10b-5 Damages: A Legal Economic, and Policy Analysis, 47 Stan. L. Rev. 7-37 (1994).3.Mahoney, Paul G. Mandatory Disclosure as a Solution to Agency Problems, 62 U. Chi. L. Rev. 1047-1112 (1995).4.Seligman, Joel The Merits Do Matter, 108 Harv. L. Rev. 438 (1994).5.Seligman, Joel The Obsolescence of Wall Street: A Contextual Approach to the Evolving Structure of Federal Securities Regulation, 93 Mich. L. Rev. 649-702 (1995).6.Stout, Lynn A. Are Stock Markets Costly Casinos? Disagreement, Mark Failure, and Securities Regulation, 81 V a. L. Rev. 611 (1995).7.Weiss, Elliott J. and John S. Beckerman Let the Money Do the Monitoring: How Institutional Investors Can Reduce Agency Costs in Securities Class Actions, 104 Y ale L.J. 2053-2127 (1995).1994年:公司法:1.Fraidin, Stephen and Hanson, Jon D. Toward Unlocking Lockups, 103 Y ale L.J. 1739-1834 (1994)2.Gordon, Jeffrey N. Institutions as Relational Investors: A New Look at Cumulative V oting, 94 Colum. L. Rev. 124-192 (1994)3.Karpoff, Jonathan M., and Lott, John R., Jr. The Reputational Penalty Firms Bear From Committing Criminal Fraud, 36 J.L. & Econ. 757-802 (1993)4.Kraakman, Reiner, Park, Hyun, and Shavell, Steven When Are Shareholder Suits in Shareholder Interests?, 82 Geo. L.J. 1733-1775 (1994)5.Mitchell, Lawrence E. Fairness and Trust in Corporate Law, 43 Duke L.J. 425- 491 (1993)6.Oesterle, Dale A. and Palmiter, Alan R. Judicial Schizophrenia in Shareholder V oting Cases, 79 Iowa L. Rev. 485-583 (1994)7. Pound, John The Rise of the Political Model of Corporate Governance and Corporate Control, 68 N.Y.U. L. Rev. 1003-1071 (1993)8.Skeel, David A., Jr. Rethinking the Line Between Corporate Law and Corporate Bankruptcy, 72 Tex. L. Rev. 471-557 (1994)9.Thompson, Robert B. Unpacking Limited Liability: Direct and V icarious Liability of Corporate Participants for Torts of the Enterprise, 47 V and. L. Rev. 1-41 (1994)证券法:1.Alexander, Janet Cooper The V alue of Bad News in Securities Class Actions, 41 UCLA L.Rev. 1421-1469 (1994)2.Bainbridge, Stephen M. Insider Trading Under the Restatement of the Law Governing Lawyers, 19 J. Corp. L. 1-40 (1993)3.Black, Bernard S. and Coffee, John C. Jr. Hail Britannia?: Institutional Investor Behavior Under Limited Regulation, 92 Mich. L. Rev. 1997-2087 (1994)4.Booth, Richard A. The Efficient Market, portfolio Theory, and the Downward Sloping Demand Hypothesis, 68 N.Y.U. L. Rev. 1187-1212 (1993)5.Coffee, John C., Jr. The SEC and the Institutional Investor: A Half-Time Report, 15 Cardozo L. Rev 837-907 (1994)6.Fox, Merritt B. Insider Trading Deterrence V ersus Managerial Incentives: A Unified Theory of Section 16(b), 92 Mich. L. Rev. 2088-2203 (1994)7.Grundfest, Joseph A. Disimplying Private Rights of Action Under the Federal Securities Laws: The Commission's Authority, 107 Harv. L. Rev. 961-1024 (1994)8.Macey, Jonathan R. Administrative Agency Obsolescence and Interest Group Formation: A Case Study of the SEC at Sixty, 15 Cardozo L. Rev. 909-949 (1994)9.Rock, Edward B. Controlling the Dark Side of Relational Investing, 15 Cardozo L. Rev. 987-1031 (1994)。

第九章 有效市场假说

半强式有效市场 (Semistrong-form)

• The “Semistrong” form asserts that目前价格中包 含所有的公共信息(all publicly available information is fully reflected in securities prices). In other words, fundamental analysis is of no use. • Examples of publicly available information are: annual reports of companies, investment advisory data such as "Heard on the Street" in the Wall Street Journal, or ticker tape information. All of this information is relatively inexpensive to collect.

Financial Economics_WCY 10

强式有效市场(Strong-form)Байду номын сангаас

• Strong-form: 所有的信息(历史交易信息 ,公开信息以及公司内部非公开信息) 都 反映在现时证券价格中(all information, both publicly and privately available (almost everyone rejects due to the investment performance of insiders)

Financial Economics_WCY

28_Chap011 The Efficient Market Hypothesis 博迪投资学课

11-14

Semistrong Tests: Anomalies

• P/E Effect • Small Firm Effect (January Effect) • Neglected Firm Effect and Liquidity Effects • Book-to-Market Ratios • Post-Earnings Announcement Price Drift

11-20

Figure 11.6 Returns to Style Portfolio as a Predictor of GDP Growth

11-21

Interpreting the Evidence Continued

• Anomalies or Data Mining • The noisy market hypothesis • Fundamental indexing

11-22

Stock Market Analysts

• Do Analysts Add Value – Mixed evidence – Ambiguity in results

11-23

Mutual Fund Performance

• Some evidence of persistent positive and negative performance

Efficient Market Hypothesis (EMH)

• Do security prices reflect information ? • Why look at market efficiency?

ch04 理解利率 双语分析

payment loan might require you to pay $126

every year for 25 years.

Slide 4–16

• 3. A coupon bond 息票债券 pays the owner of the bond a fixed interest payment (coupon payment) every year until the maturity date, when a specified final amount (face value or par value 面值) is repaid.息票债券持有人在到 期前定期(每年、半年或每季)要得到定额的利 息支付,到期则要收回票面金额和到期当年的利 息支付。 • The coupon payment is so named because the bondholder used to obtain payment by clipping a coupon off the bond and sending it to the bond issuer, who then sent the payment to the holder. Nowadays, it is no longer necessary to send in coupons to receive these payments.

Slide 4–19

• These four types of instruments require payments at different times: Simple loans and discount bonds make payment only at their maturity dates, whereas fixed-payment loans and coupon bonds have payments periodically until maturity. • How would you decide which of these instruments provides you with more income? • To solve this problem, we use the concept of present value, explained earlier, to provide us with a procedure for measuring interest rates on these different types of instruments.

有效市场假说英文名词解释

有效市场假说英文名词解释The Efficient Market Hypothesis (EMH) is a theory that suggests that financial markets are efficient and that asset prices already reflect all available information. This means that it is impossible to consistently achieve higher than average returns in the market, as all relevant information is already factored into stock prices. The EMH is based on the idea that in an efficient market, competition among investors will cause existing information to be reflected in stock prices quickly and accurately.EMH is commonly categorized into three forms: weak form, semi-strong form, and strong form. The weak form EMH suggests that all past trading information is already reflected in stock prices, meaning that technical analysis cannot be used to consistently outperform the market. The semi-strong form EMH goes further to suggest that all publicly available information is already reflected in stock prices, making fundamental analysis ineffective. The strong form EMH asserts that all information, both public and private, is already reflected in stock prices, makinginsider trading and other forms of informational advantage impossible.The implications of the EMH are significant for investors, as it suggests that it is extremely difficult to consistently beat the market. This has led to the rise of index funds and passive investing, as many investors believe that it is more rational to simply track the market rather than trying to beat it.有效市场假说(EMH)是一种理论,认为金融市场是高效的,资产价格已经反映了所有可获得的信息。

有效资本市场假说EfficientMarketHypothesisEMH课件

相关历史数据不能用于预测未来价格。

半强式有效市场

基于公共信息无法获得超额收益,但内幕消息可获得超额收益。

强式有效市场

内幕消息和公共信息都无法获得超额收益。

市场有效性的特征与假设

特征

• 信息的迅速反应 • 价格的准确反映 • 无法获得超额收益

假设

• 投资者理性 • 无摩擦交易 • 信息公开

有效资本市场假说 EfficientMarketHypothesis EMHppt课件

有效资本市场假说(EMH)是一个关键的投资理论,它认为市场是高效的, 价格反映了所有可获得的信息。

定义与概念

有效资本市场假说定义市场高效,反应快,价格准确。这一理论认为无法预 测市场的短期价格变动。

市场有效性类型

信息的对称与非对称

对称信息指共享的信息,非对称信息指一方拥有其他方不知道的信息,可能导致市场失真或利益不平衡。

信息的影响

1 缺乏对称信息

投资者无法全面了解市场

2 非对称信息

拥有内幕消息的投资者可

3 市场反应速度与信息

含量关系

情况,交易可能受到限制。

能获得不公平的交易优势。

较新的信息通常会更快地

影响市场价格。

其他因素影响市场有效性

费解信源理论

投资者被情感和非理性决策影 响。

投资者行为

投资者倾向于跟随市场趋势而 非理性决策。

救市

政府干预可能影响市场的有效 性。

其他影响市场有效性因素的关系

场外交易

场外交易可能导致信息不对称, 影响市场的有效性。

股权结构

做市商

股权结构可能影响市场的有效性。

做市商在提供流动性和降低交易 成本方面发挥重要作用。

(完整word版)金融术语中英文对照(word文档良心出品)

Back-door listing 借壳上市Back-end load 撤离费;后收费用Back office 后勤办公室Back to back FX agreement 背靠背外汇协议Balance of payments 国际收支平衡;收支结余Balance of trade 贸易平衡Balance sheet 资产负债表Balance sheet date 年结日Balloon maturity 到期大额偿还Balloon payment 期末大额偿还Bank, Banker, Banking 银行;银行家;银行业国际结算银行Bank forInternational Settlements(BIS)Bankruptcy 破产Base day 基准日Base rate 基准利率Basel Capital Accord 巴塞尔资本协议Basis Point (BP) 基点;点子一个基点等如一个百分点(%)的百分之一。

举例:25个基点=0.25%Basis swap 基准掉期Basket of currencies 一揽子货币Basket warrant 一揽子备兑证Bear market 熊市;股市行情看淡Bear position 空仓;空头Bear raid 疯狂抛售Bearer 持票人Bearer stock 不记名股票Behind-the-scene 未开拓市场Below par 低于平值Benchmark 比较基准Benchmark mortgage pool 按揭贷款基准组合Beneficiary 受益人Bermudan option 百慕大期权百慕大期权介乎美式与欧式之间,持有人有权在到期日前的一个或多个日期执行期权。

Best practice 最佳做法;典范做法Beta (Market beta) 贝他(系数);市场风险指数Bid 出价;投标价;买盘指由买方报出表示愿意按此水平买入的一个价格。

全球新能源汽车贸易网络结构特征及其竞争关系研究

全球新能源汽车贸易网络结构特征及其竞争关系研究目录一、内容综述 (2)1.1 研究背景与意义 (2)1.2 国内外研究现状综述 (4)1.3 研究内容与方法 (5)1.4 论文结构安排 (6)二、全球新能源汽车市场概述 (7)2.1 新能源汽车定义及类型 (8)2.2 全球新能源汽车市场分布 (9)2.3 新能源汽车市场规模与增长趋势 (11)三、全球新能源汽车贸易网络结构特征 (12)3.1 贸易网络节点分析 (13)3.2 贸易网络边权分析 (14)3.3 贸易网络密度与中心性分析 (16)3.4 贸易网络稳定性分析 (17)四、全球新能源汽车贸易竞争关系研究 (18)4.1 竞争对手识别与分类 (19)4.2 竞争力评价指标体系构建 (20)4.3 竞争关系测度方法与应用 (22)4.4 竞争优势与劣势分析 (23)五、全球新能源汽车贸易网络竞争策略研究 (25)5.1 市场定位与战略选择 (26)5.2 合作与竞争平衡策略 (28)5.3 技术创新与知识产权保护策略 (29)5.4 品牌建设与国际市场拓展策略 (31)六、结论与展望 (32)6.1 研究结论总结 (34)6.2 政策建议与实践意义 (35)6.3 研究不足与未来展望 (36)一、内容综述随着全球气候变化和环境问题日益严重,新能源汽车作为绿色出行工具受到了各国政府和企业的高度关注。

在此背景下,新能源汽车贸易网络结构特征及其竞争关系成为了学术界研究的热点问题。

本文旨在对全球新能源汽车贸易网络的结构特征进行深入探讨,并分析不同国家和地区之间的竞争关系。

在竞争关系方面,学者们主要关注以下几个方面。

通过对这些问题的研究,我们可以得出以下在全球新能源汽车贸易网络中,竞争日益激烈,各国都在努力提升自身在产业链中的地位和竞争力;同时,贸易政策和技术创新也成为影响竞争关系的重要因素。

现有研究已经取得了丰富的成果,为深入理解全球新能源汽车贸易网络结构特征及其竞争关系提供了重要支撑。

银行管理(第六版)课件 Ch04

4-8

Loan Accounts

Gross Loans – Sum of All Loans Allowance for Possible Loan Losses

Contra Asset Account For Potential Future Loan Losses

Net Loans Nonperforming Loans

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

4-6

Cash Assets

Account is Called Cash and Deposits Due from Bank Includes:

Vault Cash Deposits with Other Banks Cash Items in Process of Collection Reserve Account with the Federal Reserve

4-3

Bank Financial Statements

Report of Condition – Balance Sheet Report of Income – Income Statement Sources and Uses of Funds Statement Statement of Stockholders’ Equity

Cash and Deposits Due from Banks Investment Securities Fed Funds Sold and Repos. Total Loans and Leases (Net)

Commercial and Industrial Consumer Real Estate To Depository Institutions To Foreign Governments Agriculture Other Loans Leases Assets Held in Trading Accounts Bank Premises and FA (Net) Other Assets

HullOFOD8eSolutionsCh04

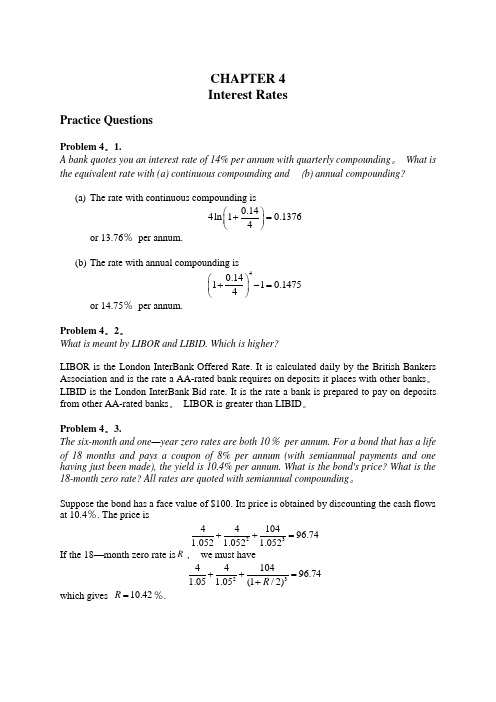

CHAPTER 4Interest RatesPractice QuestionsProblem 4。

1.A bank quotes you an interest rate of 14% per annum with quarterly compounding 。

What is the equivalent rate with (a) continuous compounding and (b) annual compounding?(a) The rate with continuous compounding is 0144ln 1013764.⎛⎫+=. ⎪⎝⎭or 13.76% per annum.(b) The rate with annual compounding is 401411014754.⎛⎫+-=. ⎪⎝⎭ or 14.75% per annum.Problem 4。

2。

What is meant by LIBOR and LIBID. Which is higher?LIBOR is the London InterBank Offered Rate. It is calculated daily by the British Bankers Association and is the rate a AA-rated bank requires on deposits it places with other banks 。

LIBID is the London InterBank Bid rate. It is the rate a bank is prepared to pay on deposits from other AA-rated banks 。

LIBOR is greater than LIBID 。

Problem 4。

3.The six-month and one —year zero rates are both 10% per annum. For a bond that has a life of 18 months and pays a coupon of 8% per annum (with semiannual payments and one having just been made), the yield is 10.4% per annum. What is the bond's price? What is the 18-month zero rate? All rates are quoted with semiannual compounding 。

胡志明市证券交易所的规章制度

胡志明市证券交易所的规章制度胡志明市证券交易所(Ho Chi Minh City Securities Trading Center,简称HOSE)是越南最大的股票交易所之一,它依法负责越南证券市场的管理和监管。

为了保护投资者权益、维护市场秩序,HOSE制定了一系列的规章制度,从而规范了证券交易及市场运行。

1. 证券上市规定HOSE根据越南证券法规定,制定了一套严格的证券上市规定。

该规定规定了公司上市的条件和程序,包括申请提交、审核流程、信息披露要求等。

公司必须满足一系列的财务、治理和运营要求,同时还需要通过HOSE的审核才能上市交易。

2. 交易制度HOSE的交易制度是其规章制度的核心部分,主要包括交易时间安排、交易品种和交易方式。

证券交易时间按照越南政府的规定进行安排,通常为上午9:00至11:30和下午13:00至15:00。

HOSE提供的交易品种包括股票、债券、衍生品等。

交易方式主要有现金交易和融资交易。

HOSE还规定了交易的熔断机制和停牌制度,以维护市场的稳定运行。

3. 信息披露要求为了保护投资者的权益,HOSE对上市公司的信息披露提出了严格的要求。

上市公司必须及时、准确地披露相关信息,包括财务报告、重大事项公告、股东变动等。

信息披露要求包括定期报告和临时报告,公司必须遵守制定的时间表和披露要求。

4. 监管措施HOSE作为越南证券市场的管理机构,有权对市场进行监管并采取相应的监管措施。

HOSE可以对违规行为进行处罚,包括警告、罚款、暂停交易等。

同时,HOSE还制定了规范行为准则,要求市场参与者遵守道德规范和行为规则,保持市场的健康和透明。

5. 投资者保护为了保护投资者的权益,HOSE实施了一系列措施。

例如,HOSE要求上市公司对投资者进行充分的信息披露,保证投资者能够及时了解公司的经营状况和风险情况。

除此之外,HOSE还规定了投资者教育计划,提供培训和教育资源,帮助投资者提高投资知识和风险意识。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

expected security return = riskless return + beta * (expected market risk premium)

6

The Capital Asset Pricing Model

ASSUMPTIONS

• • • • • • • •

• • •

•

All assets in the world are traded All assets are infinitely divisible All investors in the world collectively hold all assets For every borrower, there is a lender There is a riskless security in the world All investors borrow and lend at the riskless rate Everyone agrees on the inputs to the Mean-STD picture Preferences are well-described by simple utility functions Security distributions are normal, or at least well described by two parameters All investors have identical investment horizons (two time periods) All investors have identical opinions about expected returns, volatilities and correlations of available investments The are no transaction costs and no taxes

• Expected value of noise = 0 • Market efficient in expected value sense • Role for accounting information

18

Market Response to Earnings

Ballard Power Systems Inc.

Efficient Securities Markets

Scott Chapter 4

EMH & CAPM - Theories developed in the 1960s

1

Efficient Market Hypothesis

Assumptions

• Active market with large numbers of rational, profit-maximizing investors • All market participants have same information • Prices respond only to available information • Therefore, equilibrium prices reflect all available information

Unusual and non-recurring items Operating income: Income from continuing operations Discontinued operations

Extraordinary items

Cumulative effect of accounting change Net income

15

CAPM return

CAPM

E(Rjt) = Rf(1 - βj) + βjE(RMt)

4.2

Only firm-specific component is ß j

• How does accounting information affect share price?

E(Rjt) =

E(Pjt + Djt)

Two sources of cash flows:

• Dividends • Sale of investment

Distribution of Earnings

12

Equation 4.1, p. 103

Actual return (ex post concept)

Rjt =

Pjt + Djt Pj,t-1

10

Role of Accounting Information

For investors:

• Usefulness = information helpful in predicting the future cash flows that accrue to the investor as a result of holding the investment

• Fundamental analysis useless

The "Strong" form

• Inside information useless

3

Securities Market Efficiency

IMPLICATIONS:

• Random walk Prices cannot be predicted No investment pattern can be discerned Best estimate of future price is current price • Given transaction costs, EMH predicts index fund would be more profitable than a managed portfolio • Role of accounting information???

19

Information Asymmetry

The Adverse Selection Problem

• Inside information

Insiderral Hazard Problem

• Manager shirking

20

Social Implications of Adverse Selection

4

Accounting Implications of EMH

Accounting policies selected by firms don’t matter when

• There is full disclosure • No cash flow effects

More information is better for markets

If investors believe EMH …

17

A Logical Inconsistency (2)

Partly Informative Share Prices

• Two types of investors

Rational speculators or arbitrageurs Noise traders who trade on the basis of imperfect information

• 4th Quarter loss doubles compared with same quarter of previous year • R & D spending up • revenue doubles

Is rise in share price to $189 “efficient?”

Expected Future Dividends

Future Stock Price

Permanent vs. Transitory Earnings

14

Hierarchy of Income Numbers

Core earnings: net income before unusual and non-recurring items

• Cost/benefit considerations?

“Naïve” investors price-protected Many sources of information

• Accountants in competition with other providers

5

CAPM

E(Rjt) = Rf(1 - βj) + βjE(RMt)

9

Limitation of Portfolio Theory

Diversification can eliminate nonsystematic risk Risk associated with economy-wide events remain

• Changes in interest rates • Inflation • Recession

8

Interview with Bill Sharpe

Did the CAPM evolve? Of course. … But the fundamental idea remains that there's no reason to expect reward just for bearing risk. Otherwise, you'd make a lot of money in Las Vegas. If there's reward for risk, it's got to be special. There's got to be some economics behind it or else the world is a very crazy place. I don't think differently about those basic ideas at all.